COMPUTER TASK GROUP INC - Annual Report: 2022 (Form 10-K)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended , 2022

OR

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Transition period from to

Commission File No. 1-9410b

COMPUTER TASK GROUP, INCORPORATED

(Exact name of registrant as specified in its charter)

New York |

|

16-0912632 |

(State or other jurisdiction of incorporation or organization) |

|

(I.R.S. Employer Identification No.) |

300 Corporate Parkway, Suite 214N, Amherst, New York |

|

14226 |

(Address of principal executive offices) |

|

(Zip Code) |

Registrant’s telephone number, including area code: (716) 882-8000

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

|

Trading Symbol |

Name of each exchange on which registered |

Common Stock, par value $0.01 per share |

|

CTG |

The NASDAQ Stock Market, LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “an emerging growth company” in Rule 12b-2 of the Exchange Act:

Large accelerated filer |

☐ |

Accelerated filer |

☒ |

|

|

|

|

Non-accelerated filer |

☐ |

Smaller reporting company |

☒ |

|

|

Emerging growth company |

☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). YES ☐ NO ☒

The aggregate market value of the registrant’s voting and non-voting common equity held by non-affiliates, computed by reference to the price at which the common equity was last sold on the last business day of the registrant’s most recently completed second quarter was $132.1 million. Solely for the purposes of this calculation, all persons who are or may be executive officers or directors of the registrant have been deemed to be affiliates.

The total number of shares of Common Stock of the Registrant outstanding at March 10, 2023 was 15,747,376.

PCAOB Auditor Firm Id: 248 Auditor Name: Grant Thornton LLP Auditor Location: Cleveland, OH, United States

DOCUMENTS INCORPORATED BY REFERENCE: None.

SEC Form 10-K Index

Section |

|

Page |

Part I |

|

|

Item 1. |

2 |

|

Item 1A. |

9 |

|

Item 1B. |

15 |

|

Item 2. |

16 |

|

Item 3. |

16 |

|

Item 4. |

16 |

|

Part II |

|

|

Item 5. |

17 |

|

Item 6. |

19 |

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

20 |

Item 7A. |

29 |

|

Item 8. |

30 |

|

Item 9. |

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

67 |

Item 9A. |

67 |

|

Item 9B. |

69 |

|

Item 9C. |

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections |

69 |

Part III |

|

|

Item 10. |

70 |

|

Item 11. |

74 |

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

89 |

Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

90 |

Item 14. |

91 |

|

Part IV |

|

|

Item 15. |

92 |

|

Item 16. |

94 |

|

|

96 |

|

As used in this annual report on Form 10-K, references to “CTG,” “the Company,” “the Registrant,” “we,” “us,” or “our” refer to Computer Task Group, Incorporated and its subsidiaries, unless the context suggests otherwise.

PART I

Forward-Looking Statements

This annual report on Form 10-K contains forward-looking information and statements made by the management of the Company that are based on the beliefs of management as well as assumptions made by, and information currently available to, the Company, and are subject to a number of risks and uncertainties. Further, certain forward-looking statements are based upon assumptions as to future events that may not prove to be accurate. These forward-looking statements are current only as of the date of this annual report. The Company assumes no obligation to update these statements based on information from and after the date of this report. Generally, forward-looking statements include words or phrases such as “anticipates,” “believes,” “expects,” “might,” “plans,” “may,” “will,” “would,” “should,” “could,” “seeks,” “estimates,” ”anticipates,” “project,” “predict,” “potential,” “currently,” “continue,” “intends,” “outlook,” and words and phrases of similar impact. The forward-looking statements include, but are not limited to, statements regarding future operations, industry trends or conditions and the business environment, and statements regarding future levels of or trends in business strategy and expectations, new business opportunities, cost control initiatives, business wins, market demand, revenue, operating expenses, capital expenditures, and financing. The forward-looking statements are made pursuant to safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Numerous factors and risks could cause actual results to differ materially from those in the forward-looking statements, including the following:

1

Item 1. Business

Overview

CTG was incorporated in Buffalo, New York on March 11, 1966, and its corporate headquarters is located at 300 Corporate Parkway, Suite 214N, Amherst, New York 14226 (716-882-8000). CTG has operations in North and South America, Western Europe, and India. CTG’s employees and billable subcontractors total approximately 3,200 people worldwide at December 31, 2022. During 2022, the parent, Computer Task Group, Incorporated (United States), had seventeen operating subsidiaries:

The Company provides information technology (“IT”) and related services to its clients. These services include information and technology-related solutions, including staffing as a solution. With solution services, the Company generally takes responsibility for the deliverables and some level of project and staff management, and services may include high-end advisory or business-related consulting. When providing staffing services, including managed staffing, staff augmentation, and volume staffing, personnel are provided to clients, who then, in turn, take their direction from the clients’ managers.

IT Solutions and Services

CTG is a leading provider of IT solutions and services, serving as a catalyst for our clients’ digital transformation. We increase project momentum and the speed at which our clients achieve their desired outcomes. Our solutions portfolio addresses critical challenges for clients in North America, South America, Western Europe, and India in high-growth industries. Clients we typically support are organizations with large, complex technology, information, and data requirements. Some have begun their digital transformation and are struggling to drive their desired results, while many are just starting to define their digital transformation needs and strategy.

CTG's Digital Transformation Solutions portfolio spans three areas that collectively address many of our clients' most pressing transformation challenges and are designed to address their unique business, technology, and operational needs. Our capabilities ensure that our clients utilize the right information technology to meet their business needs, maximize their IT systems' value, and operate efficiently and effectively. The following describes the typical services provided:

2

Non-Strategic Technology Services - Staffing

CTG’s staffing services address a range of information and technology resource needs, from filling specific talent gaps to managing high-volume staffing programs. CTG recruits, retains, and manages IT talent for its clients, which are primarily large technology service providers and other companies with multiple locations and a significant need for high-volume professional IT resources.

Capabilities

Our expertise in key technologies–what we call Digital Accelerators–underpins our solutions and ensures our clients receive optimal value from their digital technologies and methodologies. CTG's Digital Accelerators evolve to meet market needs and address the most innovative technology platforms and thinking. These Digital Accelerators include Agile and DevOps, Internet of Things (IoT), Intelligent Automation, Data and Analytics, Cloud, and Automated Testing.

As the pace of change accelerates, CTG accelerates our clients' digital environment through a unique combination of Transformation Solutions, Digital Accelerators, leading industry talent, domain expertise, innovative tools and methodologies, a partner ecosystem, and a Global Delivery Network.

3

Acquisition of Eleviant

On September 29, 2022, CTG acquired Eleviant Technologies, an expert in mobile, cloud, web blockchain, robotic process automation (RPA) and artificial intelligence (AI) technologies. The acquisition strengthened CTG’s digital offerings in areas such as AI, machine learning (ML), and intelligent automation while expanding capabilities in cloud migration, mobile application development, and emerging technologies, including blockchain. CTG's software-as-a-service (SaaS) offerings expand through leveraging Eleviant’s PeopleOne intranet solution, vChat, vBots, and other platforms. In addition, CTG's Global Delivery Network capacity, agility, and flexibility increases with the addition of established Eleviant teams in Chennai and Coimbatore, India.

