Horizon Therapeutics Public Ltd Co - Annual Report: 2021 (Form 10-K)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2021

or

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 001-35238

HORIZON THERAPEUTICS PUBLIC LIMITED COMPANY

(Exact name of Registrant as specified in its charter)

|

Ireland |

Not Applicable |

|

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

|

|

|

|

|

|

70 St. Stephen’s Green Dublin 2, D02 E2X4, Ireland |

Not Applicable |

|

|

(Address of principal executive offices) |

(Zip Code) |

|

011 353 1 772 2100

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class |

Trading Symbol |

Name of Each Exchange on Which Registered |

|

Ordinary shares, nominal value $0.0001 per share |

HZNP |

The Nasdaq Global Select Market |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer |

|

☒ |

Accelerated filer |

|

☐ |

|

|

|

|

|

|

|

|

Non-accelerated filer |

|

☐ |

Smaller reporting company |

|

☐ |

|

|

|

|

|

|

|

|

Emerging growth company |

|

☐ |

|

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined by Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the registrant’s voting ordinary shares held by non-affiliates of the registrant, based upon the $93.64 per share closing sale price of the registrant’s ordinary shares on June 30, 2021 (the last business day of the registrant’s most recently completed second quarter), was approximately $20.9 billion. Solely for purposes of this calculation, the registrant’s directors and executive officers and holders of 10% or more of the registrant’s outstanding ordinary shares have been assumed to be affiliates and an aggregate of 2,427,888 ordinary shares held by such persons on June 30, 2021 are not included in this calculation.

As of February 23, 2022, the registrant had outstanding 229,167,089 ordinary shares.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement for the registrant’s 2022 Annual General Meeting of Shareholders are incorporated by reference into Part III of this Annual Report on Form 10-K.

HORIZON THERAPEUTICS PLC

FORM 10-K — ANNUAL REPORT

For the Fiscal Year Ended December 31, 2021

TABLE OF CONTENTS

PART I

Special Note Regarding Forward-Looking Statements

This Annual Report on Form 10-K contains “forward-looking statements” — that is, statements related to future, not past, events — as defined in Section 21E of the Securities Exchange Act of 1934, as amended, that reflect our current expectations regarding our future growth, results of operations, business strategy and plans, financial condition, cash flows, performance, development plans and timelines, business prospects, and opportunities, as well as assumptions made by, and information currently available to, our management. Forward-looking statements include any statement that does not directly relate to a current or historical fact. Forward-looking statements generally can be identified by words such as “believe,” “may,” “could,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “seek,” “plan,” “expect,” “should,” “would”, or similar expressions. These statements are based on current expectations and assumptions that are subject to risks and uncertainties inherent in our business, which could cause our actual results to differ materially from those indicated in the forward-looking statements. Factors that could cause actual results to differ materially from those indicated in the forward-looking statements include, without limitation: our ability to successfully execute our sales and marketing strategy, including continuing to successfully recruit and retain sales and marketing personnel and to successfully build the market for our medicines; our ability to build a sustainable pipeline of new medicine candidates; whether we will be able to realize the expected benefits of strategic transactions, including whether and when such transactions will be accretive to our net income; the rate and degree of market acceptance of, and our ability and our distribution and marketing partners’ ability to obtain coverage and adequate reimbursement and pricing for, our medicines from government and third-party payers; the scope and duration of impacts of the COVID-19 pandemic on our business, our industry and the economy, including impacts to supply chains and clinical trials; our ability to maintain regulatory approvals for our medicines; our ability to conduct clinical development and obtain regulatory approvals for our medicine candidates, including potential delays in initiating and completing studies and filing for and obtaining regulatory approvals and whether data from clinical studies will support regulatory approval; our need for and ability to obtain additional financing; the accuracy of our estimates regarding future financial results; our ability to successfully execute our strategy to develop or acquire additional medicines or companies, including disruption from any future acquisition or whether any acquired development programs will be successful; our ability to manage our anticipated future growth; the ability of our medicines to compete with alternative therapies, including generic medicines and new medicines that may be developed by our competitors; our ability and our distribution and marketing partners’ ability to comply with regulatory requirements regarding the sales, marketing and manufacturing of our medicines and medicine candidates; the performance of our third-party distribution partners, licensees and manufacturers over which we have limited control; our ability to obtain and maintain intellectual property protection for our medicines; our ability to defend our intellectual property rights with respect to our medicines; our ability to operate our business without infringing the intellectual property rights of others; the loss of key commercial or management personnel; regulatory developments in the United States and other countries, including potential changes in healthcare laws and regulations; and other risks detailed below in Part I — Item 1A. “Risk Factors”. Although we believe that the expectations reflected in our forward-looking statements are reasonable, we cannot guarantee future results, events, levels of activity, performance or achievement. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, unless required by law.

