ESTEE LAUDER COMPANIES INC - Annual Report: 2017 (Form 10-K)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

ý ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended June 30, 2017

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number 1-14064

The Estée Lauder Companies Inc.

(Exact name of registrant as specified in its charter)

|

Delaware |

|

11-2408943 |

|

(State or other jurisdiction of incorporation or organization) |

|

(I.R.S. Employer Identification No.) |

|

|

|

|

|

767 Fifth Avenue, New York, New York |

|

10153 |

|

(Address of principal executive offices) |

|

(Zip Code) |

Registrant’s telephone number, including area code 212-572-4200

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class |

|

Name of each exchange |

|

|

|

|

|

Class A Common Stock, $.01 par value |

|

New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ý |

|

Accelerated filer o |

|

|

|

Non-accelerated filer o (Do not check if a smaller reporting company) |

|

Smaller reporting company o |

|

Emerging growth company o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

The aggregate market value of the registrant’s voting common equity held by non-affiliates of the registrant was approximately $17 billion at December 31, 2016 (the last business day of the registrant’s most recently completed second quarter).*

At August 18, 2017, 224,193,862 shares of the registrant’s Class A Common Stock, $.01 par value, and 143,762,288 shares of the registrant’s Class B Common Stock, $.01 par value, were outstanding.

Documents Incorporated by Reference

|

Document |

|

Where Incorporated |

|

|

|

|

|

Proxy Statement for Annual Meeting of |

|

Part III |

* Calculated by excluding all shares held by executive officers and directors of registrant and certain trusts without conceding that all such persons are “affiliates” of registrant for purposes of the Federal securities laws.

THE ESTÉE LAUDER COMPANIES INC.

INDEX TO ANNUAL REPORT ON FORM 10-K

Cautionary Note Regarding Forward-Looking Information and Risk Factors

This Annual Report on Form 10-K includes “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements include our expectations regarding sales, earnings or other future operations, financial performance or liquidity, our long-term strategy, restructuring and other initiatives, product introductions, geographic regions or channels, information systems initiatives and new methods of sale. Although we believe that our expectations are based on reasonable assumptions within the bounds of our knowledge of our business and operations, we cannot assure that actual results will not differ materially from our expectations. Factors that could cause actual results to differ from expectations are described herein; in particular, see “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations – Cautionary Note Regarding Forward-Looking Information.” In addition, there is a discussion of risks associated with an investment in our securities, see “Item 1A. Risk Factors.”

Unless the context requires otherwise, references to “we,” “us,” “our” and the “Company” refer to The Estée Lauder Companies Inc. and its subsidiaries.

The Estée Lauder Companies Inc., founded in 1946 by Estée and Joseph Lauder, is one of the world’s leading manufacturers and marketers of quality skin care, makeup, fragrance and hair care products. Our products are sold in over 150 countries and territories under a number of well-known brand names including: Estée Lauder, Clinique, Origins, MžAžC, Bobbi Brown, La Mer, Jo Malone London, Aveda and Too Faced. We are also the global licensee for fragrances and/or cosmetics sold under various designer brand names, including Tommy Hilfiger, Donna Karan New York, DKNY, Michael Kors and Tom Ford. Each brand is distinctly positioned within the market for cosmetics and other beauty products.

We believe we are a leader in the beauty industry due to the global recognition of our brand names, our leadership in product innovation, our strong position in key geographic markets and the consistently high quality of our products and “High-Touch” services. We sell our prestige products principally through limited distribution channels to complement the images associated with our brands. These channels consist primarily of department stores, specialty multi-brand retailers, upscale perfumeries and pharmacies and prestige salons and spas. In addition, our products are sold in our own and authorized freestanding stores, our own and authorized retailer websites, stores in airports and on cruise ships, in-flight, and duty-free shops. We believe that our strategy of pursuing selective distribution strengthens our relationships with retailers and consumers, enables our brands to be among the best selling product lines at the stores and online, and heightens the aspirational quality of our brands.

For a discussion of recent developments, see Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations – Results of Operations – Overview.

For segment and geographical area financial information, see Item 8. Financial Statements and Supplementary Data – Note 21 – Segment Data and Related Information.

We have been controlled by the Lauder family since the founding of our Company. Members of the Lauder family, some of whom are directors, executive officers and/or employees, beneficially own, directly or indirectly, as of August 18, 2017, shares of Class A Common Stock and Class B Common Stock having approximately 87% of the outstanding voting power of the Common Stock.

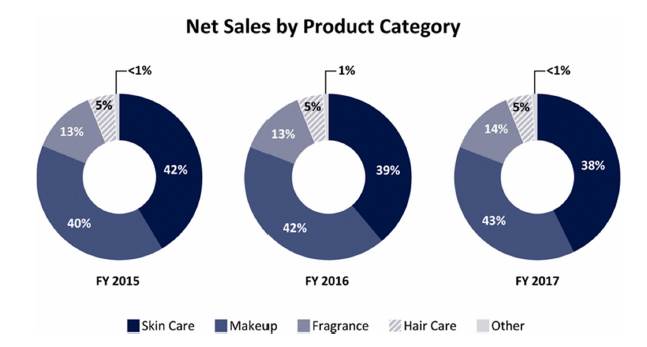

Products

Skin Care - Our broad range of skin care products addresses various skin care needs. These products include moisturizers, serums, cleansers, toners, body care, exfoliators, acne and oil correctors, facial masks, cleansing devices and sun care products. A number of our products are developed for use on particular areas of the body, such as the face, the hands or around the eyes.

Makeup - We manufacture, market and sell a full array of makeup products, including those for the face, eyes, lips and nails. Many of the products are offered in an extensive palette of shades and colors. We also sell related items such as compacts, brushes and other makeup tools.

Fragrance - We offer a variety of fragrance products. The fragrances are sold in various forms, including eau de parfum sprays and colognes, as well as lotions, powders, creams, bath/shower products, candles and soaps that are infused with a particular fragrance.

Hair Care - Hair care products are offered mainly in prestige salons and in freestanding stores as well as some department stores and specialty multi-brand retailers, and include shampoos, conditioners, styling products, treatment, finishing sprays and hair color products.

Other - We also sell ancillary products and services.

Our Brands

Given the personal nature of our products and the wide array of consumer preferences and tastes, as well as competition for the attention of consumers, our strategy has been to market and promote our products through distinctive brands seeking to address broad preferences and tastes. Each brand has a single global image that is promoted with consistent logos, packaging and advertising designed to enhance its image and differentiate it from other brands in the market. Beauty brands are differentiated by numerous factors, including quality, performance, a particular lifestyle, where they are distributed (e.g., prestige, mass) and price point. Below is a chart showing most of the brands that we sell and how we view them based on lifestyle and price point:

In addition to the brands described above, we manufacture and sell products under the Prescriptives, RODIN olio lusso and FLIRT! brands. We also develop and sell products under a license from Kiton.

Our “heritage brands” are Estée Lauder, Clinique and Origins. Our “makeup artist brands” are MžAžC and Bobbi Brown. Our “luxury brands” are La Mer, Jo Malone London, Tom Ford, AERIN, RODIN olio lusso, Le Labo, Editions de Parfums Frédéric Malle and By Kilian. Our “designer fragrances” are sold under the Tommy Hilfiger, Donna Karan New York, DKNY, Michael Kors, Kiton, Ermenegildo Zegna and Tory Burch licenses noted above.

