CLEVELAND-CLIFFS INC. - Quarter Report: 2020 September (Form 10-Q)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||||

For the quarterly period ended September 30, 2020

OR

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||||

For the transition period from to .

Commission File Number: 1-8944

CLEVELAND-CLIFFS INC.

(Exact Name of Registrant as Specified in Its Charter)

| Ohio | 34-1464672 | |||||||||||||||||||

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |||||||||||||||||||

| 200 Public Square, | Cleveland, | Ohio | 44114-2315 | |||||||||||||||||

| (Address of Principal Executive Offices) | (Zip Code) | |||||||||||||||||||

Registrant’s Telephone Number, Including Area Code: (216) 694-5700

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

| Common shares, par value $0.125 per share | CLF | New York Stock Exchange | ||||||||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☒ | Accelerated filer | ☐ | ||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ☐ | ||||||||

| Emerging growth company | ☐ | ||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☒

The number of shares outstanding of the registrant’s common shares, par value $0.125 per share, was 399,241,687 as of October 22, 2020.

TABLE OF CONTENTS

| Page Number | |||||||||||||||||

| DEFINITIONS | |||||||||||||||||

| PART I - FINANCIAL INFORMATION | |||||||||||||||||

| Item 1. | Financial Statements | ||||||||||||||||

| Statements of Unaudited Condensed Consolidated Financial Position as of September 30, 2020 and December 31, 2019 | |||||||||||||||||

| Statements of Unaudited Condensed Consolidated Operations for the Three and Nine Months Ended September 30, 2020 and 2019 | |||||||||||||||||

| Statements of Unaudited Condensed Consolidated Comprehensive Income (Loss) for the Three and Nine Months Ended September 30, 2020 and 2019 | |||||||||||||||||

| Statements of Unaudited Condensed Consolidated Cash Flows for the Nine Months Ended September 30, 2020 and 2019 | |||||||||||||||||

| Statements of Unaudited Condensed Consolidated Changes in Equity for the Three and Nine Months Ended September 30, 2020 and 2019 | |||||||||||||||||

| Notes to Unaudited Condensed Consolidated Financial Statements | |||||||||||||||||

| Item 2. | Management's Discussion and Analysis of Financial Condition and Results of Operations | ||||||||||||||||

| Item 3. | Quantitative and Qualitative Disclosures About Market Risk | ||||||||||||||||

| Item 4. | Controls and Procedures | ||||||||||||||||

| PART II - OTHER INFORMATION | |||||||||||||||||

| Item 1. | Legal Proceedings | ||||||||||||||||

| Item 1A. | Risk Factors | ||||||||||||||||

| Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds | ||||||||||||||||

| Item 4. | Mine Safety Disclosures | ||||||||||||||||

| Item 5. | Other Information | ||||||||||||||||

| Item 6. | Exhibits | ||||||||||||||||

| Signatures | |||||||||||||||||

DEFINITIONS

The following abbreviations or acronyms are used in the text. References in this report to the “Company,” “we,” “us,” “our” and “Cliffs” are to Cleveland-Cliffs Inc. and subsidiaries, collectively, unless stated otherwise or the context indicates otherwise.

| Abbreviation or acronym | Term | |||||||

| ABL Facility | Asset-Based Revolving Credit Agreement, by and among Bank of America, N.A., as Agent, the Lenders that are parties thereto, as the Lenders, and Cleveland-Cliffs Inc., as Parent and a Borrower, dated as of March 13, 2020, as amended | |||||||

| Adjusted EBITDA | EBITDA excluding certain items such as EBITDA of noncontrolling interests, extinguishment of debt, severance, acquisition-related costs, amortization of inventory step-up, impacts of discontinued operations and intersegment corporate allocations of selling, general and administrative costs | |||||||

| AK Coal | AK Coal Resources, Inc., an indirect, wholly owned subsidiary of AK Steel, and related coal mining assets | |||||||

| AK Steel | AK Steel Holding Corporation and its consolidated subsidiaries, including AK Steel Corporation, its direct, wholly owned subsidiary, collectively, unless stated otherwise or the context indicates otherwise | |||||||

| AK Tube | AK Tube LLC, an indirect, wholly owned subsidiary of AK Steel | |||||||

| AMT | Alternative Minimum Tax | |||||||

| AOCI | Accumulated Other Comprehensive Income (Loss) | |||||||

| ArcelorMittal S.A. | ArcelorMittal S.A., an entity formed under the laws of Luxembourg and the ultimate parent entity of ArcelorMittal USA | |||||||

| ArcelorMittal USA | ArcelorMittal USA LLC (including many of its United States affiliates, subsidiaries and representatives. References to ArcelorMittal USA comprise all such relationships unless a specific ArcelorMittal USA entity is referenced) | |||||||

| ASC | Accounting Standards Codification | |||||||

| Atlantic Basin Pellet Premium | Platts Atlantic Basin Blast Furnace 65% Fe pellet premium | |||||||

| Board | The Board of Directors of Cleveland-Cliffs Inc. | |||||||

| CARES Act | Coronavirus Aid, Relief, and Economic Security Act | |||||||

| CERCLA | Comprehensive Environmental Response, Compensation and Liability Act | |||||||

| Compensation Committee | Compensation and Organization Committee of the Board | |||||||

| COVID-19 | A novel strain of coronavirus that the World Health Organization declared a global pandemic in March 2020 | |||||||

| Dodd-Frank Act | Dodd-Frank Wall Street Reform and Consumer Protection Act | |||||||

| DR-grade | Direct Reduction-grade | |||||||

| EAF | Electric Arc Furnace | |||||||

| EBITDA | Earnings before interest, taxes, depreciation and amortization | |||||||

| Empire | Empire Iron Mining Partnership | |||||||

| EPA | U.S. Environmental Protection Agency | |||||||

| ERISA | Employee Retirement Income Security Act of 1974, as amended | |||||||

| Exchange Act | Securities Exchange Act of 1934, as amended | |||||||

| Fe | Iron | |||||||

| FILO | First-in, last-out | |||||||

| Former ABL Facility | Amended and Restated Syndicated Facility Agreement by and among Bank of America, N.A., as Administrative Agent, the Lenders that are parties thereto, as the Lenders, Cleveland-Cliffs Inc., as Parent and a Borrower, and the Subsidiaries of Parent party thereto, as Borrowers, dated as of March 30, 2015, as amended and restated as of February 28, 2018, and as further amended | |||||||

| GAAP | Accounting principles generally accepted in the United States | |||||||

| HBI | Hot Briquetted Iron | |||||||

| Hibbing | Hibbing Taconite Company, an unincorporated joint venture | |||||||

| Hot-rolled coil steel price | Estimated average annual daily market price for hot-rolled coil steel | |||||||

| IRBs | Industrial Revenue Bonds | |||||||

| LIBOR | London Interbank Offered Rate | |||||||

| LIFO | Last-in, first-out | |||||||

| Long ton | 2,240 pounds | |||||||

| Merger | The merger of Merger Sub with and into AK Steel, with AK Steel surviving the merger as a wholly owned subsidiary of Cliffs, subject to the terms and conditions set forth in the Merger Agreement, effective as of March 13, 2020 | |||||||

| Merger Agreement | Agreement and Plan of Merger, dated as of December 2, 2019, among Cliffs, AK Steel and Merger Sub | |||||||

| Merger Sub | Pepper Merger Sub Inc., a direct, wholly owned subsidiary of Cliffs prior to the Merger | |||||||

| Metric ton | 2,205 pounds | |||||||

| MMBtu | Million British Thermal Units | |||||||

| MSHA | U.S. Mine Safety and Health Administration | |||||||

| Net ton | 2,000 pounds | |||||||

| Northshore | Northshore Mining Company | |||||||

| OPEB | Other postretirement benefits | |||||||

| Platts 62% Price | Platts IODEX 62% Fe Fines cost and freight North China | |||||||

| PPI | Producer Price Indices | |||||||

1

| Abbreviation or acronym | Term | |||||||

| Precision Partners | PPHC Holdings, LLC (an indirect, wholly owned subsidiary of AK Steel) and its subsidiaries, collectively, unless stated otherwise or the context indicates otherwise | |||||||

| RCRA | Resource Conservation and Recovery Act | |||||||

| SEC | U.S. Securities and Exchange Commission | |||||||

| Section 232 | Section 232 of the Trade Expansion Act of 1962, as amended | |||||||

| Securities Act | Securities Act of 1933, as amended | |||||||

| SunCoke Middletown | Middletown Coke Company, LLC, a subsidiary of SunCoke Energy, Inc. | |||||||

| Tilden | Tilden Mining Company L.C. | |||||||

| Topic 805 | ASC Topic 805, Business Combinations | |||||||

| Topic 815 | ASC Topic 815, Derivatives and Hedging | |||||||

| Transaction | The purchase of substantially all of the operations of ArcelorMittal USA, subject to the terms and conditions set forth in the Transaction Agreement | |||||||

| Transaction Agreement | Transaction Agreement, by and between Cliffs and ArcelorMittal S.A., dated as of September 28, 2020 | |||||||

| United Taconite | United Taconite LLC | |||||||

| U.S. | United States of America | |||||||

| U.S. Steel | Ontario Hibbing Company, a subsidiary of United States Steel Corporation and a participant in Hibbing | |||||||

| USMCA | United States-Mexico-Canada Agreement | |||||||

| VIE | Variable Interest Entity | |||||||

2

PART I

| Item 1. | Financial Statements | ||||

Statements of Unaudited Condensed Consolidated Financial Position

Cleveland-Cliffs Inc. and Subsidiaries

| (In Millions) | |||||||||||

| September 30, 2020 | December 31, 2019 | ||||||||||

| ASSETS | |||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | 56.0 | $ | 352.6 | |||||||