Risk Factors Summary

Our business faces significant risks and uncertainties. If any of the following risks are realized, our business, financial condition and results of operations could be materially and adversely affected. You should carefully review and consider the full discussion of our risk factors in the section titled “Risk Factors” in Part I, Item 1A of this Annual Report on Form 10-K. Set forth below is a summary list of the principal risk factors as of the date of the filing this Annual Report on Form 10-K:

|

|

• |

The COVID-19 global pandemic may continue to adversely impact our business, including the commercialization of our medicines, our supply chain, our clinical trials, our liquidity and access to capital markets and our business development activities. |

|

|

• |

Our ability to generate revenues from our medicines is subject to attaining significant market acceptance among physicians, patients and healthcare payers. |

|

|

• |

Our future prospects are highly dependent on our ability to successfully develop and execute commercialization strategies for each of our medicines. Failure to do so would adversely impact our financial condition and prospects. |

|

|

• |

In order to increase adoption and sales of our medicines, we will need to continue developing our commercial organization as well as recruit and retain qualified sales representatives. |

|

|

• |

Coverage and reimbursement may not be available, or reimbursement may be available at only limited levels, for our medicines, which could make it difficult for us to sell our medicines profitably. |

1

|

|

• |

Our medicines are subject to extensive regulation, and we may not obtain additional regulatory approvals for our medicines. |

|

|

• |

We are subject to ongoing obligations and continued regulatory review by the FDA and equivalent foreign regulatory agencies, and we may be subject to penalties and litigation and large incremental expenses if we fail to comply with regulatory requirements or experience problems with our medicines. |

|

|

• |

We rely on third parties to manufacture commercial supplies of all of our medicines, and we currently intend to rely, in whole or in part, on third parties to manufacture commercial supplies of any other approved medicines. The commercialization of any of our medicines could be stopped, delayed or made less profitable if those third parties fail to provide us with sufficient quantities of medicine or fail to do so at acceptable quality levels or prices or fail to maintain or achieve satisfactory regulatory compliance. |

|

|

• |

We face significant competition from other biotechnology and pharmaceutical companies, including those marketing generic medicines and our operating results will suffer if we fail to compete effectively. |

|

|

• |

Clinical development of drugs and biologics involves a lengthy and expensive process with an uncertain outcome, and results of earlier studies and trials may not be predictive of future trial results. |

|

|

• |

If we fail to develop or acquire other medicine candidates or medicines, our business and prospects would be limited. |

|

|

• |

We are subject to federal, state and foreign healthcare laws and regulations and implementation or changes to such healthcare laws and regulations could adversely affect our business and results of operations. |

|

|

• |

If we are unable to obtain or protect intellectual property rights related to our medicines and medicine candidates, we may not be able to compete effectively in our markets. |

Item 1. Business

Unless otherwise indicated or the context otherwise requires, references to the “Company”, “we”, “us” and “our” refer to Horizon Therapeutics plc and its consolidated subsidiaries.

Overview

We are focused on the discovery, development and commercialization of medicines that address critical needs for people impacted by rare, autoimmune and severe inflammatory diseases. Our pipeline is purposeful: we apply scientific expertise and courage to bring clinically meaningful therapies to patients. We believe science and compassion must work together to transform lives.

Our Strategy

Horizon is a leading high-growth, innovation-driven, profitable biotech company. We are focused on the discovery, development and commercialization of medicines that address critical needs for people impacted by rare, autoimmune and severe inflammatory diseases. Our three strategic goals are to: (i) maximize the benefit and value of our on-market medicines through commercial execution and clinical investment; (ii) expand our pipeline through significant investment in research and development, or R&D, and business development; and (iii) build a global presence in targeted international markets. Our vision is to build healthier communities, urgently and responsibly, supported by our philosophy to make a meaningful difference for patients and communities in need. We believe this generates value for our multiple stakeholders, including our shareholders.

