FEDERAL NATIONAL MORTGAGE ASSOCIATION FANNIE MAE - Quarter Report: 2023 September (Form 10-Q)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

☑ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended September 30, 2023

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number: 0-50231

Federal National Mortgage Association

(Exact name of registrant as specified in its charter)

Fannie Mae

Federally chartered corporation | 52-0883107 | 1100 15th Street, NW | 800 | 232-6643 | |||||||||||||||||||||||||

| Washington, | DC | 20005 | |||||||||||||||||||||||||||

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | (Address of principal executive offices, including zip code) | (Registrant’s telephone number, including area code) | ||||||||||||||||||||||||||

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

| None | N/A | N/A | ||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☑ | |||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ☐ | |||||||||||

| Emerging growth company | ☐ | |||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes☐ No ☑

As of October 13, 2023, there were 1,158,087,567 shares of common stock of the registrant outstanding.

| TABLE OF CONTENTS | ||||||||

| Page | ||||||||

| PART I—Financial Information | ||||||||

| Item 1. | ||||||||

| Item 2. | ||||||||

| Introduction | ||||||||

| Executive Summary | ||||||||

| Summary of Our Financial Performance | ||||||||

| Liquidity Provided in the First Nine Months of 2023 | ||||||||

| Key Market Economic Indicators | ||||||||

| Consolidated Results of Operations | ||||||||

Guaranty Book of Business | ||||||||

| Single-Family Mortgage Market | ||||||||

| Single-Family Mortgage-Related Securities Issuances Share | ||||||||

| Single-Family Business Metrics | ||||||||

| Single-Family Business Financial Results | ||||||||

| Single-Family Mortgage Credit Risk Management | ||||||||

| Multifamily Mortgage Market | ||||||||

| Multifamily Business Metrics | ||||||||

| Multifamily Business Financial Results | ||||||||

| Multifamily Mortgage Credit Risk Management | ||||||||

| Consolidated Credit Ratios and Select Credit Information | ||||||||

| Market Risk Management, including Interest-Rate Risk Management | ||||||||

| Critical Accounting Estimates | ||||||||

| Fannie Mae Third Quarter 2023 Form 10-Q | i | |||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| PART II—Other Information | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

| Fannie Mae Third Quarter 2023 Form 10-Q | ii | |||||||

| MD&A | Introduction | ||||||||

PART I—FINANCIAL INFORMATION

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

We have been under conservatorship, with the Federal Housing Finance Agency (“FHFA”) acting as conservator, since September 6, 2008. As conservator, FHFA succeeded to all rights, titles, powers and privileges of the company, and of any shareholder, officer or director of the company with respect to the company and its assets. The conservator has since provided for the exercise of certain functions and authorities by our Board of Directors. Our directors owe their fiduciary duties of care and loyalty solely to the conservator. Thus, while we are in conservatorship, the Board has no fiduciary duties to the company or its stockholders. | ||||||||

We do not know when or how the conservatorship will terminate, what further changes to our business will be made during or following conservatorship, what form we will have and what ownership interest, if any, our current common and preferred stockholders will hold in us after the conservatorship is terminated or whether we will continue to exist following conservatorship. | ||||||||

We are not currently permitted to pay dividends or other distributions to stockholders. Our agreements with the U.S. Department of the Treasury (“Treasury”) include a commitment from Treasury to provide us with funds to maintain a positive net worth under specified conditions; however, the U.S. government does not guarantee our securities or other obligations. Our agreements with Treasury also include covenants that significantly restrict our business activities. For additional information on the conservatorship, the uncertainty of our future, and our agreements with Treasury, see “Business—Conservatorship and Treasury Agreements” and “Risk Factors—GSE and Conservatorship Risk” in our Form 10-K for the year ended December 31, 2022 (“2022 Form 10-K”). | ||||||||

You should read this Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) in conjunction with our unaudited condensed consolidated financial statements and related notes in this report and the more detailed information in our 2022 Form 10-K. You can find a “Glossary of Terms Used in This Report” in MD&A in our 2022 Form 10-K.

Forward-looking statements in this report are based on management’s current expectations and are subject to significant uncertainties and changes in circumstances, as we describe in “Forward-Looking Statements.” Future events and our future results may differ materially from those reflected in our forward-looking statements due to a variety of factors, including those discussed in “Risk Factors” in our 2022 Form 10-K and elsewhere in our 2022 Form 10-K and in this report.

Introduction

Fannie Mae is a leading source of financing for mortgages in the United States. Organized as a government-sponsored enterprise, Fannie Mae is a shareholder-owned corporation. We were chartered by Congress to provide liquidity and stability to the residential mortgage market and to promote access to mortgage credit. Our revenues are primarily driven by guaranty fees we receive for assuming the credit risk on loans underlying the mortgage-backed securities we issue. We do not originate mortgage loans or lend money directly to borrowers. Rather, we work primarily with lenders who originate mortgage loans to borrowers. We acquire and securitize those loans into mortgage-backed securities that we guarantee (which we refer to as Fannie Mae MBS or our MBS).

| Fannie Mae Third Quarter 2023 Form 10-Q | 1 | |||||||

| MD&A | Executive Summary | ||||||||

Executive Summary

Summary of Our Financial Performance

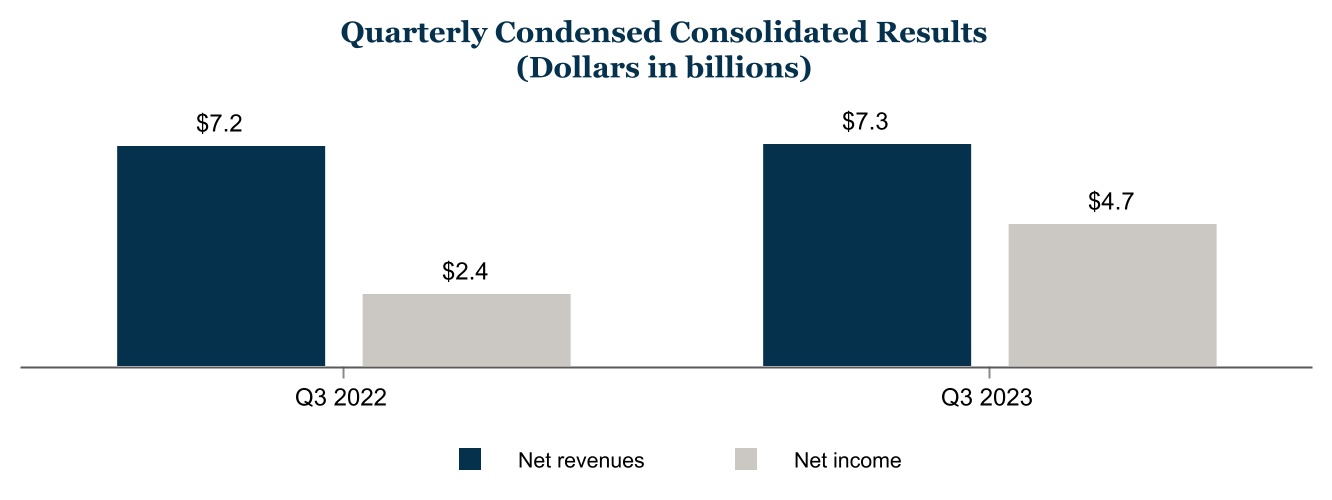

•Net revenues were relatively flat, with an increase of $67 million in the third quarter of 2023 compared with the third quarter of 2022.

•Net income increased $2.3 billion for the third quarter of 2023 compared with the third quarter of 2022, driven primarily by a $3.2 billion shift to benefit for credit losses in the third quarter of 2023 from provision for credit losses in the third quarter of 2022 and a $503 million increase in fair value gains. Our benefit for credit losses for the third quarter of 2023 was driven primarily by increases in actual and forecasted single-family home prices, partially offset by a provision relating to the redesignation of single-family loans from held for investment to held for sale. Fair value gains in the third quarter of 2023 were primarily due to increases in interest rates during the period. The increase in net income was partially offset by an increase in other expenses, net primarily due to $491 million of expense attributable to a jury verdict and an award of prejudgment interest for Fannie Mae preferred shareholders in two cases consolidated for trial in the U.S. District Court for the District of Columbia.

•Net worth increased to $73.7 billion as of September 30, 2023 from $69.0 billion as of June 30, 2023. The increase is attributable to $4.7 billion of comprehensive income for the third quarter of 2023.

