|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| | 2,254 | | | 2,237 | | | 3,021 | | | 3,121 | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | |

|

| 2020 | | 2021 | | 2022 | | 2023 |

| | | | | | | | | | | | |

| | 116 | | | 114 | | | 113 | | | 134 | |

| | | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

|

| 33,723 |

The following table sets forth the location of our facilities and the number of operational beds and units located at our skilled nursing, senior living and campus facilities as of December 31, 2023:

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Facility Counts | | Bed / Unit Counts |

| Skilled Nursing Operations | Senior Living Communities | Campus Operations | Total | | Skilled Nursing Beds | Senior Living Units | Total Beds / Units |

| California | 67 | — | 3 | 70 | | 6,764 | 197 | 6,961 |

| Texas | 77 | 1 | 5 | 83 | | 9,954 | 603 | 10,557 |

| Arizona | 30 | 1 | 5 | 36 | | 4,535 | 731 | 5,266 |

| Wisconsin | 2 | — | — | 2 | | 100 | — | 100 |

| Utah | 18 | 2 | 1 | 21 | | 1,968 | 163 | 2,131 |

| Colorado | 19 | 5 | 1 | 25 | | 1,986 | 723 | 2,709 |

| Washington | 15 | 1 | — | 16 | | 1,413 | 98 | 1,511 |

| Idaho | 11 | — | 1 | 12 | | 1,002 | 21 | 1,023 |

| Nebraska | 4 | 1 | 2 | 7 | | 413 | 341 | 754 |

| Kansas | 1 | — | 7 | 8 | | 615 | 213 | 828 |

| Iowa | 4 | — | 2 | 6 | | 368 | 31 | 399 |

| South Carolina | 9 | — | — | 9 | | 1,126 | — | 1,126 |

| Nevada | 2 | — | — | 2 | | 358 | — | 358 |

| 259 | 11 | 27 | 297 | | 30,602 | 3,121 | 33,723 |

Real Estate Properties — As of December 31, 2023, we owned 113 real estate properties in Arizona, California, Colorado, Idaho, Kansas, Nebraska, Nevada, South Carolina, Texas, Utah, Washington and Wisconsin, which include 83 of the 297 facilities that we operate and manage. Of our 113 real estate properties, 30 operations are leased to and operated by third-party operators. One senior living facility is located on the same real estate property as a skilled nursing facility that we own and operate. We further own the real estate property of our Service Center's California location and continue to lease a portion of the office space to third-party tenants. Our Standard Bearer segment reflects the results of operations for 108 of the 113 owned real estate properties.

The following table provides summary information regarding the location of our owned real estate properties as of December 31, 2023:

| | | | | | | | | | | | | | | | | | | | | | | | |

|

| Owned and Operated by Ensign(1) | | Owned and Leased to Third-Party Operators(1) | | Service Center | | Total Properties(1) | |

| California | 11 | | 2 | | 1 | | 14 | |

Texas(1) | 22 | | 6 | | — | | 27 | |

| Arizona | 13 | | 1 | | — | | 14 | |

| Wisconsin | 2 | | 19 | | — | | 21 | |

| Utah | 7 | | — | | — | | 7 | |

| Colorado | 8 | | — | | — | | 8 | |

| Washington | 4 | | 1 | | — | | 5 | |

| Idaho | 5 | | — | | — | | 5 | |

| Nebraska | 2 | | — | | — | | 2 | |

| Kansas | 4 | | — | | — | | 4 | |

| | | | | | |

| South Carolina | 5 | | — | | — | | 5 | |

| Nevada | — | | 1 | | — | | 1 | |

| 83 | | 30 | | 1 | | 113 | |

(1) One senior living operation in Texas, which is owned by Ensign and leased to a third-party operator, is located on the same real estate property as a skilled nursing facility that we own and operate. In this situation, the senior living operation is included in the total under "Owned and Leased to Third Party Operators" and the skilled nursing operation is included in the total under "Owned and Operated by Ensign", however, the amount reflected under "Total Properties" only recognizes the operation as a single property.

Item 3. LEGAL PROCEEDINGS

Indemnities — From time to time, we enter into certain types of contracts that contingently require us to indemnify parties against third-party claims. These contracts primarily include (i) certain real estate leases, under which we may be required to indemnify property owners or prior facility operators for post-transfer environmental or other liabilities and other claims arising from our use of the applicable premises, (ii) operations transfer agreements, in which we agree to indemnify past operators of facilities we acquire against certain liabilities arising from the transfer of the operation and/or the operation thereof after the transfer to our independent subsidiary, (iii) certain lending agreements, under which we may be required to indemnify the lender against various claims and liabilities, and (iv) certain agreements with our officers, directors and others, under which we may be required to indemnify such persons for liabilities based on the nature of their relationship to us. The terms of such obligations vary by contract and, in most instances, do not expressly state or include a specific or maximum dollar amount. Generally, amounts under these contracts cannot be reasonably estimated until a specific claim is asserted. Consequently, because no claims have been asserted, no liabilities have been recorded for these obligations on our balance sheets for any of the periods presented.

In connection with the spin-off transaction in 2019, certain landlords required, in exchange for their consent to the transaction, that our lease guarantees remain in place for a certain period of time following the spin-off. These guarantees could result in significant additional liabilities and obligations for us if Pennant were to default on their obligations under their leases with respect to these properties.

Litigation and Regulatory Matters — Laws and regulations governing Medicare and Medicaid programs are complex and subject to review and interpretation. Compliance with such laws and regulations is evaluated regularly, the results of which can be subject to future governmental review and interpretation, and can include significant regulatory action with fines, penalties, and exclusion from certain governmental programs. Included in these laws and regulations is monitoring performed by the Office of Civil Rights which covers the Health Insurance Portability and Accountability Act of 1996, the terms of which require healthcare providers (among other things) to safeguard the privacy and security of certain patient protected health information.

Both government and private pay sources have instituted cost-containment measures designed to limit payments made to providers of healthcare services, and there can be no assurance that future measures designed to limit payments made to providers will not adversely affect us.

We and our independent subsidiaries are party to various legal actions and administrative proceedings and are subject to various claims arising in the ordinary course of business, including claims that services provided to patients by our independent subsidiaries have resulted in injury or death, and claims related to employment and commercial matters. For example, in a four-week medical negligence trial in the State of Arizona, the jury returned a verdict against one of our independent subsidiaries in late November 2023. We intend to appeal the verdict. We have in the past appealed and have in some circumstances received returned decisions in our favor. Although we intend to vigorously defend against these claims and in general these types of claims and cases, there can be no assurance that the outcomes of these matters will not have a material adverse effect on operational results and financial condition. Additionally, in certain states in which we have or have had independent subsidiaries, insurance coverage for the risk of punitive damages arising from general and professional liability litigation may not be available due to state law and/or public policy prohibitions. There can be no assurance that we and or our independent subsidiaries will not be liable for punitive damages awarded in litigation arising in states for which punitive damage insurance coverage is not available.

The skilled nursing and post-acute care industry is heavily regulated. As such, we and our independent subsidiaries are continuously subject to state and federal regulatory scrutiny, supervision and control in the ordinary course of business. Such regulatory scrutiny often includes inquiries, investigations, examinations, audits, site visits and surveys, some of which are non-routine. In addition to being subject to direct regulatory oversight from state and federal agencies, the skilled nursing and post-acute care industry is also subject to regulatory requirements which, if noncompliance is identified, could result in civil, administrative or criminal fines, penalties or restitutionary relief, and reimbursement; authorities could also seek the suspension or exclusion of the provider or individual from participation in their programs. We believe that there has been, and will continue to be, an increase in governmental investigations of post-acute providers, particularly in the area of Medicare/Medicaid false claims, as well as an increase in enforcement actions resulting from these investigations. Adverse determinations in civil legal proceedings or governmental investigations, whether currently asserted or arising in the future, could have a material adverse effect on our financial position, results of operations, and cash flows. Additionally, such proceedings and/or investigation can be a distraction to the business.

