EVIO, INC. - Quarter Report: 2016 December (Form 10-Q)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended December 31, 2016

or

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ___________________ to ___________________ .

Commission File Number:000-12350

|

SIGNAL BAY, INC. |

|

(Exact name of registrant as specified in its charter) |

|

Colorado |

|

47-1890509 |

|

(State of Incorporation) |

|

(I.R.S. Employer Identification No.) |

|

| ||

|

62930 O. B. Riley Rd, Suite 300, Bend, OR |

|

97703 |

|

(Address of principal executive offices) |

|

(Zip Code) |

(541) 633-4568

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer |

¨ |

Non-accelerated filer |

¨ |

|

Accelerated filer |

¨ |

Smaller reporting company |

x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

|

Title of Each Class |

|

Outstanding as of April 19, 2017 |

|

Common stock, par value $0.0001 per share |

|

952,467,800 |

|

Class A Preferred Stock, par value $0.0001 per share |

|

0 |

|

Class B Preferred Stock, par value $0.0001 per share |

|

5,000,000 |

|

Class C Preferred Stock, par value $0.0001 per share |

|

500,000 |

|

Class D Preferred Stock, par value $0.0001 per share |

|

832,500 |

FORM 10-Q

December 31, 2016

TABLE OF CONTENTS

|

| |||||

|

|

3 |

| |||

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

24 |

| ||

|

|

30 |

| |||

|

|

30 |

||||

|

| |||||

|

| |||||

|

|

33 |

| |||

|

|

33 |

| |||

|

|

33 |

| |||

|

|

33 |

| |||

|

|

33 |

| |||

|

|

33 |

| |||

|

|

34 |

||||

| 2 |

PART I -- FINANCIAL INFORMATION

|

SIGNAL BAY, INC. | ||||||||

|

UNAUDITED CONSOLIDATED BALANCE SHEETS | ||||||||

|

|

|

|

|

|

| |||

|

|

|

December 31, 2016 |

|

|

September 30, 2016 |

| ||

|

ASSETS | ||||||||

|

|

|

|

|

|

|

| ||

|

Current assets |

|

|

|

|

|

| ||

|

Cash |

|

$ | 151,883 |

|

|

$ | 57,486 |

|

|

Accounts receivable |

|

|

241,521 |

|

|

|

9,483 |

|

|

Prepaid expenses |

|

|

12,176 |

|

|

|

- |

|

|

Other current asset |

|

|

- |

|

|

|

40,000 |

|

|

Note receivable |

|

|

- |

|

|

|

25,000 |

|

|

Total current assets |

|

|

405,580 |

|

|

|

131,969 |

|

|

|

|

|

|

|

|

|

|

|

|

Fixed assets, net of accumulated depreciation of $96,523 and $68,610, respectively |

|

|

409,974 |

|

|

|

205,842 |

|

|

Security deposits |

|

|

9,271 |

|

|

|

6,476 |

|

|

Intangible assets, net of accumulated amortization of $74,243 and $49,319 |

|

|

638,658 |

|

|

|

426,301 |

|

|

Goodwill |

|

|

2,415,057 |

|

|

|

1,415,408 |

|

|

|

|

|

|

|

|

|

|

|

|

Total assets |

|

$ | 3,878,540 |

|

|

$ | 2,185,996 |

|

|

|

|

|

|

|

|

|

|

|

|

LIABILITIES AND STOCKHOLDERS' EQUITY (DEFICIT) | ||||||||

|

|

|

|

|

|

|

|

|

|

|

Current liabilities |

|

|

|

|

|

|

|

|

|

Accounts payable and accrued liabilities |

|

$ | 518,427 |

|

|

$ | 223,316 |

|

|

Client deposits |

|

|

151,049 |

|

|

|

22,500 |

|

|

Interest payable |

|

|

41,610 |

|

|

|

27,197 |

|

|

Capital lease obligation, current |

|

|

29,510 |

|

|

|

- |

|

|

Derivative liability |

|

|

190,280 |

|

|

|

775,246 |

|

|

Convertible notes payable, net of discounts of $33,130 and $121,496, respectively |

|

|

120,171 |

|

|

|

257,605 |

|

|

Loan payable, current |

|

|

45,688 |

|

|

|

77,375 |

|

|

Loans payable, related party, current |

|

|

368,376 |

|

|

|

333,007 |

|

|

Total current liabilities |

|

|

1,465,111 |

|

|

|

1,716,246 |

|

|

|

|

|

|

|

|

|

|

|

|

Capital lease obligation, net of current portion |

|

|

75,610 |

|

|

|

- |

|

|

Loans payable, related party, net of current portion |

|

|

1,408,412 |

|

|

|

876,751 |

|

|

Total liabilities |

|

|

2,949,133 |

|

|

|

2,592,997 |

|

|

|

|

|

|

|

|

|

|

|

|

Stockholders' equity (deficit) |

|

|

|

|

|

|

|

|

|

Series A Convertible Preferred Stock, Par Value $0.0001; 1,840,000 authorized; 0 and 1,840,000 shares issued and outstanding at December 31, 2016 and September 30, 2016, respectively |

|

|

- |

|

|

|

184 |

|

|

Series B Convertible Preferred Stock, Par Value $0.0001; 5,000,000 authorized; 5,000,000 shares issued and outstanding at December 31, 2016 and September 30, 2016, respectively |

|

|

500 |

|

|

|

500 |

|

|

Series C Convertible Preferred Stock, Par Value $0.0001; 500,000 authorized; 500,000 shares issued and outstanding at December 31, 2016 and September 30, 2016, respectively |

|

|

50 |

|

|

|

50 |

|

|

Series D Convertible Preferred Stock, Par Value $.0001; 1,000,000 authorized; 832,500 and 48,000 shares issued and outstanding at December 31, 2016 and September 30, 2016, respectively |

|

|

83 |

|

|

|

5 |

|

|

Common Stock, Par Value $.0001, 3,000,000,000 authorized; 946,192,800 and 850,064,268 issued and outstanding at December 31, 2016 and September 30, 2016, respectively |

|

|

94,619 |

|

|

|

85,006 |

|

|

Additional Paid in Capital |

|

|

5,499,334 |

|

|

|

3,351,452 |

|

|

Accumulated Deficit |

|

|

(4,857,894 | ) |

|

|

(4,032,177 | ) |

|

Total stockholders' equity (deficit) |

|

|

736,692 |

|

|

|

(594,980 | ) |

|

Non-controlling interest |

|

|

192,715 |

|

|

|

187,979 |

|

|

Total equity (deficit) |

|

|

929,407 |

|

|

|

(407,001 | ) |

|

|

|

|

|

|

|

|

|

|

|

Total liabilities and stockholders' equity (deficit) |

|

$ | 3,878,540 |

|

|

$ | 2,185,996 |

|

The accompanying notes are an integral part of these unaudited consolidated financial statements.

