ADIAL PHARMACEUTICALS, INC. - Annual Report: 2021 (Form 10-K)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2021

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File Number: 001-38323

ADIAL PHARMACEUTICALS, INC.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 82-3074668 | |

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) |

1180 Seminole Trail, Suite 495

Charlottesville, Virginia 22901

(Address of Principal Executive Offices) (Zip Code)

(434) 422-9800

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbols | Name of each exchange on which registered | ||

| Common Stock, par value $0.001 per share | ADIL | The Nasdaq Stock Market LLC | ||

| Warrants to Purchase Shares of Common Stock, par value $0.001 per share | ADILW | The Nasdaq Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the issuer: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer, “accelerated filer” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☒ | Smaller reporting company | ☒ |

| Emerging growth company | ☒ | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant, based on the closing price of a share of the registrant’s common stock on June 30, 2021 (the last business day of the registrant’s mostly recently completed second fiscal quarter) as reported by the Nasdaq Capital Market on such date was $40,504,498. This calculation does not reflect a determination that certain persons are affiliates of the registrant for any other purpose.

As of March 23, 2022, the issuer had 23,718,962 shares of common stock outstanding.

Documents incorporated by reference: None

FORM 10-K

TABLE OF CONTENTS

i

PART I

ADIAL PHARMACEUTICALS, INC.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). In particular, statements contained in this Annual Report on Form 10-K, including but not limited to, statements regarding the sufficiency of our cash, our ability to finance our operations and business initiatives and obtain funding for such activities; our future results of operations and financial position, business strategy and plan prospects, or costs and objectives of management for future initiatives, are forward-looking statements. These forward-looking statements relate to our future plans, objectives, expectations and intentions and may be identified by words such as “may,” “will,” “should,” “expects,” “plans,” “anticipates,” “intends,” “targets,” “projects,” “contemplates,” “believes,” “seeks,” “goals,” “estimates,” “predicts,” “potential” and “continue” or similar words. Readers are cautioned that these forward-looking statements are based on our current beliefs, expectations and assumptions and are subject to risks, uncertainties, and assumptions that are difficult to predict, including those identified below, under Part I, Item lA. “Risk Factors” and elsewhere in this Annual Report on Form 10-K. Therefore, actual results may differ materially and adversely from those expressed, projected or implied in any forward-looking statements. We undertake no obligation to revise or update any forward-looking statements for any reason.

NOTE REGARDING COMPANY REFERENCES

Throughout this Annual Report on Form 10-K, “Adial,” the “Company,” “we,” “us” and “our” refer to Adial Pharmaceuticals, Inc.

Summary Risk Factors

Our business faces significant risks and uncertainties of which investors should be aware before making a decision to invest in our common stock. If any of the following risks are realized, our business, financial condition and results of operations could be materially and adversely affected. The following is a summary of the more significant risks relating to the Company. A more detailed description of our risk factors set forth under the caption “Risk Factors” in Item 1A in Part I of this Annual Report on Form 10-K.

Risks Relating to Our Company

| ● | We have a limited operating history with which to compare, have incurred significant losses since our inception, and expect to incur substantial and increasing losses for the foreseeable future. |

| ● | We currently have no product revenues and may not generate revenue at any time in the near future, if at all. |

| ● | We will need to secure additional financing, which may not be available to us on favorable terms, if at all. |

| ● | We have identified weaknesses in our internal controls. |

| ● | We rely on a license to use various technologies that are material to our business. |

1

| ● | Our business is dependent upon the success of our lead product candidate, AD04, which requires significant additional clinical testing before we can seek regulatory approval and potentially launch commercial sales. |

| ● | The active ingredient of our product candidate, ondansetron, is currently available in generic form. |

| ● | Coronavirus or other global health crises could adversely impact our business, including our clinical trials. |

| ● | Business disruptions could seriously harm our future revenue and financial conditions. |

| ● | For ondansetron, under short-term use, there are currently no long-term use clinical safety data available. |

| ● | All of our current data for our lead product candidate do not necessarily provide sufficient evidence that our products are viable as potential pharmaceutical products. |

| ● | The FDA and/or EMA may not accept our planned Phase 3 endpoints for final approval of AD04. |

| ● | AD04 is dependent on a successful development, approval, and commercialization of a genetic test. |

| ● | We have limited experience as a company conducting clinical trials. |

| ● | Our success will be dependent upon adoption of our products by physicians. |

Risks Relating to Purnovate, Inc. (“Purnovate”)

| ● | The combined company may not experience the anticipated strategic benefits of the acquisition and we may be unable to successfully integrate the Purnovate businesses. |

| ● | Purnovate has a limited operating history upon which to evaluate its ability to commercialize its products. |

| ● | The product candidates of Purnovate are in the early stages of development and there is uncertainty as to whether Purnovate’s technology will result in any successful drug candidates. |

Risks Relating to Our Business and Industry

| ● | We must obtain regulatory approvals in every jurisdiction in which we intend to sell our product candidate and the regulatory approval in one jurisdiction does not guarantee the approval in another jurisdiction. |

| ● | Clinical trials are very expensive, time-consuming and difficult to design and implement. |

| ● | AD04 and any future product candidates may cause undesirable side effects. |

| ● | We may incur substantial liabilities and may be required to limit commercialization of our products in response to product liability lawsuits. |

| ● | There is uncertainty as to market acceptance of our technology and product candidates. |

| ● | We will continue to be subject to ongoing and extensive regulatory requirements even after regulatory approval, and compliance with such regulatory requirements cannot be assured. |

| ● | Our employees, independent contractors, consultants, commercial partners and vendors may engage in misconduct or other improper activities. |

| ● | We have no experience selling, marketing or distributing products and have no internal capability to do so. |

2

| ● | We may not be successful in establishing and maintaining strategic partnerships. |

| ● | Our internal computer systems, or those used by our CROs or other contractors or consultants, may fail or suffer security breaches and we may face particular data protection, data security and privacy risks. |

| ● | We have limited protection for our intellectual property. Our licensed patents and proprietary rights may not prohibit potential competitors from commercializing products. |

| ● | We may be involved in lawsuits to protect or enforce the patents of our licensors, or if independent contractors have wrongfully used or disclosed confidential information of third parties, which could be expensive, time-consuming and unsuccessful. |

| ● | Obtaining and maintaining patent protection depends on compliance with requirements imposed by governmental patent agencies and the Courts. |

| ● | Our ability to generate product revenues will be diminished if our products sell for inadequate prices or patients are unable to obtain adequate levels of reimbursement. |

| ● | We rely on key executive officers and scientific, regulatory and medical advisors. |

| ● | Certain of our officers may have a conflict of interest. |

| ● | We may acquire other businesses or form joint ventures or make investments in other companies or technologies that could harm our operating results, dilute our stockholders’ ownership, increase our debt or cause us to incur significant expense. |

| ● | Declining general economic or business conditions may have a negative impact on our business. |

| ● | Health care policy changes, including legislation reforming the U.S. health care system and other legislative initiatives, may have a material adverse effect on our financial condition, results of operations and cash flows. |

Risks Related to Our Securities and Investing in Our Securities

| ● | Certain of our shareholders have sufficient voting power to make corporate governance decisions that could have a significant influence on us and the other stockholders. |

| ● | Future sales of securities could result in additional dilution. |

| ● | Issuance of additional securities available could adversely affect the rights of the holders of our common stock. |

| ● | If we issue preferred stock with superior rights than our common stock, it could result in a decrease in the value of our common stock and delay or prevent a change in control of us. |

| ● | We have never paid dividends and have no plans to pay dividends in the foreseeable future. |

| ● | Our failure to meet the continued listing requirements of The Nasdaq Capital Market could result in a de-listing of our common stock. |

| ● | We are an “emerging growth company,” and we cannot be certain if the reduced SEC reporting requirements applicable to emerging growth companies will make our common stock less attractive to investors. |

| ● | As a result of being a public company, we are subject to additional reporting and corporate governance requirements that will require additional management time, resources and expense. |

| ● | Our common stock has often been thinly traded, so you may be unable to sell at or near ask prices or at all. |

| ● | Our stock price has fluctuated in the past, has recently been volatile and may be volatile in the future. |

| ● | Our need for future financing may result in the issuance of additional securities which will cause investors to experience dilution. |

| ● | Fluctuations in the international currency markets may significantly impact the cost of our planned trial. |