Segments

In prior years, and in 2021 prior to the fourth quarter, the Company reported its results in one segment. This included operating segments for each of North America and Europe. The services the Company provided, regardless of geography or industry, were similar in nature and produced similar results. Additionally, the CEO, who is the Company’s chief operating decision maker, made decisions on investments and allocated resources at the North America or Europe level. Accordingly, given the consistency in the services provided and the results, the Company aggregated those results into one reporting segment.

During the 2021 fourth quarter, the Company further refined its strategy around providing digital services within its IT solutions business in both North America and Europe. As part of this process, the Company also determined that there are certain accounts that are no longer part of the Company’s long-term business plan. Accordingly, the Company is operating and reporting in three segments within its business; North America IT Solutions and Services, Europe IT Solutions and Services, and Non-Strategic Technology Services.

CTG’s revenue by segment for the three years ended December 31, 2022, 2021 and 2020 was as follows:

(amounts in thousands) |

|

2022 |

|

|

2021 |

|

|

2020 |

|

|||

North America IT Solutions and Services |

|

$ |

84,038 |

|

|

$ |

101,506 |

|

|

$ |

67,948 |

|

Europe IT Solutions and Services |

|

|

149,931 |

|

|

|

169,341 |

|

|

|

154,847 |

|

Non-Strategic Technology Services |

|

|

91,111 |

|

|

|

121,438 |

|

|

|

143,296 |

|

Total |

|

$ |

325,080 |

|

|

$ |

392,285 |

|

|

$ |

366,091 |

|

IT Solutions and Services (North America and Europe)

Consistent with its long-term strategy, the Company invested in recent years in business development, solutions, delivery, recruiting and marketing resources to drive its IT Solutions and Services. IT Solutions and Services include the activities described under “IT Solutions and Services” and “Capabilities” above. In North America, IT Solutions and Services revenue decreased 17.2% in 2022 from 2021 as the Company completed in 2021 a very large project totaling more than $25 million in revenue that was not repeated in 2022. Revenue in Europe decreased 11.5% from the prior year as foreign currency exchange rates decreased significantly in 2022 which reduced revenue year-over-year. In 2021, as compared with 2020, North America IT Solutions and Services revenue increased 49.4%, while the increase in revenue was 9.4% in Europe over that same time period. The increases were mainly the result of strong demand for the Company’s services, including the significant project previously referenced, and as a direct result of the business development investments that the Company had made. Additionally, the revenue from the Company’s acquisition of Eleviant is included in the North America IT Solutions and Services segment.

Non-Strategic Technology Services

Consistent with its long-term strategy, the Company is not investing in low margin Non-Strategic Technology Services, and as these contracts expire, is often electing to disengage from the project. This segment only consists of lower margin IT staffing and related services in North America and Europe as described in “Non-Strategic Technology Services - Staffing” above. Nearly all of the revenue in this segment is in North America. The revenue in this segment decreased 25.0% in 2022 as compared to 2021, and 15.3% in 2021 as compared to 2020.

Vertical Markets

The Company provides a majority of its services through five vertical market focus areas: technology service providers, healthcare (which includes services provided to healthcare providers, health insurers (payers), and life sciences

4

companies), financial services, manufacturing, and energy. The remainder of CTG’s revenue is derived from general markets.

CTG’s revenue by vertical market as a percentage of consolidated revenue for the three years ended December 31, 2022, 2021, and 2020 was as follows:

|

|

2022 |

|

|

2021 |

|

|

2020 |

|

|||

Technology service providers |

|

|

22.5 |

% |

|

|

26.7 |

% |

|

|

31.3 |

% |

Healthcare |

|

|

18.1 |

% |

|

|

21.6 |

% |

|

|

14.9 |

% |

Financial services |

|

|

15.9 |

% |

|

|

16.2 |

% |

|

|

15.8 |

% |

Manufacturing |

|

|

15.5 |

% |

|

|

11.7 |

% |

|

|

13.5 |

% |

Energy |

|

|

5.8 |

% |

|

|

5.1 |

% |

|

|

6.2 |

% |

General markets |

|

|

22.2 |

% |

|

|

18.7 |

% |

|

|

18.3 |

% |

Total |

|

|

100.0 |

% |

|

|

100.0 |

% |

|

|

100.0 |

% |

Technology Service Providers

Demand from our largest Non-Strategic Technology Services client, IBM, which is included in this vertical market, decreased in both 2022 and 2021. Additionally, revenue as a percentage of consolidated revenue decreased in 2022 and 2021 as compared with previous years due to a change in business mix as the Company focused on driving its IT Solutions and Services, which are not included in this vertical market.

Healthcare

In 2022, the overall demand from our healthcare clients decreased as a result of a large training, implementation, and support engagement for a health system in North America completed in the 2021 fourth quarter that was not repeated in 2022. In contrast, consolidated revenue for the Company’s healthcare vertical market increased in 2021 as compared to 2020 as a result of the large 2021 fourth quarter project.

Financial Services

Revenue for the Company’s financial services vertical market as a percentage of consolidated revenue decreased in 2022 as compared with 2021 due to weaker demand from several clients in the Europe IT Solutions and Services segment. Revenue for the Company’s financial services vertical market as a percentage of consolidated revenue increased in 2021 as compared to 2020 due to strong demand from several clients for project related work in the North America IT Solutions and Services segment.

Manufacturing

The consolidated revenue in our manufacturing vertical market is primarily generated from several large Non-Strategic Technology Services clients, including Lenovo (through SDI International as a vendor manager for Lenovo), which is one of our largest clients. Revenue from Lenovo and other large clients increased in 2022 as a percentage of consolidated revenue compared with 2021 as a result of the significant reduction in consolidated revenue, and decreased in 2021 as compared with 2020 as the demand for these services decreased in recent years. Additionally, the Company continues to disengage from its lowest margin Non-Strategic Technology Services business, which is generally included in this vertical market.

Energy

Revenue for the Company's energy vertical market increased as a percentage of consolidated revenue in 2022 given strong demand for our services in this vertical market, but decreased as a percentage of revenue in 2021.

For the year ended December 31, 2022, CTG provided its services to approximately 541 clients, primarily in North America and Europe. In North America, the Company operates in the United States and Canada, with about 99% of 2022 North American revenue generated in the United States. In Europe, the Company operates in Belgium, Luxembourg, France, and the United Kingdom. Of total 2022 consolidated revenue of $325.1 million, approximately 53.3% was generated in North America and 46.7% in Europe. Revenue generated in India and Colombia was insignificant and is included in the North America total, but now includes our recent acquisition of Eleviant in late 2022, and we expect this to increase in future years. One client, IBM, accounted for greater than 10% of CTG’s consolidated revenue in 2022.