| Accounts receivable, net | 653.7 | 94.0 | |||||||||

| Inventories | 1,795.1 | 317.4 | |||||||||

| Income tax receivable, current | 9.0 | 58.6 | |||||||||

| Other current assets | 115.0 | 75.3 | |||||||||

| Total current assets | 2,628.8 | 897.9 | |||||||||

| Non-current assets: | |||||||||||

| Property, plant and equipment, net | 4,550.7 | 1,929.0 | |||||||||

| Goodwill | 144.0 | 2.1 | |||||||||

| Intangible assets, net | 190.1 | 48.1 | |||||||||

| Income tax receivable, non-current | — | 62.7 | |||||||||

| Deferred income taxes | 519.5 | 459.5 | |||||||||

| Right-of-use asset, operating lease | 207.7 | 11.7 | |||||||||

| Other non-current assets | 240.1 | 92.8 | |||||||||

| TOTAL ASSETS | $ | 8,480.9 | $ | 3,503.8 | |||||||

| LIABILITIES AND EQUITY | |||||||||||

| Current liabilities: | |||||||||||

| Accounts payable | $ | 710.7 | $ | 193.2 | |||||||

| Accrued liabilities | 279.4 | 126.3 | |||||||||

| Other current liabilities | 224.0 | 89.9 | |||||||||

| Total current liabilities | 1,214.1 | 409.4 | |||||||||

| Non-current liabilities: | |||||||||||

| Long-term debt | 4,309.8 | 2,113.8 | |||||||||

| Operating lease liability, non-current | 174.1 | 10.5 | |||||||||

| Intangible liabilities, net | 65.9 | — | |||||||||

| Pension and OPEB liabilities | 1,130.6 | 311.5 | |||||||||

| Asset retirement obligations | 182.0 | 163.2 | |||||||||

| Other non-current liabilities | 280.7 | 137.5 | |||||||||

| TOTAL LIABILITIES | 7,357.2 | 3,145.9 | |||||||||

| Commitments and contingencies (See Note 18) | |||||||||||

| Equity: | |||||||||||

Common shares - par value $0.125 per share | |||||||||||

Authorized - 600,000,000 shares (2019 - 600,000,000 shares); | |||||||||||

Issued - 428,645,866 shares (2019 - 301,886,794 shares); | |||||||||||

Outstanding - 399,229,917 shares (2019 - 270,084,005 shares) | 53.6 | 37.7 | |||||||||

| Capital in excess of par value of shares | 4,446.3 | 3,872.1 | |||||||||

| Retained deficit | (3,052.5) | (2,842.4) | |||||||||

Cost of 29,415,949 common shares in treasury (2019 - 31,802,789 shares) | (354.8) | (390.7) | |||||||||

| Accumulated other comprehensive loss | (282.0) | (318.8) | |||||||||

| Total Cliffs shareholders' equity | 810.6 | 357.9 | |||||||||

| Noncontrolling interest | 313.1 | — | |||||||||

| TOTAL EQUITY | 1,123.7 | 357.9 | |||||||||

| TOTAL LIABILITIES AND EQUITY | $ | 8,480.9 | $ | 3,503.8 | |||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

3

Statements of Unaudited Condensed Consolidated Operations

Cleveland-Cliffs Inc. and Subsidiaries

| (In Millions, Except Per Share Amounts) | |||||||||||||||||||||||

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | ||||||||||||||||||||

| Revenues | $ | 1,646.0 | $ | 555.6 | $ | 3,063.2 | $ | 1,455.8 | |||||||||||||||

| Realization of deferred revenue | — | — | 34.6 | — | |||||||||||||||||||

| Operating costs: | |||||||||||||||||||||||

| Cost of goods sold | (1,525.4) | (400.7) | (3,088.9) | (1,007.0) | |||||||||||||||||||

| Selling, general and administrative expenses | (59.6) | (25.5) | (149.2) | (82.2) | |||||||||||||||||||

| Acquisition-related costs | (7.5) | — | (68.4) | — | |||||||||||||||||||

| Miscellaneous – net | (15.5) | (7.8) | (40.5) | (19.0) | |||||||||||||||||||

| Total operating costs | (1,608.0) | (434.0) | (3,347.0) | (1,108.2) | |||||||||||||||||||

| Operating income (loss) | 38.0 | 121.6 | (249.2) | 347.6 | |||||||||||||||||||

| Other income (expense): | |||||||||||||||||||||||

| Interest expense, net | (68.2) | (25.3) | (167.9) | (76.5) | |||||||||||||||||||

| Gain (loss) on extinguishment of debt | — | — | 132.6 | (18.2) | |||||||||||||||||||

| Other non-operating income | 10.0 | 0.3 | 31.2 | 1.3 | |||||||||||||||||||

| Total other expense | (58.2) | (25.0) | (4.1) | (93.4) | |||||||||||||||||||

| Income (loss) from continuing operations before income taxes | (20.2) | 96.6 | (253.3) | 254.2 | |||||||||||||||||||

| Income tax benefit (expense) | 22.4 | (4.8) | 98.5 | (23.1) | |||||||||||||||||||

| Income (loss) from continuing operations | 2.2 | 91.8 | (154.8) | 231.1 | |||||||||||||||||||

| Loss from discontinued operations, net of tax | (0.3) | (0.9) | — | (1.5) | |||||||||||||||||||

| Net income (loss) | 1.9 | 90.9 | (154.8) | 229.6 | |||||||||||||||||||

| Income attributable to noncontrolling interest | (11.9) | — | (31.2) | — | |||||||||||||||||||

| Net income (loss) attributable to Cliffs shareholders | $ | (10.0) | $ | 90.9 | $ | (186.0) | $ | 229.6 | |||||||||||||||

| Earnings (loss) per common share attributable to Cliffs shareholders - basic | |||||||||||||||||||||||

| Continuing operations | $ | (0.02) | $ | 0.34 | $ | (0.51) | $ | 0.83 | |||||||||||||||

| Discontinued operations | — | — | — | (0.01) | |||||||||||||||||||

| $ | (0.02) | $ | 0.34 | $ | (0.51) | $ | 0.82 | ||||||||||||||||

| Earnings (loss) per common share attributable to Cliffs shareholders - diluted | |||||||||||||||||||||||

| Continuing operations | $ | (0.02) | $ | 0.33 | $ | (0.51) | $ | 0.80 | |||||||||||||||

| Discontinued operations | — | — | — | — | |||||||||||||||||||

| $ | (0.02) | $ | 0.33 | $ | (0.51) | $ | 0.80 | ||||||||||||||||

| Average number of shares (in thousands) | |||||||||||||||||||||||

| Basic | 399,399 | 269,960 | 365,245 | 278,418 | |||||||||||||||||||

| Diluted | 399,399 | 276,578 | 365,245 | 287,755 | |||||||||||||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

4

Statements of Unaudited Condensed Consolidated Comprehensive Income (Loss)

Cleveland-Cliffs Inc. and Subsidiaries

| (In Millions) | |||||||||||||||||||||||

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | ||||||||||||||||||||

| Net income (loss) | $ | 1.9 | $ | 90.9 | $ | (154.8) | $ | 229.6 | |||||||||||||||

| Other comprehensive income: | |||||||||||||||||||||||

| Changes in pension and OPEB, net of tax | 6.6 | 5.8 | 18.2 | 17.3 | |||||||||||||||||||

| Changes in foreign currency translation | 1.6 | — | 1.4 | — | |||||||||||||||||||

| Changes in derivative financial instruments, net of tax | 15.7 | 0.4 | 17.2 | 1.0 | |||||||||||||||||||

| Total other comprehensive income | 23.9 | 6.2 | 36.8 | 18.3 | |||||||||||||||||||

| Comprehensive income (loss) | 25.8 | 97.1 | (118.0) | 247.9 | |||||||||||||||||||

| Comprehensive income attributable to noncontrolling interests | (11.9) | — | (31.2) | — | |||||||||||||||||||

| Comprehensive income (loss) attributable to Cliffs shareholders | $ | 13.9 | $ | 97.1 | $ | (149.2) | $ | 247.9 | |||||||||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

5

Statements of Unaudited Condensed Consolidated Cash Flows

Cleveland-Cliffs Inc. and Subsidiaries

| (In Millions) | |||||||||||

| Nine Months Ended September 30, | |||||||||||

| 2020 | 2019 | ||||||||||

| OPERATING ACTIVITIES | |||||||||||

| Net income (loss) | $ | (154.8) | $ | 229.6 | |||||||

| Adjustments to reconcile net income (loss) to net cash provided (used) by operating activities: | |||||||||||

| Depreciation, depletion and amortization | 183.9 | 63.1 | |||||||||

| Amortization of inventory step-up | 74.0 | — | |||||||||

| Deferred income taxes | (89.9) | 22.7 | |||||||||

| Loss (gain) on extinguishment of debt | (132.6) | 18.2 | |||||||||

| Loss (gain) on derivatives | (19.1) | 48.4 | |||||||||

| Other | (13.0) | 49.4 | |||||||||

| Changes in operating assets and liabilities, net of business combination: | |||||||||||

| Receivables and other assets | 259.8 | 174.1 | |||||||||

| Inventories | (4.2) | (147.0) | |||||||||

| Payables, accrued expenses and other liabilities | (157.3) | (70.4) | |||||||||

| Net cash provided (used) by operating activities | (53.2) | 388.1 | |||||||||

| INVESTING ACTIVITIES | |||||||||||

| Purchase of property, plant and equipment | (378.9) | (460.7) | |||||||||

| Acquisition of AK Steel, net of cash acquired | (869.3) | — | |||||||||

| Other investing activities | 8.0 | 11.2 | |||||||||

| Net cash used by investing activities | (1,240.2) | (449.5) | |||||||||

| FINANCING ACTIVITIES | |||||||||||

| Repurchase of common shares | — | (252.9) | |||||||||

| Proceeds from issuance of debt | 1,762.9 | 720.9 | |||||||||

| Debt issuance costs | (57.5) | (6.8) | |||||||||

| Repurchase of debt | (999.5) | (729.3) | |||||||||

| Borrowings under credit facilities | 800.0 | — | |||||||||

| Repayments under credit facilities | (400.0) | — | |||||||||

| Dividends paid | (40.8) | (45.1) | |||||||||

| SunCoke Middletown distributions to noncontrolling interest owners | (47.6) | — | |||||||||

| Other financing activities | (23.3) | (53.7) | |||||||||

| Net cash provided (used) by financing activities | 994.2 | (366.9) | |||||||||

| Decrease in cash and cash equivalents, including cash classified within other current assets related to discontinued operations | (299.2) | (428.3) | |||||||||

| Less: decrease in cash and cash equivalents from discontinued operations, classified within other current assets | (2.6) | (4.4) | |||||||||

| Net decrease in cash and cash equivalents | (296.6) | (423.9) | |||||||||

| Cash and cash equivalents at beginning of period | 352.6 | 823.2 | |||||||||

| Cash and cash equivalents at end of period | $ | 56.0 | $ | 399.3 | |||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