For example, in 2020, the U.S. House of Representatives Select Subcommittee on the Coronavirus Crisis launched a nation-wide investigation into the COVID-19 pandemic, which included the impact of the coronavirus on residents and employees in nursing homes. In June 2020, we and our independent subsidiaries received a document and information request from the House Select Subcommittee. We and our independent subsidiaries cooperated in responding to this inquiry. In July 2022 and thereafter, we and our independent subsidiaries received follow up requests for additional documents and information. We and our independent subsidiaries responded to these requests and cooperated with the House Select Subcommittee in connection with its investigation. On December 9, 2022, the House Select Subcommittee issued its final report summarizing its investigation and related recommendations designed "to strengthen the nation's ability to prevent and respond to public health and economic emergencies." According to the information provided by the House Select Subcommittee, the issuance of this report was the House Select Subcommittee's final official act in connection with their assigned responsibilities. Also, we, on behalf of our independent subsidiaries, received a Civil Investigative Demand (CID) from the U.S. Department of Justice (DOJ) in January of 2024 indicating that the DOJ is investigating the Company to determine whether we have caused the submission of claims to Medicare and Texas Medicaid for services which were unnecessary or otherwise not consistent with existing reimbursement requirements. The CID covers the period from January 1, 2016 to the present. As a general matter, our independent subsidiaries maintain policies and procedures to promote compliance with all applicable Medicare and Medicaid requirements, including, but not limited to those relating to the presentation of claims for reimbursement for services provided. We intend to fully cooperate with the DOJ in response to the CID. However, we cannot predict the outcome of the investigation or its potential impact to the consolidated financial statements.

In addition to the potential lawsuits and claims described above, we and our independent subsidiaries are also subject to potential lawsuits under the FCA and comparable state laws alleging submission of fraudulent claims for services to any healthcare program (such as Medicare or Medicaid) or other payor. A violation may provide the basis for exclusion from federally funded healthcare programs. Such exclusions could have a correlative negative impact on our financial performance. In addition, and pursuant to the qui tam or "whistleblower" provisions of the FCA, a private individual with knowledge of fraud or potential fraud may bring a claim on behalf of the federal government and receive a percentage of the federal government's recovery. Due to these whistleblower incentives, qui tam lawsuits have become more frequent.

For example, on May 31, 2018, we, on behalf of our independent subsidiaries, received a CID from the DOJ stating that it was investigating to determine whether there had been a violation of the False Claims Act (FCA) and/or the Anti-Kickback Statute (AKS) with respect to the relationships between certain of our independent subsidiaries and persons who serve or have served as medical directors. We fully cooperated with the DOJ and promptly responded to its requests for information. In April 2020, we were advised that the DOJ declined to intervene in any subsequent action filed in connection with the subject matter of this investigation. Despite the decision of the DOJ to decline to participate in litigation based on the subject matter of its previously issued CID, the involved qui tam relator moved forward with the complaint in December 2020. From that time until December 2023, and notwithstanding our success in early pre-trial motions, we continued to incur legal defense costs and fees, including significant amounts as part of discovery in the fourth quarter of 2023. In early January 2024, we entered into mediation and on January 19, 2024, the parties agreed to settle the civil case for $48.0 million, subject to the review of the DOJ and other relevant government entities. The settlement does not include admissions on the part of the Company or our independent subsidiaries, and we maintain that we have and continue to comply with all applicable State and Federal statutes (including but not limited to the FCA and the AKS).

In addition to the FCA, some states, including California, Arizona and Texas, have enacted similar whistleblower and false claims laws and regulations. Further, the Deficit Reduction Act of 2005 created incentives for states to enact anti-fraud legislation modeled on the FCA. As such, we and our independent subsidiaries could face increased scrutiny, potential liability and legal expenses and costs based on claims under state false claims acts in markets where our independent subsidiaries do business.

In May 2009, Congress passed the FERA which made significant changes to the FCA and expanded the types of activities subject to prosecution and whistleblower liability. Following changes by FERA, health care providers face significant penalties for the knowing retention of government overpayments, even if no false claim was involved. Health care providers can now be liable for knowingly and improperly avoiding or decreasing an obligation to pay money or property to the government. This includes the retention of any government overpayment. The government can argue, therefore, that an FCA violation can occur without any affirmative fraudulent action or statement, as long as the action or statement is knowingly improper. In addition, FERA extended protections against retaliation for whistleblowers, including protections not only for employees, but also contractors and agents. Thus, an employment relationship is generally not required in order to qualify for protection against retaliation for whistleblowing.

Healthcare litigation (including class action litigation) is common and is filed based upon a wide variety of claims and theories, and our independent subsidiaries are routinely subjected to varying types of claims, including class action "staffing" suits where the allegation is understaffing at the facility level. These class-action “staffing” suits have the potential to result in large jury verdicts and settlements. We expect the plaintiffs' bar to continue to be aggressive in their pursuit of these staffing and similar claims.

We and our independent subsidiaries have been, and continue to be, subject to claims, findings and legal actions that arise in the ordinary course of the various businesses, including in connection with the delivery of healthcare and non-healthcare services. These claims include but are not limited to potential claims related to patient care and treatment (professional negligence claims) as well as employment related claims. In addition, we and our independent subsidiaries, and others in the industry, are subject to claims and lawsuits in connection with COVID-19 and facility preparation for and/or response to the COVID-19 pandemic. While we have been able to settle or otherwise resolve many of these types of claims without an ongoing material adverse effect on our business, a significant increase in the number of these claims, or an increase in the amounts owing should plaintiffs be successful in their prosecution of remaining or future claims, could materially adversely affect our business, financial condition, results of operations and cash flows. In addition, these claims could impact our ability to procure insurance to cover our exposure related to the various services provided by our independent subsidiaries to their residents, customers and patients.

Claims and suits, including class actions, continue to be filed against our independent subsidiaries and other companies in the post-acute care industry. We and our independent subsidiaries have been subjected to, and/or are currently involved in, class action litigation alleging violations (alone or in combination) of state and federal wage and hour law as related to the alleged failure to pay wages, to timely provide and authorize meal and rest breaks, and other such similar causes of action. We do not believe that the ultimate resolution of these actions will have a material adverse effect on our business, cash flows, financial condition or results of operations.

Medicare Revenue Recoupments — We and our independent subsidiaries are subject to regulatory reviews relating to the provision of Medicare services, billings and potential overpayments resulting from reviews conducted via RAC, Program Safeguard Contractors, and Medicaid Integrity Contractors (collectively referred to as Reviews). For several months during the COVID-19 pandemic, CMS suspended its Targeted Probe and Educate (TPE) Program. Beginning in August 2020, CMS resumed TPE Program activity. If an operation fails a Review and/or subsequent Reviews, the operation could then be subject to extended review or an extrapolation of the identified error rate to billings in the same time period. We anticipate that these Reviews could increase in frequency in the future. As of December 31, 2023, and through the filing date of this report, 40 of our independent subsidiaries had Reviews scheduled or in process.

In June 2023, CMS announced a new nationwide audit, the “SNF 5-Claim Probe & Educate Review”, in which the Medicare Administrative Contractors will review five claims from each SNF to check for compliance. In implementing this SNF 5-Claim Probe & Educate Review, CMS acknowledged that the increase in observed improper payments from 2021 to 2022 may have arisen from a “misunderstanding” by SNFs about how to appropriately bill for claims of service after October 1, 2019. All facilities that are not undergoing TPE reviews, or have not recently passed a TPE review, will be subject to the nationwide audit. MACs will complete only one round of probe-and-educate for each SNF, rather than the three rounds that typically occur in the TPE Program. Additionally, CMS’s education for each SNF will be individualized and based on observed claim review errors, with rationales for denial explained to the SNF on a claim-by-claim basis. This program will apply only to claims submitted after October 1, 2019, and will exclude claims containing a COVID-19 diagnosis.

Item 4. MINE SAFETY DISCLOSURES

None.

PART II.

Item 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Market Information

Our common stock has been traded under the symbol “ENSG” on the NASDAQ Global Select Market since our initial public offering on November 8, 2007. Prior to that time, there was no public market for our common stock. As of January 29, 2024, there were approximately 315 holders of record of our common stock.