| 3 |

| Table of Contents |

|

SIGNAL BAY, INC. | ||||||||

|

UNAUDITED CONSOLIDATED STATEMENTS OF OPERATIONS | ||||||||

|

|

|

|

|

| ||||

|

|

|

Three months ended December 31, |

| |||||

|

Revenues |

|

2016 |

|

|

2015 |

| ||

|

Testing services |

|

$ | 568,578 |

|

|

$ | 39,638 |

|

|

Consulting services |

|

|

99,878 |

|

|

|

131,086 |

|

|

Total revenue |

|

|

668,456 |

|

|

|

170,724 |

|

|

|

|

|

|

|

|

|

|

|

|

Cost of revenue |

|

|

|

|

|

|

|

|

|

Testing services |

|

|

559,277 |

|

|

|

100,896 |

|

|

Consulting services |

|

|

12,500 |

|

|

|

37,534 |

|

|

Depreciation and amortization |

|

|

18,302 |

|

|

|

- |

|

|

Total cost of revenue |

|

|

590,079 |

|

|

|

138,430 |

|

|

|

|

|

|

|

|

|

|

|

|

Gross margin |

|

|

78,377 |

|

|

|

32,294 |

|

|

|

|

|

|

|

|

|

|

|

|

Operating expenses |

|

|

|

|

|

|

|

|

|

Selling, general and administrative |

|

|

435,158 |

|

|

|

123,809 |

|

|

Depreciation and amortization |

|

|

34,535 |

|

|

|

12,030 |

|

|

Total operating expenses |

|

|

469,693 |

|

|

|

135,839 |

|

|

|

|

|

|

|

|

|

|

|

|

Loss from operations |

|

|

(391,316 | ) |

|

|

(103,545 | ) |

|

|

|

|

|

|

|

|

|

|

|

Other income (expense) |

|

|

|

|

|

|

|

|

|

Interest expense |

|

|

(323,422 | ) |

|

|

(51,753 | ) |

|

Loss on disposal of asset |

|

|

- |

|

|

|

(719 | ) |

|

(Loss) gain on change in fair market value of derivative liabilities |

|

|

(106,243 | ) |

|

|

86,413 |

|

|

Total other income (expense) |

|

|

(429,665 | ) |

|

|

33,941 |

|

|

|

|

|

|

|

|

|

|

|

|

Net loss |

|

$ | (820,981 | ) |

|

$ | (69,604 | ) |

|

Gain (loss) attributable to non-controlling interest |

|

|

4,736 |

|

|

|

(4,721 | ) |

|

Net loss attributable to Signal Bay, Inc. |

|

$ | (825,717 | ) |

|

$ | (64,883 | ) |

|

|

|

|

|

|

|

|

|

|

|

Basic and diluted loss per common share |

|

$ | (0.00 | ) |

|

$ | (0.00 | ) |

|

|

|

|

|

|

|

|

|

|

|

Weighted average common shares outstanding |

|

|

883,348,109 |

|

|

|

399,435,484 |

|

The accompanying notes are an integral part of these unaudited consolidated financial statements.

| 4 |

| Table of Contents |

|

SIGNAL BAY, INC. | ||||||||

|

UNAUDITED CONSOLIDATED STATEMENTS OF CASH FLOWS | ||||||||

|

|

|

|

| |||||

|

|

|

Three months ended December 31, |

| |||||

|

|

|

2016 |

|

|

2015 |

| ||

|

Cash flows from operating activities |

|

|

|

|

|

| ||

|

Net loss |

|

$ | (820,981 | ) |

|

$ | (69,604 | ) |

|

Adjustments to reconcile net loss to net cash used in operating activities: |

|

|

|

|

|

|

|

|

|

Stock based compensation |

|

|

166,924 |

|

|

|

48,999 |

|

|

Loss on disposal of asset |

|

|

- |

|

|

|

719 |

|

|

Depreciation and amortization expense |

|

|

52,837 |

|

|

|

12,030 |

|

|

Amortization of debt discount |

|

|

293,316 |

|

|

|

51,250 |

|

|

Loss (gain) on derivative liability |

|

|

106,243 |

|

|

|

(86,413 | ) |

|

Reduction of security deposit for rent expense |

|

|

2,095 |

|

|

|

- |

|

|

Changes in operating assets and liabilities: |

|

|

|

|

|

|

|

|

|

Accounts receivable |

|

|

(210,271 | ) |

|

|

4,805 |

|

|

Prepaid expenses |

|

|

(11,876 | ) |

|

|

5,000 |

|

|

Other current asset |

|

|

40,000 |

|

|

|

- |

|

|

Security deposits |

|

|

(4,190 | ) |

|

|

(6,476 | ) |

|

Accounts payable and accrued liabilities |

|

|

221,243 |

|

|

|

19,039 |

|

|

Interest payable |

|

|

28,420 |

|

|

|

- |

|

|

Customer deposits |

|

|

128,549 |

|

|

|

18,975 |

|

|

Net cash used in operating activities |

|

|

(7,691 | ) |

|

|

(1,676 | ) |

|

|

|

|

|

|

|

|

|

|

|

Cash flows from investing activities |

|

|

|

|

|

|

|

|

|

Purchase of equipment |

|

|

(26,314 | ) |

|

|

(9,253 | ) |

|

Net cash paid in acquisitions of subsidiaries |

|

|

(6,930 | ) |

|

|

- |

|

|

Net cash used in investing activities |

|

|

(33,244 | ) |

|

|

(9,253 | ) |

|

|

|

|

|

|

|

|

|

|

|

Cash flows from financing activities |

|

|

|

|

|

|

|

|

|

Proceeds from the issuance of series D preferred stock |

|

|

114,500 |

|

|

|

- |

|

|

Proceeds from convertible notes, net of original issue discounts and fees |

|

|

70,000 |

|

|

|

- |

|

|

Payment on loan payable |

|

|

(31,687 | ) |

|

|

- |

|

|

Proceeds from notes payable - related party |

|

|

80,000 |

|

|

|

- |

|

|

Payments on notes payable - related party |

|

|

(97,481 | ) |

|

|

(3,263 | ) |

|

Net cash provided by financing activities |

|

|

135,332 |

|

|

|

(3,263 | ) |

|

|

|

|

|

|

|

|

|

|

|

Net cash increase for period |

|

|

94,397 |

|

|

|

(14,192 | ) |

|

Cash balance, beginning of period |

|

|

57,486 |

|

|

|

25,966 |

|

|

Cash balance, end of period |

|

$ | 151,883 |

|

|

$ | 11,774 |

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental disclosure of cash flow information: |

|

|

|

|

|

|

|

|

|

Cash paid for interest |

|

$ | - |

|

|

$ | 91 |

|

|

Cash paid for income tax |

|

$ | - |

|

|

$ | - |

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental disclosure of non-cash investing and financing activities: |

|

|

|

|

|

|

|

|

|

Conversion of convertible note and accrued interest into common stock |

|

$ | 316,457 |

|

|

$ | - |

|

|

Conversion of Series A Preferred stock to common stock |

|

$ | 4,388 |

|

|

$ | - |

|

|

Reclassification of derivative liability to additional paid in capital |

|

$ | 889,509 |

|

|

$ | - |

|

|

Acquisition of Green Style Consulting assets through issuance of preferred shares and note payable |

|

$ | 260,000 |

|

|

$ | - |

|

|

Acquisition of Greenhaus Analytical Labs, LLC through issuance of preferred shares and note payable |

|

$ | 800,000 |

|

|

$ | - |

|

|

Debt discount from derivative liability |

|

$ | 198,300 |

|

|

$ | - |

|

|

Capital leases financed through accounts payable |

|

$ |

105,120 |

|

|

$ |

- |

|

The accompanying notes are an integral part of these unaudited consolidated financial statements.