We have made tremendous progress since our beginnings as a public company in 2011, when we had two on-market medicines and total net sales of $6.9 million. With 2021 total net sales of $3.2 billion, we now have a portfolio of 12 on-market medicines with three key growth drivers, a growing pipeline of more than 20 programs and a strong financial position that gives us the capacity to support future pipeline expansion opportunities.

We have achieved our transformation into an innovation-driven biotech company through our strong strategic execution and by leveraging the three elements we believe set Horizon apart: (i) our excellence in commercial execution; (ii) our proven and disciplined business development strategy; and (iii) our strong clinical development capability. Our excellence in commercial execution has accelerated our growth trajectory and allowed us to pursue maximizing the potential of our medicines. Through our strong in-house business development capability, we acquire and license medicines focused on opportunities for which we believe we are uniquely positioned to drive value. We leverage our deep collective drug development experience and agile approach to continually explore new ways for patients to benefit from our existing medicines and develop new medicines.

2

We have two reportable segments, (i) the orphan segment, our strategic growth business, and (ii) the inflammation segment, and we report net sales and segment operating income for each segment.

Our Company

We are a public limited company formed under the laws of Ireland. We operate through a number of U.S. and other international subsidiaries with principal business purposes of performing R&D or manufacturing operations, serving as distributors of our medicines, holding intellectual property assets or providing us with services and financial support.

Our principal executive offices are located at 70 St. Stephen’s Green, Dublin 2, D02 E2X4, Ireland and our telephone number is 011 353 1 772 2100. Our website address is www.horizontherapeutics.com. Information found on, or accessible through, our website is not a part of, and is not incorporated into, this Annual Report on Form 10-K.

Acquisitions and Divestitures

Since January 1, 2019, we completed the following acquisitions and divestitures:

|

|

• |

In July 2021, we completed the purchase of a biologic drug product manufacturing facility from EirGen Pharma Limited, or EirGen, a subsidiary of OPKO Health, Inc., in Waterford, Ireland. |

|

|

• |

In March 2021, we completed the acquisition of Viela Bio, Inc., or Viela, in which we acquired all of the issued and outstanding shares of Viela’s common stock. |

|

|

• |

In October 2020, we sold our rights to develop and commercialize RAVICTI ® and BUPHENYL® in Japan to Medical Need Europe AB, part of the Immedica Group, or Immedica. We have retained the rights to RAVICTI and BUPHENYL in North America. |

|

|

• |

In April 2020, we acquired Curzion Pharmaceuticals, Inc., or Curzion, a privately held development-stage biopharma company, and its development-stage oral selective lysophosphatidic acid 1 receptor (LPAR1) antagonist, CZN001 (renamed HZN-825), for an upfront payment with additional payments contingent on the achievement of development and regulatory milestones. |

|

|

• |

In June 2019, we sold our rights to MIGERGOT to Cosette Pharmaceuticals, Inc., for an upfront payment and potential additional contingent consideration payments. |

|

|

• |

Effective January 2019, we amended our license and supply agreements with Jagotec AG and Skyepharma AG, which are affiliates of Vectura Group plc, or Vectura. Under these amendments, our rights to LODOTRA® in Europe were transferred to Vectura. |

The consolidated financial statements presented herein include the results of operations of the acquired businesses from the applicable dates of acquisition. Refer to Note 4, Acquisitions, Divestitures and other Arrangements, of the Notes to Consolidated Financial Statements, included in Item 15 of this Annual Report on Form 10-K, for further details of our acquisitions and divestitures.

3

Impact of COVID-19

Beginning in March 2020, many states and municipalities in the United States took aggressive actions to reduce the spread of the COVID-19 pandemic, including limiting non-essential gatherings of people, ceasing all non-essential travel, ordering certain businesses and government agencies to cease non-essential operations at physical locations and issuing “shelter-in-place” orders which directed individuals to shelter at their places of residence (subject to limited exceptions). Similarly, the Irish government limited gatherings of people and encouraged employees to work from their homes. Vaccines and treatments have now enabled a resumption of more normal business practices and initiatives in many countries, including the United States and Ireland. While our financial results during the year ended December 31, 2021 were strong and we continue to have a significant amount of available liquidity, the COVID-19 pandemic may continue to have a negative impact on net sales during 2022, including due to the emergence of new variants of the virus and potential actions to combat their transmission. In addition, our clinical trials have been and may in the future be affected by the COVID-19 pandemic as referred to below.