6

Statements of Unaudited Condensed Consolidated Changes in Equity

Cleveland-Cliffs Inc. and Subsidiaries

| (In Millions) | |||||||||||||||||||||||||||||||||||||||||||||||

| Number of Common Shares Outstanding | Par Value of Common Shares Issued | Capital in Excess of Par Value of Shares | Retained Deficit | Common Shares in Treasury | AOCI | Non-controlling Interests | Total | ||||||||||||||||||||||||||||||||||||||||

| December 31, 2019 | 270.1 | $ | 37.7 | $ | 3,872.1 | $ | (2,842.4) | $ | (390.7) | $ | (318.8) | $ | — | $ | 357.9 | ||||||||||||||||||||||||||||||||

| Comprehensive income (loss) | — | — | — | (52.1) | — | 1.7 | 3.5 | (46.9) | |||||||||||||||||||||||||||||||||||||||

| Stock and other incentive plans | 1.7 | — | (23.6) | — | 25.7 | — | — | 2.1 | |||||||||||||||||||||||||||||||||||||||

| Acquisition of AK Steel | 126.8 | 15.9 | 601.7 | — | — | — | 329.8 | 947.4 | |||||||||||||||||||||||||||||||||||||||

Common share dividends ($0.06 per share) | — | — | — | (24.0) | — | — | — | (24.0) | |||||||||||||||||||||||||||||||||||||||

| Net distributions to noncontrolling interests | — | — | — | — | — | — | (5.5) | (5.5) | |||||||||||||||||||||||||||||||||||||||

| March 31, 2020 | 398.6 | $ | 53.6 | $ | 4,450.2 | $ | (2,918.5) | $ | (365.0) | $ | (317.1) | $ | 327.8 | $ | 1,231.0 | ||||||||||||||||||||||||||||||||

| Comprehensive income (loss) | — | — | — | (123.9) | — | 11.2 | 15.8 | (96.9) | |||||||||||||||||||||||||||||||||||||||

| Stock and other incentive plans | 0.6 | — | (6.6) | — | 9.1 | — | — | 2.5 | |||||||||||||||||||||||||||||||||||||||

| Common share dividends | — | — | — | (0.1) | — | — | — | (0.1) | |||||||||||||||||||||||||||||||||||||||

| Net distributions to noncontrolling interests | — | — | — | — | — | — | (18.3) | (18.3) | |||||||||||||||||||||||||||||||||||||||

| June 30, 2020 | 399.2 | $ | 53.6 | $ | 4,443.6 | $ | (3,042.5) | $ | (355.9) | $ | (305.9) | $ | 325.3 | $ | 1,118.2 | ||||||||||||||||||||||||||||||||

| Comprehensive income (loss) | — | — | — | (10.0) | — | 23.9 | 11.9 | 25.8 | |||||||||||||||||||||||||||||||||||||||

| Stock and other incentive plans | — | — | 2.7 | — | 1.1 | — | — | 3.8 | |||||||||||||||||||||||||||||||||||||||

| Net distributions to noncontrolling interests | — | — | — | — | — | — | (24.1) | (24.1) | |||||||||||||||||||||||||||||||||||||||

| September 30, 2020 | 399.2 | $ | 53.6 | $ | 4,446.3 | $ | (3,052.5) | $ | (354.8) | $ | (282.0) | $ | 313.1 | $ | 1,123.7 | ||||||||||||||||||||||||||||||||

| (In Millions) | |||||||||||||||||||||||||||||||||||||||||

| Number of Common Shares Outstanding | Par Value of Common Shares Issued | Capital in Excess of Par Value of Shares | Retained Deficit | Common Shares in Treasury | AOCI | Total | |||||||||||||||||||||||||||||||||||

| December 31, 2018 | 292.6 | $ | 37.7 | $ | 3,916.7 | $ | (3,060.2) | $ | (186.1) | $ | (283.9) | $ | 424.2 | ||||||||||||||||||||||||||||

| Comprehensive income (loss) | — | — | — | (22.1) | — | 8.4 | (13.7) | ||||||||||||||||||||||||||||||||||

| Stock and other incentive plans | 1.7 | — | (56.5) | — | 46.5 | — | (10.0) | ||||||||||||||||||||||||||||||||||

| Common share repurchases | (11.5) | — | — | — | (124.3) | — | (124.3) | ||||||||||||||||||||||||||||||||||

Common share dividends ($0.05 per share) | — | — | — | (14.5) | — | — | (14.5) | ||||||||||||||||||||||||||||||||||

| March 31, 2019 | 282.8 | $ | 37.7 | $ | 3,860.2 | $ | (3,096.8) | $ | (263.9) | $ | (275.5) | $ | 261.7 | ||||||||||||||||||||||||||||

| Comprehensive income | — | — | — | 160.8 | — | 3.7 | 164.5 | ||||||||||||||||||||||||||||||||||

| Stock and other incentive plans | 0.1 | — | 3.4 | — | 1.2 | — | 4.6 | ||||||||||||||||||||||||||||||||||

| Common share repurchases | (12.9) | — | — | — | (128.6) | — | (128.6) | ||||||||||||||||||||||||||||||||||

Common share dividends ($0.06 per share) | — | — | — | (16.6) | — | — | (16.6) | ||||||||||||||||||||||||||||||||||

| June 30, 2019 | 270.0 | $ | 37.7 | $ | 3,863.6 | $ | (2,952.6) | $ | (391.3) | $ | (271.8) | $ | 285.6 | ||||||||||||||||||||||||||||

| Comprehensive income | — | — | — | 90.9 | — | 6.2 | 97.1 | ||||||||||||||||||||||||||||||||||

| Stock and other incentive plans | 0.1 | — | 4.1 | — | 0.4 | — | 4.5 | ||||||||||||||||||||||||||||||||||

Common share dividends ($0.10 per share) | — | — | — | (27.3) | — | — | (27.3) | ||||||||||||||||||||||||||||||||||

| September 30, 2019 | 270.1 | $ | 37.7 | $ | 3,867.7 | $ | (2,889.0) | $ | (390.9) | $ | (265.6) | $ | 359.9 | ||||||||||||||||||||||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

7

Notes to Unaudited Condensed Consolidated Financial Statements

Cleveland-Cliffs Inc. and Subsidiaries

NOTE 1 - BASIS OF PRESENTATION AND SIGNIFICANT ACCOUNTING POLICIES

Business, Consolidation and Presentation

The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with SEC rules and regulations and, in the opinion of management, include all adjustments (consisting of normal recurring adjustments) necessary to present fairly the financial position, results of operations, comprehensive income (loss), cash flows and changes in equity for the periods presented. The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the amounts reported in the financial statements and accompanying notes. Management bases its estimates on various assumptions and historical experience, which are believed to be reasonable; however, due to the inherent nature of estimates, actual results may differ significantly due to changed conditions or assumptions. The results of operations for the three and nine months ended September 30, 2020 are not necessarily indicative of results to be expected for the year ending December 31, 2020 or any other future period. Due to the acquisition of AK Steel, certain balances have become material and are no longer being condensed in our Statements of Unaudited Condensed Consolidated Financial Position, such as balances for Right-of-use asset, operating lease and Operating lease liability, non-current. As a result, certain prior period amounts have been reclassified to conform with the current year presentation. These unaudited condensed consolidated financial statements should be read in conjunction with the financial statements and notes included in our Annual Report on Form 10-K for the year ended December 31, 2019 and in our Quarterly Reports on Form 10-Q for the quarterly periods ended March 31, 2020 and June 30, 2020.

Proposed acquisition of substantially all of the operations of ArcelorMittal USA

On September 28, 2020, we entered into a Transaction Agreement with ArcelorMittal S.A., pursuant to which Cliffs will acquire substantially all of the operations of ArcelorMittal USA for an aggregate purchase price of approximately $1.4 billion, consisting of (i) $505 million in cash, (ii) 78,186,671 of our common shares, par value $0.125 per share, and (iii) 583,273 shares of a new series of our Serial Preferred Stock, Class B, without par value, to be designated as the “Series B Participating Redeemable Preferred Stock” at closing. The cash portion of the purchase price is subject to customary working capital and purchase price adjustments.

We expect to complete the Transaction in the fourth quarter of 2020. Completion of the Transaction is subject to various customary closing conditions, including the receipt of required regulatory approvals in identified jurisdictions, including the expiration or termination of the waiting period under the Hart-Scott-Rodino Act, and it is possible that factors outside of our control could result in the Transaction being completed at a later time or not at all. The Transaction Agreement also contains certain termination rights that may be exercised by either us or ArcelorMittal S.A. We plan to complete the Transaction as soon as reasonably practicable following the satisfaction or waiver of all applicable conditions.