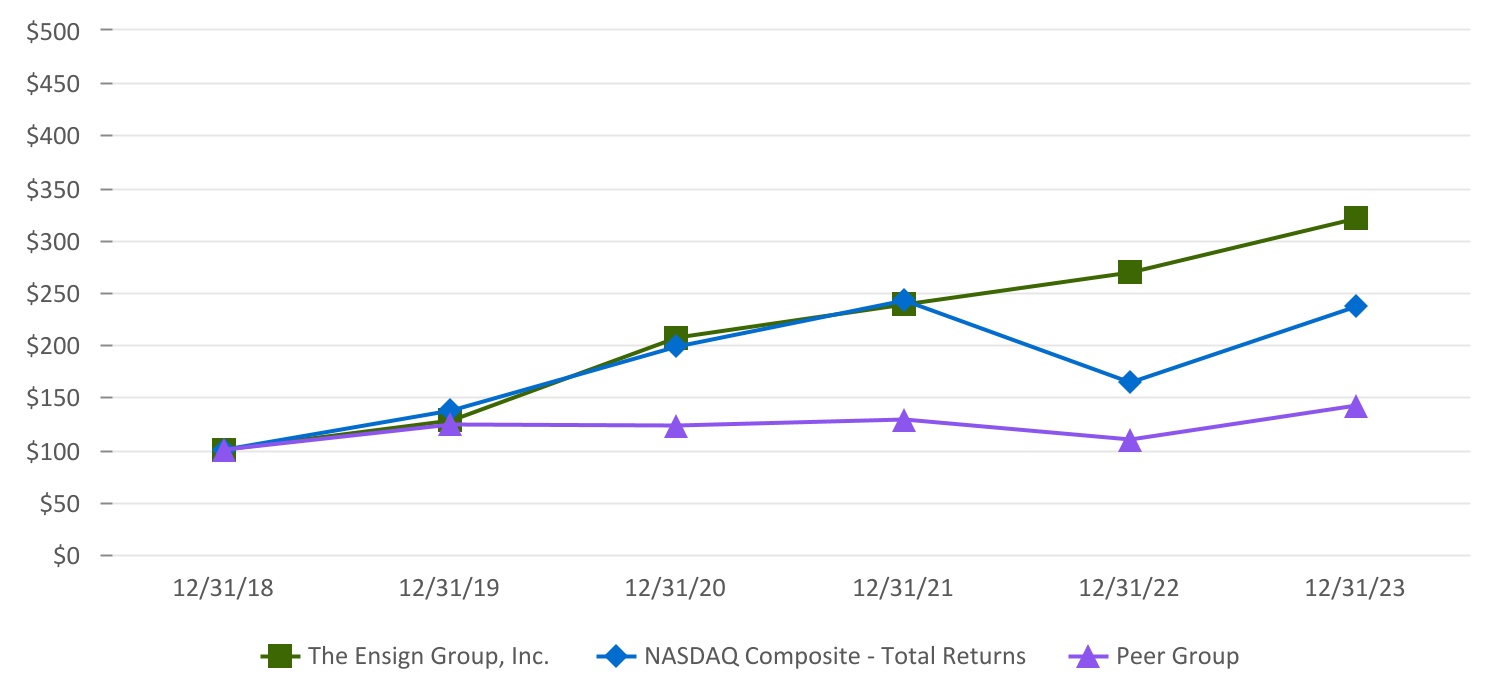

Notwithstanding anything to the contrary set forth in any of our filings under the Securities Act or the Exchange Act that might incorporate future filings, including the Annual Report on Form 10-K, in whole or in part, the Stock Performance Graph and supporting data which follows shall not be deemed to be incorporated by reference into any such filings except to the extent that we specifically incorporate any such information into any such future filings.

The graph below shows the cumulative total stockholder return of investment of $100 (and the reinvestment of any dividends thereafter) on December 31, 2018 in (i) our common stock, (ii) the Skilled Nursing Facilities Peer Group 1 and (iii) the NASDAQ Market Index. Our stock price performance shown in the graph below is not indicative of future stock price performance.

Since our inception in 1999, we completed the spin-off of two independent publicly traded companies. On June 1, 2014, Ensign completed the spin-off of CareTrust REIT, Inc. (CareTrust) into an independent publicly traded company. On October 1, 2019, Ensign completed the spin-off of The Pennant Group, Inc. (Pennant) with the pro rata distribution of 1.18 shares of Pennant’s common stock for every share of Ensign’s common stock to our stockholders, pursuant to which Pennant became an independent company. Pennant's stock traded at $6.15 at opening price on the first day of trading and closed at $15.09. Ensign's stock price was reduced by the same value on the same day. For the purpose of this graph, the effect of the final separation of Pennant is reflected in the cumulative total return of Ensign Common Stock as a reinvested dividend.

COMPARISON OF 60 MONTH CUMULATIVE TOTAL RETURN*

Among Ensign Group, the NASDAQ Composite Index and Our Peer Group

December 2023

*Assumes $100 invested on December 31, 2018 in stock in index, including reinvestment of dividends.

Fiscal year ended December 31.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | December 31, |

| | 2018 | | 2019 | | 2020 | | 2021 | | 2022 | | 2023 |

The Ensign Group, Inc.(2) | | $ | 100.00 | | | $ | 127.85 | | | $ | 206.31 | | | $ | 238.12 | | | $ | 268.99 | | | $ | 319.74 | |

| NASDAQ Market Index | | 100.00 | | | 136.69 | | | 198.10 | | | 242.03 | | | 163.28 | | | 236.17 | |

Peer Group(1) | | 100.00 | | | 123.99 | | | 122.37 | | | 128.11 | | | 108.87 | | | 141.47 | |

(1) The current composition of our Peer Group is as follows: Amedysis, Inc., CareTrust REIT Inc., Encompass Healthcare Corp., LTC Properties, Inc., National Healthcare Corporation, National Health Investors, Inc., Omega Healthcare Investors, Inc., Select Medical Holdings Corp. and Welltower Inc.

(2) The value displayed only incorporates the value of The Ensign Group, Inc. stock and does not incorporate the value shareholders received in connection with our spin-off of The Pennant Group, Inc.

Dividend Policy

We do not have a formal dividend policy, but we currently intend to continue to pay regular quarterly dividends to the holders of our common stock. We have been a dividend-paying company since 2002 and have increased our dividend every year for the last 21 years.

Issuer Repurchases of Equity Securities

Stock Repurchase Programs — On August 29, 2023, the Board of Directors approved a stock repurchase program pursuant to which we may repurchase up to $20.0 million of our common stock under the program for a period of approximately 12 months from September 1, 2023. Under this program, we are authorized to repurchase our issued and outstanding common shares from time to time in open-market and privately negotiated transactions and block trades in accordance with federal securities laws. We did not purchase any shares pursuant to this stock repurchase program during the year ended December 31, 2023.

Previously on July 28, 2022, the Board of Directors approved a stock repurchase program pursuant to which we could repurchase up to $20.0 million of our common stock under the program for a period of approximately 12 months from August 2, 2022. Under this program, we were authorized to repurchase our issued and outstanding common shares from time to time in open-market and privately negotiated transactions and block trades in accordance with federal securities laws. The share repurchase program does not obligate us to acquire any specific number of shares. The stock repurchase program expired on August 2, 2023 and is no longer in effect. We did not purchase any shares pursuant to this stock repurchase program.

Item 6. [RESERVED]

Item 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion should be read in conjunction with the consolidated financial statements and accompanying notes, which appear elsewhere in this Annual Report on Form 10-K. This discussion contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in these forward-looking statements as a result of various factors, including those discussed below and elsewhere in this Annual Report on Form 10-K. See Part I. Item 1A. Risk Factors and Cautionary Note Regarding Forward-Looking Statements.

For discussion of 2021 items and year-over-year comparisons between 2022 and 2021 that are not included in this 2023 Form 10-K, refer to “Item 7. – Management’s Discussion and Analysis of Financial Condition and Results of Operations” found in our Form 10-K for the year ended December 31, 2022, that was filed with the Securities and Exchange Commission on February 2, 2023.

Overview

We are a provider of health care services across the post-acute care continuum. We engage in the operation, ownership, acquisition, development and leasing of skilled nursing, senior living and other healthcare related properties and ancillary businesses located in Arizona, California, Colorado, Idaho, Iowa, Kansas, Nebraska, Nevada, South Carolina, Texas, Utah, Washington and Wisconsin. Our independent subsidiaries, each of which strive to be the operation of choice in the community they serve, provide a broad spectrum of services. As of December 31, 2023, we offered skilled nursing, senior living and rehabilitative care services through 297 skilled nursing and senior living facilities. Our real estate portfolio includes 113 owned real estate properties, which includes 83 facilities operated and managed by us, 30 operations leased to and operated by third-party operators and the Service Center location. Of the 30 real estate operations leased to third-party operators, one senior living facility is located on the same real estate property as a skilled nursing facility that we own and operate.

|

|

|

|

|

Segments We have two reportable segments: (1) skilled services, which includes the operation of skilled nursing facilities and rehabilitation therapy services and (2) Standard Bearer, which is comprised of select properties owned by us through our captive REIT and leased to skilled nursing and senior living operations, including our own independent subsidiaries and third-party operators.

We also reported an “all other” category that includes operating results from our senior living operations, mobile diagnostics, transportation, other real estate and other ancillary operations. These businesses are neither significant individually, nor in aggregate and therefore do not constitute a reportable segment. Our Chief Executive Officer, who is our chief operating decision maker, or CODM, reviews financial information at the operating segment level.