5

Revenue Recognition and Backlog

The Company recognizes revenue when control of the promised good or service is transferred to clients, in an amount that reflects the consideration the Company expects to be entitled to in exchange for those goods or services. For time-and-material contracts, revenue is recognized as hours are incurred and costs are expended. For contracts with progress billing schedules, primarily monthly, revenue is recognized as services are rendered to the client. Revenue for fixed-price contracts is recognized over time using an input-based approach. Over time revenue recognition best portrays the Company’s performance in transferring control of the goods or services to the client. On most fixed-price contracts, revenue recognition is supported through contractual clauses that require the client to pay for work performed to date, including cost plus a reasonable profit margin, for goods or services that have no alternative use to the Company. On certain contracts, revenue recognition is supported through contractual clauses that indicate the client controls the asset, or work in process, as the Company creates or enhances the asset. On a given project, actual salary and indirect labor costs incurred are measured and compared with the total estimate of costs of such items at the completion of the project. Revenue is recognized based upon the percentage-of-completion calculation of total incurred costs to total estimated costs. The Company infrequently works on fixed-price projects that include significant amounts of material or other non-labor related costs that could distort the percent complete within a percentage-of-completion calculation. The Company’s estimate of the total labor costs it expects to incur over the term of the contract is based on the nature of the project and our experience on similar projects, and includes management judgments and estimates that affect the amount of revenue recognized on fixed-price contracts in any accounting period. Losses on fixed-price projects are recorded when identified.

The Company’s revenue from contracts accounted for under time-and-material, progress billing, and percentage-of-completion methods as a percentage of consolidated revenue for the three years ended December 31, 2022, 2021, and 2020 was as follows:

|

|

2022 |

|

|

2021 |

|

|

2020 |

|

|||

Time-and-material |

|

|

76.1 |

% |

|

|

79.8 |

% |

|

|

81.0 |

% |

Progress billing |

|

|

19.1 |

% |

|

|

17.8 |

% |

|

|

15.9 |

% |

Percentage-of-completion |

|

|

4.8 |

% |

|

|

2.4 |

% |

|

|

3.1 |

% |

Total |

|

|

100.0 |

% |

|

|

100.0 |

% |

|

|

100.0 |

% |

As of December 31, 2022 and 2021, the backlog for fixed-price and all managed-support contracts was approximately $47.6 million and $68.5 million, respectively. Approximately 69% or $32.9 million of the December 31, 2022 backlog is expected to be earned in 2023. Approximately 47% of the $68.5 million of backlog at December 31, 2021, or $32.1 million, was earned in 2022. Revenue is subject to slight seasonal variations, with a minor slowdown and a decrease in billable resource utilization in months of high vacation and legal holidays (July, August, and December). Backlog does not tend to be seasonal; however, it does fluctuate based upon the timing of entry into long-term contracts.

Competition

The IT services market, for both information and technology solutions and IT and professional staffing services, is highly competitive. The market is also highly fragmented with many providers and no single competitor maintaining clear market leadership. Competition varies by location, the type of service, and the client to whom services are provided. The Company’s competition comes from four major channels: large national or international companies, including major accounting and consulting firms and large companies headquartered in India; hardware vendors and suppliers of packaged software systems; small local firms or individuals specializing in specific programming services or applications; and from a client’s internal IT staff. CTG competes against all four of these channels for its share of the market. The Company believes that to compete successfully, it is necessary to have a local geographic presence, offer appropriate IT solutions, provide skilled professional resources, and price its services competitively.

Intellectual Property

The Company has registered its symbol and logo with the U.S. Patent and Trademark Office and has taken steps to preserve its rights in other countries where it operates. We regard patents, trademarks, copyrights and other intellectual property as important to our success, and we rely on them in the United States and foreign countries to protect our investments in products and technology. Our patents expire at various times, but we believe that the loss or expiration of any individual patent would not materially affect our business. We, like any other company, may be subject to claims of alleged infringement of the patents, trademarks and other intellectual property rights of third parties from time to time in the ordinary course of business. CTG has entered into agreements with various software and hardware vendors from time to time in the normal course of business, and has capitalized certain costs under software development projects.

6

Human Capital Resources

Employees

CTG’s business depends on the Company’s ability to attract, develop and retain qualified professional staff to execute our strategy and provide services to its clients. The Company has a structured recruiting organization that works with its clients to meet their requirements by recruiting, retaining, and providing high quality, motivated staff. As the Company works with a number of subcontractors, the Company includes subcontractors in its total headcount, which equals approximately 3,200 total resources worldwide, with approximately 1,800 in North America, South America and India, with the remaining 1,400 in Europe as of December 31, 2022. Of these resources, approximately 86% are IT professionals and 14% are individuals who work in sales, recruiting, delivery, administrative and support positions. The Company believes that its relationship with its employees is good and supported by the Company’s 2022 recognition as a Great Place to Work® in nearly all eligible countries in which we operate. No employees are covered by a collective bargaining agreement or are represented by a labor union. CTG is an equal opportunity employer.

In 2022, we focused on adding additional staff with IT Solutions backgrounds in both North America and Europe to drive our IT Solutions and Services segments in line with our business strategy. Employees are encouraged to learn and grow their careers, by using our internal learning tools to complete classes or reach certifications, externally through classes primarily to achieve certifications, or through external classes paid for in part or in full through a tuition reimbursement program.

Social Responsibility

Our social responsibility principles inform the way we work. CTG is committed to the highest standards in our labor practices, the health and safety of our employees, and business ethics.

CTG has business operations in North America, Western Europe, India and Colombia, all regions with strict labor laws regarding human rights. We have internal policies intended to ensure our compliance with these laws, and we will not knowingly conduct business with anyone who violates these laws or basic human rights. We are committed to adhering to the Fair Labor Standards Act (“FLSA”), local labor laws, and prevailing wage rates. CTG prohibits any form of workplace or sexual harassment, and all employees are required to work in a manner that prevents harassment in the workplace. This policy is one component of CTG’s commitment to a discrimination-free work environment.

None of CTG’s leased office space is subject to industrial hazards and all adhere to the Occupational Safety and Health Administration (“OSHA”) office standards. We will not knowingly transact business with, or place our team members at, companies that do not enforce appropriate workplace safety and health standards.

Our Code of Business Conduct serves as our baseline for business ethics, and all employees are required to adhere to these guidelines. We are committed to providing clients with high-quality services that conform to mutually agreed-upon requirements and maintain certifications that support our Quality Policy, including ISO 9001:2015 certification for our European operations.

CTG Luxembourg PSF holds the “Entreprise Socialement Responsable” (Socially Responsible Enterprise) label that is awarded by the INDR Luxembourg (Institut National pour le Développement Durable et la Responsabilité Sociale des Entreprises), an organization that aims to promote responsible business practices in Luxembourg.

Our whistleblower hotline ensures that there is a confidential way to report any concerns with CTG business practices. Specific to CTG Luxembourg, PSF S.A., we have complaint handling (traitement des réclamations) processes for clients, in accordance with the Commission de Surveillance du Secteur Financier's (CSSF) Regulation 16-07 and Circular 17/671.