| ● | The application of the “penny stock” rules to our common stock could limit the trading and liquidity. |

| ● | Provisions in our corporate charter documents and under Delaware law could make an acquisition of our company more difficult and may prevent attempts to replace or remove our current management. |

| ● | Our Certificate of Incorporation and our bylaws provide that the Court of Chancery of the State of Delaware will be the exclusive forum for certain types of state actions. |

| ● | If securities or industry analysts do not publish research or publish inaccurate or unfavorable research about our business, our stock price and trading volume could decline. |

| ● | The warrants that we have issued are speculative in nature and holders of the warrants will have no rights as a common stockholder except as otherwise provided in the warrants until they acquire our common stock. |

| ● | There is no established market for the warrants. |

3

PART I

Item 1. Business

Overview

We are a clinical-stage biopharmaceutical company focused on the development of therapeutics for the treatment or prevention of addiction and related disorders. Our lead investigational new drug product, AD04, is being developed as a therapeutic agent for the treatment of alcohol use disorder (“AUD”). In January 2021, we expanded our portfolio in the field of addiction with the acquisition of Purnovate, LLC via a merger into our wholly owned subsidiary, Purnovate, Inc., (“Purnovate”) and we continue to explore opportunities to expand our portfolio in the field of addiction and related disorders such as pain reduction, both through internal development and through acquisitions. Our vision is to create the world’s leading addiction focused pharmaceutical company. Additionally, we are using Purnovate’s adenosine drug discovery and development platform to invent and develop novel chemical entities as drug candidates for large unmet medical needs with the intention of spinning off or licensing drug candidates and development programs not related to the field of addiction (see Purnovate and the Adenosine Platform below).

Alcohol Use Disorder and AD04

AUD is characterized by an urge to consume alcohol and an inability to control the levels of consumption. We have completed the clinical phase of the landmark ONWARD™ pivotal Phase 3 clinical trial using AD04 for the potential treatment of AUD in subjects with certain target genotypes. As of this filing, all 302 patients included in the trial had completed dosing and follow up visits and the final monitoring and close-out activities are underway (a total of 303 patients were recruited and then randomized in the trial, however, one subject never initiated treatment and has been excluded from enrollment numbers and will not be included in the full analysis data set or efficacy analysis for the trial). ONWARD trial data is expected to be unblinded and analyzed in the second quarter of 2022. We believe our approach is unique in that it targets the serotonin system and individualizes the treatment of AUD, through the use of genetic screening (i.e., a companion diagnostic genetic biomarker). We have created an investigational companion diagnostic biomarker test for the genetic screening of patients with certain biomarkers that, as reported in the American Journal of Psychiatry (Johnson, et. al. 2011 & 2013), we believe will benefit from treatment with AD04. Our strategy is to integrate the pre-treatment genetic screening into AD04’s label to create a patient-specific treatment in one integrated therapeutic offering. Our goal is to develop a genetically targeted, effective and safe product candidate to treat AUD by reducing or eliminating the patients’ consumption of alcohol.

We have a worldwide, exclusive license from the University of Virginia Patent Foundation (d.b.a the Licensing & Venture Group) (“UVA LVG”), which is the licensing arm of the University of Virginia, to commercialize our investigational drug candidate, AD04, subject to Food and Drug Administration (“FDA”) approval of the product, based upon three separate patent application families, with patents issued in over 40 jurisdictions, including three issued patents in the U.S. Our investigational agent has been used in several investigator-sponsored trials and we possess or have rights to use toxicology, pharmacokinetic and other preclinical and clinical data that support our landmark ONWARD pivotal Phase 3 clinical trial. Our therapeutic agent was the product candidate used in a University of Virginia investigator sponsored Phase 2b clinical trial of 283 patients. In this Phase 2b clinical trial, ultra-low dose ondansetron, the active pharmaceutical agent in AD04, showed a statistically significant difference between ondansetron and placebo for both the primary endpoint and secondary endpoint, which were reduction in severity of drinking measured in drinks per drinking day (1.71 drinks/drinking day; p=0.0042), and reduction in frequency of drinking measured in days of abstinence/no drinking (11.56%; p=0.0352), respectively. Additionally, and importantly, the Phase 2b results showed a significant decrease in the percentage of heavy drinking days (11.08%; p=0.0445) with a “heavy drinking day” defined as a day with four (4) or more alcoholic drinks for women or five (5) or more alcoholic drinks for men consumed in the same day.

The active pharmaceutical agent in AD04, our lead investigational new drug product, is ondansetron, which is also the active ingredient in Zofran®, which was granted FDA approval in 1991 for nausea and vomiting post-operatively and after chemotherapy or radiation treatment and is now commercially available in generic form. In studies of Zofran®, conducted as part of its FDA review process, ondansetron was given acutely at dosages up to almost 100 times the dosage expected to be formulated in AD04 with the highest doses of Zofran® given intravenously (“i.v.”), which results in approximately 160% of the exposure level as oral dosing. Even at high doses given i.v. the studies found that ondansetron is well-tolerated and results in few adverse side effects at the currently marketed doses, which reach more than 80 times the AD04 dose and are given i.v. The formulation dosage of ondansetron used in our drug candidate (and expected to be used by us in our Phase 3 clinical trials) has the potential advantage that it contains a much lower concentration of ondansetron than the generic formulation/dosage that has been used in prior clinical trials, is dosed orally, and is available with use of a companion diagnostic genetic biomarker. Our development plan for AD04 is designed to demonstrate both the efficacy of AD04 in the genetically targeted population and the safety of ondansetron when administered chronically at the AD04 dosage. However, to the best of our knowledge, no comprehensive clinical study has been performed to date that has evaluated the safety profile of ondansetron at any dosage for long-term use as anticipated in our ongoing and planned clinical trials.

4

According to the National Institute of Alcohol Abuse and Alcoholism (the “NIAAA”) and the Journal of the American Medical Association (“JAMA”), in the United States alone, approximately 35 million people each year have AUD (such number is based upon the 2012 data provided in Grant et. al. the JAMA 2015 publication and has been adjusted to reflect a compound annual growth rate of 1.13%, which is the growth rate reported by U.S. Census Bureau for the general adult population from 2012-2017), resulting in significant health, social and financial costs with excessive alcohol use being the third leading cause of preventable death and is responsible for 31% of driving fatalities in the United States (NIAAA Alcohol Facts & Statistics). AUD contributes to over 200 different diseases and 10% of children live with a person that has an alcohol problem. According to the American Society of Clinical Oncologists, 5-6% of new cancers and cancer deaths globally are directly attributable to alcohol. And, The Lancet published that alcohol is the leading cause of death in people ages 15-49 globally. The Centers for Disease Control (the “CDC”) has reported that AUD costs the U.S. economy about $250 billion annually, with heavy drinking accounting for greater than 75% of the social and health related costs. Despite this, according to the article in the JAMA 2015 publication, only 7.7% of patients (i.e., approximately 2.7 million people) with AUD are estimated to have been treated in any way and only 3.6% by a physician (i.e., approximately 1.3 million people). In addition, according to the JAMA 2017 publication, the problem in the United States appears to be growing with almost a 50% increase in AUD prevalence between 2002 and 2013.

AUD is characterized by an urge to consume alcohol and an inability to control the levels of consumption. Until the publication of the fifth revision of the Diagnostic and Statistical Manual of Mental Disorders in 2013 (the “DSM-5”), AUD was broken into “alcohol dependence” and “alcohol abuse”. More broadly, overdrinking due to the inability to moderate drinking is called alcohol addiction and is often called “alcoholism”, sometimes pejoratively.

Since ondansetron is already manufactured for generic sale, the active ingredient for AD04 is readily available from several manufacturers, and we have contracted with a U.S. manufacturer to acquire ondansetron at a cost expected to be under $0.01 per dose. Clinical trial material (“CTM”) has already been manufactured for the ONWARD Phase 3 trial. The CTM has demonstrated good stability after four years with the stability studies to date.

We have also developed the manufacturing process at a third-party vendor to produce tablets at what we expect will serve for commercial scale production (i.e., greater than 1 million tablets per batch), also at a cost expected to be less than $0.01 per dose. A proprietary packaging process has been developed, which appears to extend the stability of the drug product. Packaging costs are expected to be less than $0.05 per dose. We do not have a written commitment for supply of either the tablets or the packaging and believe that alternative suppliers are available to whom we can transfer the processes that have been developed.

