DEERE & CO - Quarter Report: 2022 July (Form 10-Q)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

(Mark One)

☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended July 31, 2022

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____ to ____

Commission file no: 1-4121

(Exact name of registrant as specified in its charter)

Delaware | 36-2382580 |

One John Deere Place

Moline, Illinois 61265

(Address of principal executive offices)

Telephone Number: (309) 765-8000

Securities Registered Pursuant to Section 12(b) of the Act:

Title of each class | Trading symbol | Name of each exchange on which registered | ||

Common stock, $1 par value | DE | New York Stock Exchange | ||

6.55% Debentures Due 2028 | DE28 | New York Stock Exchange |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☒ | Accelerated filer | ☐ |

Non-accelerated filer | ☐ | Smaller reporting company | ☐ |

Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☒

At July 31, 2022, 301,819,630 shares of common stock, $1 par value, of the registrant were outstanding.

PART I. FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS | |||||||||||||

DEERE & COMPANY | |||||||||||||

STATEMENTS OF CONSOLIDATED INCOME | |||||||||||||

For the Three and Nine Months Ended July 31, 2022 and August 1, 2021 | |||||||||||||

(In millions of dollars and shares except per share amounts) Unaudited | |||||||||||||

Three Months Ended | Nine Months Ended | ||||||||||||

| 2022 |

| 2021 |

| 2022 |

| 2021 |

| |||||

Net Sales and Revenues | |||||||||||||

Net sales |

| $ | 13,000 | $ | 10,413 |

| $ | 33,565 | $ | 29,461 | |||

Finance and interest income | 846 |

| 825 | 2,441 |

| 2,468 | |||||||

Other income | 256 |

| 289 | 1,035 |

| 768 | |||||||

Total | 14,102 |

| 11,527 | 37,041 |

| 32,697 | |||||||

Costs and Expenses | |||||||||||||

Cost of sales | 9,511 |

| 7,574 | 25,124 |

| 21,307 | |||||||

Research and development expenses | 481 |

| 394 | 1,336 |

| 1,137 | |||||||

Selling, administrative and general expenses | 959 |

| 841 | 2,672 |

| 2,448 | |||||||

Interest expense | 296 |

| 244 | 713 |

| 783 | |||||||

Other operating expenses | 316 |

| 324 | 954 |

| 1,033 | |||||||

Total | 11,563 |

| 9,377 | 30,799 |

| 26,708 | |||||||

Income of Consolidated Group before Income Taxes | 2,539 |

| 2,150 | 6,242 |

| 5,989 | |||||||

Provision for income taxes | 654 |

| 491 | 1,364 |

| 1,328 | |||||||

Income of Consolidated Group | 1,885 |

| 1,659 | 4,878 |

| 4,661 | |||||||

Equity in income of unconsolidated affiliates |

|

| 8 | 8 |

| 21 | |||||||

Net Income | 1,885 |

| 1,667 | 4,886 |

| 4,682 | |||||||

Less: Net income attributable to noncontrolling interests | 1 |

|

| 1 |

| 2 | |||||||

Net Income Attributable to Deere & Company |

| $ | 1,884 | $ | 1,667 |

| $ | 4,885 | $ | 4,680 | |||

Per Share Data | |||||||||||||

Basic |

| $ | 6.20 | $ | 5.36 |

| $ | 15.97 | $ | 14.98 | |||

Diluted |

| $ | 6.16 | $ | 5.32 |

| $ | 15.88 | $ | 14.86 | |||

Dividends declared | $ | 1.13 | $ | .90 | $ | 3.23 | $ | 2.56 | |||||

Dividends paid | $ | 1.05 | $ | .90 | $ | 3.15 | $ | 2.42 | |||||

Average Shares Outstanding | |||||||||||||

Basic | 304.1 |

| 311.0 | 305.8 |

| 312.4 | |||||||

Diluted | 305.7 |

| 313.4 | 307.7 |

| 314.9 | |||||||

See Condensed Notes to Interim Consolidated Financial Statements.

2

DEERE & COMPANY | |||||||||||||

STATEMENTS OF CONSOLIDATED COMPREHENSIVE INCOME | |||||||||||||

For the Three and Nine Months Ended July 31, 2022 and August 1, 2021 | |||||||||||||

(In millions of dollars) Unaudited | |||||||||||||

Three Months Ended | Nine Months Ended | ||||||||||||

| 2022 |

| 2021 |

| 2022 |

| 2021 |

| |||||

| |||||||||||||

Net Income |

| $ | 1,885 | $ | 1,667 |

| $ | 4,886 | $ | 4,682 | |||

Other Comprehensive Income (Loss), Net of Income Taxes | |||||||||||||

Retirement benefits adjustment | 79 |

| 54 | (137) |

| 208 | |||||||

Cumulative translation adjustment | (269) |

| (114) | (784) |

| 319 | |||||||

Unrealized gain (loss) on derivatives | (1) |

| 1 | 41 |

| 8 | |||||||

Unrealized gain (loss) on debt securities | 6 |

| 8 | (57) |

| (7) | |||||||

Other Comprehensive Income (Loss), Net of Income Taxes | (185) |

| (51) | (937) |

| 528 | |||||||

Comprehensive Income of Consolidated Group | 1,700 |

| 1,616 | 3,949 |

| 5,210 | |||||||

Less: Comprehensive income (loss) attributable to noncontrolling interests | (3) |

| (8) |

| 2 | ||||||||

Comprehensive Income Attributable to Deere & Company |

| $ | 1,703 | $ | 1,616 |

| $ | 3,957 | $ | 5,208 | |||

See Condensed Notes to Interim Consolidated Financial Statements.

3

DEERE & COMPANY | | |||||||||

CONDENSED CONSOLIDATED BALANCE SHEETS | ||||||||||

(In millions of dollars) Unaudited | ||||||||||

| July 31 |

| October 31 |

| August 1 |

| ||||

2022 | 2021 | 2021 |

| |||||||

Assets | ||||||||||

Cash and cash equivalents |

| $ | 4,359 | $ | 8,017 | $ | 7,519 | |||

Marketable securities | 719 |

| 728 |

| 688 | |||||

Trade accounts and notes receivable – net | 6,696 |

| 4,208 |

| 5,268 | |||||

Financing receivables – net | 35,056 |

| 33,799 |

| 31,449 | |||||

5,141 |

| 4,659 |

| 5,401 | ||||||

Other receivables | 1,999 |

| 1,765 |

| 1,702 | |||||

Equipment on operating leases – net | 6,554 |

| 6,988 |

| 6,982 | |||||

Inventories | 9,121 |

| 6,781 |

| 6,410 | |||||

Property and equipment – net | 5,666 |

| 5,820 |

| 5,649 | |||||

Goodwill | 3,754 |

| 3,291 |

| 3,148 | |||||

Other intangible assets – net | 1,281 |

| 1,275 |

| 1,267 | |||||

Retirement benefits | 3,125 |

| 3,601 |

| 990 | |||||

Deferred income taxes | 1,110 |

| 1,037 |

| 1,767 | |||||

Other assets | 2,236 |

| 2,145 |

| 2,448 | |||||

Total Assets |

| $ | 86,817 | $ | 84,114 | $ | 80,688 | |||

Liabilities and Stockholders’ Equity | ||||||||||

Liabilities | ||||||||||

Short-term borrowings | $ | 14,176 | $ | 10,919 | $ | 10,404 | ||||

Short-term securitization borrowings | 4,920 |

| 4,605 |

| 5,277 | |||||

Accounts payable and accrued expenses | 12,986 |

| 12,348 |

| 11,207 | |||||

Deferred income taxes | 561 |

| 576 |

| 515 | |||||

Long-term borrowings | 32,132 |

| 32,888 |

| 32,280 | |||||

Retirement benefits and other liabilities | 2,911 |

| 4,344 |

| 5,272 | |||||

Total liabilities | 67,686 |

| 65,680 |

| 64,955 | |||||

Commitments and contingencies (Note 15) | ||||||||||

Redeemable noncontrolling interest (Note 19) | 95 |

|

| |||||||

Stockholders’ Equity | ||||||||||

Common stock, $1 par value (issued shares at | 5,139 |

| 5,054 |

| 5,031 | |||||

Common stock in treasury | (22,976) |

| (20,533) |

| (19,780) | |||||

Retained earnings | 40,346 |

| 36,449 |

| 35,491 | |||||

Accumulated other comprehensive income (loss) | (3,476) |

| (2,539) |

| (5,011) | |||||

Total Deere & Company stockholders’ equity | 19,033 |

| 18,431 |

| 15,731 | |||||

Noncontrolling interests | 3 |

| 3 |

| 2 | |||||

Total stockholders’ equity | 19,036 |

| 18,434 |

| 15,733 | |||||

Total Liabilities and Stockholders’ Equity | $ | 86,817 | $ | 84,114 | $ | 80,688 | ||||

See Condensed Notes to Interim Consolidated Financial Statements.