Environmental Responsibility

CTG maintains a relatively small carbon/environmental footprint. As a professional services provider, much of our focus is on the individual behavior of our team members and the decisions we make in managing our office spaces. Our environmental strategy has three areas of focus:

Personal Initiative

Many of our improvements come from our employee's environmentally conscious efforts. CTG supports these efforts by:

7

Corporate Contracts and Purchasing

CTG is committed to doing business with companies that share our environmental concern. Examples include purchasing environmentally-friendly products and prioritizing property management companies and office spaces that utilize environmentally friendly materials, policies, and services.

Corporate Stewardship

We are conscious of our impact on the communities our teams call home. Over the years, we have made significant improvements that support reducing the carbon/environmental footprint of our North American corporate headquarters, located in Amherst, New York. In all locations, we are committed to ensuring that none of our outdated computer systems and electronics end up in landfills and that our office waste be disposed of through local energy-from-waste programs.

Available Company Information

The Company’s annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 (Exchange Act), and reports filed under Section 16 of the Exchange Act are available without charge on the Company’s website at www.ctg.com as soon as reasonably practicable after such reports are filed with, or furnished to, the SEC. The Company’s code of ethics (Code of Business Conduct), committee charters and governance policies (including a fraud and insider trading policy) are also available without charge on the Company’s website at https://investors.ctg.com/corporate-governance/governance-documents. If applicable, the Company intends to disclose future amendments to, or waivers from, certain provisions of the Code of Conduct on the Company's website or in a current report on Form 8-K. The information on our website is not part of this Annual Report on Form 10-K. Additionally, the SEC’s website, www.sec.gov, contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC.

8

Item 1A. Risk Factors

The following risk factors should be read carefully in connection with evaluating our business and the forward-looking information contained in this Annual Report on Form 10-K. The risk factors below represent what we believe are the known material risk factors with respect to the Company and our business, but are not the only risks we face. Additional risks unknown to us or that we currently believe are insignificant may also affect our business. Any of the risks described below or elsewhere in this Annual Report on Form 10-K or our other filings with the SEC could materially adversely affect our business, operations, financial position or future financial results.

Business Related Risks

Our business depends on the availability of a large number of highly qualified IT professionals, sales and management personnel, and our ability to recruit and retain these individuals.

We actively compete with many other IT service providers for qualified personnel, including professional IT staff, recruiters, sales and business development specialists, and management. The Company is experiencing significant competition for qualified resources due to a general shortage of available IT digital solutions talent. We believe this competition will continue in the future, and it may have a negative impact on the Company’s operating results if we are unable to hire the resources we need to meet the requirements from our clients on a timely basis.

The availability of qualified personnel may affect our ability to provide services and meet the requirements of our clients. An inability to fulfill client requirements at agreed-upon rates due to a lack of available qualified personnel may adversely affect our revenue and operating results in the future.

The Company also continues to experience wage inflation globally, making hiring and retaining key personnel difficult. Continued increases in wage requirements may reduce operating profits if the Company is unable to pass such increases along to clients. Additionally, the turnover of employees is disruptive to providing our services to clients and may impact our ability to complete engagements as required, impacting our operating results and our reputation as a digital IT Solutions provider, which may in turn impact our ability to win future engagements.

Our business long-term strategy to disengage from Non-Strategic Technology Services could have an adverse effect on our revenue and operating results if not successfully executed.

During the fourth quarter of 2021, the Company further refined its strategy to focus on providing digital services within its IT Solutions and Services businesses in both North America and Europe. As part of this process, the Company determined that there are certain lower-margin staffing services accounts within its business that are no longer part of the Company’s long-term business plans. The Company’s inability to successfully execute on its strategy of disengaging from its lowest margin staffing services, Non-Strategic Technology Services, may negatively impact revenue and operating results.

Decreases in demand for our services in the future would have an adverse effect on our revenue and operating results.

The Company’s revenue and operating results are significantly impacted by changes in demand for its services. In the past, when global economic conditions declined, there was a significant decrease in demand for the Company’s services, which negatively affected the Company’s revenue and operating results as compared with prior years. Declines in demand for our IT services in 2023 or future years would adversely affect our revenue and operating results as it has in the past.

Our client contracts generally have a short term or are terminable on short notice, and a significant number of failures to renew contracts in place, or early terminations or renegotiations of our existing client contracts could adversely affect our results of operations.

Our clients typically retain us on a non-exclusive, engagement-by-engagement basis, rather than under exclusive long-term contracts. We performed 76.1% of our services on a time-and-materials basis during 2022. As such, our clients generally have the right to terminate a contract with us upon written notice without the payment of any financial penalty. Client projects may involve multiple engagements or stages, and there is a risk that a client may choose not to retain us for additional stages of a project, or that a client will cancel or delay additional planned engagements. These terminations, cancellations, or delays could result from factors that are beyond our control and are unrelated to our work product or the progress of the project but could be related to business or financial conditions of the client, changes in client strategies or the economy in general. When contracts are terminated, we lose the anticipated future revenue, and we may not be able to eliminate the associated costs that would have been required to support those contracts in a timely manner.

9

Consequently, our operating results in subsequent periods may be lower than expected. Our clients can cancel or reduce the scope of their engagements with us on short notice. If they do so, we may be unable to reassign our professionals to new engagements without delay. The cancellation or reduction in scope of an engagement could, therefore, reduce the utilization rate of our professionals, which would have a negative impact on our business, financial condition, and results of operations. As a result of these and other factors, our past financial performance should not be relied on as a guarantee of similar or improved future performance. Due to these factors, we believe that our results from operations in the future may fluctuate from period to period.

Cyber Related Risks

We could be subject to liability and damage to our reputation resulting from cyber-attacks or data breaches.

Cyber risks for companies providing global IT and professional services, especially in regulated industries, continue to increase. This increase in risk may be attributed to the increasing value and dependence on data, including organizations’ intellectual property and citizens’ personal data that could be misused for identity theft and fraud. While the value and dependence of data has increased, likewise the reliance on electronic communications, mobile technologies, social networking, hybrid and cloud-based resources, smart devices, and emerging technologies continues to grow. In most regions, the regulatory compliance requirements surrounding data protection and privacy have also increased. In addition, the sophistication, motivation, and organization of cyber-attacks continues to evolve, as does the sophistication of threat actors such as organized crime, hackers, terrorists, activists, insider threats, and foreign governments.

The Company’s business, operations, and its clients rely on the secure processing, transmission, storage, integrity, and availability of data, services, and resources provided by its IT environments and operational processes. The Company’s complex IT environments and variety of delivery services support a wide range of technologies, industries, regulatory compliance requirements, and clients globally.