Methods for the companion diagnostic genetic test have been developed as a blood test, and we established the test with a third-party vendor capable of supporting our clinical program. Additionally, we have built validation and possible approval of the companion diagnostic into the Phase 3 program, including that we plan to store blood samples for all patients in the event additional genetic testing is required by regulatory authorities.

COVID-19 Impact

Recruitment of patients in the ONWARD Phase 3 trial was slower than anticipated due to COVID-19 related governmental lockdowns in countries in which we were conducting the ONWARD Phase 3 trial. However, we have now completed the trial. Our corporate offices were open and operating without pause throughout the pandemic.

Recent Developments

On February 24, 2022, we provided the following highlighted updates on our landmark ONWARD pivotal Phase 3 clinical trial of AD04 for the treatment of AUD

| ● | All subjects have completed dosing in the ONWARD trial |

| ● | 302 subjects were enrolled in the ONWARD trial; this exceeded the 290 subjects targeted for enrollment |

| ● | Subjects were enrolled across 25 clinical sites in six countries. |

5

Disease Targets and Markets for AD04

Limitations of Current AUD Therapies

Today the most common treatments for AUD are directed at achieving abstinence and typical treatments include psychological and social interventions. Most therapies actually require abstinence prior to initiating therapy. Abstinence requires dramatic lifestyle changes often with serious work and social consequences. Frequently, patients cannot attend family and social events in order to ensure compliance with abstinence, and patients often must suffer from the stigma of having been labelled an alcoholic. Significant side effects of current pharmacologic therapies include mental side effects such as psychiatric disorders and depressive symptoms and physical side effects such as nausea, dizziness, vomiting, abdominal pain, and hepatoxicity. In fact, according to peer reviewed studies referenced in The Sober Truth: Debunking the Bad Science Behind 12-Step Programs and the Rehab Industry, L. Dodes and Z. Dodes, 2014 by Dr. Lance Dodes, the former Director of the substance abuse treatment unit of Harvard’s McLean Hospital, 90% or more of patients that use current therapy solutions, such as Alcoholics Anonymous, do not achieve long-term abstinence.

There are four drugs approved by the FDA and marketed in the United States for the treatment of alcohol addiction, Antabuse® (disulfram) Vivitrol® (naltrexone), Revia® (naltrexone) and Campral® (acomprosate) and one drug, Selincro® (nalmefene) is marketed outside of the United States. All of the approved drugs, other than Selincro®, require abstinence prior to commencing treatment with the drug, and all five drugs are known to have significant side effects.

Antabuse® was approved for the treatment of alcohol dependence more than 50 years ago, making it the oldest such drug on the market. It works by interfering with the body’s ability to process alcohol. Its method of action and purpose is to cause patients that drink alcohol while taking Antabuse® to experience numerous and extremely unpleasant adverse effects, including, among others, flushing, nausea, and palpitations, with the goal that patients will continue the medication but refrain from drinking in order to avoid these effects.

Naltrexone, which can be taken as a once-daily pill (Revia®) or in an approved once-monthly injectable form (Vivitrol® ) that requires a doctor to administer is often associated with gastrointestinal complaints and has been reported to cause liver damage when given at certain high doses. As a result, it carries an FDA boxed warning, a special emphasized warning, for this side effect.

Campral®, taken by mouth three times daily, acts on chemical messenger systems in the brain.

Selincro® has not been approved for sale in the United States.

Our Proposed Solution

Our goal with AD04 is to develop an effective and safe product to treat AUD that does not require abstinence as part of the treatment and does not have the negative side effects of the current drugs on the market. Our product candidate, AD04, is designed for genotype positive patients who desire to control their drinking but cannot or do not want to completely abstain from drinking. By removing the difficulties associated with abstinence and the side effects associated with the other current products on the market, we believe that we may be able to remove barriers to patient adoption that inhibit adoption of current therapies and can attract a greater portion of the many millions of patients with AUD that remain untreated. Unlike other therapies, our investigational product, AD04, uses a novel mode of action for treating AUD that involves genetic screening with a companion diagnostic genetic test prior to treatment and is designed to reduce cravings for alcohol to effectively curb alcohol intake, without the requirement of abstinence prior to or during treatment. Our product candidate is intended to be easy to use since it is administered orally, currently on a twice daily basis and with a once-a-day tablet planned as part of the product’s life cycle management. To date, clinical testing of AD04 has shown it to have a positive safety and tolerability profile with side effects similar to placebo.

The companion diagnostic genetic test to be used to identify patients that are most likely to benefit from treatment with AD04 may potentially enhance the likelihood of a successful outcome for those undergoing treatment. Additionally, it may provide doctors with the opportunity to have a non-threatening conversation about alcohol with their patients and may provide the patient an acceptable path to help them determine if they might be a candidate for help with their alcohol use. If the test results are positive, they would have a science-based rationale for their treatment, which reduces some of the stigma patients might otherwise endure, and potentially allows them to be treated in the confidence of their doctor with an oral tablet.

6

Strengths and Competitive Advantages

Large Market Opportunity for an Effective Solution

In the United States alone, approximately 35 million people each year have AUD. Based on data from the Phase 2b trial of AD04 and our analysis of publicly available genetic databases, we preliminarily estimate that about one in three patients with AUD in the U.S. will have the genetic markers to indicate possible treatment with AD04. At this time, we are not aware of any oral pharmaceutical treatment approved in the U.S. that addresses the needs of patients who desire to control their drinking but cannot or do not want to abstain from drinking. The current abstinence-based treatments have limitations. The limited side effects expected for our investigational new drug, based on clinical data so far, are also believed to be an important factor in the expected rapid uptake of AD04 in the market. Our approach, if approved by FDA, may allow for social drinking to continue and is aimed at reducing the dangerous, heavy drinking. This would allow patients to live the life they want without the stigma associated with complete abstention and currently endured by those seeking help for their excessive drinking. Assuming that one-third of AUD patients are genotype positive for treatment with AD04 and a $255 price for a one month supply of the drug (assumed pricing based on an average of prices published by Blue Cross Blue Shield in June 2017 for tier-3 oral, on-patent, chronic maintenance drugs, discounted by 16.6%, to reflect the average difference between retail and wholesale pricing for branded drugs as reported by drugs.com), the total potential market for AD04 would be approximately $36 billion in the United States alone.

Beyond the United States, alcohol consumption worldwide is a serious health issue. The 2014 Global Status Report on Alcohol and Health published by the World Health Organization (the “WHO”) states that 5.9% of all deaths (about 3.3 million per year) and 5.1% of disease worldwide are attributable to alcohol consumption. Europe consumes over 25% of the total alcohol consumed worldwide despite only having 14.7% of the world’s population. The WHO estimates that about 55 million people in Europe have AUD and, within Europe, Eastern Europe has a particularly acute problem with Russia estimated to have about 21 million people with AUD. The WHO further estimates that 17.4% of adult Russians and 31% of adult Russian males have AUD, and the Organization for Economic Cooperation and Development data indicates that 30% of all deaths in Russia are alcohol related as reported by Quartz Media.

Companion Genetic Bio-Marker Aimed at Identifying Patients Most Likely to Respond To Treatment, Potentially Results in Increased Use of AD04

We believe our drug is unique in that it is designed to reduce heavy drinking in individuals with certain genotypes. We are pursuing a strategy that aims to integrate pre-treatment screening with the companion diagnostic genetic test into the drug label, essentially combining the test and treatment into one integrated therapeutic offering that has combined intellectual property protections. This companion diagnostic testing approach may be a useful genetic screening tool to predict those most likely to respond to the drug and to have minimal side effects. Based on the clinical experience to date and publicly available databases, we believe the genetic prevalence of genotype positive people is about 33% of the population in the United States. We previously believed the prevalence in Scandinavia and in certain areas of Central and Eastern Europe may be greater than 50%, but our experience in the ONWARD Phase 3 clinical trial indicates the prevalence in this area to also be about 33%. The FDA has agreed that the Phase 3 trials of AD04 can proceed only enrolling patients that are genotype positive, which greatly reduces the cost, time and risk relative to a trial that also enrolled patients that are genotype negative for treatment with AD04. We are conducting our current landmark ONWARD pivotal Phase 3 clinical trial in counties in Scandinavia and Central and Eastern Europe, including Finland, Sweden, Latvia, Poland, Bulgaria, and Croatia. We expect to use the ONWARD trial as a pivotal Phase 3 trial to serve as a basis for approval in both the United States and Europe.