Distribution

We sell our products primarily through limited distribution channels that complement the luxury image and prestige status of our brands. These channels consist primarily of department stores, specialty multi-brand retailers, upscale perfumeries and pharmacies and prestige salons and spas. In addition, our products are sold in freestanding stores that are operated either by us or by authorized third parties, through our own and third-party operated e-commerce websites and websites of our authorized retailers, in various travel retail locations such as stores in airports and on cruise ships, in-flight and duty-free shops, and certain fragrances are sold in self-select outlets. As is customary in the cosmetics industry, our practice is to accept returns of our products from retailers if properly requested and approved.

We have strategically opened new freestanding stores globally that we or authorized third parties operate, led by MžAžC, Jo Malone London, Bobbi Brown and Aveda. We are also evaluating opportunities to open additional freestanding stores for certain of our other brands. As of June 30, 2017, we operated approximately 1,430 freestanding stores, and more than 500 freestanding stores are operated around the world by authorized third parties. We expect the number of freestanding stores to increase over the next several years.

We currently sell products from most of our brands directly to consumers online through Company-owned and operated e-commerce and m-commerce sites in approximately 35 countries. While today a majority of our online sales are generated in the United States and the United Kingdom, we have ample opportunity for expansion of online sales growth globally. Additionally, our products are sold through various websites operated by authorized retailers.

We maintain dedicated sales teams that manage our retail accounts. We have wholly-owned operations in over 50 countries, and two controlling interests that operate in several countries, through which we market, sell and distribute our products. In certain countries, we sell our products through carefully selected distributors that share our commitment to protecting the image and position of our brands. In addition, we sell certain products in select domestic and international U.S. military exchanges. For information regarding our net sales and long-lived assets by geographic region, see Item 8. Financial Statements and Supplementary Data – Note 21 – Segment Data and Related Information.

Customers

Our strategy is to build strong relationships globally with select retailers, as well as with our consumers directly through freestanding stores, e-commerce sites and social media. Senior management works with executives of our major retail accounts on a regular basis, and we believe we are viewed as an important supplier to these customers. Our largest customer, Macy’s Inc., sells products primarily within the United States and accounted for 8% of our consolidated net sales for fiscal 2017, 9% for fiscal 2016 and 10% for fiscal 2015, and 8% and 13% of our accounts receivable as of June 30, 2017 and 2016, respectively.

Marketing

Our strategy to market and promote our products begins with our well-diversified portfolio of more than 25 distinctive brands across four product categories. Our portfolio can be deployed in multiple distribution channels and geographies where our global reputation and awareness of our brands benefit us. Our geographic and distribution channel diversity allows us to engage local consumers across an array of developed and emerging markets by emphasizing products and services with the greatest local relevance and appeal. This strategy is built around “Bringing the Best to Everyone We Touch.” Our founder, Mrs. Estée Lauder, formulated this unique marketing philosophy to provide “High-Touch” service and high quality products as the foundation for a solid and loyal consumer base. Our “High-Touch” approach is demonstrated through our integrated consumer engagement models that leverage our product specialists and technology to provide the consumer with a distinct experience that can include personal consultations with beauty advisors, in person or online, who demonstrate and educate the consumer on product usage and application. We plan to continue to leverage our core strengths, including the quality of our products, our “High-Touch” care to consumers and a diversified portfolio of brands, channels and geographies.

Our marketing strategies vary by brand, local market and distribution channel. Our diverse portfolio of brands employ different engagement models suited to each brand’s equity, distribution, product focus and understanding of the core consumer. This enables us to elevate the consumer experience as we attract new customers, build loyalty, drive consumer advocacy and address the transformation of consumer shopping behaviors. Our marketing planning approach leverages local insights to optimize allocation of resources across different media outlets and retail touch points to resonate with our most discerning consumers most effectively. This includes strategically deploying our brands and tailoring product assortments and communications to fit local tastes and preferences in cities and neighborhoods. Most of our creative marketing work is done by in-house teams that design and produce the sales materials, social media strategies, advertisements and packaging for products in each brand. We build brand equity and drive traffic to retail locations and to our own and authorized retailers’ websites through digital and social media, magazines and newspapers, television, billboards in cities and airports, and direct mail and email. In addition, we seek editorial coverage for our brands and products in digital and social media and print, to drive influencer amplification.

We are increasing our brand awareness and sales by continuing to elevate our digital presence encompassing e-commerce and m-commerce, as well as digital, social media and influencer marketing. We continue to innovate to better meet consumer online shopping preferences (e.g., how-to videos, ratings and reviews and mobile phone and tablet applications), support e-commerce and m-commerce businesses via digital and social marketing activities designed to build brand equity and “High-Touch” consumer engagement, in order to continue to offer unparalleled service and set the standard for prestige beauty shopping online. We also support our authorized retailers to strengthen their e-commerce businesses and drive sales of our brands on their websites. We have opportunities to expand our brand portfolio online around the world, and we are investing in and testing new omnichannel concepts in the United States and other established markets to increase brand loyalty by better serving consumers as they shop across channels. We have dedicated resources to implement creative, coordinated, brand-enhancing strategies across all online activities to increase our direct access to consumers.

Promotional activities and in-store displays are designed to attract new consumers and introduce existing consumers to other product offerings from the respective brands. Our marketing efforts also benefit from cooperative advertising programs with some retailers, some of which are supported by coordinated promotions, such as sampling programs, including purchase with purchase and gift with purchase, and we continue to believe that the quality and perceived benefits of sample products have been effective inducements to purchases by new and existing consumers. Such activities attract consumers to our counters and websites and keep existing consumers engaged. Our marketing and sales executives spend considerable time in the field meeting with consumers, retailers, beauty advisors and makeup artists at the points of sale to enable us to offer a seamless experience across channels of distribution.

Information Systems

Information systems support business processes including product development, marketing, sales, order processing, production, distribution and finance. We continue to maintain and enhance these systems in alignment with our long-term strategy. Many elements of our global information technology infrastructure are managed by third-party providers under vendor-owned, cloud-based models where we pay for services as they are consumed. This allows a more scalable platform to support current and future requirements and improves our agility and flexibility to respond to the demands of the business by leveraging more advanced technologies.

We continue to upgrade many of our legacy systems, including retail systems and retail capabilities globally. The retail system upgrades are expected to enhance the effectiveness of store operations, and support our omnichannel objectives. During fiscal 2017, we substantially completed retail system upgrades to our freestanding stores in North America and began our implementation in the Asia/Pacific region. Over the next few years, we plan to continue to implement upgraded point of sale, retail merchandising, and retail workforce management solutions in certain key markets globally.

Most of our locations are currently enabled with SAP-based technologies (“SAP”). We continue to develop and invest in new data insight and analytic capabilities to allow us to more effectively utilize the information provided by SAP, as well as strategic sources of both internal and external data. In addition, we are making continuous investments to integrate changes to systems applications with SAP that we expect will bring value creation to the business and increase productivity. In particular, we are optimizing certain of our supply chain capabilities, including inventory and warehouse management, as well as adding capabilities to enhance certain financial processes and workforce management solutions.