Although the Company has not experienced any prior material data breaches, regulatory non-compliance incidents, or cyber security incidents, its environments may be impacted by cyber-attacks or cyber security incidents caused via the aforementioned threat actors, the Company's personnel, or the Company’s third party providers. These incidents could result in data loss, the disruption or loss of the Company's internal or client-supporting operations and services, adversely affect the Company’s adherence with regulatory requirements, or result in a data breach. Data losses and data breaches could include the unauthorized disclosure, misuse, loss, and destruction of both the Company’s and its clients’ intellectual property, financial information, or other regulated or privacy-related information. This includes but is not limited to United States personally identifiable information (PII), personal data under the European General Data Protection Regulation (GDPR), data covered under Luxembourg Law on the Financial Sector, protected health information (PHI) under the United States Health Insurance Portability and Accountability Act of 1996 (HIPAA), and data covered under the increasing number of U.S. state privacy and data breach laws, and other countries’ privacy laws.

The Company’s failure to protect sensitive data and address the regulatory compliance requirements of data and associated internal or delivery services under the Company’s control could result in reputational damage, fines and penalties, litigation costs, external investigations, compensation costs including reimbursement and monetary awards, prohibition of providing services in a region or industry, and/or additional compliance and remediation costs that could have a material, adverse impact on the Company's operations. It could also have an adverse impact on the Company’s ability to maintain and execute new contracts with clients that produce or work with similar data, and make it more difficult to retain and recruit qualified personnel to perform its services in the future. As cyber threats continue to become more sophisticated and the regulatory compliance and privacy landscape continues to evolve resulting in changes to the Company’s risk profile, the Company may be required to expend and invest in additional resources, personnel, and technologies to enhance and implement new risk mitigation strategies.

Competition Related Risks

Increased competition and the bargaining power of our large clients may cause our billing rates to decline, which would have an adverse effect on our revenue and, if we are unable to control our personnel costs accordingly, on our margins and operating results.

We have experienced reductions in the rates we bill a number of our larger clients for services due to highly competitive market conditions. Additionally, we actively compete against many other companies for business at both new and existing clients. Billing rate reductions or competitive pressures may lead to a decline in revenue. When faced with such pressures, if we are unable to make commensurate reductions in our personnel costs, our margins and operating results would be adversely affected.

10

Existing and potential clients may outsource or consider outsourcing their IT requirements to foreign countries in which we may not currently have operations, which could have an adverse effect on our ability to retain existing clients or obtain new clients.

In recent years, more companies are using, or are considering using, low-cost offshore outsourcing centers to perform technology-related work and complete projects. Currently, we have partnered with clients to perform services outside of North America in both India and Colombia to mitigate and reduce this risk to our Company. However, the risk of additional outsourcing of IT solutions overseas to countries where we do not have operations could have a material, adverse impact on our future operations.

The IT services industry is highly competitive and fragmented, which means that our clients have a number of choices for providers of IT services, and we may not be able to compete effectively.

The market for our services is highly competitive. Moreover, the market is fragmented, and no company holds a dominant position. Accordingly, our competition for client requirements and experienced personnel varies significantly by geographic area and by the type of service provided. Some of our competitors are larger and have greater technical, financial, and marketing resources, and greater name recognition than we have in the markets we collectively serve. In addition, clients may elect to increase their internal IT system resources to satisfy their custom software development and integration needs. Finally, our industry is being impacted by the growing use of lower-cost offshore delivery capabilities (primarily India and other parts of Asia). There can be no assurance that we will be able to continue to compete successfully with existing or future competitors or that future competition will not have a material adverse effect on our results of operations and financial condition.

The introduction of new IT services or changes in client requirements for IT services may render our existing offerings obsolete or unnecessary, which, if we are unable to keep pace with these corresponding changes, could have an adverse effect on our business.

Our success depends, in part, on our ability to implement and deliver services that anticipate and keep pace with rapid and continuing changes in technology, industry standards, and client preferences and requirements. We may not be successful in anticipating or responding to these developments on a timely basis, and our offerings may not be successful in the marketplace. Also, services, solutions, and technologies developed by our competitors may make our solutions or staffing offerings uncompetitive or obsolete. Any one of these circumstances could have a material adverse effect on our ability to obtain and successfully complete client engagements.

Operations Related Risks

We derive a significant portion of our revenue from one client, and a significant reduction in the amount of requirements requested by this client would have an adverse effect on our revenue and operating results.

IBM is CTG’s largest client, and we provide services to various IBM divisions in a number of locations. The National Technical Services Agreement (NTS Agreement) with IBM expires on October 27, 2023. In 2022, 2021, and 2020, IBM accounted for $57.1 million or 17.6%, $74.8 million or 19.1%, and $77.5 million or 21.2% of the Company’s consolidated revenue, respectively. The Company’s accounts receivable from IBM at December 31, 2022 and 2021 totaled $14.0 million and $8.9 million, respectively.

If we are unable to bill for our services or collect our receivables, our results of operations, financial condition, and cash flows could be adversely affected.

Our business depends on our ability to obtain payment from our clients of the amounts they owe us for work performed. We evaluate the financial condition of our clients and typically bill and collect on reasonable cycles. However, we might not accurately assess the creditworthiness of our clients, or macroeconomic conditions could result in financial difficulties for our clients, including bankruptcy and insolvency. In certain industries, some clients have requested longer payment terms, which has adversely affected, and may continue to adversely affect, our cash flows. The timely collection of client balances also depends on our ability to complete our contractual commitments as required. If we are unable to meet our commitments or bill our clients on a timely basis, our results of operations and cash flows could be adversely affected. We have established allowances for losses of receivables and unbilled services where we deem amounts to be uncollectible. The actual uncollectible amounts from clients could differ from those that we currently anticipate and have reserved for.

11

If we repatriate our cash balances from our foreign operations, we may be subject to additional tax liabilities.

We earn a portion of our operating income outside of the United States, and any repatriation or deemed repatriation of funds currently held in foreign jurisdictions to the United States may result in additional tax liabilities for the Company. In addition, there have been changes to the tax laws in the United States that impact how United States-based multinational corporations are taxed on foreign earnings. Any further changes in these tax laws could have a material adverse impact on our tax expense and cash flows.

Ineffective internal controls could affect the Company's business and operating results.

The Company's internal control over financial reporting may not prevent or detect misstatements because of the inherent limitations of internal controls, including the possibility of human error, the circumvention or overriding of controls, poorly designed or ineffective controls, or fraud. Internal controls that are deemed effective can provide only reasonable assurance with respect to the preparation and fair presentation of the Company's consolidated financial statements. If the Company fails to maintain the adequacy of its internal controls, including the failure to implement new or improve existing controls, or fails to properly execute or properly test these controls, the Company's business and operating results could be adversely impacted and the Company could fail to meet its financial reporting obligations.

Changing economic conditions and the effect of such changes on accounting estimates could have a material impact on our results of operations.