We believe that the companion diagnostic genetic test enables physicians to more easily have an initial conversation with their patients about alcohol use and, for the patient, provides a less threatening and obtrusive first step toward treatment because the conversation will include the topic of genetic testing and not be solely about behavior. Patients that then test positive against the AD04 genetic panel would be expected to be more likely to then receive a prescription for AD04 (based on an external quantitative market study of 156 primary care physicians and psychiatrists that was conducted by Ipsos-Insight LLC, who we commissioned, and that concluded a majority of genetically targeted patients currently receiving pharmacologic treatment would be switched to a drug with the characteristics expected for AD04).

7

Prior Work of Universities and our Ability to Leverage Relationships Creates Cost Efficiencies

We have a worldwide, exclusive license to intellectual property developed at the University of Virginia by our Chief Medical Officer, Dr. Bankole A. Johnson, who was Chairman of the Department of Psychiatry & Neurobehavioral Sciences at the University of Virginia (and prior to that the Chief of the Division of Alcohol and Drug Addiction at the University of Texas) and was Chair, Department of Psychiatry and Director of the Brain Science Research Consortium Unit at the University of Maryland. Dr. Johnson has spent almost three decades researching the underlying subject matter. Significant portions of the supporting research were also funded under grants from the National Institute of Health to the University of Virginia and the University of Texas. On July 5, 2019, we entered into a Master Services Agreement and statement of work with Psychological Education Publishing Company (“PEPCO”), a company owned by Dr. Johnson, that is engaged in the business of administering a behavioral therapy program, Brief Behavioral Compliance Enhancement Treatment, for our Phase 3 clinical trial using AD04, for the treatment of AUD.

By leveraging the prior work of universities and their researchers, including their pre-clinical studies and accumulated data, we believe we have developed a significant drug development opportunity. Because of the licensing approach taken to secure intellectual property, including, without limitation, patents and rights to clinical trial data, and our collaborations with the University of Virginia, we, historically have not had to incur the significant costs that would normally be required to develop therapeutic treatments to the point of being ready to commence a Phase 3 clinical trial, which often amount to tens of millions of dollars or more. In fact, based upon current information, and depending on what the regulatory authorities may require to secure marketing authorization, we estimate that we will require approximately $10.7 million for the current Phase 3 clinical trial (not including company overhead) and an additional $30 million or more of additional capital to complete our second Phase 3 program (which includes $20 million for a confirmatory Phase 3 trial and any necessary Phase 1 clinical trials and other development expenses and does not include the additional cost of a possible third Phase 3 clinical trial) as currently contemplated in order to achieve regulatory approval for the use of AD04 to treat AUD in the United States and Europe. We have already used approximately $8.9 million in funds derived from our initial public offering and subsequent financings and warrant exercises to fund trial activities. We anticipate that the approximate $2.1 million needed to complete the initial Phase 3 clinical trial to the point of releasing data and the completion of follow-up activities will be fully funded from our cash on hand. We anticipate, with our expected rate of expenditure, including Purnovate related research and development projects and Company overhead, to have exhausted our funds on hand by the end of April 2023. Additional funding will be needed to fund an additional Phase 3 trial of AD04, if necessary, as well as Purnovate research and development projects and Company overhead. There is no assurance that such funds could be raised in time to complete the trial on acceptable terms.

The NIAAA has provided and continues to provide technical assistance and advice to us, and we have applied for an NIAAA Research Resource Award, which if granted would provide financial support for our Phase 3 clinical trial. Although there can be no assurance that we will be selected by the NIAAA to receive funding, since we are not aware of any pharmaceutical company planning Phase 3 pivotal trials to serve as a basis for marketing approval for products for the treatment of AUD, we believe AD04 would be a competitive candidate. Currently, much of the funding expected for grants such as those for which we have applied has been diverted to COVID-19-related grants, and we are not certain if and when funding for grants such as ours will be available.

8

Known, Well-Tested Agent Has Shown Favorable Results in Non-AUD Uses

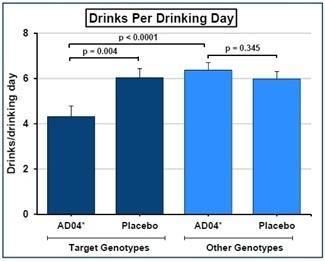

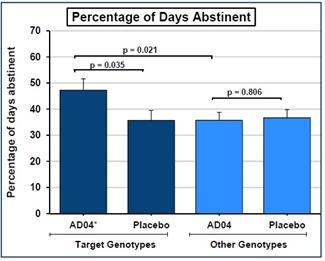

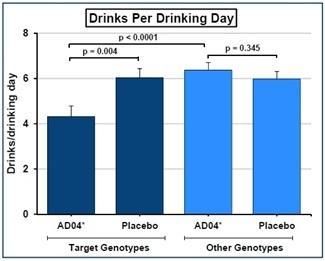

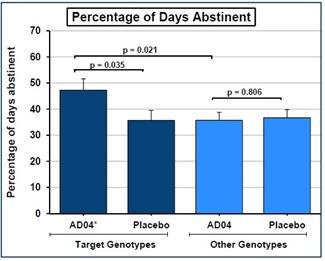

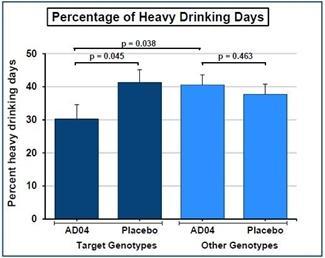

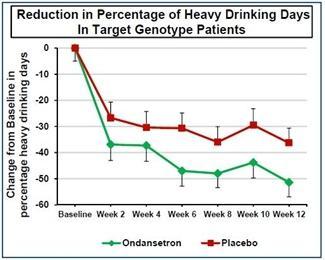

Ondansetron, the principal active pharmaceutical agent in AD04 has been approved by the FDA to treat nausea and vomiting but is administered at much higher doses than we intend to use and has shown limited side effects even at the higher dosages currently on the market. However, it has not been approved in our anticipated dosage or for our anticipated uses and treatment period. Consequently, we expect to submit a new drug application, pursuant to section 505(b)(2) of the Federal Food, Drug, and Cosmetic Act, for U.S. marketing authorization. Section 505(b)(2) of the Federal Food, Drug, and Cosmetic Act allows the FDA to rely, for approval of an NDA, on data not developed by the applicant. Such an NDA contains full reports of investigations of safety and effectiveness, but where at least some of the information required for approval comes from studies not conducted by or for the applicant and for which the applicant has not obtained a right of reference. Such applications permit approval of applications other than those for duplicate products and permits reliance for such approvals on literature or an FDA finding of safety and/or effectiveness for an approved drug product. A Phase 2b University of Virginia investigator sponsored clinical trial of AD04 for the treatment of AUD showed promising results and no overt safety concerns (there were no statistically significant serious adverse events reported). Not only did the trial show no statistically significant, serious adverse side effects, but both of the pre-specified endpoints, reduction in severity of drinking measured in drinks per day of drinking day and reduction in frequency of drinking measured in days of abstinence, were met with statistical significance as shown in the graph below:

Phase 2b Clinical Trial Results– Analysis of Primary and Secondary Efficacy Endpoints for Target Genotypes

A 12-week, randomized, two-center, parallel-group, double-blind, placebo-controlled, two-arm (four cell) clinical trial of oral ondansetron (n=283) conducted by University of Virginia

|

|

Our Substantial Proprietary Estate and Protection from Competition

We currently hold a worldwide, exclusive license to three (3) patent families that provide us with the ability to exclude potential competitors from practicing the claimed inventions, such as the use of ondansetron to treat any of the four (4) specified genotypes for AUD. Our licensed patent estate is expected to provide us patent protection through 2032 plus possible extensions. Ondansetron, the active ingredient in AD04, has never been approved in a low dosage near the AD04 dose of 0.33mg per tablet, and we believe our licensed patents will protect AD04 from any competitor that attempts to bring to market an ondansetron dose at or near the AD04 dose for treatment of patients having one or more of the four target genotypes.

We believe use of the currently marketed doses “off-label” will not be significant due to (i) the lack of demonstrated efficacy at currently marketed doses, (ii) potential safety concerns if the currently marketed doses are used chronically as is expected to be necessary for treating AUD, and (iii) cutting the smallest currently marketed dose into the 12 pieces that would be necessary to achieve the AD04 dose is deemed by us to be impractical and likely to result in inaccurate dosing.