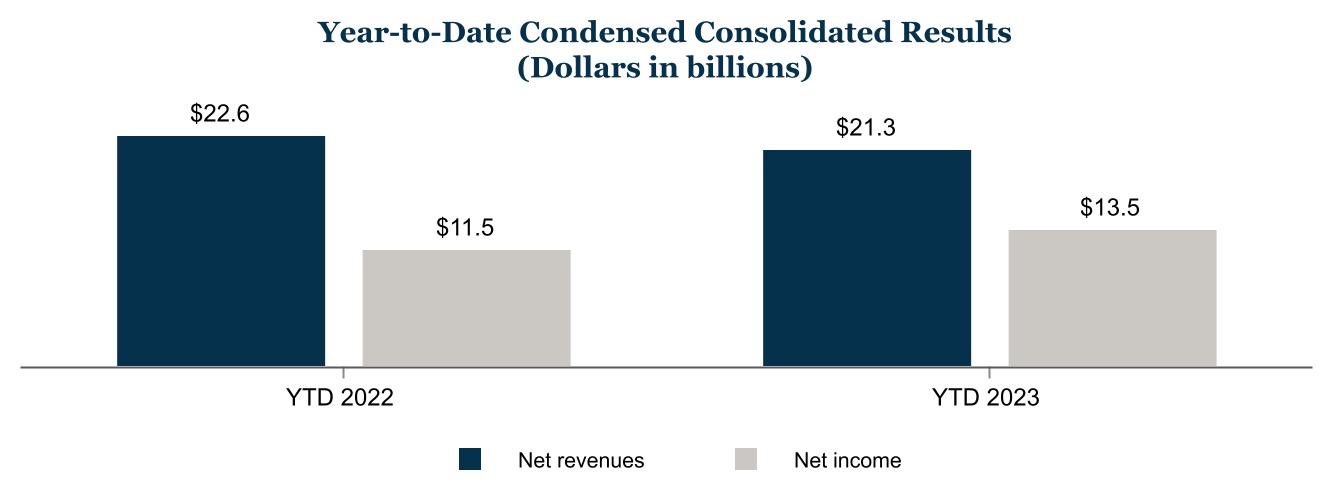

•Net revenues decreased $1.4 billion in the first nine months of 2023 compared with the first nine months of 2022, primarily due to lower net amortization income, partially offset by higher income from portfolios.

| Fannie Mae Third Quarter 2023 Form 10-Q | 2 | |||||||

| MD&A | Executive Summary | ||||||||

◦Lower amortization income was driven by a higher interest-rate environment in the first nine months of 2023, which significantly slowed refinancing activity, driving lower loan prepayment volumes compared with the first nine months of 2022.

◦Higher income from portfolios was primarily driven by higher interest rates in the first nine months of 2023 than in the first nine months of 2022 on assets in our other investments portfolio.

•Net income increased $2.0 billion for the first nine months of 2023 compared with the first nine months of 2022, driven primarily by a $4.8 billion shift to benefit for credit losses in the first nine months of 2023 from provision for credit losses in the first nine months of 2022 due to increases in actual and forecasted single-family home prices, partially offset by lower net revenues as described above.

•Net worth increased to $73.7 billion as of September 30, 2023 from $60.3 billion as of December 31, 2022. The increase is attributable to $13.4 billion of comprehensive income for the first nine months of 2023.

Liquidity Provided in the First Nine Months of 2023

Through our single-family and multifamily business segments, we provided $288 billion in liquidity to the mortgage market in the first nine months of 2023, enabling the financing of approximately 1,154,000 home purchases, refinancings and rental units.

Fannie Mae Provided $288 Billion in Liquidity in the First Nine Months of 2023

| Unpaid Principal Balance | Units | |||||||||||||

| $211B | 621K Single-Family Home Purchases | |||||||||||||

| $35B | 144K Single-Family Refinancings | |||||||||||||

| $42B | 389K Multifamily Rental Units | |||||||||||||

Legislation and Regulation

The information in this section updates and supplements information regarding legislative, regulatory, conservatorship and other developments affecting our business set forth in “Business—Conservatorship and Treasury Agreements” and “Business—Legislation and Regulation” in our 2022 Form 10-K, as well as in “MD&A—Legislation and Regulation” in our Form 10-Q for the quarter ended March 31, 2023 (“First Quarter 2023 Form 10-Q”) and in our Form 10-Q for the quarter ended June 30, 2023 (“Second Quarter 2023 Form 10-Q”). Also see “Risk Factors” in our 2022 Form 10-K for discussions of risks relating to legislative and regulatory matters.

2022 Housing Goals Performance

In October 2023, FHFA notified us that it had determined that we met all of our single-family and multifamily housing goals for 2022. See “Business—Legislation and Regulation—GSE-Focused Matters—Housing Goals” in our 2022 Form 10-K for more information regarding our 2022 housing goals.

| Fannie Mae Third Quarter 2023 Form 10-Q | 3 | |||||||

| MD&A | Key Market Economic Indicators | ||||||||

Key Market Economic Indicators

Below we discuss how varying macroeconomic conditions can influence our financial results across different business and economic environments. Our forecasts and expectations are based on many assumptions, subject to many uncertainties and may change, perhaps substantially, from our current forecasts and expectations. See “Risk Factors” in our 2022 Form 10-K and “Forward-Looking Statements” in this report for a discussion of factors that could cause actual results to differ materially from our current forecasts and expectations. For further discussion on housing activity, see “Single-Family Business—Single-Family Mortgage Market” and “Multifamily Business—Multifamily Mortgage Market.”

Selected Benchmark Interest Rates

(1)Refers to the U.S. weekly average fixed-rate mortgage rate according to Freddie Mac's Primary Mortgage Market Survey®. These rates are reported using the latest available data for a given period.

(2)According to Bloomberg.

(3)Refers to the daily rate per the Federal Reserve Bank of New York.

How Interest Rates Can Affect Our Financial Results

•Net interest income. In a rising interest-rate environment, our mortgage loans generally prepay more slowly as borrowers are less likely to refinance. We amortize various cost basis adjustments over the life of the mortgage loan, including those relating to certain upfront fees we receive at the time we acquire single-family loans. As a result, prepayment of a loan results in an accelerated realization of those upfront fees as income. Therefore, as loan prepayments slow, the accelerated realization of amortization income also slows. Conversely, in a declining interest-rate environment, our mortgage loans generally prepay faster as borrowers are more likely to refinance, typically resulting in the opposite trend of higher amortization income from cost basis adjustments on mortgage loans. Interest rates also affect the amount of interest income we earn on our assets. Our other investments portfolio and our retained mortgage portfolio typically earn more interest income in a higher interest-rate environment and less interest income in a lower interest-rate environment, which, depending on the size of these portfolios, can impact the amount of interest income we recognize during the period. See “Consolidated Results of Operations—Net Interest Income” for a discussion of how interest rate changes impacted our financial results.

•Fair value gains (losses). We have exposure to fair value gains and losses resulting from changes in interest rates, primarily through our mortgage commitment derivatives and risk management derivatives, which we mark to market through earnings. Fair value gains and losses on our mortgage commitment derivatives fluctuate depending on how interest rates and prices move between the time a commitment is opened and when it settles. The net position and composition across the yield curve of our risk management derivatives changes over time. As a result, interest rate changes (increases or decreases) and yield curve changes (parallel, steepening or flattening shifts) will generate varying amounts of fair value gains or losses in a given

| Fannie Mae Third Quarter 2023 Form 10-Q | 4 | |||||||

| MD&A | Key Market Economic Indicators | ||||||||

period. For more information about fair value gains (losses), including the impact of hedge accounting, see “Consolidated Results of Operations—Fair Value Gains, Net.”

•Benefit (provision) for credit losses. When single-family and multifamily mortgage interest rates increase, our expected credit losses on loans increases because (1) we generally expect fewer borrowers will refinance their loans, thereby extending the expected life of the loan, which increases our expectation of loss and (2) borrowers with adjustable-rate loans or multifamily loans with balloon balances due at maturity face increased costs and a reduced ability to refinance. This increase in our expectation of loss contributes to our provision for credit losses. Conversely, when single-family and multifamily mortgage interest rates decrease, our expectation of loss decreases, which reduces our provision for credit losses. For more information on benefit (provision) for credit losses, see “Consolidated Results of Operations—Benefit (Provision) for Credit Losses.”

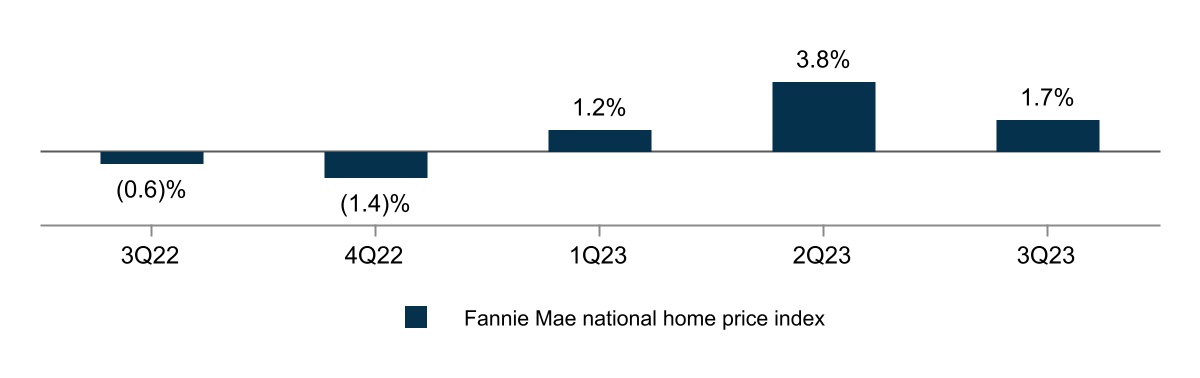

Single-Family Quarterly Home Price Growth (Decline) Rate(1)

(1)Calculated internally using property data on loans purchased by Fannie Mae, Freddie Mac and other third-party home sales data. Fannie Mae’s home price index is a weighted repeat-transactions index, measuring average price changes in repeat sales on the same properties. Fannie Mae’s home price index excludes prices on properties sold in foreclosure. Fannie Mae’s home price growth (decline) rates represent estimates based on non-seasonally adjusted preliminary data and are subject to change as additional data becomes available.

How Home Prices Can Affect Our Financial Results

•Actual and forecasted home prices impact our provision or benefit for credit losses as well as the growth and size of our guaranty book of business.

•Changes in home prices affect the amount of equity that borrowers have in their homes. Borrowers with less equity typically have higher delinquency and default rates, particularly in times of economic stress.

•As home prices increase, the severity of losses we incur on defaulted loans that we hold or guarantee decreases because the amount we can recover from the properties securing the loans increases. Declines in home prices may increase the losses we incur on defaulted loans.