The Company has made a number of estimates and assumptions relating to the reporting of its assets and liabilities and the disclosure of contingent assets and liabilities to prepare its consolidated financial statements pursuant to the rules and regulations of the SEC and other accounting rulemaking authorities. Such estimates primarily relate to the valuation of stock options for recording equity-based compensation expense, allowances for credit losses, investment valuation, discount rates associated with pension plans, incurred but not recorded claims related to the Company's self-insured medical plan, valuation allowances for deferred tax assets, goodwill, acquisition and related accounting, legal matters, other contingencies and estimates of progress toward completion and direct profit or loss on contracts, as applicable. As future events and their effects cannot be determined with precision, actual results could differ from these estimates. Changes in the economic climates in which the Company operates may affect these estimates and will be reflected in the Company’s consolidated financial statements in the event they occur. Such changes could result in a material impact on the Company’s results of operations.

An impairment of our long-lived assets, including goodwill, could have a material non-cash adverse impact on our results of operations.

As of December 31, 2022, the Company carried a goodwill balance of $36.0 million. The Company assesses goodwill for impairment when events or circumstances indicate that the carrying value may not be recoverable, or at a minimum, on an annual basis. The valuation of goodwill depends on a variety of factors, including the success of the Company’s business, global market and economic conditions, earnings growth and expected cash flows. Impairments to goodwill and other intangible assets may be caused by factors outside the Company’s control, such as increasing competitive pricing pressures, changes in foreign currency exchange rates, lower than expected sales and profit growth rates, and various other factors. Significant and unanticipated changes could require a non-cash charge for impairment in a future period, which may significantly affect the Company’s results of operations in the period of such change.

Global Pandemic and Related Risks

The impact of the COVID-19 pandemic has had, and may continue to have, an adverse effect on our business and our financial results.

The COVID-19 pandemic has negatively affected the global economy, disrupted consumer spending and global supply chains, and created significant volatility and disruption of financial markets. The COVID-19 pandemic has had and may to continue to have an adverse effect on our business and financial performance. The extent of any further lingering impacts of the COVID-19 pandemic on our business, including our ability to execute our business strategies as planned, are uncertain and cannot be predicted.

Our business, financial condition and results, cash flows and liquidity and results of operations could be materially and adversely affected by any such future developments.

12

Regulatory or Legislative Related Risks

Our business is subject to economic, political, regulatory and other risks associated with domestic and international operations which could have an adverse effect on our operating results if we are unable to mitigate or hedge these risks.

We have operations in the United States and Canada in North America, in Belgium, Luxembourg, France, and the United Kingdom in Europe, in India, and in Colombia. Although our foreign operations conduct their business in their local currencies, these operations are subject to their own currency fluctuations, legislation, employment and tax law changes, and economic climates. As they relate to our foreign operations, these factors are different from those of the United States. Although we actively manage these foreign operations with local management teams, our overall operating results may be negatively affected by local economic conditions, changes in foreign currency exchange rates, or tax, regulatory or other economic changes beyond our control.

Our foreign operations will continue to expose us to foreign currency exchange rate fluctuations, including the impact of the significant decline in the value of the Euro on the Company's consolidated operating results. The future impact of foreign currency exchange rate fluctuations on our results of operations cannot be accurately predicted. Accordingly, there can be no assurance that foreign currency exchange rates:

• will be stable in the future;

• can be mitigated with currency hedging or other risk management strategies; or

• will not have a material adverse effect on our business, operating results and financial condition.

In addition, any widespread outbreak of an illness, pandemic or other local or global health issue (including COVID-19), natural disasters, climate change impacts, economic weakness, including continued inflation or a recession, or uncertain political climates, international hostilities including recent developments in China and war, such as the conflict between Russia and Ukraine, or any terrorist activities, could adversely affect customer demand, the Company’s operations, and its ability to source and deliver services to its customers, which could have a material adverse effect on the Company’s financial results. The Company continues to monitor the impact that Brexit has had on its operations. To date, there has been a nominal impact on the Company’s operating results from Brexit. As the total revenue generated by our British subsidiary is immaterial as compared with the Company’s total consolidated revenue, we do not expect the nominal impact the exit has had on the Company’s operations to date to change in the foreseeable future. Furthermore, although we have no operations directly in the Ukraine, the global economy has been negatively impacted by the military conflict there, which in part has exacerbated inflationary conditions in North America and Western Europe where we conduct nearly all our operations. Macroeconomic conditions continue to also impact the global economy. The scope and duration of these conditions is uncertain. However, the Company is already seeing an impact through its clients delaying IT purchasing decisions and increasing labor and other costs. These conditions may have a significant negative impact on the Company’s operating results in the future if they continue to persist.

All of these factors are outside of our control, but may nonetheless harm our future results and cause us to adjust our strategy in order to compete effectively.

Increased focus and expectations on climate change and other ESG matters could have a material adverse effect on our business, financial condition and results of operations and damage our reputation.

An increase in focus on ESG matters by institutional investors, governmental and non-governmental organizations, consumers, shareholders, communities, and other stakeholders and the related expectations could have a material, adverse effect on our business, financial condition and results of operations and our reputation. These trends have led to, among other things, increased public and private social accountability reporting requirements relating to labor practices, climate change, and other ESG matters and thus greater demands on our solutions and services. The increased focus may also lead to new regulations and client, shareholder and consumer demands that could require us to incur additional costs or make changes to our operations to comply with these regulations. We expect that these trends will continue. If we are unable to adequately respond to, or we are not perceived as adequately responding to, existing or new requirements or demands, clients may choose to obtain services from a competitor.

Government cuts in healthcare programs, such as Medicare, and delays in legislative or regulatory healthcare mandates could cause a reduction in IT spending by our healthcare clients, which could materially and adversely affect our revenue and results of operations.

The Company’s growth efforts include a focus on the healthcare market. Growth in this market depends on continued spending by our healthcare clients on IT projects. Cuts in government healthcare programs, such as sequestration, which has periodically cut Medicare reimbursements to hospitals and health systems, may result in reduced expenditures by our healthcare clients on IT projects. If additional government cuts in healthcare programs occur, whether due to the failure of Congress to adopt a budget, pass appropriations bills or raise the U.S. debt ceiling or for

13

other reasons, there may be delays, reductions or cessation of funding to our clients, which could cause our clients to purchase less IT services from us, and materially and adversely affect our revenue and results of operations.

In addition, delays in implementation of legislative or regulatory healthcare mandates could adversely affect the IT spending by our healthcare clients to implement such mandates. If the implementation of existing or contemplated legislative or regulatory healthcare mandates are deferred, the resulting reduction in IT spending by our healthcare clients could materially and adversely affect our revenue and results of operations.

Changes in government regulations and laws affecting the IT services industry, and the industries in which our clients operate, including accounting principles and interpretations, and the taxation of domestic operations could adversely affect our results of operations.

Changing laws, regulations and standards relating to corporate governance and public disclosure, including new SEC regulations, create uncertainty for companies such as ours. These laws, regulations, and standards are subject to varying interpretations which, in many instances, is due to their lack of specificity. As a result, the application of these standards and regulations in practice may evolve over time as new guidance is provided by regulatory and governing bodies. This could result in continuing uncertainty regarding compliance matters and higher costs necessitated by ongoing revisions to disclosure and governance practices. We are committed to maintaining high standards of corporate governance and public disclosure. As a result, our efforts to comply with evolving laws, tax regulations and other standards have resulted in, and are likely to continue to result in, increased general and administrative expenses and a diversion of management time and attention from revenue-generating activities to compliance activities.

