HERSHEY CO - Annual Report: 2019 (Form 10-K)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2019

OR

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ______to_______

Commission file number 1-183

THE HERSHEY COMPANY

(Exact name of registrant as specified in its charter)

Delaware | 23-0691590 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

19 East Chocolate Avenue, Hershey, PA 17033

(Address of principal executive offices and Zip Code)

(717) 534-4200

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

Common Stock, one dollar par value | HSY | New York Stock Exchange | ||

Securities registered pursuant to Section 12(g) of the Act: Class B Common Stock, one dollar par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | x | Accelerated filer | ¨ | Non-accelerated filer | ¨ | Smaller reporting company | ☐ | |||

Emerging growth company | ☐ | |||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No x

As of June 28, 2019 (the last business day of the registrant’s most recently completed second fiscal quarter), the aggregate market value of the voting and non-voting common equity held by non-affiliates was $19,932,748,865. Class B Common Stock is not listed for public trading on any exchange or market system. However, Class B shares are convertible into shares of Common Stock at any time on a share-for-share basis. Determination of aggregate market value assumes all outstanding shares of Class B Common Stock were converted to Common Stock as of June 28, 2019. The market value indicated is calculated based on the closing price of the Common Stock on the New York Stock Exchange on June 28, 2019 ($134.03 per share).

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date.

Common Stock, one dollar par value—148,135,834 shares, as of February 14, 2020.

Class B Common Stock, one dollar par value—61,613,777 shares, as of February 14, 2020.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Company's Proxy Statement for the 2020 Annual Meeting of Stockholders are incorporated by reference into Part III of this Annual Report on Form 10-K.

THE HERSHEY COMPANY

Annual Report on Form 10-K

For the Fiscal Year Ended December 31, 2019

TABLE OF CONTENTS

PART I | ||||

PART II | ||||

PART III | ||||

PART IV | ||||

PART I

Item 1. | BUSINESS |

The Hershey Company was incorporated under the laws of the State of Delaware on October 24, 1927 as a successor to a business founded in 1894 by Milton S. Hershey. In this report, the terms “Hershey,” “Company,” “we,” “us” or “our” mean The Hershey Company and its wholly-owned subsidiaries and entities in which it has a controlling financial interest, unless the context indicates otherwise.

Hershey is a global confectionery leader known for bringing goodness to the world through chocolate, sweets, mints, gum and other great tasting snacks. We are the largest producer of quality chocolate in North America, a leading snack maker in the United States and a global leader in chocolate and non-chocolate confectionery. We market, sell and distribute our products under more than 80 brand names in approximately 85 countries worldwide.

Reportable Segments

Our organizational structure is designed to ensure continued focus on North America, coupled with an emphasis on profitable growth in our focus international markets. Our business is primarily organized around geographic regions, which enables us to build processes for repeatable success in our global markets. As a result, we have defined our operating segments on a geographic basis, as this aligns with how our Chief Operating Decision Maker (“CODM”) manages our business, including resource allocation and performance assessment. Our North America business, which generates approximately 89% of our consolidated revenue, is our only reportable segment. None of our other operating segments meet the quantitative thresholds to qualify as reportable segments; therefore, these operating segments are combined and disclosed below as International and Other.

• | North America - This segment is responsible for our traditional chocolate and non-chocolate confectionery market position, as well as our grocery and growing snacks market positions, in the United States and Canada. This includes developing and growing our business in chocolate and non-chocolate confectionery, pantry, food service and other snacking product lines. |

• | International and Other - International and Other is a combination of all other operating segments that are not individually material, including those geographic regions where we operate outside of North America. We currently have operations and manufacture product in China, Mexico, Brazil, India and Malaysia, primarily for consumers in these regions, and also distribute and sell confectionery products in export markets of Asia, Latin America, Middle East, Europe, Africa and other regions. This segment also includes our global retail operations, including Hershey's Chocolate World stores in Hershey, Pennsylvania, New York City, Las Vegas, Niagara Falls (Ontario) and Singapore, as well as operations associated with licensing the use of certain of the Company's trademarks and products to third parties around the world. |

Financial and other information regarding our reportable segments is provided in our Management’s Discussion and Analysis and Note 13 to the Consolidated Financial Statements.

Business Acquisitions

In September 2019, we completed the acquisition of ONE Brands, LLC ("ONE Brands"), previously a privately

held company that sells a line of low-sugar, high-protein nutrition bars to retailers and distributors in the United States,

with the ONE Bar as its primary product.

In October 2018, we completed the acquisition of Pirate Brands, which includes the Pirate's Booty, Smart Puffs and Original Tings brands, from B&G Foods, Inc. Pirate Brands offers baked, trans fat free and gluten free snacks and is available in a wide range of food distribution channels in the United States.

In January 2018, we completed the acquisition of all of the outstanding shares of Amplify Snack Brands, Inc. ("Amplify"), a publicly traded company based in Austin, Texas that owns several popular better-for-you snack brands such as SkinnyPop, Oatmega and Paqui. The acquisition enables us to capture more consumer snacking occasions by creating a broader portfolio of brands.

The Hershey Company | 2019 Form 10-K | Page 1

Products and Brands

Our principal product offerings include chocolate and non-chocolate confectionery products; gum and mint refreshment products; snack items such as popcorn, protein bars and cookies, spreads, bars and snack bites/mixes, and meat snacks; and pantry items, such as baking ingredients, toppings and beverages.

• | Within our North America markets, our product portfolio includes a wide variety of chocolate offerings marketed and sold under the renowned brands of Hershey’s, Reese’s and Kisses, along with other popular chocolate and non-chocolate confectionery brands such as Jolly Rancher, Almond Joy, Brookside, barkTHINS, Cadbury, Good & Plenty, Heath, Kit Kat®, Lancaster, Payday, Rolo®, Twizzlers, Whoppers and York. We also offer premium chocolate products, primarily in the United States, through the Scharffen Berger and Dagoba brands. Our gum and mint products include Ice Breakers mints and chewing gum, Breathsavers mints and Bubble Yum bubble gum. Our pantry and snack items that are principally sold in North America include ready-to-eat SkinnyPop popcorn, baked and trans fat free Pirate's Booty snacks and other better-for-you snack brands such as Oatmega, Paqui and ONE Bar, baking products, toppings and sundae syrups sold under the Hershey’s, Reese’s and Heath brands, as well as Hershey’s and Reese’s chocolate spreads, snack bites and mixes, and Krave meat snack products. |

• | Within our International and Other markets, we manufacture, market and sell many of these same brands, as well as other brands that are marketed regionally, such as Pelon Pelo Rico confectionery products in Mexico, IO-IO snack products in Brazil, and Nutrine and Maha Lacto confectionery products and Jumpin and Sofit beverage products in India. |

Principal Customers and Marketing Strategy

Our customers are mainly wholesale distributors, chain grocery stores, mass merchandisers, chain drug stores, vending companies, wholesale clubs, convenience stores, dollar stores, concessionaires and department stores. The majority of our customers, with the exception of wholesale distributors, resell our products to end-consumers in retail outlets in North America and other locations worldwide.

In 2019, approximately 30% of our consolidated net sales were made to McLane Company, Inc., one of the largest wholesale distributors in the United States to convenience stores, drug stores, wholesale clubs and mass merchandisers and the primary distributor of our products to Wal-Mart Stores, Inc.

The foundation of our marketing strategy is our strong brand equities, product innovation and the consistently superior quality of our products. We devote considerable resources to the identification, development, testing, manufacturing and marketing of new products. We utilize a variety of promotional programs directed towards our customers, as well as advertising and promotional programs for consumers of our products, to stimulate sales of certain products at various times throughout the year.

In conjunction with our sales and marketing efforts, our efficient product distribution network helps us maintain sales growth and provide superior customer service by facilitating the shipment of our products from our manufacturing plants to strategically located distribution centers. We primarily use common carriers to deliver our products from these distribution points to our customers.