Acquisition of AK Steel

On March 13, 2020, we consummated the Merger, pursuant to which, upon the terms and subject to the conditions set forth in the Merger Agreement, Merger Sub was merged with and into AK Steel, with AK Steel surviving the Merger as a wholly owned subsidiary of Cliffs. Refer to NOTE 3 - ACQUISITION OF AK STEEL for further information.

AK Steel is a leading North American producer of flat-rolled carbon, stainless and electrical steel products, primarily for the automotive, infrastructure and manufacturing markets. The acquisition of AK Steel has transformed us into a vertically integrated producer of value-added iron ore and steel products.

COVID-19

In response to the COVID-19 pandemic, we made various operational changes to adjust to the demand for our products. Although steel and iron ore production have been considered “essential” by the states in which we operate, certain of our facilities and construction activities were temporarily idled during the second quarter of 2020. Most of these temporarily idled facilities were restarted during the second quarter, and the remaining operations were restarted during the third quarter.

8

Basis of Consolidation

The unaudited condensed consolidated financial statements consolidate our accounts and the accounts of our wholly owned subsidiaries, all subsidiaries in which we have a controlling interest and two variable interest entities for which we are the primary beneficiary. All intercompany transactions and balances are eliminated upon consolidation.

Reportable Segments

The acquisition of AK Steel has transformed us into a vertically integrated producer of value-added iron ore and steel products and we are organized according to our differentiated products in two reportable segments - the Steel and Manufacturing segment and the Mining and Pelletizing segment. Our new Steel and Manufacturing segment includes the assets acquired through the acquisition of AK Steel and our previously reported Metallics segment, and our Mining and Pelletizing segment includes our three active operating mines and our indefinitely idled mine.

Investments in Affiliates

We have investments in several businesses accounted for using the equity method of accounting. We review an investment for impairment when circumstances indicate that a loss in value below its carrying amount is other than temporary. Investees and equity ownership percentages are presented below:

| Investee | Segment Reported Within | Equity Ownership Percentage | ||||||||||||

| Combined Metals of Chicago, LLC | Steel and Manufacturing | 40.0% | ||||||||||||

| Hibbing Taconite Company | Mining and Pelletizing | 23.0% | ||||||||||||

| Spartan Steel Coating, LLC | Steel and Manufacturing | 48.0% | ||||||||||||

We recorded a basis difference for Spartan Steel of $32.5 million as part of our acquisition of AK Steel. The basis difference relates to the excess of the fair value over the investee's carrying amount of property, plant and equipment and will be amortized over the remaining useful lives of the underlying assets.

Significant Accounting Policies

A detailed description of our significant accounting policies can be found in the audited financial statements included in our Annual Report on Form 10-K for the year ended December 31, 2019 filed with the SEC, which were updated and can be found in the unaudited condensed consolidated financial statements included in our Quarterly Reports on Form 10-Q for the quarterly periods ended March 31, 2020 and June 30, 2020 filed with the SEC. There have been no material changes in our significant accounting policies and estimates from those disclosed therein.

Recent Accounting Pronouncements

Issued and Adopted

On March 2, 2020, the SEC issued a final rule that amended the disclosure requirements related to certain registered securities under SEC Regulation S-X, Rule 3-10, which required separate financial statements for subsidiary issuers and guarantors of registered debt securities unless certain exceptions are met. The final rule replaces the previous requirement under Rule 3-10 to provide condensed consolidating financial information in the registrant’s financial statements with a requirement to provide alternative financial disclosures (which include summarized financial information of the parent and any issuers and guarantors, as well as other qualitative disclosures) in either the registrant’s Management's Discussion and Analysis of Financial Condition and Results of Operations or its financial statements, in addition to other simplifications. The final rule is effective for filings on or after January 4, 2021, and early adoption is permitted. We elected to early adopt this disclosure update for the period ended March 31, 2020. As a result, we have excluded the footnote disclosures required under the previous Rule 3-10, and applied the final rule by including the summarized financial information and qualitative disclosures in Part I - Item 2. Management's Discussion and Analysis of Financial Condition and Results of Operations of this Quarterly Report on Form 10-Q and Exhibit 22.1, hereto.

9

Issued and Not Effective

In August 2020, the Financial Accounting Standards Board issued Accounting Standards Update No. 2020-06, Debt—Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging—Contracts in Entity’s Own Equity (Subtopic 815-40). This update requires certain convertible instruments to be accounted for as a single liability measured at its amortized cost. Additionally, the update requires the use of the "if-converted" method, removing the treasury stock method, when calculating diluted shares. The two methods of adoption are the full and modified retrospective approaches. We expect to utilize the modified retrospective approach. Using this approach, the guidance shall be applied to transactions outstanding as of the beginning of the fiscal year in which the amendment is adopted. The final rule is effective for fiscal years beginning after December 15, 2021. Early adoption is permitted for fiscal years beginning after December 15, 2020, including interim periods within those fiscal years. We are continuing to evaluate the impact of this update to our financials and would expect to adopt at the required adoption date of January 1, 2022.

NOTE 2 - SUPPLEMENTARY FINANCIAL STATEMENT INFORMATION

Revenues

The following table represents our consolidated Revenues (excluding intercompany revenues) by market:

| (In Millions) | |||||||||||||||||||||||

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | ||||||||||||||||||||

| Steel and Manufacturing: | |||||||||||||||||||||||

| Automotive | $ | 920.0 | $ | — | $ | 1,404.0 | $ | — | |||||||||||||||

| Infrastructure and manufacturing | 198.8 | — | 446.2 | — | |||||||||||||||||||

| Distributors and converters | 142.9 | — | 344.1 | — | |||||||||||||||||||

| Total Steel and Manufacturing | 1,261.7 | — | 2,194.3 | — | |||||||||||||||||||

| Mining and Pelletizing: | |||||||||||||||||||||||

Steel producers1 | 384.3 | 555.6 | 903.5 | 1,455.8 | |||||||||||||||||||

| Total revenues | $ | 1,646.0 | $ | 555.6 | $ | 3,097.8 | $ | 1,455.8 | |||||||||||||||

1 Includes Realization of deferred revenue of $34.6 million for the nine months ended September 30, 2020. | |||||||||||||||||||||||

The following table represents our consolidated Revenues (excluding intercompany revenues) by product line:

| (In Millions) | |||||||||||||||||||||||

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | ||||||||||||||||||||

| Steel and Manufacturing: | |||||||||||||||||||||||

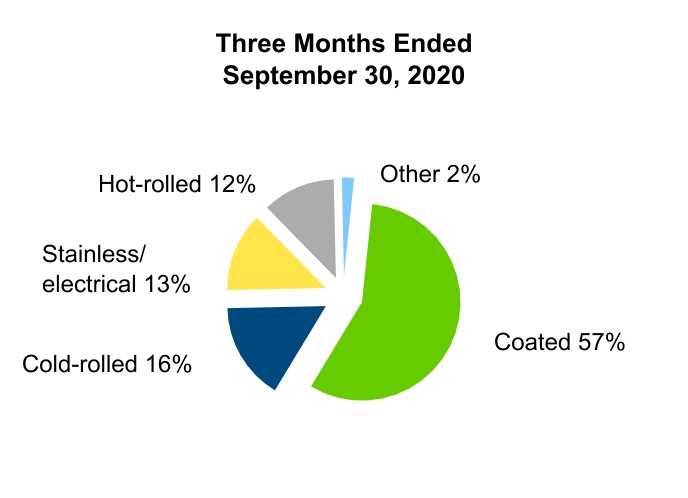

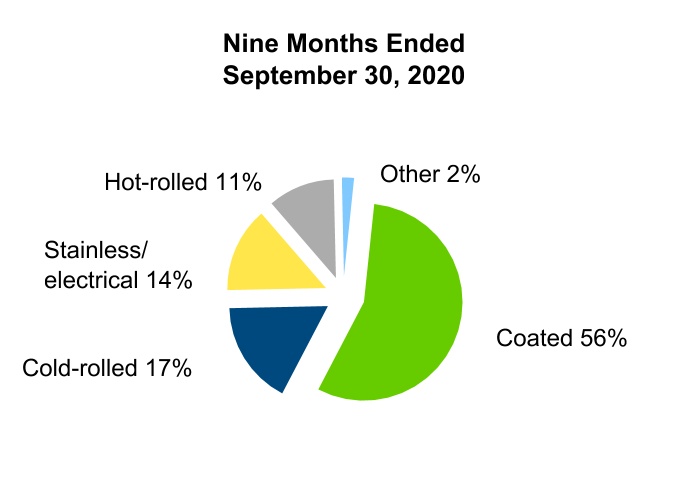

| Carbon steel | $ | 821.2 | $ | — | $ | 1,391.6 | $ | — | |||||||||||||||

| Stainless and electrical steel | 303.2 | — | 585.1 | — | |||||||||||||||||||

| Tubular products, components and other | 137.3 | — | 217.6 | — | |||||||||||||||||||

| Total Steel and Manufacturing | 1,261.7 | — | 2,194.3 | — | |||||||||||||||||||

| Mining and Pelletizing: | |||||||||||||||||||||||

Iron ore1 | 357.1 | 515.0 | 838.1 | 1,357.8 | |||||||||||||||||||

| Freight | 27.2 | 40.6 | 65.4 | 98.0 | |||||||||||||||||||

| Total Mining and Pelletizing | 384.3 | 555.6 | 903.5 | 1,455.8 | |||||||||||||||||||

| Total revenues | $ | 1,646.0 | $ | 555.6 | $ | 3,097.8 | $ | 1,455.8 | |||||||||||||||

1 Includes Realization of deferred revenue of $34.6 million for the nine months ended September 30, 2020. | |||||||||||||||||||||||

10

We sell to customers located primarily in the United States and to foreign customers, primarily in Canada, Mexico and Western Europe. Net revenues to customers located outside the United States were $265.0 million and $487.7 million for the three and nine months ended September 30, 2020, respectively, and $138.9 million and $318.3 million for the three and nine months ended September 30, 2019, respectively.