4

DEERE & COMPANY | |||||||

STATEMENTS OF CONSOLIDATED CASH FLOWS | |||||||

For the Nine Months Ended July 31, 2022 and August 1, 2021 | |||||||

(In millions of dollars) Unaudited | |||||||

| 2022 |

| 2021 |

| |||

Cash Flows from Operating Activities |

|

| |||||

Net income |

| $ | 4,886 | $ | 4,682 | ||

Adjustments to reconcile net income to net cash provided by operating activities: | |||||||

Provision (credit) for credit losses | 62 |

| (17) | ||||

Provision for depreciation and amortization | 1,443 |

| 1,569 | ||||

Impairment charges | 81 |

| 50 | ||||

Share-based compensation expense | 64 |

| 64 | ||||

Gain on remeasurement of previously held equity investment | (326) |

|

| ||||

Undistributed earnings of unconsolidated affiliates | (1) |

| 4 | ||||

Credit for deferred income taxes | (6) |

| (271) | ||||

Changes in assets and liabilities: | |||||||

Trade, notes, and financing receivables related to sales | (2,357) |

| (444) | ||||

Inventories | (2,526) |

| (1,817) | ||||

Accounts payable and accrued expenses | (15) |

| 742 | ||||

Accrued income taxes payable/receivable | 82 |

| 34 | ||||

Retirement benefits | (1,014) |

| 13 | ||||

Other | 45 |

| (295) | ||||

Net cash provided by operating activities | 418 |

| 4,314 | ||||

Cash Flows from Investing Activities | |||||||

Collections of receivables (excluding receivables related to sales) | 15,774 |

| 14,480 | ||||

Proceeds from sales of equipment on operating leases | 1,501 |

| 1,510 | ||||

Cost of receivables acquired (excluding receivables related to sales) | (18,578) |

| (17,161) | ||||

Acquisitions of businesses, net of cash acquired | (488) |

| (19) | ||||

Purchases of property and equipment | (596) |

| (492) | ||||

Cost of equipment on operating leases acquired | (1,717) |

| (1,210) | ||||

Collateral on derivatives – net | (193) | (189) | |||||

Other | (133) |

| (21) | ||||

Net cash used for investing activities | (4,430) |

| (3,102) | ||||

Cash Flows from Financing Activities | |||||||

Increase in total short-term borrowings | 4,267 |

| 929 | ||||

Proceeds from long-term borrowings | 6,281 |

| 5,877 | ||||

Payments of long-term borrowings | (6,578) |

| (5,172) | ||||

Proceeds from issuance of common stock | 55 |

| 136 | ||||

Repurchases of common stock | (2,477) |

| (1,780) | ||||

Dividends paid | (971) |

| (761) | ||||

Other | (62) |

| (80) | ||||

Net cash provided by (used for) financing activities | 515 |

| (851) | ||||

Effect of Exchange Rate Changes on Cash, Cash Equivalents, and Restricted Cash | (143) |

| 106 | ||||

Net Increase (Decrease) in Cash, Cash Equivalents, and Restricted Cash | (3,640) | 467 | |||||

Cash, Cash Equivalents, and Restricted Cash at Beginning of Period | 8,125 |

| 7,172 | ||||

Cash, Cash Equivalents, and Restricted Cash at End of Period | $ | 4,485 | $ | 7,639 | |||

Components of cash, cash equivalents, and restricted cash | |||||||

Cash and cash equivalents | $ | 4,359 | $ | 7,519 | |||

Restricted cash (Other assets) | 126 | 120 | |||||

Total cash, cash equivalents, and restricted cash | $ | 4,485 | $ | 7,639 | |||

See Condensed Notes to Interim Consolidated Financial Statements.

5

DEERE & COMPANY | |||||||||||||||||||||||

STATEMENTS OF CHANGES IN CONSOLIDATED STOCKHOLDERS’ EQUITY | |||||||||||||||||||||||

For the Three and Nine Months Ended July 31, 2022 and August 1, 2021 | |||||||||||||||||||||||

(In millions of dollars) Unaudited | |||||||||||||||||||||||

Total Stockholders’ Equity | |||||||||||||||||||||||

Deere & Company Stockholders |

| ||||||||||||||||||||||

Accumulated | |||||||||||||||||||||||

Total | Other | Redeemable | |||||||||||||||||||||

Stockholders’ | Common | Treasury | Retained | Comprehensive | Noncontrolling | Noncontrolling | |||||||||||||||||

| Equity |

| Stock |

| Stock |

| Earnings |

| Income (Loss) |

| Interests |

|

| Interest | |||||||||

|

| ||||||||||||||||||||||

Three Months Ended August 1, 2021 | |||||||||||||||||||||||

Balance May 2, 2021 |

| $ | 15,096 | $ | 4,999 | $ | (19,052) | $ | 34,105 | $ | (4,960) | $ | 4 | ||||||||||

Net income |

| 1,667 | 1,667 |

|

| ||||||||||||||||||

Other comprehensive loss |

| (51) | (51) |

|

| ||||||||||||||||||

Repurchases of common stock |

| (736) | (736) | ||||||||||||||||||||

Treasury shares reissued |

| 8 | 8 | ||||||||||||||||||||

Dividends declared |

| (282) | (280) | (2) |

| ||||||||||||||||||

Stock options and other |

| 31 | 32 | (1) |

|

| |||||||||||||||||

Balance August 1, 2021 | $ | 15,733 | $ | 5,031 | $ | (19,780) | $ | 35,491 | $ | (5,011) | $ | 2 |

| ||||||||||

Nine Months Ended August 1, 2021 |

|

| |||||||||||||||||||||

Balance November 1, 2020 |

| $ | 12,944 | $ | 4,895 | $ | (18,065) | $ | 31,646 | $ | (5,539) | $ | 7 |

| |||||||||

ASU No. 2016-13 adoption | (35) | (35) | |||||||||||||||||||||

Net income |

| 4,682 | 4,680 | 2 | |||||||||||||||||||

Other comprehensive income |

| 528 | 528 |

| |||||||||||||||||||

Repurchases of common stock |

| (1,780) | (1,780) | ||||||||||||||||||||

Treasury shares reissued |

| 65 | 65 | ||||||||||||||||||||

Dividends declared |

| (802) | (800) | (2) | |||||||||||||||||||

Stock options and other |

| 131 | 136 |

| (5) |

| |||||||||||||||||

Balance August 1, 2021 | $ | 15,733 | $ | 5,031 | $ | (19,780) | $ | 35,491 | $ | (5,011) | $ | 2 |

| ||||||||||

|

| ||||||||||||||||||||||

Three Months Ended July 31, 2022 | |||||||||||||||||||||||

Balance May 1, 2022 | $ | 18,907 | $ | 5,117 | $ | (21,727) | $ | 38,805 | $ | (3,291) | $ | 3 | $ | 99 | |||||||||

Net income | 1,884 | 1,884 |

| 1 | |||||||||||||||||||

Other comprehensive loss | (185) | (185) |

| (4) | |||||||||||||||||||

Repurchases of common stock | (1,251) | (1,251) | |||||||||||||||||||||

Treasury shares reissued | 2 | 2 | |||||||||||||||||||||

Dividends declared | (343) | (343) |

|

| |||||||||||||||||||

Stock options and other | 22 | 22 |

|

| (1) | ||||||||||||||||||

Balance July 31, 2022 | $ | 19,036 | $ | 5,139 | $ | (22,976) | $ | 40,346 | $ | (3,476) | $ | 3 | $ | 95 | |||||||||

Nine Months Ended July 31, 2022 | |||||||||||||||||||||||

Balance October 31, 2021 | $ | 18,434 | $ | 5,054 | $ | (20,533) | $ | 36,449 | $ | (2,539) | $ | 3 |

| ||||||||||

Acquisitions (see Note 19) |

| $ | 105 | ||||||||||||||||||||

Net income (loss) | 4,887 | 4,885 | 2 | (1) | |||||||||||||||||||

Other comprehensive loss | (937) | (937) |

| (9) | |||||||||||||||||||

Repurchases of common stock | (2,477) | (2,477) | |||||||||||||||||||||

Treasury shares reissued | 34 | 34 | |||||||||||||||||||||

Dividends declared | (990) | (988) | (2) |

| |||||||||||||||||||

Stock options and other | 85 | 85 |

|

|

| ||||||||||||||||||

Balance July 31, 2022 | $ | 19,036 | $ | 5,139 | $ | (22,976) | $ | 40,346 | $ | (3,476) | $ | 3 | $ | 95 | |||||||||

See Condensed Notes to Interim Consolidated Financial Statements.

6

Condensed Notes to Interim Consolidated Financial Statements (Unaudited)

(1) Organization and Consolidation

Deere & Company has been developing innovative solutions to help our customers become more profitable for 185 years. References to Deere & Company, John Deere, Deere, or the Company include our consolidated subsidiaries, including our consolidated variable interest entities (VIEs). The Company is managed through the following operating segments: production and precision agriculture (PPA), small agriculture and turf (SAT), construction and forestry (CF), and financial services (FS). References to agriculture and turf include both production and precision agriculture and small agriculture and turf.

The Company uses a 52/53 week fiscal year with quarters ending on the last Sunday in the reporting period. The third quarter ends for fiscal year 2022 and 2021 were July 31, 2022 and August 1, 2021, respectively. Both third quarters contained 13 weeks, while both year-to-date periods contained 39 weeks. Unless otherwise stated, references to particular years or quarters refer to the Company’s fiscal years generally ending in October and the associated periods in those fiscal years.

Prior to fiscal year 2021, the operating results of the Wirtgen Group (Wirtgen) were incorporated into the Company’s consolidated financial statements using a one-month lag period. The reporting lag was eliminated resulting in one additional month of Wirtgen activity in both the first quarter and the year-to-date period of 2021. The effect was an increase to Net sales of $270 million, which the Company considers immaterial to construction and forestry’s annual Net sales.

As a result of recent acquisitions (see Note 19), the Company updated the presentation on the consolidated balance sheet to remove the following lines: Receivables from unconsolidated affiliates, Investments in unconsolidated affiliates, and Payables to unconsolidated affiliates. These balances are now immaterial to the Company’s consolidated balance sheet and have been reclassified into Other receivables, Other assets, and Accounts payable and accrued expenses, respectively.

The Company consolidates certain VIEs related to retail note securitizations (see Note 9).

(2) Summary of Significant Accounting Policies and New Accounting Standards

Quarterly Financial Statements

The interim consolidated financial statements of Deere & Company have been prepared by the Company, without audit, pursuant to the rules and regulations of the U.S. Securities and Exchange Commission (SEC). Certain information and footnote disclosures normally included in annual financial statements prepared in accordance with accounting principles generally accepted in the U.S. have been condensed or omitted as permitted by such rules and regulations. All adjustments, consisting of normal recurring adjustments, have been included. Management believes the disclosures are adequate to present fairly the financial position, results of operations, and cash flows at the dates and for the periods presented. It is suggested these interim consolidated financial statements be read in conjunction with the consolidated financial statements and the notes thereto appearing in the Company’s latest Annual Report on Form 10-K. Results for interim periods are not necessarily indicative of those to be expected for the fiscal year.

Use of Estimates in Financial Statements

The preparation of financial statements in conformity with accounting principles generally accepted in the U.S. requires management to make estimates and assumptions that affect the reported amounts and related disclosures. Actual results could differ from those estimates.

