GIBRALTAR INDUSTRIES, INC. - Annual Report: 2019 (Form 10-K)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES ACT OF 1934 |

For the fiscal year ended December 31, 2019

OR

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 0-22462

GIBRALTAR INDUSTRIES, INC.

Delaware | 16-1445150 | |||||

(State or incorporation ) | (I.R.S. Employer Identification No.) | |||||

3556 Lake Shore Road | P.O. Box 2028 | Buffalo , | New York | 14219-0228 | ||

(Address of principal executive offices) | ||||||

Registrant’s telephone number, including area code: (716) 826-6500

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol | Name of each exchange on which registered | ||

Common Stock, $0.01 par value per share | ROCK | NASDAQ Stock Market | ||

Securities registered pursuant to Section 12(g) of the Act: NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file report pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definition of “large accelerated filer”, “accelerated filer”, “small reporting company”, and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☒ | Accelerated filer | ☐ | Emerging growth company | ☐ | ||

Non-accelerated filer | ☐ | Smaller reporting company | ☐ | ||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

Aggregate market value of voting Common Stock held by non-affiliates of the registrant as of June 30, 2019 was: $1.3 billion.

As of February 27, 2020, the number of common shares outstanding was: 32,358,728.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s Definitive Proxy Statement to be filed for its 2020 Annual Meeting of Stockholders

are incorporated by reference into Part III of this Annual Report on Form 10-K.

1

Form 10-K Index

Page Number | ||

Item 1 | ||

Item 1A | ||

Item 1B | ||

Item 2 | ||

Item 3 | ||

Item 4 | ||

Item 5 | ||

Item 6 | ||

Item 7 | ||

Item 7A | ||

Item 8 | ||

Item 9 | ||

Item 9A | ||

Item 10 | ||

Item 11 | ||

Item 12 | ||

Item 13 | ||

Item 14 | ||

Item 15 | ||

2

Safe Harbor Statement

Certain information set forth herein includes statements that express our opinions, expectations, beliefs, plans, objectives, assumptions or projections regarding future events or future results and, therefore, are, or may be deemed to be, “forward-looking statements.” These forward-looking statements can generally be identified by the use of forward-looking terminology, including the terms “believes,” “estimates,” “anticipates,” “expects,” “seeks,” “projects,” “intends,” “plans,” “may,” “will” or “should” or, in each case, their negative or other variations or comparable terminology. These forward-looking statements include all matters that are not historical facts. They include statements regarding our intentions, beliefs or current expectations concerning, among other things, our results of operations, financial condition, liquidity, prospects, growth, competition, strategies and the industries in which we operate. By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. We believe that these risks and uncertainties include, but are not limited to, those described in Item 1A “Risk Factors.” Those factors should not be construed as exhaustive and should be read with the other cautionary statements in Item 1A “Risk Factors.” Although we base these forward-looking statements on assumptions that we believe are reasonable when made, we caution you that forward-looking statements are not guarantees of future performance and that our actual results of operations, financial condition and liquidity and the development of the industries in which we operate may differ materially from those made in or suggested by the forward-looking statements contained herein. In addition, even if our results of operations, financial condition and liquidity and the development of the industries in which we operate are consistent with the forward-looking statements contained in this document, those results or developments may not be indicative of results or developments in subsequent periods. Given these risks and uncertainties, you are cautioned not to place undue reliance on these forward-looking statements. Any forward-looking statements that we make herein speak only as of the date of those statements, and we undertake no obligation to update those statements or to publicly announce the results of any revisions to any of those statements to reflect future events or developments. Comparisons of results for current and any prior periods are not intended to express any future trends or indications of future performance, unless expressed as such, and should only be viewed as historical data.

PART I

Item 1. | Business |

The Company

Gibraltar Industries, Inc. (the "Company") is a leading manufacturer and provider of products and services for the renewable energy, conservation, residential, industrial and infrastructure markets. Gibraltar’s mission is to create compounding and sustainable value with strong leadership positions in higher growth, profitable end markets. At the beginning of 2019, after four years of steady improvement in operational execution and financial results under the leadership of Frank Heard, the Company announced the appointment of Bill Bosway as Chief Executive Officer, with Frank Heard vacating the CEO role and being appointed Executive Vice Chair of the Board through his planned retirement in March 2020. Under Mr. Bosway’s leadership, management completed a thorough evaluation of the markets in which the Company participates in, as well as its position in each market. This work solidified the Company’s strategy and defined plans to accelerate growth and further improve the Company’s margin profile, both through organic and inorganic investment. It has also helped focus and prioritize the Company's key investments such that it deliver increasing returns and sustainable value for its shareholders.

Over the past twelve months, the Company migrated from a Four-Pillar strategy to a Three-Pillar Strategy with the operating foundation focused on three core tenets: Business Systems, Portfolio Management, and Organizational Development.

1. | Business Systems, which combines two of the Company's previous strategic pillars - operational excellence and product innovation - is supported by an execution review of the Company's monthly business performance, implementation of key investments, IT operating and digital systems performance, and new product and services innovation. |

2. | Portfolio Management, which combines the two other previous strategic pillars - acquisitions and portfolio management - is focused on optimizing the Company’s business portfolio and ensuring our human and financial capital are invested to provide sustainable, profitable growth while expanding our relevance with customers and shaping our markets. The recent acquisitions of Apeks Supercritical, LLC ("Apeks") in August 2019, Thermo |

3

Energy Systems ("Thermo) in January 2020, and Delta Separations (“Delta”) in February 2020 were the direct result of our portfolio management strategy.

3. | Organizational Development is the third pillar of our strategy. In order to execute Business Systems and Portfolio Management, the Company must have a strong organization to execute, and the organization must continuously develop and improve. The Company aspires to make our place of work the "Best Place to Work", where we focus on creating the best development and learning environment for our people, proactively operate businesses that solve global challenges, and engage and support the communities we are present in. We believe doing so helps us attract and retain the best people so we can execute our business plans. |

The Company serves customers primarily in North America including renewable energy (solar) developers, institutional and commercial growers of food and plants, home improvement retailers, wholesalers, distributors, and contractors. As of December 31, 2019, we operated 41 facilities, comprised of 29 manufacturing facilities, five distribution centers, and seven offices, which are located in 18 states, Canada, China, and Japan. Our operational infrastructure provides the necessary scale to support local, regional, and national customers in each of our markets.

The Company operates and reports its results in the following three reporting segments:

• | Renewable Energy and Conservation; |

• | Residential Products; and |

• | Industrial and Infrastructure Products. |

The following table sets forth the primary products, applications, and end markets for each segment:

Renewable Energy and Conservation Segment

Products & Services | Applications | End Users | ||

Renewable Energy: Design, engineering, manufacturing and installation of solar racking and electrical balance of systems | Commercial & distributed generation scale commercial solar installations |  | Solar developers; power companies; solar energy EPC contractors | |

Conservation: Provide growing and processing solutions including the designing, engineering, manufacturing and installation of greenhouses, and botanical extraction systems | Retail, vegetable, flowers, cannabis, commercial, institutional and conservatories, car wash tunnels, botanical oil extraction | Retail garden centers; conservatories and botanical gardens; commercial growers; public and private agricultural research; botanical oil processors | ||

Residential Products Segment

Product | Applications | End Market | ||

Roof and foundation ventilation products | Ventilation and whole-house air flow | | Residential: new construction and repair and remodeling | |

Centralized mail systems and electronic package solutions | Secure storage for mail and package deliveries | |||

Retractable awnings & gutter guards | Sun protection; gutter protection | |||

Rain dispersion, trims and flashings, other accessories | Water & protection from natural elements | |||

4

Industrial and Infrastructure Products Segment

Product | Applications | End Market | ||

Fabricated expanded metal and perforated metal products | Perimeter security barriers; walkways / catwalks; filtration; architectural facades | | Industrial and commercial construction, automotive, energy and power generation | |

Structural bearings, expansion joints and pavement sealant for bridges and roadways | Preserve functionality under varying weight, wind, temperature and seismic conditions | Bridge and elevated highway construction, airport pavements | ||

The Company’s operating businesses have established leadership positions in attractive end markets by building core capabilities in innovation, new products and services, manufacturing and field operations, business systems, quality performance, along with a healthy balance sheet and the strength of our people. We will continue our focus of time, talent, and energy on strengthening our position in each market we serve.

Attractive End Markets. Our markets are focused on solving global challenges as it relates to accelerating renewable energy generation, maintaining healthy home environments, growing food and plants more effectively and efficiently, supporting postal and parcel home delivery, and improving our country’s transportation infrastructure and ways of transporting people.

Value-Added Products and Services. We provide industry-best solutions to our customers: racking and electrical systems for photovoltaic (PV) solar systems, commercial growing greenhouses and processing extraction technology for biologically grown food, cannabis, and other plants; roof-related ventilation to support healthy home environments; postal and parcel storage for home and retail sites; and structural bearings and expansion joints for bridges and other transportation structures. Our products and services are highly engineered, supported with intellectual property, and driven by effective business systems and IT infrastructure.

Commitment to Customer & Quality. We strive to be connected directly with our end customers, where we receive unfiltered feedback on performance, insight on customer problems and opportunities, and cooperation on ideas for new products, services, and business model optimization. The percentage of our total business contracted directly with end users of our products and services exceeded 45% in 2019, and we expect this to grow in future years. Our commitment to quality is a core operating tenet for the Company, and our quality management systems are designed to ensure we deliver to customer and stakeholder expectations while meeting statutory and regulatory requirements related to our products and services.

Strong liquidity profile. We strive to manage our cash resources to ensure sufficient liquidity to fund growth initiatives, support the seasonality of our businesses, manage effectively through economic cycles. As of December 31, 2019, our liquidity was $585 million, including $191 million of cash and $394 million of availability under our revolving credit facility. We believe our low leverage and ample borrowing capacity, along with enhanced flexibility in our Senior Credit Agreement, provides us with the financial capacity to fund our ongoing business requirements, strategic initiatives, and acquisition opportunities.

Recent developments

On February 13, 2020, the Company acquired the assets of California-based Delta Separations and Teaching Tech ("Delta Separations"), a privately held ethanol-based extraction systems manufacturer and training and laboratory design and operations consultative partner for $50 million in an all cash transaction. Delta Separations had revenue of approximately $46 million in 2019.

On January 15, 2020, the Company acquired the assets of Canadian-based Thermo Energy Systems ("Thermo"), a privately held provider of commercial greenhouse solutions in North America supporting the biologically grown organic food market, in an all cash transaction for approximately $7 million. The Company also expects to invest approximately $25 million into Thermo to provide an appropriate level of working capital. Thermo is expected to contribute annual revenue at a run rate of approximately $75 million.

5

On August 30, 2019, the Company acquired all of the outstanding membership interests of Apeks LLC ("Apeks"), a designer and manufacturer of botanical oil extraction systems utilizing subcritical and supercritical carbon dioxide ("CO2"). The acquisition was financed through cash on hand of $12 million. Apeks had trailing twelve months of revenues as of June 30, 2019 of $17.7 million. The results of operations of Apeks have been included in the Renewable Energy and Conservation segment of the Company's consolidated financial statements from the date of acquisition.

On March 18, 2019, the Company appointed Patrick M. Burns as Chief Operating Officer. In his position as Chief Operating Officer, Mr. Burns is responsible for all aspects of Gibraltar’s day-to-day operations across its businesses and such other executive duties as he is assigned from time to time by the Board of Directors and the Chief Executive Officer.

On January 24, 2019, we entered into the Company's Sixth Amended and Restated Credit Agreement (the "Senior Credit Agreement") which includes a 5-year, $400 million revolving credit facility. The Senior Credit Agreement also provides the Company the opportunity, upon request, to increase the amount of the revolving credit facility to $700 million. In conjunction with entering into the Senior Credit Agreement, on February 1, 2019, the Company redeemed all $210 million of its outstanding 6.25% Senior Subordinated Bonds. The amended Senior Credit Agreement provides the Company with access to capital and improves our financial flexibility.

On January 2, 2019, the Company appointed William T. Bosway as President and Chief Executive Officer of the Company and a member of the Board of Directors. Over the past 29 years, Mr. Bosway has worked for two Fortune 500 industrial companies and brings to the Company strong leadership skills and significant experience in acquisitions, driving organic growth, lean manufacturing and continuous improvement techniques. In connection with Mr. Bosway’s appointment, then Chief Executive Officer Frank Heard was appointed Executive Vice Chair of the Board and he announced his intention to retire on March 3, 2020.

Customers and Products

Our customers are located primarily throughout North America. One customer, a home improvement retailer which purchases from both the Residential Products segment and Renewable Energy and Conservation segment, represented 12% of our consolidated net sales for each of the three years ended December 31, 2019, 2018, and 2017. No other customer in any segment or segments accounted for more than 10% of our consolidated net sales.

Our products are primarily distributed to our customers using common carriers. We maintain distribution centers that complement our manufacturing plants from which we ship products and ensure on-time delivery while maintaining efficiency within our distribution system. Our customers and product offerings by segment are described below.

Renewable Energy and Conservation

The Renewable Energy and Conservation segment is primarily a designer and manufacturer of fully-engineered solutions for solar mounting systems, greenhouse structures and botanical oil extraction systems. This segment offers a fully integrated approach to the design, engineering, manufacturing and installation of solar racking systems, including electrical balance of systems, and commercial, institutional, and retail greenhouse structures servicing customers, such as community solar owners and developers, retail garden centers, conservatories and botanical gardens, commercial growers, schools and universities, and botanical oil processors. With the recently announced acquisitions of Thermo and Delta Separations, we have 10 manufacturing facilities and 2 distribution centers and operate in the United States, China and Japan.

An integral part of solar racking and greenhouse projects is the fabrication of specifically designed metal structures for highly-engineered applications including: racking for ground-mounted solar arrays; single-axis solar tracker solutions; carports that integrate solar PV panels; as well as commercial-scale greenhouses and other glass structures. Both the solar racking and greenhouse projects involve securing glass and plastic to metal and use the same raw materials including steel and aluminum. Most of our production is completed using computer numerical control machines, roll forming machines, laser cutters and other fabrication tools. The structural metal components are designed, engineered, fabricated and installed in accordance with applicable building codes.

We strive to improve our offerings of products by introducing new products, enhancing existing products, adjusting product specifications to respond to commercial building codes and regulatory changes, and providing solutions to contractors and end users. New products introduced in recent years include botanical oil extraction systems, single-axis tracker systems, metal framed structures for car washes, and solar racking systems for carports and canopies. Our botanical oil extraction systems provide equipment for extracting plant oils for hemp, cannabis, and nutraceutical

6

processors. The single-axis tracker systems within our solar mounting solutions group provide flexibility to adapt to a variety of site conditions that impact tracker site designs when using other solutions in the market and can vastly reduce the costs associated with civil work on projects. The patented design eliminates complexities incorporated in the traditional systems, simplifying the operations and maintenance of the system, along with streamlining the installation process. Our car washes serve a market preference for light- transparent structures. Solar racking systems for carports serve as protection for cars from the effects of the sun and intense heat while providing a renewable energy source. Similarly, solar racking systems installed on idle land, such as solid waste landfills, converts such land into a useful property by providing clean renewable power generating capabilities.

Residential Products

Our Residential Products segment services the residential repair and remodeling and to a lesser extent the new housing construction markets in North America with products including roof and foundation ventilation products, centralized mail systems and electronic package solutions, outdoor living products (retractable sun-shades), rain dispersion products and other roofing and related accessories. Our residential product offerings are sold through a number of sales channels including major retail home centers, building material wholesalers, building product distributors, buying groups, roofing distributors, residential contractors, property management companies and postal services distributors and providers. This segment operates 11 manufacturing facilities throughout the United States, giving it a base of operations to provide manufacturing capability of high quality products, customer service, delivery and technical support to a broad network of regional and national customers across North America.

Our roof and foundation ventilation products and accessories include solar powered units. Our centralized mail and electronic package solutions include single mailboxes, cluster style mail and parcel boxes for single and multi-family housing and electronic package locker systems. Our remaining residential product offerings consist of roof edging and flashing, soffits and trim, drywall corner bead, metal roofing and accessories, rain dispersion products, including gutters and accessories, and exterior retractable awnings. Each of these product offerings can be sold separately or as part of a system solution.

Within our Residential Products businesses, we are constantly striving to improve our product/solution offerings by introducing new products, enhancing existing products, adapting to building code and regulatory changes, and providing new and innovative solutions to homeowners and contractors. New products introduced in recent years include electronic parcel lockers, roof top safety kits, chimney caps, heat trace coils, exterior, remote-controlled deck awnings for sun protection, and high-efficiency and solar-powered ventilation products. Our electronic parcel lockers and parcel room systems provide residents in multi-family communities a secure storage receptacle to handle both package deliveries and receipt of other delivered goods. Our ventilation and roof flashing products provide protection and extend the life of structures while providing a safer, healthier environment for residents. Our cluster box mail delivery products provide delivery cost savings to the postal service while offering secure storage for delivered mail and packages. Our building products are manufactured primarily from galvanized and painted steel, anodized and painted aluminum, and various resins.

Within our manufacturing facilities, we leverage significant production capabilities which allow us to process a wide range of metals and plastics for our residential products. Most of our production is completed using automatic roll forming machines, stamping presses, welding, paint lines, and injection molding equipment. We maintain our equipment according to a thorough preventive maintenance program allowing us to meet the demanding quality and delivery requirements of our customers. In some cases, the Company sources products from third-party vendors to optimize cost and quality in order to provide the very best and affordable solution for our customers.

Industrial and Infrastructure Products

Our Industrial and Infrastructure Products segment serves a variety of end markets such as industrial and commercial construction, highway and bridge construction, automotive, airports and energy and power generation through a number of sales channels including discrete and process manufacturers, steel fabricators and distributors, commercial and transportation contractors, and power generating utilities. Our Industrial and Infrastructure product offerings include perimeter security, expanded and perforated metal, plank grating, as well as, expansion joints and structural bearings for highway bridges. We operate 10 manufacturing facilities and 3 distribution centers throughout the United States and Canada giving us a base of operations to provide customer support, delivery, service, and quality to a number of regional and national customers, and providing us with manufacturing and distribution efficiencies in North America.

Our expanded and perforated metal and plank grating is used in walkways, catwalks, architectural facades, perimeter security barriers, shelving, and other applications where both visibility and security are necessary. Our fiberglass grating is used by our customers where high strength, light weight, low maintenance, corrosion resistance and non-

7

conductivity are required. Our remaining product offerings in this segment include expansion joint systems, bearing assemblies, and pavement sealing systems used in bridges, elevated highways, airport runways, and rail crossings.

We strive to improve our offerings of industrial and infrastructure products by introducing new products, enhancing existing products, adjusting product specifications to respond to commercial building code and regulatory changes, and providing additional solutions to original equipment manufacturers and contractors. New products introduced in recent years include customized perforated and expanded metal to penetrate a range of new markets such as architectural facades for buildings (museums, sports stadiums and retail outlets) and perimeter security barriers for protecting critical infrastructure. In addition, we have extended our transportation infrastructure products into new markets. For example, our long-lasting pavement sealants for roadways are now being installed on airport runways internationally, our structural bearings for elevated highways and bridges have been installed on an offshore oil production platform, and our corrosion-protection products for cable-suspension bridges are now marketed and sold internationally.

Our production capabilities allow us to process a wide range of metals necessary for manufacturing industrial products. Most of our production is completed using computer numerical control machines, shears, slitters, press brakes, milling, welding, and numerous automated assembly machines. We maintain our equipment according to a thorough preventive maintenance program, including in-house tool and die shops, allowing us to meet the demanding service requirements of our customers.

Engineering and Technical Services

Our business segments employ engineers and other technical personnel to perform a variety of key tasks which include the identification and implementation of improvements to our manufacturing process, redesign of our products for better performance, the development of new products and identification and execution of cost reduction activities. In addition, our engineering staff employs a range of drafting software to design highly specialized and technically precise products. In our Renewable Energy and Conservation and Industrial and Infrastructure Products segments, drawings are approved and stamped by state licensed professional engineers. Technical service personnel also work in conjunction with our sales force in the new product development process to determine the types of products and services that suit the particular needs of our customers.

Suppliers and Raw Materials

Our business is required to maintain sufficient quantities of raw material inventory in order to accommodate our customers’ short lead times. Accordingly, we plan our purchases to maintain raw materials at sufficient levels to satisfy the anticipated needs of our customers. We have implemented enterprise resource planning systems along with a corporate wide SIOP (Sales, Inventory, Operations Planning process) to better manage our inventory, forecast customer orders, enable efficient supply chain management, and allow for more timely counter-measures to changing customer demand and market conditions.

The primary raw materials we purchase are flat-rolled and plate steel, aluminum coil and extrusions, and resins. We purchase flat-rolled and plate steel and aluminum at regular intervals on an as-needed basis, primarily from the major North American mills, as well as, a limited amount from domestic service centers and foreign steel importers. Substantially all of our resins are purchased from domestic vendors, primarily through distributors, with a small amount purchased directly from manufacturers. Supply has historically been adequate from these sources to fulfill our needs. Because of our strategy to develop longstanding relationships in our supply chain, we have been able to adjust our deliveries of raw materials to match our required inventory positions to support our on-time deliveries to customers while allowing us to manage our investment in inventory and working capital. Management continually evaluates improvements in our purchasing practices across our geographically dispersed facilities in order to streamline purchasing across similar commodities.

We purchase natural gas and electricity from suppliers in proximity to our operations.

8

Intellectual Property

We actively protect our proprietary rights by the use of trademark, copyright, and patent registrations. While we do not believe that any individual item of our intellectual property is material, we believe our trademarks, copyrights, and patents provide us with a competitive advantage when marketing our products to customers. We also believe our brands are well recognized in the markets we serve and we believe they stand for high-quality manufactured goods at a competitive price. These trademarks, copyrights, and patent registrations help us maintain product leadership positions for the goods we offer. In 2019, 11% of our annual revenues were generated from patented products.

Sales and Marketing

In 2019, approximately 48% of our revenues were generated from products and services that were sold directly to the end user, with the remainder of revenues generated through retailers, wholesalers and distributors, up from 43% in 2018. Continual communication with our customers allows us to understand their challenges and provides us with the opportunity to identify solutions that will meet their needs. We have organized sales teams to focus on specific customers and national accounts through which we provide enhanced solutions and improve our ability to increase the relevance of products and services that we sell. Our sales regularly involve competitive bidding processes, and our reputation for meeting delivery requirements and strict specifications make us a preferred provider for many customers.

Our sales staff works with certain retail customers to optimize shelf space for our products which is expected to increase sales at these locations. Our retail customers are provided with point-of-sale marketing aids to encourage consumer spending on our products in their stores. We focus on providing our customers with industry leading customer service. We are able to meet our customers’ demand requirements due to our efficient manufacturing processes and extensive distribution network.

Backlog

While the majority of our products have short lead time order cycles, we had aggregated approximately $218 million of backlog at December 31, 2019 compared to $161 million at December 31, 2018. The backlog primarily relates to certain business units in our Renewable Energy and Conservation and our Industrial and Infrastructure segments. We believe that the majority of our backlog will be shipped, completed and installed during 2020.

Competition

The Company operates in highly competitive markets. We compete against several competitors in all three of our segments with different competitors in each major product category. We compete with competitors based on the range of products offered, quality, price, and delivery, as well as serving as a full service provider for project management in certain segments. Although some of our competitors are large companies, the majority are small to medium-sized and do not offer the large range of products that we offer.

We believe our broad range of products, high quality, and sustained ability to meet exacting customer delivery requirements gives us a competitive advantage over many of our competitors. We also believe that execution of our business strategy further differentiates us from many of our competitors and allows us to capitalize on those areas that give us a competitive advantage over many of our competitors.

Seasonality

The Company’s business has historically been subjected to seasonal influences, with higher sales typically realized in the second and third quarters. General economic forces, such as tax credit expirations and imposed tariffs, along with changes in the Company’s products and customer mix have shifted traditional seasonal fluctuations in revenue over the past few years.

Governmental Regulation

Our production processes involve the use of environmentally regulated materials. We believe that we operate our business in material compliance with all federal, state and local environmental laws and regulations, and do not anticipate any material adverse effect on our financial condition or results of operations to maintain compliance with such laws and regulations. However, we could incur operating costs or capital expenditures in complying with new or more stringent environmental requirements in the future or with current requirements if they are applied to our

9

manufacturing facilities or distribution centers in a way we do not anticipate. In addition, new or more stringent regulation of our energy suppliers could cause them to increase the price of energy.

Our operations are also governed by many other laws and regulations covering our labor relationships, the import and export of goods, the zoning of our facilities, taxes, our general business practices, and other matters. We believe that we are in material compliance with these laws and regulations and do not believe that future compliance with such laws and regulations will have a material adverse effect on our financial condition or results of operations.

Internet Information

Copies of the Company’s Proxy Statements on Schedule 14A filed pursuant to Section 14 of the Securities Exchange Act of 1934 and Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 are available free of charge through the Company’s website (www.gibraltar1.com) as soon as reasonably practicable after the Company electronically files the material with, or furnishes it to, the Securities and Exchange Commission.

Employees

The Company employed 1,932 and 1,939 employees at December 31, 2019 and 2018, respectively.

Information About Executive Officers

Our senior management team is composed of talented and experienced managers possessing broad experience in operational excellence, new product development, and driving profitable growth gained over multiple business cycles:

William Bosway - President, Chief Executive Officer (CEO) and a member of the Board of Directors. Mr. Bosway was appointed President, Chief Executive Office and a member of the Board of Directors effective January 2, 2019. Mr. Bosway joined our Company with extensive experience in global manufacturing industries, driving organic growth, acquisitions, lean manufacturing and continuous improvement techniques. Mr. Bosway was appointed as successor to the former CEO and President, Frank Heard, who announced that he would retire in March 2020.

Frank Heard - Vice Chair of the Board of Directors. Mr. Heard was appointed Vice Chair effective January 2, 2019 after announcement of his intentions to retire from the Company in March 2020. As the former CEO and President of the Company since January 2015, Mr. Heard assisted in transitioning the role of CEO to Mr. Bosway.

Patrick Burns - Chief Operating Office (COO). Mr. Burns was appointed COO of the Company on March 18, 2019. Mr. Burns joined with Company with significant experience in key leadership and operational strategy roles at various multi-industrial companies over his career.

Timothy Murphy - Chief Financial Officer (CFO) and Senior Vice President (SVP). Mr. Murphy was appointed CFO and SVP of the Company on April 1, 2017. Mr. Murphy joined the Company in 2004 as Director of Financial Reporting, and subsequently served as the Company's Vice President, Treasurer and Secretary.

Cherri Syvrud - SVP of Human Resources and Organizational Development. Ms. Syvrud was appointed SVP of Human Resources and Organizational Development on April 1, 2016. Ms. Syvrud joined the Company with significant experience in human resources and organization development, including 25 years of employment at Illinois Tool Works, Inc.

Jeffrey Watorek - Vice President, Treasurer and Secretary. Mr. Watorek was appointed as Vice President, Treasurer and Secretary on April 1, 2017. Mr. Watorek joined the Company in 2008 as Manager of Financial Reporting, and subsequently served as the Company's Director of Financial Planning and Analysis.

Item 1A. | Risk Factors |

Our business, financial condition and results of operations, and the market price for the Company's common shares are subject to numerous risks, many of which are driven by factors that cannot be controlled or predicted. The following discussion, as well as other sections of this Annual Report on Form 10-K, including “Part II, Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations,” describe certain business and other risks

10

affecting the Company. In conjunction with reviewing the forward-looking statements and other information contained in this Annual Report on Form 10-K, consideration should be given to the risk factors described below as well as those in the Safe Harbor Statement at the beginning of this Annual Report on Form 10-K.These risks are not the only risks we face. Our business operations and the market for our securities could also be adversely affected by additional factors that are not presently known to us, or that we currently consider to be immaterial in our operations.

Macroeconomic factors outside of our control may adversely affect our business, our industry, and the businesses and industries of many of our customer and suppliers.

Macroeconomic factors have a significant impact on our business, customer demand and the availability of credit and other capital, affecting our ability to generate profitable margins. Our operations are subject to the effects of domestic and international economic conditions including government monetary and trade policies, tax laws and regulations, as well as, the relative debt levels of the U.S. and the other countries in which we sell our products. Tariffs placed on imported products used by our customers could impact cost and availability of these products to our customers which could impact the demand for our products or services. In addition, fluctuations in the U.S. dollar impact the prices we charge and costs we incur to export and import products.

We are unable to predict the impact on our business of changes in domestic and international economic conditions. The markets in which we operate have been challenging in the past, and the possibility remains that the domestic or global economies, or certain industry sectors of those economies that are key to our sales, may deteriorate, which could result in a corresponding decrease in demand for our products and negatively impact our results of operations and financial condition.

Increases in future levels of leverage and size of debt service obligations could adversely affect our ability to raise additional capital to fund our operations, limit our ability to react to changes in the economy or our industry and prevent us from meeting our obligations.

As of December 31, 2019, we did not have any outstanding indebtedness. Nonetheless, we may need to incur debt in the future to fund strategic acquisitions, investments or for other purposes, which debt could have significant adverse consequences to our business. Our Senior Credit Agreement entered into on January 24, 2019 contains several financial and other restrictive covenants. A significant decline in our operating income along with increased levels of debt could cause us to violate these covenants which could result in our incurring of additional financing fees that would be costly and adversely affect our profitability and cash flows. We may also use our Senior Credit Agreement or otherwise incur additional debt for acquisitions, operations and capital expenditures that could adversely impact our ability to meet these covenants.

We apply judgments and make estimates in accounting for contracts, and changes in these judgments or estimates may have significant impacts on our earnings.

Changes in judgments or required estimates and any subsequent adjustments to those judgments or estimates (such as performance incentives, penalties, contract claims and contract modifications) could have a material adverse effect on sales and profits. Due to the substantial judgments applied and estimations involved with this process, our actual results could differ materially or could be settled unfavorably from our estimates. Revenue representing 35%, 32% and 28% of 2019, 2018 and 2017 consolidated net sales, respectively, were recognized over time under the cost-to-cost method. Refer to “Critical Accounting Estimates” within Item 7 of this Form 10-K for more detail of how our financial statements can be affected by accounting for revenue from contracts with customers.

A significant portion of our net sales are concentrated with a few customers. The loss of those customers would adversely affect our business, results of operations, and cash flows.

A loss of sales, whether due to decreased demand from the end markets we serve or from the loss of any significant customer in these markets, a decrease in the prices that we can realize from sales of our products to customers in these markets, or a loss, bankruptcy, or significant decrease in business from any of our major customers, could have a significant adverse effect on our profitability and cash flows. Our ten largest customers accounted for approximately 32%, 38%, and 36% of our net sales during 2019, 2018, and 2017, respectively, with our largest customer, a retail home improvement center, accounting for approximately 12% of our consolidated net sales during each of the years 2019, 2018 and 2017.

11

The volatility of the commodity market on our pricing of our principal raw materials, and the highly competitive market environment in which we do business could significantly impact our gross profit, net income, and cash flow.

Our principal raw materials are commodity products consisting of steel, aluminum, and resins, for which, at times, availability and pricing can be volatile due to a number of factors beyond our control, including general economic conditions, domestic and worldwide demand, labor costs, competition, import duties, tariffs, and currency exchange rates. Commodity price fluctuations and increased competition could force us to lower our prices or to offer additional services or enhanced products at a higher cost to us, which could reduce our gross profit, net income, and cash flow and cause us to lose market share.

A portion of our business is dependent on laws and regulations pertaining to the cannabis industry, and this industry faces significant opposition that could adversely affect this portion of our business.

One of our businesses makes and sells greenhouses and botanical extraction and processing equipment which may be sold to companies that cultivate, process and sell cannabis products for recreational and medicinal use. This business is dependent on state laws and regulations pertaining to the cannabis industry that legalize and regulate cannabis use. While several states have legalized cannabis for medical or recreational purposes, it remains illegal under federal law. Even in those states in which cannabis use has been legalized, its use remains a violation of federal criminal law, which preempts state laws that legalize its use. Strict enforcement of federal law regarding cannabis would likely have an adverse impact on our customers, and correspondingly, may adversely impact our gross profit, net income and cash flows.

The cultivation, processing and distribution of cannabis in states where it has been legalized is subject to significant regulatory requirements. If our customers who purchase greenhouses and extraction and processing equipment are unable to obtain and maintain the licenses, permits, authorizations or accreditations required to comply with state and local regulations, we may experience adverse effects on our business and results of operations.

Our business that engages in the sale of greenhouses and botanical extraction equipment is dependent, in part, on increasing legalization and market acceptance of medical and recreational cannabis use. We cannot predict the future increase in state legalization or the future market potential of legalized cannabis use. Other well-established business sectors with powerful economic influence may take action that could adversely impact the cannabis market. The failure of further legalization or market acceptance, or the adverse action by competing well-established business sectors, may suppress our customers’ demand for our products and thereby reduce our gross profit and net income.

Our business is highly competitive and increased competition could reduce our gross profit, net income, and cash flow.

The principal markets that we serve are highly competitive. Competition is based primarily on product functionality, quality, price, raw material and inventory availability, and the ability to meet delivery schedules dictated by customers. We compete in our principal markets with companies of various sizes, some of which have greater financial and other resources than we do, and some of which have better established brand names in the markets we serve. Increased competition could force us to lower our prices or to offer additional services or enhanced products at a higher cost to us, which could reduce our gross profit, net income, and cash flow and cause us to lose market share.

Our business and financial performance may be adversely affected by cybersecurity attacks, information systems interruptions, equipment failures, and technology integration.

Our business may be impacted by disruptions to our own or third-party information technology (“IT”) infrastructure, which could result from (among other causes) cyber-attacks on, or failures of, such infrastructure or compromises to its physical security, as well as from damaging weather or other acts of nature. Cyber-based risks, in particular, are evolving and include, but are not limited to, both attacks on our IT infrastructure and attacks on the IT infrastructure of third parties (both on premises and in the cloud) attempting to gain unauthorized access to our confidential or other proprietary information, classified information, or information relating to our employees, customers and other third parties.

Due to the evolving threat landscape, cyber-based attacks will continue and we may experience them going forward, potentially with more frequency. We continue to make investments and adopt measures designed to enhance our protection, detection, response, and recovery capabilities, and to mitigate potential risks to our technology, products,

12

services and operations from potential cyber-attacks. However, given the unpredictability, sophistication and scope of cyber-attacks, it is possible that potential vulnerabilities could go undetected for an extended period. We could potentially be subject to production downtimes, operational delays, other detrimental impacts on our operations or ability to provide products and services to our customers, the compromise of confidential or otherwise protected information, misappropriation of assets, destruction or corruption of data, security breaches, other manipulation or improper use of our or third-party systems, networks or products, financial losses from remedial actions, loss of business or potential liability, and/or damage to our reputation. Due to the evolving nature of such risks, the impact of any potential incident cannot be predicted, but under certain circumstances could materially and adversely affect our competitive position, results of operations and cash flows.

If the subcontractors and suppliers we rely upon do not perform to their contractual obligations, our revenues and cash flows would be adversely affected.

Several of our construction contracts with customers involve subcontracts with other companies that perform a portion of the services we provide to our customers. There is a risk that our subcontractors may not perform their contractual obligations, and therefore may cause disputes regarding the quality and timeliness of work performed by our subcontractors or customer concerns with the subcontractor. Any such disputes or concerns could materially and adversely impact our ability to perform our obligations as the prime contractor. Similarly, the failure by our suppliers to deliver raw materials, components or equipment parts according to schedule, or at all, may affect our ability to meet our customers' needs and may have an adverse effect upon our profitability. Failure of our raw materials or components to conform to our specification could also result in delays in our ability to timely deliver, and may have an adverse impact on our relationships with our customers, and our ability to fully realize the revenue expected from sales to those customers.

Our strategy depends on identification, management and successful business and system integration of future acquisitions.

Historically, we have grown through a combination of internal growth plus external expansion through acquisitions. We intend to continue to seek additional acquisition opportunities in accordance with our business strategy. However, we cannot provide any assurance that the following risks involved in completing acquisitions will not occur nor adversely impact our operations and financial results:

• | Failure to identify appropriate acquisition candidates, or, if we do, failure to successfully negotiate the terms of an acquisition; |

• | Diversion of senior management’s attention from existing business activities; |

• | Failure to integrate any acquisition into our operations successfully that may result in incurring unforeseen obligations, loss of key customers, suppliers, and employees of the acquired businesses, or loss of existing customers and suppliers; |

• | Difficulties or delays in integrating and assimilating information and systems that may require significant unforeseen upgrades or replacement of our primary information technology systems across significant parts of our businesses and operations to successfully integrate acquisitions. The implementation of new information technology solutions could lead to interruptions of information flow internally and to our customers and suppliers while the implementation project is being completed. Any failure to integrate legacy systems of acquisitions or to implement new systems properly could negatively impact our operations and financial results. |

• | Consummating a large acquisition could require us to raise additional funds through additional equity or debt financing, which could be dilutive to shareholder value, increase our interest expense and reduce our cash flows and available funds. |

• | Adverse impact on overall profitability if the acquired business does not achieve the return on investment projected at the time of acquisition. |

We depend on our senior management team and other key employees, and the unexpected loss of any member could adversely affect our operations.

Our success is dependent on the management and leadership skills of our senior executive and divisional management teams. The unexpected loss of any of these individuals or our inability to attract and retain additional personnel could prevent us from successfully executing our business strategy. We cannot assure you that we will be able to retain our existing senior management personnel or to attract additional qualified personnel when needed. We have not entered into employment agreements with any of our senior management personnel other than Frank G. Heard, our Vice Chairman of the Board.

13

We could incur substantial costs in order to comply with, or to address any violations of, environmental, health and safety laws.

Our operations and facilities are subject to a variety of stringent federal, state, local, and foreign laws and regulations relating to the protection of the environment and human health and safety. Compliance with these laws and regulations sometimes involves substantial operating costs and capital expenditures, and failure to maintain or achieve compliance with these laws and regulations or with the permits required for our operations could result in substantial costs and liabilities, such as fines and civil or criminal sanctions, third-party claims for property damage or personal injury, cleanup costs or temporary or permanent discontinuance of operations, including claims arising from the businesses and facilities that we have sold. For certain businesses we have divested, we have provided limited indemnifications for environmental contamination to the successor owners. We have also acquired and continue to acquire businesses and facilities to add to our operations. While we sometimes receive indemnification for pre-existing environmental contamination, the party providing the indemnification may not have sufficient resources to cover the cost of any required measures. Certain facilities of ours have been in operation for many years and we may be liable for remediation of any contamination at our current or former facilities; or at off-site locations where wastes have been sent for disposal, regardless of fault or whether we, our predecessors or others are responsible for such contamination. We have been responsible for remediation of contamination at some of our locations, and while such costs have not been material to date, the cost of remediation of any of these and any newly-discovered contamination cannot be quantified, and we cannot assure you that it will not materially affect our profits or cash flows. Changes in environmental laws, regulations or enforcement policies, including without limitation new or additional regulations affecting disposal of hazardous substances and waste, greenhouse gas emissions or use of fossil fuels, could have a material adverse effect on our business, financial condition, or results of operations.

Climate change and climate change legislation or regulations may adversely affect our business.

Legislative and regulatory changes in response to the potential effects of climate change may require additional costs and investment for compliance, including but not limited to, an increase in the cost of purchased energy and electricity. Physical effects of climate change, such as disruption in production and product distribution as a result of major storm events and shifts in regional weather patterns and intensities, may also significantly affect our operations and financial results.

Our operations are subject to seasonal fluctuations that may impact our cash flow.

Our net sales are generally lower in the first and fourth quarters primarily as a result of reduced activity in the building industry due to inclement weather. Therefore, our cash flow from operations may vary from quarter to quarter. If, as a result of any such fluctuation, our quarterly cash flows were significantly reduced, we may not be able to service our indebtedness or maintain covenant compliance.

Economic, political, and other risks associated with foreign operations could adversely affect our financial results and cash flows.

Although the large majority of our business activity takes place in the United States, we derive a portion of our revenues and earnings from operations in Canada, China and Japan, and are subject to risks associated with doing business internationally. Our sales originating outside the United States represented approximately 5% of our consolidated net sales during the year ended December 31, 2019. We believe that our business activities outside of the United States involve a higher degree of risk than our domestic activities, such as the possibility of unfavorable circumstances arising from host country laws or regulations, changes in tariff and trade barriers and import or export licensing requirements. In addition, any local or global health issue or uncertain political climates, international hostilities, natural disasters, or any terrorist activities could adversely affect customer demand, our operations and our ability to source and deliver products and services to our customers.

Future terror attacks, war, natural disasters or other catastrophic events beyond our control could negatively impact our operations and financial results.

Terror attacks, war, or other civil disturbances, natural disasters, other catastrophic events or public health crises, such as the coronavirus, could lead to economic instability, decreased capacity to produce our products and decreased demand for our products. From time to time, terrorist attacks worldwide have caused instability in global financial markets. Concerns over global climate changes and environmental sustainability over time or a prolonged virus outbreak may influence the Company's strategic direction, supply chain, or delivery channels. Also, our facilities could be subject to damage from fires, floods, earthquakes or other natural or man-made disasters. Such interruptions could have an adverse effect on our operations, cash flows and financial results.

14

The nature of our business exposes us to product liability, product warranty and other claims, and other legal proceedings.

We are involved in product liability, product warranty and other claims relating to the products we manufacture and distribute. Although we currently maintain what we believe to be suitable and adequate insurance in excess of our self-insured amounts for product liability and other claims, there can be no assurance that we will be able to maintain such insurance on acceptable terms or that such insurance will provide adequate protection against potential liabilities. Product liability claims can be expensive to defend and can divert the attention of management and other personnel for significant periods, regardless of the ultimate outcome. Claims of this nature could also have a negative impact on customer confidence in our products and our Company. We cannot assure you that any current or future claims will not adversely affect our reputation, financial condition, operating results, and cash flows.

If events occur or indicators of impairment are present that may cause the carrying value of long-lived and indefinite-lived assets to no longer be recoverable or to exceed the fair value of the asset, or that may lead to a reduction in the fair value of the asset, significant non-cash impairment charges to earnings may be taken that may have a material adverse impact on our results of operations.

In prior years, we have recorded significant non-cash impairment charges for goodwill and other intangible assets as a result of reductions in the estimated fair values of certain businesses. It is possible that we will be required to record additional non-cash impairment charges to our earnings in the future, which could be significant and have a material adverse impact on our results of operations. Refer to “Critical Accounting Estimates” within Item 7 of this Form 10-K for more detail of how our financial statements can be affected by asset impairment.

The expiration, elimination or reduction of solar rebates, credits and incentives may adversely impact our business.

A variety of federal, state and local government agencies provide incentives to promote electricity generation from renewable sources such as solar power. These incentives are in the form of rebates, tax credits and other financial incentives which help to motivate end users, distributors, system integrators and others to install solar powered generating systems. Any changes to reduce, shorten or eliminate the scope and availability of these incentive programs could materially and adversely impact the demand for our related products, our financial condition and results of operations.

Recently imposed tariffs and potential future tariffs may result in increased costs and could adversely affect our results of operations.

In 2018, the United States imposed Section 232 tariffs on certain steel (25%) and aluminum (10%) products imported into the U.S. These tariffs have created volatility in the market and have increased the costs of these inputs. Increased costs for imported steel and aluminum products have led domestic sellers to respond with market-based increases to prices for such inputs as well. The new tariffs, along with any additional tariffs or trade restrictions that may be implemented by the U.S. or other countries, could result in further increased costs, shifting in competitive positions and a decreased available supply of steel and aluminum as well as additional imported components and inputs. We may not be able to pass price increases on to our customers and may not be able to secure adequate alternative sources of steel and aluminum on a timely basis. While retaliatory tariffs imposed by other countries on U.S. goods have not yet had a significant impact, we cannot predict further developments. The tariffs could adversely affect the income from operations for some of our businesses and customer demand for some of our products which could have a material adverse effect on our consolidated results of operations, financial position and cash flows.

Item 1B. | Unresolved Staff Comments |

None.

15

Item 2. | Properties |

We lease our principal executive office and corporate headquarters in Buffalo, New York. The number, type, location and classification of the properties used by our operations by segment and corporate as of December 31, 2019, are as follows:

Number and type of properties | ||||||||||||

Plant | Distribution Center | Office | Total | |||||||||

Renewable Energy and Conservation | 8 | 2 | 3 | 13 | ||||||||

Residential Products | 11 | — | 2 | 13 | ||||||||

Industrial and Infrastructure Products | 10 | 3 | — | 13 | ||||||||

Corporate | — | — | 2 | 2 | ||||||||

Total | 29 | 5 | 7 | 41 | ||||||||

Location of properties | Classification of properties | |||||||||||

Domestic | Foreign | Owned | Leased | |||||||||

Renewable Energy and Conservation | 10 | 3 | 2 | 11 | ||||||||

Residential Products | 13 | — | 5 | 8 | ||||||||

Industrial and Infrastructure Products | 10 | 3 | 5 | 8 | ||||||||

Corporate | 2 | — | — | 2 | ||||||||

Total | 35 | 6 | 12 | 29 | ||||||||

We believe that our properties are effectively utilized, well maintained, in good condition, and will be able to accommodate our capacity needs to meet current levels of demand. In addition we believe that our properties are located to optimize customer service, market requirements, distribution capability and freight costs.

Item 3. | Legal Proceedings |

From time to time, the Company is named a defendant in legal actions arising out of the normal course of business. The Company is not a party to any material pending legal proceedings. The Company is also not a party to any other pending legal proceedings other than ordinary, routine litigation incidental to its business. The Company maintains liability insurance against risks arising out of the normal course of business.

Item 4. | Mine Safety Disclosures |

Not applicable.

16

PART II

Item 5. | Market for Common Equity and Related Stockholder Matters |

The Company’s common stock is traded on the NASDAQ Global Select Market (“NASDAQ”) under the symbol “ROCK.”

As of February 27, 2020, there were 39 shareholders of record of the Company’s common stock. However, the Company believes that it has a significantly higher number of beneficial owners because of the number of shares that are held by banks, brokers, and other financial institutions.

The Company did not declare any cash dividends during the years ended December 31, 2019 and 2018. The Company intends to use cash generated by operations to reinvest in the businesses and to fund acquisitions. The Company's disclosure in Item 7 of this Annual Report on Form 10-K regarding Liquidity and Capital Resources and disclosures in Note 9 of the Company’s audited consolidated financial statements included in Item 8 of this Annual Report on Form 10-K provide additional information regarding restrictions on potential dividends.

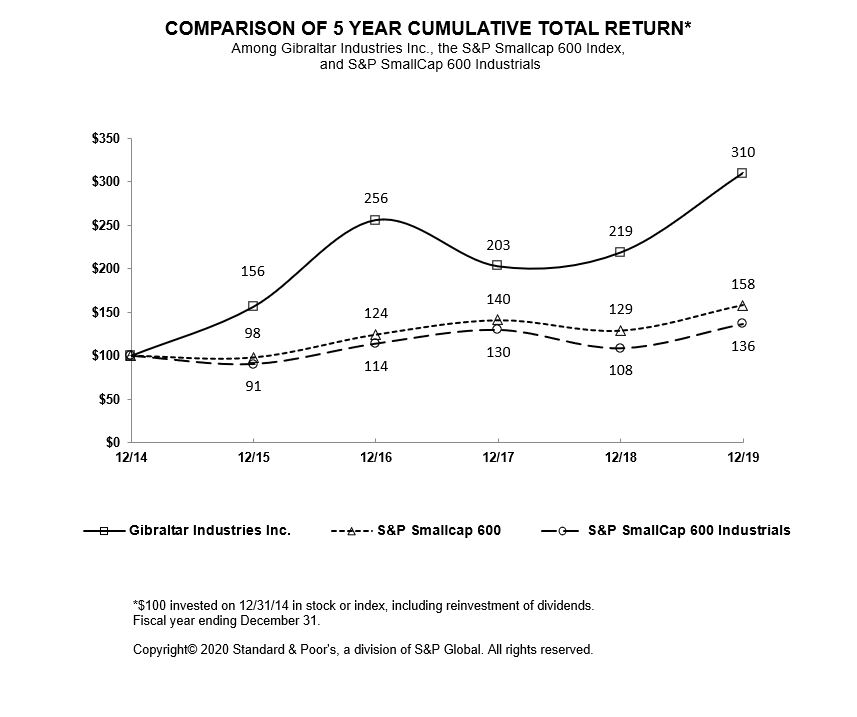

Performance Graph

The performance graph shown below compares the cumulative total shareholder return on the Company’s common stock, based on the market price of the common stock, with the total return of the S&P SmallCap 600 Index and the S&P SmallCap 600 Industrials Index for the five-year period ended December 31, 2019. The comparison of total return assumes that a fixed investment of $100 was invested on December 31, 2014 in common stock and in each of the foregoing indices and further assumes the reinvestment of dividends. The stock price performance shown on the graph is based on historical results and is not necessarily indicative of future price performance.

17

Item 6. | Selected Financial Data |

The selected historical consolidated financial data for each of the five years presented ended December 31 (in thousands, except per share data) are derived from the Company’s audited financial statements as reclassified for discontinued operations. The selected historical consolidated financial data should be read in conjunction with the Company’s audited consolidated financial statements and notes thereto contained in Item 8 and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” set forth in Item 7 of this Annual Report on Form 10-K. These historical results are not necessarily indicative of the results to be expected in any future periods.

Years Ended December 31, | |||||||||||||||||||

2019 | 2018 | 2017 | 2016 | 2015 | |||||||||||||||

Net sales | $ | 1,047,439 | $ | 1,002,372 | $ | 986,918 | $ | 1,007,981 | $ | 1,040,873 | |||||||||

Intangible asset impairment | $ | — | $ | 1,552 | $ | 247 | $ | 10,175 | $ | 4,863 | |||||||||

Income from operations | $ | 87,839 | $ | 93,968 | $ | 92,849 | $ | 73,488 | $ | 48,732 | |||||||||

Interest expense | $ | 2,205 | $ | 12,064 | $ | 14,032 | $ | 14,577 | $ | 15,003 | |||||||||

Income before taxes | $ | 84,763 | $ | 79,945 | $ | 77,908 | $ | 49,983 | $ | 37,100 | |||||||||

Provision for income taxes | $ | 19,672 | $ | 16,136 | $ | 14,943 | $ | 16,264 | $ | 13,624 | |||||||||

Income from continuing operations | $ | 65,091 | $ | 63,809 | $ | 62,965 | $ | 33,719 | $ | 23,476 | |||||||||

Income from continuing operations per share – Basic | $ | 2.01 | $ | 2.00 | $ | 1.98 | $ | 1.07 | $ | 0.75 | |||||||||

Weighted average shares outstanding – Basic | 32,389 | 31,979 | 31,701 | 31,536 | 31,233 | ||||||||||||||

Income from continuing operations per share – Diluted | $ | 1.99 | $ | 1.96 | $ | 1.95 | $ | 1.05 | $ | 0.74 | |||||||||

Weighted average shares outstanding – Diluted | 32,722 | 32,534 | 32,250 | 32,069 | 31,545 | ||||||||||||||

Current assets | $ | 437,102 | $ | 544,553 | $ | 462,764 | $ | 391,197 | $ | 351,422 | |||||||||

Current liabilities | $ | 229,197 | $ | 392,872 | $ | 171,033 | $ | 152,088 | $ | 185,395 | |||||||||

Total assets | $ | 984,450 | $ | 1,061,645 | $ | 991,385 | $ | 918,245 | $ | 889,772 | |||||||||

Total debt | $ | — | $ | 210,405 | $ | 210,021 | $ | 209,637 | $ | 209,282 | |||||||||

Total shareholders’ equity | $ | 673,964 | $ | 596,693 | $ | 531,719 | $ | 460,880 | $ | 410,086 | |||||||||

Capital expenditures | $ | 11,184 | $ | 12,457 | $ | 11,399 | $ | 10,779 | $ | 12,373 | |||||||||

Depreciation | $ | 12,678 | $ | 12,152 | $ | 12,929 | $ | 14,477 | $ | 17,869 | |||||||||

Amortization | $ | 7,271 | $ | 8,222 | $ | 8,761 | $ | 9,637 | $ | 12,679 | |||||||||

As described in Note 1 "Summary of Significant Accounting Policies" in the footnotes to the Company's consolidated financial statements, the Company adopted ASU No. 2016-02 - Leases (Topic 842) effective January 1, 2019 using the modified retrospective method. As such, all prior period information has not been restated and continues to be reported under the accounting standard in effect for that period.

18

Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

The following Management’s Discussion and Analysis of Financial Condition and Results of Operations should be read in conjunction with the Company’s risk factors and its consolidated financial statements and notes thereto included in Item 1A and Item 8, respectively, of this Annual Report on Form 10-K. Certain information set forth in this Item 7 constitutes “forward-looking statements” as that term is used in the Private Securities Litigation Reform Act of 1995. Such forward-looking statements are based, in whole or in part, on management’s beliefs, estimates, assumptions, and currently available information. For a more detailed discussion of what constitutes a forward-looking statement and of some of the factors that could cause actual results to differ materially from such forward-looking statements, please refer to the “Safe Harbor Statement” on page 3 of this Annual Report on Form 10-K.

We omitted discussion of results of operations for the year ended December 31, 2018 compared to the year ended December 31, 2017 where it would be redundant to the discussion previously included in Part II, Item 7, Results of Operations, in our Form 10-K for the fiscal year ended December 31, 2018 filed with the Securities and Exchange Commission on February 27, 2019.

We use certain operating performance measures, specifically consolidated gross margin, operating margin by segment and consolidated operating margin, to manage our businesses, set operational goals, and establish performance targets for incentive compensation for our employees. We define consolidated gross margin as a percentage of total consolidated gross profit to total consolidated net sales. We define operating margin by segment as a percentage of total income from operations by segment to total net sales by segment and consolidated operating margin as a percentage of total consolidated income from operations to total consolidated net sales. We believe gross margin and operating margin may be useful to investors in evaluating the profitability of our segments and Company on a consolidated basis.

Company Overview

Gibraltar Industries, Inc. (the "Company") is a leading manufacturer and provider of products and services for the renewable energy, conservation, residential, industrial and infrastructure markets. Gibraltar’s mission is to create compounding and sustainable value with strong leadership positions in higher growth, profitable end markets. At the beginning of 2019, after four years of steady improvement in operational execution and financial results under the leadership of Frank Heard, the Company announced the appointment of Bill Bosway as Chief Executive Officer, with Frank Heard vacating the CEO role and being appointed Executive Vice Chair of the Board through his planned retirement in March 2020. Under Bill’s leadership, management completed a thorough evaluation of the markets the Company participates in, as well as its position in each market. This work solidified the Company’s strategy and defined plans to accelerate growth and further improve the Company’s margin profile, both through organic and inorganic investment. It has also helped focus and prioritize the Company's key investments such that it deliver increasing returns and sustainable value for its shareholders.

Over the past twelve months, the Company migrated from a Four-Pillar strategy to a Three-Pillar strategy with the operating foundation focused on three core tenets: Business Systems, Portfolio Management, and Organizational Development.

1. | Business Systems, which combines two of the Company's previous strategic pillars - operational excellence and product innovation - is supported by an execution review of the Company's monthly business performance, implementation of key investments, IT operating and digital systems performance, and new product and services innovation. |

2. | Portfolio Management, which combines the two other previous strategic pillars - acquisitions and portfolio management - is focused on optimizing the Company’s business portfolio and ensuring our human and financial capital are invested to provide sustainable, profitable growth while expanding our relevance with customers and shaping our markets. The recent acquisitions of Apeks Supercritical, LLC ("Apeks") in August 2019, Thermo Energy Systems ("Thermo) in January 2020, and Delta Separations (“Delta”) in February 2020 were the direct result of our portfolio management strategy. |

3. | Organizational Development is the third pillar of our strategy. In order to execute Business Systems and Portfolio Management, the Company must have a strong organization to execute, and the organization must continuously develop and improve. The Company aspires to make our place of work the "Best Place to Work", where we focus on creating the best development and learning environment for our people, proactively operate |

19

businesses that solve global challenges, and engage and support the communities we are present in. We believe doing so helps us attract and retain the best people so we can execute our business plans.

In addition to migrating from a Four-Pillar strategy to a Three-Pillar strategy over the past twelve months, the Company:

• | Implemented new management tools to complement our core 80/20 toolkit and drive improvements in our operating margins; |

• | Increased the percentage of our sales that are direct to end customer, allowing us to have a more meaningful connection with our end customer, providing the opportunity to better understand the challenges our customers face, and developing solutions to these challenges; and |

• | Continued to shift the focus of our portfolio to take advantage of rising tides in the renewable energy and conservation markets. |

The Company serves customers primarily in North America including renewable energy (solar) developers, institutional and commercial growers of food and plants, home improvement retailers, wholesalers, distributors, and contractors. As of December 31, 2019, we operated 41 facilities in 18 states, Canada, China and Japan which includes 29 manufacturing facilities and five distribution centers. Our operational infrastructure provides the necessary scale to support local, regional, and national customers in each of our markets.

The Company operates and reports its results in the following three reporting segments:

• | Renewable Energy and Conservation; |

• | Residential Products; and |

• | Industrial and Infrastructure Products. |