Companion Genetic Bio-Marker Aimed at Identifying Patients Most Likely to Respond To Treatment, Potentially Results in Increased Use of AD04

We believe our drug is unique in that it is designed to treat individuals with certain genotypes. We are pursuing a strategy that aims to integrate pre-treatment screening with the companion diagnostic genetic test into the drug label, essentially combining the test and treatment into one integrated therapeutic offering that has combined intellectual property protections. This companion diagnostic testing approach may be a useful genetic screening tool to predict those most likely to respond to the drug and to have minimal side effects. Based on the clinical experience to date and publicly available databases, we believe the genetic prevalence of genotype positive people is about 33% of the population in the United. We previously believed the prevalence in Scandinavia and in certain areas of Central and Eastern Europe may be greater than 50%, but our experience in the ONWARD Phase 3 clinical trial indicates the prevalence in this area to also be about 33%. The FDA has agreed that the Phase 3 trials of AD04 can proceed only enrolling patients that are genotype positive, which greatly reduces, the cost, time and risk relative to a trial that also enrolled patients that are genotype negative for treatment with AD04. The FDA has indicated that any approval based on a trial only in genotype positive patients would result in labeling restricted to treating genotype positive patients.

We believe that the companion diagnostic genetic test enables physicians to more easily have an initial conversation with their patients about alcohol use and, for the patient, provides a less threatening and obtrusive first step toward treatment because the conversation will include the topic of genetic testing and not be solely about behavior. Patients that then test positive against the AD04 genetic panel would be expected to be more likely to then receive a prescription for AD04.

9

Experienced Leadership

Our management, advisors and board of directors have extensive experience in pharmaceutical development, the clinical trial and regulatory approval processes, drug commercialization, financing capital-intensive projects, and developing new markets for pharmaceutical agents. Members of our team have previously worked in senior management and senior officer positions, or led significant research initiatives at Gensia, Clinical Data, Shire, Viagene, New River Pharmaceuticals, Collateral Therapeutics, Indivior, Krystal Biotech, Sucampo Pharmaceuticals, Osiris Therapeutics, Adenosine Therapeutics, and the University of Virginia and University of Maryland in a broad range of therapeutic areas. Our management and board members have particular expertise in the science and development of addiction related drugs and bringing new drugs to the market.

Our Strategy for AD04 and Addiction Related Diseases and Disorders

We develop pharmaceutical treatments for addictions and addictive disorders and related diseases and disorders. Our business strategy is to advance AD04, our lead investigational drug candidate, toward regulatory approval for alcohol addiction in the United States, the European Union, and then eventually other territories. We subsequently plan to develop label expansions into other indications (e.g., opioid use disorder, other drug addictions, obesity, smoking cessation, eating disorders and anxiety). Additionally, we are inventing and developing novel therapeutic agents at our chemistry facilities and seeking to acquire addiction related assets, particularly those expected to be synergistic with AD04 once it is marketed, if it is approved.

Our goals in executing this strategy are to keep capital requirements to a minimum, expedite product development, gain access to clinical research and manufacturing expertise that will advance product development, approval and eventual market uptake of our product, and rely on a well-defined and carefully executed intellectual property strategy in order to position our products with long-term, defensible, competitive advantages. Execution of this strategy may include seeking grant funding and funding from partners and collaborators when available on terms we believe to be favorable to us, and on which there is no guarantee will be available. In collaboration with our CRO, we have been and are working to adapt the implementation of our strategy in response to the ongoing coronavirus pandemic.

Our near-term strategy includes:

| ● | Obtaining regulatory approval for our lead product in the United States and Europe. We have completed our initial Phase 3 clinical trial for the treatment of AUD in Scandinavia and Central and Eastern Europe and are conducting close-out activities to allow data analysis and reporting of results. If our initial Phase 3 clinical trial is successful, we expect to conduct a second, and possibly a third, Phase 3 clinical trial in the same areas but with additional clinical sites in the United States and Western Europe. |

| ● | Prosecuting and expanding our intellectual property and product portfolio. We have acquired rights to a promising drug candidate and made a significant investment in the development of our licensed patent portfolio to protect our technologies and programs, and we intend to continue to do so. We have obtained exclusive rights to three different patent families directed to therapeutic methods related to our AD04 platform. These families include 3 issued U.S. patents, and at least one foreign equivalent patent covering AD04 issued in over 40 national jurisdictions, including most of Europe and Eurasia. Divisional and continuation applications to expand the coverage have also been filed in certain jurisdictions. Additionally, commencing in early 2021, we have an adenosine platform that has and is expected to continue to generate what we believe are patentable new chemical entities. We intend that further product portfolio expansions will be focused on promising addiction therapies and/or late-stage clinical assets. | |

| ● | Evaluating the additional use of our product candidate in other indications. In addition to alcohol addiction, we plan to conduct exploratory work to investigate using AD04 as a potential treatment for opioid use disorder, gambling addiction, smoking cessation, obesity, and other addiction related disorders in which 5-HT3 antagonism may have a treatment effect. We believe we will be able to undertake this initial exploratory effort with minimal additional cash cost to our company through the use of academic partnerships, grants, human laboratory studies and/or non-clinical studies. We believe that, due to its hypothesized mechanism of action (i.e., the modulation of the serotonin system in patients that are genetically targeted based on the apparent sensitivity to such modulation, where the modulation appears to reduce cravings), AD04 has the potential to be used for the treatment of such other addictive disorders. To date, we have not discussed these potential uses with the FDA or any other regulatory bodies. |

10

| ● |

Maximizing commercial opportunity for our technology. AD04 targets large markets with significant unmet medical need. We intend to develop an extended release, once-a-day formulation of AD04 to enhance compliance and market appeal

| |

| ● | Managing our business with efficiency and discipline. We believe we have efficiently utilized our capital and human resources to develop and acquire our product candidate and programs and create a broad intellectual property portfolio. We operate cross-functionally and are led by an experienced management team with backgrounds in developing product candidates. We use project management techniques to assist us in making disciplined strategic program decisions and to attempt to limit the risk profile of our product pipeline. |

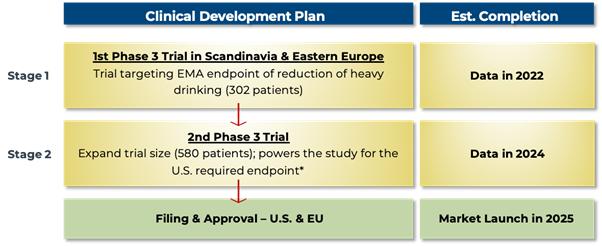

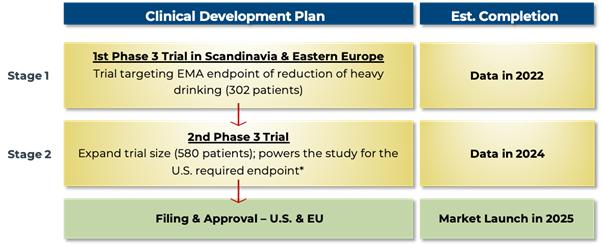

The clinical development plan for AD04 can be described as a two-stage development strategy in which we expend limited resources to achieve the significant value inflection point of Phase 3 data in our primary indication of AUD. With a successful trial and the risk reduction associated with that success, we would then be ready to conduct the final trials to seek approval in the U.S. and Europe as shown below:

AD04 — Two-Stage Clinical Development Strategy — Conduct the Phase 3 clinical trials sequentially

| * | Even if the 1st Phase 3 trial is not accepted by the FDA as a pivotal trial due to the study not being well-powered for the FDA’s currently stated end point, we still expect that the EMA will require only one additional trial. In this case, however, a 3rd trial might be required by the FDA (i.e., three Phase 3 trials in total). If two additional trials are required for FDA approval after an initial Phase 3 trial conducted in the EMA, we would expect to run the 2nd and 3rd trials in parallel (i.e., at the same time) so as not to increase the expected time to approval. The 2nd Phase 3 trial is expected to require $20 million in direct expenses, and up to $10 million in additional other development expenses is expected to be required. A possible 3rd Phase 3 trial would be expected to require an additional $20 million in clinical trial related expenditures. |

