DCP Midstream, LP - Annual Report: 2022 (Form 10-K)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||

For the fiscal year ended December 31, 2022

or

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||

For the transition period from to

Commission File Number: 001-32678

DCP MIDSTREAM, LP

(Exact name of registrant as specified in its charter)

| Delaware | 03-0567133 | |||||||

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

6900 E. Layton Ave, Suite 900 Denver, Colorado | 80237 | |||||||

| (Address of principal executive offices) | (Zip Code) | |||||||

Registrant’s telephone number, including area code: (303) 595-3331

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class: | Trading Symbol(s) | Name of Each Exchange on Which Registered: | ||||||||||||

| Common Units Representing Limited Partner Interests | DCP | New York Stock Exchange | ||||||||||||

| 7.875% Series B Fixed-to-Floating Rate Cumulative Redeemable Perpetual Preferred Units | DCP PRB | New York Stock Exchange | ||||||||||||

| 7.95% Series C Fixed-to-Floating Rate Cumulative Redeemable Perpetual Preferred Units | DCP PRC | New York Stock Exchange | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act:

None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Exchange Act of 1934, or the Act. Yes ý No¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Act during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and such files). Yes ý No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ý | Accelerated filer | ¨ | |||||||||||

| Non-accelerated filer | ¨ | Smaller reporting company | ¨ | |||||||||||

| Emerging growth company | ¨ | |||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial

1

reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report ý

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant

included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based

compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No ý

The aggregate market value of common units held by non-affiliates of the registrant on June 30, 2022, was approximately $2,680,617,000. The aggregate market value was computed by reference to the last sale price of the registrant’s common units on the New York Stock Exchange on June 30, 2022.

As of February 10, 2023, there were 208,550,632 common units representing limited partner interests outstanding.

DOCUMENTS INCORPORATED BY REFERENCE:

None

2

DCP MIDSTREAM, LP

FORM 10-K FOR THE YEAR ENDED DECEMBER 31, 2022

TABLE OF CONTENTS

| Item | Page | |||||||

| PART I | ||||||||

| 1 | Business | |||||||

| 1A. | Risk Factors | |||||||

| 1B. | Unresolved Staff Comments | |||||||

| 2 | Properties | |||||||

| 3 | Legal Proceedings | |||||||

| 4 | Mine Safety Disclosures | |||||||

| PART II | ||||||||

| 5 | Market for Registrant's Common Units, Related Unitholder Matters and Issuer Purchases of Common Units | |||||||

| 6 | [Reserved] | |||||||

| 7 | Management's Discussion and Analysis of Financial Condition and Results of Operations | |||||||

| 7A. | Quantitative and Qualitative Disclosures about Market Risk | |||||||

| 8 | Financial Statements and Supplementary Data | |||||||

| 9 | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | |||||||

| 9A. | Controls and Procedures | |||||||

| 9B. | Other Information | |||||||

| 9C. | Disclosure Regarding Foreign Jurisdictions that Prevent Inspections | |||||||

| PART III | ||||||||

| 10 | Directors, Executive Officers and Corporate Governance | |||||||

| 11 | Executive Compensation | |||||||

| 12 | Security Ownership of Certain Beneficial Owners and Management and Related Unitholder Matters | |||||||

| 13 | Certain Relationships and Related Transactions, and Director Independence | |||||||

| 14 | Principal Accountant Fees and Services | |||||||

| PART IV | ||||||||

| 15 | Exhibits and Financial Statement Schedules | |||||||

| 16 | Form 10-K Summary | |||||||

| Signatures | ||||||||

i

GLOSSARY OF TERMS

The following is a list of terms used in the industry and throughout this report:

| ASC | accounting standards codification | |||||||

| ASU | accounting standards update | |||||||

| Bbl | barrel | |||||||

| Bbls/d | barrels per day | |||||||

| Bcf | billion cubic feet | |||||||

| Bcf/d | billion cubic feet per day | |||||||

| Btu | British thermal unit, a measurement of energy | |||||||

| COBRA | Consolidated Omnibus Budget Reconciliation Act | |||||||

| Credit Agreement | Credit Agreement governing our Credit Facility | |||||||

| Credit Facility | Our $1.4 billion unsecured revolving credit facility, maturing March 18, 2027 | |||||||

| Fractionation | the process by which natural gas liquids are separated into individual components | |||||||

| GAAP | generally accepted accounting principles in the United States of America | |||||||

| LIBOR | London Interbank Offered Rate | |||||||

| MBbls | thousand barrels | |||||||

| MBbls/d | thousand barrels per day | |||||||

| MMBbls | million barrels | |||||||

| MMBtu | million Btus | |||||||

| MMBtu/d | million Btus per day | |||||||

| MMcf | million cubic feet | |||||||

| MMcf/d | million cubic feet per day | |||||||

| NGLs | natural gas liquids | |||||||

| OPEC | Organization of the Petroleum Exporting Countries | |||||||

| OPEC+ | OPEC members plus ten other oil producing countries | |||||||

| OPIS | Oil Price Information Service | |||||||

| Railroad Commission | the Railroad Commission of Texas | |||||||

| SEC | U.S. Securities and Exchange Commission | |||||||

| Securitization Facility | $350 million Accounts Receivable Securitization Facility, maturing August 12, 2024 | |||||||

| SOFR | Secured Overnight Financing Rate | |||||||

| TBtu/d | trillion Btus per day | |||||||

| Throughput | the volume of product transported or passing through a pipeline or other facility | |||||||

ii

CAUTIONARY STATEMENT ABOUT FORWARD-LOOKING STATEMENTS

Our reports, filings and other public announcements may from time to time contain statements that do not directly or exclusively relate to historical facts. Such statements are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. You can typically identify forward-looking statements by the use of forward-looking words, such as “may,” “could,” “should,” “intend,” “assume,” “project,” “believe,” “anticipate,” “expect,” “estimate,” “potential,” “plan,” “forecast” and other similar words.

All statements that are not statements of historical facts, including, but not limited to, statements regarding our future financial position, business strategy, budgets, projected costs and plans and objectives of management for future operations, are forward-looking statements.

These forward-looking statements reflect our intentions, plans, expectations, assumptions and beliefs about future events and are subject to risks, uncertainties and other factors, many of which are outside our control. Important factors that could cause actual results to differ materially from the expectations expressed or implied in the forward-looking statements include known and unknown risks. Known risks and uncertainties include, but are not limited to, the risks set forth in Item 1A. “Risk Factors” in this Annual Report on Form 10-K for the year ended December 31, 2022, including the following risks and uncertainties:

•the timing and completion of our pending merger with Phillips 66 pursuant to which Phillips 66 will acquire all of our issued and outstanding common units not already owned by DCP Midstream, LLC or its subsidiaries;

•conflicts of interest may exist between our individual unitholders and Phillips 66, which has the authority to conduct, direct and manage the activities of DCP Midstream, LLC associated with the Partnership and our general partner;

•risks related to the disruption of economies around the world including the oil, gas and NGL industry in which we operate and the resulting adverse impact on our business, liquidity, commodity prices, workforce, third-party and counterparty effects and resulting federal, state and local actions;

•the extent of changes in commodity prices and the demand for our products and services, our ability to effectively limit a portion of the adverse impact of potential changes in commodity prices through derivative financial instruments, and the potential impact of price, and of producers’ access to capital on natural gas drilling, demand for our services, and the volume of NGLs and condensate extracted;

•the demand for crude oil, residue gas and NGL products;

•the level and success of drilling and quality of production volumes around our assets and our ability to connect supplies to our gathering and processing systems, as well as our residue gas and NGL infrastructure;

•new, additions to, and changes in, laws and regulations, particularly with regard to taxes, safety, regulatory and protection of the environment, including, but not limited to, climate change legislation, regulation of over-the-counter derivatives markets and entities, and hydraulic fracturing regulations, or the increased regulation of our industry, including additional local control over such activities, and their impact on producers and customers served by our systems;

•other factors beyond our control including the increased cost of labor, contractors, services, supplies and materials due to persistent inflation;

•general economic, market and business conditions;

•the amount of natural gas we gather, compress, treat, process, transport, store and sell, or the NGLs we produce, fractionate, transport, store and sell, may be reduced if the pipelines, storage and fractionation facilities to which we deliver the natural gas or NGLs are capacity constrained and cannot, or will not, accept the natural gas or NGLs or we may be required to find alternative markets and arrangements for our natural gas and NGLs;

•our ability to continue the safe and reliable operation of our assets;

•our ability to grow through organic growth projects, or acquisitions, and the successful integration and future performance of such assets;