Raw Materials and Pricing

Cocoa products, including cocoa liquor, cocoa butter and cocoa powder processed from cocoa beans, are the most significant raw materials we use to produce our chocolate products. These cocoa products are purchased directly from third-party suppliers, who source cocoa beans that are grown principally in Far Eastern, West African, Central and South American regions. West Africa accounts for approximately 70% of the world’s supply of cocoa beans.

Adverse weather, crop disease, political unrest and other problems in cocoa-producing countries have caused price fluctuations in the past, but have never resulted in the total loss of a particular producing country’s cocoa crop and/or exports. In the event that a significant disruption occurs in any given country, we believe cocoa from other producing countries and from current physical cocoa stocks in consuming countries would provide a significant supply buffer.

The Hershey Company | 2019 Form 10-K | Page 2

Our trading company in Switzerland performs all aspects of cocoa procurement, including price risk management, physical supply procurement and sustainable sourcing oversight. The trading company was implemented to optimize the supply chain for our cocoa requirements, with a strategic focus on gaining real time access to cocoa market intelligence. It also provides us with the ability to recruit and retain world class commodities traders and procurement professionals and enables enhanced collaboration with commodities trade groups, the global cocoa community and sustainable sourcing resources.

We also use substantial quantities of sugar, Class II and IV dairy products, peanuts, almonds and energy in our production process. Most of these inputs for our domestic and Canadian operations are purchased from suppliers in the United States. For our international operations, inputs not locally available may be imported from other countries.

We change prices and weights of our products when necessary to accommodate changes in input costs, the competitive environment and profit objectives, while at the same time maintaining consumer value. Price increases and weight changes help to offset increases in our input costs, including raw and packaging materials, fuel, utilities, transportation costs and employee benefits. When we implement price increases, there is usually a time lag between the effective date of the list price increases and the impact of the price increases on net sales, in part because we typically honor previous commitments to planned consumer and customer promotions and merchandising events subsequent to the effective date of the price increases. In addition, promotional allowances may be increased subsequent to the effective date, delaying or partially offsetting the impact of price increases on net sales.

Competition

Many of our confectionery brands enjoy wide consumer acceptance and are among the leading brands sold in the marketplace in North America and certain markets in Latin America. We sell our brands in highly competitive markets with many other global multinational, national, regional and local firms. Some of our competitors are large companies with significant resources and substantial international operations. Competition in our product categories is based on product innovation, product quality, price, brand recognition and loyalty, effectiveness of marketing and promotional activity, the ability to identify and satisfy consumer preferences, as well as convenience and service. We have also experienced increased competition from other snack items, which we are focused on expanding the boundaries of our core confection brands to capture new snacking occasions.

Working Capital, Seasonality and Backlog

Our sales are typically higher during the third and fourth quarters of the year, representing seasonal and holiday-related sales patterns. We manufacture primarily for stock and typically fill customer orders within a few days of receipt. Therefore, the backlog of any unfilled orders is not material to our total annual sales. Additional information relating to our cash flows from operations and working capital practices is provided in our Management’s Discussion and Analysis.

Trademarks, Service Marks and License Agreements

We own various registered and unregistered trademarks and service marks. The trademarks covering our key product brands are of material importance to our business. We follow a practice of seeking trademark protection in the United States and other key international markets where our products are sold. We also grant trademark licenses to third parties to produce and sell pantry items, flavored milks and various other products primarily under the Hershey’s and Reese’s brand names.

The Hershey Company | 2019 Form 10-K | Page 3

Furthermore, we have rights under license agreements with several companies to manufacture and/or sell and distribute certain products. Our rights under these agreements are extendible on a long-term basis at our option. Our most significant licensing agreements are as follows:

Company | Brand | Location | Requirements | ||||

Kraft Foods Ireland Intellectual Property Limited/Cadbury UK Limited | York Peter Paul Almond Joy Peter Paul Mounds | Worldwide | None | ||||

Cadbury UK Limited | Cadbury Caramello | United States | Minimum sales requirement exceeded in 2019 | ||||

Société des Produits Nestlé SA | Kit Kat® Rolo® | United States | Minimum unit volume sales exceeded in 2019 | ||||

Iconic IP Interests, LLC | Good & Plenty Heath Jolly Rancher Milk Duds Payday Whoppers | Worldwide | None | ||||

Research and Development

We engage in a variety of research and development activities in a number of countries, including the United States, Mexico, Brazil, India and China. We develop new products, improve the quality of existing products, improve and modernize production processes, and develop and implement new technologies to enhance the quality and value of both current and proposed product lines. Information concerning our research and development expense is contained in Note 1 to the Consolidated Financial Statements.

Food Quality and Safety Regulation

The manufacture and sale of consumer food products is highly regulated. In the United States, our activities are subject to regulation by various government agencies, including the Food and Drug Administration, the Department of Agriculture, the Federal Trade Commission, the Department of Commerce and the Environmental Protection Agency, as well as various state and local agencies. Similar agencies also regulate our businesses outside of the United States.

We believe our Product Excellence Program provides us with an effective product quality and safety program. This program is integral to our global supply chain platform and is intended to ensure that all products we purchase, manufacture and distribute are safe, are of high quality and comply with applicable laws and regulations.

Through our Product Excellence Program, we evaluate our supply chain including ingredients, packaging, processes, products, distribution and the environment to determine where product quality and safety controls are necessary. We identify risks and establish controls intended to ensure product quality and safety. Various government agencies and third-party firms as well as our quality assurance staff conduct audits of all facilities that manufacture our products to assure effectiveness and compliance with our program and applicable laws and regulations.

Environmental Considerations

Beyond ordinary course operating and capital expenditures we make to comply with environmental laws and regulations, we have made a number of commitments to protect and reduce our impact on the environment in recent years, including efforts to protect forests and forested habitats and reduce emissions across our supply chain. The annual operating and capital expenditures associated with these ordinary course payments and additional commitments are not material with respect to our results of operations, capital expenditures or competitive position.

The Hershey Company | 2019 Form 10-K | Page 4

Employees

As of December 31, 2019, the Company employed approximately 14,520 full-time and 1,620 part-time employees worldwide. Collective bargaining agreements covered approximately 5,500 employees, or approximately 34% of the Company’s employees worldwide. During 2020, agreements will be negotiated for certain employees at three facilities outside of the United States and one United States facility, comprising approximately 74% of total employees under collective bargaining agreements. We believe that our employee relations are generally good.

Financial Information by Geographic Area

Our principal operations and markets are located in the United States. The percentage of total consolidated net sales for our businesses outside of the United States was 15.8% for 2019, 16.1% for 2018 and 16.7% for 2017. The percentage of total long-lived assets outside of the United States was 20.2% as of December 31, 2019 and 21.7% as of December 31, 2018.

Sustainability

The Hershey Company’s commitment to sustainability started with our founder’s belief in responsible citizenship. He was a purpose-driven leader who believed we could use chocolate to create goodness in the world. This belief resulted in strong investment in local communities and the establishment of the Milton Hershey School for disadvantaged kids. We continue that legacy today through our sustainability strategy “The Shared Goodness Promise” by operating the business with sustainable practices, sourcing ingredients responsibly, protecting our environment, making a difference in our communities and helping kids globally reach their full potential. To learn more about our sustainability goals, progress and initiatives, you can access our full Sustainability Report at https://www.thehersheycompany.com/en_us/sustainability.html.

Available Information

The Company's website address is www.thehersheycompany.com. We file or furnish annual, quarterly and current reports, proxy statements and other information with the United States Securities and Exchange Commission (“SEC”). You may obtain a copy of any of these reports, free of charge, from the Investors section of our website as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. The SEC maintains an Internet site that also contains these reports at: www.sec.gov. In addition, copies of the Company's annual report will be made available, free of charge, on written request to the Company.

