QXO BUILDING PRODUCTS, INC. - Annual Report: 2021 (Form 10-K)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES AND EXCHANGE ACT OF 1934

For the Fiscal Year Ended September 30, 2021

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Transition Period from ________ to ________

Commission File Number 000-50924

BEACON ROOFING SUPPLY, INC.

(Exact name of registrant as specified in its charter)

Delaware |

|

36-4173371 |

State or other jurisdiction of incorporation or organization |

|

I.R.S. Employer Identification No. |

505 Huntmar Park Drive, Suite 300, Herndon, VA 20170

Address of Principal Executive Offices, Zip Code

(571) 323-3939

Registrant’s telephone number, including area code

Securities registered pursuant to section 12(b) of the Act:

Title of each class |

Trading Symbol |

Name of each exchange on which registered |

|

|

|

Common Stock, $0.01 par value |

BECN |

NASDAQ Global Select Market |

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities and Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer |

☒ |

Accelerated filer |

☐ |

Emerging growth company |

☐ |

|

|

Non-accelerated filer |

☐ |

Smaller reporting company |

☐ |

|

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the voting common equity held by non-affiliates of the registrant, computed by reference to the closing price at which the common stock was sold as of the end of the second fiscal quarter ended March 31, 2021, was $2.90 billion.

The number of shares of common stock outstanding as of October 31, 2021 was 70,112,948.

DOCUMENTS INCORPORATED BY REFERENCE

The information required by Part III (Items 10, 11, 12, 13 and 14) will be incorporated by reference from the Registrant’s definitive proxy statement for its 2022 Annual Meeting of Stockholders, which will be filed pursuant to Regulation 14A with the United States Securities and Exchange Commission (“SEC”) within 120 days after the end of the fiscal year to which this report relates.

BEACON ROOFING SUPPLY, INC.

Index to Annual Report on Form 10-K

Year Ended September 30, 2021

|

|

Page |

|

4 |

|

Item 1. |

4 |

|

Item 1A. |

9 |

|

Item 1B. |

15 |

|

Item 2. |

15 |

|

Item 3. |

17 |

|

Item 4. |

17 |

|

|

|

|

|

18 |

|

Item 5. |

18 |

|

Item 6. |

18 |

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

19 |

Item 7A. |

31 |

|

Item 8. |

32 |

|

Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

33 |

Item 9A. |

33 |

|

Item 9B. |

35 |

|

Item 9C. |

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections |

35 |

|

|

|

|

36 |

|

|

|

|

|

36 |

|

Item 15. |

36 |

|

Item 16. |

38 |

2

FORWARD-LOOKING STATEMENTS

The matters discussed in this Form 10-K that are forward-looking statements are based on current management expectations that involve substantial risks and uncertainties, which could cause actual results to differ materially from the results expressed in, or implied by, these forward-looking statements. These statements can be identified by the fact that they do not relate strictly to historical or current facts. They use words such as “aim,” “anticipate,” “believe,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “project,” “should,” “will be,” “will continue,” “will likely result,” “would” and other words and terms of similar meaning in conjunction with a discussion of future operating or financial performance. You should read statements that contain these words carefully, because they discuss our future expectations, contain projections of our future results of operations or of our financial position or state other “forward-looking” information.

We believe that it is important to communicate our future expectations to our investors. However, there are events in the future that we are not able to accurately predict or control. The factors listed under Item 1A, Risk Factors, as well as any cautionary language in this Form 10-K, provide examples of risks, uncertainties and events that may cause our actual results to differ materially from the expectations we describe in our forward-looking statements. Although we believe that our expectations are based on reasonable assumptions, actual results may differ materially from those in the forward-looking statements as a result of various factors, including, but not limited to, those described under Item 1A, Risk Factors and elsewhere in this Form 10-K.

Forward-looking statements speak only as of the date of this Form 10-K. Except as required under federal securities laws and the rules and regulations of the SEC, we do not have any intention, and do not undertake, to update any forward-looking statements to reflect events or circumstances arising after the date of this Form 10-K, whether as a result of new information, future events or otherwise. As a result of these risks and uncertainties, readers are cautioned not to place undue reliance on the forward-looking statements included in this Form 10-K or that may be made elsewhere from time to time by or on behalf of us. All forward-looking statements attributable to us are expressly qualified by these cautionary statements.

3

PART I

ITEM 1. BUSINESS

Unless the context suggests otherwise, the terms “Beacon,” the “Company,” “we,” “our” or “us” are referring to Beacon Roofing Supply, Inc.

Overview

Beacon is the largest publicly traded distributor of roofing materials and complementary building products in North America. We have served the building industry for over 90 years and as of September 30, 2021, operated 446 branches throughout all 50 states in the U.S. and six provinces in Canada. We offer an extensive range of high-quality professional grade exterior products comprising over 100,000 SKUs, and we serve over 80,000 residential and non-residential customers who trust us to help them save time, work more efficiently, and enhance their businesses.

We differentiate ourselves in the industry by providing our customers with seamless execution, practical innovation, and a hands-on approach that allows us to serve each of our individual customer’s specific needs. We also work closely with our suppliers, who rely on us to position their products advantageously in the market, supporting advances in products and services that ultimately benefit our customers.

Interior Products Divestiture

On February 10, 2021, we completed the sale of our interior products and insulation businesses (“Interior Products”) to Foundation Building Materials Holding Company LLC (“FBM”) for approximately $850 million in cash (subject to a working capital and certain other adjustments as set forth in the Purchase Agreement). As of September 30, 2021, the adjusted purchase price for Interior Products was $842.7 million. We used the proceeds from the divestiture of our Interior Products business to reduce net debt leverage and strengthen our balance sheet, which provides us the financial flexibility to pursue strategic growth initiatives in our core exterior products business. Beginning with the condensed consolidated financial statements for the three months ended December 31, 2020, we have reflected Interior Products as discontinued operations for all periods presented. Unless otherwise noted, amounts and disclosures relate to our continuing operations. For additional information, see Note 3 in the Notes to Consolidated Financial Statements.

Our Industry

Roofing and complementary product distributors serve the important role of facilitating the supply chain relationships between a small number of manufacturers and thousands of local, regional, and national contractors. Distributors can maintain localized inventories, extend trade credit, give product advice, and provide delivery and logistics services.

The exterior products industry experienced constrained supply chain dynamics in 2021. As a result, we experienced cost increases and, at times, a limited ability to purchase enough product to meet consumer demand. We took proactive measures to actively increase our inventory, price efficiently and deliver high-value solutions to our customers’ critical building material needs. These trends, caused in large part from global disruptions related to the COVID-19 pandemic, may persist in the near-term. As a leading distributor of essential building materials, we will continue to react quickly to market and supply chain developments and ensure high-quality service for our customers.

Market Size

Based on management’s estimates, we believe the roofing distribution market in the United States and Canada represents more than $28 billion in annual sales with roughly 70% of the market in residential roofing and 30% in non-residential. We also distribute complementary building products, including siding, plywood/oriented strand board (OSB), windows and doors, and waterproofing. Collectively, we believe these other building products have an addressable market opportunity nearly as large as our primary roofing distribution business.