•our ability to access the debt and equity markets and the resulting cost of capital, which will depend on general market conditions, our financial and operating results, inflation rates, interest rates, our ability to comply with the covenants in our Credit Agreement or other credit facilities, and the indentures governing our notes, as well as our ability to maintain our credit ratings;

iii

•the creditworthiness of our customers and the counterparties to our transactions, including the impact of bankruptcies;

•the amount of collateral we may be required to post from time to time in our transactions;

•industry changes, including consolidations, alternative energy sources, technological advances, infrastructure constraints and changes in competition;

•our ability to construct and start up facilities on budget and in a timely fashion, which is partially dependent on obtaining required construction, environmental and other permits issued by federal, state and municipal governments, or agencies thereof, the availability of specialized contractors and laborers, and the price of and demand for materials;

•our ability to hire, train, and retain qualified personnel and key management to execute our business strategy;

•our ability to successfully manage our ongoing integration with Phillips 66;

•volatility in the price of our common units and preferred units;

•weather, weather-related conditions and other natural phenomena, including, but not limited to, their potential impact on demand for the commodities we sell and the operation of company-owned and third party-owned infrastructure;

•security threats such as terrorist attacks, and cybersecurity attacks and breaches, against, or otherwise impacting, our facilities and systems;

•our ability to obtain insurance on commercially reasonable terms, if at all, as well as the adequacy of insurance to cover our losses; and

•the factors generally described in “Item 1A. Risk Factors” in this report.

In light of these risks, uncertainties and assumptions, the events described in the forward-looking statements might not occur or might occur to a different extent or at a different time than we have described. The forward-looking statements in this report speak as of the filing date of this report. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by applicable securities laws.

iv

PART I

Item 1. Business

OVERVIEW

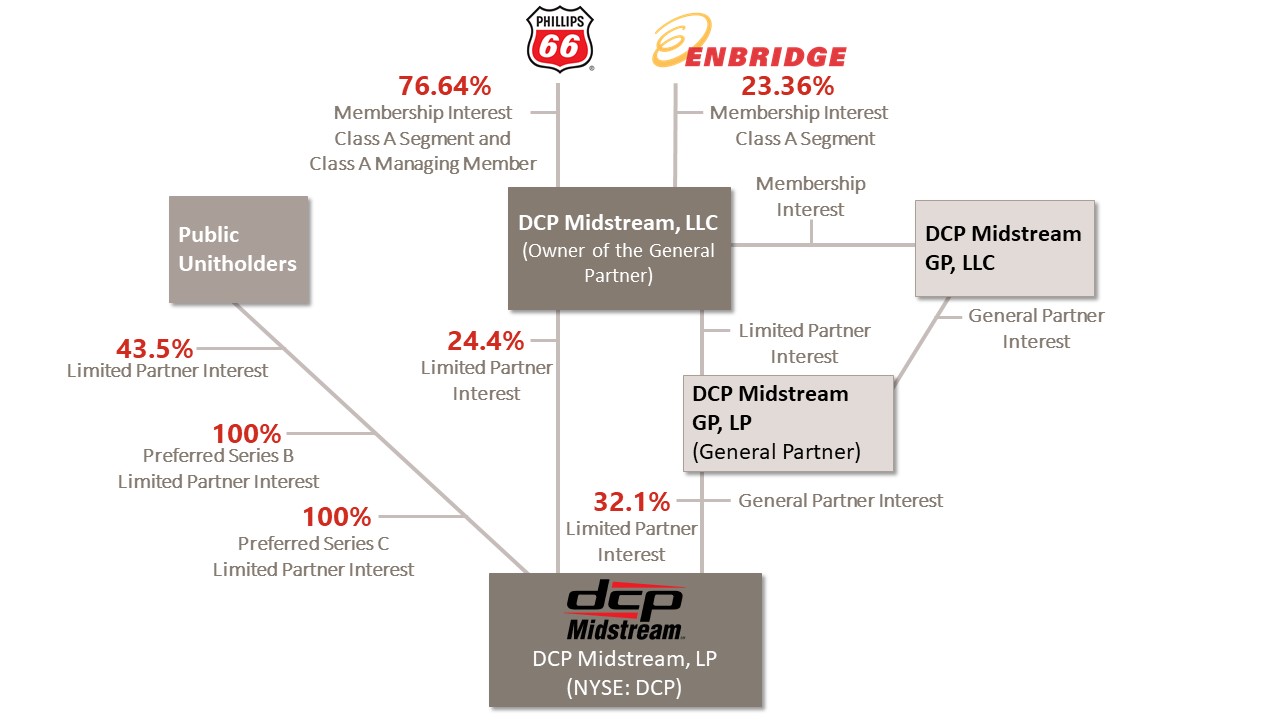

DCP Midstream, LP (together with its consolidated subsidiaries, “we,” “our,” “us,” the “registrant,” or the “Partnership”) is a Delaware limited Partnership formed in 2005 by DCP Midstream, LLC to own, operate, acquire and develop a diversified portfolio of complementary midstream energy assets. DCP Midstream, LLC and its subsidiaries and affiliates, collectively referred to as DCP Midstream, LLC is a joint venture between Phillips 66 and Enbridge, Inc. (“Enbridge”) that, prior to the realignment transaction in August of 2022 described below, was owned 50% by Phillips 66 and 50% by Enbridge.

Our operations are organized into two reportable segments: (i) Logistics and Marketing and (ii) Gathering and Processing. Our Logistics and Marketing segment includes transporting, trading, marketing, and storing natural gas and NGLs, and fractionating NGLs. Our Gathering and Processing segment consists of gathering, compressing, treating, and processing natural gas, producing and fractionating NGLs, and recovering condensate. The remainder of our business operations are presented as “Other,” and consist of unallocated corporate costs.

Realignment Transaction

On August 17, 2022, Phillips 66 and Enbridge, through their respective subsidiaries, entered into an Agreement and Plan of Merger for the purpose of realigning their respective economic and governance interests in the Partnership and Gray Oak Pipeline, LLC through the merger of DCP Midstream, LLC with another joint venture owned by Phillips 66 and Enbridge (the “Realignment Transaction”). In connection with the closing of the Realignment Transaction, Phillips Gas Company LLC, an indirect wholly owned subsidiary of Phillips 66 (“PGC”), and Spectra DEFS Holding, LLC, an indirect wholly owned subsidiary of Enbridge, as the members of DCP Midstream, LLC, entered into a Third Amended and Restated Limited Liability Company Agreement of DCP Midstream, LLC (the “Third A&R LLC Agreement”), which, among other things, designated PGC as the Class A Managing Member of DCP Midstream, LLC with the power to conduct, direct and manage all activities of DCP Midstream, LLC associated with the Partnership and each of its subsidiaries, DCP Midstream GP, LP (“GP LP”), our general partner, and DCP Midstream GP, LLC, the general partner of GP LP (the “General Partner”), and, in each case, the businesses, activities and liabilities thereof. The Third A&R LLC Agreement also provided PGC with the power to exercise DCP Midstream, LLC’s rights to appoint or remove any director on the board of directors of our General Partner and vote the common units representing limited partner interests in the Partnership that are owned directly or indirectly by DCP Midstream, LLC.

The diagram below depicts our organizational structure as of December 31, 2022.

1

Pending Merger with Phillips 66

On August 17, 2022, the board of directors of our General Partner received a non-binding proposal from Phillips 66 to acquire all of the Partnership’s issued and outstanding publicly-held common units not already owned by DCP Midstream, LLC or its subsidiaries at a value of $34.75 per common unit (the “Proposal”). The board of directors of our General Partner appointed the special committee to review, evaluate and negotiate the Proposal.

On January 5, 2023, we entered into an Agreement and Plan of Merger (the “Merger Agreement”) with Phillips 66, Phillips 66 Project Development Inc., a wholly owned subsidiary of Phillips 66 (“PDI”), Dynamo Merger Sub LLC, a wholly owned subsidiary of PDI (“Merger Sub”), GP LP and our General Partner, pursuant to which Merger Sub will merge with and into the Partnership, with the Partnership surviving as a Delaware limited partnership (the “Merger”). Under the terms of the Merger Agreement, at the effective time of the Merger, each common unit representing a limited partner interest in the Partnership (other than the common units owned by DCP Midstream, LLC and GP LP) will be converted into the right to receive $41.75 per common unit in cash, without interest. The Partnership’s Preferred Units will be unaffected by the Merger and will remain outstanding following the Merger.