We have a Code of Conduct that applies to our Board of Directors (“Board”) and all Company officers and employees, including, without limitation, our Chief Executive Officer and “senior financial officers” (including the Chief Financial Officer, Chief Accounting Officer and persons performing similar functions). You can obtain a copy of our Code of Conduct, as well as our Corporate Governance Guidelines and charters for each of the Board’s standing committees, from the Investors section of our website. If we change or waive any portion of the Code of Conduct that applies to any of our directors, executive officers or senior financial officers, we will post that information on our website.

The Hershey Company | 2019 Form 10-K | Page 5

Item 1A. | RISK FACTORS |

Cautionary Note Regarding Forward-Looking Statements

This Annual Report on Form 10-K, including the exhibits hereto and the information incorporated by reference herein, contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, which are subject to risks and uncertainties. Other than statements of historical fact, information regarding activities, events and developments that we expect or anticipate will or may occur in the future, including, but not limited to, information relating to our future growth and profitability targets and strategies designed to increase total shareholder value, are forward-looking statements based on management’s estimates, assumptions and projections. Forward-looking statements also include, but are not limited to, statements regarding our future economic and financial condition and results of operations, the plans and objectives of management and our assumptions regarding our performance and such plans and objectives. Many of the forward-looking statements contained in this document may be identified by the use of words such as “intend,” “believe,” “expect,” “anticipate,” “should,” “planned,” “projected,” “estimated” and “potential,” among others. Forward-looking statements contained in this Annual Report on Form 10-K are predictions only and actual results could differ materially from management’s expectations due to a variety of factors, including those described below. All forward-looking statements attributable to us or persons working on our behalf are expressly qualified in their entirety by such risk factors. The forward-looking statements that we make in this Annual Report on Form 10-K are based on management’s current views and assumptions regarding future events and speak only as of their dates. We assume no obligation to update developments of these risk factors or to announce publicly any revisions to any of the forward-looking statements that we make, or to make corrections to reflect future events or developments, except as required by the federal securities laws.

Our Company’s reputation or brand image might be impacted as a result of issues or concerns relating to the quality and safety of our products, ingredients or packaging, human and workplace rights, and other environmental, social or governance matters, which in turn could negatively impact our operating results.

In order to sell our iconic, branded products, we need to maintain a good reputation with our customers, consumers, suppliers, vendors and employees, among others. Issues related to the quality and safety of our products, ingredients or packaging could jeopardize our Company’s image and reputation. Negative publicity related to these types of concerns, or related to product contamination or product tampering, whether valid or not, could decrease demand for our products or cause production and delivery disruptions. We may need to recall products if any of our products become unfit for consumption, and we could potentially be subject to litigation or government actions, which could result in payments of fines or damages. In addition, negative publicity related to our environmental, social or governance practices could also impact our reputation with customers, consumers, suppliers and vendors. Costs associated with these potential actions, as well as the potential impact on our ability to sell our products, could negatively affect our operating results.

The Hershey Company | 2019 Form 10-K | Page 6

Increases in raw material and energy costs along with the availability of adequate supplies of raw materials could affect future financial results.

We use many different commodities for our business, including cocoa products, sugar, corn products, dairy products, peanuts, almonds, natural gas and diesel fuel.

Commodities are subject to price volatility and changes in supply caused by numerous factors, including:

• | Commodity market fluctuations; |

• | Currency exchanges rates; |

• | Imbalances between supply and demand; |

• | The effect of weather on crop yield and quality; |

• | Speculative influences; |

• | Trade agreements among producing and consuming nations; |

• | Supplier compliance with commitments; |

• | Import/export requirements for raw materials and finished goods; |

• | Political unrest in producing countries; and |

• | Changes in governmental agricultural programs and energy policies. |

Although we use forward contracts and commodity futures and options contracts where possible to hedge commodity prices, commodity price increases ultimately result in corresponding increases in our raw material and energy costs. If we are unable to offset cost increases for major raw materials and energy, there could be a negative impact on our financial condition and results of operations.

Price increases may not be sufficient to offset cost increases and maintain profitability or may result in sales volume declines associated with pricing elasticity.

We may be able to pass some or all raw material, energy and other input cost increases to customers by increasing the selling prices of our products or decreasing the size of our products; however, higher product prices or decreased product sizes may also result in a reduction in sales volume and/or consumption. If we are not able to increase our selling prices or reduce product sizes sufficiently, or in a timely manner, to offset increased raw material, energy or other input costs, including packaging, freight, direct labor, overhead and employee benefits, or if our sales volume decreases significantly, there could be a negative impact on our financial condition and results of operations.

Market demand for new and existing products could decline.

We operate in highly competitive markets and rely on continued demand for our products. To generate revenues and profits, we must sell products that appeal to our customers and to consumers. Our continued success is impacted by many factors, including the following:

• | Effective retail execution; |

• | Appropriate advertising campaigns and marketing programs; |

• | Our ability to secure adequate shelf space at retail locations; |

• | Our ability to drive sustainable innovation and maintain a strong pipeline of new products in the confectionery and broader snacking categories; |

• | Changes in product category consumption; |

• | Our response to consumer demographics and trends, including but not limited to, trends relating to store trips and the impact of the growing digital commerce channel; and |

• | Consumer health concerns, including obesity and the consumption of certain ingredients. |

There continues to be competitive product and pricing pressures in the markets where we operate, as well as challenges in maintaining profit margins. We must maintain mutually beneficial relationships with our key customers, including retailers and distributors, to compete effectively. Our largest customer, McLane Company, Inc., accounted for approximately 30% of our total net sales in 2019. McLane Company, Inc. is one of the largest wholesale distributors in the United States to convenience stores, drug stores, wholesale clubs and mass merchandisers, including Wal-Mart Stores, Inc.

The Hershey Company | 2019 Form 10-K | Page 7

Increased marketplace competition could hurt our business.

The global confectionery packaged goods industry is intensely competitive and consolidation in this industry continues. Some of our competitors are large companies that have significant resources and substantial international operations. We continue to experience increased levels of in-store activity for other snack items, which has pressured confectionery category growth. In order to protect our existing market share or capture increased market share in this highly competitive retail environment, we may be required to increase expenditures for promotions and advertising, and must continue to introduce and establish new products. Due to inherent risks in the marketplace associated with advertising and new product introductions, including uncertainties about trade and consumer acceptance, increased expenditures may not prove successful in maintaining or enhancing our market share and could result in lower sales and profits. In addition, we may incur increased credit and other business risks because we operate in a highly competitive retail environment.

Disruption to our manufacturing operations or supply chain could impair our ability to produce or deliver finished products, resulting in a negative impact on our operating results.

Approximately 70% of our manufacturing capacity is located in the United States. Disruption to our global manufacturing operations or our supply chain could result from, among other factors, the following:

• | Natural disaster; |

• | Pandemic outbreak of disease; |

• | Weather; |

• | Fire or explosion; |

• | Terrorism or other acts of violence; |

• | Labor strikes or other labor activities; |

• | Unavailability of raw or packaging materials; |

• | Operational and/or financial instability of key suppliers, and other vendors or service providers; and |

• | Suboptimal production planning which could impact our ability to cost-effectively meet product demand. |

We believe that we take adequate precautions to mitigate the impact of possible disruptions. We have strategies and plans in place to manage disruptive events if they were to occur, including our global supply chain strategies and our principle-based global labor relations strategy. If we are unable, or find that it is not financially feasible, to effectively plan for or mitigate the potential impacts of such disruptive events on our manufacturing operations or supply chain, our financial condition and results of operations could be negatively impacted if such events were to occur.

Our financial results may be adversely impacted by the failure to successfully execute or integrate acquisitions, divestitures and joint ventures.