Revenue Sources

Skilled Services — Within our skilled nursing operations, we generate revenue from Medicaid, private pay, managed care and Medicare payors. We believe that our skilled mix, which we define as the number of days Medicare, managed care and other skilled patients are receiving services at our skilled nursing operations divided by the total number of days patients are receiving services at our skilled nursing operations, from all payor sources (less days from senior living services) for any given period, is an important indicator of our success in attracting high-acuity patients because it represents the percentage of our patients who are reimbursed by Medicare, managed care and other skilled payors, for whom we receive higher reimbursement rates.

We participate in supplemental payment programs and quality improvement programs in various states that provide supplemental Medicaid payments for skilled nursing facilities that are licensed to non-state government-owned entities such as city and county hospital districts. Numerous independent subsidiaries entered into transactions with various hospital districts providing for the transfer of the licenses for those skilled nursing facilities to the hospital districts. Each affected independent subsidiary agreement between the hospital district and our subsidiary is terminable by either party to fully restore the prior license status.

Standard Bearer — We generate rental revenue primarily by leasing post-acute care properties that we acquired to healthcare operators under triple-net lease arrangements, whereby the tenants are solely responsible for the costs related to the property, including property taxes, insurance and maintenance and repair costs, subject to certain exceptions. As of December 31, 2023, our real estate portfolio within Standard Bearer is comprised of 108 real estate properties. Of these properties, 79 are leased to our independent subsidiaries and 30 are leased to facilities wholly-owned and managed by third-party operators. During the year ended December 31, 2023, we generated rental revenues of $82.5 million, of which $66.7 million, was derived from our independent subsidiaries' operators and therefore eliminated in consolidation.

Other — Within our senior living operations, we generate revenue primarily from private pay sources, with a portion earned from Medicaid payors or through other state-specific programs. In addition, we hold majority membership interests in certain of our other ancillary operations. Payment for these services varies and is based upon the service provided. The payment is adjusted for an inability to obtain appropriate billing documentation or authorizations acceptable to the payor and other reasons unrelated to credit risk.

Primary Components of Expense

Cost of Services (exclusive of rent and depreciation and amortization shown separately) — Our cost of services represents the costs of operating our independent subsidiaries, which primarily consists of payroll and related benefits, supplies, purchased services, and ancillary expenses such as the cost of pharmacy and therapy services provided to patients. Cost of services also includes the cost of general and professional liability insurance, rent expenses related to leasing our operational facilities that are not included in facility rent - cost of services, and other general cost of services with respect to our operations.

Facility Rent - Cost of Services — Rent - cost of services consists solely of base minimum rent amounts payable under lease agreements to third-party real estate owners. Our independent subsidiaries lease and operate but do not own the underlying real estate and these amounts do not include taxes, insurance, impounds, capital reserves or other charges payable under the applicable lease agreements. Expenses related to leasing our operations are included in cost of services.

General and Administrative Expense — General and administrative expense consists primarily of payroll and related benefits and travel expenses for our Service Center personnel, including training and other operational support. General and administrative expense also includes professional fees (including accounting and legal fees), litigation expense related to specific proceedings that are outside the ordinary course of business, costs relating to our information systems and stock-based compensation related to our Service Center employees.

Depreciation and Amortization — Property and equipment are recorded at their original historical cost. Depreciation is computed using the straight-line method over the estimated useful lives of the depreciable assets. The following is a summary of the depreciable lives of our depreciable assets:

| | | | | |

| Buildings and improvements | Minimum of three years to a maximum of 59 years, generally 45 years |

| Leasehold improvements | Shorter of the lease term or estimated useful life, generally 5 to 15 years |

| Furniture and equipment | 3 to 10 years |

| |

Critical Accounting Estimates

Our discussion and analysis of our financial condition and results of operations are based on our consolidated financial statements, which have been prepared in accordance with U.S. Generally Accepted Accounting Principles (GAAP). The preparation of these financial statements and related disclosures requires us to make judgments, estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the reporting period. We believe that the application of the following accounting policies, which are important to our financial position and results of operations, require significant judgments and estimates on the part of management. For a summary of our significant accounting policies, including the accounting policies discussed below, see Note 2, Summary of Significant Accounting Policies of the Notes to Consolidated Financial Statements.

Variable consideration within revenue recognition — Revenue recognized from healthcare services are adjusted for estimates of variable consideration to arrive at the transaction price. We determine the transaction price based on contractually agreed-upon amounts or rates, adjusted for estimates of variable consideration. We use the expected value method in determining the variable component that should be used to arrive at the transaction price, using contractual agreements and historical reimbursement experience within each payor type. The amount of variable consideration which is included in the transaction price may be constrained and is included in the net revenue only to the extent that it is probable that a significant reversal in the amount of the cumulative revenue recognized will not occur in a future period. If actual amounts of consideration ultimately received differ from our estimates, we adjust these estimates, which would affect net service revenue in the period such variances become known.

Self-insurance for general and professional liability — The self-insured retention and deductible limits for general and professional liability for all states are self-insured through our wholly-owned captive insurance subsidiary (the Captive Insurance), the related assets and liabilities of which are included in the accompanying consolidated balance sheets. Our general and professional liability as of the year ended December 31, 2023 and 2022 was $117.7 million and $87.0 million, respectively.

Our policy is to accrue amounts equal to the actuarially estimated costs to settle open claims of insureds, as well as an estimate of the cost of insured claims that have been incurred but not reported. We develop information about the size of the ultimate claims based on historical experience, current industry information and actuarial analysis, and evaluate the estimates for claim loss exposure on a quarterly basis. We use actuarial valuations to estimate the liability based on historical experience and industry information.

RESULTS OF OPERATIONS

We believe we exist to dignify and transform post-acute care. We set out a strategy to achieve our goal of ensuring our patients are receiving the best possible care through our ability to acquire, integrate and improve our operations. Our results serve as a strong indicator that our strategy is working and our transformation is underway. Over the last five years, our total revenue increased by $2.0 billion, or 112.5%, representing a 16.3% compound annual growth rate (CAGR) while our diluted GAAP earning per share (EPS) from continued operations grew by $2.56 from 2018 to $3.65 in 2023, representing a 27.4% CAGR.

Our total revenue for the year ended December 31, 2023 increased $703.9 million, or 23.3%, compared to the year ended December 31, 2022. Throughout 2023, we have continued to make progress on targeted initiatives related to increasing occupancy in our facilities, attracting and developing our people and acquiring new skilled nursing operations and integrating them with our proven cultural and operational principals. We continue to experience healthy growth in both revenue and operational earnings.

Our combined Same Facilities and Transitioning Facilities occupancy increased by 3.2% compared to 2022. As our census continues to return to pre-pandemic levels, we anticipate a return to our historical seasonality trends, which typically result in higher occupancy and skilled mix during the first and fourth quarters and softening in the second and third quarters. See Recent Activities for our operational update.

During the year ended December 31, 2023, we added 26 new operations, which included 17 operations in California. These California facilities include a group of highly skilled team members who will further our mission of dignifying long term care. We continue to work diligently with existing and recently acquired operations so that each can reach its full clinical and financial potential.

Our strength remains in our operating model, which empowers each operator to form their own market-specific strategy and adjust to the needs of their local medical communities, including methods for attracting new healthcare professionals into our workforce and retaining and developing existing staff. Despite continued labor pressures, there are positive trends on both turnover and agency usage in some of our markets. During 2023, we added over 5,000 team members, or 18%, to our independent subsidiaries and the Service Center.

The following table sets forth details of operating results for our revenue, expenses and earnings, and their respective components, as a percentage of total revenue for the periods indicated:

| | | | | | | | | | | | | | | | |

|

|

| | | | | | | | |

| REVENUE: | | | | | | | | |

| % | | 99.4 | % | |

| | 0.6 | | |

| % | | 100.0 | % | |

| | | | |

| | | | |

| Expenses: | | | | | | | | |

| | 77.8 | | |

| | | | |

| | | | |

| | | | |

| | 5.1 | | |

| | 5.2 | | |

| | 2.1 | | |

| | 90.2 | | |

| | 9.8 | | |

| Other income (expense): | | | | | | | | |

| | (0.3) | | |

| | — | | |

| | (0.3) | | |

| | 9.5 | | |

| | 2.1 | | |

| | | | |

| | | | |

| | 7.4 | | |

| | — | | |

| | | | |

| % | | 7.4 | % | |

| | | | | | | | |

| | | | |

| | | | | | | | | | | | | | | | |

|

|

| | | | | | | | |

|

| 464,925 | | | $ | 408,732 | | |

| | 27,871 | | |

| NON-GAAP FINANCIAL MEASURES: | | | | | | | | |

| PERFORMANCE METRICS | | | | | | | | |

| | | | |

| | 314,609 | | |

| | 359,209 | | |

| | | | |

| | | | |

| | 383,570 | | |

| | | | |

| | 49,484 | | |

| | | | | | | | |

| VALUATION METRICS | | | | | | | | |

| 616,854 | | | | |

|

| 2022 |

| | |

|

| 272,762 | | | $ | 289,089 | |

| | |

| | 22,720 | |

| | |

| | (4,380) | |

| | |

| | |

| 365,310 | | | $ | 314,609 | |

(a) Litigation relates to specific proceedings arising outside of the ordinary course of business, which includes the portion attributable to non-controlling interests.