The Merger Agreement and the transactions contemplated thereby, including the Merger, were unanimously approved on behalf of the Partnership by the special committee and the board of directors of our General Partner, which is the general partner of GP LP. The special committee, which is comprised of independent members of the board of directors of our general partner, retained independent legal and financial advisors to assist it in evaluating and negotiating the Merger Agreement and the Merger. Concurrently with the execution and delivery of the Merger Agreement, DCP Midstream, LLC and GP LP, which, together own greater than a majority of the common units representing limited partner interests in the Partnership, delivered a written consent to GP LP that was sufficient to approve the Merger Agreement and the Merger. The Merger is expected to close in the second quarter of 2023. Completion of the Merger is subject to certain customary conditions as set forth in the Merger Agreement. There can be no assurance that the Merger will be consummated on the terms described above or at all.

2

OUR BUSINESS STRATEGY

Our primary business objectives are to achieve sustained company profitability, a strong balance sheet and profitable growth. We intend to accomplish these objectives by prudently executing the following business strategies:

Operational Performance. We believe our operating efficiency and reliability enhance our ability to attract new natural gas supplies by enabling us to offer more competitive terms, services and service flexibility to producers. Our logistics assets and gathering and processing systems consist of high-quality, well-maintained facilities, resulting in low-cost, efficient operations. Our goal is to establish a reputation in the midstream industry as a reliable, safe and low cost supplier of services to our customers. We will continue to pursue incremental revenue, cost efficiencies and operating improvements of our assets through process and technology improvements. We seek to increase the utilization of our existing facilities by providing additional services to our existing customers, by establishing relationships with new customers and by strategically rationalizing assets. In addition, we maximize efficiency by coordinating the completion of new facilities in a manner that is consistent with the expected production that supports them.

Organic Growth. We intend to use our strategic asset base in the United States and our position as one of the largest processors of natural gas, and as one of the largest producers and marketers of NGLs in the United States, as a platform for future growth. We plan to grow our business by leveraging our diverse and strategic asset base to increase supply across our fully integrated value chain. We will also make selective and capital efficient investments in our assets and energy transition.

Strategic Acquisitions and Partnerships. We intend to pursue economically attractive and strategic acquisition and partnership opportunities within the midstream energy industry, both in new and existing lines of business, and areas of operation.

OUR COMPETITIVE STRENGTHS

We are one of the largest processors of natural gas and one of the largest producers and marketers of NGLs in the United States with a diversified portfolio of integrated assets across our value chain. In 2022, our total wellhead volume was approximately 4.4 Bcf/d of natural gas and we produced an average of approximately 421 MBbls/d of NGLs. We provide natural gas gathering services to the wellhead, and leverage our strategic footprint to extend the value chain through our integrated NGL and natural gas pipelines and marketing infrastructure. We believe our ability to provide all of these services gives us an advantage in competing for new supplies of natural gas because we can provide substantially all services to move natural gas and NGLs from wellhead to market, and creates value for our customers. We believe that we are well positioned to execute our business strategies and achieve one of our primary business objectives of sustaining our cash distribution per unit because of the following competitive strengths:

Integrated Logistics and Marketing Operations. We believe the strategic location of our assets coupled with their geographic diversity and our reputation for running our business reliably and effectively, presents us with continuing opportunities to provide competitive services to our customers and attract new natural gas production to our gathering and processing operations. We have connected our gathering and processing operations to key markets with NGL pipelines that we own or operate to offer our customers a competitive, integrated midstream service. We have strategically located NGL transportation pipelines that provide takeaway capabilities for our gathering and processing operations in the Permian Basin, the Denver-Julesburg Basin (“DJ Basin”), the Midcontinent, East Texas, the Gulf Coast, South Texas, and Central Texas. Our NGL pipelines connect to various natural gas processing plants and transport the NGLs to fractionation facilities, a petrochemical plant, a third party underground NGL storage facility and other markets along the Gulf Coast. Our Logistics and Marketing operations also consists of multiple downstream assets including NGL fractionation facilities, an NGL storage facility and a residue gas storage facility.

Strategically Located Gas Gathering and Processing Operations. Our assets are strategically located in areas with the potential for increasing our wellhead volumes and cash flow generation. We have operations in some of the largest producing regions in the United States including the DJ Basin, Midcontinent, Permian Basin, and Eagle Ford. In addition, we operate one of the largest portfolios of natural gas processing plants in the United States. Our gathering systems and processing plants are connected to numerous key natural gas pipeline systems that provide producers with access to a variety of natural gas market hubs.

Stable Cash Flows. Our operations consist of a mix of fee-based and commodity-based services, which together with our commodity hedging program, are intended to generate relatively stable cash flows. The long term growth in our fee-based earnings will reduce the impact of unhedged margins. Additionally, while certain of our gathering and processing contracts

3

subject us to commodity price risk, we have mitigated a portion of our currently anticipated commodity price risk associated with the equity volumes from our gathering and processing operations with fixed price commodity swaps. As of December 31, 2022, we were approximately 70% fee-based.

Established Relationships with Oil, Natural Gas and Petrochemical Companies. We have long-term relationships with many of our suppliers and customers, and we expect that we will continue to benefit from these relationships.

Digital Transformation. We are driving workforce efficiencies through automation, improving safety and decreasing emissions via real-time monitoring and predictive analytics and optimizing margins while increasing cost efficiencies.

Experienced Management Team. Our senior management team and the board of directors of our General Partner have extensive experience in the midstream industry.

Affiliation with DCP Midstream, LLC and Phillips 66. Our relationship with DCP Midstream, LLC and its Class A Managing Member, Phillips 66, should continue to provide us with significant business opportunities. Through our relationship with DCP Midstream, LLC and Phillips 66, we believe our strong commercial relationships throughout the energy industry, including with major producers of natural gas and NGLs in the United States, will help facilitate the implementation of our strategies.

DCP Midstream, LLC has a significant interest in us through its ownership, together with GP LP, of approximately 57% of our common units. Through its ownership interest in DCP Midstream, LLC, Phillips 66 holds an indirect economic interest in us of approximately 43%, and is responsible, as the Class A Managing Member of DCP Midstream, LLC, for conducting, directing and managing all activities associated with us, our subsidiaries, GP LP and our General Partner.

4

OUR OPERATING SEGMENTS

Logistics and Marketing Segment

General

We market our NGLs, residue gas and condensate and provide logistics and marketing services to third-party NGL producers and sales customers in significant NGL production and market centers in the United States. This includes purchasing NGLs on behalf of third-party NGL producers for shipment on our NGL pipelines and resale in key markets.

Our NGL services include plant tailgate purchases, transportation, fractionation, flexible pricing options and price risk management. Our primary NGL operations are located in close proximity to our Gathering and Processing assets in each of the operating regions.

5

Our NGL pipelines transport NGLs from natural gas processing plants to fractionation facilities, petrochemical plants and a third party underground NGL storage facility. Our pipelines provide transportation services to customers primarily on a fee basis. Therefore, the results of operations for this business are generally dependent upon the volume of product transported and the level of fees charged to customers. The volumes of NGLs transported on our pipelines are dependent on the level of production of NGLs from processing plants connected to our NGL pipelines. When natural gas prices are high relative to NGL prices, it is less profitable to recover NGLs from natural gas because of the higher value of natural gas compared to the value of NGLs. As a result, we have experienced periods, and will likely experience periods in the future, when higher relative natural gas prices reduce the volume of NGLs produced at plants connected to our NGL pipelines.

Our natural gas systems have the ability to deliver gas into numerous downstream transportation pipelines and markets. We sell residue gas on behalf of our producer customers and residue gas which we earn under our gas supply agreements, supplying the residue gas demands of end-use customers physically attached to our pipeline systems and managing excess capacity of our owned storage and transportation assets. End-users include large industrial companies, natural gas distribution companies and electric utilities. We are focused on extracting the highest possible value for the residue gas that results from our processing and transportation operations. We sell the residue gas at market-based prices.