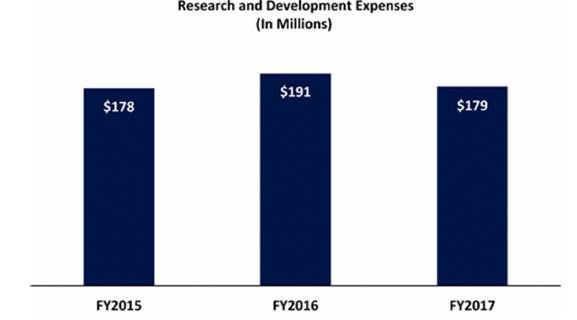

Research and Development

We believe that we are an industry leader in the development of new products. Our research and development group, which includes scientists and other employees involved in product innovation and packaging design and development, works closely with our marketing and product development teams and third-party suppliers to generate ideas, develop new products and product-line extensions, create new packaging concepts, and improve, redesign or reformulate existing products. In addition, these research and development personnel provide ongoing technical assistance and know-how to quality assurance and manufacturing personnel on a worldwide basis, to ensure consistent global standards for our products and to deliver products that meet or exceed consumer expectations. The research and development group has long-standing working relationships with several U.S. and international medical and educational facilities, which supplement internal capabilities. Members of the research and development group are also responsible for regulatory compliance matters.

Research and development costs are expensed as incurred. As of June 30, 2017, we had approximately 760 employees engaged in research and development activities. We maintain research and development programs at certain of our principal facilities and facilities dedicated to performing research and development, see Item 2. Properties.

We do not conduct animal testing on our products or ingredients, and do not ask others to test on our behalf, except when required by law.

Manufacturing, Warehousing and Raw Materials

We manufacture our products primarily in the United States, Belgium, Switzerland, the United Kingdom and Canada. We continue to streamline our manufacturing processes and identify sourcing opportunities to improve innovation, increase efficiencies, minimize our impact on the environment and reduce costs. Our major manufacturing facilities operate as “focus” plants that primarily manufacture one category of product (e.g., makeup) for most of our principal brands. Our plants are modern, and our manufacturing processes are substantially automated. While we believe that our network of manufacturing facilities and third-party manufacturers is sufficient to meet current and reasonably anticipated manufacturing requirements, we continue to identify opportunities to make significant improvements in capacity, technology, and productivity and align our manufacturing with regional sales demand. To capitalize on innovation and other supply chain benefits, we also continue to utilize a network of third-party manufacturers on a global basis.

We have established a global distribution network designed to meet the changing demands of our customers while maintaining service levels. We are continuously evaluating and adjusting this physical distribution network. We have established regional distribution centers, including those maintained by third parties, strategically positioned throughout the world in order to facilitate efficient delivery of our products to our customers.

The principal raw materials used in the manufacture of our products are essential oils, alcohols and specialty chemicals. We also purchase packaging components that are manufactured to our design specifications. Procurement of materials for all manufacturing facilities is generally made on a global basis through our Global Supplier Relations function. We review our supplier base periodically with the specific objectives of improving quality, increasing innovation and speed-to-market and reducing costs. In addition, we focus on supply sourcing within the region of manufacture to allow for improved supply chain efficiencies. Some of our products rely on a single or limited number of suppliers; however, we believe that our portfolio of suppliers has adequate resources and facilities to overcome most unforeseen interruptions of supply. In the past, we have been able to obtain an adequate supply of essential raw materials and currently believe we have adequate sources of supply for virtually all components of our products.

We are continually benchmarking the performance of our supply chain and will change suppliers and adjust our distribution networks and manufacturing footprint based upon the changing needs of the business. As we integrate acquired brands, we continually seek new ways to leverage our production and sourcing capabilities to improve our overall supply chain performance.

Competition

There is significant competition within each market where our skin care, makeup, fragrance and hair care products are sold. Brand recognition, product quality and effectiveness, distribution channels, accessibility, and price point are some of the factors that impact consumers’ choices among competing products and brands. Marketing (including social media activities), merchandising, in-store experiences and demonstrations, and new product innovations also have an impact on consumers’ purchasing decisions. With our portfolio of diverse brands sold in a variety of channels we are one of the world’s leading manufacturers and marketers of skin care, makeup, fragrance and hair care products. We compete against a number of companies, some of which have substantially greater resources than we do.

Some of our competitors are large, well-known, multinational manufacturers and marketers of skin care, makeup, fragrance and hair care products, most of which market and sell their products under multiple brand names. They include L’Oreal S.A.; Shiseido Company, Ltd.; LVMH Moët Hennessey Louis Vuitton; Coty, Inc.; The Procter & Gamble Company; Chanel S.A.; Groupe Clarins; Amorepacific; and Unilever. We also face competition from a number of independent brands, some of which are backed by private-equity investors, as well as some retailers that have their own beauty brands. Certain of our competitors also have ownership interests in retailers that are customers of ours.

Trademarks, Patents and Copyrights

We own the trademark rights used in connection with the manufacturing, marketing, distribution and sale of our products both in the United States and in the other principal countries where such products are sold, including Estée Lauder, Clinique, Aramis, Prescriptives, Lab Series, Origins, MžAžC, Bobbi Brown, La Mer, Aveda, Jo Malone London, Bumble and bumble, Darphin, GoodSkin Labs, Ojon, Smashbox, Osiao, Le Labo, RODIN olio lusso, Editions de Parfums Frédéric Malle, GLAMGLOW, By Kilian, BECCA and Too Faced and the names of many of the products sold under these brands. We are the exclusive worldwide licensee for fragrances, cosmetics and/or related products for Tommy Hilfiger, Donna Karan New York, DKNY, Kiton, Michael Kors, Tom Ford, Dr. Andrew Weil, Ermenegildo Zegna, AERIN and Tory Burch. For further discussion on license arrangements, including their duration, see Item 8. Financial Statements and Supplementary Data – Note 2 – Summary of Significant Accounting Policies – License Arrangements. We protect our trademarks in the United States and significant markets worldwide. We consider the protection of our trademarks to be important to our business.

A number of our products incorporate patented, patent-pending or proprietary technology. In addition, several products and packaging for such products are covered by design patents or copyrights. While we consider these patents and copyrights, and the protection thereof, to be important, no single patent or copyright, or group of patents or copyrights, is considered material to the conduct of our business.

Employees

At June 30, 2017, we had approximately 46,000 full-time employees worldwide (including demonstrators at points of sale who are employed by us). We have no employees in the United States that are covered by a collective bargaining agreement. A limited number of employees outside of the United States are covered by a works council agreement or other syndicate arrangements.

Government Regulation

We and our products are subject to regulation by the Food and Drug Administration and the Federal Trade Commission in the United States, as well as by various other federal, state, local and international regulatory authorities and the regulatory authorities in the countries in which our products are produced or sold. Such regulations principally relate to the ingredients, manufacturing, labeling, packaging, marketing, advertising, shipment, disposal and safety of our products. We believe that we are in substantial compliance with such regulations, as well as with applicable federal, state, local and international and other countries’ rules and regulations governing the discharge of materials hazardous to the environment or that relate to climate change. There are no significant capital expenditures for environmental control or climate change matters either planned in the current year or expected in the near future.