11

Assuming approval of AD04, we plan to execute a two-stage commercialization plan. With psychiatrists and addiction specialists treating a majority of the current AUD patients today and with psychiatrists most likely to be familiar with the mechanism of action of AD04, we believe that a relatively small psychiatry-targeted, specialty sales force could successfully sell AD04 into the market. This plan creates the opportunity for us to develop into a commercial enterprise with an initial niche-market sales force at a relatively low cost for market entry. It also expands the universe of potential acquirers of our company or AD04 to smaller and mid-size pharmaceutical companies. Once success is shown in the niche market and the thought leaders and early adopters are prescribing AD04, market adoption risk will have been greatly reduced and we would expect to be able to sell or partner with a large pharmaceutical partner to develop AD04 as a blockbuster product. This commercialization plan is shown below:

AD04 — Two-Stage Commercialization Strategy — Initial launch with a specialty sales force to build the market, then partner or sell to a large pharmaceutical partner to capture market share and optimize the market

Ondansetron History and Foundation for Treating AUD

Ondansetron is a 5-HT3 receptor antagonist. Preclinical and pharmacobehavioral studies suggest that blockade of serotonin-3 receptors will influence the dopamine reward system activated by alcohol, decreasing dopamine release and attenuating craving for alcohol (Dawes, MA et al., 2005b; Johnson, BA et al., 2002; Lovinger, DM, 1999a). Early clinical studies found that the efficacy of ondansetron is limited to certain subgroups of the alcohol-dependent population and suggested the differential effect could be predicted based on age of onset of alcoholism, an indistinct concept likely confounded by genetic, regional and ethnic differences (Johnson, BA et al., 2000; Kranzler, HR et al., 2003). Recent research suggests the variable effect may be predictable based on molecular mechanism of ondansetron action and individual subject genotype of key genes in the serotonin system (Enoch, MA et al., 2010; Johnson, BA et al., 2011; Kenna, GA et al., 2009).

We are pursuing development of ondansetron in the alcohol-dependent population. Clinical studies will initially focus on the use of a low dose, oral tablet (0.33 mg administered twice daily) to reduce alcohol consumption in subjects with genotypes that have been correlated with a responsive to treatment with ondansetron.

Ondansetron was first approved by the FDA in 1991 as a solution for injection. Subsequent approvals were obtained for oral tablets in dosage forms and an oral solution. It is marketed as Zofran® and is also available in generic formulations, and it has been used widely for the approved indications – prevention of nausea and vomiting associated with certain cancer chemotherapies and radiotherapies and for the prevention of postoperative nausea or vomiting — at adult doses of 8–24 mg/day with manageable side effects.

Ondansetron has been administered to dogs‚ rats‚ and mice as part of a preclinical toxicology program which included single-dose acute‚ repeated-dose studies. Ondansetron was not mutagenic in the standard battery of microbial tests for mutagenicity and no carcinogenic effects were seen in 2-year studies in rats and mice with oral ondansetron doses up to 10 and 30 mg/kg/day, respectively. In studies of rats and rabbits there was no evidence of reproductive toxicity seen on fertility, early embryonic development, perinatal/postnatal development or fetal development of the F2 generation. Based on these studies, as well as over 20 years of human use in clinical trials and the post-marketing environment, ondansetron is considered to be a well-tolerated drug with a generally mild safety profile.

Ondansetron, by blocking the 5-HT3 receptor, is known to affect dopaminergic signaling in the brain; and the scientific rational for use of a 5-HT3 antagonist in the treatment of alcohol dependence is well established (Johnson, BA, 2004). Briefly, studies suggest that: the rewarding effects of alcohol involve activation of the 5-HT3 receptors leading to release of dopamine within the mesolimbic system of the brain (McBride, WJ et al., 2004). Thus, by blocking activation of the 5-HT3 receptor, ondansetron may reduce the ethanol-stimulated release of dopamine leading to reduced feelings of pleasure or reward and consequently, reduced consumption (Carboni, E et al., 1989; Costall, B et al., 1987; Hagan, RM et al., 1990; Imperato, A and Angelucci, L, 1989; Lovinger, DM, 1999b; McBride, WJ et al., 2004; Minabe, Y et al., 1991; Rasmussen, K et al., 1991; Wozniak, KM et al., 1990; Yoshimoto, K et al., 1996).

12

Preclinical studies have demonstrated that alcohol stimulates the release of both serotonin (5-hydroxytryptamine or 5-HT) and dopamine within the cortio-mesolimbic system (Campbell, AD et al., 1996; Campbell, AD and McBride, WJ, 1995; Di Chiara, G and Imperato, A, 1988; Imperato, A and Angelucci, L, 1989; Yoshimoto, K et al., 1992; Yoshimoto, K et al., 1996; Zazpe, A et al., 1994). Other studies have shown that alcohol potentiates the effects of 5-HT at the 5-HT3 receptor, leading to augmented release of dopamine, and that ondansetron and the selective antagonists of the 5-HT3 receptor inhibit dopaminergic firing and release of dopamine in response to alcohol and serotonin (Costall, B et al., 1987; Lovinger, DM, 1991; Minabe, Y et al., 1991; Rasmussen, K et al., 1991; Yoshimoto, K et al., 1996; Zazpe, A et al., 1994; Zhou, Q et al., 1998). Finally, numerous in vivo studies in rats and mice have shown that ondansetron and other selective antagonist of the 5-HT3 receptor reduce volitional intake of alcohol in models selectively bred for alcohol preference (Fadda, F et al., 1991; Hodge, CW et al., 1993; McBride, WJ and Li, TK, 1998; Meert, TF, 1993; Tomkins, DM et al., 1995).

The aforementioned nonclinical studies have shown that 5-HT3 and dopamine interactions in the cortico-mesolimbic system appear to mediate many of the reinforcing effects of alcohol. Collectively the available nonclinical studies suggest that, by inhibiting the 5-HT3 receptor and reducing the release of dopamine in the cortico-mesolimbic area, ondansetron can interfere with the dopamine reward system activated by alcohol and lead to reduced alcohol intake (Barnes, NM and Sharp, T, 1999; Dawes, MA et al., 2005b; Johnson, BA et al., 1993; Johnson, BA and Cowen, PJ, 1993; Lovinger, DM, 1991, 1999a; Swift, RM et al., 1996; Tomkins, DM et al., 1995).

Five clinical studies have been conducted that demonstrate ondansetron is a promising treatment for alcohol-dependent individuals (Johnson, BA et al., 2011; Johnson, BA et al., 2000; Kenna, GA et al., 2009; Kranzler, HR et al., 2003; Sellers, EM et al., 1994). Several important findings in these studies guide the design of future clinical studies, including:

| (1) | Ondansetron’s efficacy in alcohol-dependent individuals is associated optimally with a small dose of the compound (0.25-0.33 mg twice daily), a dose that is <1/10 of the dose used for adults for the currently approved indications. |

| (2) | In clinical studies in over 600 subjects, ondansetron was well-tolerated and safe, with a mild side-effect profile when administered to currently drinking alcohol-dependent individuals. Overall, the types of adverse events reported during multi-week clinical studies in alcohol dependence appear similar to those outlined in the package insert for the approved indications and to those reported in the literature for treatment in chronic liver disease, chronic fatigue syndrome and schizophrenia. |

| (3) | The extent of benefit with ondansetron treatment varies among different subtypes of alcohol-dependent subjects. Prior studies found that ondansetron benefited subjects with early-onset alcoholism (EOA) but not late-onset alcoholism (LOA). The pharmacological reason for this was not known, but it was presumed that the differential effect was due to a higher degree of serotonergic dysfunction in EOA (Johnson, BA et al., 2000; Kranzler, HR et al., 2003). |

13

The below table summarizes the five clinical studies demonstrating ondansetron is a promising treatment for alcohol-dependent individuals

| Study type (Reference) | Number of Subjects |

Dosing (Duration) |

Summary Results | |||

|

Phase 2 (Sellers, EM et al., Clinical Efficacy of the 5-HT3 Antagonist Ondansetron in Alcohol Abuse and Dependence, Alcohol Clin Exp Res, 18 (1994) 879-885.) |