Economic and health conditions in the United States and across most of the world are continuing to change rapidly because of the COVID-19 pandemic. Although COVID-19 is a global issue that is altering business and consumer activity, the pharmaceutical industry is considered a critical and essential industry in the United States and many other countries and, therefore, we do not currently expect any government-imposed extended shut downs of suppliers or distribution channels, although our suppliers and other third parties on which we rely could be impacted by employee absences due to COVID-19 illnesses. In respect of our medicines, we believe we have sufficient inventory of raw materials and finished goods and we expect patients to be able to continue to receive their medicines at a site of care, for our infused medicines, and from their current pharmacies, alternative pharmacies or, if necessary, by direct shipment from our third-party providers that have such capability, for our other medicines.

TEPEZZA ®

The launch of our infused medicine for thyroid eye disease, or TED, TEPEZZA, which was approved by the U.S. Food and Drug Administration, or FDA, on January 21, 2020, significantly exceeded our expectations. In early 2019, we initiated our pre-launch disease awareness, market development and market access efforts with multi-functional field-based teams beginning to engage with key stakeholders in July 2019. We believe these pre-launch efforts, the severity and acute nature of TED, and a highly motivated patient population have generated significant demand for the medicine. While we experienced a much higher number of new patients in 2020 than our initial estimates, the impact from COVID-19 slowed the generation of TEPEZZA patient enrollment forms, which drive new patient starts.

In December 2020, pursuant to the Defense Production Act of 1950, or DPA, Catalent Indiana, LLC, or Catalent, was ordered to prioritize certain COVID-19 vaccine manufacturing, resulting in the cancellation of previously guaranteed and contracted TEPEZZA drug product manufacturing slots, which were required to maintain TEPEZZA supply. To offset the reduced slots, we accelerated plans to increase the production scale of TEPEZZA drug product at Catalent.

In March 2021, the FDA approved a prior approval supplement to the TEPEZZA biologics license application, or BLA (which was previously approved in January 2020), giving us authorization to manufacture more TEPEZZA drug product in a batch resulting in an increased number of vials with each manufacturing slot. We commenced resupply of TEPEZZA to the market in April 2021. In addition, we received FDA approval in December 2021 for a second drug product manufacturer, Patheon Pharmaceuticals Inc., or Patheon (contract development and manufacturing organization services of Thermo Fisher Scientific). During the third quarter of 2021, we were informed that one of our contract manufacturers for TEPEZZA is manufacturing an adjuvant for a COVID-19 vaccine. The adjuvant is being manufactured on a different line to the line used to manufacture our medicine. We do not expect the manufacturing of this adjuvant to impact the supply of our medicine. Other than Catalent and the other previously mentioned contract manufacturer, we are not aware of any manufacturing facilities that are part of the supply chain for our medicines that are being utilized for the manufacture of vaccines for COVID-19. At this time, we consider our medicine inventories on hand to be sufficient to meet our commercial requirements.

4

As a result of the prior supply disruption, we delayed the start of an FDA-required post-marketing study to evaluate safety of TEPEZZA in a larger patient population and retreatment rates relative to how long patients receive the medicine. The FDA-required post-marketing study was initiated in the fourth quarter of 2021. We also delayed the start of our planned TEPEZZA clinical trial in chronic TED and an exploratory trial of TEPEZZA in diffuse cutaneous systemic sclerosis. The TEPEZZA clinical trial in chronic TED was initiated in the third quarter of 2021, and the exploratory trial of TEPEZZA in diffuse cutaneous systemic sclerosis was initiated in the fourth quarter of 2021.

KRYSTEXXA® and UPLIZNA®

KRYSTEXXA is an infused medicine for uncontrolled gout and was also achieving rapid growth prior to the COVID-19 pandemic. While the vast majority of patients on therapy maintained therapy, many new patients delayed infusions due to shelter-in-place guidelines and patients voluntarily delaying visits to healthcare providers and infusion centers. While there continues to be some impact on demand for KRYSTEXXA, we have seen improvements as healthcare systems have adapted to cope with the pandemic and vaccines have been widely administered in the United States.