The following is operating data for our Logistics and Marketing segment:

| Operating Data | ||||||||||||||||||||||||||||||||||||||||||||

| Year Ended December 31, 2022 | ||||||||||||||||||||||||||||||||||||||||||||

| System | Approximate System Length (Miles) | Fractionators | Approximate Throughput Capacity (MBbls/d) (a) | Approximate Gas Throughput Capacity (TBtus/d) (a) | Pipeline Throughput (MBbls/d) (a) | Pipeline Throughput (TBtus/d) (a)(b) | Fractionator Throughput (MBbls/d) (a) | |||||||||||||||||||||||||||||||||||||

| Sand Hills pipeline | 1,400 | — | 333 | — | 299 | — | — | |||||||||||||||||||||||||||||||||||||

| Southern Hills pipeline | 950 | — | 128 | — | 118 | — | — | |||||||||||||||||||||||||||||||||||||

| Front Range pipeline | 450 | — | 87 | — | 77 | — | — | |||||||||||||||||||||||||||||||||||||

| Texas Express pipeline | 600 | — | 37 | — | 22 | — | — | |||||||||||||||||||||||||||||||||||||

| Other NGL pipelines (a) | 1,050 | — | 310 | — | 189 | — | — | |||||||||||||||||||||||||||||||||||||

| Gulf Coast Express pipeline | 500 | — | — | 0.50 | — | 0.49 | — | |||||||||||||||||||||||||||||||||||||

| Guadalupe pipeline | 600 | — | — | 0.25 | — | 0.29 | — | |||||||||||||||||||||||||||||||||||||

| Cheyenne Connector | 70 | — | — | 0.30 | — | 0.31 | — | |||||||||||||||||||||||||||||||||||||

| Mont Belvieu fractionators | — | 2 | — | — | — | — | 55 | |||||||||||||||||||||||||||||||||||||

| Total | 5,620 | 2 | 895 | 1.05 | 705 | 1.09 | 55 | |||||||||||||||||||||||||||||||||||||

(a) Represents total capacity or total volumes allocated to our proportionate ownership share.

(b) Represents average throughput for full year 2022.

NGL Pipelines

DCP Sand Hills Pipeline, LLC, or the Sand Hills pipeline, an interstate NGL pipeline which is owned 66.67% by us and 33.33% by Phillips 66, is a common carrier pipeline that provides takeaway service from plants in the Permian and the Eagle Ford basins to fractionation facilities along the Texas Gulf Coast and at the Mont Belvieu, Texas market hub.

DCP Southern Hills Pipeline, LLC, or the Southern Hills pipeline, an interstate NGL pipeline which is owned 66.67% by us and 33.33% by Phillips 66, provides takeaway service from the North and Midcontinent regions to fractionation facilities at the Mont Belvieu, Texas market hub.

Front Range Pipeline LLC, or the Front Range pipeline, an interstate NGL pipeline in which we own a 33.33% interest, originates in the DJ Basin and extends to Skellytown, Texas. The Front Range pipeline connects to our O'Connor plants, Lucerne 1, Lucerne 2, and Mewbourn plants, as well as third party plants in the DJ Basin. Enterprise Products Partners L.P., or Enterprise, is the operator of the pipeline.

Texas Express Pipeline LLC, or the Texas Express pipeline, an intrastate NGL pipeline in which we own a 10% interest, originates near Skellytown in Carson County, Texas, and extends to Enterprise's natural gas liquids fractionation and storage

6

complex at Mont Belvieu, Texas. The pipeline also provides access to other third party facilities in the area. Enterprise is the operator of the pipeline.

The Southern Hills, Texas Express, and Front Range pipelines have in place long-term, fee-based transportation agreements, a portion of which are ship-or-pay, with us as well as third party shippers. These NGL pipelines collect fee-based transportation revenue under regulated tariffs.

Natural Gas Pipelines

Gulf Coast Express LLC, or the Gulf Coast Express pipeline, an intrastate natural gas pipeline in which we own a 25% interest, originates from the Waha area in West Texas to Agua Dulce, in Nueces County, Texas. Kinder Morgan is the operator of the pipeline. The Gulf Coast Express pipeline is fully subscribed under long-term transportation contracts with us and third party shippers.

The Guadalupe pipeline is an intrastate natural gas pipeline that provides us access to market centers/hubs including Waha, Texas, Katy, Texas and the Houston Ship Channel and is used primarily in our natural gas asset based trading activities. We may transport volumes for third party shippers using our available capacity in the future.

Cheyenne Connector, LLC, or the Cheyenne Connector is an interstate natural gas pipeline in which we own a 50% interest, which provides residue gas takeaway from the DJ Basin to the Rockies Express Cheyenne Hub, just south of the Colorado-Wyoming border. Tallgrass Energy is the operator of the Cheyenne Connector. The Cheyenne Connector is fully subscribed under long-term transportation contracts with us and third party shippers.

NGL Fractionation Facilities

We own a 12.5% interest in the Enterprise fractionator operated by Enterprise and a 20% interest in the Mont Belvieu 1 fractionator operated by ONEOK Partners, both located in Mont Belvieu, Texas. The fractionation facilities separate NGLs received from processing plants into their individual components. These fractionation services are provided on a fee basis. The results of operations for this business are generally dependent upon the volume of NGLs fractionated and the level of fees charged to customers.

Storage Facilities

Our Marysville NGL storage facility, which stores ethane, propane and butane, is located in Michigan and has strategic access to Marcellus, Utica and Canadian NGLs. Our facility includes 11 underground salt caverns with approximately 8 MMBbls of storage capacity. Our facility serves regional refining and petrochemical demand, and helps to balance the seasonality of propane distribution in the Midwestern and Northeastern United States and in Sarnia, Canada. We provide services to customers primarily on a fee basis under multi-year storage agreements. The results of operations for this business are generally dependent upon the volume stored and the level of fees charged to customers.

Our Spindletop natural gas storage facility is located in Texas and plays an important role in our ability to act as a full-service natural gas marketer. The facility has capacity for residue gas of approximately 12 Bcf. We may lease a portion of the facility’s capacity to third-party customers, and use the balance to manage relatively constant natural gas supply volumes with uneven demand levels, provide “backup” service to our customers and support our asset-based trading activities. Our asset based trading activities are designed to realize margins related to fluctuations in commodity prices, time spreads and basis differentials and to maximize the value of our storage facility.

Trading and Marketing

Our energy trading operations are exposed to market variables and commodity price risk. We manage commodity price risk related to our natural gas storage and pipeline assets by engaging in natural gas asset based trading and marketing. We may enter into physical contracts and financial instruments with the objective of realizing a positive margin from the purchase and sale of commodity-based instruments.

Our NGL proprietary trading activity includes trading energy related products and services. We undertake these activities through the use of fixed forward sales and purchases, basis and spread trades, storage opportunities, put/call options, term contracts and spot market trading. Our energy trading operations are exposed to market variables and commodity price risk with respect to these products and services, and these operations may enter into physical contracts and financial instruments with the objective of realizing a positive margin from the purchase and sale of commodity-based instruments.

7

We may execute a time spread transaction when the difference between the current price of natural gas (cash or futures) and the futures market price for natural gas exceeds our cost of storing physical gas in our owned and/or leased storage facilities. The time spread transaction allows us to lock in a margin when this market condition exists. A time spread transaction is executed by establishing a long gas position at one point in time and establishing an equal short gas position at a different point in time.

We may execute basis spread transactions when the market price differential between locations on a pipeline asset exceeds our cost of transporting physical gas through our owned and/or leased pipeline assets. When this market condition exists, we may execute derivative instruments around this differential at the market price. The basis spread transaction allows us to lock in a margin on our physical purchases and sales of gas.

Customers and Contracts

We sell our commodities to a variety of customers ranging from large, multi-national petrochemical and refining companies to small regional retail propane distributors. Substantially all of our NGL sales are made at market-based prices.

Competition

The Logistics and Marketing business is highly competitive in our markets and includes interstate and intrastate pipelines, integrated oil and gas companies that produce, fractionate, transport, store and sell natural gas and NGLs, and underground storage facilities. Competition is often the greatest in geographic areas experiencing robust drilling by producers and strong petrochemical demand and during periods of high NGL prices relative to natural gas. Competition is also increased in those geographic areas where our contracts with our customers are shorter term and therefore must be renegotiated on a more frequent basis.

Competition in the NGLs marketing area comes from other midstream NGL marketing companies, international producers/traders, chemical companies, refineries and other asset owners. Along with numerous marketing competitors, we offer price risk management and other services. We believe it is important that we tailor our services to the end-use customer to remain competitive.

Gathering and Processing Segment

General

Our Gathering and Processing segment consists of a geographically diverse complement of assets and ownership interests that provide a varied array of wellhead to market services for our producer customers in Alabama, Colorado, Kansas, Louisiana, Michigan, New Mexico, Oklahoma, Texas and Wyoming. These services include gathering, compressing, treating, and processing natural gas, producing and fractionating NGLs, and recovering condensate. Our Gathering and Processing segment’s operations are organized into four regions: North, Permian, Midcontinent and South. Our geographic diversity helps to mitigate our natural gas supply risk in that we are not tied to one natural gas resource type or producing area. We believe our current geographic mix of assets is an important factor for the maintenance and long term growth of overall volumes and cash flow for this segment. Our assets are positioned in certain areas with active drilling programs and opportunities for organic growth.