From time to time, we may evaluate potential acquisitions, divestitures or joint ventures that align with our strategic objectives. The success of such activity depends, in part, upon our ability to identify suitable buyers, sellers or business partners; perform effective assessments prior to contract execution; negotiate contract terms; and, if applicable, obtain government approval. These activities may present certain financial, managerial, staffing and talent, and operational risks, including diversion of management’s attention from existing core businesses; difficulties integrating or separating businesses from existing operations; and challenges presented by acquisitions or joint ventures which may not achieve sales levels and profitability that justify the investments made. If the acquisitions, divestitures or joint ventures are not successfully implemented or completed, there could be a negative impact on our financial condition, results of operations and cash flows.

We completed the acquisitions of ONE Brands, LLC in September 2019, Pirate Brands in October 2018 and Amplify Snack Brands, Inc. in January 2018, respectively. While we believe significant operating synergies can be obtained in connection with these acquisitions, achievement of these synergies will be driven by our ability to successfully leverage Hershey's resources, expertise, capability-building, distribution locations and customer base. In addition, these acquisitions are important steps in our journey to expand our breadth in snacking, as they should enable us to bring scale and category management capabilities to a key sub-segment of the warehouse snack aisle. If we are unable to successfully couple Hershey’s scale and expertise in brand building with ONE Brands, Pirate Brands and Amplify's existing operations, it may impact our ability to expand our snacking footprint at our desired pace.

The Hershey Company | 2019 Form 10-K | Page 8

Changes in governmental laws and regulations could increase our costs and liabilities or impact demand for our products.

Changes in laws and regulations and the manner in which they are interpreted or applied may alter our business environment. These negative impacts could result from changes in food and drug laws, laws related to advertising and marketing practices, accounting standards, taxation requirements, competition laws, employment laws, import/export requirements and environmental laws, among others. It is possible that we could become subject to additional liabilities in the future resulting from changes in laws and regulations that could result in an adverse effect on our financial condition and results of operations.

Political, economic and/or financial market conditions could negatively impact our financial results.

Our operations are impacted by consumer spending levels and impulse purchases which are affected by general macroeconomic conditions, consumer confidence, employment levels, the availability of consumer credit and interest rates on that credit, consumer debt levels, energy costs and other factors. Volatility in food and energy costs, sustained global recessions, broad political instability, rising unemployment, pandemic outbreak of disease, weather, natural and other disasters and declines in personal spending could adversely impact our revenues, profitability and financial condition.

Changes in financial market conditions may make it difficult to access credit markets on commercially acceptable terms, which may reduce liquidity or increase borrowing costs for our Company, our customers and our suppliers. A significant reduction in liquidity could increase counterparty risk associated with certain suppliers and service providers, resulting in disruption to our supply chain and/or higher costs, and could impact our customers, resulting in a reduction in our revenue, or a possible increase in bad debt expense.

Our international operations may not achieve projected growth objectives, which could adversely impact our overall business and results of operations.

In 2019, 2018 and 2017, respectively, we derived approximately 16%, 16% and 17% of our net sales from customers located outside of the United States. Additionally, approximately 20% of our total long-lived assets were located outside of the United States as of December 31, 2019. As part of our strategy, we have made investments outside of the United States, particularly in Canada, China, Malaysia, Mexico, Brazil and India. As a result, we are subject to risks and uncertainties relating to international sales and operations, including:

• | Unforeseen global economic and environmental changes resulting in business interruption, supply constraints, inflation, deflation or decreased demand; |

• | Inability to establish, develop and achieve market acceptance of our global brands in international markets; |

• | Difficulties and costs associated with compliance and enforcement of remedies under a wide variety of complex laws, treaties and regulations; |

• | Unexpected changes in regulatory environments; |

• | Political and economic instability, including the possibility of civil unrest, terrorism, mass violence or armed conflict; |

• | Nationalization of our properties by foreign governments; |

• | Tax rates that may exceed those in the United States and earnings that may be subject to withholding requirements and incremental taxes upon repatriation; |

• | Potentially negative consequences from changes in tax laws; |

• | The imposition of tariffs, quotas, trade barriers, other trade protection measures and import or export licensing requirements; |

• | Increased costs, disruptions in shipping or reduced availability of freight transportation; |

• | The impact of currency exchange rate fluctuations between the U.S. dollar and foreign currencies; |

• | Failure to gain sufficient profitable scale in certain international markets resulting in an inability to cover manufacturing fixed costs or resulting in losses from impairment or sale of assets; and |

• | Failure to recruit, retain and build a talented and engaged global workforce. |

If we are not able to achieve our projected international growth objectives and mitigate the numerous risks and uncertainties associated with our international operations, there could be a negative impact on our financial condition and results of operations.

The Hershey Company | 2019 Form 10-K | Page 9

Disruptions, failures or security breaches of our information technology infrastructure could have a negative impact on our operations.

Information technology is critically important to our business operations. We use information technology to manage all business processes including manufacturing, financial, logistics, sales, marketing and administrative functions. These processes collect, interpret and distribute business data and communicate internally and externally with employees, suppliers, customers and others.

We are regularly the target of attempted cyber and other security threats. Therefore, we continuously monitor and update our information technology networks and infrastructure to prevent, detect, address and mitigate the risk of unauthorized access, misuse, computer viruses and other events that could have a security impact. We invest in industry standard security technology to protect the Company’s data and business processes against risk of data security breach and cyber attack. Our data security management program includes identity, trust, vulnerability and threat management business processes as well as adoption of standard data protection policies. We measure our data security effectiveness through industry accepted methods and remediate significant findings. Additionally, we certify our major technology suppliers and any outsourced services through accepted security certification standards. We maintain and routinely test backup systems and disaster recovery, along with external network security penetration testing by an independent third party as part of our business continuity preparedness. We also have processes in place to prevent disruptions resulting from the implementation of new software and systems of the latest technology.

While we have been subject to cyber attacks and other security breaches, these incidents did not have a significant impact on our business operations. We believe our security technology tools and processes provide adequate measures of protection against security breaches and in reducing cybersecurity risks. Nevertheless, despite continued vigilance in these areas, disruptions in or failures of information technology systems are possible and could have a negative impact on our operations or business reputation. Failure of our systems, including failures due to cyber attacks that would prevent the ability of systems to function as intended, could cause transaction errors, loss of customers and sales, and could have negative consequences to our Company, our employees and those with whom we do business. This in turn could have a negative impact on our financial condition and results or operations. In addition, the cost to remediate any damages to our information technology systems suffered as a result of a cyber attack could be significant.

We might not be able to hire, engage and retain the talented global workforce we need to drive our growth strategies.

Our future success depends upon our ability to identify, hire, develop, engage and retain talented personnel across the globe. Competition for global talent is intense, and we might not be able to identify and hire the personnel we need to continue to evolve and grow our business. In particular, if we are unable to hire the right individuals to fill new or existing senior management positions as vacancies arise, our business performance may be impacted.

Activities related to identifying, recruiting, hiring and integrating qualified individuals require significant time and attention. We may also need to invest significant amounts of cash and equity to attract talented new employees, and we may never realize returns on these investments.

In addition to hiring new employees, we must continue to focus on retaining and engaging the talented individuals we need to sustain our core business and lead our developing businesses into new markets, channels and categories. This may require significant investments in training, coaching and other career development and retention activities. If we are not able to effectively retain and grow our talent, our ability to achieve our strategic objectives will be adversely affected, which may impact our financial condition and results of operations.

The Hershey Company | 2019 Form 10-K | Page 10

We may not fully realize the expected costs savings and/or operating efficiencies associated with our strategic initiatives or restructuring programs, which may have an adverse impact on our business.