| 5 |

| Table of Contents |

SIGNAL BAY, INC. AND SUBSIDIARIES

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2016

NOTE 1 – NATURE OF ACTIVITIES AND CONTINUANCE OF BUSINESS

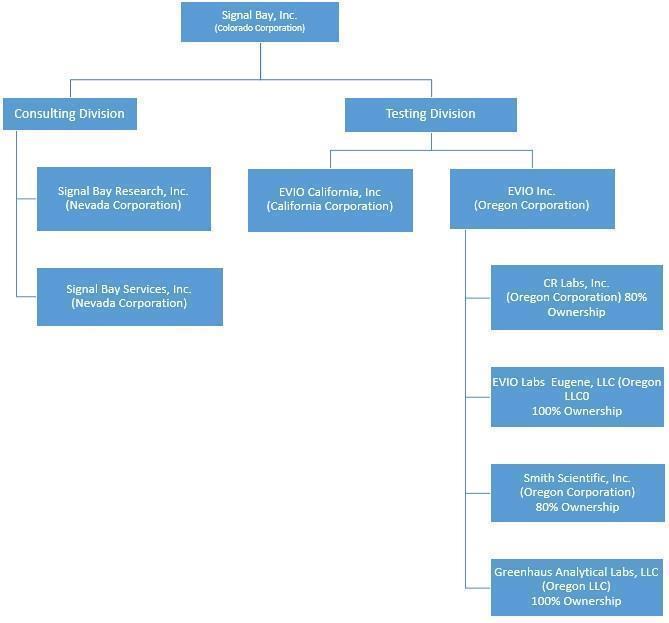

Signal Bay, Inc., a Colorado corporation and its subsidiaries provide advisory, management and analytical testing services to the emerging legalized cannabis industry. Signal Bay, Inc. was originally incorporated in the State of New York, December 12, 1977 under the name 3171 Holding Corporation. On February 22, 1979 the name was changed to Electronomic Industries Corp. and on February 23, 1983 the name was changed to Quantech Electronics Corp. The Company was reincorporated in the State of Colorado on December 15, 2003. On August 29, 2014, the Company completed a reverse merger with Signal Bay Research, Inc., a Nevada Corporation, and assumed its operations. In September 2014, the Company changed its name from Quantech Electronics Corp. to Signal Bay, Inc. The Company has selected September 30 as its fiscal year end. Signal Bay, Inc. is domiciled in the State of Colorado, and its corporate headquarters is located in Bend, Oregon.

As a part of and prior to the consummation of the reverse merger, William Waldrop and Lori Glauser, principals of Signal Bay Research, Inc., purchased 28,811,933 shares of the Company (80% of the issued and outstanding common stock) from WB Partners. The merger between the Company and Signal Bay Research was finalized and closed contemporaneously with the share purchase. As part of this share purchase, Mr. Waldrop and Ms. Glauser became the officers and directors of the Company. Signal Bay Research was acquired through the issuance of 254,188,067 shares of common stock and 5,000,000 shares of Series B Preferred Stock to Mr. Waldrop and Ms. Glauser, pro rata. After the reverse merger, William Waldrop and Lori Glauser individually each own 127,500,000 shares of common stock and 2,500,000 shares of Series B Preferred stock in the Company. Immediately prior to the reverse merger, neither William Waldrop nor Lori Glauser had any interest in the Company. Immediately after to the reverse, WB Partners owned less than 5% of the common stock. The company filed a Form 10-12G on November 25, 2014, and was determined to be a shell company by the SEC as per the Form 10-12G/A which went effective on January 24, 2015. On January 29, 2015, the company filed an 8-K stating it entered into a material agreement and was no longer a shell company.

After the reverse merger, Signal Bay Research, Inc. continues to operate as a wholly owned subsidiary providing compliance, research and advisory services for Signal Bay, Inc.

Signal Bay Services was formed on January 25, 2015, as the management services division of Signal Bay.

On September 17, 2015, Signal Bay entered into a share exchange agreement with CR Labs, Inc., an Oregon Corporation, pursuant to which the company issued 40,000,000 shares of the Company’s common stock resulting in exchange for 80% of the outstanding common stock of CR Labs, Inc.

EVIO Inc. was formed on April 4, 2016 to become the holding company for all laboratory operations.

EVIO Labs Eugene was formed on May 23, 2016, as a wholly owned subsidiary of EVIO Inc. Subsequently on May 24, 2016, EVIO Labs Eugene acquired all of the assets of Oregon Analytical Services, LLC, inclusive of client lists, equipment, trade names and personnel.

On June 1, 2016, EVIO Inc. entered into a share purchase agreement to purchase 80% of the outstanding common stock of Smith Scientific Industries, Inc. d/b/a Kenevir Research in Medford, OR.

On October 19, 2016, the Company entered into a Membership Interest Purchase Agreement to purchase 100% of the ownership of Greenhaus Analytical Labs, LLC.

On October 26, 2016, the Company entered in to an Asset Purchase Agreement with Green Style Consulting, LLC which was closed on November 1, 2016.

| 6 |

| Table of Contents |

Going Concern

The Company's financial statements are prepared using accounting principles generally accepted in the United States of America applicable to a going concern, which contemplates the realization of assets and liquidation of liabilities in the normal course of business. However, the Company has negative working capital, recurring losses, and does not have an established source of revenues sufficient to cover its operating costs. These factors raise substantial doubt about the Company’s ability to continue as a going concern.

The ability of the Company to continue as a going concern is dependent upon its ability to successfully accomplish the plan described in the preceding paragraph and eventually attain profitable operations. The accompanying financial statements do not include any adjustments that may be necessary if the Company is unable to continue as a going concern.

In the coming year, the Company’s foreseeable cash requirements will relate to continual development of the operations of its business, maintaining its good standing and making the requisite filings with the Securities and Exchange Commission, and the payment of expenses associated with operations and business developments. The Company may experience a cash shortfall and be required to raise additional capital.

Historically, it has mostly relied upon internally generated funds such as shareholder loans and advances to finance its operations and growth. Management may raise additional capital by retaining net earnings or through future public or private offerings of the Company’s stock or through loans from private investors, although there can be no assurance that it will be able to obtain such financing. The Company’s failure to do so could have a material and adverse effect upon it and its shareholders.

NOTE 2 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation:

The accompanying unaudited interim consolidated financial statements of the Company have been prepared in accordance with accounting principles generally accepted in the United States of America and the rules of the Securities and Exchange Commission, and should be read in conjunction with the audited consolidated financial statements and notes thereto contained in the Company’s most recent Annual Financial Statements filed with the SEC on Form 10-K. In the opinion of management, all adjustments, consisting of normal recurring adjustments, necessary for a fair presentation of financial position and the results of operations for the interim period presented have been reflected herein. The results of operations for the interim period are not necessarily indicative of the results to be expected for the full year. Notes to the financial statements which would substantially duplicate the disclosures contained in the audited consolidated financial statements for the most recent fiscal period, as reported in the Form 10-K, have been omitted

Principles of Consolidation

The Company prepares its financial statements on the accrual basis of accounting. The accompanying consolidated financial statements include the accounts of the Company and its wholly and partially owned subsidiaries, all of which have a fiscal year end of September 30. All significant intercompany accounts, balances and transactions have been eliminated in the consolidation.

The Company consolidates its subsidiaries in accordance with ASC 810, and specifically ASC 810-10-15-8 which states, the usual condition for a controlling financial interest is ownership of a majority voting interest, and, therefore, as a general rule ownership by one reporting entity, directly or indirectly, or over 50% of the outstanding voting shares of another entity is a condition pointing toward consolidation.

Use of Estimates

The preparation of financial statements in accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. A change in managements’ estimates or assumptions could have a material impact on Signal Bay, Inc.’s financial condition and results of operations during the period in which such changes occurred. Actual results could differ from those estimates. Signal Bay, Inc.’s financial statements reflect all adjustments that management believes are necessary for the fair presentation of their financial condition and results of operations for the periods presented.

| 7 |

| Table of Contents |

Reclassification of Prior Period Presentation

Certain amounts have been reclassified on the September 30, 2016 balance sheet to conform to current period presentation. Specifically, websites and domains net of accumulated amortization of $31,178 have been reclassified on the balance sheet to be included in intangibles assets where previously they were included in fixed assets. These reclassifications have no impact on net loss.

Financial Instruments

Level 1 - applies to assets or liabilities for which there are quoted prices in active markets for identical assets or liabilities.