We provide our producer customers with gathering and processing services that allow them to move their raw (unprocessed) natural gas to market. Raw natural gas is gathered, compressed and transported through pipelines to our processing facilities. In order for the raw natural gas to be accepted by the downstream market, we remove water, nitrogen and carbon dioxide and separate NGLs for further processing. Processed natural gas, usually referred to as residue natural gas, is then recompressed and delivered to natural gas pipelines and end users. The separated NGLs are in a mixed, unfractionated form and are sold and delivered through natural gas liquids pipelines to fractionation facilities for further separation.

We own or operate 36 active natural gas processing plants, including an interest in a plant through our 40% equity interest in Discovery Producer Services, LLC, or Discovery. At some of these facilities, we fractionate NGLs into individual components (ethane, propane, butane and natural gasoline).

We receive natural gas from a diverse group of producers under contracts with varying durations, and we receive fees or commodities from the producers to transport the natural gas from the wellhead to the processing plant. We receive fees or commodities as payment for our natural gas processing services, depending on the types of contracts we enter into with each supplier. We purchase or take custody of substantially all of our natural gas from producers, principally under fee-based or percent-of-proceeds/index processing contracts.

8

We actively seek new producing customers of natural gas on all of our systems to increase throughput volume and to offset natural declines in the production from connected wells. We obtain new natural gas supplies in our operating areas by contracting for production from new wells, by connecting new wells drilled on dedicated acreage and by obtaining natural gas that has been directly received or released from other gathering systems.

Our contracts with our producing customers in our Gathering and Processing segment are a mix of non-commodity sensitive fee-based contracts and commodity sensitive percent-of-proceeds and percent-of-liquids contracts. Percent-of-proceeds contracts are directly related to the price of natural gas, NGLs and condensate and percent-of-liquids contracts are directly related to the price of NGLs and condensate. Additionally, these contracts may include fee-based components. Generally, the initial term of these purchase agreements is three to five years and in some cases, the life of the lease. As we negotiate new agreements and renegotiate existing agreements, this may result in a change in contract mix period over period.

We enter into derivative financial instruments to mitigate a portion of the risk of weakening natural gas, NGL and condensate prices associated with our gathering, processing and sales activities, thereby stabilizing our cash flows. Our commodity derivative instruments used for our hedging program are a combination of direct NGL product, crude oil, and natural gas hedges.

During 2022, total wellhead volume on our assets was approximately 4.4 Bcf/d, originating from a diversified mix of customers. Our systems each have significant customer acreage dedications that we expect will continue to provide opportunities for growth as those customers execute their drilling plans over time. Our gathering systems also attract new natural gas volumes through numerous smaller acreage dedications and by contracting with undedicated producers who are operating in or around our gathering footprint. During 2022, the combined NGL production from our processing facilities was approximately 421 MBbls/d and was delivered and sold into various NGL takeaway pipelines.

The following is operating data for our Gathering and Processing segment by region:

| Operating Data | ||||||||||||||||||||||||||||||||

| Year ended December 31, 2022 | ||||||||||||||||||||||||||||||||

| Regions | Plants | Approximate Gathering and Transmission Systems (Miles) | Approximate Net Nameplate Plant Capacity (MMcf/d) (a) | Natural Gas Wellhead Volume (MMcf/d) (a) | NGL Production (MBbls/d) (a) | |||||||||||||||||||||||||||

| North | 13 | 3,500 | 1,580 | 1,584 | 157 | |||||||||||||||||||||||||||

| Midcontinent | 6 | 23,000 | 1,110 | 825 | 70 | |||||||||||||||||||||||||||

| Permian | 10 | 15,000 | 1,220 | 999 | 123 | |||||||||||||||||||||||||||

| South | 7 | 6,500 | 1,630 | 945 | 71 | |||||||||||||||||||||||||||

| Total | 36 | 48,000 | 5,540 | 4,353 | 421 | |||||||||||||||||||||||||||

(a) Represents total capacity or total volumes allocated to our proportionate ownership share.

9

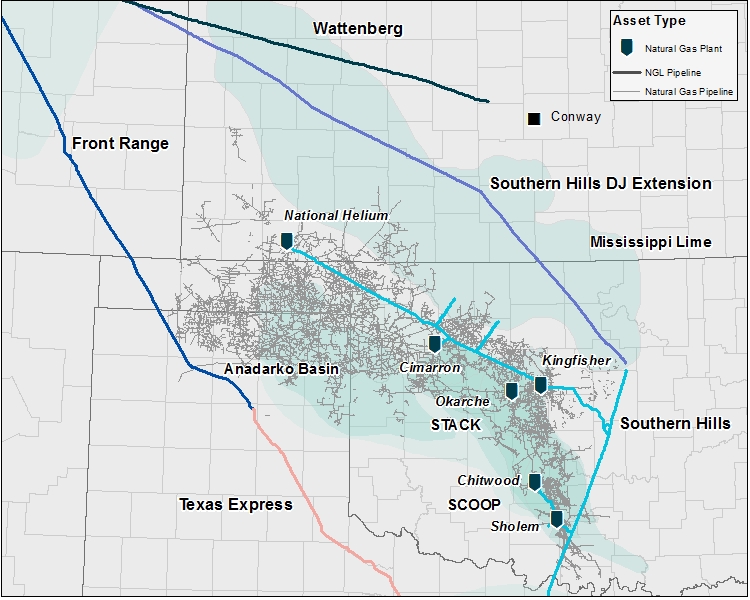

North Region

Our North region primarily consists of our DJ Basin system. We have a broad network of gathering, compression, treating, and processing facilities in Weld County, Colorado that provide significant optionality and flexibility.

Our DJ Basin system delivers to the Mont Belvieu hub in Mont Belvieu, Texas via the Southern Hills, Front Range and Texas Express pipelines, to the Conway hub in Bushton, Kansas via our Wattenberg pipeline, and Rockies Express Cheyenne Hub via the Cheyenne Connector.

10

Midcontinent Region

Our Midcontinent region primarily includes our Liberal system and South Central Oklahoma system. We gather and process raw natural gas primarily from the Ardmore and Anadarko Basins, including the South Central Oklahoma Oil Province (“SCOOP”) play and the Sooner Trend Anadarko Basin Canadian and Kingfisher (“STACK”) play.

Our gathering system footprint in the eastern Midcontinent region, which includes our South Central Oklahoma system, serves the SCOOP and STACK plays. Existing production in the western Midcontinent region, which includes our Liberal system in the Hugoton Basin, is typically from mature fields with shallow decline profiles that we expect will provide our plants with a dependable source of raw natural gas over a long term. We believe the infrastructure of our plants and gathering facilities is uniquely positioned to pursue our consolidation strategy in the western Midcontinent region.

Our gathering and processing assets in the Midcontinent region deliver NGLs primarily to the Gulf Coast and Mont Belvieu via our Southern Hills pipeline.

11

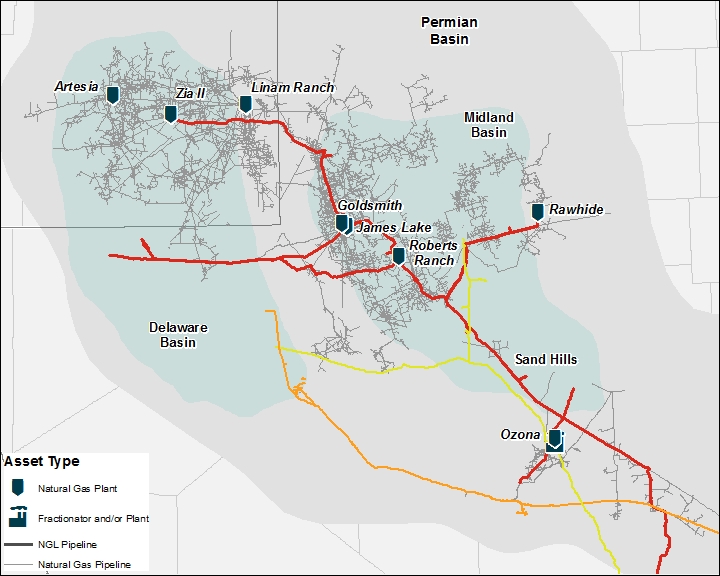

Permian Region

Our Permian region primarily includes our West Texas system in the Midland Basin, our Southeast New Mexico system in the Delaware Basin, and our James Lake System that has connectivity to both the Midland and Delaware Basins. Producers continue to focus drilling activity on the most attractive acreage in the Midland and Delaware Basins.