Demand Drivers

We believe the majority of roofing demand is driven by re-roofing activity (estimated at 80%) with the remaining demand tied to new construction. Re-roofing projects are typically related to necessary maintenance and repairs and are therefore less likely to be postponed during periods of recession or slower economic growth. As a result, demand for roofing products historically has been less volatile than overall demand for construction products.

Our complementary building products demand comes from both the residential and non-residential sectors. These products allow us to be the supplier of choice to exteriors-focused customers and possess relatively greater end-market exposure to new construction compared to roofing products.

4

In addition to our domestic operations, we also operate in six provinces across Canada. These international locations represented approximately 3.3% of our total net sales for the fiscal year ended September 30, 2021. For further geographic information, see Notes 4 and 15 in the Notes to Consolidated Financial Statements.

Competition

Our competition is primarily composed of national, regional and local specialty roofing distributors and, to a lesser extent, other building supply distributors and big box retailers. Among distributors, we compete against a small number of large distributors and many small, privately-owned distributors. Given significant consolidation in the past decade, Beacon and two other distributors now represent over 50% of the roofing distribution industry in North America. Although we are the largest publicly traded distributor of roofing materials and complementary building products in North America, the industry remains highly competitive. The principal competitive factors in our business include, but are not limited to, the availability of materials and supplies; technical product knowledge and advisory expertise; delivery and other services including digital capabilities; pricing of products; and the availability of credit and capital.

Our Customers

Our mission is to empower our customers to build more for their customers, businesses and communities. Our project lifecycle support helps our customers find projects, land the job, do the work and close it out with guidance that allows them to deliver on project specifications and timelines that are critical to their success. Using an omni-channel approach and our PRO+ digital suite, we differentiate our services and drive customer retention.

Our customer base is composed of professional contractors, home builders, building owners, lumberyards and retailers across the United States and Canada who depend on reliable local access to building products for residential and non-residential projects. Our customers vary in size, ranging from relatively small contractors to large contractors and builders that operate on a national scale. A significant number of our customers have relied on us as their vendor of choice for decades. For the fiscal year ended September 30, 2021, no single customer accounted for more than 1% of our net sales.

Our Strategic Initiatives

Our objective is to be the preferred supplier of exterior building products across markets in the United States and Canada. Our four strategic priorities, as outlined below, are focused on driving top-line growth and bottom-line efficiency. These strategies are central to achieving sales growth, improving operational performance, and increasing profitability. Most importantly, our customers benefit from these initiatives as they are designed to make us more efficient and easier to do business with, differentiating our service from competitors.

Growth

Our history has been strongly influenced by significant acquisition-driven growth, highlighted by the acquisitions of Allied Building Products Corp. (“Allied”) for $2.88 billion in 2018 (the “Allied Acquisition”) and Roofing Supply Group, LLC for $1.17 billion in 2016. These strategic acquisitions expanded our geographic footprint, enhanced our market presence and diversified our product offerings. The scale we have achieved from our expansion efforts serves as a competitive advantage, allowing us to use our assets more efficiently and control our expenses to drive operating leverage.

We have also pursued and finalized numerous smaller acquisitions in key markets to complement the expansion of our geographic footprint, such as our recently announced acquisition of Midway Sales & Distributing, Inc., a leading Midwest distributor of residential and commercial exterior building and roofing supplies with 10 branches across Kansas, Missouri and Nebraska and annual sales of approximately $130 million. We will continue to pursue strategic acquisitions to grow our business, and we remain heavily focused on improving our operations and continuing to identify additional opportunities for organic growth.

To achieve organic growth, we are investing in sales models and channels that add value to our customers. Further development and facilitation of relationships between our local sales teams and contractors give us considerable opportunities to differentiate our service offerings. We are focused on additional training for our sales organization, helping our sales team build on existing customer relationships, leading to higher productivity. In addition, we supplement the sales team’s outreach efforts with branch personnel, digital platform engagement, centralized sales, marketing and pricing support and call center support. Our customer relationship management (CRM) software elevates customer contact efficiency and provides coaching metrics to our sales team, while additional tools and analytics are being employed to enhance the sales team’s pricing proficiency.

We are also pursuing organic growth via new greenfield locations to expand service to customers in key markets. In 2021 we opened three branches in North Port, Florida, Denton, Texas and San Marcos, Texas.

5

Digital

We provide the most complete digital offering in building products distribution and continue to expand our capabilities. Beacon PRO+ is our proprietary digital account management suite which allows customers to manage their business with us online, and Beacon 3D+ is our roofing estimating tool for our residential customers. Our digital platform enables customers to order online from our catalog of over 100,000 products, have 24/7 access to view real-time pricing, process and review the status of orders, track deliveries, monitor local storm activity and vendor promotions, request and approve quotes, and pay their bills online. We are further enhancing PRO+ through partner integrations to help our customers improve estimating, project management and the homeowner experience. Beacon PRO+ provides us with additional opportunities to engage with our customers and helps them save time, work more efficiently, and grow their businesses.

By expanding and promoting our digital solutions, we intend to meet our customers’ changing needs and improve our returns through e-commerce. We will also build strong relationships with suppliers who rely on us to position their products advantageously in the market.

Beacon OTC® Network

Our On Time & Complete (OTC) Network is an operating model in which networked branches share inventory, fleet, equipment, employees and systems for an optimal customer delivery experience. Customers benefit with improved service levels, delivery times and product availability, while we gain efficiencies in staffing, fleet and inventory. We are transitioning to this model in our markets containing an appropriate level of branch density, which we believe will drive shared success for our teams. As of September 30, 2021, our OTC Networks are operational in 58 markets, consisting of over 250 branches.

Branch Performance

We are a learning organization intent on continuous improvement. In particular, we maintain an intensified focus on our branches falling in the bottom quintile of our operating performance metrics in order to determine the appropriate actions to improve the profitability of these locations. Using extensive data from our enterprise resource planning (ERP) system and a regular management reporting cadence, we are able to diagnose issues and make sustainable improvements. We will continue to focus on driving sales and operating improvements to bring these branches up to their potential.

Our Products & Services

Our product lines are designed to meet the requirements of our residential, non-residential and complementary building products customers. We carry one of the most extensive arrays of high-quality branded products in the industry, including our private label brand, TRI-BUILT. Our TRI-BUILT products offer a high-quality and superior-value alternative for our customers while delivering higher margins and brand exclusivity in the marketplace. We fulfill the vast majority of our warehouse orders with inventory on hand because of the breadth and depth of the inventories at our branches.

In the residential market, asphalt shingles comprise the largest share of the products we sell. In the non-residential market, single-ply membranes, insulation, and accessories comprise the largest share of our product offering. In the area of complementary building products, siding, plywood/OSB, windows and doors, and waterproofing comprise the largest share of the products in our portfolio.

During the year ended September 30, 2021, our distribution infrastructure served more than 1.4 million customer deliveries. We maintained a fleet of 1,667 straight trucks, 605 tractors and 893 trailers. Nearly all of our delivery vehicles are equipped with specialized equipment, including 2,225 truck-mounted forklifts, cranes, hydraulic booms and conveyors, which are necessary to deliver products to job sites in an efficient and safe manner and in accordance with our customers’ requirements.