Level 2 - applies to assets or liabilities for which there are inputs other than quoted prices that are observable for the asset or liability such as quoted prices for similar assets or liabilities in active markets; quoted prices for identical assets or liabilities in markets with insufficient volume or infrequent transactions (less active markets); or model-derived valuations in which significant inputs are observable or can be derived principally from, or corroborated by, observable market data.

Level 3 - applies to assets or liabilities for which there are unobservable inputs to the valuation methodology that are significant to the measurement of the fair value of the assets or liabilities.

The Company's financial instruments consist principally of cash, accounts payable, and accrued liabilities. Pursuant to ASC 820 and 825, the fair value of cash is determined based on "Level 1" inputs, which consist of quoted prices in active markets for identical assets. The recorded values of all other financial instruments approximate their current fair values because of their nature and respective maturity dates or durations.

The following table sets forth by level with the fair value hierarchy the Company's financial assets and liabilities measured at fair value on

December 31, 2016:

|

|

|

Level 1 |

|

|

Level 2 |

|

|

Level 3 |

|

|

Total |

| ||||

|

Liabilities |

|

|

|

|

|

|

|

|

|

|

|

| ||||

|

Derivative financial instruments |

|

$ | - |

|

|

$ | - |

|

|

$ | 190,280 |

|

|

$ | 190,280 |

|

The following table sets forth by level with the fair value hierarchy the Company's financial assets and liabilities measured at fair value on

September 30, 2016:

|

|

|

Level 1 |

|

|

Level 2 |

|

|

Level 3 |

|

|

Total |

| ||||

|

Liabilities |

|

|

|

|

|

|

|

|

|

|

|

| ||||

|

Derivative financial instruments |

|

$ | - |

|

|

$ | - |

|

|

$ | 775,246 |

|

|

$ | 775,246 |

|

Recently Issued Accounting Pronouncements

In February 2015, the FASB issued ASC 2015-02, "Consolidation (Topic 810) - Amendments to the Consolidation Analysis." This standard modifies existing consolidation guidance for reporting organizations that are required to evaluate whether they should consolidate certain legal entities. ASU 2015-02 is effective for fiscal years beginning after December 15, 2015, and requires either a retrospective or a modified retrospective approach to adoption. Early adoption is permitted. The Company adopted has this standard and determined it does not have a significant impact on its consolidated financial statements.

| 8 |

| Table of Contents |

In September 2015, the FASB issued ASU 2015-16, “Business Combinations (Topic 805) – Simplifying the Accounting for Measurement-Period Adjustments.” This update eliminates the requirement to restate prior period financial statements for measurement period adjustments. The new guidance requires that the cumulative impact of a measurement period adjustment (including the impact on prior periods) be recognized in the reporting period in which the adjustment is identified. The new standard should be applied prospectively to measurement period adjustments that occur after the effective date. The new standard is effective for interim and annual periods beginning after December 15, 2015 and early adoption is permitted. The Company has adopted this guidance and the adoption of this guidance did not have an impact on the Company’s results of operations, financial position, or cash flows for the three months ended December 31, 2016 or 2015.

Management believes recently issued accounting pronouncements will have no impact on the financial statements of the Company.

NOTE 3 – ACQUISITIONS

Greenhaus Analytical Labs, LLC (or “GHA”)

On October 19, 2016, the Company entered into a Membership Interest Purchase Agreement to purchase 100% of the ownership of Greenhaus Analytical Labs, LLC. for 460,000 shares of Series “D” preferred stock and a $340,000 promissory note.

The Company applied the acquisition method to the business combination and valued each of the assets acquired (cash, accounts receivable, prepaid expenses, security deposits, customer lists, certain testing licenses and property, plant and equipment) and liabilities assumed (accounts payable, related party payables and notes payable) at fair value as of the acquisition date. The cash, accounts receivable and accounts payable were deemed to be recorded at fair value as of the acquisition date. The Company determined the fair value of property, plant and equipment to be historical book value. The preliminary allocation of the purchase price was based on estimates of the fair value of the assets and liabilities assumed. Under the purchase agreement, the Company issued 460,000 shares of Series “D” preferred stock, valued at $460,000 and a $340,000 promissory note for total consideration of $800,000. The following table shows the estimated fair values of the assets acquired and liabilities assumed at the date of acquisition:

|

ASSETS ACQUIRED |

|

|

| |

|

CASH |

|

$ | 13,070 |

|

|

ACCOUNTS RECEIVABLE |

|

|

21,767 |

|

|

PREPAID EXPENSES |

|

|

300 |

|

|

SECURITY DEPOSITS |

|

|

700 |

|

|

PROPERTY PLANT AND EQUIPMENT |

|

|

81,311 |

|

|

LICENSE |

|

|

132,668 |

|

|

CUSTOMER LIST |

|

|

43,562 |

|

|

GOODWILL |

|

|

800,000 |

|

|

TOTAL ASSETS ACQUIRED |

|

$ | 1,093,378 |

|

|

|

|

|

|

|

|

LIABILITIES ASSUMED |

|

|

|

|

|

ACCOUNTS PAYABLE |

|

$ | (73,866 | ) |

|

RELATED PARTY PAYABLES |

|

|

(194,512 | ) |

|

NOTES PAYABLE |

|

|

(25,000 | ) |

|

TOTAL LIABILITIES ASSUMED |

|

|

(293,378 | ) |

|

|

|

|

|

|

|

NET ASSETS ACQUIRED FROM GHA ACQUISITION |

|

$ | 800,000 |

|

| 9 |

| Table of Contents |

Green Style Consulting, LLC

On October 26, 2016, the Company entered in to an Asset Purchase Agreement with Green Style Consulting, LLC. Effective, November 1, 2016, the company owned all assets of Green Style Consulting, LLC d/b/a Green Style Analytics, including 1,300 client names, analytical testing equipment, brands/websites, and the vanity toll-free number 844-420-TEST for 210,000 shares of Series “D” preferred stock, $20,000 cash down payment and a $50,000 promissory note.

The Company applied the acquisition method to the business combination and valued each of the assets acquired (customer lists and property, plant and equipment) at fair value as of the acquisition date. The property, plant and equipment were deemed to be recorded at fair value as of the acquisition date. The Company determined the fair value of property, plant and equipment to be historical book value. The preliminary allocation of the purchase price was based on estimates of the fair value of the assets and liabilities assumed. Under the purchase agreement, the Company issued 210,000 shares of Series “D” preferred stock, valued at $210,000, a cash payment of $20,000 and a $50,000 promissory note for total consideration of $280,000. Additionally, the Company has agreed to pay the sellers 20% of Evio California, Inc.’s net profits effective November 1, 2016 for a period of three years ending October 31, 2019. The following table shows the estimated fair values of the assets acquired and liabilities assumed at the date of acquisition:

|

ASSETS ACQUIRED |

|

|

| |

|

PROPERTY PLANT AND EQUIPMENT |

|

$ | 19,300 |

|

|

CUSTOMER LIST |

|

|

61,051 |

|

|

GOODWILL |

|

|

199,649 |

|

|

TOTAL ASSETS ACQUIRED |

|

$ | 280,000 |

|

|

|

|

|

|

|

|

LIABILITIES ASSUMED |

|

|

- |

|

|

NET ASSETS ACQUIRED FROM GREEN STYLE ACQUISITION |

|

$ | 280,000 |

|

In accordance with ASC 805-10-50, the Company is providing the following unaudited pro-forma to present a summary of the combined results of the Company’s consolidated operations with all acquisitions. as if the acquisitions had been completed as of the beginning of the reporting period. Adjustments were made to eliminate any inter-company transactions in the periods presented.