Seasonality

Our results of operations in total, by region and by product category, are subject to seasonal fluctuations, with net sales in the first half of the fiscal year typically being slightly higher than in the second half of the fiscal year. The higher net sales in the first half of the fiscal year are attributable to the increased levels of purchasing by retailers for the holiday selling season. Fluctuations in net sales and operating income in total and by geographic region and product category in any fiscal quarter may be attributable to the level and scope of new product introductions or the particular retail calendars followed by our customers that are retailers, which may impact their order placement and receipt of goods. Additionally, gross margins and operating expenses are impacted on a quarter-by-quarter basis by variations in our launch calendar and the timing of promotions, including purchase with purchase and gift with purchase promotions.

Availability of Reports

We make available financial information, news releases and other information on our website at www.elcompanies.com. Our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and other reports, as well as any amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, are available free of charge via the EDGAR database at www.sec.gov or our website, as soon as reasonably practicable after we file such reports and amendments with, or furnish them to, the Securities and Exchange Commission. Stockholders may also contact Investor Relations at 767 Fifth Avenue, New York, New York 10153 or call 800-308-2334 to obtain a hard copy of these reports without charge.

Corporate Governance Guidelines and Code of Conduct

The Board of Directors has developed corporate governance practices to help it fulfill its responsibilities to stockholders in providing general direction and oversight of management. These practices are set forth in our Corporate Governance Guidelines. We also have a Code of Conduct (“Code”) applicable to all employees, officers and directors of the Company, including the Chief Executive Officer, the Chief Financial Officer and other senior financial officers. These documents and any waiver of a provision of the Code granted to any senior officer or director or any material amendment to the Code, may be found in the “Investors” section of our website: www.elcompanies.com under the heading “Corporate Governance.” The charters for the Audit Committee, Compensation Committee and Nominating and Board Affairs Committee may be found in the same location on our website. Stockholders may also contact Investor Relations at 767 Fifth Avenue, New York, New York 10153 or call 800-308-2334 to obtain a hard copy of these documents without charge.

Executive Officers

The following table sets forth certain information with respect to our executive officers:

|

Name |

|

Age |

|

Position(s) Held |

|

John Demsey |

|

61 |

|

Executive Group President |

|

Fabrizio Freda |

|

59 |

|

President, Chief Executive Officer and a Director |

|

Carl Haney |

|

54 |

|

Executive Vice President, Global Research and Development, Corporate Product Innovation, Package Development |

|

Leonard A. Lauder |

|

84 |

|

Chairman Emeritus and a Director |

|

Ronald S. Lauder |

|

73 |

|

Chairman of Clinique Laboratories, LLC and a Director |

|

William P. Lauder |

|

57 |

|

Executive Chairman and a Director |

|

Sara E. Moss |

|

70 |

|

Executive Vice President and General Counsel |

|

Michael O’Hare |

|

49 |

|

Executive Vice President – Global Human Resources |

|

Gregory F. Polcer |

|

62 |

|

Executive Vice President – Global Supply Chain |

|

Cedric Prouvé |

|

57 |

|

Group President – International |

|

Tracey T. Travis |

|

55 |

|

Executive Vice President and Chief Financial Officer |

|

Alexandra C. Trower |

|

52 |

|

Executive Vice President – Global Communications |

John Demsey is Executive Group President. In this role, he is responsible for numerous brands, including Clinique, Aramis, Prescriptives, M·A·C, Jo Malone London, Smashbox, Tom Ford, RODIN olio lusso, Le Labo, Editions de Parfums Frédéric Malle, GLAMGLOW, By Kilian, and Too Faced. Mr. Demsey served as Group President from July 2006 to January 2016, and was appointed Executive Group President in January 2016. He became Global Brand President of Estée Lauder in January 2005 after serving as President and Managing Director of M∙A∙C since 1998. From 1991 to 1998, Mr. Demsey held several positions with Estée Lauder, including Senior Vice President of Sales and Education for Estée Lauder USA and Canada. Before joining us, he worked in sales and marketing for Revlon, Borghese, Alexandra de Markoff Cosmetics, and Lancaster Cosmetics. Mr. Demsey also held various executive retail positions at Bloomingdale’s, Macy’s, Benetton and Saks Fifth Avenue. He serves as Chairman of the M∙A∙C AIDS Fund and is on the Board of Directors of Baccarat S.A.

Fabrizio Freda has been President and Chief Executive Officer of the Company since July 2009. From March 2008 through June 2009, he was President and Chief Operating Officer of the Company where he oversaw the Clinique, Bobbi Brown, La Mer, Jo Malone London, Aveda and Bumble and bumble brands and the Aramis and Designer Fragrances division. He also was responsible for the Company’s International Division, as well as Global Operations, Research and Development, Packaging, Quality Assurance, Merchandise Design, Corporate Store Design and Retail Store Operations. Prior to joining the Company, Mr. Freda served in a number of positions of increasing responsibility at The Procter & Gamble Company (“P&G”), where he was responsible for various operating, marketing and key strategic efforts for over 20 years. From 2001 through 2007, Mr. Freda was President, Global Snacks, at P&G. He also spent more than a decade in the Health and Beauty Care division at P&G. From 1986 to 1988 he directed marketing and strategic planning for Gucci SpA. Mr. Freda is currently a member of the Board of Directors of BlackRock, Inc., a global asset management company.

Carl Haney is Executive Vice President, Global Research and Development, Corporate Product Innovation, Package Development. Prior to joining the Company in 2012, Mr. Haney was Vice President, R&D Global, Male Grooming, Gillette, Braun and Devices, leading teams in all aspects of innovation, including product, packaging, process development and engineering at The Procter & Gamble Company (“P&G”) from 2007 through May 2012. Mr. Haney started his career at P&G in 1984, and over the years held numerous leadership positions in locations around the world. In 1997, he was promoted to Director, Latin America Beauty Care R&D. Mr. Haney also held R&D leadership roles for P&G Global Cosmetics and Oral Care and led P&G innovation teams in Latin America, Europe and Asia.

Leonard A. Lauder is Chairman Emeritus and a member of the Board of Directors. He was Chairman of the Board of Directors from 1995 through June 2009 and served as our Chief Executive Officer from 1982 through 1999 and President from 1972 until 1995. Mr. Lauder has held various positions since formally joining the Company in 1958 after serving as an officer in the United States Navy. He is Chairman Emeritus of the Board of Trustees of the Whitney Museum of American Art, a Charter Trustee of The University of Pennsylvania, a Trustee of The Aspen Institute and the co-founder and Co-Chairman of the Alzheimer’s Drug Discovery Foundation. Mr. Lauder is Honorary Chairman of the Breast Cancer Research Foundation. He also served as a member of the White House Advisory Committee on Trade Policy and Negotiations under President Reagan.

Ronald S. Lauder has served as Chairman of Clinique Laboratories, LLC since returning from government service in 1987 and was Chairman of Estee Lauder International, Inc. from 1987 through 2002. He joined the Company in 1964 and has served in various capacities. Mr. Lauder was elected as a member of the Board of Directors of the Company in 2016; previously he was a member of the Board of Directors of the Company from 1968 to 1986 and again from 1988 to July 2009. From 1983 to 1986, he served as Deputy Assistant Secretary of Defense for European and NATO Affairs. From 1986 to 1987, he was U.S. Ambassador to Austria. Mr. Lauder is an Honorary Chairman of the Board of Trustees of the Museum of Modern Art and President of the Neue Galerie. He is also Chairman of the Board of Governors of the Joseph H. Lauder Institute of Management and International Studies at the Wharton School at the University of Pennsylvania and the co-founder and Co-Chairman of the Alzheimer’s Drug Discovery Foundation.