Beyond product delivery, we emphasize superior value-added services to our customers. We employ a knowledgeable sales force that possesses an in-depth understanding of roofing and the building products we provide. Our sales force provides guidance to our customers throughout the lifecycles of their projects, including training, technical support and access to Beacon PRO+ and 3D+, where they can find leads, track storms, order online, track deliveries, view order history, participate in promotions and pay invoices.

Our Supply Chain

We are a key distributor for our suppliers due to our industry expertise, scale, track record of growth, financial strength, and the substantial volume of products that we distribute. We maintain strong relationships with numerous manufacturers of roofing materials and complementary building products in order to reduce the dependence on any single company, maintain purchasing leverage and ensure breadth of product availability. This has been particularly relevant as the building materials industry has experienced constrained supply chain dynamics both domestically and internationally. Our largest suppliers include companies such as Atlas Roofing, Berger

6

Building Products, Carlisle Syntec, CertainTeed Roofing, CertainTeed Siding, Firestone Building Products, GAF, IKO Manufacturing, Johns Manville Roofing, Malarkey, Owens Corning Roofing, Ply Gem, and TAMKO Building Products.

We manage the procurement of products through our national headquarters, regional offices and local branches, allowing us to take advantage of both scale and local market conditions to purchase products more economically than most of our competitors. Product is shipped by the manufacturers either to our branches, our OTC Network hubs, or directly to our customers.

Our Values – Environment, Social and Governance (ESG)

Beacon was founded on a set of principles that have guided our business practices and growth philosophy for over 90 years. Through growth, geographic expansion, and acquisition of building supply brands throughout the United States and Canada, we have sustained a values-based company culture. Our values continue to be the foundation of being a preferred provider for our customers, employees, suppliers and communities.

Environmental

We believe that protection of the environment is important to the long-term success of our business, and we are committed to sustainable business practices. We are continually looking for ways to run our business successfully while safeguarding natural resources for future generations. We also expect our suppliers to preserve natural resources and continuously improve the environmental impact of their products and services as we have expressed in our Supplier Code of Conduct.

We recognize that our greatest impact on the environment is through fleet emissions, and we have committed to using the Beacon OTC® Network strategy to minimize our average gallons of fuel per delivery. OTC focuses on transforming multi-branch markets into a holistic market model that optimizes customer deliveries by shipping from the closest branch to the customer’s delivery address. Further, we continually invest in modernizing our fleet to reduce emissions and improve safety for our drivers. In 2021, we became an EPA SmartWay Partner to benchmark with and learn from companies that have similar large fleets and are seeking to minimize emissions.

Social – Human Capital

We value putting people first and strive to help our employees, customers, and suppliers reach their full potential. We emphasize our core values to all our employees, establishing shared expectations of respect and inclusivity, work ethic, collaboration, and a commitment to deliver quality results.

We are committed to a culture of safety, including a focus on the overall health and wellness of our employees. We maintain a comprehensive safety tracking and companywide scorecard program. We track and closely manage overall workers’ compensation and auto claims, OSHA recordable incidents, lost time rates, Department of Transportation compliance, and other internally established safety prevention elements in an effort to make every workday safe. We conduct new hire and annual training to promote compliance and continuously raise safety awareness. In 2021, we continued to implement COVID-19 protocols across all locations in response to the pandemic to encourage both the safety of our employees and compliance with all federal and local ordinances.

We conduct a comprehensive annual organization and talent review process, culminating with a report to the Board of Directors covering key elements such as: executive succession and development, organizational structure, diversity, talent pipelines and workforce planning requirements. We maintain a broad suite of e-learning courses to deliver new hire, professional development, and annual training on subjects such as management skills, product knowledge, and operational proficiency.

Our Total Rewards program encompasses compensation, benefits and employee development. We track voluntary and involuntary turnover and conduct exit interviews to gain relevant information and adapt our engagement and retention strategy as appropriate.

We are taking steps to expand our role as an employer that champions diversity, inclusion and equality of opportunity. We have a Diversity and Inclusion framework and a companywide council composed of thirteen diverse team members. Julian Francis, our Chief Executive Officer, has signed the CEO Action for Diversity & Inclusion pledge and we have provided e-learning courses on unconscious bias for our branch leaders and corporate staff. In 2021, we took a leadership role in our industry by providing LGBTQ+ introductory training at the National Women in Roofing conference and have partnered with INROADS to provide internships for racially and ethnically diverse students. We measure demographics, including gender and diversity, by business and function and are placing a more targeted focus on our incoming college graduate pipeline and branch operations roles to improve overall representation. In addition, we are a founding sponsor of National Women in Roofing, a volunteer-based organization that supports and advances the careers of women roofing professionals, and in 2021 we inaugurated our North American Female Roofing Professional of the Year contest.

We promote a culture of charitable giving and other community support, highlighted by our annual Beacon of Hope contest that was created to give back to distinguished military veterans by providing roofing replacements or repairs. To date, the contest has helped

7

deliver new or repaired roofs for 32 former service people facing adversity in the years following their military service. In 2021 we launched Beacon CaReS, an employee assistance fund to support team members who are impacted by unexpected financial crisis. The fund is supported by donations from both us and our employees. In addition, an inaugural group of outstanding students whose parents work at Beacon were awarded Robert R. Buck Scholarships totaling $25,000 to pursue post-secondary education.

As of September 30, 2021, we had 6,676 active employees. We have 356 employees that are represented by labor unions and there are no material outstanding labor disputes.

Governance

Our employees, managers and officers conduct our business under the direction of our CEO and the oversight of our Board of Directors (our Board) to enhance our long-term value for our stockholders. The core responsibility of our Board is to exercise its fiduciary duty to act in the best interests of our company and our stockholders. In exercising this obligation, our Board and committees perform a number of specific functions, including risk assessment, review and oversight. While management is responsible for the day-to-day management of risk, our Board retains oversight of risk management for our company as a whole, assisting management by providing guidance on strategic risks, financial risks, and operational risks.

Maintaining our leadership position in the building products distribution industry requires that our information technology deliver against our goal to help our customers build more. Our information security team deploys an array of cybersecurity capabilities to protect our various business systems and data. We continually invest in protecting against, monitoring, and mitigating risks across the enterprise including, as one of our risk mitigation controls, an information security risk insurance policy.

Our information security and privacy policies are in place and regularly updated based on business, compliance, and any other needs. Our Chief Information Officer briefs the Audit Committee of our Board of Directors quarterly regarding information security matters.

We provide new hire and annual security awareness and privacy training to all online employees. In addition, targeted training is conducted for key departments dealing with sensitive data types. Beacon conducts monthly phishing assessment exercises to ensure employees are aware and educated about phishing threats and are trained to identify and report them.

External and internal resources perform assessments and penetration testing throughout the year on Beacon applications, networks, and environments. We perform an annual review to verify our compliance with the Payment Card Industries Data Security Standards (PCI DSS).

In the event of a security issue, we have an incident response plan and trusted experts to quickly triage, contain and understand the issue, as well as protect against it going forward. We had no material publicly reportable information security incidents in the fiscal year ended September 30, 2021.