|

SIGNAL BAY, INC. | ||||||||

|

UNAUDITED PRO FORMA CONSOLIDATED STATEMENTS OF OPERATIONS | ||||||||

|

|

|

|

|

| ||||

|

|

|

Three months ended December 31, |

| |||||

|

Revenues |

|

2016 |

|

|

2015 |

| ||

|

Testing services |

|

$ | 608,774 |

|

|

$ | 71,142 |

|

|

Consulting services |

|

|

99,878 |

|

|

|

131,086 |

|

|

Total revenue |

|

|

708,652 |

|

|

|

202,228 |

|

|

|

|

|

|

|

|

|

|

|

|

Cost of revenue |

|

|

|

|

|

|

|

|

|

Testing services |

|

|

596,813 |

|

|

|

123,732 |

|

|

Consulting services |

|

|

12,500 |

|

|

|

37,534 |

|

|

Total cost of revenue |

|

|

609,313 |

|

|

|

161,266 |

|

|

|

|

|

|

|

|

|

|

|

|

Gross margin |

|

|

99,339 |

|

|

|

40,962 |

|

|

|

|

|

|

|

|

|

|

|

|

Operating expenses |

|

|

|

|

|

|

|

|

|

Selling, general and administrative |

|

|

439,259 |

|

|

|

156,535 |

|

|

Depreciation and amortization |

|

|

28,660 |

|

|

|

12,030 |

|

|

Total operating expenses |

|

|

467,919 |

|

|

|

168,565 |

|

|

|

|

|

|

|

|

|

|

|

|

Loss from operations |

|

|

(368,580 | ) |

|

|

(127,603 | ) |

|

|

|

|

|

|

|

|

|

|

|

Other income (expense) |

|

|

|

|

|

|

|

|

|

Interest expense |

|

|

(323,878 | ) |

|

|

(52,775 | ) |

|

Loss on disposal of asset |

|

|

- |

|

|

|

(719 | ) |

|

(Loss) gain on change in fair market value of derivative liabilities |

|

|

(106,243 | ) |

|

|

86,413 |

|

|

Total other income (expense) |

|

|

(430,121 | ) |

|

|

32,919 |

|

|

|

|

|

|

|

|

|

|

|

|

Net loss |

|

$ | (798,701 | ) |

|

$ | (94,684 | ) |

| 10 |

| Table of Contents |

Future Amortization

The future amortization associated with the intangible assets acquired in the above mentioned and prior acquisitions is as follows:

|

For the years ended September 30, |

|

Amortization |

| |

|

2017 |

|

$ | 101,723 |

|

|

2018 |

|

|

135,630 |

|

|

2019 |

|

|

135,630 |

|

|

2020 |

|

|

135,630 |

|

|

2021 |

|

|

93,455 |

|

|

Thereafter |

|

|

3,955 |

|

|

Total |

|

$ | 606,023 |

|

NOTE 4 – RELATED PARTY TRANSACTIONS

Through September 30, 2016, the Company received loans from its Chief Operating Officer totaling $96,000. Through September 30, 2016, the Company made repayments totaling $4,295. There were no repayments made during the three months ended December 31, 2016. There was $91,705 due as of December 31, 2016 and September 30, 2016, and is included in the accompanying consolidated balance sheets as a current portion of notes payable to related parties. The loans carry a 0% interest rate and are due on demand.

During the three months ended December 31, 2016 and 2015, the Company incurred total expenses of $14,548 and $21,400 for management consulting services performed by Newport Commercial Advisors, an entity fully owned and controlled by our Chief Executive Officer. There was not a balance payable to Newport Commercial Advisors as of December 31, 2016 or September 30, 2016.

During the three months ended December 31, 2016, the Company received loans from its Chief Executive Officer totaling $80,000. The loans are non-interest bearing and due on demand. There was $80,000 due as of December 31, 2016.

During the three months ended December 31, 2016 the Company made repayments to Eric Ezrine, a shareholder of CR Labs, on an outstanding note payable totaling $3,574. The loans carry an interest rate of 0% per annum. There was $9,695 and $13,269 due as of December 31, 2016 and September 30, 2016, respectively. Additionally, the Company entered into a severance agreement with Mr. Ezrine whereby it agreed to make payments totaling $44,500 through August 2018. The Company made repayments of $4,000 during the three months ended December 31, 2016. There was $40,500 and $44,500 accrued as of December 31, 2016 and September 30, 2016.

Through March 31, 2016, our executive, administrative and operating offices were located at 2996 Panorama Ridge Dr. Henderson, NV 89052. The office space was being provided by one of our Directors at no cost to the Company.

On May 24, 2016, the Company executed an asset purchase agreement with Sara Lausmann, managing member owner of Oregon Analytical Services, LLC, for $972,500. The terms of the purchase required the issuance of 200,000 shares of Series C Preferred Stock, valued at $80,000, $72,500 in a short-term loan and $700,000 in a long-term note. During the three months ended December 31, 2016, the Company repaid $13,808 to Sara Lausmann, Vice President Client Services. The total amount owed is $723,776 and $737,584 as of December 31, 2016 and September 30, 2016, respectively. As of December 31, 2016 and September 30, 2016, $23,776 and $37,584 and $700,000 and $700,000 are included in the accompanying consolidated balance sheets as current and long-term portions of notes payable to related party, respectively. The notes carry interest at a rate of 5% per annum and had accrued interest totaling $22,642 and $13,521 due as of December 31, 2016 and September 30, 2016, respectively.

| 11 |

| Table of Contents |

On June 1, 2016, the company executed a share purchase agreement with Anthony Smith, for the purchase of 80% of Smith Scientific Industries for $636,000. The terms of the purchase required the issuance of 300,000 shares of Series C Preferred Stock, valued at $135,000 and $336,000 in a promissory note. During the three months ended December 31, 2016, the Company repaid $25,000 to Anthony Smith, our Chief Science Officer. The note carries interest at a rate of 5% per annum. There was $286,000 and $311,000 of principal due as of December 31, 2016 and September 30, 2016 and $8,859 and $5,155 of accrued interest due as of December 31, 2016 and September 30, 2016, respectively.

On October 19, 2016, the Company assumed a $194,512 payable due to Henry Grimmett, and officer of Greenhaus and current Director of the Company, with its acquisition of Greenhaus Analytical Services, LLC. The note bears interest at 0% per annum and requires repayments of $25,000 quarterly. During the three months ended December 31, 2016, the Company made repayments totaling $11,100. There was a total of $183,412 due as of December 31, 2016 of which $100,000 is current and $83,412 is long term.

On October 19, 2016, the Company entered into a $340,000 note payable as part of its acquisition of Greenhaus Analytical Services, LLC. The note carries interest at a rate of 6% per annum and matures on October 16, 2020. There was $340,000 of principal and $4,248 of accrued interest due as of December 31, 2016.

On November 1, 2016, the Company entered into a $50,000 note payable to Green Style Consulting, LLC as part of the asset purchase agreement . Green Style Consulting, LLC Managing Member is our General Manager Northern California, who was hired by the Company concurrent to the asset purchase. The note carries interest at a rate of 5% per annum and matures on October 31, 2018. During the three months ended December 31, 2016, the Company made repayments of $1,000. There was $49,000 of principal and $411 of accrued interest due as of December 31, 2016.

Through September 30, 2016, the Company borrowed a total of $16,200 from our Chief Science Officer to fund operations. The loans are non-interest bearing, due on demand and as such are included in current liabilities. During the three months ended December 31, 2016, the Company made repayments totaling $3,000. There was $13,200 and $16,200 due as of December 31, 2016 and September 30, 2016, respectively.