William P. Lauder is Executive Chairman and, in such role, he is Chairman of the Board of Directors. He was Chief Executive Officer of the Company from March 2008 through June 2009 and President and Chief Executive Officer from July 2004 through February 2008. From January 2003 through June 2004, he was Chief Operating Officer. From July 2001 through 2002, he was Group President responsible for the worldwide business of the Clinique and Origins brands and the Company’s retail store and online operations. From 1998 to 2001, he was President of Clinique Laboratories, LLC. Prior to 1998, he was President of Origins Natural Resources Inc., and he had been the senior officer of that division since its inception in 1990. Prior thereto, he served in various positions since joining the Company in 1986. Mr. Lauder currently serves as Chairman of the Board of the Fresh Air Fund, a member of the boards of trustees of The University of Pennsylvania and The Trinity School in New York City, a member of the boards of directors of the 92nd Street Y and the Partnership for New York City, and is on the Advisory Board of Zelnick Media. He is also Co-Chairman of the Breast Cancer Research Foundation.

Sara E. Moss is Executive Vice President and General Counsel. She joined us as Senior Vice President, General Counsel and Secretary in September 2003 and became Executive Vice President in November 2004. She was Senior Vice President and General Counsel of Pitney Bowes Inc. from 1996 to February 2003, and Senior Litigation Partner for Howard, Smith & Levin (now Covington & Burling) in New York from 1984 to 1996. Prior to 1984, Ms. Moss served as an Assistant United States Attorney in the Criminal Division in the Southern District of New York, was an associate at the law firm of Davis, Polk & Wardwell and was Law Clerk to the Honorable Constance Baker Motley, U.S. District Judge in the Southern District of New York.

Michael O’Hare is Executive Vice President - Global Human Resources. Prior to joining the Company in 2013, he was with Heineken N.V., a global brewer based in the Netherlands, where he served since 2009 as Global Chief Human Resources Officer. Prior to that, Mr. O’Hare spent 13 years at PepsiCo, a global food and beverage company, where he held a variety of senior roles in Human Resources, including Chief Personnel Officer/Vice President for Asia Pacific.

Gregory F. Polcer is Executive Vice President - Global Supply Chain. He is responsible for Global Direct and Indirect Procurement, Manufacturing, Logistics, Quality Assurance and Environmental Affairs and Safety. From 1988 to 2008, when he joined the Company, Mr. Polcer worked for Unilever where he designed and implemented global, regional and local initiatives. From 2006 to 2008, he served as the Senior Vice President, Supply Chain for Unilever where he integrated the North and Latin American Supply Chains, provided senior leadership for all global supply management and established a global outsourcing plan. Mr. Polcer served as Senior Vice President, Supply Chain - North America from 2005 to 2006 and Senior Vice President, Supply Chain, Home and Personal Care – North America from 2002 to 2004.

Cedric Prouvé is Group President – International. He is responsible for our International Division, which includes all markets outside of the United States and Canada, our Travel Retail business worldwide and all of the activities of our sales affiliates and distributor relationships. He became Group President – International in January 2003. From August 2000 through December 2002, he was the General Manager of our Japanese sales affiliate. From January 1997 to August 2000, he was Vice President, General Manager, Travel Retail. Mr. Prouvé started with us in 1994 as General Manager, Travel Retailing - Asia Pacific Region and was given the added responsibility of General Manager of our Singapore affiliate in 1995. Previously, he worked at L’Oreal in sales and management positions in the Americas and Asia/Pacific.

Tracey T. Travis is Executive Vice President and Chief Financial Officer. Prior to joining the Company in 2012, she was Senior Vice President and Chief Financial Officer of Ralph Lauren Corporation since 2005, responsible for Global Finance, Internal Audit, Treasury, Tax, Business Development, Investor Relations and Global Information Technology. Previously, Ms. Travis was Senior Vice President, Finance of Intimate Brands for Limited Brands, Inc. from 2002 to 2004. She also spent a decade at PepsiCo Inc. and the Pepsi Bottling Group, where she held operations management and finance roles. She began her career as an engineer and financial analyst at General Motors Company. Ms. Travis joined the Board of Directors of Accenture plc in July 2017, and she is also a member of the Board of Directors of Campbell Soup Company. In addition, she is a member of the Board of Overseers at Columbia Business School.

Alexandra C. Trower is Executive Vice President - Global Communications. She directs the Company’s overall communications strategy, overseeing brand communications, corporate communications, internal communications and philanthropic communications. Prior to joining the Company in 2008, Ms. Trower was Senior Vice President, Media Relations for Bank of America from July 2003 to March 2008. From 1997 to 2003, she worked at JPMorgan Chase, where she was responsible for corporate communications at JPMorgan Fleming Asset Management. From 1987 to 1997, Ms. Trower worked at a former division of Citibank, Chancellor Capital Management (now part of Invesco), where she held a variety of communications roles. Ms. Trower serves on the Board of Directors of Hollins University, and she is co-chair of The International Women’s Media Foundation.

Each executive officer serves for a one-year term ending at the next annual election of officers, subject to his or her applicable employment agreement and his or her earlier death, resignation or removal.

There are risks associated with an investment in our securities. Please consider the following risks and all of the other information in this annual report on Form 10-K and in our subsequent filings with the Securities and Exchange Commission (“SEC”). Our business may also be adversely affected by risks and uncertainties not presently known to us or that we currently believe to be immaterial. If any of the events contemplated by the following discussion of risks should occur or other risks arise or develop, our business, prospects, financial condition and results of operations, as well as the trading prices of our securities, may be adversely affected.

The beauty business is highly competitive, and if we are unable to compete effectively our results will suffer.

We face vigorous competition from companies throughout the world, including multinational consumer product companies. Some of these competitors have greater resources than we do and others are newer companies (some backed by private-equity investors) competing in distribution channels where we are less represented. In some cases, our competitors may be able to respond to changing business and economic conditions more quickly than us. Competition in the beauty business is based on a variety of factors including pricing of products, innovation, perceived value, service to the consumer, promotional activities, advertising, special events, new product introductions, e-commerce and m-commerce initiatives and other activities. It is difficult for us to predict the timing and scale of our competitors’ actions in these areas.

Our ability to compete also depends on the continued strength of our brands, our ability to attract and retain key talent and other personnel, the efficiency of our manufacturing facilities and distribution network, and our ability to maintain and protect our intellectual property and those other rights used in our business. Our Company has a well-recognized and strong reputation that could be negatively impacted by many factors. If our reputation is adversely affected, our ability to attract and retain customers and consumers could be impacted. In addition, certain of our key retailers around the world market and sell competing brands or are owned or otherwise affiliated with companies that market and sell competing brands. Our inability to continue to compete effectively in key countries around the world could have an adverse impact on our business.

Our inability to anticipate and respond to market trends and changes in consumer preferences could adversely affect our financial results.