Allowance for Credit Losses

The following is a roll forward of our allowance for credit losses associated with Accounts receivable, net:

| (In Millions) | |||||||||||

| 2020 | 2019 | ||||||||||

| Allowance for credit losses as of January 1 | $ | — | $ | — | |||||||

| Increase in allowance | 5.2 | — | |||||||||

| Allowance for credit losses as of September 30 | $ | 5.2 | $ | — | |||||||

Inventories

The following table presents the detail of our Inventories in the Statements of Unaudited Condensed Consolidated Financial Position:

| (In Millions) | |||||||||||

| September 30, 2020 | December 31, 2019 | ||||||||||

| Product inventories | |||||||||||

| Finished and semi-finished goods | $ | 940.5 | $ | 114.1 | |||||||

| Work-in-process | 78.2 | 68.7 | |||||||||

| Raw materials | 382.3 | 9.4 | |||||||||

| Total product inventories | 1,401.0 | 192.2 | |||||||||

| Manufacturing supplies and critical spares | 394.1 | 125.2 | |||||||||

| Inventories | $ | 1,795.1 | $ | 317.4 | |||||||

Deferred Revenue

The table below summarizes our deferred revenue balances:

| (In Millions) | |||||||||||||||||||||||

| Deferred Revenue (Current) | Deferred Revenue (Long-Term) | ||||||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | ||||||||||||||||||||

| Opening balance as of January 1 | $ | 22.1 | $ | 21.0 | $ | 25.7 | $ | 38.5 | |||||||||||||||

| Net decrease | (19.8) | (2.7) | (25.7) | (8.5) | |||||||||||||||||||

| Closing balance as of September 30 | $ | 2.3 | $ | 18.3 | $ | — | $ | 30.0 | |||||||||||||||

Prior to the Merger, our iron ore pellet sales agreement with Severstal, subsequently assumed by AK Steel, required supplemental payments to be paid by the customer during the period 2009 through 2013. Installment amounts received under this arrangement in excess of sales were classified as deferred revenue in the Statements of Consolidated Financial Position upon receipt of payment and the revenue was recognized over the term of the supply agreement, which had extended until 2022, in equal annual installments. As a result of the termination of that iron ore pellet sales agreement, we realized $34.6 million of deferred revenue, which was recognized within Realization of deferred revenue in the Statements of Unaudited Condensed Consolidated Operations, during the nine months ended September 30, 2020.

We have certain other sales agreements that require customers to pay in advance. Payments received pursuant to these agreements prior to revenue being recognized are recorded as deferred revenue in Other current liabilities.

11

Accrued Liabilities

The following table presents the detail of our Accrued liabilities in the Statements of Unaudited Condensed Consolidated Financial Position:

| (In Millions) | |||||||||||

| September 30, 2020 | December 31, 2019 | ||||||||||

| Accrued employment costs | $ | 146.6 | $ | 61.7 | |||||||

| Accrued interest | 81.8 | 29.0 | |||||||||

| Accrued dividends | 1.0 | 17.8 | |||||||||

| Other | 50.0 | 17.8 | |||||||||

| Accrued liabilities | $ | 279.4 | $ | 126.3 | |||||||

Cash Flow Information

A reconciliation of capital additions to cash paid for capital expenditures is as follows:

| (In Millions) | |||||||||||

| Nine Months Ended September 30, | |||||||||||

| 2020 | 2019 | ||||||||||

| Capital additions | $ | 333.0 | $ | 505.6 | |||||||

| Less: | |||||||||||

| Non-cash accruals | (88.4) | 26.1 | |||||||||

| Right-of-use assets - finance leases | 42.5 | 29.3 | |||||||||

| Grants | — | (10.5) | |||||||||

| Cash paid for capital expenditures including deposits | $ | 378.9 | $ | 460.7 | |||||||

Cash payments (receipts) for income taxes and interest are as follows:

| (In Millions) | |||||||||||

| Nine Months Ended September 30, | |||||||||||

| 2020 | 2019 | ||||||||||

| Taxes paid on income | $ | 3.2 | $ | 0.1 | |||||||

| Income tax refunds | (119.3) | (117.9) | |||||||||

Interest paid on debt obligations net of capitalized interest1 | 106.0 | 71.9 | |||||||||

1 Capitalized interest was $38.0 million and $16.9 million for the nine months ended September 30, 2020 and 2019, respectively. | |||||||||||

Non-Cash Investing and Financing Activities

| (In Millions) | |||||||||||

| Nine Months Ended September 30, | |||||||||||

| 2020 | 2019 | ||||||||||

| Fair value of common shares issued for consideration for business combination | $ | 617.6 | $ | — | |||||||

| Fair value of equity awards assumed from AK Steel acquisition | 3.9 | — | |||||||||

NOTE 3 - ACQUISITION OF AK STEEL

Overview

On March 13, 2020, pursuant to the Merger Agreement, we completed the acquisition of AK Steel, in which we were the acquirer. As a result of the Merger, each share of AK Steel common stock issued and outstanding

12

immediately prior to the effective time of the Merger (other than excluded shares) was converted into the right to receive 0.400 Cliffs common shares and, if applicable, cash in lieu of any fractional Cliffs common shares.

The acquisition combined Cliffs, North America’s largest producer of iron ore pellets, with AK Steel, a leading producer of innovative flat-rolled carbon, stainless and electrical steel products, to create a vertically integrated producer of value-added iron ore and steel products. The combination is expected to create significant opportunities to generate additional value from market trends across the entire steel value chain and enable more consistent, predictable performance through normal market cycles. Together, Cliffs and AK Steel have a presence across the entire manufacturing process, from mining to pelletizing to the development and production of finished high value steel products, including Next Generation Advanced High Strength Steels for automotive and other markets. We expect the combination will generate additional cost synergies, which we have identified and already set into motion savings of approximately $150 million, primarily from consolidating corporate functions, reducing duplicative overhead costs, and procurement and energy cost savings, as well as operational and supply chain efficiencies. The combined company is well positioned to provide high-value iron ore and steel solutions to customers primarily across North America.

Total net revenues for AK Steel for the most recent pre-acquisition year ended December 31, 2019 were $6,359.4 million. Following the acquisition, the operating results of AK Steel are included in our unaudited condensed consolidated financial statements and are reported as part of our Steel and Manufacturing segment. For the three months ended September 30, 2020, AK Steel generated Revenues of $1,261.7 million and a loss of $30.4 million included within Net income (loss) attributable to Cliffs shareholders, which included $14.6 million and $2.4 million related to amortization of the fair value inventory step-up and severance costs, respectively. For the period subsequent to the acquisition (March 13, 2020 through September 30, 2020), AK Steel generated Revenues of $2,194.3 million and a loss of $292.0 million included within Net income (loss) attributable to Cliffs shareholders, which included $74.0 million and $35.1 million related to amortization of the fair value inventory step-up and severance costs, respectively.

Additionally, we incurred acquisition-related costs in connection with the acquisition of AK Steel, excluding severance costs, of $0.6 million and $25.6 million for the three and nine months ended September 30, 2020, respectively, which were recorded in Acquisition-related costs on the Statements of Unaudited Condensed Consolidated Operations.

Refer to NOTE 7 - DEBT AND CREDIT FACILITIES for information regarding debt transactions executed in connection with the Merger.

The Merger was accounted for under the acquisition method of accounting for business combinations. The acquisition date fair value of the consideration transferred totaled $1.5 billion. The following tables summarize the consideration paid for AK Steel and the estimated fair values of the assets acquired and liabilities assumed at the acquisition date.

The fair value of the total purchase consideration was determined as follows:

| (In Millions) | |||||

| Fair value of Cliffs common shares issued for AK Steel outstanding common stock | $ | 617.6 | |||

| Fair value of replacement equity awards | 3.9 | ||||

| Fair value of AK Steel debt | 913.6 | ||||

| Total purchase consideration | $ | 1,535.1 | |||

13

The fair value of Cliffs common shares issued for outstanding shares of AK Steel common stock and with respect to Cliffs common shares underlying converted AK Steel equity awards that vested upon completion of the Merger is calculated as follows:

| (In Millions, Except Per Share Amounts) | |||||

| Number of shares of AK Steel common stock issued and outstanding | 316.9 | ||||

| Exchange ratio | 0.400 | ||||

| Number of Cliffs common shares issued to AK Steel stockholders | 126.8 | ||||

| Price per share of Cliffs common shares | $ | 4.87 | |||

| Fair value of Cliffs common shares issued for AK Steel outstanding common stock | $ | 617.6 | |||

The fair value of AK Steel's debt included in the consideration is calculated as follows:

| (In Millions) | |||||

| Credit Facility | $ | 590.0 | |||

| 7.50% Senior Secured Notes due July 2023 | 323.6 | ||||

| Fair value of debt included in consideration | $ | 913.6 | |||

Valuation Assumption and Preliminary Purchase Price Allocation

We estimated fair values at March 13, 2020 for the preliminary allocation of consideration to the net tangible and intangible assets acquired and liabilities assumed. During the measurement period, we will continue to obtain information to assist in finalizing the fair value of assets acquired and liabilities assumed, which may differ materially from these preliminary estimates. If we determine any measurement period adjustments are material, we will apply those adjustments, including any related impacts to net income, in the reporting period in which the adjustments are determined. We are in the process of conducting a valuation of the assets acquired and liabilities assumed related to the acquisition, most notably, inventories, including manufacturing supplies and critical spares, personal and real property, leases, investments, deferred taxes, asset retirement obligations, pension and OPEB liabilities and intangible assets and liabilities, and the final allocation will be made when completed, including the result of any identified goodwill. Accordingly, the provisional measurements noted below are preliminary and subject to modification in the future.