We depend on our ability to evolve and grow, and as changes in our business environment occur, we may adjust our business plans by introducing new strategic initiatives or restructuring programs to meet these changes. Recently introduced strategic initiatives include our efforts to continue to expand our presence in digital commerce, to transform our manufacturing, commercial and corporate operations through digital technologies and to enhance our data analytics capabilities to develop new commercial insights. If we are not able to capture our share of the expanding digital commerce market, if we do not adequately leverage technology to improve operating efficiencies or if we are unable to develop the data analytics capabilities needed to generate actionable commercial insights, our business performance may be impacted, which may negatively impact our financial condition and results of operations.

Additionally, from time to time we implement business realignment activities to support key strategic initiatives designed to maintain long-term sustainable growth, such as the Margin for Growth Program we commenced in the first quarter of 2017. These programs are intended to increase our operating effectiveness and efficiency, to reduce our costs and/or to generate savings that can be reinvested in other areas of our business. We cannot guarantee that we will be able to successfully implement these strategic initiatives and restructuring programs, that we will achieve or sustain the intended benefits under these programs, or that the benefits, even if achieved, will be adequate to meet our long-term growth and profitability expectations, which could in turn adversely affect our business.

Complications with the design or implementation of our new enterprise resource planning system could adversely impact our business and operations.

We rely extensively on information systems and technology to manage our business and summarize operating results. We are in the process of a multi-year implementation of a new global enterprise resource planning (“ERP”) system. This ERP system will replace our existing operating and financial systems. The ERP system is designed to accurately maintain the Company’s financial records, enhance operational functionality and provide timely information to the Company’s management team related to the operation of the business. The ERP system implementation process has required, and will continue to require, the investment of significant personnel and financial resources. We may not be able to successfully implement the ERP system without experiencing delays, increased costs and other difficulties. If we are unable to successfully design and implement the new ERP system as planned, our financial positions, results of operations and cash flows could be negatively impacted. Additionally, if we do not effectively implement the ERP system as planned or the ERP system does not operate as intended, the effectiveness of our internal control over financial reporting could be adversely affected or our ability to assess those controls adequately could be delayed.

Item 1B. | UNRESOLVED STAFF COMMENTS |

None.

The Hershey Company | 2019 Form 10-K | Page 11

Item 2. | PROPERTIES |

Our principal properties include the following:

Country | Location | Type | Status (Own/Lease) | |||

United States | Hershey, Pennsylvania (2 principal plants) | Manufacturing—confectionery products and pantry items | Own | |||

Lancaster, Pennsylvania | Manufacturing—confectionery products | Own | ||||

Hazleton, Pennsylvania | Manufacturing—confectionery products | Own | ||||

Robinson, Illinois | Manufacturing—confectionery products and pantry items | Own | ||||

Stuarts Draft, Virginia | Manufacturing—confectionery products and pantry items | Own | ||||

Edwardsville, Illinois | Distribution | Own | ||||

Palmyra, Pennsylvania | Distribution | Own | ||||

Ogden, Utah | Distribution | Own | ||||

Kennesaw, Georgia | Distribution | Lease | ||||

New York, New York | Retail | Lease | ||||

Canada | Brantford, Ontario | Distribution | Lease | |||

Mexico | Monterrey, Mexico | Manufacturing—confectionery products | Own | |||

El Salto, Mexico | Manufacturing—confectionery products and pantry items | Own | ||||

Malaysia | Johor, Malaysia | Manufacturing—confectionery products | Own | |||

In addition to the locations indicated above, we also own or lease several other properties and buildings worldwide which we use for manufacturing, sales, distribution and administrative functions. Our facilities are well maintained and generally have adequate capacity to accommodate seasonal demands, changing product mixes and certain additional growth. We regularly improve our facilities to incorporate the latest technologies. The largest facilities are located in Hershey, Lancaster and Hazleton, Pennsylvania; Monterrey and El Salto, Mexico; and Stuarts Draft, Virginia. The U.S., Canada and Mexico facilities in the table above primarily support our North America segment, while the Malaysia facility primarily serve our International and Other segment. As discussed in Note 13 to the Consolidated Financial Statements, we do not manage our assets on a segment basis given the integration of certain manufacturing, warehousing, distribution and other activities in support of our global operations.

Item 3. | LEGAL PROCEEDINGS |

The Company is subject to certain legal proceedings and claims arising out of the ordinary course of our business, which cover a wide range of matters including trade regulation, product liability, advertising, contracts, environmental issues, patent and trademark matters, labor and employment matters and tax. While it is not feasible to predict or determine the outcome of such proceedings and claims with certainty, in our opinion these matters, both individually and in the aggregate, are not expected to have a material effect on our financial condition, results of operations or cash flows.

Item 4. | MINE SAFETY DISCLOSURES |

Not applicable.

The Hershey Company | 2019 Form 10-K | Page 12

SUPPLEMENTAL ITEM. INFORMATION ABOUT OUR EXECUTIVE OFFICERS

The executive officers of the Company, their positions and, as of February 14, 2020, their ages are set forth below.

Name | Age | Positions Held During the Last Five Years | ||

Damien Atkins (1) | 49 | Senior Vice President, General Counsel and Secretary (August 2018) | ||

Michele G. Buck | 58 | Chairman of the Board, President and Chief Executive Officer (October 2019); President and Chief Executive Officer (March 2017); Executive Vice President, Chief Operating Officer (June 2016); President, North America (May 2013) | ||

Terence L. O’Day (2) | 70 | Senior Vice President, Chief Technology and Data Officer (June 2019); Senior Vice President, Chief Product Supply and Technology Officer (March 2017); Senior Vice President, Chief Supply Chain Officer (May 2013) | ||

Charles R. Raup | 52 | President, U.S. (January 2020); Vice President, U.S. CMG (June 2018); Vice President and General Manager, Chocolate (August 2017); Vice President and General Manager, Mexico (October 2015); Vice President, Emerging Brands (November 2014) | ||

Jason Reiman | 48 | Senior Vice President, Chief Supply Chain Officer (June 2019); Vice President, Supply Chain Operations (August 2018); Vice President, US Supply Chain Operations (July 2017); Vice President, International Operations (May 2017); Vice President, AEMA Supply Chain Operations (October 2015); President, Global Logistics Excellence (January 2013) | ||

Kristen J. Riggs | 41 | Senior Vice President, Chief Growth Officer (January 2020); Vice President, Innovation and Strategic Growth Platforms (September 2019); Vice President, Commercial Planning (June 2018); Vice President, Brand Commercialization (July 2017); Senior Director, Reese’s (October 2015); Team Lead, Sam’s Club (September 2013) | ||

Christopher M. Scalia | 44 | Senior Vice President, Chief Human Resources Officer (January 2020); Vice President, Global Human Resources (March 2018); Vice President, Talent, HR Operations and Analytics (December 2014) | ||

Steven E. Voskuil (3) | 51 | Senior Vice President, Chief Financial Officer and Chief Accounting Officer (November 2019); Senior Vice President, Chief Financial Officer (May 2019) | ||

There are no family relationships among any of the above-named officers of our Company.

(1) | Mr. Atkins was elected Senior Vice President, General Counsel and Secretary effective August 13, 2018. Prior to joining our Company he was General Counsel and Corporate Secretary at Panasonic Corporation of North America, Inc. (May 2015) and Senior Vice President, Deputy General Counsel (Corporate) and Chief Compliance Officer at AOL, Inc. (July 2010). |

(2) | On December 18, 2019, the Company announced the planned retirement of Mr. O'Day, to be effective March 31, 2020. |

(3) | Mr. Voskuil was elected Senior Vice President, Chief Financial Officer effective May 13, 2019. Prior to joining our Company he was Senior Vice President and Chief Financial Officer at Avanos Medical, Inc. (November 2014). |

Our Executive Officers are generally elected each year at the organization meeting of the Board in May.

The Hershey Company | 2019 Form 10-K | Page 13

PART II

Item 5. | MARKET FOR THE REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Our Common Stock is listed and traded principally on the New York Stock Exchange under the ticker symbol “HSY.” The Class B Common Stock (“Class B Stock”) is not publicly traded.