71 | 0.25 mg, 2 mg, and placebo b.i.d. (6 weeks) |

The 0.25 mg dose showed a near significant effect in reducing severity of drinking measured in DDD (p=0.06) while the 2 mg dose was similar to placebo. | |||

|

Phase 2 (Johnson, BA et al., Ondansetron for Reduction of Drinking among Biologically Predisposed Alcoholic Patients: A Randomized Controlled Trial, JAMA, 284 (2000) 963-971)

|

321 | 1, 4, and 16 ug/kg b.i.d. (11 weeks) |

Ondansetron treatment at doses of 1, 4, and 16 µg/kg bid resulted in significant reductions in DDD in EOA subjects, but only the 4 µg/kg dose showed such a reduction in frequency of drinking measured in PDA and the maximal effect was shown at the µg/kg does. Only the 4 µg/kg bid showed significant improvements in PDA in the LOA group. | |||

|

Phase 2 (Kranzler, HR et al., A within-Group Design of Nontreatment Seeking 5-HTTLPR Genotyped Alcohol-Dependent Subjects Receiving Ondansetron and Sertraline, Alcohol Clin Exp Res, 33 (2009) 315-323)

|

40 | 4 ug/kg bid for 8 weeks | EOA subjects showed significant improvement over LOA subjects in DDD. | |||

|

Phase 2 (Kenna, GA et al., Pharmacogenetic Approach at the Serotonin Transporter Gene as a Method of Reducing the Severity of Alcohol Drinking, Am J Psychiatry, 168 (2011) 265-275)

|

21 | .5 mg/day for 3 weeks | LL genotype subject showed significant improvement in DDD. | |||

|

Phase 2b (Johnson, BA et al., Determination of Genotype Combinations That Can Predict the Outcome of the Treatment of Alcohol Dependence Using the 5-HT3 Antagonist Ondansetron, Am J Psychiatry (2013) |

283 | 4 ug/kg bid (12 weeks, including 1 week placebo run-in) |

The target genotype group showed significant improvement in DDD and PDA against both the placebo groups and other genotypes on drug. |

Additional detail with respect to four of the clinical studies referenced in the chart above is provided below with the fifth being the Phase 2b clinical trial upon which we are basing the development of AD04 and which is described more fully in the following section titled “Phase 2b Investigator Initiated Clinical Trial of AD04 for Alcohol Use Disorder Conducted by the University of Virginia.”

A Dose-Ranging, Placebo-Controlled, 6-Week Study of Ondansetron in Alcoholic-Dependent Subjects

In 1994, Sellers et al. reported on the effects of administration of 0.25 mg bid ondansetron (N=23), 2 mg bid ondansetron (N=25), or placebo (N=23) for 6 weeks in alcohol-dependent males (Sellers, EM et al., 1994). Endpoints included change in drinks per drinking day (“DDD”) and proportion of responders, where a responder was defined as a subject with a Reliable Change score > 1.96, representing an improvement of at least 2 standard deviations. The Reliable Change score was calculated as the difference between pre- and post-test DDD divided by the standard error. Analyses were conducted comparing pre-treatment with the Week 6 visit, representing the end-of-study medication administration, and pre-treatment with the Week 7 visit, after completion of a 1-week follow-up period.

In the 71 subjects who completed the study, the on-treatment changes in DDD were approximately -1.9 (0.25 mg bid), -1.2 (2 mg bid), and -1.3 (placebo), with neither ondansetron effect being statistically different from the placebo effect. The corresponding changes from pre-treatment to Week 7 (after 6 weeks of treatment and a 1-week follow-up) were approximately -2.7 (0.25 mg bid), -1.1 (2 mg bid), and -1.6 (placebo), with the difference between low-dose ondansetron and placebo approaching statistical significance (p=0.06). By Week 6, nearly twice as many subjects on low-dose ondansetron compared with those on either high-dose ondansetron or placebo showed significant improvement according to the Reliable Change score. Lower baseline drinking and higher level of education were significant predictors of reduction in drinking while on treatment.

14

A Dose-Ranging, Placebo-Controlled, 11-Week Study of Ondansetron in Alcoholic-Dependent Subjects

In 2000, Johnson et al. reported on the co-administration of weekly cognitive behavioral therapy and either placebo or ondansetron at doses of 1, 4, and 16 µg/kg bid for 11 weeks (after a 1-week, single-blind, placebo lead-in) in 321 alcohol-dependent subjects (Johnson, BA et al., 2000). Endpoints included drinks per day, DDD, percentage of days abstinent (“PDA”), total days abstinent, and plasma carbohydrate deficient transferrin (CDT) level, an objective measure of drinking. Analyses were conducted comparing each dose group with placebo, with drinking response variables analyzed as means of data collected from Weeks 3 through 12.

The table below sets forth treatment results. Ondansetron treatment at doses of 1, 4, and 16 µg/kg bid resulted in statistically significant reductions in DDD and drinks per day compared with placebo for EOA (age of onset ≤25 years). The maximum clinical effect was observed at the middle dose (4 µg/kg bid), though the differences between doses were not statistically significant. At 4 µg/kg bid (but not at 1 or 16 µg/kg bid), significant improvements in days and PDA were also achieved. LOA (age of onset ≥26 years) did not benefit from ondansetron treatment at any dose studied.

Treatment Effect Size in EOA Subjects and Statistical Comparison to Placebo Effect

| Variable | 1 µg/kg bid | 4 µg/kg bid | 16 µg/kg bid | ||||||

| Drinks/drinking day | 0.25 (p≤0.05) | 0.41 (p≤0.01) | 0.23 (p≤0.05) | ||||||

| Drinks/day | 0.26 (p≤0.05) | 0.37 (p≤0.01) | 0.22 (p≤0.05) | ||||||

| Days abstinent (%) | 0.13(ns) | 0.26 (p≤0.01) | 0.17(ns) | ||||||

| Days abstinent | 0.06(ns) | 0.24 (p≤0.05) | 0.18(ns) |

The findings in this study support the earlier evidence that the dose-response effect of ondansetron in reduction of alcohol consumption is not linear. Of the doses used in this study, only 4 µg/kg (0.28 mg for a 70 kg person) bid exhibited clinically and statistically meaningful improvements in all efficacy endpoints. This study also suggested that ondansetron may be an appropriate therapy for EOA, but not LOA.

An Open-Label, 8-Week Study Comparing Ondansetron Effect in Early-Onset and Late-Onset Alcoholic Subjects

In 2003, Kranzler et al. reported on the co-administration of weekly cognitive behavioral therapy and ondansetron at 4 µg/kg bid for 8 weeks to 40 alcohol-dependent subjects (Kranzler, HR et al., 2003). The subjects were evenly divided between early-onset alcoholism (EOA; age of onset of the disorder <25 years) and late-onset alcoholism (LOA; age of onset of the disorder ≥25 years). Endpoints included drinks per day, DDD, PDA, Drinker Inventory of Consequences (DrInC) score, and percentage of heavy-drinking days, where heavy drinking was defined as ≥5 drinks in a day for a male subject or ≥4 drinks in a day for a female subject. Analyses were conducted comparing pre-treatment with 8-week values within onset category (EOA or LOA) and comparing treatment effects between categories.

The table below sets forth treatment results. All efficacy parameters improved significantly on treatment in both groups. EOA subjects reported significantly greater improvements in drinks per day, DDD, and DrInC score than LOA subjects. These findings, as noted earlier by Johnson et al., suggest that ondansetron shows promise for treatment of EOA by improving drinking outcomes.

Results of Study Comparing Effects of Ondansetron in EOA versus LOA

| EOA | LOA | EOA v LOA | |||||||||||||

change mean (SD) | p-value | change mean (SD) | p-value | p-value | |||||||||||

| Drinks/drinking day | 5.78 (8.9) | 0.009 | 1.55 (2.0) | 0.004 | 0.032 | ||||||||||

| Drinks/day | 4.53 (4.5) | <0.001 | 1.98 (2.1) | 0.001 | 0.013 | ||||||||||

| Days abstinent (%) | 30.2 (29.4) | <0.001 | 24.8 (21.2) | <0.001 | 0.373 | ||||||||||

| Heavy-drinking days (%) | 35.1 (24.7) | <0.001 | 26.7 (27.4) | <0.001 | 0.139 | ||||||||||

| DrInC total score | 30.3 (27.7) | <0.001 | 11.4 (11.2) | <0.001 | 0.013 | ||||||||||

15

A 3-Period Study of Ondansetron Effect and Sertraline Effect in Subgroups of Alcoholics Constructed Based on Genotypes of the Serotonin Transporter Gene

Constructed Based on Genotypes of the Serotonin Transporter Gene

In 2009, Kenna et al. reported on a placebo-controlled cross-over study in which 21 alcohol-dependent subjects received 0.5 mg/day ondansetron or 200 mg/day sertraline for 3 weeks, placebo for 3 weeks and the alternative active medication for 3 weeks (Kenna, GA et al., 2009). An alcohol self-administration experiment was conducted at the end of each treatment period. The primary endpoint was DDD during the final week of each treatment period.