The Financial Accounting Standards Board (FASB), the SEC, and the Public Company Accounting Oversight Board (PCAOB) or other accounting rule making authorities have issued and may continue to issue new accounting rules or auditing standards that are different from those that we presently apply to our financial results. Such new accounting rules or auditing standards could require significant changes from the way we currently report our financial condition, results of operations or cash flows.

U.S. generally accepted accounting principles have been the subject of frequent changes in interpretations, and the frequency of future accounting policy changes may accelerate. Such future changes in financial accounting standards may have a significant effect on our reported results of operations, including results of transactions entered into before the effective date of the changes.

We are subject to income and other taxes in the United States (federal and state) and numerous foreign jurisdictions. Our provisions for income and other taxes and our tax liabilities in the future could be adversely affected by numerous factors. These factors include, but are not limited to, income before taxes being lower than anticipated in countries with lower statutory tax rates and higher than anticipated in countries with higher statutory tax rates, changes in the valuation of deferred tax assets and liabilities, and changes in various federal, state and international tax laws, regulations, accounting principles or interpretations thereof, which could adversely impact our financial condition, results of operations, and cash flows in future periods.

Acquisition Related Risks

Risks to the Company from acquisitions include integration challenges, disruptions of the Company's core business, a failure to achieve objectives, and the assumption of liabilities.

The Company regularly evaluates acquisitions to aid the Company's growth in revenue and profits by expanding the services the Company offers in the geographies in which the Company operates, and its client base. Acquisitions often present significant challenges and risks relating to the integration of the business into the Company, and there can be no assurances that the Company will manage acquisitions successfully, that the Company's core business will not be significantly disrupted after an acquisition is finalized, or that strategic acquisition opportunities will be available to the Company on acceptable terms. The risks from an acquisition include the Company failing to achieve strategic objectives and anticipated revenue and profit improvements, borrowing a significant amount of money to fund the acquisitions which creates financial stress for the Company's operations, as well as failing to retain the key personnel of the acquired business. Additionally, failure to meet financial objectives of an acquisition could lead to impairment charges of intangible assets and goodwill in future periods. Finally, the assumption of liabilities related to litigation or other legal proceedings involving the acquired business may present a significant risk.

14

Capital Resources Related Risks

We may require additional capital to support our business, and this capital may not be available to us on acceptable terms, if at all.

The Company entered into an asset-based lending revolving credit agreement (Credit Agreement) during the 2021 second quarter, which has a five-year term that expires in May 2026, replacing its previous agreement. Under this Credit Agreement, the Company can borrow up to $50.0 million depending on collateral availability. The Credit Agreement is collateralized by the Company’s accounts receivable in the United States, Belgium, and Luxembourg. The London Interbank Offered Rate (“LIBOR”), the interest rate benchmark used as a reference rate on our Credit Agreement, began being phased out at the beginning of calendar year 2022, with the one-month LIBOR scheduled to cease immediately after June 30, 2023. A reference rate based on the Secured Overnight Financing Rate (“SOFR”), and other alternative benchmark rates, are replacing LIBOR. Interest rates range from 1.5% to 2.0% over SOFR or EURIBOR loans, and 0.5% to 1.0% over base rate (prime rate) loans. The Company can borrow under the agreement at either rate at its discretion. It is possible that the volatility of and uncertainty around SOFR as a LIBOR replacement rate and the applicable credit adjustment as well as rising interest rates would result in higher borrowing costs for us, and would adversely affect our liquidity, financial condition, and earnings. The Company’s previous Credit and Security Agreement was terminated during the 2021 second quarter.

At December 31, 2022, we had no borrowings outstanding under our revolving credit facility. The Company may be dependent on our revolving credit facility to meet working capital and operational requirements, and access to our facility is dependent on, among other things, compliance with applicable covenants, including fixed charge coverage ratio, consolidated earnings before interest, taxes, depreciation, and amortization (EBITDA) targets, and a limit on annual expenditures for property, plant, equipment, and capitalized software. The fixed charge coverage ratio is only tested if availability on a measurement date is below a threshold. The amount available for borrowing under the revolving credit facility could be significantly reduced due to poor operational performance, or other factors. Any loss or material reduction of our ability to access funds under the revolving credit facility could materially and negatively impact our liquidity.

Risk from Activist Shareholders

Actions of activist stockholders could cause us to incur substantial costs, divert management’s and the board’s attention and resources, and have an adverse effect on our business and stock price.

From time to time, we may be subject to proposals by stockholders urging us to take certain corporate actions. If activist stockholder activities ensue, our business could be adversely affected as responding to proxy contests and reacting to other actions by activist stockholders can be costly and time-consuming, disrupt our operations, and divert the attention of management and our board of directors, all of which could interfere with our ability to execute our strategic plan. We may be required to retain the services of various professionals to advise us on activist stockholder matters, including legal, financial and communications advisors, the costs of which may adversely affect our financial results. In addition, the perceived uncertainties as to our future direction, strategy or leadership created as a consequence of activist stockholder initiatives may result in the loss of potential business opportunities, harm our ability to attract new investors, clients, and employees, and cause our stock price to experience periods of volatility or stagnation.

Share Price Related Risks

Our share price could fluctuate and be difficult to predict.

Our share price has fluctuated in the past and could continue to fluctuate in the future in response to various factors, including both external and internal, and those beyond our control. These factors may include, among others:

Item 1B. Unresolved Staff Comments

None.

15

Item 2. Properties

All of the Company locations, totaling approximately 23 sites, are leased facilities. Of the total locations, 11 of these are located in Europe in the countries of Belgium, Luxembourg, France and the United Kingdom, where our European operations support the Europe IT Solutions and Services segment. The Company has one location in Canada, five in India, one in Colombia, and the remaining locations are in the United States. All of these locations support the North America IT Solutions and Services segment. These facilities generally serve as sales and support offices and their size varies with the number of people employed at each office, ranging from approximately 100 to 23,000 square feet. The Company’s lease terms vary from periods of less than a year to fifteen years and typically have flexible renewal options. The Company believes that its leased facilities are adequate to support its current and anticipated future needs.

Item 3. Legal Proceedings

The Company and its subsidiaries are involved from time to time in various legal proceedings arising in the ordinary course of business. Although the outcome of lawsuits or other proceedings involving the Company and its subsidiaries cannot be predicted with certainty and the amount of any liability that could arise with respect to such lawsuits or other proceedings cannot be predicted accurately, management does not expect these matters, if any, to have a material adverse effect on the financial position, results of operations, or cash flows of the Company. See footnote 12 to the Company’s audited financial statements for the fiscal year ended December 31, 2022 included in Item 8, “Financial Statements and Supplementary Data.”

Item 4. Mine Safety Disclosures

Not applicable.