The closing price of our Common Stock on December 31, 2019, was $146.98. There were 25,773 stockholders of record of our Common Stock and 6 stockholders of record of our Class B Stock as of December 31, 2019.

We paid $610.3 million in cash dividends on our Common Stock and Class B Stock in 2019 and $562.5 million in 2018. The annual dividend rate on our Common Stock in 2019 was $2.990 per share.

Information regarding dividends paid and the quarterly high and low market prices for our Common Stock and dividends paid for our Class B Stock for the two most recent fiscal years is disclosed in Note 19 to the Consolidated Financial Statements.

On January 28, 2020, our Board declared a quarterly dividend of $0.773 per share of Common Stock payable on March 16, 2020, to stockholders of record as of February 21, 2020. It is the Company’s 361st consecutive quarterly Common Stock dividend. A quarterly dividend of $0.702 per share of Class B Stock also was declared.

Unregistered Sales of Equity Securities and Use of Proceeds

None.

Issuer Purchases of Equity Securities

In October 2017, our Board approved a $100 million share repurchase authorization. This program was completed in the first quarter of 2019. In July 2018, our Board of Directors approved an additional $500 million share repurchase authorization, to commence after the existing 2017 authorization was completed. As of December 31, 2019, approximately $410 million remained available for repurchases of our Common Stock under this program. The share repurchase program does not have an expiration date.

In August 2017, the Company entered into a Stock Purchase Agreement with Hershey Trust Company, as trustee for the Milton Hershey School Trust (the “Trust”), pursuant to which the Company agreed to purchase 1,500,000 shares of the Company’s common stock from the Trust at a price equal to $106.01 per share, for a total purchase price of $159 million.

In November 2018, the Company entered into a Stock Purchase Agreement with Hershey Trust Company, as trustee for the Trust, pursuant to which the Company agreed to purchase 450,000 shares of the Company’s common stock from the Trust at a price equal to $106.30 per share, for a total purchase price of $47.8 million.

The Hershey Company | 2019 Form 10-K | Page 14

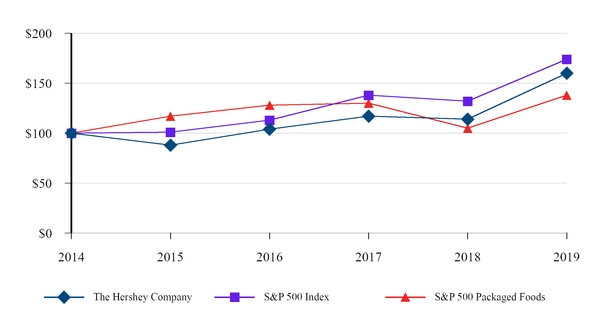

Stockholder Return Performance Graph

The following graph compares our cumulative total stockholder return (Common Stock price appreciation plus dividends, on a reinvested basis) over the last five fiscal years with the Standard & Poor’s 500 Index and the Standard & Poor’s Packaged Foods Index.

Comparison of 5 Year Cumulative Total Return*

Among The Hershey Company, the S&P 500 Index,

and the S&P Packaged Foods Index

*$100 invested on December 31, 2014 in stock or index, including reinvestment of dividends.

December 31, | ||||||||||||||||||||||||

Company/Index | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | ||||||||||||||||||

The Hershey Company | $ | 100 | $ | 88 | $ | 104 | $ | 117 | $ | 114 | $ | 160 | ||||||||||||

S&P 500 Index | $ | 100 | $ | 101 | $ | 113 | $ | 138 | $ | 132 | $ | 174 | ||||||||||||

S&P 500 Packaged Foods Index | $ | 100 | $ | 117 | $ | 128 | $ | 130 | $ | 105 | $ | 138 | ||||||||||||

The stock price performance included in this graph is not necessarily indicative of future stock price performance.

The Hershey Company | 2019 Form 10-K | Page 15

Item 6. | SELECTED FINANCIAL DATA |

FIVE-YEAR CONSOLIDATED FINANCIAL SUMMARY

(All dollar and share amounts in thousands except market price and per share statistics)

2019 | 2018 | 2017 | 2016 | 2015 | ||||||||||||

Summary of Operations | ||||||||||||||||

Net Sales | $ | 7,986,252 | 7,791,069 | 7,515,426 | 7,440,181 | 7,386,626 | ||||||||||

Cost of Sales | $ | 4,363,774 | 4,215,744 | 4,060,050 | 4,270,642 | 4,000,071 | ||||||||||

Selling, Marketing and Administrative | $ | 1,905,929 | 1,874,829 | 1,885,492 | 1,891,305 | 1,945,361 | ||||||||||

Goodwill, Long-Lived & Intangible Asset Impairment Charges | $ | 112,485 | 57,729 | 208,712 | 4,204 | 280,802 | ||||||||||

Business Realignment Costs | $ | 8,112 | 19,103 | 47,763 | 18,857 | 84,628 | ||||||||||

Interest Expense, Net | $ | 144,125 | 138,837 | 98,282 | 90,143 | 105,773 | ||||||||||

Provision for Income Taxes | $ | 234,032 | 239,010 | 354,131 | 379,437 | 388,896 | ||||||||||

Net Income Attributable to The Hershey Company | $ | 1,149,692 | 1,177,562 | 782,981 | 720,044 | 512,951 | ||||||||||

Net Income Per Share: | ||||||||||||||||

—Basic—Common Stock | $ | 5.64 | 5.76 | 3.79 | 3.45 | 2.40 | ||||||||||

—Diluted—Common Stock | $ | 5.46 | 5.58 | 3.66 | 3.34 | 2.32 | ||||||||||

—Basic—Class B Stock | $ | 5.12 | 5.24 | 3.44 | 3.15 | 2.19 | ||||||||||

—Diluted—Class B Stock | $ | 5.10 | 5.22 | 3.44 | 3.14 | 2.19 | ||||||||||

Weighted-Average Shares Outstanding: | ||||||||||||||||

—Basic—Common Stock | 148,841 | 149,379 | 151,625 | 153,519 | 158,471 | |||||||||||

—Basic—Class B Stock | 60,614 | 60,614 | 60,620 | 60,620 | 60,620 | |||||||||||

—Diluted—Common Stock | 210,702 | 210,989 | 213,742 | 215,304 | 220,651 | |||||||||||

Dividends Paid on Common Stock | $ | 445,618 | 412,491 | 387,466 | 369.292 | 352,953 | ||||||||||

Per Share | $ | 2.990 | 2.756 | 2.548 | 2.402 | 2.236 | ||||||||||

Dividends Paid on Class B Stock | $ | 164,627 | 151,789 | 140,394 | 132,394 | 123,179 | ||||||||||

Per Share | $ | 2.716 | 2.504 | 2.316 | 2.184 | 2.032 | ||||||||||

Depreciation | $ | 218,096 | 231,012 | 211,592 | 231,735 | 197,054 | ||||||||||

Amortization | $ | 73,448 | 64,132 | 50,261 | 70,102 | 47,874 | ||||||||||

Advertising | $ | 513,302 | 479,908 | 541,293 | 521,479 | 561,644 | ||||||||||

Year-End Position and Statistics | ||||||||||||||||

Capital Additions (including software) | $ | 318,192 | 328,601 | 257,675 | 269,476 | 356,810 | ||||||||||

Total Assets | $ | 8,140,395 | 7,703,020 | 5,553,726 | 5,524,333 | 5,344,371 | ||||||||||

Short-term Debt and Current Portion of Long-term Debt | $ | 735,672 | 1,203,316 | 859,457 | 632,714 | 863,436 | ||||||||||

Long-term Portion of Debt | $ | 3,530,813 | 3,254,280 | 2,061,023 | 2,347,455 | 1,557,091 | ||||||||||