14

The preliminary purchase price allocation to assets acquired and liabilities assumed in the Merger was:

| (In Millions) | |||||||||||||||||

| Initial Allocation of Consideration | Measurement Period Adjustments | Updated Preliminary Allocation | |||||||||||||||

| Cash and cash equivalents | $ | 37.7 | $ | 2.0 | $ | 39.7 | |||||||||||

| Accounts receivable | 666.0 | (3.1) | 662.9 | ||||||||||||||

| Inventories | 1,562.8 | (39.8) | 1,523.0 | ||||||||||||||

| Other current assets | 67.5 | (15.4) | 52.1 | ||||||||||||||

| Property, plant and equipment | 2,184.4 | (20.1) | 2,164.3 | ||||||||||||||

| Intangible assets | 163.0 | (15.0) | 148.0 | ||||||||||||||

| Right of use asset, operating leases | 225.9 | (16.3) | 209.6 | ||||||||||||||

| Other non-current assets | 85.9 | 26.2 | 112.1 | ||||||||||||||

| Accounts payable | (636.3) | (6.1) | (642.4) | ||||||||||||||

| Accrued liabilities | (222.5) | 0.1 | (222.4) | ||||||||||||||

| Other current liabilities | (181.8) | 6.6 | (175.2) | ||||||||||||||

| Long-term debt | (1,179.4) | — | (1,179.4) | ||||||||||||||

| Deferred income taxes | (19.7) | (0.2) | (19.9) | ||||||||||||||

| Operating lease liability, non-current | (188.1) | 12.7 | (175.4) | ||||||||||||||

| Intangible liabilities | (140.0) | 69.5 | (70.5) | ||||||||||||||

| Pension and OPEB liabilities | (873.0) | 2.1 | (870.9) | ||||||||||||||

| Asset retirement obligations | (13.9) | (2.0) | (15.9) | ||||||||||||||

| Other non-current liabilities | (144.2) | (2.3) | (146.5) | ||||||||||||||

| Net identifiable assets acquired | 1,394.3 | (1.1) | 1,393.2 | ||||||||||||||

| Goodwill | 141.2 | 0.7 | 141.9 | ||||||||||||||

| Total net assets acquired | $ | 1,535.5 | $ | (0.4) | $ | 1,535.1 | |||||||||||

During the second and third quarter of 2020, we made certain measurement period adjustments to the acquired assets and liabilities assumed due to clarification of information utilized to determine fair value during the measurement period. The Inventories measurement period adjustments of $39.8 million resulted in a favorable impact of $0.2 million and $8.0 million, respectively, to Cost of goods sold for the three and nine months ended September 30, 2020.

The goodwill resulting from the acquisition of AK Steel was assigned to Precision Partners, our downstream tooling and stamping operations, and AK Tube, our tubing operations, that are reporting units included in the Steel and Manufacturing segment. Goodwill is calculated as the excess of the purchase price over the net identifiable assets recognized and primarily represents the growth opportunities in lightweighting solutions to automotive customers, as well as any synergistic benefits to be realized from the acquisition of AK Steel. None of the goodwill is expected be deductible for income tax purposes.

The preliminary purchase price allocated to identifiable intangible assets and liabilities acquired was:

| (In Millions) | Weighted Average Life (In Years) | ||||||||||

| Intangible assets: | |||||||||||

| Customer relationships | $ | 77.0 | 18 | ||||||||

| Developed technology | 60.0 | 17 | |||||||||

| Trade names and trademarks | 11.0 | 10 | |||||||||

| Total identifiable intangible assets | $ | 148.0 | 17 | ||||||||

| Intangible liabilities: | |||||||||||

| Above-market supply contracts | $ | (70.5) | 12 | ||||||||

15

The above-market supply contracts relate to the long-term coke and energy supply agreements with SunCoke Energy, which includes SunCoke Middletown, a consolidated VIE. Refer to NOTE 16 - VARIABLE INTEREST ENTITIES for further information.

Pro Forma Results

The following table provides unaudited pro forma financial information, prepared in accordance with Topic 805, for the three and nine months ended September 30, 2020 and 2019, as if AK Steel had been acquired as of January 1, 2019:

| (In Millions) | |||||||||||||||||||||||

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | ||||||||||||||||||||

| Revenues | $ | 1,646.0 | $ | 1,937.6 | $ | 4,265.1 | $ | 5,958.7 | |||||||||||||||

| Net income (loss) attributable to Cliffs shareholders | (6.0) | 84.2 | (123.9) | 213.3 | |||||||||||||||||||

The unaudited pro forma financial information has been calculated after applying our accounting policies and adjusting the historical results with pro forma adjustments, net of tax, that assume the acquisition occurred on January 1, 2019. Significant pro forma adjustments include the following:

1.The elimination of intercompany revenues between Cliffs and AK Steel of $135.6 million and $394.8 million for the three and nine months ended September 30, 2020, respectively, and $153.5 million and $410.8 million for the three and nine months ended September 30, 2019, respectively.

2.The 2020 pro forma net loss was adjusted to exclude $14.6 million and $74.0 million of non-recurring inventory acquisition accounting adjustments incurred during the three and nine months ended September 30, 2020, respectively. The 2019 pro forma net income was adjusted to include $74.0 million of non-recurring inventory acquisition accounting adjustments for the nine months ended September 30, 2019.

3.The elimination of nonrecurring transaction costs incurred by Cliffs and AK Steel in connection with the Merger of $0.7 million and $29.1 million for the three and nine months ended September 30, 2020, respectively.

4.Total other pro forma adjustments included expense of $10.0 million for the three and nine months ended September 30, 2020, primarily due to increased interest expense, offset by reduced amortization expense, depreciation expense and pension and OPEB expense. Total other pro forma adjustments for the three and nine months ended September 30, 2019 included expense of $1.1 million and $7.0 million, respectively, primarily due to reduced interest and amortization expense, offset by additional depreciation expense and pension and OPEB expense.

5.The income tax impact of pro forma transaction adjustments that affect Net income (loss) attributable to Cliffs shareholders at a statutory rate of 24.3% resulted in an income tax benefit of $5.6 million and $2.1 million for the three and nine months ended September 30, 2020, respectively, and an income tax benefit of $2.1 million and $4.5 million for the three and nine months ended September 30, 2019, respectively.

The unaudited pro forma financial information does not reflect the potential realization of synergies or cost savings, nor does it reflect other costs relating to the integration of the two companies. This unaudited pro forma financial information should not be considered indicative of the results that would have actually occurred if the acquisition had been consummated on January 1, 2019, nor are they indicative of future results.

16

NOTE 4 - SEGMENT REPORTING

Our Company is a vertically integrated producer of value-added iron ore and steel products. Our operations are organized and managed in two operating segments according to our upstream and downstream operations. Our Steel and Manufacturing segment is a leading producer of flat-rolled carbon, stainless and electrical steel products, primarily for the automotive, infrastructure and manufacturing, and distributors and converters markets. Our Steel and Manufacturing segment includes subsidiaries that provide customer solutions with carbon and stainless steel tubing products, advanced-engineered solutions, tool design and build, hot- and cold-stamped steel components, and complex assemblies. Construction of our HBI production plant in Toledo, Ohio, included as part of our Steel and Manufacturing segment, is expected to be completed with production beginning in the fourth quarter of 2020. Our Mining and Pelletizing segment is a major supplier of iron ore pellets to the North American steel industry from our mines and pellet plants located in Michigan and Minnesota. All intercompany transactions were eliminated in consolidation.

We evaluate performance on a segment basis, as well as a consolidated basis, based on Adjusted EBITDA, which is a non-GAAP measure. This measure is used by management, investors, lenders and other external users of our financial statements to assess our operating performance and to compare operating performance to other companies in the steel and iron ore industries. In addition, management believes Adjusted EBITDA is a useful measure to assess the earnings power of the business without the impact of capital structure and can be used to assess our ability to service debt and fund future capital expenditures in the business.

Our results by segment are as follows:

| (In Millions, Except Sales Tons) | |||||||||||||||||||||||

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | ||||||||||||||||||||

| Sales volume (in thousands): | |||||||||||||||||||||||

| Steel and Manufacturing (net tons) | 1,117 | — | 1,935 | — | |||||||||||||||||||

| Mining and Pelletizing sales (long tons) | 4,907 | 5,750 | 11,800 | 13,527 | |||||||||||||||||||

| Less: Intercompany sales (long tons) | (1,204) | (346) | (3,028) | (384) | |||||||||||||||||||

| Mining and Pelletizing consolidated sales (long tons) | 3,703 | 5,404 | 8,772 | 13,143 | |||||||||||||||||||

| Revenues: | |||||||||||||||||||||||

| Steel and Manufacturing net sales to external customers | $ | 1,261.7 | $ | — | $ | 2,194.3 | $ | — | |||||||||||||||

Mining and Pelletizing net sales1 | 520.3 | 590.6 | 1,238.7 | 1,494.8 | |||||||||||||||||||

| Less: Intercompany sales | (136.0) | (35.0) | (335.2) | (39.0) | |||||||||||||||||||

| Mining and Pelletizing net sales to external customers | 384.3 | 555.6 | 903.5 | 1,455.8 | |||||||||||||||||||

| Total revenues | $ | 1,646.0 | $ | 555.6 | $ | 3,097.8 | $ | 1,455.8 | |||||||||||||||

| Adjusted EBITDA: | |||||||||||||||||||||||

| Steel and Manufacturing | $ | 33.3 | $ | (2.1) | $ | (81.8) | $ | (4.0) | |||||||||||||||

| Mining and Pelletizing | 145.3 | 182.7 | 309.5 | 510.7 | |||||||||||||||||||

| Corporate and eliminations | (52.3) | (36.5) | (160.7) | (93.0) | |||||||||||||||||||

| Total Adjusted EBITDA | $ | 126.3 | $ | 144.1 | $ | 67.0 | $ | 413.7 | |||||||||||||||

1 Includes Realization of deferred revenue of $34.6 million for the nine months ended September 30, 2020. | |||||||||||||||||||||||