•As home prices rise, the principal balance of loans associated with newly acquired purchase loans may increase, causing growth in the size of our guaranty book. Additionally, rising home prices can increase the amount of equity borrowers have in their home, which may lead to an increase in origination volumes for cash-out refinance loans with higher principal balances than the existing loan. Replacing existing loans with newly acquired cash-out refinances can affect the growth and size of our guaranty book.

•Home prices on a national basis grew by an estimated 6.9% in the first nine months of 2023. We forecast national home price growth of 6.7% for the full year of 2023. We expect regional variation in home price changes.

| Fannie Mae Third Quarter 2023 Form 10-Q | 5 | |||||||

| MD&A | Key Market Economic Indicators | ||||||||

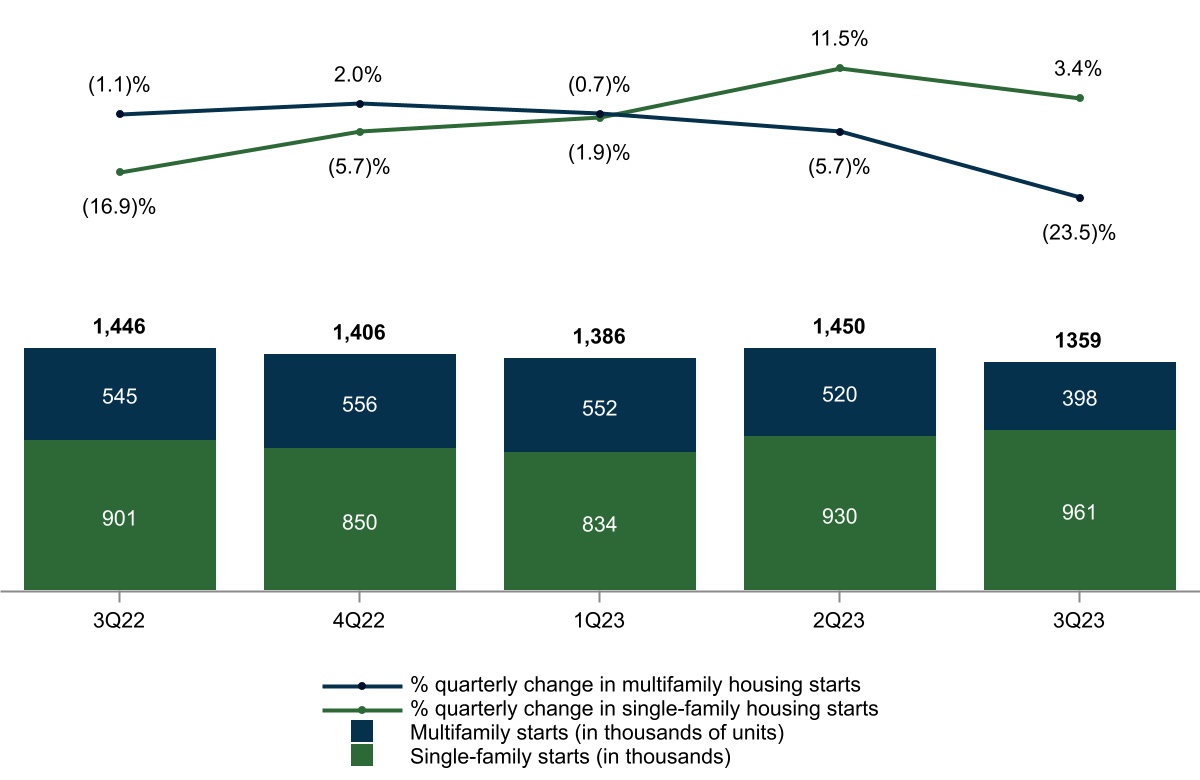

New Housing Starts(1)

(1)According to the U.S. Census Bureau and subject to revision.

How Housing Activity Can Affect Our Financial Results

•Housing is among the most interest-rate sensitive sectors of the economy. In addition to interest rates, two key aspects of economic activity that can impact supply and demand for housing, and thus our business and financial results, are the rates of household formation and housing construction.

•Household formation is a key driver of demand for both single-family and multifamily housing as a newly formed household will either rent or purchase a home. Thus, changes in the pace of household formation can affect home prices, multifamily property values and credit performance as well as the degree of loss on defaulted loans.

•Growth of household formation stimulates homebuilding. Homebuilding has typically been a cyclical leader, weakening prior to a slowdown in U.S. economic activity and accelerating prior to a recovery, which contributes to the growth of U.S. gross domestic product (“GDP”) and employment.

•A decline in housing starts results in fewer new homes being available for purchase and potentially a lower volume of mortgage originations. Construction activity can also affect credit losses through its impact on home prices. If the growth of demand exceeds the growth of supply, prices will appreciate and impact the risk profile of newly originated home purchase mortgages, depending on where in the housing cycle the market is. A reduced pace of construction is often associated with a broader economic slowdown and may signal expected increases in delinquency and losses on defaulted loans.

•We expect further declines in single-family new home construction, new home sales and existing home sales in the near term, given the recent rapid rise in mortgage rates.

| Fannie Mae Third Quarter 2023 Form 10-Q | 6 | |||||||

| MD&A | Key Market Economic Indicators | ||||||||

GDP, Unemployment Rate and Personal Consumption

(1)Real GDP growth (decline) and personal consumption growth (decline) are based on the quarterly series calculated by the Bureau of Economic Analysis and are subject to revision.

(2)According to the U.S. Bureau of Labor Statistics and subject to revision.

How GDP, the Unemployment Rate and Personal Consumption Can Affect Our Financial Results

•Changes in GDP, the unemployment rate and personal consumption can affect several mortgage market factors, including the demand for both single-family and multifamily housing and the level of loan delinquencies, which impacts credit losses.

•Economic growth is a key factor for the performance of mortgage-related assets. In a growing economy, employment and income are typically rising, thus allowing borrowers to meet payment requirements, existing homeowners to consider purchasing and moving to another home, and renters to consider becoming homeowners. Homebuilding typically increases to meet the rise in demand. Mortgage delinquencies typically fall in an expanding economy, thereby decreasing credit losses.

•In a slowing economy, income growth and housing activity typically slow as an early indicator of reduced economic activity, followed by slowing employment. Typically, as an economic slowdown intensifies, households reduce their spending. This reduction in consumption then accelerates the slowdown. An economic slowdown can lead to employment losses, impairing the ability of borrowers and renters to meet mortgage and rental payments, thus causing loan delinquencies to rise. Home sales and mortgage originations also typically fall in a slowing economy.

•GDP increased in the first nine months of 2023. We expect that a modest recession is likely to occur beginning in the first half of 2024, resulting in an increase in the unemployment rate. We expect our economic outlook will be influenced by a number of factors that are subject to change, such as the persistence of inflationary pressures, changes in monetary policy and the risk of financial market disruptions.

•Stress in the banking sector, particularly for regional banks with significant exposure to commercial real estate, could further tighten bank credit conditions, dampen consumer and business confidence, and lead to reduced consumer spending, business investment, and hiring activity.

See “Market and Industry Risk” and “Credit Risk” in “Risk Factors” in our 2022 Form 10-K for further discussion of risks to our business and financial results associated with interest rates, home prices, housing activity, economic conditions, and our reliance on institutional counterparties and mortgage servicers.

| Fannie Mae Third Quarter 2023 Form 10-Q | 7 | |||||||

| MD&A | Consolidated Results of Operations | ||||||||

Consolidated Results of Operations

This section discusses our condensed consolidated results of operations and should be read together with our condensed consolidated financial statements and the accompanying notes.

Summary of Condensed Consolidated Results of Operations | ||||||||||||||||||||||||||||||||||||||

| For the Three Months Ended September 30, | For the Nine Months Ended September 30, | |||||||||||||||||||||||||||||||||||||

| 2023 | 2022 | Variance | 2023 | 2022 | Variance | |||||||||||||||||||||||||||||||||

| (Dollars in millions) | ||||||||||||||||||||||||||||||||||||||

| Net interest income | $ | 7,220 | $ | 7,124 | $ | 96 | $ | 21,041 | $ | 22,331 | $ | (1,290) | ||||||||||||||||||||||||||

Fee and other income(1) | 76 | 105 | (29) | 209 | 269 | (60) | ||||||||||||||||||||||||||||||||

| Net revenues | 7,296 | 7,229 | 67 | 21,250 | 22,600 | (1,350) | ||||||||||||||||||||||||||||||||

| Investment gains (losses), net | 8 | (172) | 180 | (34) | (323) | 289 | ||||||||||||||||||||||||||||||||

| Fair value gains, net | 795 | 292 | 503 | 1,403 | 1,301 | 102 | ||||||||||||||||||||||||||||||||

| Administrative expenses | (897) | (870) | (27) | (2,629) | (2,473) | (156) | ||||||||||||||||||||||||||||||||

| Benefit (provision) for credit losses | 652 | (2,536) | 3,188 | 1,786 | (2,994) | 4,780 | ||||||||||||||||||||||||||||||||

TCCA fees(2) | (860) | (850) | (10) | (2,571) | (2,515) | (56) | ||||||||||||||||||||||||||||||||

Credit enhancement expense(3) | (390) | (364) | (26) | (1,115) | (974) | (141) | ||||||||||||||||||||||||||||||||

Change in expected credit enhancement recoveries(4) | (128) | 290 | (418) | (168) | 303 | (471) | ||||||||||||||||||||||||||||||||

Other expenses, net(5) | (535) | (154) | (381) | (922) | (612) | (310) | ||||||||||||||||||||||||||||||||

| Income before federal income taxes | 5,941 | 2,865 | 3,076 | 17,000 | 14,313 | 2,687 | ||||||||||||||||||||||||||||||||

| Provision for federal income taxes | (1,242) | (429) | (813) | (3,535) | (2,816) | (719) | ||||||||||||||||||||||||||||||||

| Net income | $ | 4,699 | $ | 2,436 | $ | 2,263 | $ | 13,465 | $ | 11,497 | $ | 1,968 | ||||||||||||||||||||||||||

| Total comprehensive income | $ | 4,681 | $ | 2,433 | $ | 2,248 | $ | 13,448 | $ | 11,483 | $ | 1,965 | ||||||||||||||||||||||||||

(1)Single-family fee and other income consists primarily of compensation for engaging in structured transactions and providing other lender services. Multifamily fee and other income consists of fees associated with certain Multifamily business activities such as credit enhancements for tax-exempt multifamily housing revenue bonds.