Our continued success depends on our ability to anticipate, gauge and react in a timely and cost-effective manner to changes in consumer tastes for skin care, makeup, fragrance and hair care products, attitudes toward our industry and brands, as well as to where and how consumers shop. We must continually work to develop, manufacture and market new products, maintain and adapt our “High-Touch” services to existing and emerging distribution channels, maintain and enhance the recognition of our brands, achieve a favorable mix of products, successfully manage our inventories, and refine our approach as to how and where we market and sell our products. While we devote considerable effort and resources to shape, analyze and respond to consumer preferences, we recognize that consumer tastes cannot be predicted with certainty and can change rapidly. The issue is compounded by the increasing use of digital and social media by consumers and the speed by which information and opinions are shared. If we are unable to anticipate and respond to sudden challenges that we may face in the marketplace, trends in the market for our products and changing consumer demands and sentiment, our financial results will suffer. In addition, from time to time, sales growth or profitability may be concentrated in a relatively small number of our brands, channels or countries. If such a situation persists or a number of brands, channels or countries fail to perform as expected, there could be a material adverse effect on our business, financial condition and results of operations.

In key markets, such as the United States, we have seen a decline in retail traffic in our department store customers and certain of our freestanding stores. We are seeing the emergence of strong e- and m-commerce platforms (both in mass and prestige distribution) that are impacting our business. Further consolidation in the retail trade, from these or other factors, may result in us becoming increasingly dependent on key retailers. This could result in an increased risk related to the concentration of our customers. A severe, adverse impact on the business operations of our customers could have a corresponding material adverse effect on us. If one or more of our largest customers change their strategies (including pricing or promotional activities) or they or we change or terminate their relationship with us, there could be a material adverse effect on our business.

Our future success depends on our ability to achieve our long-term strategy.

Achieving our long-term strategy will require investment in new capabilities, brands, categories, distribution channels, technologies and emerging and more mature geographic markets. These investments may result in short-term costs without any current revenues and, therefore, may be dilutive to our earnings, at least in the short term. In addition, we may dispose of or discontinue select brands or streamline operations and incur costs or restructuring and other charges in doing so. Although we believe that our strategy will lead to long-term growth in revenue and profitability, we may not realize, in full or in part, the anticipated benefits. The failure to realize benefits, which may be due to our inability to execute plans, global or local economic conditions, competition, changes in the beauty industry and the other risks described herein, could have a material adverse effect on our business, financial condition and results of operations.

Acquisitions may expose us to additional risks.

We continuously review acquisition and strategic investment opportunities that would expand our current product offerings, our distribution channels, increase the size and geographic scope of our operations or otherwise offer growth and operating efficiency opportunities. There can be no assurance that we will be able to identify suitable candidates or consummate these transactions on favorable terms. If required, the financing for these transactions could result in an increase in our indebtedness, dilute the interests of our stockholders or both. The purchase price for some acquisitions may include additional amounts to be paid in cash in the future, a portion of which may be contingent on the achievement of certain future operating results of the acquired business. If the performance of any such acquired business exceeds such operating results, then we may incur additional charges and be required to pay additional amounts.

Acquisitions including strategic investments or alliances entail numerous risks, which may include:

· difficulties in integrating acquired operations or products, including the loss of key employees from, or customers of, acquired businesses;

· diversion of management’s attention from our existing businesses;

· adverse effects on existing business relationships with suppliers and customers;

· adverse impacts of margin and product cost structures different from those of our current mix of business; and

· risks of entering distribution channels, categories or markets in which we have limited or no prior experience.

Our failure to successfully complete the integration of any acquired business or to achieve the long-term plan for such business, as well as any other adverse consequences associated with our acquisition and investment activities, could have a material adverse effect on our business, financial condition and operating results.

Completed acquisitions typically result in additional goodwill and/or an increase in other intangible assets on our balance sheet. We are required at least annually, or as facts and circumstances exist, to test goodwill and other intangible assets with indefinite lives to determine if impairment has occurred. If the testing performed indicates that impairment has occurred, we are required to record a non-cash impairment charge for the difference between the carrying value of the goodwill or other intangible assets with indefinite lives and the implied fair value of the goodwill or the fair value of other intangible assets with indefinite lives in the period the determination is made. We cannot accurately predict the amount and timing of any impairment of assets. Should the value of goodwill or other intangible assets become impaired, there could be a material adverse effect on our financial condition and results of operations.

A general economic downturn, or sudden disruption in business conditions may affect consumer purchases of discretionary items and/or the financial strength of our customers that are retailers, which could adversely affect our financial results.

The general level of consumer spending is affected by a number of factors, including general economic conditions, inflation, interest rates, energy costs, and consumer confidence generally, all of which are beyond our control. Consumer purchases of discretionary items tend to decline during recessionary periods, when disposable income is lower, and may impact sales of our products. A decline in consumer purchases of discretionary items also tends to impact our customers that are retailers. We generally extend credit to a retailer based on an evaluation of its financial condition, usually without requiring collateral. However, the financial difficulties of a retailer could cause us to curtail or eliminate business with that customer. We may also assume more credit risk relating to the receivables from that retailer. Our inability to collect receivables from our largest customers or from a group of customers could have a material adverse effect on our business and our financial condition. If a retailer was to liquidate, we may incur additional costs if we choose to purchase the retailer’s inventory of our products to protect brand equity.

In addition, sudden disruptions in business conditions, for example, from events such as a pandemic, or other local or global health issues, conflicts around the world, or as a result of a terrorist attack, retaliation or similar threats, or as a result of adverse weather conditions, climate changes or seismic events, can have a short-term and, sometimes, long-term impact on consumer spending.

Events that impact consumers’ willingness or ability to travel and/or purchase our products while traveling may impact our business, including travel retail, a significant contributor to our overall results, and our strategy to market and sell products to international travelers at their destinations.

A downturn in the economies of, or continuing recessions in, the countries where we sell our products or a sudden disruption of business conditions in those countries could adversely affect consumer confidence, the financial strength of our retailers and our sales and profitability. We are cautious of the continued decline in retail traffic primarily related to brick-and-mortar department stores in the United States as a result of the impact of shifts in consumer preferences as to where and how they shop. We are also cautious of foreign currency movements and their impact on tourism, which has particularly impacted certain tourist-driven stores in the United States. Additionally, we continue to monitor the effects of the macroeconomic environments in certain countries such as Brazil and in the Middle East, the United Kingdom’s anticipated exit from the European Union, geopolitical tensions and global security issues.

Volatility in the financial markets and a related economic downturn in key markets or markets generally throughout the world could have a material adverse effect on our business. While we currently generate significant cash flows from our ongoing operations and have access to global credit markets through our various financing activities, credit markets may experience significant disruptions. Deterioration in global financial markets or an adverse change in our credit ratings could make future financing difficult or more expensive. If any financial institutions that are parties to our undrawn revolving credit facility or other financing arrangements, such as foreign exchange or interest rate hedging instruments, were to declare bankruptcy or become insolvent, they may be unable to perform under their agreements with us. This could leave us with reduced borrowing capacity or unhedged against certain foreign currency or interest rate exposures which could have an adverse impact on our financial condition and results of operations.

Changes in laws, regulations and policies that affect our business could adversely affect our financial results.