(b) Represents the write-off of deferred financing fees associated with the amendment of the Credit Facility.

(c) Costs incurred to acquire operations that are not capitalizable.

(d) Included in depreciation and amortization are amortization expenses related to patient base intangible assets at newly acquired skilled nursing and senior living facilities.

The table below reconciles net income to EBITDA, Adjusted EBITDA and Adjusted EBITDAR for the periods presented:

| | | | | | | | | | | | | | | | |

|

| 2022 | |

| | | | | | | | |

|

| 209,850 | | | $ | 224,652 | | |

| | (29) | | |

| | | | |

| | 7,736 | | |

| | 64,437 | | |

| | 62,355 | | |

| | | | |

| | | | |

| 327,303 | | | $ | 359,209 | | |

| | | | | | | | |

| | 22,720 | | |

| | | | |

| | 4,280 | | |

| | (4,380) | | |

| | | | |

| | | | |

| | 669 | | |

| | 1,072 | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| 419,496 | | | $ | 383,570 | | |

| | 153,049 | | |

| | | | |

| | | | |

| | | | |

| 616,854 | | | | |

| | | | |

| | | | | | | | |

(a) Litigation relates to specific proceedings arising outside of the ordinary course of business, which excludes the portion attributable to non-controlling interests.

(b) Costs incurred to acquire operations that are not capitalizable.

Year Ended December 31, 2023 Compared to the Year Ended December 31, 2022

The following table sets forth details of operating results for our revenue and earnings, and their respective components, by our reportable segment for the periods indicated.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Year Ended December 31, 2023 |

| | | Skilled Services | | Standard Bearer | | All Other | | Eliminations | | Consolidated |

| Total revenue | | $ | 3,578,855 | | | $ | 82,486 | | | $ | 155,804 | | | $ | (87,790) | | | $ | 3,729,355 | |

Total expenses, including other income (expense), net | | 3,113,930 | | | 53,421 | | | 377,055 | | | (87,790) | | | 3,456,616 | |

| Segment income (loss) | | 464,925 | | | 29,065 | | | (221,251) | | | — | | | 272,739 | |

| | | | | |

Gain on sale of assets and insurance recoveries from real estate, net | | | | | | | | | | 23 | |

| Income before provision for income taxes | | | | | | | | | | $ | 272,762 | |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Year Ended December 31, 2022 |

| | | Skilled Services | | Standard Bearer | | All Other | | Eliminations | | Consolidated |

| Total revenue | | $ | 2,906,215 | | | $ | 72,937 | | | $ | 122,610 | | | $ | (76,294) | | | $ | 3,025,468 | |

Total expenses, including other income (expense), net | | 2,497,483 | | | 45,066 | | | 273,391 | | | (76,294) | | | 2,739,646 | |

| Segment income (loss) | | 408,732 | | | 27,871 | | | (150,781) | | | — | | | 285,822 | |

Gain on sale of assets and insurance recoveries from real estate, net | | | | | | | | | | 3,267 | |

| Income before provision for income taxes | | | | | | | | | | $ | 289,089 | |

|

Our total revenue increased $703.9 million, or 23.3%, compared to the year ended December 31, 2022. The increase in revenue was primarily driven by an increase in occupancy of 3.2% from our skilled services Same Facilities and Transitioning Facilities coupled with increasing daily revenue rates and the impact of acquisitions. Specifically, our skilled services Recently Acquired Facilities increased total revenue by $450.0 million, when compared to the same period in 2022, with 52.0% of these operations being acquired in 2023. We believe this demonstrates our ability to increase our market share through strategic acquisitions of operations that have higher skilled mix and higher occupancy than our typical acquisitions. These increases are offset by a decrease in state relief revenue of $17.1 million as the end of the PHE created a gradual phase down of the temporary increase in FMAP funding. All state relief revenue is included in Medicaid revenue.

Skilled Services Segment

Revenue

The following table presents the skilled services revenue and key performance metrics by category during the year ended December 31, 2023 and 2022:

| | | | | | | | | | | | | | | | | | | | | | | |

| Year Ended December 31, |

| | 2023 | | 2022 | | Change | | % Change |

| | | | | | | |

| TOTAL FACILITY RESULTS: | (Dollars in thousands) |

| Skilled services revenue | $ | 3,578,855 | | | 2,906,215 | | | $ | 672,640 | | | 23.1 | % |

| Number of facilities at period end | 259 | | | 234 | | | 25 | | | 10.7 | % |

Number of campuses at period end(1) | 27 | | | 26 | | | 1 | | | 3.8 | % |

| Actual patient days | 8,590,995 | | | 7,243,781 | | | 1,347,214 | | | 18.6 | % |

| Occupancy percentage — Operational beds | 78.5 | % | | 75.3 | % | | | | 3.2 | % |

| Skilled mix by nursing days | 30.4 | % | | 31.8 | % | | | | (1.4) | % |

| Skilled mix by nursing revenue | 50.2 | % | | 52.0 | % | | | | (1.8) | % |

| | | | | | | | | | | | | | | | | | | | | | | |

| Year Ended December 31, |

| | 2023 | | 2022 | | Change | | % Change |

| | | | | | | |

SAME FACILITY RESULTS:(2) | (Dollars in thousands) |

| Skilled services revenue | $ | 2,771,633 | | | $ | 2,569,807 | | | $ | 201,826 | | | 7.9 | % |

| Number of facilities at period end | 189 | | | 189 | | | — | | | — | % |

Number of campuses at period end(1) | 24 | | | 24 | | | — | | | — | % |

| Actual patient days | 6,563,672 | | | 6,299,331 | | | 264,341 | | | 4.2 | % |

| Occupancy percentage — Operational beds | 79.2 | % | | 76.0 | % | | | | 3.2 | % |

| Skilled mix by nursing days | 31.9 | % | | 33.0 | % | | | | (1.1) | % |

| Skilled mix by nursing revenue | 51.4 | % | | 53.3 | % | | | | (1.9) | % |

| | | | | | | | | | | | | | | | | | | | | | | |

| Year Ended December 31, |

| 2023 | | 2022 | | Change | | % Change |

| | | | | | | |

TRANSITIONING FACILITY RESULTS:(3) | (Dollars in thousands) |

| Skilled services revenue | $ | 251,872 | | | $ | 231,100 | | | $ | 20,772 | | | 9.0 | % |

| Number of facilities at period end | 22 | | | 22 | | | — | | | — | % |

Number of campuses at period end(1) | 1 | | | 1 | | | — | | | — | % |

| Actual patient days | 655,659 | | | 625,085 | | | 30,574 | | | 4.9 | % |

| Occupancy percentage — Operational beds | 76.1 | % | | 72.9 | % | | | | 3.2 | % |

| Skilled mix by nursing days | 21.4 | % | | 23.1 | % | | | | (1.7) | % |

| Skilled mix by nursing revenue | 38.5 | % | | 41.4 | % | | | | (2.9) | % |

| | | | | | | | | | | | | | | | | | | | | | | |

| Year Ended December 31, |

| 2023 | | 2022 | | Change | | % Change |

| | | | | | | |

RECENTLY ACQUIRED FACILITY RESULTS:(4) | (Dollars in thousands) |

| Skilled services revenue | $ | 555,350 | | | $ | 105,308 | | | $ | 450,042 | | | NM |

| Number of facilities at period end | 48 | | | 23 | | | 25 | | | NM |

Number of campuses at period end(1) | 2 | | | 1 | | | 1 | | | NM |

| Actual patient days | 1,371,664 | | | 319,365 | | | 1,052,299 | | | NM |

| Occupancy percentage — Operational beds | 76.8 | % | | 67.9 | % | | | | NM |

| Skilled mix by nursing days | 27.5 | % | | 24.3 | % | | | | NM |

| Skilled mix by nursing revenue | 49.3 | % | | 42.8 | % | | | | NM |

(1)Campus represents a facility that offers both skilled nursing and senior living services. Revenue and expenses related to skilled nursing and senior living services have been allocated and recorded in the respective operating segment.