16

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Stock Market Information

The Company’s common stock is traded on The NASDAQ Stock Market LLC under the symbol CTG.

On March 10, 2023, there were 1,172 holders of record of the Company’s common shares. The Company currently does not pay a dividend. At December 31, 2022, under the terms of the Company's revolving credit facility, the Company is required to meet a financial covenant in order to pay dividends. The Company was in compliance with this financial covenant at December 31, 2022 and December 31, 2021. For additional information regarding these financial covenants, see Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations - Financial Condition and Liquidity." The determination of the timing, amount and the payment of dividends, if any, on the Company’s common stock in the future is at the discretion of the Board of Directors and will depend upon, among other things, the Company’s profitability, liquidity, financial condition, capital requirements, and compliance with the covenants under the Company's Credit Agreement. The Company currently has no intention to pay a dividend in the foreseeable future.

For information concerning common stock issued in connection with the Company’s equity compensation plans, see Item 12, “Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters.”

Issuer Purchases of Equity Securities

The Company’s Board of Directors has authorized the repurchase of its stock up to a total of $30.0 million. As of March 10, 2023, the Company had repurchased approximately $22.3 million shares pursuant to the authorization, leaving a remaining authorization of approximately $7.7 million. No shares were purchased during 2022 under this authorization.

The information below includes shares withheld by or surrendered to the Company to satisfy tax withholding obligations associated with employee equity awards. The information for the fiscal fourth quarter of 2022 is as follows:

|

|

|

|

|

|

|

|

Total Number |

|

|

Maximum |

|

||||

|

|

|

|

|

|

|

|

of Shares |

|

|

Dollar Amount |

|

||||

|

|

Total |

|

|

Average |

|

|

Purchased as |

|

|

that May Yet |

|

||||

|

|

Number |

|

|

Price |

|

|

Part of Publicly |

|

|

be Purchased |

|

||||

|

|

of Shares |

|

|

Paid per |

|

|

Announced Plans |

|

|

Under the Plans |

|

||||

Period |

|

Purchased |

|

|

Share* |

|

|

or Programs |

|

|

Or Programs |

|

||||

October 1 - October 31 |

|

|

— |

|

|

$ |

— |

|

|

|

— |

|

|

$ |

7,727,724 |

|

November 1 - November 30 |

|

|

— |

|

|

$ |

— |

|

|

|

— |

|

|

$ |

7,727,724 |

|

December 1 - December 31 |

|

|

— |

|

|

$ |

— |

|

|

|

— |

|

|

$ |

7,727,724 |

|

Total |

|

|

— |

|

|

$ |

— |

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

* Excludes broker commissions |

|

|

|

|

|

|

|

|

|

|

|

|

||||

17

Company Performance Graph

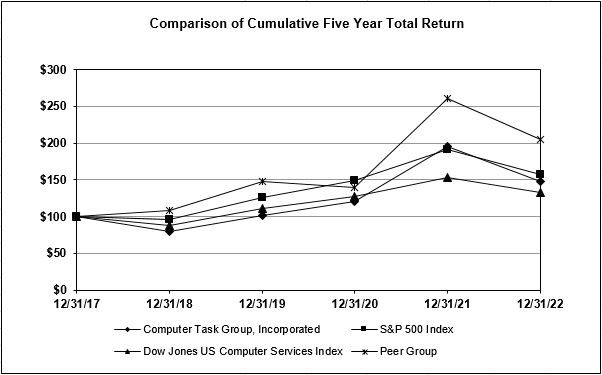

The following graph displays a five-year comparison of cumulative total shareholder returns for the Company’s common stock, the S&P 500 Index, the Dow Jones U.S. Computer Services Index, and a Peer Group, assuming a base index of $100 at the end of 2017. The cumulative total return for each annual period within the five years presented is measured by dividing (1) the sum of (A) the cumulative amount of dividends for the period, assuming dividend reinvestment, and (B) the difference between the Company’s share price at the end and the beginning of the period by (2) the share price at the beginning of the period. The calculations were made excluding trading commissions and taxes.

|

|

Base |

|

|

Indexed Returns |

|

||||||||||||||||||

|

|

December |

|

|

December |

|

|

December |

|

|

December |

|

|

December |

|

|

December |

|

||||||

|

|

2017 |

|

|

2018 |

|

|

2019 |

|

|

2020 |

|

|

2021 |

|

|

2022 |

|

||||||

Computer Task Group, Inc. |

|

$ |

100.00 |

|

|

$ |

80.00 |

|

|

$ |

101.57 |

|

|

$ |

120.00 |

|

|

$ |

195.49 |

|

|

$ |

148.24 |

|

S&P 500 Index |

|

$ |

100.00 |

|

|

$ |

95.62 |

|

|

$ |

125.72 |

|

|

$ |

148.85 |

|

|

$ |

191.58 |

|

|

$ |

156.88 |

|

Dow Jones U.S. Computer Services Index |

|

$ |

100.00 |

|

|

$ |

88.01 |

|

|

$ |

111.02 |

|

|

$ |

126.89 |

|

|

$ |

153.06 |

|

|

$ |

132.69 |

|

Peer Group |

|

$ |

100.00 |

|

|

$ |

108.05 |

|

|

$ |

148.02 |

|

|

$ |

139.96 |

|

|

$ |

260.91 |

|

|

$ |

204.66 |

|

Peer Group |

BGSF, Inc. |

Cross Country Healthcare, Inc. |

Huron Consulting Group Inc. |

Information Services Group, Inc. |

Mastech Digital, Inc. |

Perficient, Inc. |

PRGX Global, Inc. - included through March 3, 2021 when it was taken private |

RCM Technologies, Inc. |

The Hackett Group, Inc. |

The information included under this section entitled “Company Performance Graph” is deemed not to be “soliciting material” or “filed” with the SEC, is not subject to the liabilities of Section 18 of the Exchange Act, and shall not be deemed incorporated by reference into any of the filings previously made or made in the future by the Company under the Exchange Act or the Securities Act of 1933, except to the extent the Company specifically incorporates any such information into a document that is filed.

18

Item 6. [Reserved]

19

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Forward-Looking Statements

The following discussion should be read in conjunction with our Consolidated Financial Statements and related Notes contained in Part II, Item 8 of this report. This discussion contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated due to various factors discussed above under "Forward-Looking Statements" and under the caption "Risk Factors" in Part I, Item 1A of this report.

Industry Trends

The IT services industry is extremely competitive and characterized by continuous changes in client requirements and improvements in technologies. Our competition varies significantly by geographic region, as well as by the type of service provided. Many of our competitors are larger than CTG, and have greater financial, technical, sales, and marketing resources. In addition, the Company frequently competes with a client’s use of its own internal IT staff for projects. Our industry continues to be impacted by the use of lower-cost offshore delivery capabilities (primarily India and other parts of Asia). There can be no assurance that we will be able to continue to compete successfully with existing or future competitors or that future competition will not have a material adverse effect on our results of operations and financial condition.