Stockholders’ Equity | $ | 1,744,994 | 1,407,266 | 931,565 | 827,687 | 1,047,462 | ||||||||||

Full-time Employees | 14,520 | 14,930 | 15,360 | 16,300 | 19,060 | |||||||||||

Stockholders’ Data | ||||||||||||||||

Outstanding Shares of Common Stock and Class B Stock at Year-end | 208,829 | 209,729 | 210,861 | 212,260 | 216,777 | |||||||||||

Market Price of Common Stock at Year-end | $ | 146.98 | 107.18 | 113.51 | 103.43 | 89.27 | ||||||||||

Price Range During Year (high) | $ | 161.40 | 114.06 | 115.96 | 113.89 | 110.78 | ||||||||||

Price Range During Year (low) | $ | 104.30 | 89.54 | 102.87 | 83.32 | 83.58 | ||||||||||

The Hershey Company | 2019 Form 10-K | Page 16

Item 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

This Management's Discussion and Analysis (“MD&A”) is intended to provide an understanding of Hershey's financial condition, results of operations and cash flows by focusing on changes in certain key measures from year to year. The MD&A should be read in conjunction with our Consolidated Financial Statements and accompanying Notes included in Item 8 of this Annual Report on Form 10-K. This discussion contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in these forward-looking statements as a result of various factors, including those discussed elsewhere in this Annual Report on Form 10-K, particularly in Item 1A. “Risk Factors.”

The MD&A is organized in the following sections:

• | Business Model and Growth Strategy |

• | Overview |

• | Consolidated Results of Operations |

• | Segment Results |

• | Financial Condition |

• | Liquidity and Capital Resources |

• | Critical Accounting Policies and Estimates |

BUSINESS MODEL AND GROWTH STRATEGY

We are the largest producer of quality chocolate in North America, a leading snack maker in the United States and a global leader in chocolate and non-chocolate confectionery. We report our operations through two segments: North America and International and Other.

We believe we have differentiated assets and capabilities that when integrated, can create advantage in the marketplace and secure our future. Our focus on the following strategic imperatives should enable us to drive shareholder value and deliver on our financial commitments.

• | Undisputed Leader in US Confection and Capturing Incremental Snacking Occasions. We are taking actions to deepen our consumer connections, utilize our beloved brands to deliver meaningful innovation and reinvent the shopping experience, while also pursuing opportunities to diversify our portfolio and establish a strong presence across the broader snacking continuum. |

◦ | Our products frequently play an important role in special meaningful moments among family and friends. Seasons are an important part of our business model and for consumers, they are highly anticipated, cherished special times, centered around traditions. For us, it’s an opportunity for our brands to be part of many connections during the year when family and friends gather. |

◦ | Innovation is an important lever in this variety seeking category and we are leveraging work from our proprietary demand landscape analytical tool to shape our future innovation and make it more impactful. We are becoming more disciplined in our focus on platform innovation, which should enable sustainable growth over time and significant extensions to our core. |

◦ | Through our shopper insights work, we are currently collaborating with our retail partners on in-aisle strategies that we believe will breathe life into the center of the store and transform the shopping experience by improving paths to purchase, stopping power, navigation, engagement and conversion. We have also responded to the changing retail environment by investing in digital commerce capabilities. |

◦ | To expand our breadth in snacking, we are focused on expanding the boundaries of our core confection brands to capture new snacking occasions and increasing our exposure into new snack categories through acquisitions. Our expansion into snacking is being fueled by the recent acquisitions of ONE Brands in September 2019, Pirate Brands in October 2018 and Amplify in January 2018, respectively. |

The Hershey Company | 2019 Form 10-K | Page 17

• | Driving Profitable Growth, Allocating Capital Resources and Optimizing Cost Structure. We are focused on ensuring that we efficiently allocate our resources to the areas with the highest potential for profitable growth. We believe this will enable margin expansion and position us within the top quartile of operating income margin relative to our peers. |

◦ | We have reset our international investment, while holding fast to our belief that our targeted emerging market strategy will deliver long-term, profitable growth. The uncertain macroeconomic environment in many of these markets is expected to continue and we aim to ensure our investments in these international markets are appropriate relative to the size of the opportunity. |

◦ | We have heightened our selling, marketing and administrative expense discipline in an effort to make improvements to our cost structure without jeopardizing topline growth. Our expectation is that advertising and related marketing expense will grow roughly in line with sales. |

◦ | We will continue to optimize our cost of goods sold through pricing activities and programs like network supply chain optimization and lean manufacturing. |

• | Expanding Competitive Advantage Through Differentiated Capabilities. In order to generate actionable insights, we must acquire, integrate, access and utilize vast sources of the right data in an effective manner. We are working to leverage our advanced analytical techniques to gain a deep understanding of consumers, our customers, our shoppers, our end-to-end supply chain, our retail environment and key economic drivers at both a macro and precision level, including digital transformation and new media models. In addition, we are in the process of transforming our enterprise resource planning system, which will enable employees to work more efficiently and effectively. |

OVERVIEW

Hershey is a global confectionery leader known for bringing goodness to the world through chocolate, sweets, mints, gum and other great tasting snacks. We are the largest producer of quality chocolate in North America, a leading snack maker in the United States and a global leader in chocolate and non-chocolate confectionery. We market, sell and distribute our products under more than 80 brand names in approximately 85 countries worldwide.

Our principal product offerings include chocolate and non-chocolate confectionery products; gum and mint refreshment products; pantry items, such as baking ingredients, toppings and beverages; and snack items such as spreads, meat snacks, bars and snack bites and mixes, popcorn and protein bars and cookies.

Recent Developments

The Company is closely monitoring an outbreak of respiratory illness caused by a novel coronavirus that was first detected in Wuhan City, Hubei Province, China and which continues to expand. The virus has impacted a host of sectors within China including retail, manufacturing, travel and hospitality. The financial and business impacts are currently unknown at this time; however, we believe will be limited to our China business which is part of our International and Other reportable segment. We are taking steps to protect our employees, consumers and business.

Business Acquisitions

In September 2019, we completed the acquisition of ONE Brands, LLC ("ONE Brands"), previously a privately held company that sells a line of low-sugar, high-protein nutrition bars to retailers and distributors in the United States, with the ONE Bar as its primary product. ONE Brands is expected to generate annualized net sales of approximately $100 million and complements our existing snacking businesses acquired in 2018.

In October 2018, we completed the acquisition of Pirate Brands, which includes the Pirate's Booty, Smart Puffs and Original Tings brands, from B&G Foods, Inc. Pirate Brands offers baked, trans fat free and gluten free snacks and is available in a wide range of food distribution channels in the United States.

In January 2018, we completed the acquisition of all of the outstanding shares of Amplify Snack Brands, Inc. ("Amplify"), a publicly traded company based in Austin, Texas that owns several popular better-for-you snack brands such as SkinnyPop, Oatmega and Paqui. The acquisition enables us to capture more consumer snacking occasions by creating a broader portfolio of brands.