(2)Same Facility results represent all facilities purchased prior to January 1, 2020.

(3)Transitioning Facility results represent all facilities purchased from January 1, 2020 to December 31, 2021.

(4)Recently Acquired Facility (Acquisitions) results represent all facilities purchased on or subsequent to January 1, 2022.

Skilled services revenue increased $672.6 million, or 23.1%, compared to the year ended December 31, 2022. The increases in skilled services revenue were across all payer types including increases in Medicaid revenue of $315.9 million, or 23.2%, Medicare revenue of $153.6 million, or 18.5%, managed care revenue of $140.4 million, or 26.7% and private revenue of $62.7 million, or 33.1%.

The increase in skilled services revenue was driven by strong performance across our existing skilled services operations as our census continued to recover in 2023, as well as the favorable impact of skilled census from our recent acquisitions. Our consolidated occupancy increased by 3.2% during the year ended December 31, 2023 compared to the same period in 2022.

Revenue in our Same Facilities increased $201.8 million, or 7.9%, compared to the same period in 2022, due to increases in occupancy from both skilled and long-term care patients and revenue per patient day. Our diligent efforts to strengthen our partnerships with various managed care organizations, hospitals and the local communities we operate in, increased our managed care revenue by 14.8%, mainly due to increases in managed care days of 7.2% and revenue per patient day of 5.3%. We continued to see a shift in our patient population from Medicare to managed care as Medicare Advantage enrollment accounts for a larger portion of the overall population. In addition, Medicaid revenue increased by $116.7 million or 9.9%, mainly from the increases in Medicaid days and revenue per patient day.

Revenue generated by our Transitioning Facilities increased $20.8 million, or 9.0%, primarily due to improved occupancy growth and an increase in revenue per patient day. Our Medicaid revenue increased by 10.9%, Managed Care revenue increased by 12.3% and private revenue increased by 18.1%, demonstrating our ability to focus on increasing occupancy across payer types.

Skilled services revenue generated by Recently Acquired Facilities increased by approximately $450.0 million compared to the year ended December 31, 2022. The increases were primarily due to 26 operational expansions in 2023 as well as the full year impact of the 24 operational expansions in 2022.

In the future, if we acquire additional turnaround or start-up operations, we typically expect to see lower occupancy rates and skilled mix and these metrics are expected to vary from period to period based upon the maturity of the facilities within our portfolio. Historically, we have generally experienced lower occupancy rates and lower skilled mix at Recently Acquired Facilities and therefore, we anticipate generally lower overall occupancy during years of growth. Included in our metrics for Recently Acquired Facilities are 17 facilities we acquired that are mature and have higher occupancy rates, higher skilled mix days and higher skilled mix revenue than our typical acquisitions.

The following table reflects the change in skilled nursing average daily revenue rates by payor source, excluding services that are not covered by the daily rate (1): | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Year Ended December 31, |

| | Same Facility | | Transitioning | | Acquisitions | | Total |

| | 2023 | | 2022 | | 2023 | | 2022 | | 2023 | | 2022 | | 2023 | | 2022 |

| | | | | | | | | | | | | | | |

| SKILLED NURSING AVERAGE DAILY REVENUE RATES |

| Medicare | $ | 722.96 | | | $ | 694.63 | | | $ | 696.37 | | | $ | 668.05 | | | $ | 788.00 | | | $ | 652.15 | | | $ | 733.47 | | | $ | 691.25 | |

| Managed care | 537.29 | | | 510.18 | | | 536.93 | | | 501.73 | | | 555.55 | | | 455.19 | | | 539.25 | | | 508.53 | |

| Other skilled | 598.35 | | | 576.46 | | | 529.08 | | | 530.18 | | | 441.89 | | | 429.84 | | | 575.34 | | | 563.56 | |

| Total skilled revenue | 617.55 | | | 598.14 | | | 615.58 | | | 593.66 | | | 660.87 | | | 521.24 | | | 623.70 | | | 595.26 | |

| Medicaid | 275.82 | | | 259.89 | | | 270.67 | | | 254.08 | | | 256.51 | | | 227.21 | | | 272.14 | | | 257.67 | |

| Private and other payors | 263.81 | | | 250.80 | | | 253.15 | | | 248.63 | | | 263.71 | | | 199.34 | | | 262.93 | | | 248.54 | |

Total skilled nursing revenue | $ | 383.56 | | | $ | 370.57 | | | $ | 342.57 | | | $ | 332.09 | | | $ | 368.46 | | | $ | 296.15 | | | $ | 378.02 | | | $ | 363.97 | |

(1) These rates exclude state relief funding and include sequestration reversal of 1% for the second quarter in 2022 and 2% for the first quarter of 2022.

Our Medicare daily rates at Same Facilities and Transitioning Facilities increased by 4.1% and 4.2%, respectively, compared to the year ended December 31, 2022. The increase is attributable to the 2.7% and 4.0% net market basket increase that became effective in October 2022 and October 2023, respectively, offset by the phased reinstatement of the sequestration. During the year ended December 31, 2022, Medicare daily rates included three months of sequestration suspension of 1%, three months of sequestration suspension of 2% and six months of no sequestration suspension.

Our average Medicaid rates increased 5.6% due to state reimbursement increases and our participation in supplemental Medicaid payment programs and quality improvement programs in various states. Medicaid rates exclude the amount of state relief revenue we recorded.

Payor Sources as a Percentage of Skilled Nursing Services — We use our skilled mix as a measure of the quality of reimbursements we receive at our independent skilled nursing facilities over various periods.

The following tables set forth our percentage of skilled nursing patient revenue and days by payor source:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Year Ended December 31, |

| | Same Facility | | Transitioning | | Acquisitions | | Total |

| | 2023 | | 2022 | | 2023 | | 2022 | | 2023 | | 2022 | | 2023 | | 2022 |

| | | | | | | | | | | | | | | |

| PERCENTAGE OF SKILLED NURSING REVENUE |

| Medicare | 22.5 | % | | 26.0 | % | | 21.8 | % | | 24.9 | % | | 31.0 | % | | 20.4 | % | | 23.8 | % | | 25.7 | % |

| Managed care | 20.1 | | | 19.2 | | | 12.6 | | | 12.6 | | | 13.3 | | | 9.9 | | | 18.5 | | | 18.3 | |

| Other skilled | 8.8 | | | 8.1 | | | 4.1 | | | 3.9 | | | 5.0 | | | 12.5 | | | 7.9 | | | 8.0 | |

| Skilled mix | 51.4 | | | 53.3 | | | 38.5 | | | 41.4 | | | 49.3 | | | 42.8 | | | 50.2 | | | 52.0 | |

| Private and other payors | 7.5 | | | 7.0 | | | 8.6 | | | 8.1 | | | 8.0 | | | 6.4 | | | 7.6 | | | 7.0 | |

| | | | | | | | | | |

| Medicaid | 41.1 | | | 39.7 | | | 52.9 | | | 50.5 | | | 42.7 | | | 50.8 | | | 42.2 | | | 41.0 | |

| TOTAL SKILLED NURSING | 100.0 | % | | 100.0 | % | | 100.0 | % | | 100.0 | % | | 100.0 | % | | 100.0 | % | | 100.0 | % | | 100.0 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Year Ended December 31, |

| | Same Facility | | Transitioning | | Acquisitions | | Total |

| | 2023 | | 2022 | | 2023 | | 2022 | | 2023 | | 2022 | | 2023 | | 2022 |

| | | | | | | | | | | | | | | |

| PERCENTAGE OF SKILLED NURSING DAYS |

| Medicare | 11.9 | % | | 13.9 | % | | 10.7 | % | | 12.4 | % | | 14.5 | % | | 9.3 | % | | 12.3 | % | | 13.5 | % |

| Managed care | 14.4 | | | 14.0 | | | 8.0 | | | 8.3 | | | 8.8 | | | 6.4 | | | 13.0 | | | 13.1 | |

| Other skilled | 5.6 | | | 5.1 | | | 2.7 | | | 2.4 | | | 4.2 | | | 8.6 | | | 5.1 | | | 5.2 | |

| Skilled mix | 31.9 | | | 33.0 | | | 21.4 | | | 23.1 | | | 27.5 | | | 24.3 | | | 30.4 | | | 31.8 | |

| Private and other payors | 11.0 | | | 10.4 | | | 11.7 | | | 10.8 | | | 11.1 | | | 9.5 | | | 11.0 | | | 10.3 | |

| | | | | | | | | | |

|

| | | | | | | |

|

| % |

| | | | | | | |

|

|

| | 16.6 | |

| | | | | | | |

Rental revenue — Our rental revenue, including revenue generated from our independent subsidiaries, increased by $9.5 million, or 13.1%, to $82.5 million, compared to the year ended December 31, 2022. The increase in revenue is primarily attributable to five real estate purchases as well as annual rent increases since the year ended December 31, 2022.