Government Regulations

We are subject to regulation by various federal, state, provincial and local agencies. These agencies include the Environmental Protection Agency, Department of Transportation, Occupational Safety and Health Administration and Department of Labor and Equal Employment Opportunity Commission. We believe we comply, in all material respects, with applicable statutes and regulations affecting environmental issues and our employment, workplace health and workplace safety practices, and compliance with such statutes and regulations has no material effect on our capital expenditures, earnings or competitive position.

Seasonality and Quarterly Fluctuations

The demand for building materials is closely correlated to both seasonal changes and unpredictable weather patterns, therefore demand fluctuations are expected. In general, sales and net income are highest during our first, third and fourth fiscal quarters, which represent the peak months of construction and re-roofing. We typically experience a build-up of product inventories and increased cash usage in the second and third fiscal quarters of the year in anticipation of the peak selling season, followed by increased accounts receivable, accounts payable, and cash collections during the third and fourth fiscal quarters of the year, when sales volumes are generally at their highest.

At times, we experience fluctuations in our financial performance that are driven by factors outside of our control, including the impact that severe weather events and unusual weather patterns may have on the timing and magnitude of demand and material availability.

The impact of the COVID-19 pandemic has caused and may continue to cause fluctuations in our financial results and working capital that are not aligned with the seasonality we generally experience.

8

Additional Information

Beacon Roofing Supply, Inc. was incorporated in Delaware in 1997. Our principal executive offices are located at 505 Huntmar Park Drive, Suite 300, Herndon, Virginia 20170 and our telephone number is (571) 323-3939. Our Internet website address is www.becn.com.

We maintain an investor relations page on our website where our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, amendments to those reports and other required SEC filings may be accessed free of charge as soon as reasonably practicable after such material is electronically filed with, or furnished to, the SEC.

ITEM 1A. RISK FACTORS

You should carefully consider the risks and uncertainties described below and other information included in this Form 10-K in evaluating us and our business. If any of the events described below occur, our business and financial results could be adversely affected in a material way. This could cause the trading price of our common stock to decline, perhaps significantly.

Risks Related to the COVID-19 Pandemic

The impacts of the COVID-19 pandemic, or similar health concerns, could have a significant effect on supply and/or demand for our products and have a negative impact on our business operations and financial results.

A significant outbreak of epidemic, pandemic, or contagious diseases in the human population, including the COVID‑19 pandemic, could cause a widespread health crisis that could result in an economic downturn, affecting the supply and/or demand for our products. Any quarantines, labor shortages or other disruptions to us, our suppliers, or our customers would likely adversely impact our sales and operating results. A prolonged economic downturn may result in reduced cash flows or a reduction to our market capitalization, triggering the potential need to recognize significant non-cash asset impairment charges in our results of operations. It could also result in an adverse impact on the creditworthiness of our customers and the collectability of trade receivables, thereby affecting our liquidity. In addition, order lead times could be extended or delayed, and pricing could increase. Some products or services may become unavailable if the regional spread became significant enough to prevent alternative sourcing. The increase in remote working arrangements for our personnel may result in greater information technology security risks. We are unable to predict the potential future impact that the COVID‑19 pandemic, or another such virus or health concern, could have on us if the spread is unable to be contained.

The new regulations concerning mandatory COVID-19 vaccination of employees could have a material adverse impact on our business and results of operations.

On November 4, 2021, the Department of Labor's Occupational Safety and Health Administration (“OSHA”) issued emergency regulations requiring all employers with a total of 100 or more employees to develop, implement, and enforce a mandatory COVID-19 vaccination policy, with an exception for employers that instead adopt a policy requiring employees to elect either to get vaccinated or to undergo regular COVID-19 testing. We are currently developing a policy responsive to the new regulations. The validity of the new regulations is being contested in the Federal courts, and OSHA was recently stayed from enforcing them. There can be no assurance the stay will not be lifted or modified pending final adjudication.

We are unable to predict the impact the new regulations would have on us. The new regulations may have the effect of increasing costs, straining company resources, interrupting operations, reducing employee morale, or increasing employee turnover, which could adversely affect our business, results of operations, or financial condition.

Risks Related to Product Supply and Vendor Relations

An inability to obtain the products that we distribute could result in lost revenues and reduced margins and damage relationships with customers.

We distribute roofing and other specialty building materials that are manufactured by a number of major suppliers. Disruptions in our sources of supply may occur as a result of unanticipated demand or production or delivery difficulties. When shortages occur, building material suppliers often allocate products among distributors. Although we believe that our relationships with our suppliers are strong and that we would have access to similar products from competing suppliers should products be unavailable from current sources, any supply shortage, particularly of the most commonly sold items, could result in a loss of revenues and reduced margins and damage relationships with customers.

The exterior products industry experienced constrained supply chain dynamics in 2021, caused in large part from global disruptions related to the COVID-19 pandemic. As a result, we experienced, at times, a limited ability to purchase enough product to meet consumer demand, which resulted in lost revenues. These trends may persist in the near-term. Although we do not believe our lost revenues were material, there can be no assurances that future product shortages will not be so severe as to result in material reductions in revenues.

9

A change in vendor pricing and demand could adversely affect our income and gross margins.

Many of the products that we distribute are subject to price changes based upon manufacturers’ raw material costs and other manufacturer pricing decisions. For example, as a distributor of residential roofing supplies, our business is sensitive to asphalt prices, which are highly volatile and often linked to oil prices, as oil is a significant input in asphalt production. Shingle prices have been volatile in recent years, partly due to volatility in asphalt prices. Other products we distribute, such as plywood and OSB, have seen substantial recent price volatility, caused in large part from disruptions related to the COVID-19 pandemic. Historically, we have generally been able to pass increases in prices on to our customers. Although we often are able to pass on manufacturers’ price increases, our ability to pass on increases in costs and our ability to do so in a timely fashion depends on market conditions. The inability to pass along cost increases or a delay in doing so could result in lower operating margins. In addition, higher prices could impact demand for these products, resulting in lower sales volumes.

A change in vendor rebates could adversely affect our income and gross margins.

The terms on which we purchase products from many of our vendors entitle us to receive a rebate based on the volume of our purchases. These rebates effectively reduce our costs for products. If market conditions change, vendors may adversely change the terms of some or all of these programs. Although these changes would not affect the net recorded costs of product already purchased, it may lower our gross margins on products we sell and therefore the income we realize on such sales in future periods.

Risks Related to Human Capital

Loss of key talent or our inability to attract and retain new qualified talent could hurt our ability to operate and grow successfully.

Our success will continue to depend to a significant extent on our executive officers and key management personnel. We may not be able to retain our executive officers and key personnel or attract additional qualified management. The loss of any of our executive officers or other key management employees, or our inability to recruit and retain qualified employees, could adversely affect our ability to operate and make it difficult to execute our acquisition and internal growth strategies. In addition, our operating results could be adversely affected by increased competition for employees, shortages of qualified workers, or higher employee turnover, all of which could have adverse effects on levels of customer service or result in increased employee compensation or benefit costs.

Risks Related to Acquisitions

We may not be able to effectively integrate newly acquired businesses into our operations or achieve expected cost savings or profitability from our acquisitions.

Our growth strategy includes acquiring other distributors of roofing materials and complementary products. Acquisitions involve numerous risks, including:

As a result, if we fail to evaluate and execute acquisitions properly, we might not achieve the anticipated benefits of such acquisitions and we may incur costs in excess of what we anticipate.