NOTE 5 – EQUITY TRANSACTIONS

Series A Convertible Preferred Stock

The Company designated 1,850,000 shares of Series A Convertible Preferred Stock (“Series A Preferred Stock”) with a par value of $0.0001 per share. Initially, there will be no dividends due or payable on the Series A Preferred Stock. Any future terms with respect to dividends shall be determined by the Board consistent with the Corporation’s Certificate of Incorporation. Any and all such future terms concerning dividends shall be reflected in an amendment to this Certificate, which the Board shall promptly file or cause to be filed.

All shares of the Series A Preferred Stock shall rank (i) senior to the Corporation’s Common Stock and any other class or series of capital stock of the Corporation hereafter created, (ii) pari passu with any class or series of capital stock of the Corporation hereafter created and specifically ranking, by its terms, on par with the Series A Preferred Stock and (iii) junior to any class or series of capital stock of the Corporation hereafter created specifically ranking, by its terms, senior to the Series A Preferred Stock, in each case as to distribution of assets upon liquidation, dissolution or winding up of the Corporation, whether voluntary or involuntary.

The Series A Preferred shall have no liquidation preference over any other class of stock.

Except as otherwise required by law, holders of Series A Preferred Stock shall have no special voting rights and their consent shall not be required (except to the extent they are entitled to vote with holders of Common Stock or any other class or series of preferred stock) for the taking of any corporate action.

Conversion at the Option of the Holder. From 12 months from the date of issuance, each holder of shares of Series A Preferred Stock may, at any time and from time to time, convert (an “Optional Conversion”) each of its shares of Series A Preferred Stock into fully paid and nonassessable shares of Common Stock at a rate equal to 4.9% of the Common Stock.

| 12 |

| Table of Contents |

For a period of 18 months after the Preferred is convertible, the conversion price of the Series A Preferred will be subject to adjustment to prevent dilution in the event that the Company issues additional shares at a purchase price less than the applicable conversion price. The conversion price will be subject to adjustment on a weighted basis that takes into account issuances of additional shares. At the expiration of the antidilution period, the conversion rate in Section VI (A) above shall be equal to a conversion rate equal to 4.9% on the Common Stock. For example, if on the date of expiration of the antidilution clause there are 500,000,000 shares of Common Stock issued and outstanding then each Series A Preferred Stock shall convert at a rate of 13.24 common shares for each 1 Series Preferred Share.

The company has evaluated the Series A Preferred Stock in accordance with ASC 815 and has determined their conversion options were for equity and ASC 815 does not apply.

The company has evaluated the Series A Preferred Stock in accordance with FASB ASC Subtopic 470-20, and has determined that there is no beneficial conversion feature that must be accounted.

All 1,840,000 outstanding Series A Convertible Stock was converted into 43,875,385 of common shares during the three months ended December 31, 2016.

The Company has 0 and 1,840,000 shares of Series A Convertible Stock issued and outstanding as December 31, 2016 and September 30, 2016, respectively.

Series B Convertible Preferred Stock

The Company designated 5,000,000 shares of Series B Convertible Preferred Stock (“Series B Preferred Stock”) with a par value of $0.0001 per share.

Initially, there will be no dividends due or payable on the Series B Preferred Stock. Any future terms with respect to dividends shall be determined by the Board consistent with the Corporation’s Certificate of Incorporation. Any and all such future terms concerning dividends shall be reflected in an amendment to this Certificate, which the Board shall promptly file or cause to be filed.

All shares of the Series B Preferred Stock shall rank (i) senior to the Corporation’s Common Stock and any other class or series of capital stock of the Corporation hereafter created, (ii) pari passu with any class or series of capital stock of the Corporation hereafter created and specifically ranking, by its terms, on par with the Series B Preferred Stock and (iii) junior to any class or series of capital stock of the Corporation hereafter created specifically ranking, by its terms, senior to the Series B Preferred Stock, in each case as to distribution of assets upon liquidation, dissolution or winding up of the Corporation, whether voluntary or involuntary.

The Series B Preferred shall have no liquidation preference over any other class of stock.

Each holder of outstanding shares of Series B Preferred Stock shall be entitled to the number of votes equal to one hundred (100) Common Shares. Except as provided by law, or by the provisions establishing any other series of Preferred Stock, holders of Series B Preferred Stock and of any other outstanding series of Preferred Stock shall vote together with the holders of Common Stock as a single class.

Each holder of shares of Series B Preferred Stock may, at any time and from time to time, convert (an “Optional Conversion”) each of its shares of Series B Preferred Stock into a 100 of fully paid and nonassessable shares of Common Stock; provided, however, that any Optional Conversion must involve the issuance of at least 100 shares of Common Stock.

In the event of a reverse split the conversion ratio shall not change. However, in the event a forward split shall occur then the conversion ratio shall be modified to be increased by the same ratio as the forward split.

The company has evaluated the Series B Preferred Stock in accordance with ASC 815 and has determined their conversion options were for equity and ASC 815 does not apply.

The company has evaluated the Series B Preferred Stock in accordance with FASB ASC Subtopic 470-20, and has determined that there is no beneficial conversion feature that must be accounted.

The Company has 5,000,000 shares of Series B Convertible Stock issued and outstanding as of December 31, 2016 and September 30, 2016.

| 13 |

| Table of Contents |

Series C Convertible Preferred Stock

The Company designated 500,000 shares of Series C Convertible Preferred Stock (“Series C Preferred Stock”) with a par value of $0.0001 per share.

Initially, there will be no dividends due or payable on the Series C Preferred Stock. Any future terms with respect to dividends shall be determined by the Board consistent with the Corporation’s Certificate of Incorporation. Any and all such future terms concerning dividends shall be reflected in an amendment to this Certificate, which the Board shall promptly file or cause to be filed.

All shares of the Series C Preferred Stock shall rank (i) senior to the Corporation’s Common Stock and any other class or series of capital stock of the Corporation hereafter created, (ii) pari passu with any class or series of capital stock of the Corporation hereafter created and specifically ranking, by its terms, on par with the Series B Preferred Stock and (iii) junior to any class or series of capital stock of the Corporation hereafter created specifically ranking, by its terms, senior to the Series B Preferred Stock, in each case as to distribution of assets upon liquidation, dissolution or winding up of the Corporation, whether voluntary or involuntary.

In any liquidation, dissolution, or winding up of the Corporation, the holders of the Series C Preferred Stock shall be entitled to receive (a) in preference to the holders of the Common Stock (b) on a pari passu basis to any sum that the holders of the Series B Preferred Stock shall be entitled to receive, but (c) subordinate in preference to any sum that the holders of any shares of any other series of the Corporation's Preferred Stock shall be entitled, an amount equal to $1 per share (subject to appropriate adjustment in the event of any stock dividend, forward stock split, or other similar recapitalization). After payment of such sums, (i) the holders of the Series A Preferred Stock and (ii) the holders of the Common Stock, shall be entitled to receive any remaining assets of the Corporation on a pro rata, as-converted basis assuming conversion of the Series A Preferred Stock into Common Stock at the then- current Conversion Rate.

Each holder of outstanding shares of Series C Preferred Stock shall be entitled to the number of votes equal to five hundred (500) Common Shares. Except as provided by law, or by the provisions establishing any other series of Preferred Stock, holders of Series B Preferred Stock and of any other outstanding series of Preferred Stock shall vote together with the holders of Common Stock as a single class.

Each holder of shares of Series C Preferred Stock may, at any time and from time to time, convert (an “Optional Conversion”) each of its shares of Series C Preferred Stock into a 500 of fully paid and nonassessable shares of Common Stock; provided, however, that any Optional Conversion must involve the issuance of at least 10,000 shares of Common Stock.

In the event of a reverse split the conversion ratio shall not change. However, in the event a forward split shall occur then the conversion ratio shall be modified to be increased by the same ratio as the forward split.