(2)TCCA fees refers to the expense recognized as a result of the 10 basis point increase in guaranty fees on all single-family residential mortgages delivered to us on or after April 1, 2012 pursuant to the Temporary Payroll Tax Cut Continuation Act of 2011 and as extended by the Infrastructure Investment and Jobs Act, which we remit to Treasury. For more information on TCCA fees, see “Note 1, Summary of Significant Accounting Policies—Related Parties—Transactions with Treasury” in our 2022 Form 10-K.

(3)Consists of costs associated with our freestanding credit enhancements, which primarily include our Connecticut Avenue Securities® (“CAS”) and Credit Insurance Risk TransferTM (“CIRTTM”) programs, enterprise-paid mortgage insurance and certain lender risk-sharing programs.

(4)Includes estimated changes in benefits, as well as any realized amounts, from our freestanding credit enhancements.

(5)Consists of debt extinguishment gains and losses, expenses associated with legal claims, foreclosed property income (expense), gains and losses from partnership investments, housing trust fund expenses, loan subservicing costs, and servicer fees paid in connection with certain loss mitigation activities.

Net Interest Income

Our primary source of net interest income is guaranty fees we receive for managing the credit risk on loans underlying Fannie Mae MBS held by third parties.

Guaranty fees consist of two primary components:

•base guaranty fees that we receive over the life of the loan; and

•upfront fees that we receive at the time of loan acquisition primarily related to single-family loan-level price adjustments and other fees we receive from lenders, which are amortized into net interest income as cost basis adjustments over the contractual life of the loan. We refer to this as amortization income.

We recognize almost all of our guaranty fee revenue in net interest income because we consolidate the substantial majority of loans underlying our Fannie Mae MBS in consolidated trusts in our condensed consolidated balance sheets. Guaranty fees from these loans account for the difference between the interest income on loans in consolidated trusts and the interest expense on the debt of consolidated trusts.

| Fannie Mae Third Quarter 2023 Form 10-Q | 8 | |||||||

| MD&A | Consolidated Results of Operations | ||||||||

The timing of when we recognize the upfront fees received on loan acquisitions as amortization income can vary based on a number of factors, the most significant of which is a change in mortgage interest rates. Although we amortize these upfront fees over the contractual life of the mortgage loan, when a loan prepays, the remaining upfront fees on the loan are recognized as income in that period. As a result, in a declining interest-rate environment, our mortgage loans generally prepay faster as borrowers are more likely to refinance, typically resulting in higher amortization income as it accelerates the realization of those upfront fees as income. Conversely, in a rising interest-rate environment, our mortgage loans generally prepay more slowly as borrowers are less likely to refinance, which typically results in lower amortization income as those upfront fees are amortized over a longer period of time.

We also recognize net interest income on the difference between interest income earned on the assets in our retained mortgage portfolio and our other investments portfolio (collectively, our “portfolios”) and the interest expense associated with the debt that funds those assets. See “Retained Mortgage Portfolio” and “Liquidity and Capital Management—Liquidity Management—Other Investments Portfolio” for more information about our portfolios.

We recognize the effects of hedge accounting as a component of net interest income, as demonstrated in the table below. As of September 30, 2023, we had $3.6 billion in net cumulative fair value hedge basis adjustments, which will be amortized as net expenses over the remaining contractual life of the respective hedged items in the “Income (expense) from hedge accounting” line item in the table below. The substantial majority of these hedge basis adjustments relate to our funding debt. See “Fair Value Gains, Net” below and “Note 8, Derivative Instruments” in this report for more information about our hedge accounting program, as well as “Note 1, Summary of Significant Accounting Policies” in our 2022 Form 10-K.

The table below displays the components of our net interest income from our guaranty book of business, which we discuss in “Guaranty Book of Business,” and from our portfolios, as well as from hedge accounting.

| Components of Net Interest Income | ||||||||||||||||||||||||||||||||||||||

| For the Three Months Ended September 30, | For the Nine Months Ended September 30, | |||||||||||||||||||||||||||||||||||||

| 2023 | 2022 | Variance | 2023 | 2022 | Variance | |||||||||||||||||||||||||||||||||

(Dollars in millions) | ||||||||||||||||||||||||||||||||||||||

Net interest income from guaranty book of business: | ||||||||||||||||||||||||||||||||||||||

Base guaranty fee income(1) | $ | 4,060 | $ | 4,116 | $ | (56) | $ | 12,077 | $ | 12,091 | $ | (14) | ||||||||||||||||||||||||||

Base guaranty fee income related to TCCA(2) | 860 | 850 | 10 | 2,571 | 2,515 | 56 | ||||||||||||||||||||||||||||||||

Net amortization income(3) | 942 | 1,429 | (487) | 2,611 | 5,924 | (3,313) | ||||||||||||||||||||||||||||||||

Total net interest income from guaranty book of business | 5,862 | 6,395 | (533) | 17,259 | 20,530 | (3,271) | ||||||||||||||||||||||||||||||||

Net interest income from portfolios(4) | 1,596 | 794 | 802 | 4,554 | 1,747 | 2,807 | ||||||||||||||||||||||||||||||||

Income (expense) from hedge accounting | (238) | (65) | (173) | (772) | 54 | (826) | ||||||||||||||||||||||||||||||||

Total net interest income | $ | 7,220 | $ | 7,124 | $ | 96 | $ | 21,041 | $ | 22,331 | $ | (1,290) | ||||||||||||||||||||||||||

| Income (expense) from hedge accounting included in net interest income: | ||||||||||||||||||||||||||||||||||||||

| Fair value gains (losses) on designated risk management derivatives in fair value hedges | $ | 494 | $ | (1,020) | $ | 1,514 | $ | 341 | $ | (2,548) | $ | 2,889 | ||||||||||||||||||||||||||

Fair value gains (losses) on hedged mortgage loans held for investment and debt of Fannie Mae(5) | (368) | 1,192 | (1,560) | 95 | 2,981 | (2,886) | ||||||||||||||||||||||||||||||||

Contractual interest income (expense) accruals related to interest-rate swaps designated as hedging instruments | (155) | (101) | (54) | (624) | (64) | (560) | ||||||||||||||||||||||||||||||||

| Discontinued hedge-related basis adjustment amortization | (209) | (136) | (73) | (584) | (315) | (269) | ||||||||||||||||||||||||||||||||

| Total income (expense) from hedge accounting in net interest income | $ | (238) | $ | (65) | $ | (173) | $ | (772) | $ | 54 | $ | (826) | ||||||||||||||||||||||||||

| Fannie Mae Third Quarter 2023 Form 10-Q | 9 | |||||||

| MD&A | Consolidated Results of Operations | ||||||||

(1)Excludes revenues generated by the 10 basis point guaranty fee increase we implemented pursuant to the TCCA, the incremental revenue from which is remitted to Treasury and not retained by us.

(2)Represents revenues generated by the 10 basis point guaranty fee increase we implemented pursuant to the TCCA, the incremental revenue from which is remitted to Treasury and not retained by us.

(3)Net amortization income refers primarily to the net amortization of premiums and discounts on mortgage loans and debt of consolidated trusts. These cost basis adjustments represent the difference between the initial fair value and the carrying value of these instruments as well as upfront fees we receive at the time of loan acquisition. It does not include the amortization of cost basis adjustments resulting from hedge accounting, which is included in income (expense) from hedge accounting.

(4)Includes interest expense associated with our outstanding Connecticut Avenue Securities debt.

(5)Amounts are recorded as cost basis adjustments on the hedged loans or debt and amortized over the hedged item’s remaining contractual life beginning at the termination of the hedging relationship. See “Note 8, Derivative Instruments” for additional information on the effect of our fair value hedge accounting program and related disclosures.

Net interest income was relatively flat in the third quarter of 2023 compared with the third quarter of 2022. The primary offsetting drivers of net interest income were higher income from portfolios offset by lower net amortization income. Net interest income decreased in the first nine months of 2023 compared with the first nine months of 2022, primarily as a result of lower net amortization income partially offset by higher income from portfolios. More specifically, our net interest income was impacted in the periods by:

•Lower net amortization income. Throughout the third quarter and first nine months of 2023, we were in a higher interest-rate environment and observed significantly lower volumes of refinancing activity compared with the third quarter and first nine months of 2022, which drove fewer loan prepayments. As a result, we had lower amortization income in the third quarter and first nine months of 2023 compared with the third quarter and first nine months of 2022.

•Higher income from portfolios. Higher income from portfolios in the third quarter and first nine months of 2023 compared with the third quarter and first nine months of 2022 was primarily driven by higher interest rates in the first nine months of 2023 than in the first nine months of 2022 on securities in our other investments portfolio, primarily U.S. Treasuries and securities purchased under agreements to resell. This was partially offset by higher interest expense on funding debt, also as a result of higher interest rates. See “Liquidity and Capital Management—Liquidity Management—Other Investments Portfolio” for more information about our other investments portfolio.

