Magnera Corp - Quarter Report: 2016 September (Form 10-Q)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

|

☒ |

Quarterly Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the quarterly period ended September 30, 2016

or

|

☐ |

Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to

96 South George Street, Suite 520

York, Pennsylvania 17401

(Address of principal executive offices)

(717) 225-4711

(Registrant's telephone number, including area code)

|

|

Commission file number |

|

Exact name of registrant as specified in its charter |

|

IRS Employer Identification No. |

|

State or other jurisdiction of incorporation or organization |

|

|

|

1-03560 |

|

P. H. Glatfelter Company |

|

23-0628360 |

|

Pennsylvania |

|

N/A

(Former name or former address, if changed since last report)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for at the past 90 days. Yes ☒ No ☐.

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a small reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer |

☒ |

|

Accelerated filer |

☐ |

|

Non-accelerated filer |

☐ |

(Do not check if a smaller reporting company) |

Smaller reporting company |

☐ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) Yes ☐ No ☒.

Common Stock outstanding on October 25, 2016 totaled 43,549,639 shares.

P. H. GLATFELTER COMPANY AND SUBSIDIARIES

REPORT ON FORM 10-Q

For the QUARTERLY PERIOD ENDED

September 30, 2016

Table of Contents

|

|

Page |

|

Page |

|

|

|

|||

|

|

|

|

|

|

|

Item 1 |

|

|

||

|

|

|

2 |

||

|

|

|

3 |

||

|

|

Condensed Consolidated Balance Sheets as of September 30, 2016 and December 31, 2015 (unaudited) |

|

4 |

|

|

|

|

5 |

||

|

|

Notes to Condensed Consolidated Financial Statements (unaudited) |

|

6 |

|

|

|

1. |

|

6 |

|

|

|

2. |

|

6 |

|

|

|

3. |

|

7 |

|

|

|

4. |

|

8 |

|

|

|

5. |

|

10 |

|

|

|

6. |

|

10 |

|

|

7. |

|

11 |

||

|

|

8. |

|

12 |

|

|

|

9. |

|

12 |

|

|

|

10. |

|

13 |

|

|

|

11. |

|

13 |

|

|

|

12. |

|

15 |

|

|

|

13. |

|

19 |

|

|

|

14. |

|

20 |

|

|

|

|

|

|

|

|

Item 2 |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

27 |

|

|

Item 3 |

|

37 |

||

|

Item 4 |

|

37 |

||

|

|

|

|

||

|

|

38 |

|||

|

|

|

|

|

|

|

Item 6 |

|

38 |

||

|

|

|

|

|

|

|

|

|

38 |

||

P. H. GLATFELTER COMPANY AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF INCOME

(unaudited)

|

|

Three months ended September 30 |

|

|

Nine months ended September 30 |

|

||||||||||

|

In thousands, except per share |

2016 |

|

|

2015 |

|

|

2016 |

|

|

2015 |

|

||||

|

Net sales |

$ |

405,301 |

|

|

$ |

419,960 |

|

|

$ |

1,213,932 |

|

|

$ |

1,248,232 |

|

|

Energy and related sales, net |

|

1,346 |

|

|

|

1,153 |

|

|

|

4,013 |

|

|

|

3,936 |

|

|

Total revenues |

|

406,647 |

|

|

|

421,113 |

|

|

|

1,217,945 |

|

|

|

1,252,168 |

|

|

Costs of products sold |

|

345,477 |

|

|

|

361,205 |

|

|

|

1,056,209 |

|

|

|

1,107,319 |

|

|

Gross profit |

|

61,170 |

|

|

|

59,908 |

|

|

|

161,736 |

|

|

|

144,849 |

|

|

Selling, general and administrative expenses |

|

35,747 |

|

|

|

39,792 |

|

|

|

104,796 |

|

|

|

100,201 |

|

|

Losses (gains) on dispositions of plant, equipment and timberlands, net |

|

5 |

|

|

|

(123 |

) |

|

|

31 |

|

|

|

(2,888 |

) |

|

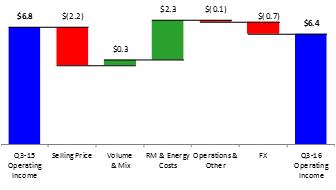

Operating income |

|

25,418 |

|

|

|

20,239 |

|

|

|

56,909 |

|

|

|

47,536 |

|

|

Non-operating income (expense) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest expense |

|

(3,895 |

) |

|

|

(4,317 |

) |

|

|

(11,964 |

) |

|

|

(13,177 |

) |

|

Interest income |

|

52 |

|

|

|

90 |

|

|

|

204 |

|

|

|

232 |

|

|

Other, net |

|

(573 |

) |

|

|

(220 |

) |

|

|

(956 |

) |

|

|

(192 |

) |

|

Total non-operating expense |

|

(4,416 |

) |

|

|

(4,447 |

) |

|

|

(12,716 |

) |

|

|

(13,137 |

) |

|

Income before income taxes |

|

21,002 |

|

|

|

15,792 |

|

|

|

44,193 |

|

|

|

34,399 |

|

|

Income tax provision |

|

1,401 |

|

|

|

2,288 |

|

|

|

6,459 |

|

|

|

4,122 |

|

|

Net income |

$ |

19,601 |

|

|

$ |

13,504 |

|

|

$ |

37,734 |

|

|

$ |

30,277 |

|

|

Earnings per share |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

$ |

0.45 |

|

|

$ |

0.31 |

|

|

$ |

0.87 |

|

|

$ |

0.70 |

|

|

Diluted |

|

0.44 |

|

|

|

0.31 |

|

|

|

0.86 |

|

|

|

0.69 |

|

|

Cash dividends declared per common share |

$ |

0.125 |

|

|

$ |

0.12 |

|

|

$ |

0.375 |

|

|

$ |

0.36 |

|

|

Weighted average shares outstanding |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

|

43,576 |

|

|

|

43,457 |

|

|

|

43,552 |

|

|

|

43,363 |

|

|

Diluted |

|

44,133 |

|

|

|

43,865 |

|

|

|

44,059 |

|

|

|

43,949 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

- 2 -

GLATFELTER

9.30.16 Form 10-Q

P. H. GLATFELTER COMPANY AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(unaudited)

|

|

Three months ended September 30 |

|

|

Nine months ended September 30 |

|

||||||||||

|

In thousands |

2016 |

|

|

2015 |

|

|

2016 |

|

|

2015 |

|

||||

|

Net income |

$ |

19,601 |

|

|

$ |

13,504 |

|

|

$ |

37,734 |

|

|

$ |

30,277 |

|

|

Foreign currency translation adjustments |

|

(1,530 |

) |

|

|

(3,262 |

) |

|

|

(2,975 |

) |

|

|

(27,895 |

) |

|

Net change in: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Deferred (gains) losses on cash flow hedges, net of taxes |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

of $289, $1,045, $88 and $938, respectively |

|

(858 |

) |

|

|

(2,823 |

) |

|

|

152 |

|

|

|

(2,558 |

) |

|

Unrecognized retirement obligations, net of taxes |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

of $(1,405), $(1,895), $(4,214) and $(5,675), respectively |

|

2,319 |

|

|

|

3,083 |

|

|

|

6,957 |

|

|

|

9,253 |

|

|

Other comprehensive income (loss) |

|

(69 |

) |

|

|

(3,002 |

) |

|

|

4,134 |

|

|

|

(21,200 |

) |

|

Comprehensive income |

$ |

19,532 |

|

|

$ |

10,502 |

|

|

$ |

41,868 |

|

|

$ |

9,077 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

- 3 -

GLATFELTER

9.30.16 Form 10-Q

P. H. GLATFELTER COMPANY AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(unaudited)

|

|

September 30 |

|

|

December 31 |

|

||

|

In thousands |

2016 |

|

|

2015 |

|

||

|

Assets |

|

|

|

|

|

|

|

|

Cash and cash equivalents |

$ |

50,752 |

|

|

$ |

105,304 |

|

|

Accounts receivable, net |

|

179,352 |

|

|

|

167,199 |

|

|

Inventories |

|

262,891 |

|

|

|

247,214 |

|

|

Prepaid expenses and other current assets |

|

36,573 |

|

|

|

32,650 |

|

|

Total current assets |

|

529,568 |

|

|

|

552,367 |

|

|

Plant, equipment and timberlands, net |

|

771,453 |

|

|

|

698,864 |

|

|

Goodwill |

|

77,268 |

|

|

|

76,056 |

|

|

Intangible assets |

|

60,721 |

|

|

|

63,057 |

|

|

Other assets |

|

115,229 |

|

|

|

110,072 |

|

|

Total assets |

$ |

1,554,239 |

|

|

$ |

1,500,416 |

|

|

Liabilities and Shareholders' Equity |

|

|

|

|

|

|

|

|

Current portion of long-term debt |

$ |

11,432 |

|

|

$ |

7,366 |

|

|

Accounts payable |

|

163,674 |

|

|

|

172,735 |

|

|

Dividends payable |

|

5,455 |

|

|

|

5,231 |

|

|

Environmental liabilities |

|

8,408 |

|

|

|

12,544 |

|

|

Other current liabilities |

|

127,149 |

|

|

|

106,444 |

|

|

Total current liabilities |

|

316,118 |

|

|

|

304,320 |

|

|

Long-term debt |

|

367,549 |

|

|

|

353,296 |

|

|

Deferred income taxes |

|

73,075 |

|

|

|

76,458 |

|

|

Other long-term liabilities |

|

105,808 |

|

|

|

103,095 |

|

|

Total liabilities |

|

862,550 |

|

|

|

837,169 |

|

|

Commitments and contingencies |

|

— |

|

|

|

— |

|

|

Shareholders’ equity |

|

|

|

|

|

|

|

|

Common stock |

|

544 |

|

|

|

544 |

|

|

Capital in excess of par value |

|

55,890 |

|

|

|

54,912 |

|

|

Retained earnings |

|

984,520 |

|

|

|

963,143 |

|

|

Accumulated other comprehensive loss |

|

(186,352 |

) |

|

|

(190,486 |

) |

|

|

|

854,602 |

|

|

|

828,113 |

|

|

Less cost of common stock in treasury |

|

(162,913 |

) |

|

|

(164,866 |

) |

|

Total shareholders’ equity |

|

691,689 |

|

|

|

663,247 |

|

|

Total liabilities and shareholders’ equity |

$ |

1,554,239 |

|

|

$ |

1,500,416 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

- 4 -

GLATFELTER

9.30.16 Form 10-Q

P. H. GLATFELTER COMPANY AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(unaudited)

|

|

Nine months ended September 30 |

|

|||||

|

In thousands |

2016 |

|

|

2015 |

|

||

|

Operating activities |

|

|

|

|

|

|

|

|

Net income |

$ |

37,734 |

|

|

$ |

30,277 |

|

|

Adjustments to reconcile to net cash provided by operations: |

|

|

|

|

|

|

|

|

Depreciation, depletion and amortization |

|

49,725 |

|

|

|

47,423 |

|

|

Amortization of debt issue costs |

|

864 |

|

|

|

893 |

|

|

Pension expense, net of unfunded benefits paid |

|

2,908 |

|

|

|

5,541 |

|

|

Charge for impairment of intangible asset |

|

— |

|

|

|

1,200 |

|

|

Deferred income tax benefit |

|

(4,266 |

) |

|

|

(2,043 |

) |

|

Losses (gains) on dispositions of plant, equipment and timberlands, net |

|

31 |

|

|

|

(2,888 |

) |

|

Share-based compensation |

|

4,218 |

|

|

|

5,502 |

|

|

Change in operating assets and liabilities |

|

|

|

|

|

|

|

|

Accounts receivable |

|

(12,927 |

) |

|

|

(21,572 |

) |

|

Inventories |

|

(17,897 |

) |

|

|

(5,714 |

) |

|

Prepaid and other current assets |

|

(4,205 |

) |

|

|

420 |

|

|

Accounts payable |

|

(9,662 |

) |

|

|

5,561 |

|

|

Accruals and other current liabilities |

|

10,257 |

|

|

|

5,180 |

|

|

Other |

|

2,657 |

|

|

|

743 |

|

|

Net cash provided by operating activities |

|

59,437 |

|

|

|

70,523 |

|

|

Investing activities |

|

|

|

|

|

|

|

|

Expenditures for purchases of plant, equipment and timberlands |

|

(116,948 |

) |

|

|

(74,280 |

) |

|

Proceeds from disposals of plant, equipment and timberlands, net |

|

55 |

|

|

|

3,181 |

|

|

Acquisition, net of cash acquired |

|

— |

|

|

|

(224 |

) |

|

Other |

|

(400 |

) |

|

|

(1,600 |

) |

|

Net cash used by investing activities |

|

(117,293 |

) |

|

|

(72,923 |

) |

|

Financing activities |

|

|

|

|

|

|

|

|

Net repayments of revolving credit facility |

|

(642 |

) |

|

|

— |

|

|

Payments of borrowing costs |

|

(136 |

) |

|

|

(1,329 |

) |

|

Proceeds from term loans |

|

19,428 |

|

|

|

— |

|

|

Repayment of term loans |

|

(3,803 |

) |

|

|

(3,387 |

) |

|

Payments of dividends |

|

(16,134 |

) |

|

|

(15,215 |

) |

|

Proceeds from government grants |

|

5,251 |

|

|

|

— |

|

|

Payments related to share-based compensation awards and other |

|

(990 |

) |

|

|

(2,015 |

) |

|

Net cash provided (used) by financing activities |

|

2,974 |

|

|

|

(21,946 |

) |

|

Effect of exchange rate changes on cash |

|

330 |

|

|

|

(1,826 |

) |

|

Net decrease in cash and cash equivalents |

|

(54,552 |

) |

|

|

(26,172 |

) |

|

Cash and cash equivalents at the beginning of period |

|

105,304 |

|

|

|

99,837 |

|

|

Cash and cash equivalents at the end of period |

$ |

50,752 |

|

|

$ |

73,665 |

|

|

|

|

|

|

|

|

|

|

|

Supplemental cash flow information |

|

|

|

|

|

|

|

|

Cash paid for: |

|

|

|

|

|

|

|

|

Interest, net of amounts capitalized |

$ |

7,376 |

|

|

$ |

8,943 |

|

|

Income taxes, net |

|

11,609 |

|

|

|

14,566 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

- 5 -

GLATFELTER

9.30.16 Form 10-Q

P. H. GLATFELTER COMPANY AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

|

1. |

P. H. Glatfelter Company and subsidiaries (“Glatfelter”) is a manufacturer of specialty papers and fiber-based engineered materials. Headquartered in York, PA, U.S. operations include facilities in Spring Grove, PA and Chillicothe and Fremont, OH. International operations include facilities in Canada, Germany, France, the United Kingdom and the Philippines, and sales and distribution offices in Russia and China. The terms “we,” “us,” “our,” “the Company,” or “Glatfelter,” refer to P. H. Glatfelter Company and subsidiaries unless the context indicates otherwise. Our products are marketed worldwide, either through wholesale paper merchants, brokers and agents, or directly to customers.

|

2. |

Basis of Presentation The unaudited condensed consolidated financial statements (“financial statements”) include the accounts of Glatfelter and its wholly-owned subsidiaries. All intercompany balances and transactions have been eliminated.

We prepared these financial statements in accordance with accounting principles generally accepted in the United States of America (“generally accepted accounting principles” or “GAAP”) and pursuant to the rules and regulations of the Securities and Exchange Commission pertaining to interim financial statements. In our opinion, the financial statements reflect all normal, recurring adjustments needed to present fairly our results for the interim periods. When preparing these financial statements, we have assumed that you have read the audited consolidated financial statements included in our 2015 Annual Report on Form 10-K.

Accounting Estimates The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingencies as of the balance sheet date and the reported amounts of revenues and expenses during the reporting period. Management believes the estimates and assumptions used in the preparation of these financial statements are reasonable, based upon currently available facts and known circumstances, but recognizes that actual results may differ from those estimates and assumptions.

Recently Issued Accounting Pronouncements In March 2016, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) No. 2016-09, Compensation – Stock Compensation (Topic 718) Improvements to Employee Share-Based Payment Accounting designed to simplify certain aspects of accounting for share-

based awards. The new ASU requires entities to recognize as a component of income tax expense all excess tax benefits or deficiencies arising from the difference between compensation costs recognized and the intrinsic value at the time an option is exercised or, in the case of restricted stock and similar awards, the fair value upon vesting of an award. Previously such differences were recognized in additional paid in capital as part of an “APIC pool.” In addition, the ASU also requires entities to exclude excess tax benefits and tax deficiencies from the calculation of common share equivalents for purposes of calculating earnings per share. The new standard is required to be adopted, either prospectively or retrospectively, in the first quarter of 2017 and early adoption is permitted. We do not believe the adoption of this standard will have a material impact on our reported results of operations or financial position.

In February 2016, the FASB issued ASU No. 2016-02, Leases (Topic 842). This ASU will require organizations such as us that lease assets to recognize on the balance sheet the assets and liabilities for the rights and obligations created by those leases. The new guidance will be effective for annual periods beginning after December 15, 2018, and interim periods therein. Early adoption is permitted. We are in the process of assessing the impact this standard will have on us and expect to follow a modified retrospective method provided for under the standard.

In May 2014, the FASB issued ASU No. 2014-09, Revenue from Contracts with Customers which clarifies the principles for recognizing revenue and develops a common revenue standard for GAAP and International Financial Reporting Standards. The new standard is required to be adopted retrospectively for fiscal years beginning after December 15, 2017 and early adoption is permitted only for reporting periods beginning after December 31, 2016. We are in the process of evaluating the impact this standard may have, if any, on our reported results of operations or financial position.

In June 2016, the FASB issued ASU No. 2016-13 Financial Instruments—Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments that changes the impairment model for most financial instruments, including trade receivables from an incurred loss method to a new forward-looking approach, based on expected losses. Under the new guidance, an allowance is recognized based on an estimate of expected credit losses. This standard is effective for us in the first quarter of 2020 and must be adopted using a modified retrospective transition approach. We are currently assessing the impact this standard may have on our results of operations and financial position.

- 6 -

GLATFELTER

9.30.16 Form 10-Q

|

3. |

The following table sets forth the details of basic and diluted earnings per share (“EPS”):

|

|

Three months ended September 30 |

|

|||||

|

In thousands, except per share |

2016 |

|

|

2015 |

|

||

|

Net income |

$ |

19,601 |

|

|

$ |

13,504 |

|

|

Weighted average common shares |

|

|

|

|

|

|

|

|

outstanding used in basic EPS |

|

43,576 |

|

|

|

43,457 |

|

|

Common shares issuable upon |

|

|

|

|

|

|

|

|

exercise of dilutive stock options |

|

|

|

|

|

|

|

|

and PSAs / RSUs |

|

557 |

|

|

|

408 |

|

|

Weighted average common shares |

|

|

|

|

|

|

|

|

outstanding and common share |

|

|

|

|

|

|

|

|

equivalents used in diluted EPS |

|

44,133 |

|

|

|

43,865 |

|

|

Earnings per share |

|

|

|

|

|

|

|

|

Basic |

$ |

0.45 |

|

|

$ |

0.31 |

|

|

Diluted |

|

0.44 |

|

|

|

0.31 |

|

|

Nine months ended September 30 |

|

||||||

|

In thousands, except per share |

2016 |

|

|

2015 |

|

||

|

Net income |

$ |

37,734 |

|

|

$ |

30,277 |

|

|

Weighted average common shares |

|

|

|

|

|

|

|

|

outstanding used in basic EPS |

|

43,552 |

|

|

|

43,363 |

|

|

Common shares issuable upon |

|

|

|

|

|

|

|

|

exercise of dilutive stock options |

|

|

|

|

|

|

|

|

and PSAs / RSUs |

|

507 |

|

|

|

586 |

|

|

Weighted average common shares |

|

|

|

|

|

|

|

|

outstanding and common share |

|

|

|

|

|

|

|

|

equivalents used in diluted EPS |

|

44,059 |

|

|

|

43,949 |

|

|

Earnings per share |

|

|

|

|

|

|

|

|

Basic |

$ |

0.87 |

|

|

$ |

0.70 |

|

|

Diluted |

|

0.86 |

|

|

|

0.69 |

|

The following table sets forth potential common shares outstanding that were not included in the computation of diluted EPS for the period indicated, because their effect would be anti-dilutive:

|

|

September 30 |

|

|||||

|

In thousands |

2016 |

|

|

2015 |

|

||

|

Three months ended |

|

681 |

|

|

|

696 |

|

|

Nine months ended |

|

683 |

|

|

|

696 |

|

- 7 -

GLATFELTER

9.30.16 Form 10-Q

The following table sets forth details of the changes in accumulated other comprehensive income (losses) for the three months and nine months ended September 30, 2016 and 2015.

|

In thousands |

Currency translation adjustments |

|

|

Unrealized gain (loss) on cash flow hedges |

|

|

Change in pensions |

|

|

Change in other postretirement defined benefit plans |

|

|

Total |

|

|||||

|

Balance at July 1, 2016 |

$ |

(74,486 |

) |

|

$ |

785 |

|

|

$ |

(115,786 |

) |

|

$ |

3,204 |

|

|

$ |

(186,283 |

) |

|

Other comprehensive income before reclassifications (net of tax) |

|

(1,530 |

) |

|

|

(1,195 |

) |

|

|

--- |

|

|

|

--- |

|

|

|

(2,725 |

) |

|

Amounts reclassified from accumulated other comprehensive income (net of tax) |

|

— |

|

|

|

337 |

|

|

|

2,464 |

|

|

|

(145 |

) |

|

|

2,656 |

|

|

Net current period other comprehensive income (loss) |

|

(1,530 |

) |

|

|

(858 |

) |

|

|

2,464 |

|

|

|

(145 |

) |

|

|

(69 |

) |

|

Balance at September 30, 2016 |

$ |

(76,016 |

) |

|

$ |

(73 |

) |

|

$ |

(113,322 |

) |

|

$ |

3,059 |

|

|

$ |

(186,352 |

) |

|

Balance at July 1, 2015 |

$ |

(58,857 |

) |

|

$ |

2,621 |

|

|

$ |

(114,076 |

) |

|

$ |

(2,756 |

) |

|

$ |

(173,068 |

) |

|

Other comprehensive income before reclassifications (net of tax) |

|

(3,262 |

) |

|

|

(1,381 |

) |

|

|

--- |

|

|

|

--- |

|

|

|

(4,643 |

) |

|

Amounts reclassified from accumulated other comprehensive income (net of tax) |

|

— |

|

|

|

(1,442 |

) |

|

|

3,090 |

|

|

|

(7 |

) |

|

|

1,641 |

|

|

Net current period other comprehensive income (loss) |

|

(3,262 |

) |

|

|

(2,823 |

) |

|

|

3,090 |

|

|

|

(7 |

) |

|

|

(3,002 |

) |

|

Balance at September 30, 2015 |

$ |

(62,119 |

) |

|

$ |

(202 |

) |

|

$ |

(110,986 |

) |

|

$ |

(2,763 |

) |

|

$ |

(176,070 |

) |

|

In thousands |

Currency translation adjustments |

|

|

Unrealized gain (loss) on cash flow hedges |

|

|

Change in pensions |

|

|

Change in other postretirement defined benefit plans |

|

|

Total |

|

|||||

|

Balance at January 1, 2016 |

$ |

(73,041 |

) |

|

$ |

(225 |

) |

|

$ |

(120,714 |

) |

|

$ |

3,494 |

|

|

$ |

(190,486 |

) |

|

Other comprehensive income before reclassifications (net of tax) |

|

(2,975 |

) |

|

|

(106 |

) |

|

|

--- |

|

|

|

--- |

|

|

|

(3,081 |

) |

|

Amounts reclassified from accumulated other comprehensive income (net of tax) |

|

— |

|

|

|

258 |

|

|

|

7,392 |

|

|

|

(435 |

) |

|

|

7,215 |

|

|

Net current period other comprehensive income (loss) |

|

(2,975 |

) |

|

|

152 |

|

|

|

7,392 |

|

|

|

(435 |

) |

|

|

4,134 |

|

|

Balance at September 30, 2016 |

$ |

(76,016 |

) |

|

$ |

(73 |

) |

|

$ |

(113,322 |

) |

|

$ |

3,059 |

|

|

$ |

(186,352 |

) |

|

Balance at January 1, 2015 |

$ |

(34,224 |

) |

|

$ |

2,356 |

|

|

$ |

(120,260 |

) |

|

$ |

(2,742 |

) |

|

$ |

(154,870 |

) |

|

Other comprehensive income before reclassifications (net of tax) |

|

(27,895 |

) |

|

|

793 |

|

|

|

--- |

|

|

|

--- |

|

|

|

(27,102 |

) |

|

Amounts reclassified from accumulated other comprehensive income (net of tax) |

|

— |

|

|

|

(3,351 |

) |

|

|

9,274 |

|

|

|

(21 |

) |

|

|

5,902 |

|

|

Net current period other comprehensive income (loss) |

|

(27,895 |

) |

|

|

(2,558 |

) |

|

|

9,274 |

|

|

|

(21 |

) |

|

|

(21,200 |

) |

|

Balance at September 30, 2015 |

$ |

(62,119 |

) |

|

$ |

(202 |

) |

|

$ |

(110,986 |

) |

|

$ |

(2,763 |

) |

|

$ |

(176,070 |

) |

- 8 -

GLATFELTER

9.30.16 Form 10-Q

Reclassifications out of accumulated other comprehensive income were as follows:

|

|

|

Three months ended September 30 |

|

|

Nine months ended September 30 |

|

|

|

||||||||||

|

In thousands |

|

2016 |

|

|

2015 |

|

|

2016 |

|

|

2015 |

|

|

|

||||

|

Description |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Line Item in Statements of Income |

|

Cash flow hedges (Note 11) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Gains) losses on cash flow hedges |

|

$ |

347 |

|

|

$ |

(1,972 |

) |

|

$ |

264 |

|

|

$ |

(4,595 |

) |

|

Costs of products sold |

|

Tax expense (benefit) |

|

|

(10 |

) |

|

|

530 |

|

|

|

(6 |

) |

|

|

1,244 |

|

|

Income tax provision |

|

Net of tax |

|

|

337 |

|

|

|

(1,442 |

) |

|

|

258 |

|

|

|

(3,351 |

) |

|

|

|

Retirement plan obligations (Note 7) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Amortization of deferred benefit pension plan items |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Prior service costs |

|

|

506 |

|

|

|

571 |

|

|

|

1,519 |

|

|

|

1,713 |

|

|

Costs of products sold |

|

|

|

|

168 |

|

|

|

189 |

|

|

|

504 |

|

|

|

568 |

|

|

Selling, general and administrative |

|

Actuarial losses |

|

|

2,450 |

|

|

|

3,144 |

|

|

|

7,350 |

|

|

|

9,432 |

|

|

Costs of products sold |

|

|

|

|

843 |

|

|

|

1,082 |

|

|

|

2,530 |

|

|

|

3,247 |

|

|

Selling, general and administrative |

|

|

|

|

3,967 |

|

|

|

4,986 |

|

|

|

11,903 |

|

|

|

14,960 |

|

|

|

|

Tax benefit |

|

|

(1,503 |

) |

|

|

(1,896 |

) |

|

|

(4,511 |

) |

|

|

(5,686 |

) |

|

Income tax provision |

|

Net of tax |

|

|

2,464 |

|

|

|

3,090 |

|

|

|

7,392 |

|

|

|

9,274 |

|

|

|

|

Amortization of deferred benefit other plan items |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Prior service costs |

|

|

(37 |

) |

|

|

(58 |

) |

|

|

(112 |

) |

|

|

(173 |

) |

|

Costs of products sold |

|

|

|

|

(8 |

) |

|

|

(12 |

) |

|

|

(24 |

) |

|

|

(37 |

) |

|

Selling, general and administrative |

|

Actuarial losses |

|

|

(156 |

) |

|

|

48 |

|

|

|

(467 |

) |

|

|

142 |

|

|

Costs of products sold |

|

|

|

|

(33 |

) |

|

|

10 |

|

|

|

(100 |

) |

|

|

31 |

|

|

Selling, general and administrative |

|

|

|

|

(234 |

) |

|

|

(12 |

) |

|

|

(703 |

) |

|

|

(37 |

) |

|

|

|

Tax expense |

|

|

89 |

|

|

|

5 |

|

|

|

268 |

|

|

|

16 |

|

|

Income tax provision |

|

Net of tax |

|

|

(145 |

) |

|

|

(7 |

) |

|

|

(435 |

) |

|

|

(21 |

) |

|

|

|

Total reclassifications, net of tax |

|

$ |

2,656 |

|

|

$ |

1,641 |

|

|

$ |

7,215 |

|

|

$ |

5,902 |

|

|

|

- 9 -

GLATFELTER

9.30.16 Form 10-Q

|

5. |

Income taxes are recognized for the amount of taxes payable or refundable for the current year and deferred tax liabilities and assets for the future tax consequences of events that have been recognized in our consolidated financial statements or tax returns. The effects of income taxes are measured based on enacted tax laws and rates.

As of September 30, 2016 and December 31, 2015, we had $15.2 million and $12.2 million of gross unrecognized tax benefits. As of September 30, 2016, if such benefits were to be recognized, approximately $12.2 million would be recorded as a component of income tax expense, thereby affecting our effective tax rate.

We, or one of our subsidiaries, file income tax returns with the United States Internal Revenue Service, as well as various state and foreign authorities.

The following table summarizes, by major jurisdiction, tax years that remain subject to examination:

|

|

Open Tax Years |

||

|

Jurisdiction |

Examinations not yet initiated |

|

Examination in progress |

|

United States |

|

|

|

|

Federal |

2013 - 2015 |

|

N/A |

|

State |

2011 - 2015 |

|

2014 |

|

Canada (1) |

2010 - 2015 |

|

N/A |

|

Germany (1) |

2012 - 2015 |

|

2007 - 2011 |

|

France |

2013 - 2015 |

|

2011 - 2012 |

|

United Kingdom |

2014 - 2015 |

|

N/A |

|

Philippines |

2015 |

|

2013, 2014 |

|

(1) |

includes provincial or similar local jurisdictions, as applicable |

The amount of income taxes we pay is subject to ongoing audits by federal, state and foreign tax authorities, which often result in proposed assessments. Management performs a comprehensive review of its global tax positions on a quarterly basis and accrues amounts for uncertain tax positions. Based on these reviews and the result of discussions and resolutions of matters with certain tax authorities and the closure of tax years subject to tax audit, reserves are adjusted as necessary. However, future results may include favorable or unfavorable adjustments to our estimated tax liabilities in the period the assessments are determined or resolved or as such statutes are closed. Due to potential for resolution of federal, state and foreign examinations, and the lapse of various statutes of limitation, it is reasonably possible our gross unrecognized tax benefits balance may decrease within the next twelve months by a range of zero to $1.8 million. Substantially all of this range relates to tax positions taken in Germany.

We recognize interest and penalties related to uncertain tax positions as income tax expense. The following table summarizes information related to interest and penalties on uncertain tax positions:

|

|

Nine months ended September 30 |

|

|||||

|

In millions |

2016 |

|

|

2015 |

|

||

|

Interest expense |

$ |

0.2 |

|

|

$ |

— |

|

|

Penalties |

|

— |

|

|

|

— |

|

|

|

September 30 |

|

|

December 31 |

|

||

|

|

2016 |

|

|

2015 |

|

||

|

Accrued interest payable |

$ |

0.8 |

|

|

$ |

0.6 |

|

The P. H. Glatfelter Amended and Restated Long Term Incentive Plan (the “LTIP”) provides for the issuance of Glatfelter common stock to eligible participants in the form of restricted stock units, restricted stock awards, non-qualified stock options, performance shares, incentive stock options and performance units.

Pursuant to terms of the LTIP, we have issued to eligible participants restricted stock units, performance share awards and stock only stock appreciation rights.

Restricted Stock Units (“RSU”) and Performance Share Awards (“PSAs”) Awards of RSUs and PSAs are made under our LTIP. The RSUs vest on the passage of time, generally on a graded scale over a three, four, and five-year period, or in certain instances the RSUs were issued with five year cliff vesting. PSAs are issued annually to members of management and each respective grant cliff vests each December 31 of the third year following the grant, assuming the achievement of predetermined, cumulative financial performance targets covering two or three year periods. The performance measures include a minimum, target and maximum performance level providing the grantees an opportunity to receive more or less shares than targeted depending on actual financial performance. For both RSUs and PSAs, the grant date fair value of the awards, which is equal to the closing price per common share on the date of the award, is used to determine the amount of expense to be recognized over the applicable service period. Settlement of RSUs and PSAs will be made in shares of our common stock currently held in treasury.

- 10 -

GLATFELTER

9.30.16 Form 10-Q

The following table summarizes RSU and PSA activity during periods indicated:

|

Units |

2016 |

|

|

2015 |

|

||

|

Balance at January 1, |

|

674,523 |

|

|

|

888,942 |

|

|

Granted |

|

298,832 |

|

|

|

160,514 |

|

|

Forfeited |

|

(146,327 |

) |

|

|

(87,567 |

) |

|

Shares delivered |

|

(149,975 |

) |

|

|

(286,857 |

) |

|

Balance at September 30, |

|

677,053 |

|

|

|

675,032 |

|

The amount granted in 2016 and 2015 includes PSAs of 199,693 and 105,017, respectively, exclusive of reinvested dividends.

The following table sets forth aggregate RSU and PSA compensation expense for the periods indicated:

|

|

September 30 |

|

|||||

|

In thousands |

2016 |

|

|

2015 |

|

||

|

Three months ended |

$ |

765 |

|

|

$ |

395 |

|

|

Nine months ended |

|

2,167 |

|

|

|

1,214 |

|

Stock Only Stock Appreciation Rights (“SOSARs”) Under terms of the SOSAR, a recipient receives the right to a payment in the form of shares of common stock equal to the difference, if any, in the fair market value of one share of common stock at the time of exercising the SOSAR and the exercise price. The SOSARs vest ratably over a three year period and have a term of ten years.

The following table sets forth information related to outstanding SOSARS.

|

|

2016 |

|

|

2015 |

|

||||||||||

|

SOSARS |

Shares |

|

|

Wtd Avg Exercise Price |

|

|

Shares |

|

|

Wtd Avg Exercise Price |

|

||||

|

Outstanding at January 1, |

|

2,199,742 |

|

|

$ |

17.82 |

|

|

|

1,864,707 |

|

|

$ |

16.20 |

|

|

Granted |

|

743,925 |

|

|

|

17.54 |

|

|

|

423,590 |

|

|

24.62 |

|

|

|

Exercised |

|

(61,190 |

) |

|

|

10.70 |

|

|

|

(70,347 |

) |

|

|

14.12 |

|

|

Canceled / forfeited |

|

(143,932 |

) |

|

|

17.87 |

|

|

|

(17,559 |

) |

|

|

25.24 |

|

|

Outstanding at September 30, |

|

2,738,545 |

|

|

$ |

17.64 |

|

|

|

2,200,391 |

|

|

$ |

17.82 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SOSAR Grants |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted average grant date |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

fair value per share |

$ |

4.07 |

|

|

|

|

|

|

$ |

7.46 |

|

|

|

|

|

|

Aggregate grant date |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

fair value (in thousands) |

$ |

3,013 |

|

|

|

|

|

|

$ |

3,134 |

|

|

|

|

|

|

Black-Scholes assumptions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dividend yield |

|

2.85 |

% |

|

|

|

|

|

|

1.94 |

% |

|

|

|

|

|

Risk free rate of return |

|

1.34 |

% |

|

|

|

|

|

|

1.64 |

% |

|

|

|

|

|

Volatility |

|

31.97 |

% |

|

|

|

|

|

|

36.38 |

% |

|

|

|

|

|

Expected life |

6 yrs |

|

|

|

|

|

|

6 yrs |

|

|

|

|

|

||

The following table sets forth SOSAR compensation expense for the periods indicated:

|

|

September 30 |

|

|||||

|

In thousands |

2016 |

|

|

2015 |

|

||

|

Three months ended |

$ |

650 |

|

|

$ |

671 |

|

|

Nine months ended |

|

2,051 |

|

|

|

1,940 |

|

|

7. |

The following tables provide information with respect to the net periodic costs of our pension and post retirement medical benefit plans.

|

|

Three months ended September 30 |

|

|||||

|

In thousands |

2016 |

|

|

2015 |

|

||

|

Pension Benefits |

|

|

|

|

|

|

|

|

Service cost |

$ |

2,614 |

|

|

$ |

2,850 |

|

|

Interest cost |

|

6,120 |

|

|

|

5,868 |

|

|

Expected return on plan assets |

|

(11,331 |

) |

|

|

(11,498 |

) |

|

Amortization of prior service cost |

|

674 |

|

|

|

760 |

|

|

Amortization of unrecognized loss |

|

3,293 |

|

|

|

4,226 |

|

|

Net periodic benefit cost |

$ |

1,370 |

|

|

$ |

2,206 |

|

|

Other Benefits |

|

|

|

|

|

|

|

|

Service cost |

$ |

287 |

|

|

$ |

358 |

|

|

Interest cost |

|

498 |

|

|

|

499 |

|

|

Amortization of prior service cost |

|

(45 |

) |

|

|

(70 |

) |

|

Amortization of unrecognized (gain)/loss |

|

(189 |

) |

|

|

58 |

|

|

Net periodic benefit cost |

$ |

551 |

|

|

$ |

845 |

|

|

|

Nine months ended September 30 |

|

|||||

|

In thousands |

2016 |

|

|

2015 |

|

||

|

Pension Benefits |

|

|

|

|

|

|

|

|

Service cost |

$ |

7,855 |

|

|

$ |

8,546 |

|

|

Interest cost |

|

18,360 |

|

|

|

17,606 |

|

|

Expected return on plan assets |

|

(33,992 |

) |

|

|

(34,495 |

) |

|

Amortization of prior service cost |

|

2,023 |

|

|

|

2,281 |

|

|

Amortization of unrecognized loss |

|

9,880 |

|

|

|

12,679 |

|

|

Net periodic benefit cost |

$ |

4,126 |

|

|

$ |

6,617 |

|

|

Other Benefits |

|

|

|

|

|

|

|

|

Service cost |

$ |

860 |

|

|

$ |

1,074 |

|

|

Interest cost |

|

1,494 |

|

|

|

1,498 |

|

|

Amortization of prior service cost |

|

(136 |

) |

|

|

(210 |

) |

|

Amortization of unrecognized (gain)/loss |

|

(567 |

) |

|

|

173 |

|

|

Net periodic benefit cost |

$ |

1,651 |

|

|

$ |

2,535 |

|

- 11 -

GLATFELTER

9.30.16 Form 10-Q

|

8. |

Inventories, net of reserves, were as follows:

|

|

September 30 |

|

|

December 31 |

|

||

|

In thousands |

2016 |

|

|

2015 |

|

||

|

Raw materials |

$ |

64,579 |

|

|

$ |

60,098 |

|

|

In-process and finished |

|

124,459 |

|

|

|

115,874 |

|

|

Supplies |

|

73,853 |

|

|

|

71,242 |

|

|

Total |

$ |

262,891 |

|

|

$ |

247,214 |

|

|

9. |

Long-term debt is summarized as follows:

|

|

September 30 |

|

|

December 31 |

|

||

|

In thousands |

2016 |

|

|

2015 |

|

||

|

Revolving credit facility, due Mar. 2020 |

$ |

59,830 |

|

|

$ |

58,792 |

|

|

5.375% Notes, due Oct. 2020 |

|

250,000 |

|

|

|

250,000 |

|

|

2.40% Term Loan, due Jun. 2022 |

|

9,566 |

|

|

|

10,109 |

|

|

2.05% Term Loan, due Mar. 2023 |

|

40,210 |

|

|

|

42,130 |

|

|

1.30% Term Loan, due Jun. 2023 |

|

11,161 |

|

|

|

- |

|

|

1.55% Term Loan, due Sep. 2025 |

|

10,941 |

|

|

|

2,839 |

|

|

Total long-term debt |

|

381,708 |

|

|

|

363,870 |

|

|

Less current portion |

|

(11,432 |

) |

|

|

(7,366 |

) |

|

Unamortized deferred issuance costs |

|

(2,727 |

) |

|

|

(3,208 |

) |

|

Long-term debt, net of current portion |

$ |

367,549 |

|

|

$ |

353,296 |

|

The amount set forth for Long-term debt, net of current portion as of December 31, 2015, has been restated to retroactively adopt ASU No. 2015-03, Interest - Imputation of Interest (Subtopic 835-30) Simplifying the Presentation of Debt Issuance Costs. This ASU requires debt issuance costs to be presented as a direct deduction from the carrying value of the related debt instrument rather than as a deferred asset except for costs associated with a revolving line of credit. We adopted this standard in the first quarter of 2016 retroactive to December 31, 2015.

On March 12, 2015, we amended our revolving credit agreement with a consortium of banks (the “Revolving Credit Facility”) which increased the amount available for borrowing to $400 million, extended the maturity of the facility to March 12, 2020, and instituted a revised interest rate pricing grid.

For all US dollar denominated borrowings under the Revolving Credit Facility, the borrowing rate is, at our option, either, (a) the bank’s base rate which is equal to the greater of i) the prime rate; ii) the federal funds rate plus 50 basis points; or iii) the daily Euro-rate plus 100 basis points plus an applicable spread over either i), ii) or iii) ranging from 12.5 basis points to 100 basis points based on the Company’s leverage ratio and its corporate credit ratings determined by Standard & Poor’s Rating Services and Moody’s Investor Service, Inc. (the “Corporate Credit Rating”); or (b) the daily

Euro-rate plus an applicable margin ranging from 112.5 basis points to 200 basis points based on the Company’s leverage ratio and the Corporate Credit Rating. For non-US dollar denominated borrowings, interest is based on (b) above.

The Revolving Credit Facility contains a number of customary covenants for financings of this type that, among other things, restrict our ability to dispose of or create liens on assets, incur additional indebtedness, repay other indebtedness, limits certain intercompany financing arrangements, make acquisitions and engage in mergers or consolidations. We are also required to comply with specified financial tests and ratios including: i) maximum net debt to earnings before interest, taxes, depreciation and amortization (“EBITDA”) ratio (the “leverage ratio”); and ii) a consolidated EBITDA to interest expense ratio. The most restrictive of our covenants is a maximum leverage ratio of 3.5x. As of September 30, 2016, the leverage ratio, as calculated in accordance with the definition in our credit agreement, was 2.1x. A breach of these requirements would give rise to certain remedies under the Revolving Credit Facility, among which are the termination of the agreement and accelerated repayment of the outstanding borrowings plus accrued and unpaid interest under the credit facility.

On October 3, 2012, we completed a private placement offering of $250.0 million aggregate principal amount of 5.375% Senior Notes due 2020 (the “5.375% Notes”). The 5.375% Notes, which are now publically registered, are fully and unconditionally guaranteed, jointly and severally, by PHG Tea Leaves, Inc., Mollanvick, Inc., Glatfelter Composite Fibers N. A., Inc., Glatfelter Advanced Materials N.A., LLC., and Glatfelter Holdings, LLC (the “Guarantors”). Interest on the 5.375% Notes is payable semiannually in arrears on April 15 and October 15.

The 5.375% Notes are redeemable, in whole or in part, at any time on or after October 15, 2016 at the redemption prices specified in the applicable Indenture. These Notes and the guarantees of the notes are senior obligations of the Company and the Guarantors, respectively, rank equally in right of payment with future senior indebtedness of the Company and the Guarantors and will mature on October 15, 2020.

The 5.375% Notes contain various covenants customary to indebtedness of this nature including limitations on i) the amount of indebtedness that may be incurred; ii) certain restricted payments including common stock dividends; iii) distributions from certain subsidiaries; iv) sales of assets; v) transactions amongst subsidiaries; and vi) incurrence of liens on assets. In addition, the 5.375% Notes contain cross default provisions that could result in all such notes becoming due and payable in the event of a failure to repay debt outstanding under the Revolving Credit Agreement at maturity or a default under the Revolving Credit Agreement that accelerates the debt outstanding thereunder. As of September 30, 2016, we met all of the requirements of our debt covenants.

- 12 -

GLATFELTER

9.30.16 Form 10-Q

Glatfelter Gernsbach GmbH & Co. KG (“Gernsbach”), a wholly-owned subsidiary of ours, entered into a series of borrowing agreements with IKB Deutsche Industriebank AG, Düsseldorf (“IKB”) as summarized below:

|

Amounts in thousands |

Original Principal |

|

|

Interest Rate |

|

|

Maturity |

||

|

Borrowing date |

|

|

|

|

|

|

|

|

|

|

Apr. 11, 2013 |

€ |

42,700 |

|

|

|

2.05 |

% |

|

Mar. 2023 |

|

Sep. 4, 2014 |

|

10,000 |

|

|

|

2.40 |

% |

|

Jun. 2022 |

|

Oct. 10, 2015 |

|

2,608 |

|

|

|

1.55 |

% |

|

Sep. 2025 |

|

May 4, 2016 |

|

7,195 |

|

|

|

1.55 |

% |

|

Sep. 2025 |

|

Apr. 26, 2016 |

|

10,000 |

|

|

|

1.30 |

% |

|

Jun. 2023 |

Each of the borrowings require quarterly repayments of principal and interest and provide for representations, warranties and covenants customary for financings of these types. The financial covenants contained in each of the IKB loans, which relate to the minimum ratio of consolidated EBITDA to consolidated interest expense and the maximum ratio of consolidated total net debt to consolidated adjusted EBITDA, are calculated by reference to our Revolving Credit Agreement.

P. H. Glatfelter Company guarantees all debt obligations of its subsidiaries. All such obligations are recorded in these condensed consolidated financial statements.

Letters of credit issued to us by certain financial institutions totaled $5.1 million and $5.3 million as of September 30, 2016 and December 31, 2015, respectively. The letters of credit, which reduce amounts available under our revolving credit facility, primarily provide financial assurances for the benefit of certain state workers compensation insurance agencies in conjunction with our self-insurance program. We bear the credit risk on this amount to the extent that we do not comply with the provisions of certain agreements. No amounts are outstanding under the letters of credit.

|

10. |

The amounts reported on the condensed consolidated balance sheets for cash and cash equivalents, accounts receivable and accounts payable approximate fair value. The following table sets forth carrying value and fair value of long-term debt:

|

|

September 30, 2016 |

|

|

December 31, 2015 |

|

||||||||||

|

In thousands |

Carrying Value |

|

|

Fair Value |

|

|

Carrying Value |

|

|

Fair Value |

|

||||

|

Variable rate debt |

$ |

59,830 |

|

|

$ |

59,830 |

|

|

$ |

58,792 |

|

|

$ |

58,792 |

|

|

Fixed-rate bonds |

|

250,000 |

|

|

|

252,658 |

|

|

|

250,000 |

|

|

|

250,938 |

|

|

2.40% Term loan |

|

9,566 |

|

|

|

9,324 |

|

|

|

10,109 |

|

|

|

10,535 |

|

|

2.05% Term loan |

|

40,210 |

|

|

|

38,735 |

|

|

|

42,130 |

|

|

|

42,886 |

|

|

1.30% Term Loan |

|

11,161 |

|

|

|

10,470 |

|

|

|

- |

|

|

|

- |

|

|

1.55% Term loan |

|

10,941 |

|

|

|

10,180 |

|

|

|

2,839 |

|

|

|

2,524 |

|

|

Total |

$ |

381,708 |

|

|

$ |

381,197 |

|

|

$ |

363,870 |

|

|

$ |

365,675 |

|

As of September 30, 2016, and December 31, 2015, we had $250.0 million of 5.375% fixed rate bonds. These bonds are publicly registered, but thinly traded. Accordingly, the values set forth above for the bonds, as well as our other debt instruments, are based on observable inputs and other relevant market data (Level 2). The fair value of financial derivatives is set forth below in Note 11.

|

11. |

As part of our overall risk management practices, we enter into financial derivatives primarily designed to either i) hedge foreign currency risks associated with forecasted transactions – “cash flow hedges” or ii) mitigate the impact that changes in currency exchange rates have on intercompany financing transactions and foreign currency denominated receivables and payables – “foreign currency hedges."

Derivatives Designated as Hedging Instruments - Cash Flow Hedges We use currency forward contracts as cash flow hedges to manage our exposure to fluctuations in the currency exchange rates on certain forecasted production costs or capital expenditures expected to be incurred. Currency forward contracts involve fixing the exchange for delivery of a specified amount of foreign currency on a specified date. As of September 30, 2016, the maturity of currency forward contracts ranged from one month to 22 months.

We designate certain currency forward contracts as cash flow hedges of forecasted raw material purchases, certain production costs or capital expenditures with exposure to changes in foreign currency exchange rates. The effective portion of changes in the fair value of derivatives designated and that qualify as cash flow hedges of foreign exchange risk is deferred as a component of accumulated other comprehensive income in the accompanying condensed consolidated balance sheets. With respect to hedges of forecasted raw material purchases or production costs, the

- 13 -

GLATFELTER

9.30.16 Form 10-Q

amount deferred is subsequently reclassified into costs of products sold in the period that inventory produced using the hedged transaction affects earnings. For hedged capital expenditures, deferred gains or losses are reclassified and included in the historical cost of the capital asset and subsequently affect earnings as depreciation is recognized. The ineffective portion of the change in fair value of the derivative is recognized directly to earnings and reflected in the accompanying condensed consolidated statements of income as non-operating income (expense) under the caption “Other, net.”

We had the following outstanding derivatives that were used to hedge foreign exchange risks associated with forecasted transactions and designated as hedging instruments:

|

In thousands |

September 30 2016 |

|

|

December 31 2015 |

|

||

|

Derivative |

|

|

|

|

|

|

|

|

Sell/Buy - sell notional |

|

|

|

|

|

|

|

|

Euro / British Pound |

|

7,703 |

|

|

|

10,527 |

|

|

Sell/Buy - buy notional |

|

|

|

|

|

|

|

|

Euro / Philippine Peso |

|

733,358 |

|

|

|

758,634 |

|

|

British Pound / Philippine Peso |

|

408,967 |

|

|

|

542,063 |

|

|

Euro / U.S. Dollar |

|

42,672 |

|

|

|

51,433 |

|

|

U.S. Dollar / Canadian Dollar |

|

34,143 |

|

|

|

34,649 |

|

|

U.S. Dollar / Euro |

|

26,774 |

|

|

|

— |

|

Derivatives Not Designated as Hedging Instruments - Foreign Currency Hedges We also enter into forward foreign exchange contracts to mitigate the impact changes in currency exchange rates have on balance sheet monetary assets and liabilities. None of these contracts are designated as hedges for financial accounting purposes and, accordingly, changes in value of the foreign exchange forward contracts and in the offsetting underlying on-balance-sheet transactions are reflected in the accompanying condensed consolidated statements of income under the caption “Other, net.”

The following sets forth derivatives used to mitigate the impact changes in currency exchange rates have on balance sheet monetary assets and liabilities:

|

In thousands |

September 30 2016 |

|

|

December 31 2015 |

|

||

|

Derivative |

|

|

|

|

|

|

|

|

Sell/Buy - sell notional |

|

|

|

|

|

|

|

|

U.S. Dollar / British Pound |

|

10,500 |

|

|

|

10,000 |

|

|

British Pound / Euro |

|

2,500 |

|

|

|

3,500 |

|

|

Sell/Buy - buy notional |

|

|

|

|

|

|

|

|

Euro / U.S. Dollar |

|

- |

|

|

|

12,500 |

|

|

British Pound / Euro |

|

18,500 |

|

|

|

13,500 |

|

These contracts have maturities of one month from the date originally entered into.

Fair Value Measurements The following table summarizes the fair values of derivative instruments for the period indicated and the line items in the accompanying condensed consolidated balance sheets where the instruments are recorded:

|

In thousands |

September 30 2016 |

|

|

December 31 2015 |

|

|

September 30 2016 |

|

|

December 31 2015 |

|

||||

|

|

Prepaid Expenses and Other |

|

|

Other |

|

||||||||||

|

Balance sheet caption |

Current Assets |

|

|

Current Liabilities |

|

||||||||||

|

Designated as hedging: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Forward foreign currency |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

exchange contracts |

$ |

330 |

|

|

$ |

955 |

|

|

$ |

958 |

|

|

$ |

1,545 |

|

|

Not designated as hedging: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Forward foreign currency |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

exchange contracts |

$ |

172 |

|

|

$ |

68 |

|

|

$ |

136 |

|

|

$ |

49 |

|

The amounts set forth in the table above represent the net asset or liability giving effect to rights of offset with each counterparty. The effect of netting the amounts presented above did not have a material effect on our consolidated financial position.

The following table summarizes the amount of income or (loss) from derivative instruments recognized in our results of operations for the periods indicated and the line items in the accompanying condensed consolidated statements of income where the results are recorded:

|

|

|

|

Three months ended September 30 |

|

|

Nine months ended September 30 |

|

||||||||||

|

In thousands |

|

|

2016 |

|

|

2015 |

|

|

2016 |

|

|

2015 |

|

||||

|

Designated as hedging: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Forward foreign currency exchange contracts: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Effective portion – cost of products sold |

|

|

$ |

(347 |

) |

|

$ |

1,972 |

|

|

$ |

(264 |

) |

|

$ |

4,595 |

|

|

Ineffective portion – other – net |

|

|

|

(69 |

) |

|

|

(184 |

) |

|

|

(399 |

) |

|

|

104 |

|

|

Not designated as hedging: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Forward foreign currency |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

exchange contracts: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other – net |

|

|

$ |

332 |

|

|

$ |

621 |

|

|

$ |

1,396 |

|

|

$ |

1,028 |

|

The impact of activity not designated as hedging was substantially all offset by the remeasurement of the underlying on-balance-sheet item.

The fair value hierarchy consists of three broad levels, which gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1) and the lowest priority to unobservable inputs (Level 3).

- 14 -

GLATFELTER

9.30.16 Form 10-Q