We may not be able to successfully complete acquisitions on acceptable terms, which would slow our growth rate.

We continually seek additional acquisition candidates in selected markets and from time to time engage in exploratory discussions with potential candidates. We are unable to predict whether or when we will be able to identify any suitable additional acquisition candidates, or the likelihood that any potential acquisition will be completed. If we cannot complete acquisitions that we identify on acceptable terms, our growth rate may decline.

Risks Related to Cyclicality and Seasonality

Cyclicality in our business and general economic conditions could result in lower revenues and reduced profitability.

A portion of the products we sell are for residential and non-residential construction. The strength of these markets depends on new housing starts and business investment, which are a function of many factors beyond our control, including credit and capital availability,

10

interest rates, foreclosure rates, housing inventory levels and occupancy, changes in the tax laws, employment levels, consumer confidence and the health of the United States economy and mortgage markets. Economic downturns in the regions and markets we serve could result in lower net sales and, since many of our expenses are fixed, lower profitability. Unfavorable changes in demographics, credit markets, consumer confidence, housing affordability, or housing inventory levels and occupancy, or a weakening of the United States economy or of any regional or local economy in which we operate, could adversely affect consumer spending, resulting in decreased demand for our products, and adversely affecting our business. In addition, instability in the economy and financial markets, including as a result of terrorism or civil or political unrest, may result in a decrease in housing starts or business investment, which would adversely affect our business.

Seasonality and weather-related conditions may have a significant impact on our financial results from period to period

The demand for building materials is heavily correlated to both seasonal changes and unpredictable weather patterns. Seasonal demand fluctuations are expected, such as in our second fiscal quarter, when winter construction cycles and cold weather patterns have an adverse impact on new construction and re-roofing activity. The timing of weather patterns (unseasonable temperatures) and severe weather events (hurricanes, storms and protracted rain) may impact our financial results within a given period either positively or negatively, making it difficult to accurately forecast our results of operations. We expect that these seasonal and weather-related variations will continue in the future.

Risks Related to Information Technology

If we encounter interruptions in the proper functioning of our information technology systems, including from cybersecurity threats, we could experience problems with our operations, including inventory, collections, customer service, cost control and business plan execution that could have a material adverse effect on our financial results, including unanticipated increases in costs or decreases in net sales.

We use our information technology systems (“IT systems” or “systems”), which include information technology networks, hardware and applications, to, among other things, provide complete integration of purchasing, receiving, order processing, shipping, inventory management, sales analysis and accounting, as well as to process, transmit, protect, store and delete sensitive and confidential electronic data, including, but not limited to, employee, supplier and customer data (“Data”). Our IT systems include third party applications and proprietary applications developed and maintained by us. We rely heavily on information technology both in serving our customers and in our enterprise infrastructure to achieve our objectives. In certain instances, we also rely on the systems of third parties to assist with conducting our business, which includes, among other things, marketing and distributing products, developing new products and services, operating our website, hosting and managing our services, securely storing Data, processing transactions, responding to customer inquiries and managing inventory and our supply chain. As a result, the secure operation of our systems (including its function of securing Data), and those of third parties upon whom we depend, are critical to the successful operation of our business.

Although our IT systems and Data are protected through security measures and business continuity plans, our systems and those of third parties upon whom we depend may be vulnerable to: natural disasters; power outages; telecommunication or utility failures; terrorist acts; breaches due to employee error or malfeasance; disruptions during the process of upgrading or replacing computer software or hardware; terminations of business relationships by us or third party service providers; and disinformation campaigns, damage or intrusion from a variety of deliberate cyber-attacks carried out by insiders or third parties, which are becoming more sophisticated and include computer viruses, worms, gaining unauthorized access to systems for purposes of misappropriating assets or sensitive information either directly or through our vendors and customers, denial of service attacks, ransomware, supply chain attacks, data corruption, malicious distribution of inaccurate information or other malicious software programs that may impact such systems and cause operational disruption. For these IT systems and related business processes to operate effectively, we or our service providers must continually maintain and update them. Delays in the maintenance, updates, upgrading, or patching of these systems and related business processes could impair their effectiveness or expose us to security risks. Even with our policies, procedures and programs designed to ensure the integrity of our IT systems and the security of Data, we may not be effective in identifying and mitigating every risk to which we are exposed. In some instances, we may have no current capability to detect certain vulnerabilities, which may allow them to persist in the environment over long periods of time.

Despite the precautions we take to mitigate the risks of such events, any attack on our IT systems or breach of our Data, or the IT systems and Data of third parties upon whom we depend, could result in, but are not limited to, the following: business disruption, misstated or misappropriated financial data, product shortages and/or an increase in accounts receivable aging, an adverse impact on our ability to attract and serve customers, delays in the execution of our business plan, theft of our intellectual property or other non-public confidential information and Data, including that of our customers, suppliers and employees, liability for stolen assets or information, and higher operating costs including increased cybersecurity protection costs. Such events could harm our reputation and have an adverse impact on our financial results, including the impact of related legal, regulatory, and remediation costs. In addition, if any information about our customers, including payment information, were the subject of a successful cybersecurity attack against us, we could be subject to litigation or other claims by the affected customers. Further, regulatory authorities have increased their focus on how companies collect, process, use, store, share, and transmit personal data. New privacy security laws and regulations, including federal and state laws in the

11

U.S. and federal and provincial laws in Canada, pose increasingly complex compliance challenges, which may increase compliance costs, and any failure to comply with data privacy laws and regulations could result in significant sanctions, monetary costs or other harm to us.

If we decide to switch providers, develop our own IT systems to replace providers, or implement upgrades or replacements to our own systems, we may be unsuccessful in this development, or we may underestimate the costs and expenses of switching providers or developing and implementing our own systems. Also, our sales levels may be negatively impacted during the period of implementing an alternative system, which period could extend longer than we anticipate.

Risks Related to Capitalization and Capital Structure

An impairment of goodwill and/or other intangible assets could reduce net income.

Acquisitions frequently result in the recording of goodwill and other intangible assets. At September 30, 2021, goodwill represented approximately 32% of our total assets. Goodwill is not amortized for financial reporting purposes and is subject to impairment testing at least annually using a fair-value based approach. The identification and measurement of goodwill impairment involves the estimation of the fair value of our reporting units. Our accounting for impairment contains uncertainty because management must use judgment in determining appropriate assumptions to be used in the measurement of fair value. We determine the fair values of our reporting units by using a qualitative approach.

We evaluate the recoverability of goodwill for impairment in between our annual tests when events or changes in circumstances, including a sustained decline in our market capitalization, indicate that the carrying amount of goodwill may not be recoverable. We also perform an annual qualitative assessment to evaluate whether evidence exists that would indicate our indefinite-lived intangibles are impaired. In addition, we review for triggering events that could indicate a need for an impairment test for finite-lived intangible assets. Any impairment of goodwill or indefinite- or finite-lived intangibles will reduce net income in the period in which the impairment is recognized.

We might need to raise additional capital, which may not be available, thus limiting our growth prospects.