The company has evaluated the Series C Preferred Stock in accordance with ASC 815 and has determined their conversion options were for equity and ASC 815 does not apply.

The company has evaluated the Series C Preferred Stock in accordance with FASB ASC Subtopic 470-20, and has determined that there is no beneficial conversion feature that must be accounted.

During the year ended September 30, 2016, the Company issued 300,000 shares of Series C Preferred Stock for the acquisition of Smith Scientific Industries, Inc. and 200,000 shares of Series C Preferred Stock for the acquisition of the assets of Oregon Analytical Services.

There were 500,000 shares of Series C Convertible Stock issued and outstanding as of December 31, 2016 and September 30, 2016.

Series D Convertible Preferred Stock

The Company designated 1,000,000 shares of Series D Convertible Preferred Stock (“Series D Preferred Stock”) with a par value of $0.0001 per share.

Initially, there will be no dividends due or payable on the Series D Preferred Stock. Any future terms with respect to dividends shall be determined by the Board consistent with the Corporation’s Certificate of Incorporation. Any and all such future terms concerning dividends shall be reflected in an amendment to this Certificate, which the Board shall promptly file or cause to be filed.

| 14 |

| Table of Contents |

All shares of the Series D Preferred Stock shall rank (i) senior to the Corporation’s Common Stock and any other class or series of capital stock of the Corporation hereafter created, (ii) pari passu with any class or series of capital stock of the Corporation hereafter created and specifically ranking, by its terms, on par with the Series B Preferred Stock and (iii) junior to any class or series of capital stock of the Corporation hereafter created specifically ranking, by its terms, senior to the Series B Preferred Stock, in each case as to distribution of assets upon liquidation, dissolution or winding up of the Corporation, whether voluntary or involuntary.

In any liquidation, dissolution, or winding up of the Corporation, the holders of the Series D Preferred Stock shall be entitled to receive (a) in preference to the holders of the Common Stock (b) on a pari passu basis to any sum that the holders of the Series B Preferred Stock shall be entitled to receive, but (c) subordinate in preference to any sum that the holders of any shares of any other series of the Corporation's Preferred Stock shall be entitled, an amount equal to $1 per share (subject to appropriate adjustment in the event of any stock dividend, forward stock split, or other similar recapitalization). After payment of such sums, (i) the holders of the Series A Preferred Stock and (ii) the holders of the Common Stock, shall be entitled to receive any remaining assets of the Corporation on a pro rata, as-converted basis assuming conversion of the Series A Preferred Stock into Common Stock at the then- current Conversion Rate.

Each holder of outstanding shares of Series D Preferred Stock shall be entitled to the number of votes equal to two hundred fifty (250) Common Shares. Except as provided by law, or by the provisions establishing any other series of Preferred Stock, holders of Series B Preferred Stock and of any other outstanding series of Preferred Stock shall vote together with the holders of Common Stock as a single class.

Each holder of shares of Series D Preferred Stock may, at any time and from time to time, convert (an “Optional Conversion”) each of its shares of Series D Preferred Stock into a 250 of fully paid and nonassessable shares of Common Stock; provided, however, that any Optional Conversion must involve the issuance of at least 50,000 shares of Common Stock.

In the event of a reverse split the conversion ratio shall not change. However, in the event a forward split shall occur then the conversion ratio shall be modified to be increased by the same ratio as the forward split.

The company has evaluated the Series D Preferred Stock in accordance with ASC 815 and has determined their conversion options were for equity and ASC 815 does not apply.

The company has evaluated the Series C Preferred Stock in accordance with FASB ASC Subtopic 470-20, and has determined that there is no beneficial conversion feature that must be accounted.

During the year ended September 30, 2016, the Company issued 48,000 shares of Series D Preferred Stock for cash proceeds of $48,000. During the three months ended December 31, 2016, the Company issued 114,500 shares of Series D Preferred Stock for cash proceeds of $114,500 and 670,000 shares of Series D Preferred Stock, valued at $670,000, in conjunction with the acquisitions as discussed in Note 3.

There were 832,500 and 48,000 shares of Series D Convertible Stock issued and outstanding as of December 31, 2016 and September 30, 2016, respectively.

Common Stock

During the year ended September 30, 2016, the Company issued 6,087,500 common shares valued at $46,473 under its employee equity incentive plan; 401,032,581 common shares for the conversion of $207,367 of outstanding principal on convertible notes payable; 1,468,582 common shares for the conversion of $4,135 of convertible accrued interest and 42,827,010 common shares for services valued at $138,447. All conversions of outstanding principal and accrued interest on convertible notes payable were done so at contractual terms.

During the three months ended December 31, 2016, the Company issued 7,976,150 common shares valued at $149,716 for services; 43,875,285 common shares for the conversion of 1,840,000 shares of Series A Preferred Stock; 41,851,494 common shares for the conversion of $302,450 of outstanding principal on convertible notes payable and 2,425,603 for the conversion of $14,006 of convertible accrued interest. All conversions of outstanding principal and accrued interest on convertible notes payable were done so at contractual terms.

There were 946,192,800 and 850,064,268 shares of common stock issued and outstanding at December 31, 2016 and September 30, 2016, respectively.

| 15 |

| Table of Contents |

NOTE 6 – LOANS PAYABLE

The Company had the following loans payable outstanding as of December 31, 2016 and September 30, 2016:

|

|

|

December 31, 2016 |

|

|

September 30, 2016 |

| ||

|

On July 22, 2016, the Company entered into a Purchase and Sale of Future Receivables agreement (the “Agreement”) with 1 Global Capital, LLC (“1GC”) for $50,000. The Agreement calls for 160 daily payments of $437.50, due on business days, for total payments of $70,000. The Company recognized an original debt discount of $20,000 as interest expense. |

|

$ | 23,188 |

|

|

$ | 49,875 |

|

|

|

|

|

|

|

|

|

|

|

|

On May 24, 2016, the Company assumed a $27,500 Promissory note with annual interest of 5%, as part of the acquisition of Oregon Analytical Services (see note 3). The note is due on demand and requires quarterly payments. |

|

|

22,500 |

|

|

|

27,500 |

|

|

|

|

|

45,688 |

|

|

|

77,375 |

|

|

Less: current portion of loans payable |

|

|

45,688 |

|

|

|

77,375 |

|

|

|

|

|

|

|

|

|

|

|

|

Long-term portion of loans payable |

|

$ | - |

|

|

$ | - |

|

As of December 31, 2016 and September 30, 2016, the Company accrued interest of $1,998 and $638, respectively.

NOTE 7 – CONVERTIBLE DEBT

The following table summarizes all convertible notes outstanding as of September 30, 2016:

|

Holder |

|

Issue Date |

|

Due Date |

|

Principal |

|

|

Unamortized Debt Discount |

|

|

Carrying Value |

|

|

Accrued Interest |

| ||||

|

Noteholder 1 |

|

5/17/2016 |

|

5/18/2017 |

|

$ | 76,650 |

|

|

$ | (5,867 | ) |

|

$ | 70,783 |

|

|

$ | 2,268 |

|

|

Noteholder 1 |

|

8/26/2016 |

|

8/26/2017 |

|

|

76,650 |

|

|

|

(6,650 | ) |

|

|

70,000 |

|

|

|

588 |

|

|

Noteholder 2 |

|

5/22/2016 |

|

5/23/2017 |

|

|

45,000 |

|

|

|

- |

|

|

|

45,000 |

|

|

|

1,282 |

|

|

Noteholder 3 |

|

3/20/2016 |

|

3/21/2017 |

|

|

27,500 |

|

|

|

(12,959 | ) |

|

|

14,541 |

|

|

|

1,454 |

|

|

Noteholder 3 |

|

5/18/2016 |

|

5/19/2017 |

|

|

76,650 |

|

|

|

(48,510 | ) |

|

|

28,140 |

|

|

|

2,252 |

|

|

Noteholder 3 |

|

9/19/2016 |

|

5/19/2017 |

|

|

76,650 |

|

|

|

(47,510 | ) |

|

|

29,140 |

|

|

|

185 |

|

|

|

|

|

|

|

|

$ | 379,100 |

|

|

$ | (121,496 | ) |

|

$ | 257,604 |

|

|

$ | 8,029 |

|

| 16 |

| Table of Contents |

The following table summarizes all convertible notes outstanding as of December 31, 2016:

|

Holder |

|

Issue Date |

|

Due Date |

|

Principal |

|

|

Unamortized Debt Discount |

|

|

Carrying Value |

|

|

Accrued Interest |

| ||||

|

Noteholder 1 |

|

8/26/2016 |

|

8/26/2017 |

|

|

76,650 |

|

|

|

(4,336 | ) |

|

|

72,314 |

|

|

|

2,137 |

|

|

Noteholder 3 |

|

9/19/2016 |

|

5/19/2017 |

|

|

76,650 |

|

|

|

(28,794 | ) |

|

|

47,856 |

|

|

|

1,730 |

|

|

|

|

|

|

|

|

$ | 153,300 |

|

|

$ | (33,130 | ) |

|

$ | 120,170 |

|

|

$ | 3,867 |

|

Noteholder 1

On May 17, 2016, the Company sold and issued a Convertible Promissory Note to an unrelated party, for the principal amount of $76,650 of which $6,650 was an original issue discount resulting in cash proceeds to the Company of $70,000 pursuant to the terms of a Securities Purchase Agreement of even date therewith. The Note, together with accrued interest at the annual rate of 8%, is due on May 18, 2017. The Note was convertible into the Company's common stock commencing 180 days from the date of issuance at a conversion price equal to 55% of the lowest trade price of the Company's common stock for the twenty prior trading days including the date of conversion. The Company analyzed the conversion feature of the agreement for derivative accounting consideration under ASC 815-15 “Derivatives and Hedging” and determined that the embedded conversion features should be classified as a derivative because the exercise price of these convertible notes are subject to “reset” provisions in the event the Company subsequently issues common stock, stock warrants, stock options or convertible debt with a stock price, exercise price or conversion price lower than conversion price of these notes. If these provisions are triggered, the conversion price of the note will be reduced. The Company has determined that the conversion feature is not considered to be solely indexed to the Company’s own stock and is therefore not afforded equity treatment. In accordance with ASC 815, the Company will bifurcate the conversion feature of the note and record a derivative liability upon the note qualifying for conversion rights on November 17, 2016. The Company may prepay the note during the first six months it is outstanding. During the three months ended December 31, 2016, the noteholder converted all outstanding principal and interest in exchange for a total of 11,157,314 common shares. There was $0 and $76,650 of principal and $0 and $2,268 of accrued interest due at December 31, 2016 and September 30, 2016, respectively.

On May 17, 2016, the Company sold and issued a Convertible Promissory Note to an unrelated party, for the principal amount of $76,650 of which $6,650 was an original issue discount resulting in cash proceeds to the Company of $70,000 which was funded on December 1, 2016 pursuant to the terms of a Securities Purchase Agreement of even date therewith. The Note, together with accrued interest at the annual rate of 8%, is due on May 18, 2017. The Note was convertible into the Company's common stock commencing 180 days from the date of issuance at a conversion price equal to 55% of the lowest trade price of the Company's common stock for the twenty prior trading days including the date of conversion. The Company analyzed the conversion feature of the agreement for derivative accounting consideration under ASC 815-15 “Derivatives and Hedging” and determined that the embedded conversion features should be classified as a derivative because the exercise price of these convertible notes are subject to “reset” provisions in the event the Company subsequently issues common stock, stock warrants, stock options or convertible debt with a stock price, exercise price or conversion price lower than conversion price of these notes. If these provisions are triggered, the conversion price of the note will be reduced. The Company has determined that the conversion feature is not considered to be solely indexed to the Company’s own stock and is therefore not afforded equity treatment. In accordance with ASC 815, the Company bifurcated the conversion feature of the note and recorded a derivative liability upon the note qualifying for conversion rights on December 13, 2016. During the three months ended December 31, 2016, the noteholder converted all outstanding principal and interest in exchange for a total of 7,164,083 common shares. There was $0 and $0 of principal and $0 and $0 of accrued interest due at December 31, 2016 and September 30, 2016, respectively.

On August 26, 2016, the Company sold and issued a Convertible Promissory Note to an unrelated party, for the principal amount of $76,650 of which $6,650 was an original issue discount resulting in cash proceeds to the Company of $70,000 pursuant to the terms of a Securities Purchase Agreement of even date therewith. The Note, together with accrued interest at the annual rate of 8%, is due on August 26, 2017. The Note is convertible into the Company's common stock commencing 180 days from the date of issuance at a conversion price equal to 55% of the lowest trade price of the Company's common stock for the twenty prior trading days including the date of conversion. The Company analyzed the conversion feature of the agreement for derivative accounting consideration under ASC 815-15 “Derivatives and Hedging” and determined that the embedded conversion features should be classified as a derivative because the exercise price of these convertible notes are subject to “reset” provisions in the event the Company subsequently issues common stock, stock warrants, stock options or convertible debt with a stock price, exercise price or conversion price lower than conversion price of these notes. If these provisions are triggered, the conversion price of the note will be reduced. The Company has determined that the conversion feature is not considered to be solely indexed to the Company’s own stock and is therefore not afforded equity treatment. In accordance with ASC 815, the Company will bifurcate the conversion feature of the note and record a derivative liability upon the note qualifying for conversion rights on February 26, 2016. The Company may prepay the note during the first six months it is outstanding. There was $76,650 and $76,650 of principal and $2,137 and $588 of accrued interest due at December 31, 2016 September 30, 2016, respectively.

Noteholder 2

On May 23, 2016, the Company sold and issued a Convertible Promissory Note to an unrelated party, for the principal amount of $45,000 resulting in cash proceeds to the Company of $45,000 pursuant to the terms of a Securities Purchase Agreement of even date therewith. The Note, together with accrued interest at the annual rate of 8%, is due on May 23, 2017. The Note is convertible into the Company's common stock commencing 180 days from the date of issuance at a conversion price equal to 72% of the lowest trade price of the Company's common stock for the ten prior trading days including the date of conversion. The Company analyzed the conversion feature of the agreement for derivative accounting consideration under ASC 815-15 “Derivatives and Hedging” and determined that the embedded conversion features should be classified as a derivative because the exercise price of these convertible notes are subject to “reset” provisions in the event the Company subsequently issues common stock, stock warrants, stock options or convertible debt with a stock price, exercise price or conversion price lower than conversion price of these notes. If these provisions are triggered, the conversion price of the note will be reduced. The Company has determined that the conversion feature is not considered to be solely indexed to the Company’s own stock and is therefore not afforded equity treatment. In accordance with ASC 815, the Company will bifurcate the conversion feature of the note and record a derivative liability upon the note qualifying for conversion rights on November 23, 2016. The Company may prepay the note during the first 90 days it is outstanding for a sum of 115% of the unpaid principal and accrued interest outstanding and within the next 90 days at a rate of 130% of the unpaid principal and accrued interest outstanding. The note may not be prepaid after 180 days from issuance. During the three months ended December 31, 2016, the noteholder elected to convert all outstanding principal and interest due in exchange for a total of 3,334,387 common shares. There was $0 and $45,000 of principal and $0 and $1,282 of accrued interest due at December 31, 2016 and September 30, 2016, respectively.

| 17 |

| Table of Contents |

Noteholder 3