UPLIZNA is an infused medicine for neuromyelitis optica spectrum disorder, or NMOSD, and was acquired through the Viela acquisition in March 2021. While there continues to be some impact on demand for UPLIZNA primarily due to limited patient access to healthcare providers and infusion centers, we have also seen improvements as healthcare systems have adapted to cope with the pandemic and vaccines have been widely administered in the United States.

Our other medicines

Our other orphan segment medicines, RAVICTI, PROCYSBI® and ACTIMMUNE®, treat serious, chronic diseases with serious consequences if left untreated. It is therefore critical for patients to maintain therapy. Patient motivation to continue treatment is high, and therefore net sales for these three medicines were stable during 2020 and 2021, with less impact from COVID-19 compared to our other medicines.

In regard to the inflammation segment, the impact of COVID-19 has significantly waned as healthcare systems have adapted to cope with the pandemic and vaccines have been widely administered in the United States, thereby facilitating the return to mainly in-person engagement by our sales representatives with healthcare providers. In addition, with our HorizonCares program, most patients do not need to physically visit a pharmacy to obtain a prescription because the vast majority of these medicines are delivered to a patient’s home through mail or local courier, depending on the participating pharmacy.

Clinical trials

Our clinical trials have been and may in the future be affected by COVID-19 or its variants. As referred to above, certain clinical trials for TEPEZZA were delayed due to the impact of the TEPEZZA supply disruption at Catalent. In addition, clinical site initiation and patient enrollment may be delayed due to staffing shortages or prioritization of hospital and healthcare resources toward COVID-19. Current or potential patients in our ongoing or planned clinical trials may also choose to not enroll, not participate in follow-up clinical visits or drop out of the trial as a result of, or a precaution against, contracting COVID-19. Further, some patients may not be able or willing to comply with clinical trial protocols if quarantines impede patient movement or interrupt healthcare services. Some clinical sites in the United States have slowed or stopped further enrollment of new patients in clinical trials, denied access to site monitors or otherwise curtailed certain operations. Similarly, our ability to recruit and retain principal investigators and site staff who, as healthcare providers, may have heightened exposure to COVID-19, may be adversely impacted. These events could delay our clinical trials, increase the cost of completing our clinical trials and negatively impact the integrity, reliability or robustness of the data from our clinical trials.

We are continuing to actively monitor the possible impacts from the COVID-19 pandemic, including the emergence of new variants of the virus, and may take further actions to alter our business operations as may be required by federal, state or local authorities or that we determine are in the best interests of patients. There is significant uncertainty about the duration and potential impact of the COVID-19 pandemic. This means that our results could change at any time and the contemplated impact of the COVID-19 pandemic on our business results and outlook represents our estimate based on the information available as of the date of this Annual Report on Form 10-K.

5

Our Medicines

We believe our medicines address unmet therapeutic needs in orphan diseases, arthritis, pain and inflammation, and inflammatory diseases and provide significant advantages over existing therapies.

As of December 31, 2021, our commercial portfolio consisted of the following medicines:

|

Medicine |

|

Indication |

|

2021 Net Sales (in millions) |

|

|

Marketing Rights |

|

|

|

|

|

|

|

|

|

|

|

|

ORPHAN SEGMENT: |

|

|

|

|

|

|

||

|

TEPEZZA |

|

Thyroid eye disease |

|

$ |

1,661.3 |

|

|

Worldwide |

|

KRYSTEXXA |

|

Chronic refractory gout (“uncontrolled gout”) |

|

$ |

565.5 |

|

|

Worldwide |

|

RAVICTI |

|

Urea cycle disorders |

|

$ |

291.9 |

|

|

North America (1) |

|

PROCYSBI |

|

Nephropathic cystinosis |

|

$ |

189.9 |

|

|

United States and certain other countries (2) |

|

ACTIMMUNE |

|

Chronic granulomatous disease and severe, malignant osteopetrosis |

|

$ |

117.2 |

|

|

United States, Canada and Japan (3) |

|

UPLIZNA |

|

Neuromyelitis optica spectrum disorder |

|

$ |

60.8 |

|

|

Worldwide, except certain countries in Asia (4) |

|

BUPHENYL |

|

Urea cycle disorders |

|

$ |

7.9 |

|

|

North America (5) |

|

QUINSAIR™ |

|

Treatment of chronic pulmonary infections due to Pseudomonas aeruginosa in cystic fibrosis patients |