Our gathering and processing assets in the Permian region provide NGL takeaway service via our Sand Hills pipeline, to fractionation facilities along the Gulf Coast and to the Mont Belvieu hub. The Guadalupe pipeline provides gas takeaway from Waha to Katy, Texas. Through our ownership interest in the Gulf Coast Express pipeline we provide additional gas takeaway in the region. In the third quarter of 2022 we completed the acquisition of the James Lake System and a 120MMcf/d cryogenic processing facility that provides connectivity to the Delaware and Midland Basins.

12

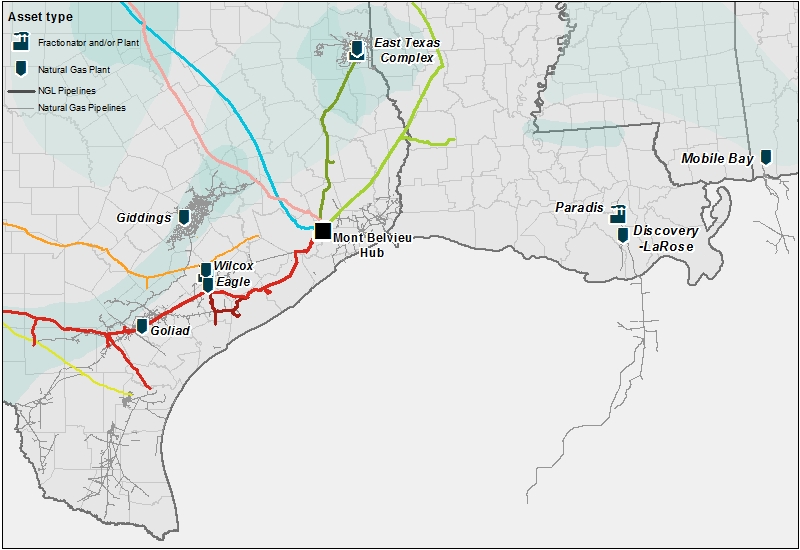

South Region

Our South region primarily includes our Eagle Ford system, East Texas system, and our 40% interest in the Discovery system. We are pursuing cost efficiencies and increasing the utilization of our existing assets.

Our Eagle Ford system delivers NGLs to the Gulf Coast petrochemical markets and to Mont Belvieu through our Sand Hills pipeline and other third party NGL pipelines. Our East Texas system provides NGL takeaway service through the Panola pipeline, owned 15% by us, and delivers gas primarily through its Carthage Hub which delivers residue gas to multiple interstate and intrastate pipelines.

The Discovery system is operated by Williams Partners L.P., which owns a 60% interest, and offers a full range of wellhead-to-market services to both onshore and offshore natural gas producers. The assets are primarily located in the eastern Gulf of Mexico and Louisiana, and have access to downstream pipelines and markets.

13

Competition

We face strong competition in acquiring raw natural gas supplies. Our competitors in obtaining additional gas supplies and in gathering and processing raw natural gas include major integrated oil and gas companies, interstate and intrastate pipelines, and companies that gather, compress, treat, process, transport, store and/or market natural gas. Competition is often the greatest in geographic areas experiencing robust drilling by producers and during periods of high commodity prices for crude oil, natural gas and/or NGLs. Competition is also increased in those geographic areas where our commercial contracts with our customers are shorter term and therefore must be renegotiated on a more frequent basis.

We have no revenue attributable to international activities.

REGULATORY AND ENVIRONMENTAL MATTERS

Safety and Maintenance Regulation

We are subject to regulation by the United States Department of Transportation, or DOT, under the Hazardous Liquids Pipeline Safety Act of 1979, as amended, or HLPSA, and comparable state statutes with respect to design, installation, testing, construction, operation, replacement and management of pipeline facilities. The HLPSA and implementing regulations apply to interstate and intrastate pipeline facilities and the pipeline transportation of liquid petroleum and petroleum products, including NGLs and condensate, and require any entity that owns or operates pipeline facilities to comply with such regulations, to permit access to and copying of records and to file certain reports and provide information as required by the United States Secretary of Transportation. These regulations include potential fines and penalties for violations. We believe that we are in compliance in all material respects with these HLPSA regulations.

We are also subject to the Natural Gas Pipeline Safety Act of 1968, as amended, or NGPSA, and the Pipeline Safety Improvement Act of 2002. The NGPSA regulates safety requirements in the design, construction, operation and maintenance of gas pipeline facilities, while the Pipeline Safety Improvement Act establishes mandatory inspections for all United States oil and natural gas transportation pipelines in high-consequence areas within 10 years. DOT, through the Pipeline and Hazardous Materials Safety Administration (PHMSA), has developed regulations implementing the Pipeline Safety Improvement Act that requires pipeline operators to implement integrity management programs, including more frequent inspections and other safety protections in areas where the consequences of potential pipeline accidents pose the greatest risk to people and their property.

Pipeline safety legislation enacted in 2012, the Pipeline Safety, Regulatory Certainty, and Job Creation Act of 2011 (the Pipeline Safety and Job Creations Act) reauthorized funding for federal pipeline safety programs through 2015, increases penalties for safety violations, establishes additional safety requirements for newly constructed pipelines, and requires studies of certain safety issues that could result in the adoption of new regulatory requirements for existing pipelines, including the expansion of integrity management, use of automatic and remote-controlled shut-off valves, leak detection systems, sufficiency of existing regulation of gathering pipelines, use of excess flow valves, verification of maximum allowable operating pressure, incident notification, and other pipeline-safety related requirements. New rules promulgated by DOT’s PHMSA address many areas of this legislation, as described below. We currently estimate we will incur approximately $92 million between 2023 and 2027 to implement integrity management program testing along certain segments of our natural gas transmission and NGL pipelines under Parts 192 and 195. This does not include the costs, if any, of any repair, remediation, preventative or mitigating actions that may be determined to be necessary as a result of the testing program, nor is it inclusive of estimated costs to implement the Final Gathering Rule (as defined and discussed in further detail below).

The Pipeline Safety and Job Creation Act requires more stringent oversight of pipelines and increased civil penalties for violations of pipeline safety rules. The legislation gave PHMSA civil penalty authority up to $213,268 per day per violation, with a maximum of $2,132,679 for any related series of violations. Any material penalties or fines under these or other statutes, rules, regulations or orders could have a material adverse impact on our business, financial condition, results of operation and cash flows.

On December 21, 2020, the U.S. Congress passed the Protecting our Infrastructure of Pipelines and Enhancing Safety Act of 2020 (the 2020 Act). The Act reauthorizes the federal pipeline safety program through September 30, 2023, and establishes annual funding levels through 2023. The 2020 Act also requires PHMSA to issue new rules for gas pipeline leak detection and repair programs and idle pipelines, and issue final rulemakings for gas gathering lines, class location changes, and the definition of unusually sensitive areas. The 2020 Act establishes additional due process requirements applicable to PHMSA enforcement actions, authorizes a new declaratory order proceeding, and obligates PHMSA to consider an operator’s self-report in assessing a civil penalty.

14

On January 11, 2021, PHMSA published a Final Rule amending certain gas pipeline safety regulations at 49 C.F.R. Parts 191 and 192 (the "Final Rule"). Although the effective date of the Final Rule is March 12, 2021, PHMSA provided a deferred compliance date of October 1, 2021. Among other changes, these Part 192 changes include provisions allowing operators to remotely monitor cathodic protection rectifier stations, provided that they perform annual testing by physical inspection of the rectifier. The Final Rule also adjusts the monetary property damage threshold in the definition of an “incident” from $50,000 to $122,000 to account for inflation, with a commitment to update the threshold annually using a defined formula. The Final Rule incorporates certain industry standards for construction of plastic pipes and changes test factors for pressure vessels.