In the future we may require equity or additional debt financing in order to consummate an acquisition, for additional working capital for expansion, or if we suffer more than seasonally expected losses. In the event such additional financing is unavailable to us on commercially attractive terms or at all (including as a result of restrictions imposed by our outstanding debt agreements and arrangement with the CD&R Stockholder (as defined below)), we may be unable to raise additional capital to make acquisitions or pursue other growth opportunities.

Major disruptions in the capital and credit markets may impact both the availability of credit and business conditions.

If the financial institutions that have extended credit commitments to us are adversely affected by major disruptions in the capital and credit markets, they may become unable to fund borrowings under those credit commitments. This could have an adverse impact on our financial condition since we need to borrow funds at times for working capital, acquisitions, capital expenditures and other corporate purposes.

Major disruptions in the capital and credit markets could also lead to broader economic downturns, which could result in lower demand for our products and increased incidence of customers’ inability to pay their accounts. The majority of our net sales volume is facilitated through the extension of trade credit to our customers. Additional customer bankruptcies or similar events caused by such broader downturns may result in a higher level of bad debt expense than we have historically experienced. Also, our suppliers may be impacted, causing potential disruptions or delays of product availability. These events would adversely impact our results of operations, cash flows and financial position.

Our level and terms of indebtedness could adversely affect our ability to raise additional capital to fund our operations, take advantage of new business opportunities, and prevent us from meeting our obligations under our debt instruments.

As of September 30, 2021, we had $296.6 million in aggregate principal amount of our 4.50% senior secured notes due in 2026 outstanding, $346.2 million in aggregate principal amount of our 4.125% senior notes due in 2029 outstanding, and $981.7 million outstanding under our senior secured term loan due in 2028. Our debt levels could have important consequences to us, including:

12

In addition, the debt agreements that currently govern our asset-based revolving line of credit and term loan and the indentures governing our outstanding senior notes impose significant operating and financial restrictions on us, including limitations on our ability to, among other things, pay dividends and make other distributions on, or redeem or repurchase, capital stock; make certain investments; incur certain liens; enter into transactions with affiliates; merge or consolidate; enter into agreements that restrict the ability of our subsidiaries to make dividends or other payments to Beacon Roofing Supply, Inc.; and transfer or sell assets. In addition, the terms of our preferred stock contain restrictions on our ability to pay dividends on our common stock, and the holders of such shares would participate in any declared common stock dividends, reducing the cash available to holders of common stock. As a result of these restrictions, we will be limited as to how we conduct our business and we may be unable to raise additional debt or equity financing to compete effectively or to capitalize on available business opportunities.

If our cash flows and capital resources are insufficient to fund our debt service obligations, we may be forced to reduce or delay capital expenditures, sell assets, seek additional capital, or restructure or refinance our indebtedness. These alternative measures may not be successful and may not permit us to meet our scheduled debt service obligations, which could cause us to default on our debt obligations and impair our liquidity. In the event of a default under any of our indebtedness, the holders of the defaulted debt could elect to declare all the funds borrowed to be due and payable, together with accrued and unpaid interest, which in turn could result in cross-defaults under our other indebtedness. The lenders under our asset-based revolving line of credit could also elect to terminate their commitments thereunder and cease making further loans, and the lenders under the asset-based revolving line of credit and term loan or holders of our senior secured notes could institute foreclosure proceedings against their collateral, which could potentially force us into bankruptcy or liquidation.

Despite our current level of indebtedness, we may be able to incur substantially more debt and enter into other transactions which could further exacerbate the risks to our financial condition described above.

We may be able to incur significant additional indebtedness in the future. Although the debt agreements that currently govern our asset-based revolving line of credit, term loan, outstanding senior notes and other debt instruments contain restrictions on the incurrence of additional indebtedness and entering into certain types of other transactions, these restrictions are subject to a number of qualifications and exceptions. Additional indebtedness incurred in compliance with these restrictions could be substantial. These restrictions also do not prevent us from incurring obligations, such as trade payables, that do not constitute indebtedness as defined under our debt instruments. To the extent we incur additional indebtedness or other obligations, the risks described in the immediately preceding risk factor and others described herein may increase.

The holders of Preferred Stock issued in connection with the Allied Acquisition have rights, preferences and privileges that are not held by, and are preferential to, the rights of our common stockholders. We may be required, under certain circumstances, to repurchase the preferred stock for cash, and such obligations could adversely affect our liquidity and financial condition.

On January 2, 2018, we issued 400,000 shares of Series A Cumulative Convertible Participating Preferred Stock, par value $0.01 per share (the “Preferred Stock”) to CD&R Boulder Holdings, L.P. (the “CD&R Stockholder”), an entity affiliated with the investment firm Clayton, Dubilier & Rice LLC, pursuant to an Investment Agreement dated August 24, 2017 (the “Investment Agreement”). The proceeds of the issuance were used to partially finance the Allied Acquisition. The Preferred Stock is convertible perpetual participating preferred stock of Beacon, with an initial conversion price of $41.26 per share, and accrues dividends at a rate of 6.0% per annum (payable in cash or in-kind, subject to specified limitations). The Preferred Stock may be converted at any time at the option of the holder into 9,694,619 shares of our common stock. In addition, under the terms of the Preferred Stock, we may, at our option, force the conversion of all (but not less than all) of the outstanding shares of Preferred Stock to common stock if at any time the market price of our common stock exceeds 200% of the then-effective conversion price per share for at least 75 days out of any trailing 90-trading day period. Any conversion of the Preferred Stock may significantly dilute our common stockholders and adversely affect both our net income per share and the market price of our common stock.

13

If we issue additional shares of Preferred Stock as “in-kind” dividend payments that, together with the 400,000 shares of Preferred Stock issued to the CD&R Stockholder, represent in excess of 12,071,937 shares of our common stock on an as-converted basis, and in certain other circumstances as provided in the Preferred Stock certificate of designations, a “Triggering Event” would occur. Upon the occurrence of a “Triggering Event,” the dividend rate will increase to 9.0% per annum for so long as the Triggering Event remains in effect, which will further dilute our common stockholders if we issue additional shares of Preferred Stock to satisfy our dividend payment obligations. Moreover, if we declare or pay a cash dividend on our common stock, we will be required to declare and pay a dividend on the outstanding Preferred Stock on a pro rata basis with the common shares determined on an as-converted basis at the time the dividend is declared. The maximum number of shares of common stock into which the Preferred Stock may be converted (taking into account any shares of Preferred Stock issued as in-kind dividend payments) will be limited to 12,071,937 shares of our common stock, which represents 19.99% of the total number of shares of common stock issued and outstanding immediately prior to the execution of the Investment Agreement, unless and until we were to obtain stockholder approval of such issuance under the Nasdaq listing rules. The terms of the Investment Agreement and Preferred Stock do not require us to obtain stockholder approval in these circumstances.

Holders of the Preferred Stock generally are entitled to vote with the holders of the shares of common stock on an as converted basis on all matters submitted for a vote of holders of shares of common stock, voting together with the holders of shares of common stock as one class (subject to the limitation that any one Preferred Stock holder, together with its affiliates, cannot vote any preferred shares in excess of 19.99% of the aggregate voting power of the common stock outstanding immediately prior to the execution of the Investment Agreement prior to stockholder approval). The prior written consent of the holders of a majority of the Preferred Stock is required to, among other things, (i) amend or modify our charter, by-laws or the certificate of designations governing the Preferred Stock that would adversely affect the Preferred Stock or (ii) amend our debt agreements to, among other things, adversely affect our ability to pay dividends on the Preferred Stock, subject to certain exceptions.