As of September 28, 2023, the U.S. weekly average interest rate for a single-family 30-year fixed-rate mortgage was 7.31%, according to Freddie Mac’s Primary Mortgage Market Survey®. As of September 30, 2023, nearly 90% of our single-family conventional guaranty book of business had an interest rate below 5.50%, resulting in a low likelihood these loans would refinance at current rates. In addition, approximately 70% of our single-family conventional guaranty book of business as of September 30, 2023 had an interest rate below 4.00%. Accordingly, even if interest rates decline meaningfully from current levels, most of the borrowers whose loans are in our single-family conventional guaranty book of business still would not be incentivized to refinance.

| Fannie Mae Third Quarter 2023 Form 10-Q | 10 | |||||||

| MD&A | Consolidated Results of Operations | ||||||||

Analysis of Net Interest Income

The following tables display an analysis of our net interest income, average balances and related yields earned on assets and incurred on liabilities. For most components of the average balances, we use a daily weighted average of unpaid principal balance net of unamortized cost basis adjustments. When daily average balance information is not available, such as for mortgage loans, we use monthly averages.

Analysis of Net Interest Income and Yield(1) | ||||||||||||||||||||||||||||||||||||||

| For the Three Months Ended September 30, | ||||||||||||||||||||||||||||||||||||||

| 2023 | 2022 | |||||||||||||||||||||||||||||||||||||

Average Balance | Interest Income/ (Expense) | Average Rates Earned/Paid | Average Balance | Interest Income/ (Expense) | Average Rates Earned/Paid | |||||||||||||||||||||||||||||||||

(Dollars in millions) | ||||||||||||||||||||||||||||||||||||||

Interest-earning assets: | ||||||||||||||||||||||||||||||||||||||

Mortgage loans of Fannie Mae | $ | 51,802 | $ | 615 | 4.75 | % | $ | 58,290 | $ | 628 | 4.31 | % | ||||||||||||||||||||||||||

Mortgage loans of consolidated trusts | 4,086,890 | 33,096 | 3.24 | 4,048,625 | 29,486 | 2.91 | ||||||||||||||||||||||||||||||||

Total mortgage loans(2) | 4,138,692 | 33,711 | 3.26 | 4,106,915 | 30,114 | 2.93 | ||||||||||||||||||||||||||||||||

Investments in securities(3) | 111,192 | 1,075 | 3.87 | 108,621 | 525 | 1.93 | ||||||||||||||||||||||||||||||||

Securities purchased under agreements to resell | 41,570 | 563 | 5.42 | 30,829 | 171 | 2.22 | ||||||||||||||||||||||||||||||||

Advances to lenders | 3,973 | 66 | 6.64 | 4,935 | 40 | 3.24 | ||||||||||||||||||||||||||||||||

Total interest-earning assets | $ | 4,295,427 | $ | 35,415 | 3.30 | % | $ | 4,251,300 | $ | 30,850 | 2.90 | % | ||||||||||||||||||||||||||

Interest-bearing liabilities: | ||||||||||||||||||||||||||||||||||||||

Short-term funding debt | $ | 15,388 | $ | (201) | 5.22 | % | $ | 3,695 | $ | (17) | 1.84 | % | ||||||||||||||||||||||||||

Long-term funding debt | 111,351 | (942) | 3.38 | 122,571 | (635) | 2.07 | ||||||||||||||||||||||||||||||||

CAS debt | 3,702 | (100) | 10.80 | 7,221 | (126) | 6.98 | ||||||||||||||||||||||||||||||||

Total debt of Fannie Mae | 130,441 | (1,243) | 3.81 | 133,487 | (778) | 2.33 | ||||||||||||||||||||||||||||||||

Debt securities of consolidated trusts held by third parties | 4,087,136 | (26,952) | 2.64 | 4,055,958 | (22,948) | 2.26 | ||||||||||||||||||||||||||||||||

Total interest-bearing liabilities | $ | 4,217,577 | $ | (28,195) | 2.67 | % | $ | 4,189,445 | $ | (23,726) | 2.27 | % | ||||||||||||||||||||||||||

Net interest income/net interest yield | $ | 7,220 | 0.67 | % | $ | 7,124 | 0.67 | % | ||||||||||||||||||||||||||||||

| Fannie Mae Third Quarter 2023 Form 10-Q | 11 | |||||||

| MD&A | Consolidated Results of Operations | ||||||||

| For the Nine Months Ended September 30, | ||||||||||||||||||||||||||||||||||||||

| 2023 | 2022 | |||||||||||||||||||||||||||||||||||||

Average Balance | Interest Income/ (Expense) | Average Rates Earned/Paid | Average Balance | Interest Income/ (Expense) | Average Rates Earned/Paid | |||||||||||||||||||||||||||||||||

(Dollars in millions) | ||||||||||||||||||||||||||||||||||||||

Interest-earning assets: | ||||||||||||||||||||||||||||||||||||||

Mortgage loans of Fannie Mae | $ | 52,179 | $ | 1,833 | 4.68 | % | $ | 62,460 | $ | 2,202 | 4.70 | % | ||||||||||||||||||||||||||

Mortgage loans of consolidated trusts | 4,078,981 | 96,670 | 3.16 | 4,004,225 | 84,136 | 2.80 | ||||||||||||||||||||||||||||||||

Total mortgage loans(2) | 4,131,160 | 98,503 | 3.18 | 4,066,685 | 86,338 | 2.83 | ||||||||||||||||||||||||||||||||

Investments in securities(3) | 114,964 | 3,157 | 3.62 | 134,028 | 1,009 | 0.99 | ||||||||||||||||||||||||||||||||

Securities purchased under agreements to resell | 39,834 | 1,505 | 4.98 | 22,495 | 205 | 1.20 | ||||||||||||||||||||||||||||||||

Advances to lenders | 3,379 | 160 | 6.24 | 5,800 | 93 | 2.11 | ||||||||||||||||||||||||||||||||

Total interest-earning assets | $ | 4,289,337 | $ | 103,325 | 3.21 | % | $ | 4,229,008 | $ | 87,645 | 2.76 | % | ||||||||||||||||||||||||||

Interest-bearing liabilities: | ||||||||||||||||||||||||||||||||||||||

Short-term funding debt | $ | 13,628 | $ | (503) | 4.87 | % | $ | 3,909 | $ | (23) | 0.78 | % | ||||||||||||||||||||||||||

Long-term funding debt | 116,433 | (2,686) | 3.08 | 146,165 | (1,724) | 1.57 | ||||||||||||||||||||||||||||||||

CAS debt | 4,381 | (332) | 10.10 | 9,358 | (373) | 5.31 | ||||||||||||||||||||||||||||||||

Total debt of Fannie Mae | 134,442 | (3,521) | 3.49 | 159,432 | (2,120) | 1.77 | ||||||||||||||||||||||||||||||||

Debt securities of consolidated trusts held by third parties | 4,081,140 | (78,763) | 2.57 | 4,016,013 | (63,194) | 2.10 | ||||||||||||||||||||||||||||||||

Total interest-bearing liabilities | $ | 4,215,582 | $ | (82,284) | 2.60 | % | $ | 4,175,445 | $ | (65,314) | 2.09 | % | ||||||||||||||||||||||||||

Net interest income/net interest yield | $ | 21,041 | 0.65 | % | $ | 22,331 | 0.70 | % | ||||||||||||||||||||||||||||||

(1) Includes the effects of discounts, premiums and other cost basis adjustments.

(2) Average balance includes mortgage loans on nonaccrual status. Interest income includes loan fee revenue of $722 million and $2.1 billion, respectively, for the third quarter of 2023 and first nine months of 2023, compared with $1.1 billion and $4.4 billion, respectively, for the third quarter of 2022 and first nine months of 2022. Loan fees primarily consist of yield maintenance revenue we recognized on the prepayment of multifamily mortgage loans and the amortization of upfront cash fees exchanged when we acquire the loan.

(3) Consists of cash, cash equivalents, U.S. Treasury securities and mortgage-related securities.

Deferred Amortization Income

We initially recognize mortgage loans and debt of consolidated trusts in our condensed consolidated balance sheets at fair value. The difference between the initial fair value and the carrying value of these instruments is recorded as a cost basis adjustment, either as a premium or a discount, in our condensed consolidated balance sheets. We amortize these cost basis adjustments over the contractual lives of the loans or debt. Although we are in a net premium position for both mortgage loans and debt of consolidated trusts, we have a greater amount of premiums with respect to debt of consolidated trusts, which represents deferred income we will recognize in our condensed consolidated statements of operations and comprehensive income as amortization income in future periods.

Deferred Amortization Income Represented by Net Premium Position

on Debt of Consolidated Trusts

(Dollars in billions)

| Fannie Mae Third Quarter 2023 Form 10-Q | 12 | |||||||

| MD&A | Consolidated Results of Operations | ||||||||

Fair Value Gains, Net

The estimated fair value of our derivatives, trading securities and other financial instruments carried at fair value may fluctuate substantially from period to period because of changes in interest rates, the yield curve, spreads and implied volatility, as well as activity related to these financial instruments.

We apply fair value hedge accounting to reduce earnings volatility in our financial statements driven by changes in benchmark interest rates. Accordingly, we recognize the fair value gains and losses and the contractual interest income and expense associated with risk management derivatives designated in qualifying hedging relationships in net interest income. For more information about our hedge accounting program, see “Impact of Hedge Accounting on Fair Value Gains (Losses), Net” below and “Note 8, Derivative Instruments” in this report, as well as “Market Risk Management, including Interest-Rate Risk Management” and “Note 1, Summary of Significant Accounting Policies” in our 2022 Form 10-K.