Revenue Recognition

Prior to fiscal year 2022, certain goods were shipped to Canadian dealers on a consignment basis under which the risk and rewards of ownership were not transferred to the dealer at the time the goods were delivered. Accordingly, sales were not recorded until a retail customer purchased the goods. The dealer contract in Canada was changed for goods delivered after November 1, 2021, resulting in transfer of control and revenue recognition upon delivery. For certain goods delivered to Canadian dealers prior to November 1, 2021, the dealer consignment terms already in place remain in effect. As of July 31, 2022 and October 31, 2021, the remaining consigned inventory was $26 million and $150 million, respectively.

New Accounting Standards

The Company closely monitors all Accounting Standard Updates (ASUs) issued by the Financial Accounting Standards Board and other authoritative guidance. ASUs adopted in 2022 did not have a material impact on the Company’s financial statements, and ASUs to be adopted in future periods are being evaluated and at this point are not expected to have a material impact on the Company’s financial statements.

7

(3) Revenue Recognition

The Company’s Net sales and revenues by primary geographic market, major product line, and timing of revenue recognition in millions of dollars follow:

Three Months Ended July 31, 2022 | ||||||||||||||||

| Production & Precision Ag |

| Small Ag & Turf |

| Construction |

| Financial |

| Total | |||||||

Primary geographic markets: |

|

| ||||||||||||||

United States | $ | 2,904 | $ | 2,177 | $ | 1,789 | $ | 602 | $ | 7,472 | ||||||

Canada | 451 | 185 | 288 |

| 149 |

| 1,073 | |||||||||

Western Europe | 645 | 646 | 380 |

| 25 |

| 1,696 | |||||||||

Central Europe and CIS | 348 | 109 | 111 |

| 14 |

| 582 | |||||||||

Latin America | 1,327 | 155 | 459 |

| 77 |

| 2,018 | |||||||||

Asia, Africa, Australia, New Zealand, and Middle East | 510 | 419 | 296 | 36 | 1,261 | |||||||||||

Total | $ | 6,185 | $ | 3,691 | $ | 3,323 | $ | 903 | $ | 14,102 | ||||||

Major product lines: |

|

| ||||||||||||||

Production agriculture | $ | 6,019 |

|

|

| $ | 6,019 | |||||||||

Small agriculture |

| $ | 2,705 |

|

|

|

| 2,705 | ||||||||

Turf |

| 842 |

|

|

|

| 842 | |||||||||

Construction |

|

| $ | 1,506 |

|

|

| 1,506 | ||||||||

Compact construction |

|

| 460 |

| 460 | |||||||||||

Roadbuilding |

|

| 910 |

|

|

| 910 | |||||||||

Forestry |

|

| 316 |

|

|

| 316 | |||||||||

Financial products | 17 | 15 | 6 | $ | 903 |

| 941 | |||||||||

Other | 149 | 129 | 125 |

|

|

| 403 | |||||||||

Total | $ | 6,185 | $ | 3,691 | $ | 3,323 | $ | 903 | $ | 14,102 | ||||||

Revenue recognized: |

|

| ||||||||||||||

At a point in time | $ | 6,154 | $ | 3,672 | $ | 3,303 | $ | 27 | $ | 13,156 | ||||||

Over time | 31 | 19 | 20 | 876 | 946 | |||||||||||

Total | $ | 6,185 | $ | 3,691 | $ | 3,323 | $ | 903 | $ | 14,102 | ||||||

| Nine Months Ended July 31, 2022 | |||||||||||||||

Production & Precision Ag |

| Small Ag & Turf |

| Construction |

| Financial |

| Total | ||||||||

Primary geographic markets: | ||||||||||||||||

United States | $ | 6,946 | $ | 5,718 | $ | 5,157 | $ | 1,744 | $ | 19,565 | ||||||

Canada | 899 | 468 | 975 |

| 450 |

| 2,792 | |||||||||

Western Europe | 1,648 | 1,836 | 1,202 |

| 76 |

| 4,762 | |||||||||

Central Europe and CIS | 954 | 386 | 452 |

| 36 |

| 1,828 | |||||||||

Latin America | 3,229 | 393 | 1,020 |

| 218 |

| 4,860 | |||||||||

Asia, Africa, Australia, New Zealand, and Middle East | 1,118 | 1,170 | 833 | 113 | 3,234 | |||||||||||

Total | $ | 14,794 | $ | 9,971 | $ | 9,639 | $ | 2,637 | $ | 37,041 | ||||||

Major product lines: |

|

| ||||||||||||||

Production agriculture | $ | 14,333 |

|

|

| $ | 14,333 | |||||||||

Small agriculture |

| $ | 7,305 |

|

|

|

| 7,305 | ||||||||

Turf |

| 2,286 |

|

|

|

| 2,286 | |||||||||

Construction |

|

| $ | 4,198 |

|

|

| 4,198 | ||||||||

Compact construction |

|

| 1,208 |

| 1,208 | |||||||||||

Roadbuilding |

|

| 2,619 |

|

|

| 2,619 | |||||||||

Forestry |

|

| 946 |

|

| 946 | ||||||||||

Financial products | 39 | 35 | 17 | $ | 2,637 |

| 2,728 | |||||||||

Other | 422 | 345 | 651 |

|

|

| 1,418 | |||||||||

Total | $ | 14,794 | $ | 9,971 | $ | 9,639 | $ | 2,637 | $ | 37,041 | ||||||

Revenue recognized: |

|

| ||||||||||||||

At a point in time | $ | 14,694 | $ | 9,919 | $ | 9,580 | $ | 77 | $ | 34,270 | ||||||

Over time | 100 | 52 | 59 | 2,560 | 2,771 | |||||||||||

Total | $ | 14,794 | $ | 9,971 | $ | 9,639 | $ | 2,637 | $ | 37,041 | ||||||

8

Three Months Ended August 1, 2021 | ||||||||||||||||

| Production & Precision Ag |

| Small Ag & Turf |

| Construction |

| Financial |

| Total | |||||||

Primary geographic markets: |

|

| ||||||||||||||

United States | $ | 1,995 | $ | 1,753 | $ | 1,559 | $ | 605 | $ | 5,912 | ||||||

Canada | 253 | 153 | 285 |

| 162 |

| 853 | |||||||||

Western Europe | 566 | 679 | 455 | 27 |

| 1,727 | ||||||||||

Central Europe and CIS | 398 | 117 | 241 | 10 |

| 766 | ||||||||||

Latin America | 758 | 125 | 227 | 60 |

| 1,170 | ||||||||||

Asia, Africa, Australia, New Zealand, and Middle East | 368 | 385 | 308 | 38 | 1,099 | |||||||||||

Total | $ | 4,338 | $ | 3,212 | $ | 3,075 | $ | 902 | $ | 11,527 | ||||||

Major product lines: |

|

| ||||||||||||||

Production agriculture | $ | 4,179 |

|

| $ | 4,179 | ||||||||||

Small agriculture | $ | 2,355 |

|

|

|

| 2,355 | |||||||||

Turf | 719 |

|

|

|

| 719 | ||||||||||

Construction |

| $ | 1,283 |

|

|

| 1,283 | |||||||||

Compact construction |

| 398 |

| 398 | ||||||||||||

Roadbuilding |

| 948 |

|

|

| 948 | ||||||||||

Forestry |

| 342 |

|

|

| 342 | ||||||||||

Financial products | 13 | 12 | 5 | $ | 902 |

| 932 | |||||||||

Other | 146 | 126 | 99 |

|

|

| 371 | |||||||||

Total | $ | 4,338 | $ | 3,212 | $ | 3,075 | $ | 902 | $ | 11,527 | ||||||

Revenue recognized: |

|

| ||||||||||||||

At a point in time | $ | 4,293 | $ | 3,191 | $ | 3,052 | $ | 27 | $ | 10,563 | ||||||

Over time | 45 | 21 | 23 | 875 | 964 | |||||||||||

Total | $ | 4,338 | $ | 3,212 | $ | 3,075 | $ | 902 | $ | 11,527 | ||||||

Nine Months Ended August 1, 2021 | ||||||||||||||||

| Production & Precision Ag |

| Small Ag & Turf |

| Construction |

| Financial |

| Total | |||||||

Primary geographic markets: | ||||||||||||||||

United States | $ | 5,814 | $ | 5,014 | $ | 4,242 | $ | 1,812 | $ | 16,882 | ||||||

Canada | 617 | 376 | 793 | 469 |

| 2,255 | ||||||||||

Western Europe | 1,604 | 1,903 | 1,408 | 77 |

| 4,992 | ||||||||||

Central Europe and CIS | 1,090 | 361 | 628 | 28 |

| 2,107 | ||||||||||

Latin America | 1,971 | 305 | 617 | 179 |

| 3,072 | ||||||||||

Asia, Africa, Australia, New Zealand, and Middle East | 991 | 1,230 | 1,054 | 114 | 3,389 | |||||||||||

Total | $ | 12,087 | $ | 9,189 | $ | 8,742 | $ | 2,679 | $ | 32,697 | ||||||

Major product lines: |

|

| ||||||||||||||

Production agriculture | $ | 11,656 |

|

|

| $ | 11,656 | |||||||||

Small agriculture |

| $ | 6,583 |

|

|

| 6,583 | |||||||||

Turf |

| 2,268 |

|

|

| 2,268 | ||||||||||

Construction |

|

| $ | 3,402 |

|

| 3,402 | |||||||||

Compact construction |

|

| 1,140 |

| 1,140 | |||||||||||

Roadbuilding |

|

| 2,924 |

|

| 2,924 | ||||||||||

Forestry |

|

| 975 |

|

| 975 | ||||||||||

Financial products | 41 | 32 | 17 | $ | 2,679 |

| 2,769 | |||||||||

Other | 390 | 306 | 284 |

|

| 980 | ||||||||||

Total | $ | 12,087 | $ | 9,189 | $ | 8,742 | $ | 2,679 | $ | 32,697 | ||||||

Revenue recognized: |

|

| ||||||||||||||

At a point in time | $ | 11,960 | $ | 9,137 | $ | 8,666 | $ | 77 | $ | 29,840 | ||||||

Over time | 127 | 52 | 76 | 2,602 | 2,857 | |||||||||||

Total | $ | 12,087 | $ | 9,189 | $ | 8,742 | $ | 2,679 | $ | 32,697 | ||||||

9

The Company invoices in advance of recognizing the sale of certain products and the revenue for certain services. These items are primarily for premiums for extended warranties, advance payments for future equipment sales, and subscription and service revenue related to precision guidance and telematic services. These advanced customer payments are presented as deferred revenue, a contract liability, in Accounts payable and accrued expenses in the consolidated balance sheets. The deferred revenue received, but not recognized in revenue, including extended warranty premiums also shown in Note 15, was $1,424 million, $1,344 million, and $1,259 million at July 31, 2022, October 31, 2021, and August 1, 2021, respectively. The contract liability is reduced as the revenue is recognized. During the three months ended July 31, 2022 and August 1, 2021, $93 million and $108 million, respectively, of revenue was recognized from deferred revenue that was recorded as a contract liability at the beginning of the respective fiscal year. During the nine months ended July 31, 2022 and August 1, 2021, $488 million and $442 million, respectively, of revenue was recognized from deferred revenue that was recorded as a contract liability at the beginning of the respective fiscal year.