During the first 3-week treatment period, ondansetron-treated subjects carrying L/L genotype (n = 3), compared to the L/S and S/S carriers (n = 4), had a significantly fewer DDD (3.66 vs. 8.40, p = 0.02). Within L/S and S/S group, there was no significant effect of ondansetron. A pronounced order effect confounded analyses after the third 3-week treatment period.

Our clinical development program is designed to demonstrate the safety and efficacy of ondansetron in the alcohol-dependent population in low dosages for long periods of time, while targeting genotypes that have been shown to benefit from ondansetron treatment. Ultimately, this development program aims to establish a scientific link between the biology of alcohol addiction and the therapeutic mechanism of ondansetron action, permitting genetically-based prediction of ondansetron effectiveness.

Phase 2b Investigator Initiated Clinical Trial of AD04 for Alcohol Use Disorder Conducted by the University of Virginia

In various studies, it has been shown that alcohol dependent individuals with the LL genotype of the 5’-HTT and the TT genotype in the 3’-UTR LL and TT genotype have lower B-CIT neuronal binding to 5-HTT. It is hypothesized that individuals with the LL or TT genotype, 5-HTT gene expression is suppressed by increased alcohol consumption, and therefore, ondansetron, which causes 5-HTT gene expression would have the greatest effect upon individuals that possess both the LL genotype of the 5’-HTT and the TT genotype in the 3’-UTR. A subsequent Phase 2b study (N = 283), conducted by the University of Virginia for which we have acquired rights to the data, showed that a prospectively identified subgroup of alcohol-dependent individuals with these specific polymorphisms of the serotonin transporter protein responded therapeutically to ondansetron administration (Johnson, BA et al., 2011). Further analysis of this same data set against 18 additional polymorphisms located on the genes for the A and B subunits of the serotonin 5-HT3 receptor revealed polymorphisms that were also associated with a therapeutic response to ondansetron. Collectively, the genotypes from the two aforementioned analyses comprise the genotypes selected for testing in Phase 3 trials for AD04. The current ONWARD Phase 3 study is testing ondansetron’s efficacy compared with placebo based on its ability to decrease the frequency and amount of heavy drinking among alcohol dependent individuals with the selected genotypes.

Phase 2b Clinical Trial Study Design

The Phase 2b clinical trial conducted by the University of Virginia was a 283-patient, 12-week, randomized, two-center, parallel-group, placebo-controlled study. Following a 1 week placebo run in (single-blind), alcohol-dependent subjects were randomized to receive either 4 µg/kg ondansetron or placebo, orally, twice daily (double-blind) for 11 additional weeks. In addition to study treatment, all subjects received weekly, standardized, manual-driven, cognitive behavioral therapy.

Eligible subjects were classified to one of twelve groups described by the 2×2 x 3 factorial combinations and randomized to placebo or ondansetron (4 mcg/kg twice daily [b.i.d.]) using a computed blocks randomization procedure that balances the twelve treatment groups on drinks/day ≤ 7.99 vs ≥8.00), age of onset (early vs. late), and genotype (LL, SS, SL).

Genotyping and analysis of the study subjects for the SNP rs1042173 (TT, TG or GG) in the 3´-UTR of the 5-SLC6A4 gene that codes for the serotonin transporter was performed following randomization but prior to database lock. Genotyping and analysis of the study subjects for SNPs located on genes that govern expression of the 5-HT3A and 5-HT3B subunits of the 5-HT3 receptor was performed after database lock.

16

During treatment, subjects were evaluated weekly at the study center for efficacy, safety, and tolerability. Alcohol consumption was collected via the self-reported Timeline Follow-Back (TLFB) method (Sobell and Sobell, Psychosocial & Biochem. Meth., 1992).

Efficacy measures were based on self-reported drinking outcomes with drinks per drinking day (“DDD”), with a standard drink equal to 14 grams of alcohol, and the percentage of days abstinent (“PDA”) being the pre-specified efficacy end points. Withdrawal symptoms, social functioning, and motivation to use alcohol were assessed using standard questionnaires and scales. Subject safety was monitored through periodic electrocardiograms (EKGs), physical exams, safety laboratories and collection of adverse events, concomitant medications, and vital signs. Additionally, a post hoc analysis was conducted using the endpoint of percentage of heavy drinking days (“PDHD”), which is the number of days of heavy drinking days in a month as a percentage of days in the month, because it is widely recognized as a clinically meaningful endpoint and is expected to be an end point in a pivotal/Phase 3 trials. The PDHD end point requires that each day be determined to be a heavy drinking day (e.g., a day in which a female drinks 4 or more drinks or a male drinks 5 or more drinks) or not, making each day binary and requiring an increased sample size to ensure statistical power. Therefore, the goal of the PDHD analysis was to determine if the was a trend toward and effect with PDHD without necessary achieving statistical significance.

The study objectives were to evaluate the safety of AD04 and to test the hypotheses that: (i) ondansetron will have a greater effect of reducing the severity of alcohol drinking and of increasing the percentage of days abstinent among alcohol-dependent subjects with the LL genotype as compared with S carriers (SS or SL) of the 5´-HTTLPR; and (ii) ondansetron’s therapeutic effect will be greatest among alcohol-dependent subjects who possess both the LL genotype of the 5´-HTTLPR and the TT genotype of rs1042173 in the 3´-UTR of the 5´-HTT. After completion of the study, a planned additional analysis of the correlation between genotype and drinking outcomes was conducted considering 18 SNPs located on the 5-HT3A and 5-HT3B subunit genes that were selected based on their minor allele frequency (≥ 0.05) in different ethnic populations, to obtain uniform physical coverage of the two genes, and on results from previous genetic association studies. This latter analysis identified three SNPs as having an apparent beneficial effect.

The primary analytic procedure used mixed-effects linear regression models and a sensitivity analysis using repeated measures models.

Additionally, based on the expectation that subjects with the LL and LL/TT variants of the SLC6A4 gene would respond to ondansetron treatment while others do not, the possibility that SNPs in the 5-HT3A and 5-HT3B subunits of the 5-HT3AB receptor complex may also influence the response to ondansetron was planned as a post hoc analysis. The possible role of SNPs on the HTR3A and HTR3B genes in the response to ondansetron is logical since the 5-HT3A receptor subunit is the primary target for ondansetron’s actions, and the 5-HT3B receptor subunit may be associated with the availability and externalization of the 5-HT3AB receptor complex. Thus, alterations in post-synaptic receptors, such as the 5-HT3AB receptor complex, could have a large impact on signal transduction along post-synaptic neurons. For these analyses, a total of 18 SNPs on the genes for the 5-HT3A and 5-HT3B subunits were examined. SNPs were selected based on their minor allele frequency (≥ 0.05) in different ethnic populations, to obtain uniform physical coverage of the two genes, and on results from previous genetic association studies.

Summary Results — Safety:

Overall, 95% of the subjects in the ondansetron group and 96% in the placebo group reported a treatment-emergent AE (TEAE) during the study. TEAEs occurred most frequently in the SOCs of gastrointestinal disorders (ondansetron 65%, placebo 61%), metabolism and nutritional disorders (38%, 43%), and nervous system disorders (60%, 58%). The incidence of TEAEs by preferred term was similar between the ondansetron and placebo groups. TEAEs that occurred at a frequency ≥ 5% in the ondansetron group compared with the placebo group included constipation (32%, 21%), fatigue (39%, 25%), and dizziness (21%, 12%). There was one death during the study; Subject #218 committed suicide on Study Day 40. The event was considered not related to study drug. Treatment-emergent SAEs were reported in 3 (2.1%) ondansetron-treated subjects and 6 (3.8%) placebo-treated subjects. No SAE was considered related to study drug, and detoxification was the only SAE that was reported for more than 1 subject (2 ondansetron subjects). No clinically meaningful changes in clinical laboratory results, vital sign measurements, ECGs or physical examinations were observed for subjects during the course of the study.

17