17

The following table provides a reconciliation of our consolidated Net income (loss) to total Adjusted EBITDA:

| (In Millions) | |||||||||||||||||||||||

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | ||||||||||||||||||||

| Net income (loss) | $ | 1.9 | $ | 90.9 | $ | (154.8) | $ | 229.6 | |||||||||||||||

| Less: | |||||||||||||||||||||||

| Interest expense, net | (68.2) | (25.4) | (167.9) | (76.8) | |||||||||||||||||||

| Income tax benefit (expense) | 22.4 | (4.8) | 98.5 | (23.1) | |||||||||||||||||||

| Depreciation, depletion and amortization | (72.4) | (22.2) | (183.9) | (63.1) | |||||||||||||||||||

| Total EBITDA | $ | 120.1 | $ | 143.3 | $ | 98.5 | $ | 392.6 | |||||||||||||||

| Less: | |||||||||||||||||||||||

EBITDA of noncontrolling interests1 | $ | 16.2 | $ | — | $ | 41.3 | $ | — | |||||||||||||||

| Gain (loss) on extinguishment of debt | — | — | 132.6 | (18.2) | |||||||||||||||||||

| Severance costs | (2.4) | — | (38.3) | (1.7) | |||||||||||||||||||

| Acquisition-related costs excluding severance costs | (5.1) | — | (30.1) | — | |||||||||||||||||||

| Amortization of inventory step-up | (14.6) | — | (74.0) | — | |||||||||||||||||||

| Impact of discontinued operations | (0.3) | (0.8) | — | (1.2) | |||||||||||||||||||

| Total Adjusted EBITDA | $ | 126.3 | $ | 144.1 | $ | 67.0 | $ | 413.7 | |||||||||||||||

1 EBITDA of noncontrolling interests includes $11.9 million and $31.2 million for income and $4.3 million and $10.1 million for depreciation, depletion and amortization for the three and nine months ended September 30, 2020, respectively. | |||||||||||||||||||||||

The following summarizes our assets by segment:

| (In Millions) | |||||||||||

| September 30, 2020 | December 31, 2019 | ||||||||||

| Assets: | |||||||||||

| Steel and Manufacturing | $ | 6,345.7 | $ | 913.6 | |||||||

| Mining and Pelletizing | 1,643.3 | 1,643.1 | |||||||||

| Total segment assets | 7,989.0 | 2,556.7 | |||||||||

| Corporate and Other (including discontinued operations) | 491.9 | 947.1 | |||||||||

| Total assets | $ | 8,480.9 | $ | 3,503.8 | |||||||

The following table summarizes our capital additions by segment:

| (In Millions) | |||||||||||||||||||||||

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | ||||||||||||||||||||

Capital additions1: | |||||||||||||||||||||||

| Steel and Manufacturing | $ | 88.0 | $ | 160.5 | $ | 266.8 | $ | 398.0 | |||||||||||||||

| Mining and Pelletizing | 13.3 | 22.1 | 64.9 | 104.5 | |||||||||||||||||||

| Corporate and Other | 1.0 | 2.1 | 1.3 | 3.1 | |||||||||||||||||||

| Total capital additions | $ | 102.3 | $ | 184.7 | $ | 333.0 | $ | 505.6 | |||||||||||||||

1 Refer to NOTE 2 - SUPPLEMENTARY FINANCIAL STATEMENT INFORMATION for additional information. | |||||||||||||||||||||||

18

NOTE 5 - PROPERTY, PLANT AND EQUIPMENT

The following table indicates the carrying value of each of the major classes of our depreciable assets:

| (In Millions) | |||||||||||

| September 30, 2020 | December 31, 2019 | ||||||||||

| Land, land improvements and mineral rights | $ | 653.2 | $ | 582.2 | |||||||

| Buildings | 454.4 | 157.8 | |||||||||

| Steel and Manufacturing equipment | 2,128.0 | 42.0 | |||||||||

| Mining and Pelletizing equipment | 1,455.2 | 1,413.6 | |||||||||

| Other | 121.3 | 101.5 | |||||||||

| Construction-in-progress | 1,145.9 | 730.3 | |||||||||

Total property, plant and equipment1 | 5,958.0 | 3,027.4 | |||||||||

| Allowance for depreciation and depletion | (1,407.3) | (1,098.4) | |||||||||

| Property, plant and equipment, net | $ | 4,550.7 | $ | 1,929.0 | |||||||

1 Includes right-of-use assets related to finance leases of $97.1 million and $49.0 million as of September 30, 2020 and December 31, 2019, respectively. | |||||||||||

We recorded capitalized interest into property, plant and equipment of $14.7 million and $38.0 million during the three and nine months ended September 30, 2020, respectively, and $7.0 million and $16.9 million for the three and nine months ended September 30, 2019, respectively.

We recorded depreciation and depletion expense of $71.8 million and $182.5 million for the three and nine months ended September 30, 2020, respectively, and $22.0 million and $62.5 million for the three and nine months ended September 30, 2019, respectively.

NOTE 6 - GOODWILL AND INTANGIBLE ASSETS AND LIABILITIES

Goodwill

The increase in the balance of Goodwill as of September 30, 2020, compared to December 31, 2019, is due to the preliminary assignment of $141.9 million to Goodwill in 2020 based on the preliminary purchase price allocation for the acquisition of AK Steel. The carrying amount of goodwill related to our Mining and Pelletizing segment was $2.1 million as of both September 30, 2020 and December 31, 2019.

19

Intangible Assets and Liabilities

The following is a summary of our intangible assets and liabilities:

| (In Millions) | |||||||||||||||||||||||

Classification1 | Gross Amount | Accumulated Amortization | Net Amount | ||||||||||||||||||||

| As of September 30, 2020 | |||||||||||||||||||||||

| Intangible assets: | |||||||||||||||||||||||

| Customer relationships | Intangible assets, net | $ | 77.0 | $ | (2.6) | $ | 74.4 | ||||||||||||||||

| Developed technology | Intangible assets, net | 60.0 | (2.1) | 57.9 | |||||||||||||||||||

| Trade names and trademarks | Intangible assets, net | 11.0 | (0.7) | 10.3 | |||||||||||||||||||

| Mining permits | Intangible assets, net | 72.2 | (24.7) | 47.5 | |||||||||||||||||||

| Total intangible assets | $ | 220.2 | $ | (30.1) | $ | 190.1 | |||||||||||||||||

| Intangible liabilities: | |||||||||||||||||||||||

| Above-market supply contracts | Intangible liabilities, net | $ | (70.5) | $ | 4.6 | $ | (65.9) | ||||||||||||||||

| As of December 31, 2019 | |||||||||||||||||||||||

| Intangible assets: | |||||||||||||||||||||||

| Mining permits | Intangible assets, net | $ | 72.2 | $ | (24.1) | $ | 48.1 | ||||||||||||||||

1 Amortization of intangible liabilities related to above-market supply contracts and intangible assets related to mining permits is recognized in Cost of goods sold. Amortization of all other intangible assets is recognized in Selling, general and administrative expenses. | |||||||||||||||||||||||

Amortization expense related to intangible assets was $2.5 million and $6.0 million for the three and nine months ended September 30, 2020, respectively, and $0.2 million and $0.6 million for the three and nine months ended September 30, 2019, respectively.

Estimated future amortization expense related to intangible assets at September 30, 2020 is as follows:

| (In Millions) | ||||||||

| Years ending December 31, | ||||||||

| 2020 (remaining period of the year) | $ | 2.5 | ||||||

| 2021 | 10.0 | |||||||

| 2022 | 10.0 | |||||||

| 2023 | 10.0 | |||||||

| 2024 | 10.0 | |||||||

| 2025 | 10.0 | |||||||

Income from amortization related to the intangible liabilities was $1.9 million and $4.6 million for the three and nine months ended September 30, 2020, respectively.

Estimated future amortization income related to the intangible liabilities at September 30, 2020 is as follows:

| (In Millions) | ||||||||

| Years ending December 31, | ||||||||

| 2020 (remaining period of the year) | $ | 2.0 | ||||||

| 2021 | 7.8 | |||||||

| 2022 | 7.8 | |||||||

| 2023 | 7.8 | |||||||

| 2024 | 7.8 | |||||||

| 2025 | 7.8 | |||||||

20

NOTE 7 - DEBT AND CREDIT FACILITIES

The following represents a summary of our long-term debt:

| (In Millions) | ||||||||||||||||||||||||||||||||||||||

| September 30, 2020 | ||||||||||||||||||||||||||||||||||||||

| Debt Instrument | Issuer1 | Annual Effective Interest Rate | Total Principal Amount | Debt Issuance Costs | Unamortized Premiums (Discounts) | Total Debt | ||||||||||||||||||||||||||||||||

| Senior Secured Notes: | ||||||||||||||||||||||||||||||||||||||

| 4.875% 2024 Senior Secured Notes | Cliffs | 5.00% | $ | 394.5 | $ | (3.7) | $ | (1.5) | $ | 389.3 | ||||||||||||||||||||||||||||

| 9.875% 2025 Senior Secured Notes | Cliffs | 10.57% | 955.2 | (8.1) | (25.8) | 921.3 | ||||||||||||||||||||||||||||||||

| 6.75% 2026 Senior Secured Notes | Cliffs | 6.99% | 845.0 | (21.4) | (9.0) | 814.6 | ||||||||||||||||||||||||||||||||

| Senior Unsecured Notes: | ||||||||||||||||||||||||||||||||||||||

| 7.625% 2021 AK Senior Notes | AK Steel | 7.33% | 33.5 | — | 0.1 | 33.6 | ||||||||||||||||||||||||||||||||

| 7.50% 2023 AK Senior Notes | AK Steel | 6.17% | 12.8 | — | 0.5 | 13.3 | ||||||||||||||||||||||||||||||||