The amount of unsatisfied performance obligations for contracts with an original duration greater than one year is $1,167 million at July 31, 2022. The estimated revenue to be recognized by fiscal year follows in millions of dollars: remainder of - $104, - $337, - $283, - $196, - $109, - $60 and - $78. As permitted, the Company elected only to disclose remaining performance obligations with an original contract duration greater than one year. The contracts with an expected duration of one year or less are generally for sales of equipment, service parts, repair services, and certain telematics services.

(4) Other Comprehensive Income Items

The after-tax components of accumulated other comprehensive income (loss) in millions of dollars follow:

July 31 | October 31 | August 1 | ||||||||

2022 | 2021 | 2021 | ||||||||

Retirement benefits adjustment | $ | (1,171) | $ | (1,034) | $ | (3,710) | ||||

Cumulative translation adjustment | (2,262) | (1,478) | (1,277) | |||||||

Unrealized loss on derivatives | (1) | (42) | (50) | |||||||

Unrealized gain (loss) on debt securities | (42) | 15 | 26 | |||||||

Total accumulated other comprehensive income (loss) | $ | (3,476) | $ | (2,539) | $ | (5,011) | ||||

Following are amounts recorded in and reclassifications out of other comprehensive income (loss), and the income tax effects, in millions of dollars. Retirement benefits adjustment reclassifications for actuarial (gain) loss, prior service (credit) cost, and settlements/curtailment are included in net periodic pension and other postretirement benefit costs (see Note 6).

| Before |

| Tax |

| After |

| ||||

Tax | (Expense) | Tax |

| |||||||

Three Months Ended July 31, 2022 | Amount | Credit | Amount |

| ||||||

Cumulative translation adjustment | $ | (267) | $ | (2) | $ | (269) | ||||

Unrealized gain (loss) on derivatives: | ||||||||||

Unrealized hedging gain (loss) | 1 | 1 | ||||||||

Reclassification of realized (gain) loss to: | ||||||||||

Interest rate contracts – Interest expense | (3) | 1 | (2) | |||||||

Net unrealized gain (loss) on derivatives | (2) | 1 | (1) | |||||||

Unrealized gain (loss) on debt securities: | ||||||||||

Unrealized holding gain (loss) | 6 | (1) | 5 | |||||||

Reclassification of realized (gain) loss – Other income | 1 |

| 1 | |||||||

Net unrealized gain (loss) on debt securities | 7 | (1) | 6 | |||||||

Retirement benefits adjustment: | ||||||||||

Net actuarial gain (loss) | 34 | (9) | 25 | |||||||

Reclassification to Other operating expenses through amortization of: | ||||||||||

Actuarial (gain) loss | 27 | (7) | 20 | |||||||

Prior service (credit) cost | 8 | (2) | 6 | |||||||

Settlements/curtailment | 36 | (8) | 28 | |||||||

Net unrealized gain (loss) on retirement benefits adjustment | 105 | (26) | 79 | |||||||

Total other comprehensive income (loss) |

| $ | (157) | $ | (28) | $ | (185) | |||

10

| Before |

| Tax |

| After |

| ||||

Tax | (Expense) | Tax |

| |||||||

Nine Months Ended July 31, 2022 | Amount | Credit | Amount |

| ||||||

Cumulative translation adjustment |

| $ | (774) | $ | (10) | $ | (784) | |||

Unrealized gain (loss) on derivatives: | ||||||||||

Unrealized hedging gain (loss) | 52 | (11) | 41 | |||||||

Net unrealized gain (loss) on derivatives | 52 | (11) | 41 | |||||||

Unrealized gain (loss) on debt securities: | ||||||||||

Unrealized holding gain (loss) | (74) | 16 | (58) | |||||||

Reclassification of realized (gain) loss – Other income | 1 |

| 1 | |||||||

Net unrealized gain (loss) on debt securities | (73) | 16 | (57) | |||||||

Retirement benefits adjustment: | ||||||||||

Net actuarial gain (loss) and prior service (cost) | (338) | 81 | (257) | |||||||

Reclassification to Other operating expenses through amortization of: | ||||||||||

Actuarial (gain) loss | 94 | (24) | 70 | |||||||

Prior service (credit) cost | 22 | (6) | 16 | |||||||

Settlements/curtailment | 44 | (10) | 34 | |||||||

Net unrealized gain (loss) on retirement benefits adjustment | (178) | 41 | (137) | |||||||

Total other comprehensive income (loss) |

| $ | (973) | $ | 36 | $ | (937) | |||

| Before |

| Tax |

| After |

| ||||

Tax | (Expense) | Tax |

| |||||||

Three Months Ended August 1, 2021 | Amount | Credit | Amount |

| ||||||

Cumulative translation adjustment |

| $ | (112) | $ | (2) | $ | (114) | |||

Unrealized gain (loss) on derivatives: | ||||||||||

Unrealized hedging gain (loss) | (1) | (1) | ||||||||

Reclassification of realized (gain) loss to: |

| |||||||||

Interest rate contracts – Interest expense | 3 | (1) | 2 | |||||||

Net unrealized gain (loss) on derivatives | 2 | (1) | 1 | |||||||

Unrealized gain (loss) on debt securities: | ||||||||||

Unrealized holding gain (loss) | 11 | (3) | 8 | |||||||

Net unrealized gain (loss) on debt securities | 11 | (3) | 8 | |||||||

Retirement benefits adjustment: | ||||||||||

Net actuarial gain (loss) | (5) | 1 | (4) | |||||||

Reclassification to Other operating expenses through amortization of: |

| |||||||||

Actuarial (gain) loss | 71 | (17) | 54 | |||||||

Prior service (credit) cost | 1 |

| 1 | |||||||

Settlements | 4 | (1) | 3 | |||||||

Net unrealized gain (loss) on retirement benefits adjustment | 71 | (17) | 54 | |||||||

Total other comprehensive income (loss) |

| $ | (28) | $ | (23) | $ | (51) | |||

11

| Before |

| Tax |

| After |

| ||||

Tax | (Expense) | Tax |

| |||||||

Nine Months Ended August 1, 2021 | Amount | Credit | Amount |

| ||||||

Cumulative translation adjustment |

| $ | 319 |

| $ | 319 | ||||

Unrealized gain (loss) on derivatives: | ||||||||||

Unrealized hedging gain (loss) | (1) | (1) | ||||||||

Reclassification of realized (gain) loss to: |

| |||||||||

Interest rate contracts – Interest expense | 11 | $ | (2) | 9 | ||||||

Net unrealized gain (loss) on derivatives | 10 | (2) | 8 | |||||||

Unrealized gain (loss) on debt securities: | ||||||||||

Unrealized holding gain (loss) | (6) | (1) | (7) | |||||||

Net unrealized gain (loss) on debt securities | (6) | (1) | (7) | |||||||

Retirement benefits adjustment: | ||||||||||

Net actuarial gain (loss) | 35 | (8) | 27 | |||||||

Reclassification to Other operating expenses through amortization of: |

| |||||||||

Actuarial (gain) loss | 213 | (53) | 160 | |||||||

Prior service (credit) cost | 5 | (1) | 4 | |||||||

Settlements | 22 | (5) | 17 | |||||||

Net unrealized gain (loss) on retirement benefits adjustment | 275 | (67) | 208 | |||||||

Total other comprehensive income (loss) |

| $ | 598 | $ | (70) | $ | 528 | |||

(5) Earnings Per Share

A reconciliation of basic and diluted net income per share attributable to Deere & Company follows in millions, except per share amounts:

| Three Months Ended | Nine Months Ended |

| ||||||||||

July 31 | August 1 | July 31 | August 1 |

| |||||||||

2022 | 2021 | 2022 | 2021 |

| |||||||||

Net income attributable to Deere & Company |

| $ | 1,884 |

| $ | 1,667 |

| $ | 4,885 |

| $ | 4,680 | |

Average shares outstanding | 304.1 |

| 311.0 | 305.8 |

| 312.4 | |||||||

Basic per share | $ | 6.20 | $ | 5.36 | $ | 15.97 | $ | 14.98 | |||||

Average shares outstanding | 304.1 |

| 311.0 | 305.8 |

| 312.4 | |||||||

Effect of dilutive share-based compensation | 1.6 |

| 2.4 | 1.9 |

| 2.5 | |||||||

Total potential shares outstanding | 305.7 |

| 313.4 | 307.7 |

| 314.9 | |||||||

Diluted per share | $ | 6.16 | $ | 5.32 | $ | 15.88 | $ | 14.86 | |||||

During both the third quarter and first nine months of 2022, .2 million shares were excluded from the computation because the incremental shares would have been antidilutive.

12

(6) Pension and Other Postretirement Benefits

The Company has several defined benefit pension plans and postretirement benefit (OPEB) plans, primarily health care and life insurance plans, covering its U.S. employees and employees in certain foreign countries.