On November 15, 2021, PHMSA published a Final Rule amending the gas pipeline safety regulations at 49 CFR Parts 191 and 192 to extend regulation over larger diameter gas gathering pipelines located in rural (Class 1) locations (the “Final Gathering Rule”). The Final Gathering Rule imposes Part 191 or Part 192 requirements on such rural gathering pipelines. All rural gathering pipelines will be subject to annual and incident reporting under Part 191, while those pipelines over 8.625 inches in diameter that are operated at a maximum allowable operating pressure ("MAOP") of more than 20% of specified minimum yield strength ("SMYS") or, where SMYS is not known, where the MAOP exceeds 125 psig, must also comply with certain Part 192 requirements. The applicable Part 192 requirements increase with increased diameter and with proximity to buildings intended for human occupancy or impacted sites. For gathering pipelines between 8.625 inches and 16 inches in diameter, the new regulations require annual and incident reporting, as well as design and construction standards, damage prevention, and emergency planning on new pipelines or those that are repaired or replaced or otherwise substantially changed. If the potential impact radius of the pipeline segment includes a building intended for human occupancy or an impacted site, corrosion control, line markers, public awareness and leakage survey and repair for pipelines of less than 12.75 inches in diameter are also added, and MAOP requirements and standards for plastic pipelines for lines are added for pipelines between 12.75 inches and 16 inches in diameter. Pipelines of more than 16 inches in diameter are subject to all of the above, whether or not the potential impact radius includes any structures intended for human occupancy or impacted sites. The Part 191 reporting requirements of the Final Gathering Rule took effect on May 16, 2022. The remaining Part 192 requirements were to take effect on November 15, 2022 or May 16, 2023, depending on the rule section. However, following GPA Midstream Association’s petition for judicial review of the new rule, PHMSA agreed to stay enforcement until May 16, 2024 with respect to smaller-diameter pipelines (8.625 to 12.75 inches). We believe that we will be able to meet the requirements of the Final Gathering Rule in all material respects by the dates set forth in the Final Gathering Rule.

We are currently evaluating the impact of the Final Gathering Rule on our operations and compliance programs. We are also evaluating opportunities to reduce the number of miles of pipeline that will be subject to the Final Gathering Rule, including changes in operating pressures and system reconfiguration or optimization.

Finally, the Company is evaluating the cost impact of the Final Gathering Rule, which depends on the results of our analysis of pipeline data. We currently estimate that we will incur costs of approximately $100 million to implement the requirements of the Final Gathering Rule, and we will refine that number as we complete our analysis.

We believe that we are in compliance in all material respects with the NGPSA and the Pipeline Safety Improvement Act of 2002 and the Pipeline Safety and Job Creation Act, and to the extent we make changes to our program to reflect the 2020 Act, we expect to be in material compliance by the effective dates of the new regulations promulgated under the 2020 Act.

States are largely preempted by federal law from regulating pipeline safety, but may assume responsibility for enforcing intrastate pipeline regulations at least as stringent as the federal standards. In practice, states vary considerably in their authority and capacity to address pipeline safety. We do not anticipate any significant problems in complying with applicable state laws and regulations in those states in which we or the entities in which we own an interest operate. Our natural gas transmission and regulated gathering pipelines have ongoing inspection and compliance programs designed to keep the facilities in compliance with pipeline safety and pollution control requirements.

In addition, we are subject to the requirements of the federal Occupational Safety and Health Act, or OSHA, and comparable state statutes, whose purpose is to protect the health and safety of workers, both generally and within the pipeline industry. In addition, the OSHA hazard communication standard, the Environmental Protection Agency, or EPA, community right-to-know regulations under Title III of the federal Superfund Amendment and Reauthorization Act and comparable state statutes require that information be maintained concerning hazardous materials used or produced in our operations and that this information be provided to employees, state and local government authorities and citizens. We and the entities in which we own an interest are also subject to OSHA Process Safety Management and EPA Risk Management Program regulations, which are designed to prevent or minimize the consequences of catastrophic releases of toxic, reactive, flammable or explosive chemicals. The OSHA regulations apply to any process that involves a chemical at or above specified thresholds, or any process that involves flammable liquid or gas, pressurized tanks, caverns and wells holding or handling these materials in quantities in excess of 10,000 pounds at various locations. Flammable liquids stored in atmospheric tanks at temperatures below the normal

15

boiling point of the liquids without the benefit of chilling or refrigeration are exempt from these standards. The EPA regulations have similar applicability thresholds. We implement these safety programs, and we have an internal program of inspection designed to monitor and enforce compliance with worker safety requirements. We believe that we are in compliance in all material respects with all applicable laws and regulations relating to worker health and safety.

FERC and State Regulation of Operations

Federal Energy Regulatory Commission (“FERC”) regulation of interstate natural gas pipelines, the marketing and sale of natural gas in interstate commerce and the transportation of NGLs in interstate commerce may affect certain aspects of our business and the market for our products and services. Regulation of gathering systems and intrastate transportation of natural gas and NGLs by state agencies may also affect our business.

Interstate Natural Gas Pipeline Regulation

Our Cimarron River, Discovery, Cheyenne Connector, and Dauphin Island Gathering Partners systems, or portions thereof, are some of our natural gas pipeline assets that are subject to regulation by FERC, under the Natural Gas Act of 1938, as amended, or NGA. Natural gas companies subject to the NGA may only charge rates that have been determined to be just and reasonable. In addition, FERC authority over natural gas companies that provide natural gas pipeline transportation services in interstate commerce includes:

•certification and construction of new facilities;

•abandonment of services and facilities;

•maintenance of accounts and records;

•acquisition and disposition of facilities;

•initiation and discontinuation of transportation services;

•terms and conditions of transportation services and service contracts with customers;

•depreciation and amortization policies;

•conduct and relationship with certain affiliates; and

•various other matters.

Generally, the maximum filed recourse rates for an interstate natural gas pipeline's transportation services are based on the pipeline's cost of service including recovery of and a return on the pipeline’s actual prudent investment cost. Key determinants in the ratemaking process are costs of providing service, allowed rate of return and volume throughput and contractual capacity commitment assumptions. The allocation of costs to various pipeline services and the manner in which rates are designed also can impact a pipeline's profitability. The maximum applicable recourse rates and terms and conditions for service are set forth in each pipeline’s FERC-approved gas tariff. FERC-regulated natural gas pipelines are permitted to discount their firm and interruptible rates without further FERC authorization down to the minimum rate or variable cost of performing service, provided they do not “unduly discriminate.”

Tariff changes can only be implemented upon approval by FERC. Two primary methods are available for changing the rates, terms and conditions of service of an interstate natural gas pipeline. Under the first method, the pipeline voluntarily seeks a tariff change by making a tariff filing with FERC justifying the proposed tariff change and providing notice, generally 30 days, to the appropriate parties. If FERC determines, as required by the NGA, that a proposed change is just and reasonable, FERC will accept the proposed change and the pipeline will implement such change in its tariff. However, if FERC determines that a proposed change may not be just and reasonable as required by NGA, then FERC may suspend such change for up to five months beyond the date on which the change would otherwise go into effect and set the matter for an administrative hearing. Subsequent to any suspension period ordered by FERC, the proposed change may be placed into effect by the company, pending final FERC approval. In most cases, a proposed rate increase is placed into effect before a final FERC determination on such rate increase, and the proposed increase is collected subject to refund (plus interest). Under the second method, FERC may, on its own motion or based on a complaint, initiate a proceeding to compel the company to change or justify its rates, terms and/or conditions of service. If FERC determines that the existing rates, terms and/or conditions of service are unjust, unreasonable, unduly discriminatory or preferential, then any rate reduction or change that it orders generally will be effective prospectively from the date of the FERC order requiring this change.

The natural gas industry historically has been heavily regulated; therefore, there is no assurance that a more stringent regulatory approach will not be pursued by FERC and Congress, especially in light of potential market power abuse by marketing companies engaged in interstate commerce. In the Energy Policy Act of 2005, or EPACT 2005, Congress amended the NGA and Federal Power Act to add anti-fraud and anti-manipulation requirements. EPACT 2005 prohibits the use of any “manipulative or deceptive device or contrivance” in connection with the purchase or sale of natural gas, electric energy or

16

transportation subject to FERC jurisdiction. FERC adopted market manipulation and market behavior rules to implement the authority granted under EPACT 2005. These rules, which prohibit fraud and manipulation in wholesale energy markets, are subject to broad interpretation. Given FERC's broad mandate granted in EPACT 2005, if energy prices are high, or exhibit what FERC deems to be “unusual” trading patterns, FERC may investigate energy markets to determine if behavior unduly impacted or “manipulated” energy prices.

In addition, EPACT 2005 gave FERC increased penalty authority for violations of the NGA and FERC's rules and regulations thereunder. FERC may issue civil penalties of up to $1.5 million per day per violation, and violators may be subject to criminal penalties of up to $1.5 million per violation and five years in prison. FERC may also order disgorgement of profits obtained in violation of FERC rules. FERC relies on its enforcement authority in issuing a number of natural gas enforcement actions. Failure to comply with the NGA and FERC's rules and regulations thereunder could result in the imposition of civil penalties and disgorgement of profits.