The conversion price of the Preferred Stock is subject to customary anti-dilution adjustments, including in the event of any stock split, stock dividend, recapitalization or similar event. Adjustments to the conversion price could dilute the ownership interest of our common stockholders. In addition, holders of the Preferred Stock have the right to receive a liquidation preference entitling them to be paid out of our assets available for distribution to stockholders, before any payment may be made to holders of shares of common stock, an amount equal to the greater of (a) 100% of the liquidation preference thereof plus all accrued and unpaid dividends or (b) the amount that such holder would have been entitled to receive upon our liquidation, dissolution and winding up if all outstanding shares of Preferred Stock had been converted into common stock immediately prior to such liquidation, dissolution or winding up, without regard to any of the limitations on conversion or convertibility.

Furthermore, the holders of the Preferred Stock will have certain redemption rights, including upon certain change of control events involving us, which, if exercised, could require us to repurchase all of the outstanding Preferred Stock for cash at the original purchase price of the Preferred Stock plus all accrued and unpaid dividends thereon. Our obligations to pay regular dividends to the holders of the Preferred Stock or any required repurchase of the outstanding Preferred Stock could impact our liquidity and reduce the amount of cash available for working capital, capital expenditures, growth opportunities, acquisitions, and other general corporate purposes. Our obligations to the holders of Preferred Stock could also limit our ability to obtain additional financing or increase our borrowing costs, which could have an adverse effect on our financial condition. The preferential rights could also result in divergent interests between the holders of the Preferred Stock and our common stockholders.

The CD&R Stockholder may sell shares of our common stock in the public market, which may cause the market price of our common stock to decrease, and therefore make it more difficult to raise equity financing or issue equity as consideration in an acquisition.

Our registration rights agreement with the CD&R Stockholder requires us to register all shares held by the CD&R Stockholder and its permitted transferees (including shares of our common stock issued upon conversion of Preferred Stock) under the Securities Act upon request of the CD&R Stockholder. The registration rights for the CD&R Stockholder will allow it to sell its shares without compliance with the volume and manner of sale limitations under Rule 144 promulgated under the Securities Act and will facilitate the resale of such securities into the public market. The market value of our common stock could decline as a result of sales by the CD&R Stockholder from time to time. In particular, the sale of a substantial number of our shares by the CD&R Stockholder within a short period of time, or the perception that such sale might occur, could cause our stock price to decrease, make it more difficult for us to raise funds through future offerings of Beacon common stock or acquire other businesses using Beacon common stock as consideration.

The CD&R Stockholder holds a significant equity interest in our business and may exercise significant influence over us, including through the influence of its two directors on our board of directors, and its interests as a preferred equity holder may diverge from, or even conflict with, the interests of our other common stockholders.

As of September 30, 2021, the CD&R Stockholder beneficially owns shares of our common stock and Preferred Stock, which, taken together on an as-converted basis, represent approximately 30.2% of our total voting power. As a result, the CD&R Stockholder may have the indirect ability to significantly influence our policies and operations. In addition, under the Investment Agreement, the CD&R Stockholder is entitled to appoint up to two directors to our board of directors. Both Nathan K. Sleeper and Philip W. Knisely, partners

14

at CD&R, currently serve as directors for the Company. Notwithstanding that all directors are subject to fiduciary duties to us and to applicable law, the interests of the directors designated by the CD&R Stockholder may differ from the interests of our other directors or common stockholders as a whole. With such representation on our board of directors, the CD&R Stockholder has influence over the appointment of management and any action requiring the vote of our board of directors, including significant corporate action such as mergers and sales of substantially all of our assets. The directors controlled by the CD&R Stockholder may also be able to influence decisions affecting our capital structure, including decisions to issue additional capital stock and incur additional debt. Additionally, for so long as the CD&R Stockholder owns Preferred Stock, certain matters will require the approval of the CD&R Stockholder, including: (1) amendments or modifications to our charter, by-laws or the certificate of designations governing the Preferred Stock that would adversely affect the Preferred Stock, (2) authorization, creation, increase in the authorized amount of, or issuance of any class or series of senior or parity equity securities or any security convertible into, shares of senior or parity equity securities (but not junior securities), (3) any increase or decrease in the authorized number of preferred shares or the issuance of additional shares of Preferred Stock, (4) amendments to our debt agreements that would, among other things, adversely affect our ability to pay dividends on the Preferred Stock, subject to certain exceptions, and (5) the liquidation, dissolution or filing of a voluntary petition for bankruptcy or receivership. The CD&R Stockholder and its affiliates are in the business of making or advising on investments in companies, including businesses that may directly or indirectly compete with certain portions of our business. In addition, the CD&R Stockholder may have an interest in pursuing acquisitions, divestitures, financings or other transactions that, in its judgment, could enhance its overall equity investment and have a negative impact to our common stockholders as a whole. Furthermore, the CD&R Stockholder may, in the future, own businesses that directly or indirectly compete with us. The CD&R Stockholder may also pursue acquisition opportunities that may be complementary to our business, and as a result, those acquisition opportunities may not be available to us. The CD&R Stockholder and its affiliates have also made investments in businesses that historically were, and remain, our suppliers and customers, and may in the future invest in businesses that are our suppliers and customers.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

As of September 30, 2021, we leased 428 branch facilities and 8 non-branch facilities throughout the United States and Canada. These leased facilities range in size from approximately 2,000 to 260,000 square feet. In addition, as of September 30, 2021, we owned 18 branch facilities. These owned facilities range in size from approximately 11,500 square feet to 68,000 square feet. We believe that our properties are in good operating condition and adequately serve our current business operations.

15

The following table summarizes the locations of our branches and facilities as of September 30, 2021:

|

|

|

|

|

Non-Branch |

|

||

Location |

|

Branches |

|

|

Facilities |

|

||

U.S. State |

|

|

|

|

|

|

||

Alabama |

|

|

7 |

|

|

|

|

|

Alaska |

|

|

1 |

|

|

|

|

|

Arizona |

|

|

5 |

|

|

|

|

|

Arkansas |

|

|

4 |

|

|

|

|

|

California |

|

|

35 |

|

|

|

|

|

Colorado |

|

|

14 |

|

|

|

|

|

Connecticut |

|

|

5 |

|

|

|

1 |

|

Delaware |

|

|

3 |

|

|

|

|

|

Florida |

|

|

27 |

|

|

|

|

|

Georgia |

|

|

12 |

|

|

|

|

|

Hawaii |

|

|

3 |

|

|

|

|

|

Idaho |

|

|

2 |

|

|

|

|

|

Illinois |

|

|

13 |

|

|

|

|

|

Indiana |

|

|

7 |

|

|

|

|

|

Iowa |

|

|

3 |

|

|

|

|

|

Kansas |

|

|

4 |

|

|

|

|

|

Kentucky |

|

|

5 |

|

|

|

|

|

Louisiana |

|

|

8 |

|

|

|

|

|

Maine |

|

|

4 |

|

|

|

|

|

Maryland |

|

|

17 |

|

|

|

1 |

|

Massachusetts |

|

|

12 |

|

|

|

|

|

Michigan |

|

|

10 |

|

|

|

|

|

Minnesota |

|

|

5 |

|

|

|

1 |

|

Mississippi |

|

|

2 |

|

|

|

|

|

Missouri |

|

|

8 |

|

|

|

|

|

Montana |

|

|

1 |

|

|

|

|

|

Nebraska |

|

|

6 |

|

|

|

|

|

Nevada |

|

|

2 |

|

|

|

|

|

New Hampshire |

|

|

3 |

|

|

|

|

|

New Jersey |

|

|

19 |

|

|

|

1 |

|

New Mexico |

|

|

1 |

|

|

|

|

|

New York |

|

|

16 |

|

|

|

|

|

North Carolina |

|

|

18 |

|

|

|

1 |

|

North Dakota |

|

|

2 |

|

|

|

|

|

Ohio |

|

|

10 |

|

|

|

|

|

Oklahoma |

|

|

2 |

|

|

|

|

|

Oregon |

|

|

7 |

|

|

|

|

|

Pennsylvania |

|

|

31 |

|

|

|

|

|

Rhode Island |

|

|

1 |

|

|

|

|

|

South Carolina |

|

|

9 |

|

|

|

|

|

South Dakota |

|

|

1 |

|

|

|

|

|

Tennessee |

|

|

7 |

|

|

|

|

|

Texas |

|

|

29 |

|

|

|

1 |

|

Utah |

|

|

5 |

|

|

|

|

|

Vermont |

|

|

1 |

|

|

|

|

|

Virginia |

|

|

14 |

|

|

|

1 |

|

Washington |

|

|

16 |

|

|

|

1 |

|

West Virginia |

|

|

4 |

|

|

|

|

|

Wisconsin |

|

|

4 |

|

|

|

|

|

Wyoming |

|

|

2 |

|

|

|

|

|

Total — United States |

|

|

427 |

|

|

|

8 |

|

|

|

|

|

|

|

|

||

Canadian Province |

|

|

|

|

|

|

||

Alberta |

|

|

3 |

|

|

|

|

|

British Columbia |

|

|

3 |

|

|

|

|

|

16

Nova Scotia |

|

|

1 |

|

|

|

|

|

Ontario |

|

|

6 |

|

|

|

|

|

Quebec |

|

|

5 |

|

|

|

|

|

Saskatchewan |

|

|

1 |

|

|

|

|

|

Total — Canada |

|

|

19 |

|

|

|

- |

|

|

|

|

|

|

|

|

||

Total — All |

|

|

446 |

|

|

|

8 |

|

ITEM 3. LEGAL PROCEEDINGS

From time to time, we are involved in lawsuits and other proceedings concerning matters arising from conducting our business, including routine legal proceedings arising in the normal course of business. These proceedings may also include actions brought against us with respect to corporate matters and transactions in which we were involved. There can be no assurance as to the ultimate outcome of a legal proceeding; however, we have generally denied, or believe we have meritorious defenses and will deny, liability in all significant litigation pending against us and intend to vigorously defend each case, other than matters deemed appropriate for settlement. We accrue a liability for legal claims when payments associated with the claims become probable and the costs can be reasonably estimated. The actual costs of resolving legal claims may be substantially higher or lower than the amounts accrued for those claims.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

17

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our common stock trades on the Nasdaq Global Select Market (the “Nasdaq”) under the symbol “BECN”. As of November 8, 2021, there were 64 registered holders of record of our common stock.

We have not paid cash dividends on our common stock and do not anticipate paying dividends in the foreseeable future. Our board of directors currently intends to retain any future earnings for reinvestment in our growing business. Any future determination to pay dividends will also be at the discretion of our board of directors and will be dependent upon our results of operations and cash flows, our financial position and capital requirements, general business conditions, legal, tax, regulatory and any contractual restrictions on the payment of dividends, and any other factors our board of directors deems relevant.

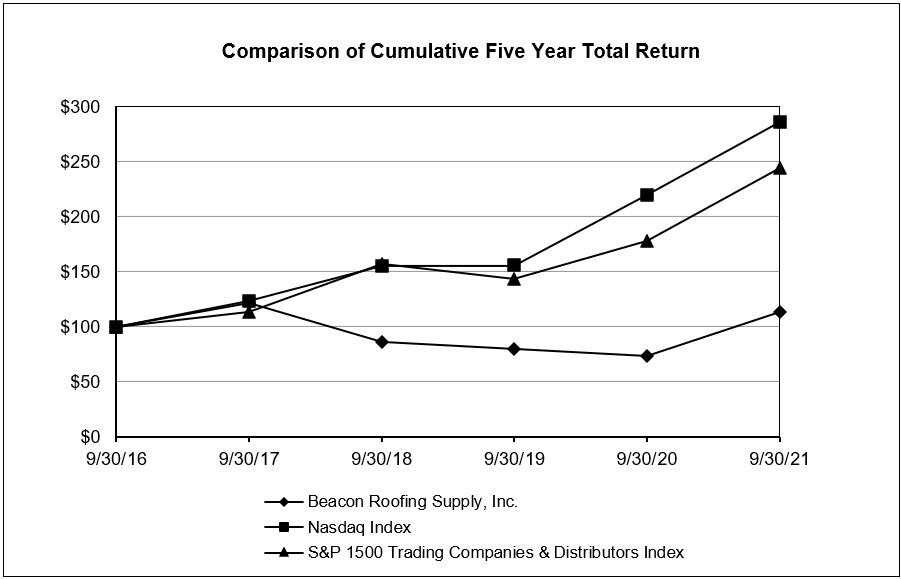

Stock Performance Graph

This stock performance graph shall not be deemed “soliciting material” or to be “filed” with the SEC for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or otherwise subject to the liabilities under that Section, and shall not be deemed to be incorporated by reference into any filing of Beacon Roofing Supply, Inc. under the Securities Act of 1933, as amended, or the Exchange Act. The performance of Beacon Roofing Supply, Inc.’s common stock depicted in the stock performance graph represents historical results only and is not necessarily indicative of future performance.

The following graph compares the cumulative total stockholder return on Beacon Roofing Supply, Inc.’s common stock (based on market prices) for the last five fiscal years with the cumulative total return on (i) the Nasdaq Index and (ii) the S&P 1500 Trading Companies & Distributors Index, assuming a hypothetical $100 investment in each on September 30, 2016 and the re-investment of all dividends. The closing price of our common stock on September 30, 2021, was $47.76.

|

|

Base |

|

INDEXED RETURNS |

|

|||||||||||||||||

|

|

Period |

|

Years Ended September 30, |

|

|||||||||||||||||

Company / Index |

|

9/30/2016 |

|

|

2017 |

|

|

|

2018 |

|

|

|

2019 |

|

|

|

2020 |

|

|

|

2021 |

|

Beacon Roofing Supply, Inc. |

|

100 |

|

|

121.82 |

|

|

|

86.02 |

|

|

|

79.70 |

|

|

|

73.85 |