The table below displays the components of our fair value gains and losses.

| Fair Value Gains, Net | ||||||||||||||||||||||||||

| For the Three Months Ended September 30, | For the Nine Months Ended September 30, | |||||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | |||||||||||||||||||||||

| (Dollars in millions) | ||||||||||||||||||||||||||

Risk management derivatives fair value gains (losses) attributable to: | ||||||||||||||||||||||||||

| Net contractual interest expense on interest-rate swaps | $ | (348) | $ | (164) | $ | (1,123) | $ | (166) | ||||||||||||||||||

| Net change in fair value during the period | 852 | (433) | 1,544 | (2,135) | ||||||||||||||||||||||

Impact of hedge accounting(1) | (339) | 1,121 | 283 | 2,612 | ||||||||||||||||||||||

| Risk management derivatives fair value gains, net | 165 | 524 | 704 | 311 | ||||||||||||||||||||||

| Mortgage commitment derivatives fair value gains, net | 591 | 517 | 675 | 2,933 | ||||||||||||||||||||||

| Credit enhancement derivatives fair value gains (losses), net | 47 | (32) | 61 | (83) | ||||||||||||||||||||||

| Total derivatives fair value gains, net | 803 | 1,009 | 1,440 | 3,161 | ||||||||||||||||||||||

| Trading securities losses, net | (318) | (1,319) | (295) | (3,754) | ||||||||||||||||||||||

| Long-term debt fair value gains, net | 406 | 787 | 356 | 2,424 | ||||||||||||||||||||||

Other, net(2) | (96) | (185) | (98) | (530) | ||||||||||||||||||||||

| Fair value gains, net | $ | 795 | $ | 292 | $ | 1,403 | $ | 1,301 | ||||||||||||||||||

(1)The “Impact of hedge accounting” reflected in this table shows the net gain or loss from swaps in hedging relationships plus any accrued interest during the applicable periods.

(2)Consists primarily of fair value gains and losses on mortgage loans held at fair value.

Fair value gains, net in the third quarter and first nine months of 2023 were primarily driven by gains on mortgage commitment derivatives, risk management derivatives, and long-term debt of consolidated trusts held at fair value, primarily due to rising interest rates.

These gains were partially offset by the impact of declining prices of fixed-rate trading securities, primarily driven by rising interest rates.

Fair value gains, net in the third quarter and first nine months of 2022 were primarily driven by:

•increases in the fair value of mortgage commitment derivatives due to gains on commitments to sell mortgage-related securities as prices decreased during the commitment period due to rising interest rates and widening of the secondary spread, which is the spread between the 30-year MBS current coupon yield and the 10-year U.S. Treasury rate; and

•gains associated with decreases in the fair value of long-term debt of consolidated trusts held at fair value, also due to rising interest rates and widening of the secondary spread.

These gains were partially offset by fair value losses in the third quarter and first nine months of 2022 on trading securities, primarily driven by increases in U.S. Treasury yields, which resulted in losses on fixed-rate securities held in our other investments portfolio.

| Fannie Mae Third Quarter 2023 Form 10-Q | 13 | |||||||

| MD&A | Consolidated Results of Operations | ||||||||

Impact of Hedge Accounting on Fair Value Gains (Losses), Net

Our earnings can experience volatility due to interest-rate changes and differing accounting treatments that apply to certain financial instruments on our balance sheet. To help address this volatility, we apply hedge accounting to reduce the current-period impact on our earnings related to changes in specified benchmark interest rates. Hedge accounting aligns the timing of when we recognize fair value changes in hedged items attributable to these benchmark interest-rate movements with fair value changes in the hedging instrument.

The table below displays the amount of contractual interest accruals and fair value gains and losses related to designated interest-rate swaps in qualifying hedging relationships that are recognized in “Net interest income” rather than “Fair value gains, net” in our condensed consolidated statements of operations and comprehensive income as a result of hedge accounting. Derivatives not in hedging relationships are not affected.

| Impact of Hedge Accounting on Fair Value Gains (Losses), Net | ||||||||||||||||||||||||||

| For the Three Months Ended September 30, | For the Nine Months Ended September 30, | |||||||||||||||||||||||||

2023 | 2022 | 2023 | 2022 | |||||||||||||||||||||||

| (Dollars in millions) | ||||||||||||||||||||||||||

| Net contractual interest expense accruals related to interest-rate swaps designated as hedging instruments recognized in net interest income | $ | (155) | $ | (101) | $ | (624) | $ | (64) | ||||||||||||||||||

| Fair value gains (losses) on derivatives designated as hedging instruments recognized in net interest income | 494 | (1,020) | 341 | (2,548) | ||||||||||||||||||||||

| Fair value gains (losses), net recognized in net interest income (expense) from hedge accounting | $ | 339 | $ | (1,121) | $ | (283) | $ | (2,612) | ||||||||||||||||||

Interest expense accruals and fair value gains in the third quarter and first nine months of 2023 were primarily affected by changes in the composition of financial instruments in our fair value portfolio and rising interest rates. For additional information on our hedge accounting program, see “Risk Management—Market Risk Management, including Interest-Rate Risk Management—Earnings Exposure to Interest-Rate Risk” in our 2022 Form 10-K and in this report and “Note 8, Derivative Instruments” in this report. For additional discussion of our fair value hedge accounting policy, see “Note 1, Summary of Significant Accounting Policies” in our 2022 Form 10-K.

Benefit (Provision) for Credit Losses

Our benefit or provision for credit losses can vary substantially from period to period based on a number of factors, such as changes in actual and forecasted home prices or property valuations, fluctuations in actual and forecasted interest rates, borrower payment behavior, events such as natural disasters or pandemics, the types, volume and effectiveness of our loss mitigation activities, including forbearances and loan modifications, the volume of foreclosures completed and the volume and pricing of loans redesignated from held for investment (“HFI”) to held for sale (“HFS”). The benefit or provision for credit losses includes our benefit or provision for loan losses, accrued interest receivable losses, our guaranty loss reserves and credit losses on our available-for-sale (“AFS”) debt securities.

Our benefit or provision for credit losses and our related loss reserves can also be impacted by updates to the models, assumptions and data used in determining our allowance for loan losses. Although we believe the estimates underlying our allowance as of September 30, 2023 are reasonable, they are subject to uncertainty. Changes in future economic conditions and loan performance from our current expectations may result in volatility in our allowance for loan losses and, as a result, our benefit or provision for credit losses. See “Critical Accounting Estimates” for additional information about how our estimate of credit losses is subject to uncertainty.

| Fannie Mae Third Quarter 2023 Form 10-Q | 14 | |||||||

| MD&A | Consolidated Results of Operations | ||||||||

The table below provides a quantitative analysis of the drivers of our single-family and multifamily benefit or provision for credit losses and the change in expected credit enhancement recoveries. Many of the drivers that contribute to our benefit or provision for credit losses overlap or are interdependent. The attribution shown below is based on internal allocation estimates.

Components of Benefit (Provision) for Credit Losses and Change in Expected Credit Enhancement Recoveries | ||||||||||||||||||||||||||

| For the Three Months Ended September 30, | For the Nine Months Ended September 30, | |||||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | |||||||||||||||||||||||

(Dollars in millions) | ||||||||||||||||||||||||||

Single-family benefit (provision) for credit losses: | ||||||||||||||||||||||||||

Changes in loan activity(1) | $ | (335) | $ | (373) | $ | (1,075) | $ | (964) | ||||||||||||||||||

Redesignation of loans from HFI to HFS | (591) | (116) | (591) | (120) | ||||||||||||||||||||||

Actual and forecasted home prices | 1,901 | (1,732) | 4,005 | (1,194) | ||||||||||||||||||||||

Actual and projected interest rates | (260) | (225) | (284) | (1,116) | ||||||||||||||||||||||

Release of economic concessions(2) | 16 | 155 | 60 | 758 | ||||||||||||||||||||||

Other(3) | 5 | (70) | 86 | (201) | ||||||||||||||||||||||

Single-family benefit (provision) for credit losses | 736 | (2,361) | 2,201 | (2,837) | ||||||||||||||||||||||

Multifamily benefit (provision) for credit losses: | ||||||||||||||||||||||||||

Changes in loan activity(1) | (103) | (65) | (187) | (54) | ||||||||||||||||||||||

Actual and projected interest rates | (242) | (97) | (234) | (258) | ||||||||||||||||||||||

Actual and projected economic data(4) | 234 | (3) | (69) | 85 | ||||||||||||||||||||||

Other(3) | 27 | (10) | 75 | 70 | ||||||||||||||||||||||

Multifamily benefit (provision) for credit losses | (84) | (175) | (415) | (157) | ||||||||||||||||||||||

Total benefit (provision) for credit losses(5) | $ | 652 | $ | (2,536) | $ | 1,786 | $ | (2,994) | ||||||||||||||||||

Change in expected credit enhancement recoveries for active loans: | ||||||||||||||||||||||||||

Single-family | $ | (170) | $ | 245 | $ | (298) | $ | 271 | ||||||||||||||||||

Multifamily | 41 | 45 | 122 | 32 | ||||||||||||||||||||||

Change in expected credit enhancement recoveries for active loans | $ | (129) | $ | 290 | $ | (176) | $ | 303 | ||||||||||||||||||

(1)Primarily consists of loan acquisitions, liquidations and amortization of modification concessions granted to borrowers and write-offs of amounts determined to be uncollectible. For multifamily, “Changes in loan activity” also includes changes in the allowance due to loan delinquencies and the impact of changes in debt service coverage ratios (“DSCRs”) based on updated property financial information, which is used to assess loan credit quality.

(2)Represents the benefit from the release of economic concessions related to loans previously designated as troubled debt restructurings (“TDRs”) that received loss mitigation arrangements during the period.

(3)Includes provision for allowance on accrued interest receivable. For single-family, also includes any benefit or provision for our guaranty loss reserves that are not separately included in the other components.

(4)Primarily consists of changes attributed to projected property net operating income, actual and projected property values, and labor market forecasts.

(5)For purposes of this attribution table, credit losses on AFS securities are excluded.

| Fannie Mae Third Quarter 2023 Form 10-Q | 15 | |||||||

| MD&A | Consolidated Results of Operations | ||||||||

Single-Family Benefit (Provision) for Credit Losses

Our single-family benefit for credit losses in the third quarter and first nine months of 2023 was primarily driven by a benefit from actual and forecasted home price growth, partially offset by a provision relating to the redesignation of loans from HFI to HFS and a provision from changes in loan activity, as described below:

•Benefit from actual and forecasted home price growth. During the third quarter and first nine months of 2023, we observed stronger than expected actual and forecasted home price appreciation. Higher home prices decrease the likelihood that loans will default and reduce the amount of losses on loans that do default, which impacts our estimate of losses and ultimately reduces our loss reserves and provision for credit losses. See “Key Market Economic Indicators” for additional information about how home prices affect our credit loss estimates, including a discussion of home price growth and declines, and our home price forecast. Also see “Critical Accounting Estimates” for more information about our home price forecast.

•Provision from redesignation of loans from HFI to HFS. We redesignated certain nonperforming and reperforming single-family loans from HFI to HFS, as we no longer intended to hold them for the foreseeable future or to maturity. Upon redesignation of these loans, we recorded the loans at the lower of cost or fair value with a write-off against the allowance for loan losses. During the third quarter of 2023, we redesignated loans with an amortized cost of $3.1 billion with an associated write-off against the allowance for loan losses of $638 million. Interest rates on the redesignated loans were below current market interest rates, and as a result, we recorded additional provision for credit losses to the extent that the carrying value of the loans exceeded their fair value at the time of redesignation.

•Provision from changes in loan activity, which includes provision on newly acquired loans. The portion of our single-family acquisitions consisting of purchase loans increased in the third quarter and first nine months of 2023 compared with the third quarter and first nine months of 2022. As our acquisitions consisted of a greater percentage of purchase loans, which generally have higher origination loan to value (“LTV”) ratios than refinance loans, the credit profile of our acquisitions weakened. This factor drove a higher estimated risk of default and loss severity in the allowance and therefore a higher credit loss provision for those loans at the time of acquisition. See “Single-Family Business—Single-Family Mortgage Credit Risk Management” for more information on our single-family loan acquisitions in the third quarter and first nine months of 2023.

Our single-family provision for credit losses in the third quarter of 2022 was primarily driven by a provision from actual and forecasted home prices. Actual home prices declined slightly on a national basis in the third quarter of 2022. In addition, our home price forecast worsened compared with the second quarter of 2022. While our second quarter 2022 home price forecast estimated home price growth in the second half of 2022 and in 2023, our third quarter 2022 home price forecast estimated additional home price declines in the fourth quarter of 2022 and throughout 2023.

The largest drivers of our single-family provision for credit losses in the first nine months of 2022 were:

•Provision from actual and forecasted home prices. The provision from actual and forecasted home prices in the third quarter of 2022 discussed above was the largest driver of our single-family provision for credit losses in the first nine months of 2022. The impact of this home-price related provision in the third quarter of 2022 was partially offset by a benefit from actual and expected home price growth in each of the first and second quarters of 2022. During the first half of 2022, our forecasted home prices were positive for the second half of 2022 through 2023. In addition, we observed strong actual home price growth through the second quarter of 2022.

•Provision from higher actual and projected interest rates as of September 30, 2022 compared with December 31, 2021. As mortgage rates increased, we expected a decrease in future prepayments on single-family loans, including modified loans accounted for as troubled debt restructurings. Lower expected prepayments extended the expected lives of these TDR loans, which increased the expected impairment relating to economic concessions provided on them, resulting in a provision for credit losses.

•Provision from changes in loan activity, which includes provision on newly acquired loans. Throughout the first nine months of 2022, refinance loan volumes continued to decline and purchase loans increased as a percentage of acquisitions compared to the first nine months of 2021. In addition, in the third quarter of 2022, our credit loss provision also increased as our more negative home price forecast impacted our estimate of losses on newly acquired loans.

| Fannie Mae Third Quarter 2023 Form 10-Q | 16 | |||||||

| MD&A | Consolidated Results of Operations | ||||||||

Multifamily Benefit (Provision) for Credit Losses

The largest driver of our multifamily provision for credit losses in the third quarter of 2023 was a provision for actual and projected interest rates. Rising interest rates increase the likelihood that loans with balloon balances due at maturity will be unable to refinance, due to higher refinancing rates. In addition, rising interest rates increase costs for loans with adjustable-rates, which increases the expected impairment and the provision for credit losses on these loans.

The impact of this factor was offset by a benefit from actual and projected economic data in the third quarter of 2023. The benefit from actual and projected economic data was primarily driven by the impact of a change in our long-term economic forecast assumptions, which was partially offset by continued declines in multifamily property values.

Our multifamily provision for credit losses in the first nine months of 2023 was primarily driven by actual and projected interest rates as described above.

See “Multifamily Business—Multifamily Mortgage Credit Risk Management—Multifamily Portfolio Monitoring” for a discussion of risks within specific property types that we are monitoring, including a discussion of seniors housing loans and loans with adjustable-rates.

The largest driver of our multifamily provision for credit losses in the third quarter and first nine months of 2022 was a provision for higher actual and projected interest rates.

Other Expenses, Net

Other expenses, net consists of debt extinguishment gains and losses, expenses associated with legal claims, foreclosed property income (expense), gains and losses from partnership investments, housing trust fund expenses, loan subservicing costs, and servicer fees paid in connection with certain loss mitigation activities. During the third quarter of 2023, we recognized $491 million of expense attributable to a jury verdict and an award of prejudgment interest for Fannie Mae preferred shareholders in two cases consolidated for trial in the U.S. District Court for the District of Columbia. For additional information, see “Note 13, Commitments and Contingencies—Senior Preferred Stock Purchase Agreements Litigation.”

| Fannie Mae Third Quarter 2023 Form 10-Q | 17 | |||||||

| MD&A | Consolidated Balance Sheet Analysis | ||||||||

Consolidated Balance Sheet Analysis

This section discusses our condensed consolidated balance sheets and should be read together with our condensed consolidated financial statements and the accompanying notes.

| Summary of Condensed Consolidated Balance Sheets | ||||||||||||||||||||

| As of | ||||||||||||||||||||

| September 30, 2023 | December 31, 2022 | Variance | ||||||||||||||||||

| (Dollars in millions) | ||||||||||||||||||||

Assets | ||||||||||||||||||||

Cash and cash equivalents and securities purchased under agreements to resell | $ | 71,454 | $ | 72,552 | $ | (1,098) | ||||||||||||||

| Restricted cash and cash equivalents | 33,195 | 29,854 | 3,341 | |||||||||||||||||

| Investments in securities, at fair value | 51,872 | 50,825 | 1,047 | |||||||||||||||||

| Mortgage loans: | ||||||||||||||||||||

| Of Fannie Mae | 52,339 | 54,085 | (1,746) | |||||||||||||||||

| Of consolidated trusts | 4,090,220 | 4,071,698 | 18,522 | |||||||||||||||||

| Allowance for loan losses | (8,671) | (11,347) | 2,676 | |||||||||||||||||

| Mortgage loans, net of allowance for loan losses | 4,133,888 | 4,114,436 | 19,452 | |||||||||||||||||

| Deferred tax assets, net | 11,885 | 12,911 | (1,026) | |||||||||||||||||

| Other assets | 27,086 | 24,710 | 2,376 | |||||||||||||||||

| Total assets | $ | 4,329,380 | $ | 4,305,288 | $ | 24,092 | ||||||||||||||

| Liabilities and equity | ||||||||||||||||||||

| Debt: | ||||||||||||||||||||

| Of Fannie Mae | $ | 125,652 | $ | 134,168 | $ | (8,516) | ||||||||||||||

| Of consolidated trusts | 4,106,110 | 4,087,720 | 18,390 | |||||||||||||||||

| Other liabilities | 23,893 | 23,123 | 770 | |||||||||||||||||

| Total liabilities | 4,255,655 | 4,245,011 | 10,644 | |||||||||||||||||

| Fannie Mae stockholders’ equity: | ||||||||||||||||||||

| Senior preferred stock | 120,836 | 120,836 | — | |||||||||||||||||

| Other net deficit | (47,111) | (60,559) | 13,448 | |||||||||||||||||

| Total equity | 73,725 | 60,277 | 13,448 | |||||||||||||||||

| Total liabilities and equity | $ | 4,329,380 | $ | 4,305,288 | $ | 24,092 | ||||||||||||||

Cash and Cash Equivalents and Securities Purchased Under Agreements to Resell

Cash and cash equivalents and securities purchased under agreements to resell decreased from December 31, 2022 to September 30, 2023, primarily driven by redemption of corporate debt outpacing issuances, partially offset by proceeds from the sale of securities and loans, and the continued accumulation of earnings retained from our operations. For further discussion, see “Liquidity and Capital Management—Liquidity Management.”

Mortgage Loans, Net of Allowance

The mortgage loans reported in our condensed consolidated balance sheets are classified as either HFS or HFI and include loans owned by Fannie Mae and loans held in consolidated trusts.

Mortgage loans, net of allowance for loan losses modestly increased from December 31, 2022 to September 30, 2023, driven primarily by loan acquisitions outpacing liquidations and sales during the first nine months of 2023, as well as a decline in our allowance for loan losses.

For additional information on our mortgage loans, see “Note 3, Mortgage Loans,” and for additional information on changes in our allowance for loan losses, see “Note 4, Allowance for Loan Losses.”

Debt

The decrease in debt of Fannie Mae from December 31, 2022 to September 30, 2023 was due to redemptions outpacing new issuances. The increase in debt of consolidated trusts from December 31, 2022 to September 30, 2023

| Fannie Mae Third Quarter 2023 Form 10-Q | 18 | |||||||

| MD&A | Consolidated Balance Sheet Analysis | ||||||||

was primarily driven by sales of Fannie Mae MBS, which also includes sales of Fannie Mae MBS that were previously held in our retained mortgage portfolio. Sales of Fannie Mae MBS are accounted for as issuances of debt of consolidated trusts in our condensed consolidated balance sheets, since the MBS certificate ownership is transferred from us to a third party. See “Liquidity and Capital Management—Liquidity Management—Debt Funding” for a summary of activity in short-term and long-term debt of Fannie Mae. Also see “Note 7, Short-Term and Long-Term Debt” for additional information on our total outstanding debt.

Stockholders’ Equity

Our stockholders’ equity (also referred to as our net worth) increased to $73.7 billion as of September 30, 2023, compared with $60.3 billion as of December 31, 2022, due to the $13.4 billion in comprehensive income recognized during the first nine months of 2023.

The aggregate liquidation preference of the senior preferred stock increased to $190.5 billion as of September 30, 2023 from $185.5 billion as of June 30, 2023, due to the $5.0 billion increase in our net worth in the second quarter of 2023. The aggregate liquidation preference of the senior preferred stock will further increase to $195.2 billion as of December 31, 2023 due to the $4.7 billion increase in our net worth in the third quarter of 2023. For more information about how this liquidation preference is determined, see “Business—Conservatorship and Treasury Agreements—Treasury Agreements—Senior Preferred Stock” in our 2022 Form 10-K and “Liquidity and Capital Management—Capital Management—Capital Activity” in this report.

Retained Mortgage Portfolio

We use our retained mortgage portfolio primarily to provide liquidity to the mortgage market through our whole loan conduit and to support our loss mitigation activities, particularly in times of economic stress when other sources of liquidity to the mortgage market may decrease or withdraw.

Our retained mortgage portfolio consists of mortgage loans and mortgage-related securities that we own, including Fannie Mae MBS and non-Fannie Mae mortgage-related securities. Assets held by consolidated MBS trusts that back mortgage-related securities owned by third parties are not included in our retained mortgage portfolio.

The chart below separates the instruments within our retained mortgage portfolio, measured by unpaid principal balance, into three categories based on each instrument’s use:

•Lender liquidity, which includes balances related to our whole loan conduit activity, supports our efforts to provide liquidity to the single-family and multifamily mortgage markets.

•Loss mitigation supports our loss mitigation efforts through the purchase of delinquent loans from our MBS trusts.

•Other represents assets that were previously purchased for investment purposes.

Retained Mortgage Portfolio

(Dollars in billions)

| Fannie Mae Third Quarter 2023 Form 10-Q | 19 | |||||||

| MD&A | Retained Mortgage Portfolio | ||||||||

The table below displays the components of our retained mortgage portfolio, measured by unpaid principal balance. Based on the nature of the asset, these balances are included in either “Investments in securities, at fair value” or “Mortgage loans, net of allowance for loan losses” in our “Summary of Condensed Consolidated Balance Sheets” table above.

Retained Mortgage Portfolio | |||||||||||||||||

| As of | |||||||||||||||||

| September 30, 2023 | December 31, 2022 | ||||||||||||||||

| (Dollars in millions) | |||||||||||||||||

| Lender liquidity: | |||||||||||||||||

Agency securities(1) | $ | 17,931 | $ | 16,410 | |||||||||||||

| Mortgage loans | 9,658 | 7,329 | |||||||||||||||

| Total lender liquidity | 27,589 | 23,739 | |||||||||||||||

Loss mitigation mortgage loans(2) | 37,656 | 38,458 | |||||||||||||||

| Other: | |||||||||||||||||

Reverse mortgage loans(3) | 4,113 | 6,565 | |||||||||||||||

Mortgage loans(4) | 3,156 | 3,365 | |||||||||||||||

Reverse mortgage securities(5) | 2,803 | 4,811 | |||||||||||||||

Other securities(6) | 645 | 804 | |||||||||||||||

| Total other | 10,717 | 15,545 | |||||||||||||||

| Total retained mortgage portfolio | $ | 75,962 | $ | 77,742 | |||||||||||||

| Retained mortgage portfolio by segment: | |||||||||||||||||

| Single-family mortgage loans and mortgage-related securities | $ | 69,531 | $ | 73,769 | |||||||||||||

| Multifamily mortgage loans and mortgage-related securities | $ | 6,431 | $ | 3,973 | |||||||||||||

(1)Consists of Fannie Mae, Freddie Mac and Ginnie Mae mortgage-related securities, including Freddie Mac securities guaranteed by Fannie Mae. Excludes Fannie Mae and Ginnie Mae reverse mortgage securities and Fannie Mae-wrapped private-label securities.

(2)Includes single-family loans on nonaccrual status of $7.3 billion and $7.1 billion as of September 30, 2023 and December 31, 2022, respectively. Also includes multifamily loans on nonaccrual status of $1.6 billion and $243 million as of September 30, 2023 and December 31, 2022, respectively.

(3)We stopped acquiring newly originated reverse mortgage loans in 2010.

(4) Consists primarily of whole loan Real Estate Mortgage Investment Conduit securities (“REMICs”), second liens, interest-only loans and government loans, which are mortgage loans guaranteed or insured, in whole or in part, by the U.S. government.

(5) Consists of Fannie Mae and Ginnie Mae reverse mortgage securities.

(6) Consists of private-label and other securities, Fannie Mae-wrapped private-label securities and mortgage revenue bonds.

The amount of mortgage assets that we may own is capped at $225 billion under the terms of our senior preferred stock purchase agreement with Treasury. In addition, we are currently required to cap our mortgage assets at $202.5 billion per instructions from FHFA. See “Business—Conservatorship and Treasury Agreements” in our 2022 Form 10-K for additional information on our mortgage assets cap.

We include 10% of the notional value of the interest-only securities we hold in calculating the size of the retained portfolio for the purpose of determining compliance with the senior preferred stock purchase agreement retained portfolio limits and associated FHFA guidance. As of September 30, 2023, 10% of the notional value of our interest-only securities was $1.6 billion, which is not included in the table above.

Under the terms of our MBS trust documents, we have the option or, in some instances, the obligation, to purchase mortgage loans that meet specific criteria from an MBS trust. The purchase price for these loans is the unpaid principal balance of the loan plus accrued interest. If a delinquent loan remains in a single-family MBS trust, the servicer is responsible for advancing the borrower’s missed scheduled principal and interest payments to the MBS holders for up to four months, after which time we must make these missed payments. In addition, we must reimburse servicers for advanced principal and interest payments.

In support of our loss mitigation strategies, we purchased $6.9 billion of loans from our single-family MBS trusts in the first nine months of 2023, the substantial majority of which were delinquent, compared with $14.2 billion of loans purchased from single-family MBS trusts in the first nine months of 2022. The amount of loans we bought out of trusts decreased in the first nine months of 2023 relative to the same period in the prior year as loans exiting COVID-19-related forbearance drove a higher number of loan modifications in 2022.

| Fannie Mae Third Quarter 2023 Form 10-Q | 20 | |||||||

| MD&A | Guaranty Book of Business | ||||||||

Guaranty Book of Business

Our “guaranty book of business” consists of:

•Fannie Mae MBS outstanding, excluding the portions of any structured securities we issue that are backed by Freddie Mac securities;

•mortgage loans of Fannie Mae held in our retained mortgage portfolio; and

•other credit enhancements that we provide on mortgage assets.

“Total Fannie Mae guarantees” consists of:

•our guaranty book of business; and

•the portions of any structured securities we issue that are backed by Freddie Mac securities.

We and Freddie Mac issue single-family uniform mortgage-backed securities, or “UMBS.” In this report, we use the term “Fannie Mae-issued UMBS” to refer to single-family Fannie Mae MBS that are directly backed by fixed-rate mortgage loans and generally eligible for trading in the to-be-announced (“TBA”) market. We use the term “Fannie Mae MBS” or “our MBS” to refer to any type of mortgage-backed security that we issue, including UMBS®, Supers®, Real Estate Mortgage Investment Conduit securities (“REMICs”) and other types of single-family or multifamily mortgage-backed securities.

Some Fannie Mae MBS that we issue are backed in whole or in part by Freddie Mac securities. When we resecuritize Freddie Mac securities into Fannie Mae-issued structured securities, such as Supers and REMICs, our guaranty of principal and interest extends to the underlying Freddie Mac securities. However, Freddie Mac continues to guarantee the payment of principal and interest on the underlying Freddie Mac securities that we have resecuritized. See “Business—Mortgage Securitizations—Uniform Mortgage-Backed Securities, or UMBS—UMBS and Structured Securities” in our 2022 Form 10-K for information regarding the upfront fee we charge to include Freddie Mac securities in our structured securities. Effective April 1, 2023, the upfront fee for commingled securities decreased from 50 basis points to 9.375 basis points on the portion of the securities made up of Freddie Mac-issued collateral. References to our single-family guaranty book of business exclude Freddie Mac-acquired mortgage loans underlying Freddie Mac securities that we have resecuritized.