FFO — Our FFO increased by $4.8 million, or 9.7%, to $54.3 million, compared to the year ended December 31, 2022. The increase in rental revenue of $9.5 million is offset by increases in interest expense of $4.3 million associated with the intercompany debt arrangements between Standard Bearer and us, as we continue to grow our real estate portfolio.

All Other Revenue

Our other revenue increased by $33.2 million, or 27.1%, to $155.8 million, compared to the year ended December 31, 2022. Other revenue for 2023 includes senior living revenue of $76.4 million, revenue from other ancillary services of $68.3 million and rental income of $11.1 million. The increase in other revenue is primarily attributable to our other ancillary services as well as senior living operations' occupancy starting to rebound from COVID-19.

Consolidated Financial Expenses

Rent-cost of services — Our rent-cost of services as a percentage of total revenue increased by 0.2% to 5.3%, primarily due to lease obligations acquired as part of our 22 operational expansions with long-term leases since the year ended December 31, 2022.

General and administrative expense — General and administrative expense increased $104.2 million or 65.6%, to $263.0 million. General and administrative expense as a percentage of revenue increased by 1.9% to 7.1%. This increase was primarily due to increases in litigation expense related to specific proceedings that are outside the ordinary course of business, system implementation costs, bonuses due to enhanced performance and headcount due to acquisition activity. Excluding the litigation expense, general and administrative expense as a percentage of revenue increased by 0.2% to 5.4%.

Depreciation and amortization — Depreciation and amortization expense increased $10.0 million, or 16.1%, to $72.4 million. This increase was primarily related to the additional depreciation and amortization incurred as a result of our newly acquired operations and capital expenditures. Depreciation and amortization decreased 0.2%, to 1.9%, as a percentage of revenue.

Other income (expense), net — Other income (expense), net as a percentage of revenue increased by 0.8%. Other income primarily includes interest income from our investments offset by interest expense related to our debt. Additionally, our deferred investment program may incur gains or losses depending on market performance. During the year ended December 31, 2023, the deferred compensation investment program had a gain of $4.6 million. During the year ended December 31, 2022, the deferred compensation investment program had a loss of $4.2 million. The offsetting expenses or reduction in expenses are allocated between cost of services and general and administrative expenses.

Provision for income taxes — Our effective tax rate was 23.1% for the year ended December 31, 2023, compared to 22.3% for the same period in 2022. The effective tax rate for both periods is driven by the impact of excess tax benefits from stock-based compensation, partially offset by non-deductible expenses, including non-deductible compensation. See Note 14, Income Taxes, in the Financial Statements for further discussion.

Liquidity and Capital Resources

Our primary sources of liquidity have historically been derived from our cash flows from operations and long-term debt secured by our real property and our Credit Facility. Our liquidity as of December 31, 2023 is impacted by cash generated from strong operational performance and increased acquisition and share repurchase activities.

Historically, we have primarily financed the majority of our acquisitions through mortgages on our properties, our Credit Facility and cash generated from operations. Cash paid to fund acquisitions was $69.0 million and $101.1 million for the year ended December 31, 2023 and 2022, respectively. Total capital expenditures for property and equipment were $106.2 million and $87.5 million for the year ended December 31, 2023 and 2022, respectively. We currently have approximately $110.0 million budgeted for renovation projects in 2024. We believe our current cash balances, our cash flow from operations and the amounts available for borrowing under our Credit Facility will be sufficient to cover our operating needs for at least the next 12 months.

We may, in the future, seek to raise additional capital to fund growth, capital renovations, operations and other business activities, but such additional capital may not be available on acceptable terms, on a timely basis, or at all.

Our cash and cash equivalents as of December 31, 2023 consisted of bank term deposits, money market funds and U.S. Treasury bill related investments. In addition, as of December 31, 2023, we held investments of approximately $109.9 million. We believe our investments that were in an unrealized loss position as of December 31, 2023 do not require an allowance for expected credit losses, nor has any event occurred subsequent to that date that would indicate so.

As mentioned above, our primary source of cash is from our ongoing operations. Our positive cash flows have supported our business and have allowed us to pay regular dividends to our stockholders. We currently anticipate that existing cash and total investments as of December 31, 2023, along with projected operating cash flows and available financing, will support our normal business operations for the foreseeable future.

On August 29, 2023, the Board of Directors approved a stock repurchase program pursuant to which we may repurchase up to $20.0 million of our common stock under the program for a period of approximately 12 months from September 1, 2023. Under this program, we are authorized to repurchase our issued and outstanding common shares from time to time in open-market and privately negotiated transactions and block trades in accordance with federal securities laws. The share repurchase program does not obligate us to acquire any specific number of shares. We did not purchase any shares pursuant to this stock repurchase program during the year ended December 31, 2023.

On July 28, 2022, the Board of Directors approved a stock repurchase program pursuant to which we may repurchase up to $20.0 million of our common stock under the program for a period of approximately 12 months from August 2, 2022. Under this program, we were authorized to repurchase our issued and outstanding common shares from time to time in open-market and privately negotiated transactions and block trades in accordance with federal securities laws. The share repurchase program did not obligate us to acquire any specific number of shares. The stock repurchase program expired on August 2, 2023 and is no longer in effect. The Company did not purchase any shares pursuant to this stock repurchase program.

The following table presents selected data from our consolidated statement of cash flows for the periods presented:

| | | | | | | | | | | | |

| Year Ended December 31, |

| | 2023 | | 2022 | |

| | | | |

|

| NET CASH PROVIDED BY/(USED IN): | (In thousands) |

| Operating activities | $ | 376,666 | | | $ | 272,513 | | |

| Investing activities | (182,698) | | | (186,182) | | |

| Financing activities | (612) | | | (32,262) | | |

|

| Net increase in cash and cash equivalents | 193,356 | | | 54,069 | | |

| Cash and cash equivalents beginning of period | 316,270 | | | 262,201 | | |

|

|

| Cash and cash equivalents at end of period | $ | 509,626 | | | $ | 316,270 | | |

Operating Activities

Cash provided by operating activities is net income adjusted for certain non-cash items and changes in operating assets and liabilities.

The $104.2 million increase in cash provided by operating activities for the year ended December 31, 2023 compared to the same period in 2022 was due to cash generated from improved results at our local operations as well as $24.2 million that was paid for deferred social security taxes in 2022, which did not occur in 2023.

Investing Activities

Investing cash flows consist primarily of capital expenditures, investment activities, insurance proceeds and cash used for acquisitions.

The $3.5 million decrease in cash used in investing activities for the year ended December 31, 2023 compared to the same period in 2022 was primarily due to a decrease in cash used for operational expansions of $32.1 million, offset by an increase in cash used for capital expenditures of $18.6 million, an increase in investments of $3.1 million and a decrease of cash proceeds from the sale of fixed assets and insurance proceeds of $7.7 million.

Financing Activities

Financing cash flows consist primarily of payment of dividends to stockholders, issuance and repayment of short-term and long-term debt, payment for share repurchases and sale of subsidiary shares.

The $31.7 million decrease in cash used in financing activities for the year ended December 31, 2023 compared to the same period in 2022, was primarily due to $29.9 million of share repurchases as part of our stock repurchase program in 2022.

A discussion of our cash flows for the year ended December 31, 2021 is included in Part II, Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations - Liquidity and Capital Resources, included in our Annual Report on Form 10-K for the year ended December 31, 2022 filed with the Securities and Exchange Commission on February 2, 2023.