Our business is subject to numerous laws, regulations and policies. Changes in the laws, regulations and policies, including the interpretation or enforcement thereof, that affect, or will affect, our business, including changes in accounting standards, tax laws and regulations, laws and regulations relating to data privacy, anti-corruption, advertising, marketing, manufacturing, distribution, product registration, ingredients, chemicals and packaging, laws in Europe and elsewhere relating to selective distribution, environmental or climate change laws, regulations or accords, trade rules and customs regulations, and the outcome and expense of legal or regulatory proceedings, and any action we may take as a result could adversely affect our financial results.

We are involved, and may become involved in the future, in disputes and other legal or regulatory proceedings that, if adversely decided or settled, could adversely affect our financial results.

We are, and may in the future become, party to litigation, other disputes or regulatory proceedings. In general, claims made by us or against us in litigation, disputes or other proceedings can be expensive and time consuming to bring or defend against and could result in settlements, injunctions or damages that could significantly affect our business or financial results. We are currently vigorously contesting certain of these claims. However, it is not possible to predict the final resolution of the litigation, disputes or proceedings to which we currently are or may in the future become party to, and the impact of certain of these matters on our business, results of operations and financial condition could be material.

Government reviews, inquiries, investigations, and actions could harm our business or reputation.

As we operate in various locations around the world, our operations in certain countries are subject to significant governmental scrutiny and may be adversely impacted by the results of such scrutiny. The regulatory environment with regard to our business is evolving, and officials often exercise broad discretion in deciding how to interpret and apply applicable regulations. From time to time, we may receive formal and informal inquiries from various government regulatory authorities, as well as self-regulatory organizations, about our business and compliance with local laws, regulations or standards. Any determination that our operations or activities, or the activities of our employees, are not in compliance with existing laws, regulations or standards could negatively impact us in a number of ways, including the imposition of substantial fines, interruptions of business, loss of supplier, vendor or other third-party relationships, termination of necessary licenses and permits, or similar results, all of which could potentially harm our business and/or reputation. Even if an inquiry does not result in these types of determinations, it potentially could create negative publicity which could harm our business and/or reputation.

Our success depends, in part, on the quality, efficacy and safety of our products.

Our success depends, in part, on the quality, efficacy and safety of our products. If our products are found to be defective or unsafe, our product claims are found to be deceptive, or our products otherwise fail to meet our consumers’ expectations, our relationships with customers or consumers could suffer, the appeal of one or more of our brands could be diminished, and we could lose sales and/or become subject to liability or claims, any of which could result in a material adverse effect on our business, results of operations and financial condition. In addition, third parties may sell counterfeit versions of some of our products. These counterfeit products may pose safety risks, may fail to meet consumers’ expectations, and may have a negative impact on our reputation.

Our success depends, in part, on our key personnel.

Our success depends, in part, on our ability to retain our key personnel, including our executive officers and senior management team. The unexpected loss of one or more of our key employees could adversely affect our business. Our success also depends, in part, on our continuing ability to identify, hire, train and retain other highly qualified personnel. Competition for these employees can be intense. We may not be able to attract, assimilate or retain qualified personnel in the future, and our failure to do so could adversely affect our business. This risk may be exacerbated by the stresses associated with the implementation of our strategic plan and other initiatives.

We are subject to risks related to the global scope of our operations.

We operate on a global basis, with a majority of our fiscal 2017 net sales and operating income generated outside the United States. We intend to reinvest these earnings in our foreign operations indefinitely, except where we are able to repatriate these earnings to the United States without material incremental tax provision. A majority of our cash and cash equivalents that result from these earnings remain outside the United States. If these indefinitely reinvested earnings were repatriated into the United States as dividends, we would be subject to additional taxes.

We maintain offices in over 50 countries and have key operational facilities located inside and outside the United States that manufacture, warehouse or distribute goods for sale throughout the world. Our global operations are subject to many risks and uncertainties, including:

· fluctuations in foreign currency exchange rates and the relative costs of operating in different places, which can affect our results of operations, the value of our foreign assets, the relative prices at which we and competitors sell products in the same markets, the cost of certain inventory and non-inventory items required in our operations, and the relative prices at which we sell our products in different markets;

· foreign or U.S. laws, regulations and policies, including restrictions on trade, immigration and travel; import and export license requirements; tariffs and taxes; operations; and investments;

· lack of well-established or reliable legal and administrative systems in certain countries in which we operate; and

· adverse weather conditions, currency exchange controls, and social, economic and geopolitical conditions, such as terrorist attacks, war or other military action.

These risks could have a material adverse effect on our business, prospects, reputation, results of operations and financial condition.

A disruption in operations or our supply chain could adversely affect our business and financial results.

As a company engaged in manufacturing and distribution on a global scale, we are subject to the risks inherent in such activities, including industrial accidents, environmental events, strikes and other labor disputes, disruptions in supply chain or information systems, loss or impairment of key manufacturing sites or suppliers, product quality control, safety, increase in commodity prices and energy costs, licensing requirements and other regulatory issues, as well as natural disasters and other external factors over which we have no control. If such an event were to occur, it could have an adverse effect on our business and financial results.

We use a wide variety of direct and indirect suppliers of goods and services from around the world. Some of our products rely on single or a limited number of suppliers. Changes in the financial or business condition of our suppliers could subject us to losses or adversely affect our ability to bring products to market. Further, the failure of our suppliers to deliver goods and services in sufficient quantities, in compliance with applicable standards, and in a timely manner could adversely affect our customer service levels and overall business. In addition, any increases in the costs of goods and services for our business may adversely affect our profit margins if we are unable to pass along any higher costs in the form of price increases or otherwise achieve cost efficiencies in our operations.

Our information systems and websites may be susceptible to cybersecurity breaches, outages, and other risks.

We rely on information systems (outsourced and in-house) that support our business processes, including product development, marketing, sales, order processing, production, distribution, finance and intracompany communications throughout the world. We have e-commerce, m-commerce and other Internet websites in the United States and many other countries. These systems may be susceptible to outages due to fire, floods, power loss, telecommunications failures, break-ins and other events. Despite the implementation of network security measures, our systems may be vulnerable to cybersecurity breaches such as computer viruses, break-ins and similar disruptions from unauthorized tampering. The occurrence of these or other events could disrupt or damage our information systems and adversely affect our business and results of operations.

Failure to adequately maintain the security of our electronic and other confidential information could materially adversely affect our financial condition and results of operations.

We are dependent upon automated information technology processes. As part of our normal business activities, we collect and store certain information that is confidential, proprietary or otherwise sensitive, including personal information with respect to customers, consumers and employees. We may share some of this information with vendors who assist us with certain aspects of our business. Moreover, the success of our e-commerce and m-commerce operations depends upon the secure transmission of confidential and personal data over public networks, including the use of cashless payments. Any failure on the part of us or our vendors to maintain the security of our confidential data and personal information, including via the penetration of our network security and the misappropriation of confidential and personal information, could result in business disruption, damage to our reputation, financial obligations to third parties, fines, penalties, regulatory proceedings and private litigation with potentially large costs, and also result in deterioration in our employees’, consumers’ and customers’ confidence in us and other competitive disadvantages, and thus could have a material adverse impact on our business, financial condition and results of operations. In addition, a security breach could require that we expend significant additional resources to enhance our information security systems and could result in a disruption to our operations.