The Hershey Company | 2019 Form 10-K | Page 18

CONSOLIDATED RESULTS OF OPERATIONS

Percent Change | ||||||||||||||||||

For the years ended December 31, | 2019 | 2018 | 2017 | 2019 vs 2018 | 2018 vs 2017 | |||||||||||||

In millions of dollars except per share amounts | ||||||||||||||||||

Net Sales | $ | 7,986.3 | $ | 7,791.1 | $ | 7,515.4 | 2.5 | % | 3.7 | % | ||||||||

Cost of Sales | 4,363.8 | 4,215.7 | 4,060.0 | 3.5 | % | 3.8 | % | |||||||||||

Gross Profit | 3,622.5 | 3,575.4 | 3,455.4 | 1.3 | % | 3.5 | % | |||||||||||

Gross Margin | 45.4 | % | 45.9 | % | 46.0 | % | ||||||||||||

SM&A Expense | 1,905.9 | 1,874.8 | 1,885.5 | 1.7 | % | (0.6 | )% | |||||||||||

SM&A Expense as a percent of net sales | 23.9 | % | 24.1 | % | 25.1 | % | ||||||||||||

Long-Lived and Intangible Asset Impairment Charges | 112.5 | 57.7 | 208.7 | 94.9 | % | (72.3 | )% | |||||||||||

Business Realignment Costs | 8.1 | 19.1 | 47.8 | (57.5 | )% | (60.0 | )% | |||||||||||

Operating Profit | 1,596.0 | 1,623.8 | 1,313.4 | (1.7 | )% | 23.6 | % | |||||||||||

Operating Profit Margin | 20.0 | % | 20.8 | % | 17.5 | % | ||||||||||||

Interest Expense, Net | 144.1 | 138.8 | 98.3 | 3.8 | % | 41.3 | % | |||||||||||

Other (Income) Expense, Net | 71.1 | 74.8 | 104.4 | (5.0 | )% | (28.4 | )% | |||||||||||

Provision for Income Taxes | 234.0 | 239.0 | 354.1 | (2.1 | )% | (32.5 | )% | |||||||||||

Effective Income Tax Rate | 16.9 | % | 17.0 | % | 31.9 | % | ||||||||||||

Net Income Including Noncontrolling Interest | 1,146.8 | 1,171.2 | 756.6 | (2.1 | )% | 54.8 | % | |||||||||||

Less: Net Loss Attributable to Noncontrolling Interest | (2.9 | ) | (6.5 | ) | (26.4 | ) | (54.8 | )% | (75.4 | )% | ||||||||

Net Income Attributable to The Hershey Company | $ | 1,149.7 | $ | 1,177.7 | $ | 783.0 | (2.4 | )% | 50.4 | % | ||||||||

Net Income Per Share—Diluted | $ | 5.46 | $ | 5.58 | $ | 3.66 | (2.2 | )% | 52.5 | % | ||||||||

Note: Percentage changes may not compute directly as shown due to rounding of amounts presented above. | ||||||||||||||||||

Net Sales

2019 compared with 2018

Net sales increased 2.5% in 2019 compared with 2018, reflecting a favorable price realization of 1.7% due to higher prices on certain products, a 1.0% benefit from net acquisitions and divestitures (predominantly driven by the 2019 acquisition of ONE Brands and the 2018 acquisition of Pirate Brands, partially offset by 2018 divestitures) and a volume increase of 0.1%, partially offset by an unfavorable impact from foreign currency exchange rates of 0.3%. Excluding foreign currency, our 2019 net sales increased 2.8%. Consolidated volumes increased due to solid marketplace growth in select international markets.

2018 compared with 2017

Net sales increased 3.7% in 2018 compared with 2017, reflecting a benefit from the recent Amplify and Pirate Brands acquisitions of 3.6% and a volume increase of 1.3%, partially offset by unfavorable price realization of 1.0% and an unfavorable impact from foreign currency exchange rates of 0.2%. Excluding the unfavorable impact from foreign currency exchange rates, our net sales increased 3.9%. Consolidated volumes increased due to the acquisitions of Amplify and Pirate Brands, as well as solid performance in select international markets, which more than offset the volume reduction resulting from the sale of Shanghai Golden Monkey ("SGM") in July 2018. The net increase in volume was partially offset by unfavorable net price realization, which was primarily attributed to incremental trade promotional expense in the North America segment in support of 2018 programming.

The Hershey Company | 2019 Form 10-K | Page 19

Key U.S. Marketplace Metrics

For the full year 2019, our total U.S. retail takeaway increased 2.5% in the expanded multi-outlet combined plus convenience store channels (IRI MULO + C-Stores), which includes candy, mint, gum, salty snacks, meat snacks and grocery items. Our U.S. candy, mint and gum ("CMG") consumer takeaway increased 2.6%, resulting in a slight CMG market share gain.

The CMG consumer takeaway and market share information reflect measured channels of distribution accounting for approximately 90% of our U.S. confectionery retail business. These channels of distribution primarily include food, drug, mass merchandisers, and convenience store channels, plus Wal-Mart Stores, Inc., partial dollar, club and military channels. These metrics are based on measured market scanned purchases as reported by Information Resources, Incorporated ("IRI"), the Company's market insights and analytics provider, and provide a means to assess our retail takeaway and market position relative to the overall category.

Cost of Sales and Gross Margin

2019 compared with 2018

Cost of sales increased 3.5% in 2019 compared with 2018. The increase was driven by higher freight and logistics costs, additional plant costs, and an incremental $33.9 million unfavorable impact from marking-to-market our commodity derivative instruments intended to economically hedge future years' commodity purchases. These drivers were partially offset by favorable supply chain productivity.

Gross margin decreased by 50 basis points in 2019 compared with 2018. The decrease was primarily due to the higher freight and logistics costs, additional plant costs, and the unfavorable year-over-year mark-to-market impact from commodity derivative instruments. These factors were partially offset by supply chain productivity, price realization, and favorable product mix.

2018 compared with 2017

Cost of sales increased 3.8% in 2018 compared with 2017. The increase was driven by higher sales volume, higher freight and logistics costs and additional plant costs. These drivers were partially offset by an incremental $125.1 million favorable impact from marking-to-market our commodity derivative instruments intended to economically hedge future years' commodity purchases and supply chain productivity,

Gross margin decreased by 10 basis points in 2018 compared with 2017. The decrease was primarily due to the higher freight and logistics costs, unfavorable product mix, additional plant costs related to new production lines, and incremental trade promotional expense. These factors were partially offset by the favorable year-over-year mark-to-market impact from commodity derivative instruments and supply chain productivity.

Selling, Marketing and Administrative

2019 compared with 2018

Selling, marketing and administrative (“SM&A”) expenses increased $31.1 million or 1.7% in 2019. Total advertising and related consumer marketing expenses increased 4.2% driven by advertising increases in North America. SM&A expenses, excluding advertising and related consumer marketing, increased approximately 0.2% in 2019 due to incremental expenses from Pirate Brands and ONE Brands, as well as higher employee related compensation, which more than offset reductions in our base spending from the Margin for Growth Program.

2018 compared with 2017

SM&A expenses decreased $10.7 million or 0.6% in 2018. Total advertising and related consumer marketing expenses declined 10.9% due mainly to spend optimization and shifts relating to our emerging brands, as well as reductions in agency and production fees. SM&A expenses, excluding advertising and related consumer marketing, increased approximately 6.2% in 2018 due to incremental expenses from Amplify and Pirate Brands and higher expenses related to the multi-year implementation of our enterprise resource planning system, which more than offset reductions in our base spending from the Margin for Growth Program.

The Hershey Company | 2019 Form 10-K | Page 20

Long-Lived and Intangible Asset Impairment Charges

In 2019, we recorded the following impairment charges:

For the year ended December 31, | 2019 | |||

In millions of dollars | ||||

Customer relationship and trademark intangible assets (1) | $ | 100.1 | ||

Other long-lived assets not held for sale (2) | 9.7 | |||

Adjustment to disposal group (3) | 2.7 | |||

Long-lived and intangible asset impairment charges | $ | 112.5 | ||

(1) | During the fourth quarter of 2019, we recorded impairment charges to write down customer relationship and trademark intangible assets associated with KRAVE Pure Foods, Inc. (“Krave”). These charges were determined by comparing the fair value of the asset group to its carrying value. We used various valuation techniques to determine fair value, with the primary techniques being discounted cash flow analysis and relief-from-royalty valuation approaches, which use significant unobservable inputs, or Level 3 inputs, as defined by the fair value hierarchy. |

(2) | During 2019, we recorded impairment charges predominantly comprised of select long-lived assets that had not yet met the held for sale criteria. The fair value of these assets was supported by potential sales prices with third-party buyers and market analysis. |