The components of net periodic pension cost consisted of the following in millions of dollars:

Three Months Ended | Nine Months Ended |

| |||||||||||

July 31 | August 1 | July 31 | August 1 |

| |||||||||

2022 | 2021 | 2022 | 2021 |

| |||||||||

Service cost |

| $ | 86 |

| $ | 83 |

| $ | 265 |

| $ | 251 | |

85 |

| 69 | 242 |

| 207 | ||||||||

(182) |

| (199) | (544) |

| (599) | ||||||||

31 |

| 64 | 107 |

| 192 | ||||||||

9 |

| 2 | 25 |

| 8 | ||||||||

36 |

| 4 | 44 |

| 22 | ||||||||

Net cost | $ | 65 | $ | 23 | $ | 139 | $ | 81 | |||||

The components of net periodic OPEB cost consisted of the following in millions of dollars:

Three Months Ended | Nine Months Ended |

| |||||||||||

July 31 | August 1 | July 31 | August 1 |

| |||||||||

2022 | 2021 | 2022 | 2021 |

| |||||||||

Service cost |

| $ | 11 |

| $ | 12 |

| $ | 34 |

| $ | 36 | |

25 |

| 25 | 74 |

| 76 | ||||||||

(28) |

| (19) | (83) |

| (58) | ||||||||

(4) |

| 7 | (13) |

| 21 | ||||||||

(1) |

| (1) | (3) |

| (3) | ||||||||

Net cost | $ | 3 | $ | 24 | $ | 9 | $ | 72 | |||||

The components of net periodic pension and OPEB costs excluding the service cost component are included in the line item Other operating expenses in the statements of consolidated income.

On November 17, 2021, employees represented by the International Union, United Automobile, Aerospace and Agricultural Implement Workers of America (UAW) approved a new collective bargaining agreement. In the first quarter of 2022, the Company remeasured the U.S. hourly pension plan due to the new collective bargaining agreement, which decreased the plan’s funded status by approximately $495 million and will increase pension expense in 2022 by nearly $80 million with $35 million negatively impacting operating profit in 2022.

During the third quarter of , the Company remeasured the U.S. hourly pension plan when 10 percent of active, eligible employees elected to freeze their defined benefit pension plan benefit for an enhanced defined contribution benefit. The remeasurement resulted in a $34 million curtailment loss, while the impact to the plan’s funded status was not material.

During the first nine months of 2022, the Company contributed $67 million to its pension plans and $1,109 million to its OPEB plans. The OPEB contributions include a voluntary contribution of $1,000 million to a U.S. plan on November 30, 2021. The Company presently anticipates contributing an additional $16 million to its pension plans and $28 million to its OPEB plans during the remainder of 2022. The remaining pension and OPEB contributions are primarily direct benefit payments from Company funds.

13

(7) Segment Reporting

Worldwide Net sales and revenues, operating profit, and identifiable assets by segment were as follows in millions of dollars:

Three Months Ended | Nine Months Ended |

| |||||||||||||||

| July 31 | August 1 | % | July 31 | August 1 | % |

| ||||||||||

2022 | 2021 | Change | 2022 | 2021 | Change |

| |||||||||||

Net sales and revenues: |

|

|

|

|

|

|

|

|

|

|

| ||||||

Production & precision ag net sales |

| $ | 6,096 | $ | 4,250 | +43 |

| $ | 14,568 | $ | 11,848 | +23 | |||||

Small ag & turf net sales | 3,635 | 3,147 | +16 | 9,836 | 9,051 | +9 | |||||||||||

Construction & forestry net sales | 3,269 |

| 3,016 | +8 | 9,161 |

| 8,562 | +7 | |||||||||

Financial services revenues | 903 |

| 902 | 2,637 |

| 2,679 | -2 | ||||||||||

Other revenues | 199 |

| 212 | -6 | 839 |

| 557 | +51 | |||||||||

Total net sales and revenues |

| $ | 14,102 | $ | 11,527 | +22 |

| $ | 37,041 | $ | 32,697 | +13 | |||||

Operating profit: | |||||||||||||||||

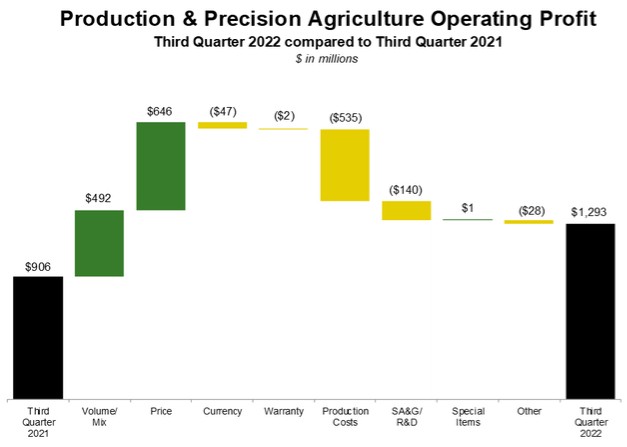

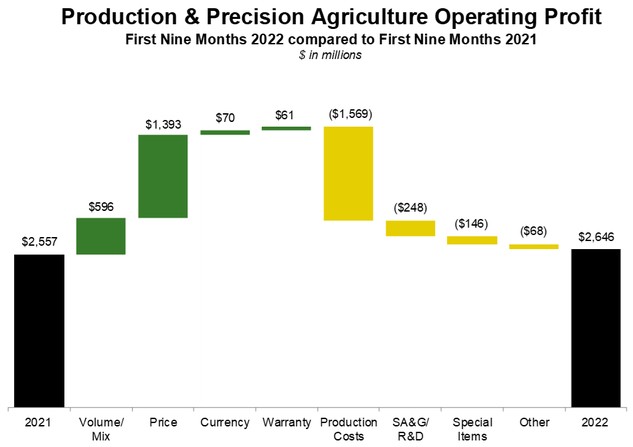

Production & precision ag |

| $ | 1,293 | $ | 906 | +43 |

| $ | 2,646 | $ | 2,557 | +3 | |||||

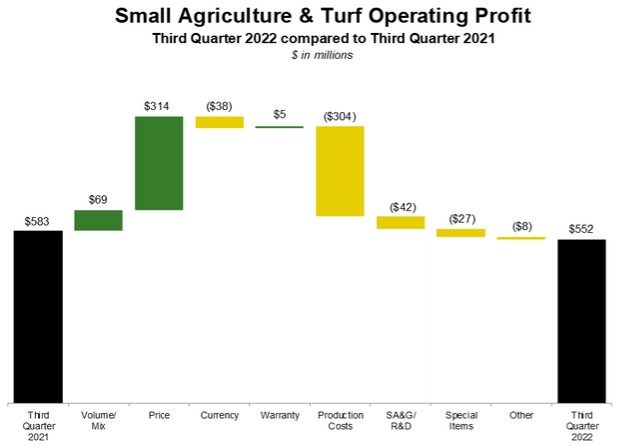

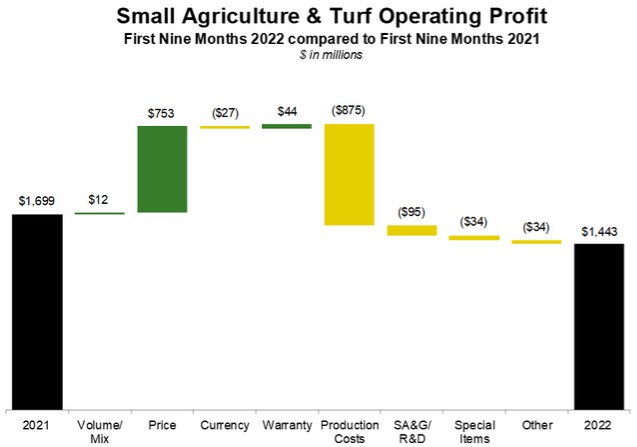

Small ag & turf | 552 | 583 | -5 | 1,443 | 1,699 | -15 | |||||||||||

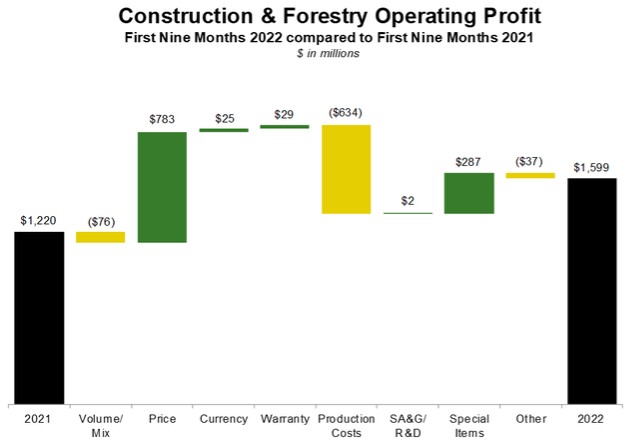

Construction & forestry | 514 |

| 463 | +11 | 1,599 |

| 1,220 | +31 | |||||||||

Financial services | 287 |

| 291 | -1 | 864 |

| 844 | +2 | |||||||||

Total operating profit | 2,646 |

| 2,243 | +18 | 6,552 |

| 6,320 | +4 | |||||||||

Reconciling items | (108) |

| (85) | +27 | (303) |

| (312) | -3 | |||||||||

Income taxes | (654) |

| (491) | +33 | (1,364) |

| (1,328) | +3 | |||||||||

Net income attributable to Deere & Company |

| $ | 1,884 | $ | 1,667 | +13 |

| $ | 4,885 | $ | 4,680 | +4 | |||||

Intersegment sales and revenues: | |||||||||||||||||

Production & precision ag net sales |

| $ | 5 | $ | 8 | -38 |

| $ | 15 | $ | 21 | -29 | |||||

Small ag & turf net sales | 2 | 2 | 8 | 9 | -11 | ||||||||||||

Construction & forestry net sales |

|

|

|

|

| ||||||||||||

Financial services revenues | 81 |

| 61 | +33 | 214 |

| 172 | +24 | |||||||||

Operating profit is income from continuing operations before reconciling items and income taxes. Operating profit of the financial services segment includes the effect of interest expense and foreign exchange gains and losses. Reconciling items to net income are primarily corporate expenses, certain external interest expense, certain foreign exchange gains and losses, pension and OPEB benefit costs excluding the service cost component, and net income attributable to noncontrolling interests.

| July 31 |

| October 31 | August 1 |

| |||||

2022 | 2021 | 2021 |

| |||||||

Identifiable assets: | ||||||||||

Production & precision ag |

| $ | 8,728 | $ | 7,021 | $ | 6,910 | |||

Small ag & turf | 4,361 | 3,959 | 3,643 | |||||||

Construction & forestry | 6,824 |

| 6,457 |

| 6,378 | |||||

Financial services | 56,008 |

| 51,624 |

| 51,647 | |||||

Corporate | 10,896 |

| 15,053 |

| 12,110 | |||||

Total assets |

| $ | 86,817 | $ | 84,114 | $ | 80,688 | |||

(8) Financing Receivables

The Company monitors the credit quality of financing receivables based on delinquency status. Past due balances of financing receivables still accruing finance income represent the total balance held (principal plus accrued interest) with any payment amounts 30 days or more past the contractual payment due date. Non-performing financing receivables represent receivables for which the Company has ceased accruing finance income. The Company ceases accruing finance income when these receivables are generally 90 days delinquent. Generally, when receivables are 120 days delinquent the estimated uncollectible amount from the customer is written off to the allowance for credit losses. Finance income for non-performing receivables is recognized on a cash basis. Accrual of finance income is generally resumed when the receivable becomes contractually current and collections are reasonably assured.