Material cash requirements from known contractual and other obligations

Total long-term debt obligations outstanding as of the end of each fiscal year were as follows:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | December 31, |

| | 2023 | | 2022 | | 2021 | | 2020 | | 2019 |

| | | | | | | | | |

| | (In thousands) |

| Credit facilities and term loans | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | 210,000 | |

Mortgage loans and promissory note | 152,388 | | | 156,271 | | | 159,967 | | | 117,806 | | | 120,350 | |

| TOTAL | $ | 152,388 | | | $ | 156,271 | | | $ | 159,967 | | | $ | 117,806 | | | $ | 330,350 | |

| | | | | | | | | |

Significant contractual obligations as of December 31, 2023 were as follows, including the future periods in which payments are expected:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 2024 | | 2025 | | 2026 | | 2027 | | 2028 | | Thereafter | | Total |

| | | | | | | | | | | | | | |

| | | (In thousands) |

| Operating lease obligations | | $ | 191,352 | | | $ | 191,269 | | | $ | 191,058 | | | $ | 190,481 | | | $ | 189,224 | | | $ | 1,722,259 | | | $ | 2,675,643 | |

| Long-term debt obligations | | 3,950 | | | 4,086 | | | 4,227 | | | 3,897 | | | 3,779 | | | 132,449 | | | 152,388 | |

| Interest payments on long-term debt | | 4,623 | | | 4,487 | | | 4,346 | | | 4,207 | | | 4,091 | | | 54,436 | | | 76,190 | |

| TOTAL | | $ | 199,925 | | | $ | 199,842 | | | $ | 199,631 | | | $ | 198,585 | | | $ | 197,094 | | | $ | 1,909,144 | | | $ | 2,904,221 | |

| | | | | | | | | | | | | | |

Not included in the table above are our actuarially determined self-insured general and professional malpractice liability, workers' compensation and medical (including prescription drugs) and dental healthcare obligations, which are broken out between current and long-term liabilities in our financial statements included in this Annual Report on Form 10-K.

As part of the proceeding discussed in Item 3. Legal Proceedings, the parties agreed to settle the litigation for $48.0 million, subject to the review and approval of all parties, including the DOJ and other relevant government entities.

Credit Facility with a Lending Consortium Arranged by Truist

We maintain a revolving credit facility with Truist Securities (Truist) (the Credit Facility) with availability up to $600.0 million in aggregate principal amount. The maturity date of the Credit Facility is April 8, 2027. Borrowings are supported by a lending consortium arranged by Truist. The interest rates applicable to loans under the Credit Facility are, at our option, equal to either a base rate plus a margin ranging from 0.25% to 1.25% per annum or SOFR plus a margin range from 1.25% to 2.25% per annum, based on the Consolidated Total Net Debt to Consolidated EBITDA ratio (as defined in the Credit Facility). In addition, there is a commitment fee on the unused portion of the commitments that ranges from 0.20% to 0.40% per annum, depending on the Consolidated Total Net Debt to Consolidated EBITDA ratio.

Mortgage Loans and Promissory Note

As of December 31, 2023, 23 of our subsidiaries have mortgage loans insured with HUD for an aggregate amount of $150.2 million, which subjects these subsidiaries to HUD oversight and periodic inspections. The mortgage loans bear effective interest rates at a range of 3.1% to 4.2%, including fixed interest rates at a range of 2.4% to 3.3% per annum. In addition to the interest rate, we incur other fees for HUD placement, including but not limited to audit fees. Amounts borrowed under the mortgage loans may be prepaid, subject to prepayment fees of the principal balance on the date of prepayment. For the majority of the loans, during the first three years, the prepayment fee is 10.0%, and is reduced by 3.0% in the fourth year of the loan, and reduced by 1.0% per year for years five through ten of the loan. There is no prepayment penalty after year ten. The terms for all the mortgage loans are 25 to 35 years.

In addition to the HUD mortgage loans, one of our subsidiaries has a promissory note that bears a fixed interest rate of 5.3% per annum and has a term of 12 years. The note, which was used for an acquisition, is secured by the real property comprising the facility and the rent, issues and profits thereof, as well as all personal property used in the operation of the facility.

Operating Leases

As of December 31, 2023, 214 of our facilities are under long-term lease arrangements, of which 96 of the operations are under nine triple-net Master Leases and one stand-alone lease with CareTrust REIT, Inc. (CareTrust). The Master Leases consist of multiple leases, each with its own pool of properties, that have varying maturities and diversity in property geography. Under each master lease, our individual subsidiaries that operate those properties are the tenants and CareTrust's individual subsidiaries that own the properties subject to the Master Leases are the landlords. The rent structure under the Master Leases includes a fixed component, subject to annual escalation equal to the lesser of the percentage change in the Consumer Price Index (but not less than zero) or 2.5%. At our option, we can extend the Master Leases for two or three five-year renewal terms beyond the initial term, on the same terms and conditions. If we elect to renew the term of a Master Lease, the renewal will be effective as to all, but not less than all, of the leased property then subject to the Master Lease. Additionally, four of the 97 facilities leased from CareTrust include an option to purchase that we can exercise starting on December 1, 2024.

We also lease certain facilities and our administrative offices under non-cancelable operating leases, most of which have initial lease terms ranging from five to 20 years and is subject to annual escalation equal to the percentage change in the Consumer Price Index with a stated cap percentage. In addition, we lease certain of our equipment under non-cancelable operating leases with initial terms ranging from three to five years. Most of these leases contain renewal options, certain of which involve rent increases.

Eighty of our independent subsidiaries, excluding the subsidiaries that are operated under the Master Leases from CareTrust, are operated under 13 separate master lease arrangements. Under these master leases, a default at a single facility could subject one or more of the other independent subsidiaries covered by the same master lease to the same default risk. Failure to comply with Medicare and Medicaid provider requirements is a default under several of our leases, master lease agreements and debt financing instruments. In addition, other potential defaults related to an individual facility may cause a default of an entire master lease portfolio and could trigger cross-default provisions in our outstanding debt arrangements and other leases. With an indivisible lease, it is difficult to restructure the composition of the portfolio or economic terms of the lease without the consent of the landlord.

Inflation

We have historically derived a substantial portion of our revenue from the Medicare program. We also derive revenue from state Medicaid and similar reimbursement programs. Payments under these programs generally provide for reimbursement levels that are adjusted for inflation annually based upon the state’s fiscal year for the Medicaid programs and in each October for the Medicare program. These adjustments may not continue in the future, and even if received, such adjustments may not reflect the actual increase in our costs for providing healthcare services.

Labor, supply expenses and capital expenditures make up a substantial portion of our cost of services. Those expenses can be subject to increase in periods of rising inflation and when labor shortages occur in the marketplace. To date, we have generally been able to implement cost control measures or obtain increases in reimbursement sufficient to offset increases in these expenses. There can be no assurance that we will be able to anticipate fully or otherwise respond to any future inflationary pressures.

Item 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Interest Rate Risk — We are exposed to risks associated with market changes in interest rates through our borrowing arrangements and investments. In particular, our Credit Facility exposes us to variability in interest payments due to changes in SOFR interest rates. We manage our exposure to this market risk by monitoring available financing alternatives. Our mortgages and promissory note require principal and interest payments through maturity pursuant to amortization schedules.

Our mortgages generally contain provisions that allow us to make repayments earlier than the stated maturity date. In some cases, we are not allowed to make early repayment prior to a cutoff date. Where prepayment is permitted, we are generally allowed to make prepayments only at a premium which is often designed to preserve a stated yield to the note holder. These prepayment rights may afford us opportunities to mitigate the risk of refinancing our debts at maturity at higher rates by refinancing prior to maturity.

We have a Credit Facility with Truist of up to $600.0 million in aggregate principal amount. We have no outstanding borrowings under our Credit Facility as of December 31, 2023 and through the filing date of this report. In addition, we have outstanding indebtedness under mortgage loans insured with HUD and a promissory note payable to a third party of $152.4 million, all of which are at fixed interest rates.

Our cash and cash equivalents as of December 31, 2023 consisted of bank term deposits, money market funds and U.S. Treasury bill related investments. In addition, as of December 31, 2023, we held investments of approximately $109.9 million. We believe our investments that were in an unrealized loss position as of December 31, 2023 do not require an allowance for expected credit losses, nor has any event occurred subsequent to that date that would indicate so. Our market risk exposure is interest income sensitivity, which is affected by changes in the general level of U.S. interest rates. The primary objective of our investment activities is to preserve principal, while at the same time maximizing the income we receive from our investments without significantly increasing risk. Due to the low risk profile of our investment portfolio, an immediate 10.0% change in interest rates would not have a material effect on the fair market value of our portfolio. Accordingly, we would not expect our operating results or cash flows to be affected to any significant degree by the effect of a sudden change in market interest rates on our securities portfolio.

The above only incorporates those exposures that exist as of December 31, 2023 and does not consider those exposures or positions which could arise after that date. If we diversify our investment portfolio into securities and other investment alternatives, we may face increased risk and exposures as a result of interest risk and the securities markets in general.

Item 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

THE ENSIGN GROUP, INC.

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

AND FINANCIAL STATEMENT SCHEDULE

| | | | | |

| |

| |

| Consolidated Financial Statements: | |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

|

|

|

|

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM