GRAN TIERRA ENERGY INC. - Quarter Report: 2023 March (Form 10-Q)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

| ☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||||

For the quarterly period ended March 31, 2023

or

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||||

For the transition period from __________ to __________

Commission file number 001-34018

GRAN TIERRA ENERGY INC.

(Exact name of registrant as specified in its charter)

| Delaware | 98-0479924 | ||||||||||||||||

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||||||||||||||

| 500 Centre Street S.E. | |||||||||||||||||

| Calgary, | Alberta | Canada | T2G 1A6 | ||||||||||||||

| (Address of principal executive offices, including zip code) | |||||||||||||||||

(403) 265-3221

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

| Common Stock, par value $0.001 per share | GTE | NYSE American | ||||||

Toronto Stock Exchange | ||||||||

London Stock Exchange | ||||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of large accelerated filer, accelerated filer, smaller reporting company, and emerging growth company in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☒ | ||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ☐ | ||||||||

| Emerging growth company | ☐ | ||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

On April 26, 2023, 368,904,496 shares of the registrant’s Common Stock, $0.001 par value, were issued.

Gran Tierra Energy Inc.

Quarterly Report on Form 10-Q

Quarterly Period Ended March 31, 2023

Table of contents

| Page | ||||||||

| PART I | Financial Information | |||||||

| Item 1. | Financial Statements | |||||||

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | |||||||

| Item 3. | Quantitative and Qualitative Disclosures About Market Risk | |||||||

| Item 4. | Controls and Procedures | |||||||

| PART II | Other Information | |||||||

| Item 1. | Legal Proceedings | |||||||

| Item 1A. | Risk Factors | |||||||

| Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds | |||||||

| Item 6. | Exhibits | |||||||

| SIGNATURES | ||||||||

1

CAUTIONARY LANGUAGE REGARDING FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). All statements other than statements of historical facts included in this Quarterly Report on Form 10-Q regarding our financial position, estimated quantities and net present values of reserves, business strategy, plans and objectives of our management for future operations, covenant compliance, capital spending plans and benefits of the changes in our capital program or expenditures, our liquidity, the impacts of the coronavirus (COVID-19) pandemic and those statements preceded by, followed by or that otherwise include the words “believe,” “expect,” “anticipate,” “intend,” “estimate,” “project,” “target,” “goal,” “plan,” “budget,” “objective,” “could,” “should,” or similar expressions or variations on these expressions are forward-looking statements. We can give no assurances that the assumptions upon which the forward-looking statements are based will prove to be correct or that, even if correct, intervening circumstances will not occur to cause actual results to be different than expected. Because forward-looking statements are subject to risks and uncertainties, actual results may differ materially from those expressed or implied by the forward-looking statements. There are a number of risks, uncertainties and other important factors that could cause our actual results to differ materially from the forward-looking statements, including, but not limited to, our operations are located in South America and unexpected problems can arise due to guerilla activity, strikes, local blockades or protests; technical difficulties and operational difficulties may arise which impact the production, transport or sale of our products; other disruptions to local operations; global health events (including the ongoing COVID-19 pandemic); global and regional changes in the demand, supply, prices, differentials or other market conditions affecting oil and gas, including inflation and changes resulting from a global health crisis, the Russian invasion of Ukraine, or from the imposition or lifting of crude oil production quotas or other actions that might be imposed by OPEC, such as its recent decision to cut production and other producing countries and the resulting company or third-party actions in response to such changes; changes in commodity prices, including volatility or a decline in these prices relative to historical or future expected levels; the risk that current global economic and credit conditions may impact oil prices and oil consumption more than we currently predicts, which could cause further modification of our strategy and capital spending program; prices and markets for oil and natural gas are unpredictable and volatile; the effect of hedges; the accuracy of productive capacity of any particular field; geographic, political and weather conditions can impact the production, transport or sale of our products; our ability to execute its business plan and realize expected benefits from current initiatives; the risk that unexpected delays and difficulties in developing currently owned properties may occur; the ability to replace reserves and production and develop and manage reserves on an economically viable basis; the accuracy of testing and production results and seismic data, pricing and cost estimates (including with respect to commodity pricing and exchange rates); the risk profile of planned exploration activities; the effects of drilling down-dip; the effects of waterflood and multi-stage fracture stimulation operations; the extent and effect of delivery disruptions, equipment performance and costs; actions by third parties; the timely receipt of regulatory or other required approvals for our operating activities; the failure of exploratory drilling to result in commercial wells; unexpected delays due to the limited availability of drilling equipment and personnel; volatility or declines in the trading price of our common stock or bonds; the risk that we do not receive the anticipated benefits of government programs, including government tax refunds; our ability to obtain a new credit agreement and comply with financial covenants in its credit agreement and indentures and make borrowings under any credit agreement; and those factors set out in Part II, Item 1A “Risk Factors” in this Quarterly Report on Form 10-Q and Part I, Item 1A “Risk Factors” in our 2022 Annual Report on Form 10-K (the “2022 Annual Report on Form 10-K”), and in our other filings with the Securities and Exchange Commission (“SEC”). The unprecedented nature of the current volatility in the worldwide economy and oil and gas industry makes it more difficult to predict the accuracy of forward-looking statements. The information included herein is given as of the filing date of this Quarterly Report on Form 10-Q with the SEC and, except as otherwise required by the federal securities laws, we disclaim any obligation or undertaking to publicly release any updates or revisions to or to withdraw, any forward-looking statement contained in this Quarterly Report on Form 10-Q to reflect any change in our expectations with regard thereto or any change in events, conditions or circumstances on which any forward-looking statement is based.

GLOSSARY OF OIL AND GAS TERMS

In this document, the abbreviations set forth below have the following meanings:

| bbl | barrel | ||||

| BOPD | barrels of oil per day | ||||

| NAR | net after royalty | ||||

Sales volumes represent production NAR adjusted for inventory changes. Our oil and gas reserves are reported as NAR. Our production is also reported NAR, except as otherwise specifically noted as "working interest production before royalties."

2

PART I - Financial Information

Item 1. Financial Statements

Gran Tierra Energy Inc.

Condensed Consolidated Statements of Operations (Unaudited)

(Thousands of U.S. Dollars, Except Share and Per Share Amounts)

| Three Months Ended March 31, | |||||||||||

| 2023 | 2022 | ||||||||||

OIL SALES (Note 6) | $ | 144,190 | $ | 174,569 | |||||||

| EXPENSES | |||||||||||

| Operating | 41,369 | 34,935 | |||||||||

| Transportation | 3,066 | 2,834 | |||||||||

Depletion, depreciation and accretion (Note 3) | 51,721 | 40,963 | |||||||||

| Inventory impairment | 475 | — | |||||||||

General and administrative (Note 9) | 12,696 | 12,336 | |||||||||

| Foreign exchange loss (gain) | 1,702 | (3,725) | |||||||||

Derivative instruments loss (Note 9) | — | 21,439 | |||||||||

Gain on re-purchase of Senior Notes (Note 4) | (1,090) | — | |||||||||

Interest expense (Note 4) | 11,836 | 12,128 | |||||||||

| 121,775 | 120,910 | ||||||||||

| INTEREST INCOME | 768 | — | |||||||||

| INCOME BEFORE INCOME TAXES | 23,183 | 53,659 | |||||||||

| INCOME TAX EXPENSE | |||||||||||

Current (Note 7) | 17,606 | 20,827 | |||||||||

Deferred (Note 7) | 15,277 | 18,713 | |||||||||

| 32,883 | 39,540 | ||||||||||

| NET AND COMPREHENSIVE (LOSS) INCOME | $ | (9,700) | $ | 14,119 | |||||||

| NET (LOSS) INCOME PER SHARE | |||||||||||

| BASIC AND DILUTED | $ | (0.03) | $ | 0.04 | |||||||

WEIGHTED AVERAGE SHARES OUTSTANDING - BASIC (Note 5) | 344,513,998 | 367,386,664 | |||||||||

WEIGHTED AVERAGE SHARES OUTSTANDING - DILUTED (Note 5) | 344,513,998 | 372,375,245 | |||||||||

(See notes to the condensed consolidated financial statements)

3

Gran Tierra Energy Inc.

Condensed Consolidated Balance Sheets (Unaudited)

(Thousands of U.S. Dollars, Except Share and Per Share Amounts)

| As at March 31, 2023 | As at December 31, 2022 | ||||||||||

| ASSETS | |||||||||||

| Current Assets | |||||||||||

Cash and cash equivalents (Note 10) | $ | 105,684 | $ | 126,873 | |||||||

Restricted cash and cash equivalents (Note 10) | 1,142 | 1,142 | |||||||||

| Accounts receivable | 13,596 | 10,706 | |||||||||

| Inventory | 20,075 | 20,192 | |||||||||

| Taxes receivable | 113 | 54 | |||||||||

Other current assets (Note 9) | 11,681 | 9,620 | |||||||||

| Total Current Assets | 152,291 | 168,587 | |||||||||

| Oil and Gas Properties | |||||||||||

| Proved | 1,036,350 | 1,000,424 | |||||||||

| Unproved | 63,454 | 74,471 | |||||||||

| Total Oil and Gas Properties | 1,099,804 | 1,074,895 | |||||||||

| Other capital assets | 25,319 | 26,007 | |||||||||

Total Property, Plant and Equipment (Note 3) | 1,125,123 | 1,100,902 | |||||||||

| Other Long-Term Assets | |||||||||||

| Deferred tax assets | 11,806 | 22,990 | |||||||||

| Taxes receivable | 31,273 | 27,796 | |||||||||

Other long-term assets (Note 9) | 5,923 | 15,335 | |||||||||

| Total Other Long-Term Assets | 49,002 | 66,121 | |||||||||

| Total Assets | $ | 1,326,416 | $ | 1,335,610 | |||||||

| LIABILITIES AND SHAREHOLDERS’ EQUITY | |||||||||||

| Current Liabilities | |||||||||||

| Accounts payable and accrued liabilities | $ | 187,598 | $ | 167,579 | |||||||

| Taxes payable | 65,202 | 58,978 | |||||||||

Equity compensation award liability (Note 5 and 9) | 8,011 | 15,082 | |||||||||

| Total Current Liabilities | 260,811 | 241,639 | |||||||||

| Long-Term Liabilities | |||||||||||

Long-term debt (Notes 4 and 9) | 581,391 | 589,593 | |||||||||

| Deferred tax liabilities | 5,377 | 28 | |||||||||

| Asset retirement obligation | 65,159 | 63,358 | |||||||||

Equity compensation award liability (Note 5 and 9) | 8,592 | 16,437 | |||||||||

| Other long-term liabilities | 7,319 | 6,989 | |||||||||

| Total Long-Term Liabilities | 667,838 | 676,405 | |||||||||

Contingencies (Note 8) | |||||||||||

| Shareholders' Equity | |||||||||||

Common Stock (Note 5) (368,898,619 issued, 333,069,042 and 346,151,157 outstanding shares of Common Stock, par value $0.001 per share, as at March 31, 2023, and December 31, 2022, respectively) | 10,272 | 10,272 | |||||||||

| Additional paid-in capital | 1,291,973 | 1,291,354 | |||||||||

Treasury Stock (Note 5) | (38,035) | (27,317) | |||||||||

| Deficit | (866,443) | (856,743) | |||||||||

| Total Shareholders’ Equity | 397,767 | 417,566 | |||||||||

| Total Liabilities and Shareholders’ Equity | $ | 1,326,416 | $ | 1,335,610 | |||||||

(See notes to the condensed consolidated financial statements)

4

Gran Tierra Energy Inc.

Condensed Consolidated Statements of Cash Flows (Unaudited)

(Thousands of U.S. Dollars)

| Three Months Ended March 31, | |||||||||||

| 2023 | 2022 | ||||||||||

| Operating Activities | |||||||||||

| Net (loss) income | $ | (9,700) | $ | 14,119 | |||||||

| Adjustments to reconcile net (loss) income to net cash provided by operating activities: | |||||||||||

| Depletion, depreciation and accretion | 51,721 | 40,963 | |||||||||

| Inventory impairment | 475 | — | |||||||||

| Deferred tax expense | 15,277 | 18,713 | |||||||||

Stock-based compensation expense (Note 5) | 1,500 | 4,557 | |||||||||

Amortization of debt issuance costs (Note 4) | 781 | 887 | |||||||||

| Unrealized foreign exchange loss (gain) | 514 | (4,839) | |||||||||

| Gain on re-purchase of Senior Notes (Note 4) | (1,090) | — | |||||||||

| Derivative instruments loss | — | 21,439 | |||||||||

| Cash settlements on derivatives instruments | — | (8,596) | |||||||||

| Cash settlement of asset retirement obligation | — | (5) | |||||||||

| Non-cash lease expenses | 1,144 | 411 | |||||||||

| Lease payments | (606) | (344) | |||||||||

Net change in assets and liabilities from operating activities (Note 10) | (10,763) | 16,520 | |||||||||

| Net cash provided by operating activities | 49,253 | 103,825 | |||||||||

| Investing Activities | |||||||||||

| Additions to property, plant and equipment | (71,062) | (41,483) | |||||||||

Changes in non-cash investing working capital (Note 10) | 14,871 | (1,803) | |||||||||

| Net cash used in investing activities | (56,191) | (43,286) | |||||||||

| Financing Activities | |||||||||||

Debt issuance costs (Note 4) | (50) | — | |||||||||

Repayment of debt (Note 4) | — | (27,525) | |||||||||

Re-purchase of Senior Notes (Note 4) | (4,225) | — | |||||||||

Re-purchase of shares of Common Stock (Note 5) | (10,718) | — | |||||||||

| Proceeds from issuance of Common Stock, net of issuance costs | — | 2 | |||||||||

| Proceeds from exercise of stock options | — | 980 | |||||||||

| Lease payments | (1,105) | (777) | |||||||||

| Net cash used in financing activities | (16,098) | (27,320) | |||||||||

| Foreign exchange loss on cash, cash equivalents and restricted cash and cash equivalents | 2,214 | 478 | |||||||||

| Net (decrease) increase in cash, cash equivalents and restricted cash and cash equivalents | (20,822) | 33,697 | |||||||||

Cash, cash equivalents and restricted cash and cash equivalents, beginning of period (Note 10) | 133,358 | 31,404 | |||||||||

Cash, cash equivalents and restricted cash and cash equivalents, end of period (Note 10) | $ | 112,536 | $ | 65,101 | |||||||

Supplemental cash flow disclosures (Note 10) | |||||||||||

(See notes to the condensed consolidated financial statements)

5

Gran Tierra Energy Inc.

Condensed Consolidated Statements of Shareholders’ Equity (Unaudited)

(Thousands of U.S. Dollars)

| Three Months Ended March 31, | |||||||||||

| 2023 | 2022 | ||||||||||

| Share Capital | |||||||||||

| Balance, beginning of period | $ | 10,272 | $ | 10,270 | |||||||

Issuance of common stock (Note 5) | — | 2 | |||||||||

| Balance, end of period | $ | 10,272 | $ | 10,272 | |||||||

| Additional Paid-in Capital | |||||||||||

| Balance, beginning of period | $ | 1,291,354 | $ | 1,287,582 | |||||||

| Exercise of stock options | — | 980 | |||||||||

Stock-based compensation (Note 5) | 619 | 600 | |||||||||

| Balance, end of period | $ | 1,291,973 | $ | 1,289,162 | |||||||

| Treasury Stock | |||||||||||

| Balance, beginning of period | $ | (27,317) | $ | — | |||||||

Purchase of treasury shares (Note 5) | (10,718) | — | |||||||||

| Balance, end of period | $ | (38,035) | $ | — | |||||||

| Deficit | |||||||||||

| Balance, beginning of period | $ | (856,743) | $ | (995,772) | |||||||

| Net (loss) income | (9,700) | 14,119 | |||||||||

| Balance, end of period | $ | (866,443) | $ | (981,653) | |||||||

| Total Shareholders’ Equity | $ | 397,767 | $ | 317,781 | |||||||

(See notes to the condensed consolidated financial statements)

6

Gran Tierra Energy Inc.

Notes to the Condensed Consolidated Financial Statements (Unaudited)

(Expressed in U.S. Dollars, unless otherwise indicated)

1. Description of Business

Gran Tierra Energy Inc. a Delaware corporation (the “Company” or “Gran Tierra”), is a publicly traded company focused on international oil and natural gas exploration and production with assets currently in Colombia and Ecuador.

2. Significant Accounting Policies

These interim unaudited condensed consolidated financial statements have been prepared in accordance with generally accepted accounting principles in the United States of America (“GAAP”). The information furnished herein reflects all normal recurring adjustments that are, in the opinion of management, necessary for the fair presentation of results for the interim periods.

The note disclosure requirements of annual consolidated financial statements provide additional disclosures required for interim unaudited condensed consolidated financial statements. Accordingly, these interim unaudited condensed consolidated financial statements should be read in conjunction with the Company’s consolidated financial statements as at and for the year ended December 31, 2022, included in the Company’s 2022 Annual Report on Form 10-K.

The Company’s significant accounting policies are described in Note 2 of the consolidated financial statements, which are included in the Company’s 2022 Annual Report on Form 10-K and are the same policies followed in these interim unaudited condensed consolidated financial statements. The Company has evaluated all subsequent events to the date these interim unaudited condensed consolidated financial statements were issued.

3. Property, Plant and Equipment

| (Thousands of U.S. Dollars) | As at March 31, 2023 | As at December 31, 2022 | |||||||||

| Oil and natural gas properties | |||||||||||

| Proved | $ | 4,702,991 | $ | 4,617,804 | |||||||

| Unproved | 63,454 | 74,471 | |||||||||

| 4,766,445 | 4,692,275 | ||||||||||

Other(1) | 59,180 | 61,386 | |||||||||

| 4,825,625 | 4,753,661 | ||||||||||

| Accumulated depletion, depreciation and impairment | (3,700,502) | (3,652,759) | |||||||||

| $ | 1,125,123 | $ | 1,100,902 | ||||||||

(1) The “other” category includes right-of-use assets for operating and finance leases of $38.3 million, which had a net book value of $24.0 million as at March 31, 2023 (December 31, 2022 - $38.9 million, which had a net book value of $24.6 million).

For the three months ended March 31, 2023 and 2022, respectively, the Company had no ceiling test impairment losses. The Company used a 12-month unweighted average of the first-day-of the month Brent price prior to the ending date of the periods March 31, 2023, and 2022 of $95.99 and $77.41 per bbl, respectively, for the purpose of the ceiling test calculations.

7

4. Debt and Debt Issuance Costs

The Company’s debt at March 31, 2023, and December 31, 2022, was as follows:

| (Thousands of U.S. Dollars) | As at March 31, 2023 | As at December 31, 2022 | |||||||||

| Long-Term | |||||||||||

6.25% Senior Notes, due February 2025 | $ | 271,909 | $ | 279,909 | |||||||

7.75% Senior Notes, due May 2027 | 300,000 | 300,000 | |||||||||

| Unamortized debt issuance costs | (11,651) | (10,992) | |||||||||

| 560,258 | 568,917 | ||||||||||

Long-term lease obligation(1) | 21,133 | 20,676 | |||||||||

| Total debt | $ | 581,391 | $ | 589,593 | |||||||

(1) The current portion of the lease obligation has been included in accounts payable and accrued liabilities on the Company’s balance sheet and totaled $4.8 million as at March 31, 2023 (December 31, 2022 - $4.8 million).

As of March 31, 2023, the Company had a credit facility with a market lender in the global commodities industry. The credit facility has a borrowing base of up to $150 million, with $100 million as an initial commitment available at March 31, 2023, and an option for an additional $50 million upon mutual agreement by the Company and the lender. The credit facility bears interest based on the secured overnight financing rate posted by the Federal Reserve Bank of New York plus a credit margin of 6.00% and a credit-adjusted spread of 0.26%. Undrawn amounts under the credit facility bear interest at 2.10% per annum, based on the amount available. The credit facility is secured by the Company’s Colombian assets and economic rights. It has a final maturity date of August 15, 2024, which may be extended to February 18, 2025, upon the satisfaction of certain conditions. The availability period for the draws under the credit facility expires on August 20, 2023. As of March 31, 2023, and December 31, 2022, the credit facility remained undrawn.

Under the terms of the credit facility, the Company is required to maintain compliance with the following financial covenants:

i.Global Coverage Ratio of at least 150%, calculated using the net present value of the consolidated future cash flows of the Company up to the final maturity date discounted at 10% over the outstanding amount on the credit facility at each reporting period. The net present value of the consolidated future cash flows of the Company is required to be based on 80% of the prevailing ICE Brent forward strip.

ii.Prepayment Life Coverage Ratio of at least 150%, calculated using the estimated aggregate value of commodities to be delivered under the commercial contract from the commencement date to the final maturity date based on 80% of the prevailing ICE Brent forward strip and adjusted for quality and transportation discounts over the outstanding amount on the credit facility including interest and all other costs payable to the lender.

i.Liquidity ratio where the Company’s projected sources of cash exceed projected uses of cash by at least 1.15 times in each quarter period included in one year consolidated future cash flows. The future cash flows represent forecasted expected cash flows from operations, less anticipated capital expenditures, and certain other adjustments. The commodity pricing assumption used in this covenant is required to be 90% of the prevailing ICE Brent forward strip for the projected future cash flows.

Senior Notes

During the three months ended March 31, 2023, the Company re-purchased in the open market $8.0 million of 6.25% Senior Notes for cash consideration of $6.8 million, of which $2.6 million was included in accounts payable on the Company’s balance sheet as of March 31, 2023. The re-purchase resulted in a $1.1 million gain, which included the write-off of deferred financing fees of $0.1 million. The re-purchased 6.25% Senior Notes were not canceled and held by the Company as treasury bonds as of March 31, 2023.

Interest Expense

The following table presents the total interest expense recognized in the accompanying interim unaudited condensed consolidated statements of operations:

8

| Three Months Ended March 31, | ||||||||

| (Thousands of U.S. Dollars) | 2023 | 2022 | ||||||

| Contractual interest and other financing expenses | $ | 11,055 | $ | 11,241 | ||||

| Amortization of debt issuance costs | 781 | 887 | ||||||

| $ | 11,836 | $ | 12,128 | |||||

5. Share Capital

| Shares of Common Stock | |||||

| Shares issued at December 31, 2022 and March 31, 2023 | 368,898,619 | ||||

| Shares outstanding at December 31, 2022 | 346,151,157 | ||||

| Treasury stock | (13,082,115) | ||||

| Shares outstanding at March 31, 2023 | 333,069,042 | ||||

During the year ended December 31, 2022, the Company implemented a share re-purchase program (the “2022 Program”) through the facilities of the Toronto Stock Exchange (“TSX”) and eligible alternative trading platforms in Canada. Under the 2022 Program, the Company is able to purchase at prevailing market prices up to 36,033,969 shares of Common Stock, representing approximately 10% of the issued and outstanding shares of Common Stock as of August 22, 2022. The 2022 Program will expire on August 31, 2023, or earlier if the 10% share maximum is reached. Re-purchases are subject to the availability of stock, prevailing market conditions, the trading price of the Company’s stock, the Company’s financial performance and other conditions.

During the three months ended March 31, 2023, the Company re-purchased 13,082,115 shares at a weighted average price of $0.82 per share (three months ended March 31, 2022 - nil). The re-purchased shares were held by the Company and recorded as treasury stock. As of March 31, 2023, the Company held 35,829,577 treasury stock shares (December 31, 2022 - 22,747,462).

Equity Compensation Awards

The following table provides information about performance stock units (“PSUs”), deferred share units (“DSUs”), and stock option activity for the three months ended March 31, 2023:

| PSUs | DSUs | Stock Options | |||||||||||||||

| Number of Outstanding Share Units | Number of Outstanding Share Units | Number of Outstanding Stock Options | Weighted Average Exercise Price/Stock Option ($) | ||||||||||||||

| Balance, December 31, 2022 | 31,528,233 | 6,561,859 | 17,302,860 | 1.15 | |||||||||||||

| Granted | 14,614,248 | 220,124 | 4,010,289 | 0.86 | |||||||||||||

| Exercised | (15,234,082) | — | — | — | |||||||||||||

| Forfeited | (30,448) | — | (13,799) | 1.01 | |||||||||||||

| Expired | — | — | (1,267,481) | 2.47 | |||||||||||||

| Balance, March 31, 2023 | 30,877,951 | 6,781,983 | 20,031,869 | 1.01 | |||||||||||||

For the three months ended March 31, 2023 and 2022, there was $1.5 million and $4.6 million of stock-based compensation expense, respectively.

At March 31, 2023, there was $19.5 million (December 31, 2022 - $10.5 million) of unrecognized compensation costs related to unvested PSUs and stock options, which are expected to be recognized over a weighted-average period of 2.1 years. During the three months ended March 31, 2023, the Company paid out $15.1 million for PSUs vested on December 31, 2022 (three months ended March 31, 2022 - $2.4 million for PSUs vested on December 31, 2021).

Net (Loss) Income per Share

9

Basic net loss or income per share is calculated by dividing net loss or income attributable to common shareholders by the weighted average number of shares of common stock issued and outstanding during each period.

Diluted net loss or income per share is calculated using the treasury stock method for share-based compensation arrangements. The treasury stock method assumes that any proceeds obtained on the exercise of share-based compensation arrangements would be used to purchase common shares at the average market price during the period. The weighted average number of shares is then adjusted by the difference between the number of shares issued from the exercise of share-based compensation arrangements and shares re-purchased from the related proceeds. Anti-dilutive shares represent potentially dilutive securities excluded from the computation of diluted loss or income per share as their impact would be anti-dilutive.

Weighted Average Shares Outstanding

| Three Months Ended March 31, | ||||||||

| 2023 | 2022 | |||||||

| Weighted average number of common shares outstanding | 344,513,998 | 367,386,664 | ||||||

| Shares issuable pursuant to stock options | — | 12,950,523 | ||||||

| Shares assumed to be purchased from proceeds of stock options | — | (7,961,942) | ||||||

| Weighted average number of diluted common shares outstanding | 344,513,998 | 372,375,245 | ||||||

For the three months ended March 31, 2023, and 2022, on a weighted average basis, all options and 5,331,160 options, respectively, were excluded from the diluted (loss) income per share calculation as the options were anti-dilutive.

6. Revenue

The Company’s revenues are generated from oil sales at prices that reflect the blended prices received upon shipment by the purchaser at defined sales points or defined by contract relative to ICE Brent and adjusted for Vasconia, Oriente or Castilla crude differentials, quality and transportation discounts and premiums each month. For the three months ended March 31, 2023, 100% (three months ended March 31, 2022 - 100%) of the Company’s revenue resulted from oil sales. During the three months ended March 31, 2023, quality and transportation discounts were 22% of the average ICE Brent price (three months ended March 31, 2022 - 13%).

During the three months ended March 31, 2023, the Company’s production was sold primarily to one major customer in Colombia, representing 97% of the total sales volumes (three months ended March 31, 2022 - two customers, representing 57% and 43% of the total sales volumes).

As at March 31, 2023, accounts receivable included $3.2 million of accrued sales revenue related to March 2023 production (December 31, 2022 - nil related to December 2022 production).

7. Taxes

The Company's effective tax rate was 142% for the three months ended March 31, 2023, compared to 74% in the comparative period of 2022. Current income tax expense was $17.6 million for the three months ended March 31, 2023, compared to $20.8 million in the corresponding period of 2022, primarily due to a decrease in taxable income.

The deferred income tax expense for the three months ended March 31, 2023, was $15.3 million mainly the result of tax depreciation being higher than accounting depreciation and the use of tax losses to offset taxable income in Colombia. The deferred income tax expense in the comparative period of 2022 was $18.7 million as the result of tax depreciation being higher compared to accounting depreciation in Colombia.

For the three months ended March 31, 2023, the difference between the effective tax rate of 142% and the 50% Colombian tax rate was primarily due to an increase in non-deductible foreign translation adjustments, the impact of foreign taxes, non-deductible royalty in Colombia and increase in the valuation allowance. These were partially offset by other permanent differences.

For the three months ended March 31, 2022, the difference between the effective tax rate of 74% and the 35% Colombian tax rate was primarily due to an increase in the impact of foreign taxes, foreign translation adjustments, increase in the valuation allowance, other permanent differences, and non-deductible stock-based compensation.

10

8. Contingencies

Legal Proceedings

Gran Tierra has several lawsuits and claims pending. The outcome of the lawsuits and disputes cannot be predicted with certainty; Gran Tierra believes the resolution of these matters would not have a material adverse effect on the Company’s consolidated financial position, results of operations, or cash flows. Gran Tierra records costs as they are incurred or become probable and determinable.

Letters of credit and other credit support

At March 31, 2023, the Company had provided letters of credit and other credit support totaling $109.6 million (December 31, 2022 - $111.1 million) as security relating to work commitment guarantees in Colombia and Ecuador contained in exploration contracts and other capital or operating requirements.

9. Financial Instruments and Fair Value Measurement

Financial Instruments

Financial instruments are initially recorded at fair value, defined as the price that would be received to sell an asset or paid to market participants to settle liability at the measurement date. For financial instruments carried at fair value, GAAP establishes a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. This hierarchy consists of three broad levels:

•Level 1 - Inputs representing quoted market prices in active markets for identical assets and liabilities

•Level 2 - Inputs other than quoted prices included within Level 1 that are observable for the assets and liabilities, either directly or indirectly

•Level 3 - Unobservable inputs for assets and liabilities

At March 31, 2023, the Company’s financial instruments recognized on the balance sheet consist of cash and cash equivalents, restricted cash and cash equivalents, accounts receivable, other long-term assets, accounts payable and accrued liabilities, other short-term payables, long-term debt, short-term and long-term equity compensation reward liability and other long-term liabilities. The Company uses appropriate valuation techniques based on the available information to measure the fair values of assets and liabilities.

Fair Value Measurement

The following table presents the Company’s fair value measurements of its financial instruments as of March 31, 2023, and December 31, 2022:

11

| As at March 31, 2023 | As at December 31, 2022 | ||||||||||

| (Thousands of U.S. Dollars) | |||||||||||

| Level 1 | |||||||||||

| Assets | |||||||||||

PEF - current (2) | $ | 8,874 | $ | 5,981 | |||||||

PEF - long-term(1) | — | 9,975 | |||||||||

| $ | 8,874 | $ | 15,956 | ||||||||

| Liabilities | |||||||||||

DSUs liability - long-term(3) | $ | 5,962 | $ | 6,496 | |||||||

6.25% Senior Notes | 233,645 | 243,801 | |||||||||

7.75% Senior Notes | 235,500 | 241,455 | |||||||||

| $ | 475,107 | $ | 491,752 | ||||||||

| Level 2 | |||||||||||

| Assets | |||||||||||

Restricted cash and cash equivalents - long-term(1) | 5,710 | 5,344 | |||||||||

| $ | 5,710 | $ | 5,344 | ||||||||

| Liabilities | |||||||||||

| PSUs liability - current | 8,011 | 15,082 | |||||||||

PSUs liability - long-term(3) | 2,630 | 9,941 | |||||||||

| $ | 10,641 | $ | 25,023 | ||||||||

(1) The long-term portion of restricted cash and PEF is included in the other long-term assets on the Company’s balance sheet

(2) The current portion of PEF is included in the other current assets on the Company’s balance sheet

(3) Long-term DSUs and PSUs liabilities are included in the long-term equity compensation award liability on the Company’s balance sheet

The fair values of cash and cash equivalents, current restricted cash and cash equivalents, accounts receivable, accounts payable and accrued liabilities approximate their carrying amounts due to the short-term maturity of these instruments.

.

Restricted cash - long-term

The fair value of long-term restricted cash and cash equivalents approximated their carrying value because interest rates are variable and reflective of market rates.

Prepaid Equity Forward (“PEF”)

To reduce the Company’s exposure to changes in the trading price of the Company’s common shares on outstanding PSUs and DSUs, the Company entered into a PEF. At the end of the term, the counterparty will pay the Company an amount equivalent to the notional amount of the shares using the price of the Company’s common shares at the valuation date. The Company has the discretion to increase or decrease the notional amount of the PEF or terminate the agreement early. As at March 31, 2023, the Company’s PEF had a notional amount of 10 million shares with a fair value of $8.9 million (As at December 31, 2022 - 16 million shares with a fair value of $16.0 million). During the three months ended March 31, 2023, the Company recorded a $1.7 million loss on the PEF in general and administrative expenses (three months ended March 31, 2022- $7.8 million gain). The

12

fair value of the PEF asset was estimated using the Company’s share price quoted in active markets at the end of each reporting period.

DSUs liability

The fair value of DSUs liability was estimated using the Company’s share price quoted in active markets at the end of each reporting period.

PSUs liability

The fair value of the PSUs liability was estimated based on a pricing model using inputs such as Company’s share price and PSUs performance factor.

Senior Notes

Financial instruments not recorded at fair value at March 31, 2023, were the Senior Notes (Note 4).

At March 31, 2023, the carrying amounts of the 6.25% Senior Notes and the 7.75% Senior Notes were $268.5 million and $293.6 million, respectively, which represented the aggregate principal amount less unamortized debt issuance costs, and the fair values were $233.6 million and $235.5 million, respectively.

During the three months ended March 31, 2023, the Company did not incur any gains or losses related to derivatives (three months ended March 31, 2022 - $21.4 million loss related to commodity price derivatives).

10. Supplemental Cash Flow Information

The following table provides a reconciliation of cash and cash equivalents and restricted cash and cash equivalents shown as a sum of these amounts in the interim unaudited condensed consolidated statements of cash flows:

| As at March 31, | As at December 31, | ||||||||||||||||

| (Thousands of U.S. Dollars) | 2023 | 2022 | 2022 | 2021 | |||||||||||||

| Cash and cash equivalents | $ | 105,684 | $ | 58,707 | $ | 126,873 | $ | 26,109 | |||||||||

| Restricted cash and cash equivalents - current | 1,142 | 1,142 | 1,142 | 392 | |||||||||||||

Restricted cash and cash equivalents - long-term (1) | 5,710 | 5,252 | 5,343 | 4,903 | |||||||||||||

| $ | 112,536 | $ | 65,101 | $ | 133,358 | $ | 31,404 | ||||||||||

(1) Included in other long-term assets on the Company’s balance sheet

Net changes in assets and liabilities from operating activities were as follows:

| Three Months Ended March 31, | |||||||||||

| (Thousands of U.S. Dollars) | 2023 | 2022 | |||||||||

| Accounts receivable and other long-term assets | $ | (3,022) | $ | (10,150) | |||||||

| Derivatives | — | 3,276 | |||||||||

| Prepaid Equity Forward | 7,806 | (10,982) | |||||||||

| Prepaids & Inventory | 740 | (159) | |||||||||

| Accounts payable and accrued and other long-term liabilities | (17,252) | 12,021 | |||||||||

| Taxes receivable and payable | 965 | 22,514 | |||||||||

| Net changes in assets and liabilities from operating activities | $ | (10,763) | $ | 16,520 | |||||||

13

Changes in non-cash investing working capital for the three months ended March 31, 2023, were comprised of an increase in accounts payable and accrued liabilities of $14.9 million (three months ended March 31, 2022, a decrease in accounts payable and accrued liabilities of $1.7 million and an increase in accounts receivable of $0.1 million).

The following table provides additional supplemental cash flow disclosures:

| Three Months Ended March 31, | |||||||||||

| (Thousands of U.S. Dollars) | 2023 | 2022 | |||||||||

| Cash paid for income taxes | $ | 8,461 | $ | 9,703 | |||||||

| Cash paid for interest | $ | 8,781 | $ | 10,042 | |||||||

| Non-cash investing activities: | |||||||||||

| Net liabilities related to property, plant and equipment, end of period | $ | 69,989 | $ | 28,339 | |||||||

14

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion of our financial condition and results of operations should be read in conjunction with the “Financial Statements” as set out in Part I, Item 1 of this Quarterly Report on Form 10-Q, as well as the “Financial Statements and Supplementary Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in Part II, Items 7 and 8, respectively, of our 2022 Annual Report on Form 10-K. Please see the cautionary language at the beginning of this Quarterly Report on Form 10-Q regarding the identification of and risks relating to forward-looking statements and the risk factors described in Part II, Item 1A “Risk Factors” of this Quarterly Report on Form 10-Q, as well as Part I, Item 1A “Risk Factors” in our 2022 Annual Report on Form 10-K.

Financial and Operational Highlights

Key Highlights for the first quarter of 2023

•Net loss in the first quarter of 2023 was $9.7 million or $(0.03) per share basic and diluted, compared to a net income of $14.1 million or $0.04 per share basic and diluted in the first quarter of 2022

•Income before income taxes in the first quarter of 2023 was $23.2 million compared to an income before income taxes of $53.7 million in the first quarter of 2022

•During the first quarter of 2023, we re-purchased $8.0 million of 6.25% Senior Notes for a cash consideration of $6.8 million and re-purchased 13,082,115 of our common shares at a weighted average price of $0.82 per share

•Funds flow from operations(2) decreased by 31% to $60.0 million compared to the first quarter of 2022, primarily due to a 16% decrease in Brent price, an 18% increase in operating costs, and an 8% increase in transportation expenses which were offset by an 11% higher sales volumes. Compared to the prior quarter, funds flow decreased by 26%, primarily due to a 7% decrease in Brent price, a 2% decrease in sales volumes, 26% higher transportation costs and offset by a 10% decrease in operating costs

•NAR production for the first quarter of 2023 increased by 12% to 25,526 BOPD, compared to 22,833 BOPD in the first quarter of 2022 and was comparable to the fourth quarter of 2022

•Sales volumes for the first quarter of 2023 increased by 11% to 25,171 BOPD, compared to 22,730 BOPD in the first quarter of 2022 and decreased by 2% from the fourth quarter of 2022

•Oil sales were $144.2 million, 17% lower compared to the first quarter of 2022, mainly due to a 16% decrease in Brent price. Oil sales decreased by 11% compared to $162.6 million in the fourth quarter of 2022 due to a 7% decrease in Brent price and a 2% lower sales volumes

•Operating expenses increased by 18% to $41.4 million or by $1.19 per bbl to $18.26 per bbl when compared to the first quarter of 2022, primarily as a result of higher lifting costs attributed to Ecuador. Operating expenses decreased by 10% or $1.27 per bbl from $46.1 million or $19.53 per bbl when compared to the fourth quarter of 2022, primarily due to lower workover activities

•Transportation expenses per bbl decreased by 3% in the first quarter of 2023 due to higher sales volumes when compared to the first quarter of 2022 and increased 31% from the fourth quarter of 2022 due to Ecuador sales

•Operating netback(2) decreased to $99.8 million compared to $136.8 million in the first quarter of 2022 and decreased from $114.1 million in the fourth quarter of 2022

•Adjusted EBITDA(2) decreased to $88.7 million compared to $119.4 million in the first quarter of 2022 and decreased from $108.8 million in the fourth quarter of 2022

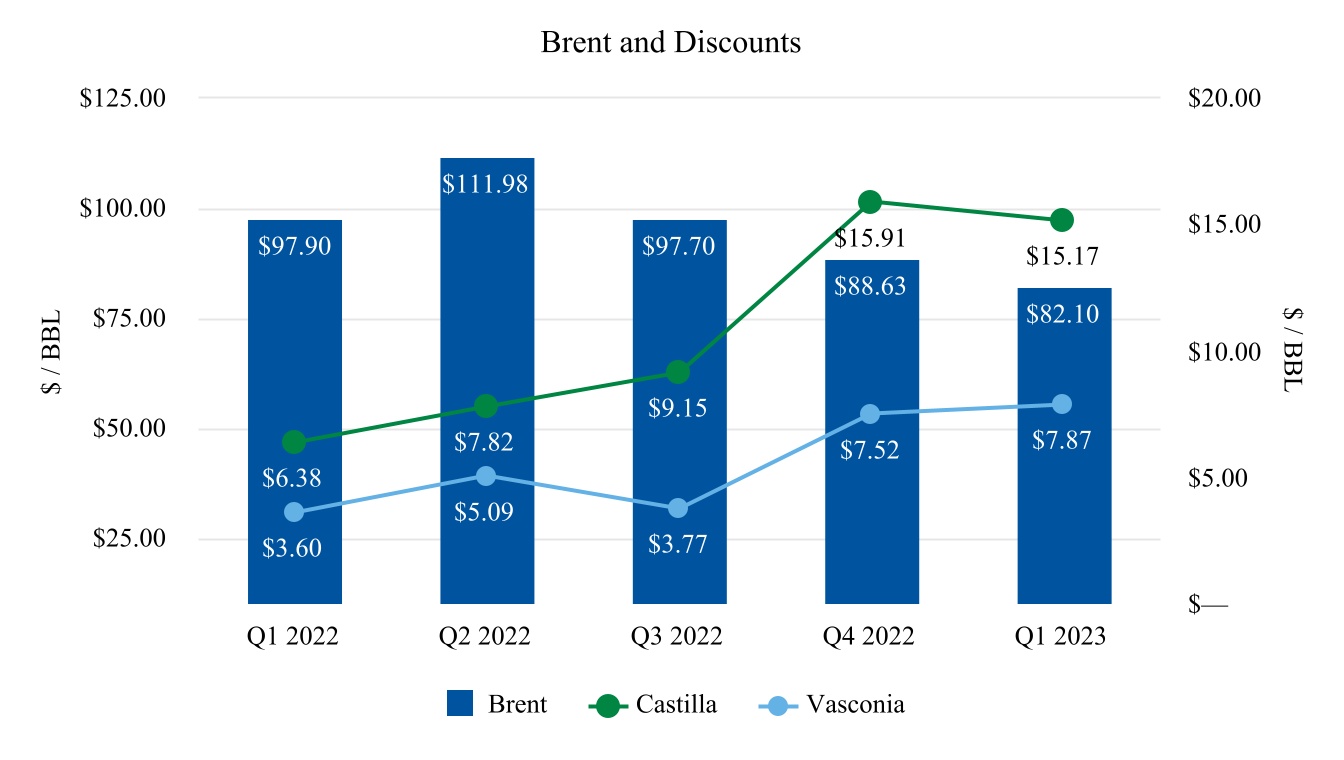

•Quality and transportation discounts for the first quarter of 2023 increased to $18.45 per bbl compared to $12.57 per bbl in the first quarter of 2022, primarily as a result of the widening of the Castilla and Vasconia differentials and decreased from $19.74 per bbl compared to the fourth quarter of 2022

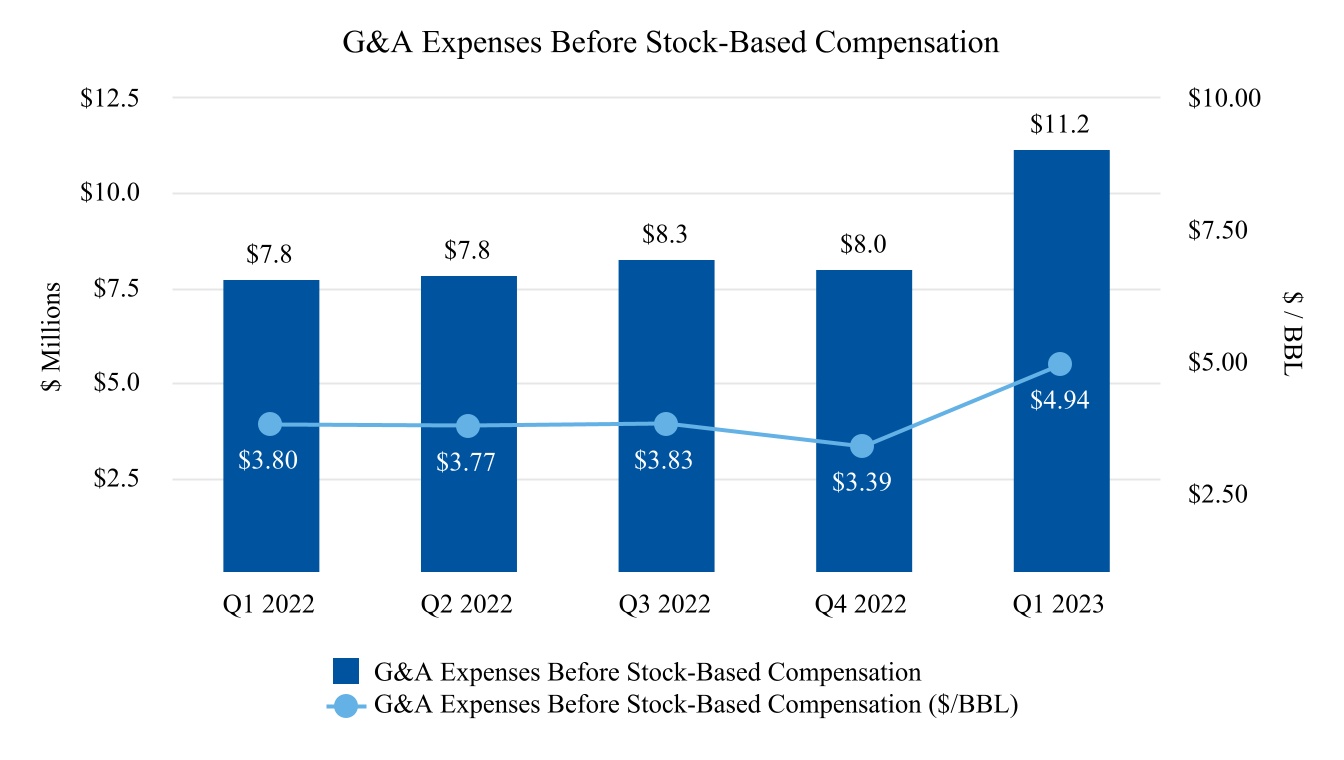

•General and administrative expenses (“G&A”) before stock-based compensation increased by 44% compared to the first quarter of 2022 due to optimization projects and lease obligations expenses and increased by 40% from the fourth quarter of 2022 for the same reason mentioned above

•Capital additions for the first quarter of 2023 were $71.1 million, an increase of 71% compared to the first quarter of 2022, as a result of the drilling program in all major fields and decreased 3% from the fourth quarter of 2022

•On April 11, 2023, we announced our agreement with Ecopetrol, the national oil company of Colombia, by which Gran Tierra and Ecopetrol renegotiated the terms and the duration of the contract for 20 years after the effective date for the Suroriente Block in the Putumayo Basin, which was scheduled to end in mid-2024. The agreement is subject to certain conditions precedent, including regulatory approval by the Superintendence of Industry and Commerce of Colombia (“SIC”). The satisfaction of such conditions precedent will determine the agreement’s effective date

15

| (Thousands of U.S. Dollars, unless otherwise indicated) | Three Months Ended March 31, | Three Months Ended December 31, | |||||||||||||||

| 2023 | 2022 | % Change | 2022 | ||||||||||||||

| Average Daily Volumes (BOPD) | |||||||||||||||||

| Consolidated | |||||||||||||||||

| Working Interest (“WI”) Production Before Royalties | 31,611 | 29,362 | 8 | 32,595 | |||||||||||||

| Royalties | (6,085) | (6,529) | (7) | (6,880) | |||||||||||||

| Production NAR | 25,526 | 22,833 | 12 | 25,715 | |||||||||||||

| Increase in Inventory | (355) | (103) | 245 | (53) | |||||||||||||

Sales(1) | 25,171 | 22,730 | 11 | 25,662 | |||||||||||||

| Net (Loss) Income | $ | (9,700) | $ | 14,119 | (169) | $ | 33,275 | ||||||||||

| Operating Netback | |||||||||||||||||

| Oil Sales | $ | 144,190 | $ | 174,569 | (17) | $ | 162,637 | ||||||||||

| Operating Expenses | (41,369) | (34,935) | 18 | (46,119) | |||||||||||||

| Transportation Expenses | (3,066) | (2,834) | 8 | (2,433) | |||||||||||||

Operating Netback(2) | $ | 99,755 | $ | 136,800 | (27) | $ | 114,085 | ||||||||||

| G&A Expenses Before Stock-Based Compensation | $ | 11,196 | $ | 7,779 | 44 | $ | 7,998 | ||||||||||

| G&A Stock-Based Compensation Expense | 1,500 | 4,557 | (67) | 2,673 | |||||||||||||

| G&A Expenses, Including Stock-Based Compensation | $ | 12,696 | $ | 12,336 | 3 | $ | 10,671 | ||||||||||

Adjusted EBITDA(2) | $ | 88,677 | $ | 119,378 | (26) | $ | 108,828 | ||||||||||

Funds Flow From Operations(2) | $ | 60,016 | $ | 87,310 | (31) | $ | 81,343 | ||||||||||

| Capital Expenditures | $ | 71,062 | $ | 41,483 | 71 | $ | 72,887 | ||||||||||

(1) Sales volumes represent production NAR adjusted for inventory changes.

(2) Non-GAAP measures

Operating netback, EBITDA, adjusted EBITDA, and funds flow from operations are non-GAAP measures that do not have any standardized meaning prescribed under GAAP. Management views these measures as financial performance measures. Investors are cautioned that these measures should not be construed as alternatives to oil sales, net (loss) income or other measures of financial performance as determined in accordance with GAAP. Our method of calculating these measures may differ from other companies and, accordingly, may not be comparable to similar measures used by other companies. Disclosure of each non-GAAP financial measure is preceded by the corresponding GAAP measure so as not to imply that more emphasis should be placed on the non-GAAP measure.

Operating netback, as presented, is defined as oil sales less operating and transportation expenses. Management believes that operating netback is a useful supplemental measure for management and investors to analyze financial performance and provides an indication of the results generated by our principal business activities prior to the consideration of other income and expenses. A reconciliation from oil sales to operating netback is provided in the table above.

EBITDA, as presented, is defined as net (loss) income adjusted for depletion, depreciation and accretion (“DD&A”) expenses, interest expense and income tax expense. Adjusted EBITDA, as presented, is defined as EBITDA adjusted for non-cash lease expense, lease payments, unrealized foreign exchange gain or loss, stock-based compensation expense or recovery, unrealized derivative instruments gain or loss, inventory impairment, gain on re-purchase of Senior Notes and other financial instruments gain. Management uses this supplemental measure to analyze performance and income generated by our principal business activities prior to the consideration of how non-cash items affect that income and believes that this financial measure is useful supplemental information for investors to analyze our performance and our financial results. A reconciliation from net (loss) income to EBITDA and adjusted EBITDA is as follows:

16

| Three Months Ended March 31, | Three Months Ended December 31, | |||||||||||||

| (Thousands of U.S. Dollars) | 2023 | 2022 | 2022 | |||||||||||

| Net (loss) income | $ | (9,700) | $ | 14,119 | $ | 33,275 | ||||||||

| Adjustments to reconcile net (loss) income to EBITDA and Adjusted EBITDA | ||||||||||||||

| DD&A expenses | 51,721 | 40,963 | 51,781 | |||||||||||

| Interest expense | 11,836 | 12,128 | 10,750 | |||||||||||

| Current income tax expense | 32,883 | 39,540 | 5,966 | |||||||||||

| EBITDA (non-GAAP) | $ | 86,740 | $ | 106,750 | $ | 101,772 | ||||||||

| Non-cash lease expense | 1,144 | 411 | 809 | |||||||||||

| Lease payments | (606) | (344) | (532) | |||||||||||

| Unrealized foreign exchange loss (gain) | 514 | (4,839) | 4,113 | |||||||||||

| Stock-based compensation expense | 1,500 | 4,557 | 2,673 | |||||||||||

| Unrealized derivative instruments loss | — | 12,843 | — | |||||||||||

| Inventory impairment | 475 | — | — | |||||||||||

| Gain on re-purchase of Senior Notes | (1,090) | — | — | |||||||||||

| Other financial instruments gain | — | — | (7) | |||||||||||

| Adjusted EBITDA (non-GAAP) | $ | 88,677 | $ | 119,378 | $ | 108,828 | ||||||||

Funds flow from operations, as presented, is defined as net (loss) income adjusted for DD&A expenses, inventory impairment, deferred tax expense or recovery, stock-based compensation expense or recovery, amortization of debt issuance costs, non-cash lease expense, lease payments, unrealized foreign exchange gain or loss, derivative instruments gain or loss, cash settlement on derivative instruments, gain on re-purchase of Senior Notes, and other financial instruments gain. Management uses this financial measure to analyze performance and income generated by our principal business activities prior to the consideration of how non-cash items affect that income and believes that this financial measure is also useful supplemental information for investors to analyze performance and our financial results. A reconciliation from net (loss) income to funds flow from operations is as follows:

| Three Months Ended March 31, | Three Months Ended December 31, | |||||||||||||

| (Thousands of U.S. Dollars) | 2023 | 2022 | 2022 | |||||||||||

| Net (loss) income | $ | (9,700) | $ | 14,119 | $ | 33,275 | ||||||||

| Adjustments to reconcile net(loss) income to funds flow from operations | ||||||||||||||

| DD&A expenses | 51,721 | 40,963 | 51,781 | |||||||||||

| Inventory impairment | 475 | — | — | |||||||||||

| Deferred income tax expense (recovery) | 15,277 | 18,713 | (11,528) | |||||||||||

| Stock-based compensation expense | 1,500 | 4,557 | 2,673 | |||||||||||

| Amortization of debt issuance costs | 781 | 887 | 759 | |||||||||||

| Non-cash lease expense | 1,144 | 411 | 809 | |||||||||||

| Lease payments | (606) | (344) | (532) | |||||||||||

| Unrealized foreign exchange loss (gain) | 514 | (4,839) | 4,113 | |||||||||||

| Derivative instruments loss | — | 21,439 | — | |||||||||||

| Cash settlements on derivative instruments | — | (8,596) | — | |||||||||||

| Gain on re-purchase of Senior Notes | (1,090) | — | — | |||||||||||

| Other financial instruments gain | — | — | (7) | |||||||||||

| Funds flow from operations (non-GAAP) | $ | 60,016 | $ | 87,310 | $ | 81,343 | ||||||||

Additional Operational Results

17

| Three Months Ended March 31, | Three Months Ended December 31, | ||||||||||||||||

| (Thousands of U.S. Dollars) | 2023 | 2022 | % Change | 2022 | |||||||||||||

| Oil sales | $ | 144,190 | $ | 174,569 | (17) | $ | 162,637 | ||||||||||

| Operating expenses | 41,369 | 34,935 | 18 | 46,119 | |||||||||||||

| Transportation expenses | 3,066 | 2,834 | 8 | 2,433 | |||||||||||||

Operating netback(1) | 99,755 | 136,800 | (27) | 114,085 | |||||||||||||

| DD&A expenses | 51,721 | 40,963 | 26 | 51,781 | |||||||||||||

| Inventory impairment | 475 | — | 100 | — | |||||||||||||

| G&A expenses before stock-based compensation | 11,196 | 7,779 | 44 | 7,998 | |||||||||||||

| G&A stock-based compensation expense | 1,500 | 4,557 | (67) | 2,673 | |||||||||||||

| Foreign exchange loss (gain) | 1,702 | (3,725) | (146) | 2,092 | |||||||||||||

| Derivative instruments loss | — | 21,439 | (100) | — | |||||||||||||

| Other financial instruments gain | — | — | — | (7) | |||||||||||||

| Gain on re-purchase of Senior Notes | (1,090) | — | 100 | — | |||||||||||||

| Interest expense | 11,836 | 12,128 | (2) | 10,750 | |||||||||||||

| 77,340 | 83,141 | (7) | 75,287 | ||||||||||||||

| Interest income | 768 | — | 100 | 443 | |||||||||||||

| Income before income taxes | 23,183 | 53,659 | (57) | 39,241 | |||||||||||||

| Current income tax expense | 17,606 | 20,827 | (15) | 17,494 | |||||||||||||

| Deferred income tax expense (recovery) | 15,277 | 18,713 | (18) | (11,528) | |||||||||||||

| 32,883 | 39,540 | (17) | 5,966 | ||||||||||||||

| Net (loss) income | $ | (9,700) | $ | 14,119 | (169) | $ | 33,275 | ||||||||||

| Sales Volumes (NAR) | |||||||||||||||||

| Total sales volumes, BOPD | 25,171 | 22,730 | 11 | 25,662 | |||||||||||||

| Brent Price per bbl | $ | 82.10 | $ | 97.90 | (16) | $ | 88.63 | ||||||||||

| Consolidated Results of Operations per bbl Sales Volumes NAR | |||||||||||||||||

| Oil sales | $ | 63.65 | $ | 85.33 | (25) | $ | 68.89 | ||||||||||

| Operating expenses | 18.26 | 17.07 | 7 | 19.53 | |||||||||||||

| Transportation expenses | 1.35 | 1.39 | (3) | 1.03 | |||||||||||||

Operating netback(1) | 44.04 | 66.87 | (34) | 48.33 | |||||||||||||

| DD&A expenses | 22.83 | 20.02 | 14 | 21.93 | |||||||||||||

| Inventory impairment | 0.21 | — | 100 | — | |||||||||||||

| G&A expenses before stock-based compensation | 4.94 | 3.80 | 30 | 3.39 | |||||||||||||

| G&A stock-based compensation expense | 0.66 | 2.23 | (70) | 1.13 | |||||||||||||

| Foreign exchange loss (gain) | 0.75 | (1.82) | (141) | 0.89 | |||||||||||||

18

| Derivative instruments loss | — | 10.48 | (100) | — | |||||||||||||

| Other financial instruments gain | — | — | — | — | |||||||||||||

| Gain on re-purchase of Senior Notes | (0.48) | — | 100 | — | |||||||||||||

| Interest expense | 5.22 | 5.93 | (12) | 4.55 | |||||||||||||

| 34.13 | 40.64 | (16) | 31.89 | ||||||||||||||

| Interest income | 0.34 | — | 100 | 0.19 | |||||||||||||

| Income before income taxes | 10.25 | 26.22 | (61) | 16.63 | |||||||||||||

| Current income tax expense | 7.77 | 10.18 | (24) | 7.41 | |||||||||||||

| Deferred income tax expense (recovery) | 6.74 | 9.15 | (26) | (4.88) | |||||||||||||

| 14.51 | 19.33 | (25) | 2.53 | ||||||||||||||

| Net (loss) income | $ | (4.26) | $ | 6.89 | (162) | $ | 14.10 | ||||||||||

(1) Operating netback is a non-GAAP measure that does not have any standardized meaning prescribed under GAAP. Refer to “Financial and Operational Highlights—non-GAAP measures” for a definition of this measure.

Oil Production and Sales Volumes, BOPD

| Three Months Ended March 31, | Three Months Ended December 31, | |||||||||||||

| 2023 | 2022 | 2022 | ||||||||||||

| Average Daily Volumes (BOPD) | ||||||||||||||

| WI Production Before Royalties | 31,611 | 29,362 | 32,595 | |||||||||||

| Royalties | (6,085) | (6,529) | (6,880) | |||||||||||

| Production NAR | 25,526 | 22,833 | 25,715 | |||||||||||

| Increase in Inventory | (355) | (103) | (53) | |||||||||||

| Sales | 25,171 | 22,730 | 25,662 | |||||||||||

| Royalties, % of WI Production Before Royalties | 19 | % | 22 | % | 21 | % | ||||||||

Oil production NAR for the three months ended March 31, 2023, increased by 12% to 25,526 from the corresponding period of 2022 due to successful drilling and workover campaigns in all major fields and production from Ecuador during the current quarter. Oil production NAR was comparable to prior quarter.

Royalties as a percentage of production for the three months ended March 31, 2023, decreased to 19% compared to the corresponding period of 2022 and the prior quarter commensurate with the decrease in benchmark oil prices and the price sensitive royalty regime in Colombia.

19

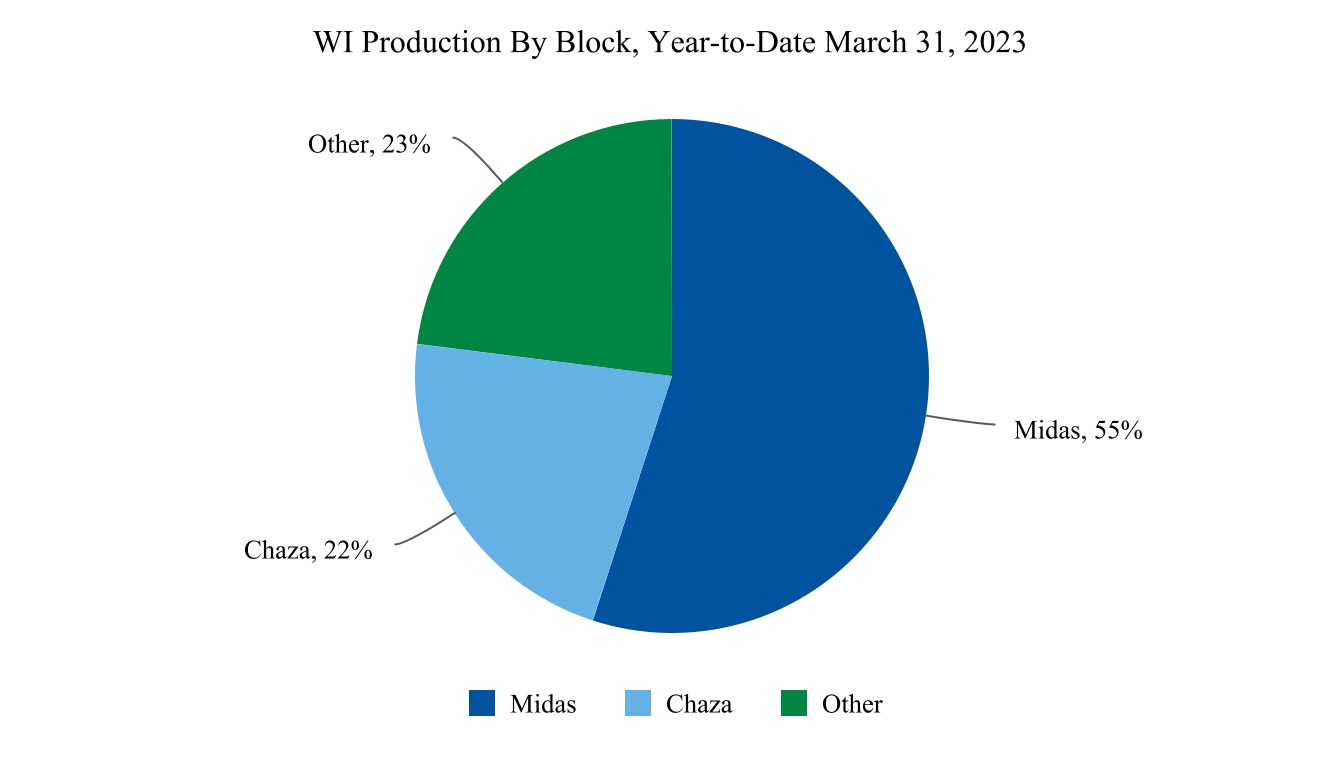

The Midas block includes the Acordionero, Chuira, and Ayombero oil fields, and the Chaza block includes the Costayaco and Moqueta oil fields.

Realized price per bbl for the three months ended March 31, 2023, decreased by 25% compared to the corresponding period of 2022, mainly as a result of a 16% decrease in Brent price and higher differentials. Castilla and Vasconia differentials increased to $15.17 per bbl and $7.87 per bbl from $6.38 per bbl and $3.60 per bbl, respectively, in the corresponding period of 2022. Compared to the prior quarter, the average realized price per bbl decreased by 8%, primarily due to a 7% decrease in Brent price.

20

Oil sales for the three months ended March 31, 2023, decreased by 17% to $144.2 million compared to the corresponding period of 2022 due to a 16% decrease in Brent price and higher Castilla and Vasconia differentials. Additionally, during the three months ended March 31, 2023, we commenced oil sales in Ecuador, which contributed $3.2 million to oil sales and were subject to a $13.89 per bbl Oriente differential.

Compared to the prior quarter, oil sales decreased by 11%, primarily as a result of a 7% decrease in Brent price and a 2% decrease in sales volumes.

The following table shows the effect of changes in realized price and sale volumes on our oil sales for the three months ended March 31, 2023, compared to the prior quarter and the corresponding period of 2022:

| (Thousands of U.S. Dollars) | First Quarter 2023 Compared with Fourth Quarter 2022 | First Quarter 2023 Compared with First Quarter 2022 | |||||||||

| Oil sales for the comparative period | $ | 162,637 | $ | 174,569 | |||||||

| Realized sales price decrease effect | (11,867) | (49,120) | |||||||||

| Sales volumes (decrease) increase effect | (6,580) | 18,741 | |||||||||

| Oil sales for the three month ended March 31, 2023 | $ | 144,190 | $ | 144,190 | |||||||

21

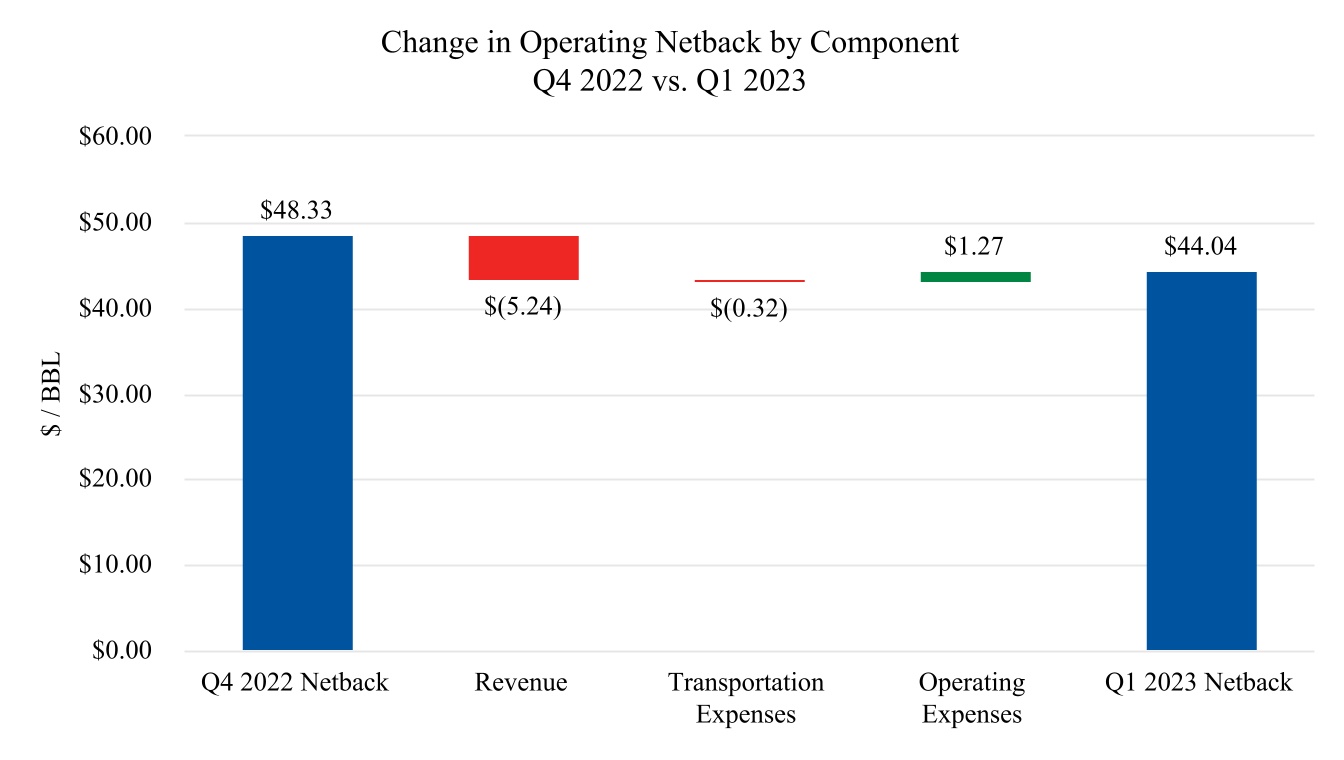

Operating Netback

| Three Months Ended March 31, | Three Months Ended December 31, | |||||||||||||

| (Thousands of U.S. Dollars) | 2023 | 2022 | 2022 | |||||||||||

| Oil Sales | $ | 144,190 | $ | 174,569 | $ | 162,637 | ||||||||

| Transportation Expenses | (3,066) | (2,834) | (2,433) | |||||||||||

| 141,124 | 171,735 | 160,204 | ||||||||||||

| Operating Expenses | (41,369) | (34,935) | (46,119) | |||||||||||

Operating Netback(1) | $ | 99,755 | $ | 136,800 | $ | 114,085 | ||||||||

| (U.S. Dollars Per bbl Sales Volumes NAR) | ||||||||||||||

| Brent | $ | 82.10 | $ | 97.90 | $ | 88.63 | ||||||||

| Quality and Transportation Discounts | (18.45) | (12.57) | (19.74) | |||||||||||

| Average Realized Price | 63.65 | 85.33 | 68.89 | |||||||||||

| Transportation Expenses | (1.35) | (1.39) | (1.03) | |||||||||||

| Average Realized Price Net of Transportation Expenses | 62.30 | 83.94 | 67.86 | |||||||||||

| Operating Expenses | (18.26) | (17.07) | (19.53) | |||||||||||

Operating Netback(1) | $ | 44.04 | $ | 66.87 | $ | 48.33 | ||||||||

(1) Operating netback is a non-GAAP measure that does not have any standardized meaning prescribed under GAAP. Refer to “Financial and Operational Highlights—non-GAAP measures” for a definition of this measure.

22

Operating expenses for the three months ended March 31, 2023, increased by 18% to $41.4 million or by $1.19 per bbl to $18.26 per bbl, compared to the corresponding period of 2022, primarily as a result of $1.23 per bbl higher lifting costs, $0.81 per bbl of which were attributed to Ecuador operations with the remainder associated with higher equipment rental in Colombia required for testing new exploration wells, partially offset by $0.04 per bbl lower workovers.

Compared to the prior quarter, operating expenses decreased by 10% or $1.27 per bbl from $46.1 million or $19.53 per bbl, primarily due to $1.08 per bbl lower workover activities and $0.19 per bbl lower lifting costs attributed to lower road maintenance activities, partially offset by operating costs incurred in Ecuador and higher equipment rental during the current quarter.

23

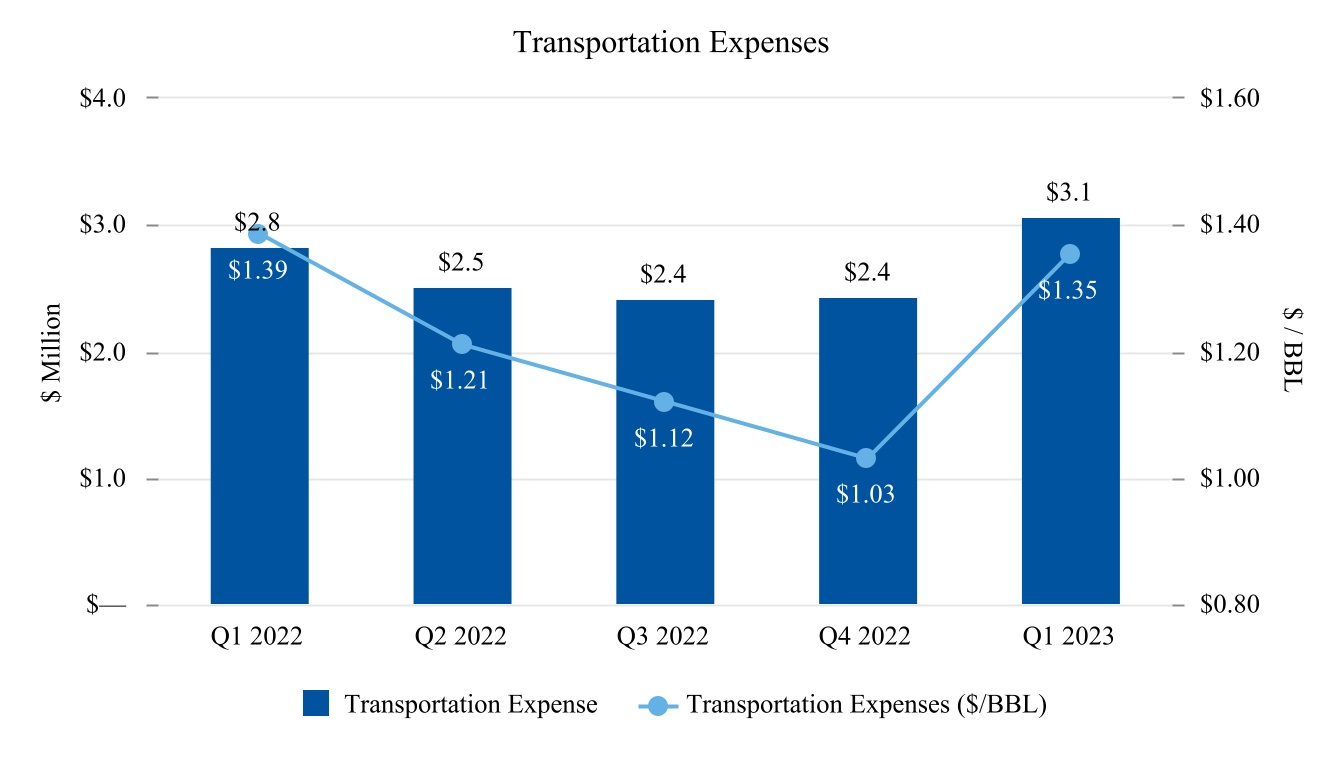

Transportation expenses

We have options to sell our oil through multiple pipelines and trucking routes. Each option has varying effects on realized sales price and transportation expenses. The following table shows the percentage of oil volumes we sold in Colombia and Ecuador using each option for the three months ended March 31, 2023, and 2022, and the prior quarter:

| Three Months Ended March 31, | Three Months Ended December 31, | |||||||||||||

| 2023 | 2022 | 2022 | ||||||||||||

| Volume transported through pipeline | 2 | % | — | % | — | % | ||||||||

| Volume sold at wellhead | 45 | % | 47 | % | 48 | % | ||||||||

| Volume transported via truck to sales point | 53 | % | 53 | % | 52 | % | ||||||||

| 100 | % | 100 | % | 100 | % | |||||||||

Volumes transported through pipeline or via truck receive a higher realized price but incur higher transportation expenses. Conversely, volumes sold at the wellhead have the opposite effect of a lower realized price, offset by lower transportation expenses.

Transportation expenses for the three months ended March 31, 2023, increased by 8% to $3.1 million, compared to the corresponding period of 2022 due to the utilization of new transportation routes for Ecuador sales and exploration wells brought online during the current quarter.

On a per bbl basis, transportation expenses decreased by 3% to $1.35 for the three months ended March 31, 2023, compared to the corresponding period of 2022 due to higher sales volumes in the current quarter.

Transportation expenses increased by 26% from $2.4 million in the prior quarter due to new transportation routes utilized for Ecuador sales and higher sales volumes transported via truck, which resulted in higher transportation costs per bbl in the current quarter.

24

DD&A Expenses

| Three Months Ended March 31, | Three Months Ended December 31, | |||||||||||||

| 2023 | 2022 | 2022 | ||||||||||||

| DD&A Expenses, thousands of U.S. Dollars | $ | 51,721 | $ | 40,963 | $ | 51,781 | ||||||||

| DD&A Expenses, U.S. Dollars per bbl | 22.83 | 20.02 | 21.93 | |||||||||||

DD&A expenses for the three months ended March 31, 2023, increased by 26% or by $2.81 per bbl due to increased production and higher costs in the depletable base compared to the corresponding period of 2022.

DD&A expenses were comparable to the prior quarter and increased by $0.90 per bbl when compared to the prior quarter, due to lower production and a higher costs in the depletable base.

G&A Expenses

| Three Months Ended March 31, | Three Months Ended December 31, | ||||||||||||||||

| (Thousands of U.S. Dollars) | 2023 | 2022 | % Change | 2022 | |||||||||||||

| G&A Expenses Before Stock-Based Compensation | $ | 11,196 | $ | 7,779 | 44 | $ | 7,998 | ||||||||||

| G&A Stock-Based Compensation Expense | 1,500 | 4,557 | (67) | 2,673 | |||||||||||||

| G&A Expenses, Including Stock-Based Compensation | $ | 12,696 | $ | 12,336 | 3 | $ | 10,671 | ||||||||||

| (U.S. Dollars Per bbl Sales Volumes NAR) | |||||||||||||||||

| G&A Expenses Before Stock-Based Compensation | $ | 4.94 | $ | 3.80 | 30 | $ | 3.39 | ||||||||||

| G&A Stock-Based Compensation Expense | 0.66 | 2.23 | (70) | 1.13 | |||||||||||||

| G&A Expenses, Including Stock-Based Compensation | $ | 5.60 | $ | 6.03 | (7) | $ | 4.52 | ||||||||||

For the three months ended March 31, 2023, G&A expenses before stock-based compensation increased by 44% to $11.2 million or by $1.14 per bbl to $4.94 per bbl due to higher costs attributed to optimization projects and lease obligations expenses associated with additional leases when compared to the corresponding period of 2022.

G&A expenses after stock-based compensation for the three months ended March 31, 2023, increased by 3% or $0.43 per bbl due to a lower share price compared to the corresponding period of 2022.

Compared to the prior quarter, G&A expenses before stock-based compensation increased by 40% or $1.55 on a per bbl basis for the same reason mentioned above.

Compared to the prior quarter, G&A expenses after stock-based compensation increased by 19% or $1.08 on a per bbl basis for the same reason as mentioned above, partially offset by lower stock-based compensation resulting from a lower share price in the first quarter of 2023.

25

Foreign Exchange Gains and Losses

For the three months ended March 31, 2023, we had a loss on foreign exchange of $1.7 million, compared to a $3.7 million gain in the corresponding period of 2022 and a $2.1 million loss in the prior quarter. Accounts receivable, taxes receivable, deferred income taxes, accounts payable, and prepaid equity forward (“PEF”) are considered monetary items and require translation from local currencies to U.S. dollar functional currency at each balance sheet date. This translation was the primary source of the foreign exchange gains and losses in the periods.

The following table presents the change in the U.S. dollar against the Colombian peso and Canadian dollar for the three months ended March 31, 2023, and 2022:

| Three Months Ended March 31, | Three Months Ended December 31, | |||||||||||||

| 2023 | 2022 | 2022 | ||||||||||||

| Change in the U.S. dollar against the Colombian peso | strengthened by | strengthened by | weakened by | |||||||||||

| 4% | 6% | 21% | ||||||||||||

| Change in the U.S. dollar against the Canadian dollar | strengthened by | strengthened by | weakened by | |||||||||||

| —% | 2% | 7% | ||||||||||||

26

Income Tax Expense

| Three Months Ended March 31, | ||||||||

| (Thousands of U.S. Dollars) | 2023 | 2022 | ||||||

| Income before income tax | $ | 23,183 | $ | 53,659 | ||||

| Current income tax expense | $ | 17,606 | $ | 20,827 | ||||

| Deferred income tax expense | 15,277 | 18,713 | ||||||

| Total income tax expense | $ | 32,883 | $ | 39,540 | ||||

| Effective tax rate | 142 | % | 74 | % | ||||

Current income tax expense was $17.6 million for the three months ended March 31, 2023, compared to $20.8 million in the corresponding period in 2022, primarily due to a decrease in taxable income.

The deferred income tax expense for the three months ended March 31, 2023, was $15.3 million mainly the result of tax depreciation being higher than accounting depreciation and the use of tax losses to offset taxable income in Colombia. The deferred income tax expense in the comparative period of 2022 was $18.7 million as the result of tax depreciation being higher compared with accounting depreciation in Colombia.

For the three months ended March 31, 2023, the difference between the effective tax rate of 142% and the 50% Colombian tax rate was primarily due to an increase in non-deductible foreign translation adjustments, the impact of foreign taxes, non-deductible royalty in Colombia and increase in the valuation allowance. These were partially offset by other permanent differences.

For the three months ended March 31, 2022, the difference between the effective tax rate of 74% and the 35% Colombian tax rate was primarily due to an increase in the impact of foreign taxes, foreign translation adjustments, increase in the valuation allowance, other permanent differences, and non-deductible stock-based compensation.

27

Net Income (Loss) and Funds Flow from Operations (a Non-GAAP Measure)

| (Thousands of U.S. Dollars) | First Quarter 2023 Compared with Fourth Quarter 2022 | % change | First Quarter 2023 Compared with First Quarter 2022 | % change | ||||||||||

| Net income for the comparative period | $ | 33,275 | $ | 14,119 | ||||||||||

| Increase (decrease) due to: | ||||||||||||||

| Sales price | (11,867) | (49,120) | ||||||||||||

| Sales volumes | (6,580) | 18,741 | ||||||||||||

| Expenses: | ||||||||||||||

| Operating | 4,750 | (6,434) | ||||||||||||

| Transportation | (633) | (232) | ||||||||||||

| Cash G&A | (3,198) | (3,417) | ||||||||||||

| Net lease payments | 261 | 471 | ||||||||||||

| Interest, net of amortization of debt issuance costs | (1,064) | 186 | ||||||||||||

| Realized foreign exchange | (3,209) | (74) | ||||||||||||

| Cash settlements on derivative instruments | — | 8,596 | ||||||||||||

| Current taxes | (112) | 3,221 | ||||||||||||

| Interest income | 325 | 768 | ||||||||||||

Net change in funds flow from operations(1) from comparative period | (21,327) | (27,294) | ||||||||||||

| Expenses: | ||||||||||||||

| Depletion, depreciation and accretion | 60 | (10,758) | ||||||||||||

| Inventory impairment | (475) | (475) | ||||||||||||

| Deferred tax | (26,805) | 3,436 | ||||||||||||

| Amortization of debt issuance costs | (22) | 106 | ||||||||||||

| Stock-based compensation | 1,173 | 3,057 | ||||||||||||

| Derivative instruments gain or loss, net of settlements on derivative instruments | — | 12,843 | ||||||||||||

| Gain on re-purchase of Senior Notes | 1,090 | 1,090 | ||||||||||||

| Other financial instruments gain | (7) | — | ||||||||||||

| Unrealized foreign exchange | 3,599 | (5,353) | ||||||||||||

| Net lease payments | (261) | (471) | ||||||||||||

| Net change in net income | (42,975) | (23,819) | ||||||||||||

| Net loss for the current period | $ | (9,700) | (129)% | $ | (9,700) | 169% | ||||||||

(1)Funds flow from operations is a non-GAAP measure that does not have any standardized meaning prescribed under GAAP. Refer to "Financial and Operational Highlights—non-GAAP measures" for a definition and reconciliation of this measure.

28

Capital expenditures during the three months ended March 31, 2023, were $71.1 million:

| (Millions of U.S. Dollars) | Colombia | Ecuador | Total | ||||||||

| Exploration | $ | 3.2 | $ | 1.1 | $ | 4.3 | |||||

| Development: | |||||||||||

| Drilling and Completions | 45.1 | — | 45.1 | ||||||||

| Facilities | 6.3 | 0.3 | 6.6 | ||||||||

| Workovers | 5.4 | — | 5.4 | ||||||||

| Other | 9.7 | — | 9.7 | ||||||||

| $ | 69.7 | $ | 1.4 | $ | 71.1 | ||||||

During the three months ended March 31, 2023, we commenced drilling the following wells in Colombia:

| Number of wells (Gross and Net) | |||||

| Colombia | |||||

| Development | 10.0 | ||||

| Service | 4.0 | ||||

| 14.0 | |||||

We spud 10 development and four water injection wells, of which eight were in Midas Block and six in Chaza. Of the development wells spud during the quarter, six were completed, and four were in-progress as of March 31, 2023. During the three months ended March 31, 2023, we have not spud any wells in Ecuador.

Liquidity and Capital Resources

| As at | |||||||||||||||||

| (Thousands of U.S. Dollars) | March 31, 2023 | % Change | December 31, 2022 | ||||||||||||||

| Cash and Cash Equivalents | $ | 105,684 | (17) | $ | 126,873 | ||||||||||||

| 6.25% Senior Notes | $ | 271,909 | (3) | $ | 279,909 | ||||||||||||

| 7.75% Senior Notes | $ | 300,000 | — | $ | 300,000 | ||||||||||||

We believe that our capital resources, including cash on hand, cash generated from operations and available borrowings under the credit facility, will provide us with sufficient liquidity to meet our strategic objectives and planned capital program for the next 12 months, given the current oil price trends and production levels. We may also access capital markets to pursue financing or refinance our Senior Notes. In accordance with our investment policy, available cash balances are held in our primary cash management banks or may be invested in U.S. or Canadian government-backed federal, provincial or state securities or other money market instruments with high credit ratings and short-term liquidity. We believe that our current financial position provides us with the flexibility to respond to both internal growth opportunities and those available through acquisitions. We intend to pursue growth opportunities and acquisitions from time to time, which may require significant capital, be located in basins or countries beyond our current operations, involve joint ventures, or be sizable compared to our current assets and operations.

At March 31, 2023, we had a credit facility with a market lender in the global commodities industry. The credit facility has a borrowing base of up to $150 million, with $100 million readily available at March 31, 2023, and a potential option for an additional $50 million of borrowings upon mutual agreement by the lender and us. The credit facility bears interest based on a risk-free rate posted by the Federal Reserve Bank of New York plus a margin of 6.00% and a credit-adjusted spread of 0.26%. Undrawn amounts under the credit facility bear interest at 2.10% per annum, based on the amount available. The credit facility is secured by our Colombian assets and economic rights. It has a final maturity date of August 15, 2024, which may be extended to February 18, 2025, upon the satisfaction of certain conditions. The availability period for the draws under the credit facility expires on August 20, 2023. As of March 31, 2023, the credit facility remained undrawn.

29

Under the terms of the credit facility, we are required to maintain compliance with the following financial covenants:

i.Coverage ratio of at least 150%, calculated using the net present value of the consolidated future cash flows of the Company up to the final maturity date discounted at 10% over the outstanding amount on the credit facility at each reporting period. The net present value of the consolidated future cash flows of the Company is required to be based on 80% of the prevailing ICE Brent forward strip.

ii.Prepayment Life Coverage Ratio of at least 150%, calculated using the estimated aggregate value of commodities to be delivered under the commercial contract from the commencement date to the final maturity date based on 80% of the prevailing ICE Brent forward strip, adjusted for quality and transportation discounts over the outstanding amount on the credit facility including interest and all other costs payable to the lender.

iii.Liquidity ratio where the Company’s projected sources of cash exceed projected uses of cash by at least 1.15 times in each quarter period included in one year consolidated future cash flows. The future cash flows represent forecasted expected cash flows from operations, less anticipated capital expenditures and certain other adjustments. The commodity pricing assumption used in this covenant is required to be 90% of the prevailing Brent strip forward for the projected future cash flows.

At March 31, 2023, we had a $271.9 million aggregate principal amount of 6.25% Senior Notes due 2025 and a $300.0 million aggregate principal amount of 7.75% Senior Notes due 2027 outstanding.