| 6.375% 2025 Senior Notes | Cliffs | 8.11% | 64.3 | (0.2) | (4.6) | 59.5 | ||||||||||||||||||||||||||||||||

| 6.375% 2025 AK Senior Notes | AK Steel | 8.11% | 38.4 | — | (2.7) | 35.7 | ||||||||||||||||||||||||||||||||

| 1.50% 2025 Convertible Senior Notes | Cliffs | 6.26% | 296.3 | (3.7) | (53.0) | 239.6 | ||||||||||||||||||||||||||||||||

| 5.75% 2025 Senior Notes | Cliffs | 6.01% | 396.2 | (2.6) | (4.1) | 389.5 | ||||||||||||||||||||||||||||||||

| 7.00% 2027 Senior Notes | Cliffs | 9.24% | 88.0 | (0.3) | (9.6) | 78.1 | ||||||||||||||||||||||||||||||||

| 7.00% 2027 AK Senior Notes | AK Steel | 9.24% | 56.3 | — | (6.0) | 50.3 | ||||||||||||||||||||||||||||||||

| 5.875% 2027 Senior Notes | Cliffs | 6.49% | 555.5 | (4.3) | (18.6) | 532.6 | ||||||||||||||||||||||||||||||||

| 6.25% 2040 Senior Notes | Cliffs | 6.34% | 262.7 | (1.8) | (2.8) | 258.1 | ||||||||||||||||||||||||||||||||

| IRBs due 2024 to 2028 | AK Steel | Various | 92.0 | — | 2.3 | 94.3 | ||||||||||||||||||||||||||||||||

| ABL Facility | Cliffs2 | 2.77% | 2,000.0 | — | — | 400.0 | ||||||||||||||||||||||||||||||||

| Total long-term debt | $ | 4,309.8 | ||||||||||||||||||||||||||||||||||||

1 Unless otherwise noted, references in this column to "Cliffs" are to Cleveland-Cliffs Inc., and references to "AK Steel" are to AK Steel Corporation.

2 Refers to Cleveland-Cliffs Inc. as borrower under our ABL Facility.

2 Refers to Cleveland-Cliffs Inc. as borrower under our ABL Facility.

| (In Millions) | ||||||||||||||||||||||||||||||||||||||

| December 31, 2019 | ||||||||||||||||||||||||||||||||||||||

| Debt Instrument | Issuer1 | Annual Effective Interest Rate | Total Principal Amount | Debt Issuance Costs | Unamortized Discounts | Total Debt | ||||||||||||||||||||||||||||||||

| Senior Secured Notes: | ||||||||||||||||||||||||||||||||||||||

| 4.875% 2024 Senior Notes | Cliffs | 5.00% | $ | 400.0 | $ | (4.6) | $ | (1.8) | $ | 393.6 | ||||||||||||||||||||||||||||

| Senior Unsecured Notes: | ||||||||||||||||||||||||||||||||||||||

| 1.50% 2025 Convertible Senior Notes | Cliffs | 6.26% | 316.3 | (4.6) | (65.0) | 246.7 | ||||||||||||||||||||||||||||||||

| 5.75% 2025 Senior Notes | Cliffs | 6.01% | 473.3 | (3.6) | (5.5) | 464.2 | ||||||||||||||||||||||||||||||||

| 5.875% 2027 Senior Notes | Cliffs | 6.49% | 750.0 | (6.3) | (27.3) | 716.4 | ||||||||||||||||||||||||||||||||

| 6.25% 2040 Senior Notes | Cliffs | 6.34% | 298.4 | (2.2) | (3.3) | 292.9 | ||||||||||||||||||||||||||||||||

| Former ABL Facility | Cliffs2 | N/A | 450.0 | N/A | N/A | — | ||||||||||||||||||||||||||||||||

| Total long-term debt | $ | 2,113.8 | ||||||||||||||||||||||||||||||||||||

1 Unless otherwise noted, references in this column to "Cliffs" are to Cleveland-Cliffs Inc.

2 Refers to Cleveland-Cliffs Inc. and certain of its subsidiaries as borrowers under our Former ABL Facility.

2 Refers to Cleveland-Cliffs Inc. and certain of its subsidiaries as borrowers under our Former ABL Facility.

21

Debt Extinguishments - 2020

On April 24, 2020, we used the net proceeds from the offering of the additional 9.875% 2025 Senior Secured Notes to repurchase $736.4 million aggregate principal amount of our outstanding senior notes of various series, which resulted in debt reduction of $181.2 million. During the second quarter of 2020, we also repurchased an additional $11.2 million aggregate principal amount of our outstanding senior notes of various series with cash on hand. On June 1, 2020, we redeemed $7.3 million aggregate principal amount of our outstanding 2020 IRBs.

On March 13, 2020, in connection with the Merger, we purchased $364.2 million aggregate principal amount of 7.625% 2021 AK Senior Notes and $310.7 million aggregate principal amount of 7.50% 2023 AK Senior Notes upon early settlement of tender offers made by Cliffs. The net proceeds from the offering of 6.75% 2026 Senior Secured Notes, along with a portion of the ABL Facility borrowings, were used to fund such purchases. As the 7.625% 2021 AK Senior Notes and 7.50% 2023 AK Senior Notes were recorded at fair value just prior to being purchased, there was no gain or loss on extinguishment. Additionally, in connection with the final settlement of the tender offers, on March 27, 2020, we purchased $8.5 million aggregate principal amount of the 7.625% 2021 AK Senior Notes and $56.5 million aggregate principal amount of the 7.50% 2023 AK Senior Notes with cash on hand.

The following is a summary of the debt extinguished and the respective gain on extinguishment:

| (In Millions) | ||||||||||||||

| Nine Months Ended September 30, 2020 | ||||||||||||||

| Debt Instrument | Debt Extinguished | Gain on Extinguishment | ||||||||||||

| 7.625% 2021 AK Senior Notes | $ | 372.7 | $ | 0.4 | ||||||||||

| 7.50% 2023 AK Senior Notes | 367.2 | 2.8 | ||||||||||||

| 4.875% 2024 Senior Secured Notes | 5.5 | 0.5 | ||||||||||||

| 6.375% 2025 Senior Notes | 167.5 | 21.3 | ||||||||||||

| 1.50% 2025 Convertible Senior Notes | 20.0 | 1.3 | ||||||||||||

| 5.75% 2025 Senior Notes | 77.1 | 16.3 | ||||||||||||

| 7.00% 2027 Senior Notes | 247.3 | 28.4 | ||||||||||||

| 5.875% 2027 Senior Notes | 194.5 | 48.7 | ||||||||||||

| 6.25% 2040 Senior Notes | 35.7 | 12.9 | ||||||||||||

| $ | 1,487.5 | $ | 132.6 | |||||||||||

Debt Extinguishments - 2019

The following is a summary of the debt extinguished with cash and the respective loss on extinguishment:

| (In Millions) | ||||||||||||||

| Nine Months Ended September 30, 2019 | ||||||||||||||

| Debt Instrument | Debt Extinguished | (Loss) on Extinguishment | ||||||||||||

| 4.875% 2021 Senior Notes | $ | 124.0 | $ | (5.3) | ||||||||||

| 5.75% 2025 Senior Notes | 600.0 | (12.9) | ||||||||||||

| $ | 724.0 | $ | (18.2) | |||||||||||

ABL Facility

As of September 30, 2020, we were in compliance with the ABL Facility liquidity requirements and, therefore, the springing financial covenant requiring a minimum fixed charge coverage ratio of 1.0 to 1.0 was not applicable.

22

The following represents a summary of our borrowing capacity under the ABL Facility:

| (In Millions) | ||||||||

| September 30, 2020 | ||||||||

Available borrowing base on ABL Facility1 | $ | 1,715.2 | ||||||

| Borrowings | (400.0) | |||||||

Letter of credit obligations2 | (192.2) | |||||||

| Borrowing capacity available | $ | 1,123.0 | ||||||

1 As of September 30, 2020, the ABL Facility has a maximum borrowing base of $2.0 billion. The available borrowing base is determined by applying customary advance rates to eligible accounts receivable, inventory and certain mobile equipment.

2 We issued standby letters of credit with certain financial institutions in order to support business obligations including, but not limited to, workers' compensation, employee severance, IRBs and environmental obligations.

2 We issued standby letters of credit with certain financial institutions in order to support business obligations including, but not limited to, workers' compensation, employee severance, IRBs and environmental obligations.

Debt Maturities

The following represents a summary of our maturities of debt instruments based on the principal amounts outstanding at September 30, 2020:

| (In Millions) | ||||||||

| Maturities of Debt | ||||||||

| 2020 (remaining period of year) | $ | — | ||||||

| 2021 | 33.5 | |||||||

| 2022 | — | |||||||

| 2023 | 12.8 | |||||||

| 2024 | 456.5 | |||||||

| Thereafter | 3,987.9 | |||||||

| Total maturities of debt | $ | 4,490.7 | ||||||

23

NOTE 8 - FAIR VALUE MEASUREMENTS

The following represents the assets and liabilities measured at fair value:

| (In Millions) | |||||||||||||||||||||||

| September 30, 2020 | |||||||||||||||||||||||

Quoted Prices in Active Markets for Identical Assets/Liabilities (Level 1) | Significant Other Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | Total | ||||||||||||||||||||

| Assets: | |||||||||||||||||||||||

| Other current assets: | |||||||||||||||||||||||

| Commodity contracts | $ | — | $ | 15.8 | $ | — | $ | 15.8 | |||||||||||||||

| Customer supply agreement | — | — | 34.5 | 34.5 | |||||||||||||||||||

| Provisional pricing arrangement | — | — | 26.9 | 26.9 | |||||||||||||||||||

| Other non-current assets: | |||||||||||||||||||||||

| Commodity contracts | — | 1.8 | — | 1.8 | |||||||||||||||||||

| Total | $ | — | $ | 17.6 | $ | 61.4 | $ | 79.0 | |||||||||||||||