We are subject to risks associated with our global information systems.

Our implementation and maintenance of global information systems (outsourced and in-house), including supply chain and finance systems, human resource management systems, creative asset management and retail operating systems, as well as associated hardware and use of cloud-based models, involve risks and uncertainties. Failure to implement and maintain these and other systems as planned, in terms of timing, specifications, costs, or otherwise, could have an adverse impact on our business and results of operations.

As we outsource functions, we become more dependent on the entities performing those functions.

As part of our long-term strategy, we are continually looking for opportunities to provide essential business services in a more cost-effective manner. In some cases, this requires the outsourcing of functions or parts of functions that can be performed more effectively by external service providers. These include certain information systems, finance and human resource functions. While we believe we conduct appropriate due diligence before entering into agreements with the outsourcing entity, the failure of one or more entities to provide the expected services, provide them on a timely basis or to provide them at the prices we expect may have a material adverse effect on our results of operations or financial condition. In addition, if we transition systems to one or more new, or among existing, external service providers, we may experience challenges that could have a material adverse effect on our results of operations or financial condition.

The trading prices of our securities periodically may rise or fall based on the accuracy of predictions of our earnings or other financial performance.

Our business planning process is designed to maximize our long-term strength, growth and profitability, not to achieve an earnings target in any particular fiscal quarter. We believe that this longer-term focus is in the best interests of the Company and our stockholders. At the same time, however, we recognize that it may be helpful to provide investors with guidance as to our forecast of net sales, earnings per share and other financial metrics or projections. Accordingly, when we announced our year-end financial results for fiscal 2017, we provided guidance as to certain assumptions, including ranges for our expected net sales and earnings per share for the quarter ending September 30, 2017 and the fiscal year ending June 30, 2018. While we generally expect to provide updates to our guidance when we report our results each fiscal quarter, we assume no responsibility to update any of our forward-looking statements at such times or otherwise. In addition, the longer-term guidance we provide is based on goals that we believe, at the time guidance is given, are reasonably attainable for growth and performance over a number of years. Such targets are more difficult to predict than our current quarter and fiscal year expectations. We historically have paid dividends on our common stock and repurchased shares of our Class A Common Stock. At any time, we could stop or suspend payment of dividends or stop or suspend our stock repurchase program, and any such action could cause the market price of our stock to decline.

In all of our public statements when we make, or update, a forward-looking statement about our net sales and/or earnings expectations or expectations regarding restructuring or other initiatives, we accompany such statements directly, or by reference to a public document, with a list of factors that could cause our actual results to differ materially from those we expect. Such a list is included, among other places, in our earnings press release and in our periodic filings with the Securities and Exchange Commission (e.g., in our reports on Form 10-K and Form 10-Q). These and other factors may make it difficult for us and for outside observers, such as research analysts, to predict what our earnings will be in any given fiscal quarter or year.

Outside analysts and investors have the right to make their own predictions of our financial results for any future period. Outside analysts, however, have access to no more material information about our results or plans than any other public investor, and we do not endorse their predictions as to our future performance. Nor do we assume any responsibility to correct the predictions of outside analysts or others when they differ from our own internal expectations. If and when we announce actual results that differ from those that outside analysts or others have been predicting, the market price of our securities could be affected. Investors who rely on the predictions of outside analysts or others when making investment decisions with respect to our securities do so at their own risk. We take no responsibility for any losses suffered as a result of such changes in the prices of our securities.

We are controlled by the Lauder family. As a result of their control of us, the Lauder family has the ability to prevent or cause a change in control or approve, prevent or influence certain actions by us.

As of August 18, 2017, members of the Lauder family beneficially own, directly or indirectly, shares of the Company’s Class A Common Stock (with one vote per share) and Class B Common Stock (with 10 votes per share) having approximately 87% of the outstanding voting power of the Common Stock. In addition, there are four members of the Lauder family who are employees and members of our Board of Directors. Another family member is a party to a consulting agreement and a license agreement with us.

As a result of the stock ownership and their positions at the Company, the Lauder family has the ability to exercise significant control and influence over our business, including, all matters requiring stockholder approval, including the election of directors, amendments to the certificate of incorporation and significant corporate transactions, such as a merger or other sale of our Company or its assets, for the foreseeable future.

We are a “controlled company” within the meaning of the New York Stock Exchange rules and, as a result, are relying on exemptions from certain corporate governance requirements that are designed to provide protection to stockholders of companies that are not “controlled companies.”

The Lauder family and their related entities own more than 50% of the total voting power of our common shares and, as a result, we are a “controlled company” under the New York Stock Exchange corporate governance standards. As a controlled company, we are exempt under the New York Stock Exchange standards from the obligation to comply with certain New York Stock Exchange corporate governance requirements, including the requirements that (1) a majority of our board of directors consists of independent directors; (2) we have a nominating committee that is composed entirely of independent directors with a written charter addressing the committee’s purpose and responsibilities; and (3) we have a compensation committee that is composed entirely of independent directors with a written charter addressing the committee’s purpose and responsibilities.

While we have voluntarily caused our Board to have a majority of independent directors and the written charters of our Nominating and Board Affairs Committee and the Compensation Committee to have the required provisions, we are not requiring our Nominating and Board Affairs Committee and Compensation Committee to be comprised solely of independent directors. As a result of our use of the “controlled company” exemptions, investors will not have the same protection afforded to stockholders of companies that are subject to all of the New York Stock Exchange corporate governance requirements.

Item 1B. Unresolved Staff Comments.

As of the filing of this annual report on Form 10-K, there were no unresolved comments from the Staff of the Securities and Exchange Commission.

The following table sets forth our principal owned and leased manufacturing, assembly, research and development and distribution facilities, some of which include contiguous office space, as of August 18, 2017. The leases expire at various times through 2026 subject to certain renewal options.

|

Location |

|

|

|

Use |

|

Approximate |

|

|

|

|

|

|

|

|

|

|

|

The Americas |

|

|

|

|

|

|

|

|

Blaine, Minnesota |

|

Owned |

|

Manufacturing and R&D |

|

275,000 |

|

|

Blaine, Minnesota |

|

Leased |

|

Distribution |

|

187,000 |

|

|

Melville, New York |

|

Owned |

|

Manufacturing |

|

353,000 |

|

|

Melville, New York |

|

Owned |

|

R&D |

|

134,000 |

|

|

Bristol, Pennsylvania |

|

Leased |

|

Manufacturing |

|

67,000 |

|

|

Bristol, Pennsylvania |

|

Leased |

|

Manufacturing and Assembly |

|

100,000 |

|

|

Bristol, Pennsylvania |

|

Leased |

|

Distribution |

|

782,000 |

|

|

Trevose, Pennsylvania |

|

Leased |

|

Manufacturing and Assembly |

|

80,000 |

|

|

Agincourt, Ontario, Canada |

|

Owned |

|

Manufacturing |

|

96,000 |

|

|

Markham, Ontario, Canada |

|

Leased |

|

Manufacturing |

|

137,000 |

|

|

Markham, Ontario, Canada |

|

Leased |

|

R&D |

|

42,000 |

|

|

Toronto, Ontario, Canada |

|

Leased |

|

Distribution |

|

186,000 |

|

|

|

|

|

|

|