14

The credit quality analysis of retail notes, financing leases, and revolving charge accounts (collectively, retail customer receivables) by year of origination was as follows in millions of dollars:

July 31, 2022 | |||||||||||||||||||||||||

2022 | 2021 | 2020 | 2019 | 2018 | Prior Years | Revolving Charge Accounts | Total | ||||||||||||||||||

Retail customer receivables: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

Agriculture and turf | |||||||||||||||||||||||||

Current | $ | 9,161 | $ | 9,169 | $ | 4,713 | $ | 2,234 | $ | 935 | $ | 378 | $ | 3,962 | $ | 30,552 | |||||||||

30-59 days past due | 40 | 70 | 38 | 23 | 8 | 4 | 18 | 201 | |||||||||||||||||

60-89 days past due | 15 | 24 | 15 | 7 | 3 | 1 | 5 | 70 | |||||||||||||||||

90+ days past due |

|

|

|

|

|

|

|

| |||||||||||||||||

Non-performing | 17 | 62 | 48 | 37 | 19 | 27 | 7 | 217 | |||||||||||||||||

Construction and forestry | |||||||||||||||||||||||||

Current | 2,336 | 2,249 | 1,004 | 382 | 106 | 20 | 102 | 6,199 | |||||||||||||||||

30-59 days past due | 47 | 54 | 26 | 12 | 4 | 1 | 3 | 147 | |||||||||||||||||

60-89 days past due | 14 | 14 | 12 | 4 | 1 |

| 1 | 46 | |||||||||||||||||

90+ days past due |

| 11 | 3 | 1 |

| 3 |

| 18 | |||||||||||||||||

Non-performing | 13 | 63 | 49 | 25 | 9 | 4 | 1 | 164 | |||||||||||||||||

Total retail customer receivables | $ | 11,643 | $ | 11,716 | $ | 5,908 | $ | 2,725 | $ | 1,085 | $ | 438 | $ | 4,099 | $ | 37,614 | |||||||||

October 31, 2021 | |||||||||||||||||||||||||

2021 | 2020 | 2019 | 2018 | 2017 | Prior | Revolving Charge Accounts | Total | ||||||||||||||||||

Retail customer receivables: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

Agriculture and turf | |||||||||||||||||||||||||

Current | $ | 12,877 | $ | 6,676 | $ | 3,463 | $ | 1,738 | $ | 728 | $ | 211 | $ | 3,704 | $ | 29,397 | |||||||||

30-59 days past due | 43 | 53 | 29 | 16 | 7 | 3 | 14 | 165 | |||||||||||||||||

60-89 days past due | 16 | 23 | 12 | 6 | 3 | 1 | 4 | 65 | |||||||||||||||||

90+ days past due |

| 1 | 1 | ||||||||||||||||||||||

Non-performing | 23 | 57 | 53 | 32 | 17 | 23 | 7 | 212 | |||||||||||||||||

Construction and forestry | |||||||||||||||||||||||||

Current | 3,122 | 1,575 | 754 | 273 | 57 | 7 | 92 | 5,880 | |||||||||||||||||

30-59 days past due | 50 | 40 | 27 | 7 | 4 | 1 | 3 | 132 | |||||||||||||||||

60-89 days past due | 15 | 11 | 9 | 6 | 1 | 1 | 43 | ||||||||||||||||||

90+ days past due | 1 | 2 | 3 | 3 | 4 | 2 | 15 | ||||||||||||||||||

Non-performing | 26 | 56 | 39 | 17 | 7 | 3 | 148 | ||||||||||||||||||

Total retail customer receivables | $ | 16,173 | $ | 8,494 | $ | 4,389 | $ | 2,098 | $ | 828 | $ | 251 | $ | 3,825 | $ | 36,058 | |||||||||

August 1, 2021 | |||||||||||||||||||||||||

2021 | 2020 | 2019 | 2018 | 2017 | Prior | Revolving Charge Accounts | Total | ||||||||||||||||||

Retail customer receivables: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

Agriculture and turf | |||||||||||||||||||||||||

Current | $ | 9,159 | $ | 7,516 | $ | 3,938 | $ | 2,053 | $ | 910 | $ | 317 | $ | 3,658 | $ | 27,551 | |||||||||

30-59 days past due | 38 | 54 | 35 | 19 | 7 | 3 | 13 | 169 | |||||||||||||||||

60-89 days past due | 14 | 28 | 15 | 6 | 3 | 1 | 4 | 71 | |||||||||||||||||

90+ days past due |

| 1 |

|

|

|

|

| 1 | |||||||||||||||||

Non-performing | 12 | 58 | 63 | 42 | 22 | 30 | 6 | 233 | |||||||||||||||||

Construction and forestry | |||||||||||||||||||||||||

Current | 2,327 | 1,845 | 938 | 357 | 84 | 13 | 86 | 5,650 | |||||||||||||||||

30-59 days past due | 35 | 44 | 26 | 9 | 4 | 1 | 3 | 122 | |||||||||||||||||

60-89 days past due | 13 | 19 | 10 | 5 | 1 | 1 | 1 | 50 | |||||||||||||||||

90+ days past due | 4 | 2 | 9 | 5 | 6 | 2 |

| 28 | |||||||||||||||||

Non-performing | 12 | 47 | 41 | 19 | 8 | 4 | 1 | 132 | |||||||||||||||||

Total retail customer receivables | $ | 11,614 | $ | 9,614 | $ | 5,075 | $ | 2,515 | $ | 1,045 | $ | 372 | $ | 3,772 | $ | 34,007 | |||||||||

15

The credit quality analysis of wholesale receivables by year of origination was as follows in millions of dollars:

July 31, 2022 | |||||||||||||||||||||||||

2022 | 2021 | 2020 | 2019 | 2018 | Prior | Revolving | Total | ||||||||||||||||||

Wholesale receivables: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

Agriculture and turf | |||||||||||||||||||||||||

Current | $ | 289 | $ | 99 | $ | 34 | $ | 6 | $ | 1 | $ | 1 | $ | 2,022 | $ | 2,452 | |||||||||

30+ days past due |

|

|

|

|

|

|

|

| |||||||||||||||||

Non-performing |

|

|

| 1 |

|

|

| 1 | |||||||||||||||||

Construction and forestry | |||||||||||||||||||||||||

Current | 11 | 32 | 3 | 1 |

| 1 | 283 | 331 | |||||||||||||||||

30+ days past due |

|

|

|

|

| 1 |

| 1 | |||||||||||||||||

Non-performing |

|

|

|

|

|

|

|

| |||||||||||||||||

Total wholesale receivables | $ | 300 | $ | 131 | $ | 37 | $ | 8 | $ | 1 | $ | 3 | $ | 2,305 | $ | 2,785 | |||||||||

October 31, 2021 | |||||||||||||||||||||||||

2021 | 2020 | 2019 | 2018 | 2017 | Prior | Revolving | Total | ||||||||||||||||||

Wholesale receivables: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

Agriculture and turf | |||||||||||||||||||||||||

Current | $ | 346 | $ | 80 | $ | 22 | $ | 9 | $ | 3 | $ | 1,696 | $ | 2,156 | |||||||||||

30+ days past due |

| ||||||||||||||||||||||||

Non-performing | 12 | 12 | |||||||||||||||||||||||

Construction and forestry | |||||||||||||||||||||||||

Current | 41 | 7 | 7 | 1 | $ | 1 | 340 | 397 | |||||||||||||||||

30+ days past due | 1 | 1 | |||||||||||||||||||||||

Non-performing |

| ||||||||||||||||||||||||

Total wholesale receivables | $ | 387 | $ | 87 | $ | 41 | $ | 9 | $ | 4 | $ | 2 | $ | 2,036 | $ | 2,566 | |||||||||

August 1, 2021 | |||||||||||||||||||||||||

2021 | 2020 | 2019 | 2018 | 2017 | Prior | Revolving | Total | ||||||||||||||||||

Wholesale receivables: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

Agriculture and turf | |||||||||||||||||||||||||

Current | $ | 263 | $ | 110 | $ | 38 | $ | 13 | $ | 3 | $ | 1 | $ | 2,256 | $ | 2,684 | |||||||||

30+ days past due |

|

|

|

|

|

|

|

| |||||||||||||||||

Non-performing |

|

| 18 |

|

|

|

| 18 | |||||||||||||||||

Construction and forestry | |||||||||||||||||||||||||

Current | 8 | 8 | 8 | 1 | 1 | 1 | 287 | 314 | |||||||||||||||||

30+ days past due |

|

|

|

|

| 1 |

| 1 | |||||||||||||||||

Non-performing |

|

|

|

|

|

|

|

| |||||||||||||||||

Total wholesale receivables | $ | 271 | $ | 118 | $ | 64 | $ | 14 | $ | 4 | $ | 3 | $ | 2,543 | $ | 3,017 | |||||||||

16

An analysis of the allowance for credit losses and investment in financing receivables in millions of dollars during the periods follows:

Retail Notes | Revolving | ||||||||||||

& Financing | Charge | Wholesale | |||||||||||

Leases | Accounts | Receivables | Total | ||||||||||

Three Months Ended July 31, 2022 | |||||||||||||

Allowance: |

|

|

|

|

|

|

|

|

|

|

| ||

Beginning of period balance |

| $ | 168 |

| $ | 17 | $ | 5 | $ | 190 | |||

Provision (credit) | 14 | 3 | (1) | 16 | |||||||||

Write-offs | (12) | (10) |

| (22) | |||||||||

Recoveries | 8 | 7 |

| 15 | |||||||||

Translation adjustments | 3 |

|

| 3 | |||||||||

End of period balance |

| $ | 181 |

| $ | 17 | $ | 4 | $ | 202 | |||

Nine Months Ended July 31, 2022 | |||||||||||||

Allowance: |

| ||||||||||||

Beginning of period balance |

| $ | 138 |

| $ | 21 | $ | 7 | $ | 166 | |||

Provision (credit) | 66 | (4) | (3) | 59 | |||||||||

Write-offs | (47) | (22) |

| (69) | |||||||||

Recoveries | 17 | 22 |

| 39 | |||||||||

Translation adjustments | 7 |

|

| 7 | |||||||||

End of period balance |

| $ | 181 |

| $ | 17 | $ | 4 | $ | 202 | |||

Financing receivables: | |||||||||||||

End of period balance |

| $ | 33,515 |

| $ | 4,099 | $ | 2,785 | $ | 40,399 | |||

Retail Notes | Revolving |

| |||||||||||

& Financing | Charge | Wholesale |

| ||||||||||

Leases | Accounts | Receivables | Total | ||||||||||

Three Months Ended August 1, 2021 | |||||||||||||

Allowance: |

|

|

|

|

|

|

|

| |||||

Beginning of period balance | $ | 152 |

| $ | 19 | $ | 7 | $ | 178 | ||||

Provision |

| 3 |

|

|

| 3 | |||||||

Write-offs |

| (14) | (9) |

|

| (23) | |||||||

Recoveries |

| 8 | 8 |

|

| 16 | |||||||

End of period balance | $ | 149 | $ | 18 | $ | 7 | $ | 174 | |||||

Nine Months Ended August 1, 2021 | |||||||||||||

Allowance: |

|

|

|

|

|

|

|

|

|

| |||

Beginning of period balance | $ | 133 |

| $ | 43 | $ | 8 | $ | 184 | ||||

ASU No. 2016-13 adoption | 44 | (13) |

| 31 | |||||||||

Provision (credit) |

| (9) | (16) | (1) |

| (26) | |||||||

Write-offs |

| (38) | (23) |

| (61) | ||||||||

Recoveries |

| 17 | 27 |

|

| 44 | |||||||

Translation adjustments | 2 |

|

|

| 2 | ||||||||

End of period balance | $ | 149 | $ | 18 | $ | 7 | $ | 174 | |||||

Financing receivables: | |||||||||||||

End of period balance | $ | 30,235 |

| $ | 3,772 | $ | 3,017 | $ | 37,024 | ||||

The allowance for credit losses increased in the third quarter and the first nine months of 2022 mainly due to higher reserves related to the events in Russia / Ukraine and higher portfolio balances. As part of the allowance setting process, the Company continues to monitor the economy, including potential impacts of inflation, commodity prices, and interest rates on portfolio performance and adjustments to the allowance are incorporated, as necessary.

A troubled debt restructuring is the modification of debt in which a creditor grants a concession it would not otherwise consider to a debtor that is experiencing financial difficulties. These modifications may include a reduction of the stated interest rate, an extension of the maturity date, a reduction of the face amount or maturity amount of the debt, or a reduction of accrued interest. During the first nine months of 2022, the Company identified 230 receivable contracts, primarily retail notes, as troubled debt restructurings with aggregate balances of $10 million pre-modification and $9 million post-modification. During the first nine months of 2021, the Company identified 304 receivable contracts, primarily retail notes, as troubled debt

17

restructurings with aggregate balances of $12 million pre-modification and $10 million post-modification. During these same periods, there were no significant troubled debt restructurings that subsequently defaulted and were written off. At July 31, 2022, the Company had no commitments to lend to borrowers whose accounts were modified in troubled debt restructurings.

(9) Securitization of Financing Receivables

As a part of its overall funding strategy, the Company periodically transfers certain financing receivables (retail notes) into VIEs that are special purpose entities (SPEs), or non-VIE banking operations, as part of its asset-backed securities programs (securitizations). The structure of these transactions is such that the transfer of the retail notes does not meet the accounting criteria for sales of receivables, and is, therefore, accounted for as a secured borrowing. SPEs utilized in securitizations of retail notes differ from other entities included in the Company’s consolidated statements because the assets they hold are legally isolated. Use of the assets held by the SPEs or the non-VIEs is restricted by terms of the documents governing the securitization transactions.

The components of consolidated restricted assets, secured borrowings, and other liabilities related to secured borrowings in securitization transactions were as follows in millions of dollars:

| July 31 |

| October 31 |

| August 1 |

| ||||

2022 | 2021 | 2021 |

| |||||||

Financing receivables securitized (retail notes) |

| $ | 5,156 | $ | 4,673 | $ | 5,421 | |||

Allowance for credit losses | (15) |

| (14) |

| (20) | |||||

Other assets (primarily restricted cash) | 136 |

| 107 |

| 113 | |||||

Total restricted securitized assets |

| $ | 5,277 | $ | 4,766 | $ | 5,514 | |||

Short-term securitization borrowings | $ | 4,920 | $ | 4,605 | $ | 5,277 | ||||

Accrued interest on borrowings | 4 | 2 |

| 2 | ||||||

Total liabilities related to restricted securitized assets | $ | 4,924 | $ | 4,607 | $ | 5,279 | ||||

(10) Inventories

Most inventories owned by Deere & Company and its U.S. equipment subsidiaries are valued at cost on the last-in, first-out (LIFO) basis. If all of the Company’s inventories had been valued on a first-in, first-out (FIFO) basis, estimated inventories by major classification in millions of dollars would have been as follows:

| July 31 |

| October 31 |

| August 1 |

| ||||

2022 | 2021 | 2021 |

| |||||||

Raw materials and supplies |

| $ | 4,508 | $ | 3,524 | $ | 2,895 | |||

Work-in-process | 1,621 |

| 994 |

| 1,124 | |||||

Finished goods and parts | 5,434 |

| 4,373 |

| 4,176 | |||||

Total FIFO value | 11,563 |

| 8,891 |

| 8,195 | |||||

Less adjustment to LIFO value | 2,442 |

| 2,110 |

| 1,785 | |||||

Inventories |

| $ | 9,121 | $ | 6,781 | $ | 6,410 | |||

(11) Goodwill and Other Intangible Assets–Net

The changes in amounts of goodwill by operating segments were as follows in millions of dollars:

| Production & |

| Small Ag |

| Construction |

|

| ||||||

Precision Ag | & Turf | & Forestry | Total |

| |||||||||

Goodwill at November 1, 2020 | $ | 333 | $ | 268 | $ | 2,480 | $ | 3,081 | |||||

Acquisition |

| 12 |

|

| 12 | ||||||||

Translation adjustments |

| 13 | (3) | 45 | 55 | ||||||||

Goodwill at August 1, 2021 | $ | 358 | $ | 265 | $ | 2,525 | $ | 3,148 | |||||

Goodwill at October 31, 2021 | $ | 542 | $ | 265 | $ | 2,484 | $ | 3,291 | |||||

Acquisitions | 132 | 69 | 597 | 798 | |||||||||

Translation adjustments | (23) | (11) | (301) | (335) | |||||||||

Goodwill at July 31, 2022 | $ | 651 | $ | 323 | $ | 2,780 | $ | 3,754 | |||||

There were no accumulated goodwill impairment losses in the reported periods.

18

The components of other intangible assets were as follows in millions of dollars:

| July 31 |

| October 31 |

| August 1 |

| ||||

2022 | 2021 | 2021 |

| |||||||

Amortized intangible assets: | ||||||||||

Customer lists and relationships | $ | 507 | $ | 542 | $ | 545 | ||||

Technology, patents, trademarks, and other | 1,320 |

| 1,104 |

| 1,080 | |||||

Total at cost | 1,827 |

| 1,646 |

| 1,625 | |||||

Less accumulated amortization: |

|

| ||||||||

Customer lists and relationships | 162 | 151 | 144 | |||||||

Technology, patents, trademarks, and other | 384 | 343 | 337 | |||||||

Total accumulated amortization | 546 | 494 | 481 | |||||||

Amortized intangible assets, net | 1,281 | 1,152 | 1,144 | |||||||

Unamortized intangible assets: | ||||||||||

In-process research and development |

| 123 | 123 | |||||||

Other intangible assets – net | $ | 1,281 | $ | 1,275 | $ | 1,267 | ||||

In September 2017, the Company acquired Blue River Technology’s in-process research and development related to machine learning technology to optimize the use of farm inputs. Those research and development activities were completed, and the Company started amortizing the acquired technology in the second quarter of 2022.

The amortization of other intangible assets in the third quarter and the first nine months of 2022 was $42 million and $104 million, and for 2021 was $27 million and $89 million, respectively. The estimated amortization expense for the next five years is as follows in millions of dollars: remainder of 2022 – $62, 2023 – $164, 2024 – $160, 2025 – $133, 2026 – $113, and 2027 – $112.