Under the NGA and the National Environmental Policy Act of 1969, FERC has broad authority to approve the construction of new interstate natural gas pipeline facilities, including imposing environmental conditions on certificates of public convenience and necessity. In February 2022, FERC issued new policy guidance that details what FERC will consider in evaluating new pipeline infrastructure projects. Considerations include, among general public benefit and adverse effect analyses, impacts on: greenhouse gas emissions, the environment, environmental justice communities, existing customers of pending projects, existing pipelines and their customers, and landowners. FERC subsequently amended these policies in March 2022 to make them draft policies only, which renders them inoperable unless and until final policies are issued. Since then, FERC has requested and received comments on the draft policies. Depending on the outcome of these policies and the promulgation of new policies, regulations or statutes, new pipeline infrastructure projects could face increased scrutiny and enhanced regulatory reviews by federal, state and/or environmental regulators due to an increased focus on climate change policies and the fossil fuel industry. While we do not currently have projects pending that are subject to material risk, any governmental or regulatory actions that place additional burdens and/or costs on future projects, could adversely impact our ability to develop new infrastructure.

Intrastate Natural Gas Pipeline Regulation

Intrastate natural gas pipeline operations are not generally subject to rate regulation by FERC, but they are subject to regulation by various agencies in the respective states where they are located. While the regulatory regime varies from state to state, state agencies typically require intrastate gas pipelines to provide service that is not unduly discriminatory and to file and/or seek approval of their rates with the agencies and permit shippers to challenge existing rates or proposed rate increases. For example, our Guadalupe system and Gulf Coast Express pipeline are intrastate pipelines regulated as a gas utility by the Railroad Commission. To the extent that an intrastate pipeline system transports natural gas in interstate commerce, the rates and terms and conditions of such interstate transportation service are subject to FERC rules and regulations under Section 311 of the Natural Gas Policy Act, or NGPA. Certain of our systems are subject to FERC jurisdiction under Section 311 of the NGPA for their interstate transportation services. Section 311 regulates, among other things, the provision of transportation services by an intrastate natural gas pipeline on behalf of a local distribution company or an interstate natural gas pipeline. Under Section 311, rates charged for transportation must be fair and equitable, and amounts collected in excess of fair and equitable rates are subject to refund with interest. Rates for service pursuant to Section 311 of the NGPA are generally subject to review and approval by FERC at least once every five years. Additionally, the terms and conditions of service set forth in the intrastate pipeline’s Statement of Operating Conditions are subject to FERC approval. Non-compliance with FERC's rules and regulations established under Section 311 of the NGPA, including failure to observe the service limitations applicable to transportation services provided under Section 311, failure to comply with the rates approved by FERC for Section 311 service, and failure to comply with the terms and conditions of service established in the pipeline’s FERC-approved Statement of Operating Conditions could result in the imposition of civil and criminal penalties. Among other matters, EPACT 2005 also amended the NGPA to give FERC authority to impose civil penalties for violations of the NGPA up to $1 million for any one violation and violators may be subject to criminal penalties of up to $1 million per violation and five years in prison.

17

Gathering Pipeline Regulation

Section 1(b) of the NGA exempts natural gas gathering facilities from the jurisdiction of FERC under the NGA. We believe that our natural gas gathering facilities meet the traditional tests FERC has used to establish a pipeline’s status as a gatherer not subject to FERC jurisdiction. However, the distinction between FERC-regulated transmission services and federally unregulated gathering services continues to be a current issue in various FERC proceedings with respect to facilities that interconnect gathering and processing plants with nearby interstate pipelines, so the classification and regulation of our gathering facilities may be subject to change based on future determinations by FERC and the courts. State regulation of gathering facilities generally includes various safety, environmental, and, in many circumstances, nondiscriminatory take requirements and complaint-based rate regulation.

Our purchasing, gathering and intrastate transportation operations are subject to ratable take and common purchaser statutes in the states in which they operate. The ratable take statutes generally require gatherers to take, without undue discrimination, natural gas production that may be tendered to the gatherer for handling. Similarly, common purchaser statutes generally require gatherers to purchase without undue discrimination as to source of supply or producer. These statutes are designed to prohibit discrimination in favor of one producer over another producer or one source of supply over another source of supply. These statutes have the effect of restricting our right as an owner of gathering facilities to decide with whom we contract to purchase or transport natural gas.

Natural gas gathering may receive greater regulatory scrutiny at both the state and federal levels where FERC has recognized a jurisdictional exemption for the gathering activities of interstate pipeline transmission companies and a number of such companies have transferred gathering facilities to unregulated affiliates. Many of the producing states have adopted some form of complaint-based regulation that generally allows natural gas producers and shippers to file complaints with state regulators in an effort to resolve grievances relating to natural gas gathering access and rate discrimination. Our gathering operations could be adversely affected should they be subject in the future to the application of state or federal regulation of rates and services. Additional rules and legislation pertaining to these matters are considered or adopted from time to time. We cannot predict what effect, if any, such changes might have on our operations, but the industry could be required to incur additional capital expenditures and increased costs depending on future legislative and regulatory changes.

Other Laws - Texas Weather Emergencies

In 2021, in response to Winter Storm Uri in February 2021, the State of Texas implemented new laws related to preparing for, preventing and responding to weather emergencies and power outages. Under the new law, several state agencies, including the Railroad Commission, the Public Utilities Commission of Texas (“TPUC”), and the Energy Reliability Council of Texas (“ERCOT”) are required to coordinate and implement new rules and processes related to weather emergencies impacting gas-fired electric generation and the natural gas production and supply chain. The Railroad Commission and TPUC implemented rules related to the critical designation of natural gas infrastructure and electric service to such critical infrastructure during an emergency. The Railroad Commission designated natural gas processing plants, natural gas pipelines and related facilities, and natural gas storage, in addition gas production and distribution facilities, as critical. We are obligated to develop a listing of our critical natural gas facilities and update it semi-annually. Electric utilities are obligated to review our critically designated facility listings and establish priorities during load shed events. The law further requires the agencies to “map” the supply chain of natural gas to electric generation facilities; natural gas facilities that are deemed critical to the supply of electricity will be required to implement measures to prepare to operate during a winter weather emergency (“weatherize”). Several of our facilities in Texas, including gas processing, gas storage and gas pipeline and compression facilities have been deemed critical to the supply of electric generation and are subject to new weatherization rules implemented by the Railroad Commission. Such critical facilities are required to implement weather emergency preparation measures and attest to such measures annually. Failure to comply with the Railroad Commission’s weatherization requirements is subject to a penalty of up to $1 million dollars per violation.

Sales of Natural Gas

The price at which we buy and sell natural gas currently is not subject to federal regulation and, for the most part, is not subject to state regulation. However, with regard to our interstate purchases and sales of natural gas, and any related hedging activities that we undertake, we are required to observe anti-market manipulation laws and related regulations enforced by FERC and/or the Commodity Futures Trading Commission, or CFTC. Should we violate the anti-market manipulation laws and regulations, in additional to civil and criminal penalties, we could be subject to related third party damage claims by, among others, market participants, sellers, royalty owners and taxing authorities.

18

Our sales of natural gas are affected by the availability, terms and cost of pipeline transportation. As noted above, the price and terms of access to pipeline transportation are subject to extensive federal and state regulation. FERC is continually proposing and implementing new rules and regulations affecting those segments of the natural gas industry, most notably interstate natural gas transmission companies that remain subject to FERC jurisdiction. These initiatives also may affect the intrastate transportation of natural gas under certain circumstances. The stated purpose of many of these regulatory changes is to promote competition among the various sectors of the natural gas industry. We cannot predict the ultimate impact of these regulatory changes to our natural gas marketing operations.

Interstate NGL Pipeline Regulation

Certain of our pipelines, including Sand Hills and Southern Hills, are common carriers that provide interstate NGL transportation services subject to FERC regulation. FERC regulates interstate common carriers under its Oil Pipeline Regulations, the Interstate Commerce Act of 1887, as amended, or ICA, and the Elkins Act of 1903, as amended. FERC requires that common carriers file tariffs containing all the rates, charges and other terms for services provided by such pipelines. The ICA requires that tariffs apply to the interstate movement of NGLs, as is the case with the Sand Hills, Southern Hills, Black Lake, Wattenberg and Front Range pipelines. Pursuant to the ICA, rates must be just, reasonable, and nondiscriminatory, and can be challenged at FERC either by protest when they are initially filed or increased or by complaint at any time they remain on file with FERC.