(12) Short-Term Borrowings

Short-term borrowings were as follows in millions of dollars:

July 31 | October 31 | August 1 | ||||||||

| 2022 |

| 2021 |

| 2021 | |||||

Commercial paper | $ | 6,035 | $ | 2,230 | $ | 1,882 | ||||

Notes payable to banks | 427 | 336 | 133 | |||||||

Finance lease obligations due within one year | 21 | 23 | 23 | |||||||

Long-term borrowings due within one year |

| 7,693 |

| 8,330 |

| 8,366 | ||||

Short-term borrowings | $ | 14,176 | $ | 10,919 | $ | 10,404 | ||||

19

(13) Long-Term Borrowings

Long-term borrowings were as follows in millions of dollars:

July 31 | October 31 | August 1 | ||||||||

| 2022 |

| 2021 |

| 2021 | |||||

Underwritten term debt |

|

|

| |||||||

U.S. dollar notes and debentures: | ||||||||||

2.75% notes due 2025 | $ | 700 | $ | 700 | $ | 700 | ||||

6.55% debentures due 2028 |

| 200 |

| 200 |

| 200 | ||||

5.375% notes due 2029 |

| 500 |

| 500 |

| 500 | ||||

3.10% notes due 2030 | 700 | 700 | 700 | |||||||

8.10% debentures due 2030 |

| 250 |

| 250 |

| 250 | ||||

7.125% notes due 2031 |

| 300 |

| 300 |

| 300 | ||||

3.90% notes due 2042 |

| 1,250 |

| 1,250 |

| 1,250 | ||||

2.875% notes due 2049 | 500 | 500 | 500 | |||||||

3.75% notes due 2050 | 850 | 850 | 850 | |||||||

Euro notes: | ||||||||||

.5% notes due 2023 (€500 principal) | 510 | 584 | 594 | |||||||

1.375% notes due 2024 (€800 principal) | 816 | 934 | 951 | |||||||

1.85% notes due 2028 (€600 principal) | 612 | 701 | 713 | |||||||

2.20% notes due 2032 (€600 principal) | 612 | 701 | 713 | |||||||

1.65% notes due 2039 (€650 principal) | 663 | 759 | 773 | |||||||

Serial issuances | ||||||||||

Medium-term notes (principal as of: July 31, 2022 - $22,983, October 31, 2021 - $22,647, August 1, 2021 - $21,892) |

| 22,593 | 22,899 | 22,346 | ||||||

Other notes and finance lease obligations |

| 1,191 |

| 1,178 |

| 1,059 | ||||

Less debt issuance costs and debt discounts | (115) | (118) | (119) | |||||||

Long-term borrowings |

| $ | 32,132 | $ | 32,888 | $ | 32,280 | |||

Medium-term notes serially due 2023 through 2032 are primarily offered by prospectus and issued at fixed and variable rates. These notes are presented in the table above with fair value adjustments related to interest rate swaps. All outstanding notes and debentures are senior unsecured borrowings and generally rank equally with each other.

In April 2022, the Company issued $600 million of sustainability-linked medium-term notes with an initial interest rate of 3.35 percent, which are due in 2029. This transaction supports the Company’s commitment to environmental sustainability. Failure to meet the stated sustainability performance target will result in a 25-basis point increase to the interest rate payable on the 2029 notes from and including April 2026.

(14) Leases - Lessor

The Company leases equipment manufactured or sold by the Company and a limited amount of non-John Deere equipment to retail customers through sales-type, direct financing, and operating leases. Sales-type and direct financing leases are reported in Financing receivables - net on the consolidated balance sheets, while operating leases are reported in Equipment on operating leases - net.

Lease revenues earned by the Company were as follows in millions of dollars:

Three Months Ended | Nine Months Ended | ||||||||||||

| July 31, 2022 |

| August 1, 2021 |

| July 31, 2022 |

| August 1, 2021 | ||||||

Sales-type and direct finance lease revenues | $ | 39 | $ | 37 | $ | 113 | $ | 107 | |||||

Operating lease revenues | 326 | 359 | 991 | 1,079 | |||||||||

Variable lease revenues | 6 | 8 | 20 | 23 | |||||||||

Total lease revenues | $ | 371 | $ | 404 | $ | 1,124 | $ | 1,209 | |||||

Variable lease revenues reported above primarily relate to separately invoiced property taxes on leased equipment in certain markets, late fees, and excess use and damage fees. Excess use and damage fees are reported in other income on the statements of consolidated income. Excess use and damage fees were $1 million and $2 million for the third quarter and first nine months ended July 31, 2022, respectively, compared with $2 million and $5 million for the same periods last year, respectively.

20

(15) Commitments and Contingencies

The Company generally determines its total warranty liability by applying historical claims rate experience to the estimated amount of equipment that has been sold and is still under warranty based on dealer inventories and retail sales. The historical claims rate is primarily determined by a review of five-year claims costs and current quality developments.

The premiums for extended warranties are primarily recognized in income in proportion to the costs expected to be incurred over the contract period. These unamortized extended warranty premiums (deferred revenue) included in the following table totaled $839 million and $709 million at July 31, 2022 and August 1, 2021, respectively.

A reconciliation of the changes in the warranty liability and unearned premiums was as follows in millions of dollars:

Three Months Ended | Nine Months Ended |

| |||||||||||

July 31 | August 1 | July 31 | August 1 |

| |||||||||

2022 | 2021 | 2022 | 2021 |

| |||||||||

Beginning of period balance |

| $ | 2,095 |

| $ | 1,876 |

| $ | 2,086 |

| $ | 1,743 | |

Payments | (240) |

| (209) | (657) |

| (626) | |||||||

Amortization of premiums received | (70) |

| (66) | (200) |

| (193) | |||||||

Accruals for warranties | 358 |

| 299 | 762 |

| 794 | |||||||

Premiums received | 103 |

| 96 | 277 |

| 258 | |||||||

Foreign exchange | (10) |

| (2) | (32) |

| 18 | |||||||

End of period balance | $ | 2,236 | $ | 1,994 | $ | 2,236 | $ | 1,994 | |||||

At July 31, 2022, the Company had approximately $330 million of guarantees issued primarily to banks outside the U.S. and Canada related to third-party receivables for the retail financing of John Deere equipment. The Company may recover a portion of any required payments incurred under these agreements from repossession of the equipment collateralizing the receivables. At July 31, 2022, the Company had accrued losses of $4 million under these agreements. The maximum remaining term of the receivables guaranteed at July 31, 2022 was approximately six years.

At July 31, 2022, the Company had commitments of $468 million for the construction and acquisition of property and equipment. Also, at July 31, 2022, the Company had restricted assets of $77 million, classified as Other assets. See Note 9 for additional restricted assets associated with borrowings related to securitizations.

The Company also had other miscellaneous contingent liabilities totaling approximately $90 million at July 31, 2022. The accrued liability for these contingencies was not material at July 31, 2022.

The Company is subject to various unresolved legal actions which arise in the normal course of its business, the most prevalent of which relate to product liability (including asbestos-related liability), retail credit, employment, patent, trademark, and antitrust matters. The Company believes the reasonably possible range of losses for these unresolved legal actions would not have a material effect on its consolidated financial statements.

(16) Fair Value Measurements

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. To determine fair value, the Company uses various methods including market and income approaches. The Company utilizes valuation models and techniques that maximize the use of observable inputs. The models are industry-standard models that consider various assumptions including time values and yield curves as well as other economic measures. These valuation techniques are consistently applied.

Level 1 measurements consist of quoted prices in active markets for identical assets or liabilities. Level 2 measurements include significant other observable inputs such as quoted prices for similar assets or liabilities in active markets; identical assets or liabilities in inactive markets; observable inputs such as interest rates and yield curves; and other market-corroborated inputs. Level 3 measurements include significant unobservable inputs.

21

The fair values of financial instruments that do not approximate the carrying values were as follows in millions of dollars. Long-term borrowings exclude finance lease liabilities.

July 31, 2022 | October 31, 2021 | August 1, 2021 |

| ||||||||||||||||

Carrying | Fair | Carrying | Fair | Carrying | Fair |

| |||||||||||||

Financing receivables – net | $ | 35,056 | $ | 34,158 | $ | 33,799 | $ | 33,718 | $ | 31,449 | $ | 31,515 | |||||||

Financing receivables securitized – net | 5,141 | 4,990 | 4,659 | 4,704 | 5,401 | 5,467 | |||||||||||||

Short-term securitization borrowings | 4,920 | 4,862 | 4,605 | 4,610 | 5,277 | 5,302 | |||||||||||||

Long-term borrowings due within one year | 7,693 | 7,608 | 8,330 | 8,364 | 8,366 | 8,440 | |||||||||||||

Long-term borrowings | 32,101 | 31,741 | 32,850 | 34,506 | 32,238 | 34,345 | |||||||||||||

Fair value measurements above were Level 3 for all financing receivables and Level 2 for all borrowings.

Fair values of the financing receivables that were issued long-term were based on the discounted values of their related cash flows at interest rates currently being offered by the Company for similar financing receivables. The fair values of the remaining financing receivables approximated the carrying amounts.

Fair values of long-term borrowings and short-term securitization borrowings were based on current market quotes for identical or similar borrowings and credit risk, or on the discounted values of their related cash flows at current market interest rates. Certain long-term borrowings have been swapped to current variable interest rates. The carrying values of these long-term borrowings included adjustments related to fair value hedges.

Assets and liabilities measured at fair value on a recurring basis in millions of dollars follow, excluding the Company’s cash equivalents, which were carried at cost that approximates fair value and consisted primarily of money market funds and time deposits.

| July 31 |

| October 31 |

| August 1 |

| ||||

2022 | 2021 | 2021 |

| |||||||

Level 1: | ||||||||||

Marketable securities | ||||||||||

International equity securities | $ | 2 | $ | 2 | $ | 3 | ||||

U.S. equity fund | 75 | 75 | 74 | |||||||

U.S. government debt securities | 63 |

| 59 |

| 60 | |||||

Total Level 1 marketable securities | 140 | 136 | 137 | |||||||

Level 2: | ||||||||||

Marketable securities | ||||||||||

U.S. government debt securities | 134 | 139 | 124 | |||||||

Municipal debt securities | 70 |

| 73 |

| 71 | |||||

Corporate debt securities | 213 |

| 224 |

| 217 | |||||

International debt securities | 1 | 2 | 3 | |||||||

Mortgage-backed securities | 161 |

| 154 |

| 136 | |||||

Total Level 2 marketable securities | 579 |

| 592 |

| 551 | |||||

Other assets | ||||||||||

Derivatives | 280 | 275 | 432 | |||||||

Accounts payable and accrued expenses | ||||||||||

Derivatives | 667 | 228 | 152 | |||||||

Level 3: | ||||||||||

Accounts payable and accrued expenses – Deferred consideration | 252 | |||||||||

22