|

$ |

1.0 |

|

|

Canada and certain other countries (6) |

|

INFLAMMATION SEGMENT: |

|

|

|

|

|

|

||

|

PENNSAID 2%® |

|

Pain of osteoarthritis of the knee(s) |

|

$ |

191.6 |

|

|

United States |

|

DUEXIS® |

|

Signs and symptoms of osteoarthritis and rheumatoid arthritis |

|

$ |

74.0 |

|

|

Worldwide |

|

RAYOS® |

|

Rheumatoid arthritis, polymyalgia rheumatic, systemic lupus erythematosus and multiple other indications |

|

$ |

56.9 |

|

|

North America (7) |

|

VIMOVO® |

|

Signs and symptoms of osteoarthritis, rheumatoid arthritis and ankylosing spondylitis |

|

$ |

8.4 |

|

|

United States |

|

|

(1) |

In December 2018 and October 2020, we sold our rights to develop and commercialize RAVICTI outside of North America to Immedica. We have retained the rights to RAVICTI in North America. |

|

|

(2) |

We market PROCYSBI in the United States and Canada. We also have marketing rights to PROCYSBI in Asia. PROCYSBI is also available in Latin America through a managed assistance program through our partner Uno Healthcare Inc. |

|

|

(3) |

ACTIMMUNE is known as IMUKIN outside the United States, Canada and Japan. In July 2018, we sold the rights to IMUKIN in all territories outside of the United States, Canada and Japan to Clinigen Group plc. |

|

|

(4) |

Our strategic partner, Mitsubishi Tanabe Pharma Corporation, or MTPC, has rights to the development and commercialization of UPLIZNA for NMOSD as well as other potential future indications in Japan and certain other countries in Asia. In March 2021, MTPC received manufacturing and marketing approval for UPLIZNA in Japan. UPLIZNA was launched in Japan during the second quarter of 2021. In addition, Hansoh Pharmaceutical Group Company Limited has rights to the development and commercialization of UPLIZNA for NMOSD as well as other potential future indications in China, Hong Kong and Macau. |

|

|

(5) |

BUPHENYL is known as AMMONAPS outside of North America and Japan. In December 2018 and October 2020, we sold our rights to develop and commercialize BUPHENYL outside of North America to Immedica. We have retained the rights to BUPHENYL in North America. |

|

|

(6) |

We market QUINSAIR in Canada. We also have marketing rights for QUINSAIR in the United States, Latin America and Asia. We have not received regulatory approval to market QUINSAIR in the United States. |

6

|

|

(7) |

Outside the United States, RAYOS is sold and marketed as LODOTRA. Effective January 2019, we amended our license and supply agreements with Jagotec AG and Skyepharma AG, which are affiliates of Vectura. Under these amendments, our rights to LODOTRA in Europe were transferred to Vectura. |

Information on our total revenues by product in each of the years ended December 31, 2021, 2020 and 2019, is included in the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this Annual Report on Form 10-K.

ORPHAN SEGMENT

Our orphan segment consists of our medicines TEPEZZA, KRYSTEXXA, RAVICTI, PROCYSBI, ACTIMMUNE, UPLIZNA, BUPHENYL and QUINSAIR.

TEPEZZA

TEPEZZA is a fully human monoclonal antibody and a targeted inhibitor of the insulin-like growth factor-1 receptor, or IGF-1R, that is the first and only FDA-approved medicine for the treatment of TED. TED is a serious, progressive and vision-threatening rare autoimmune condition. While TED often occurs in people living with hyperthyroidism or Graves’ disease, it is a distinct disease that is caused by autoantibodies activating an IGF-1R-mediated signaling complex on cells within the retro-orbital space. This leads to a cascade of negative effects, which may cause long-term, irreversible eye damage. As TED progresses, it causes serious damage – including proptosis (eye bulging), strabismus (misalignment of the eyes) and diplopia (double vision) – and in some cases can lead to blindness. Historically, patients have had to live with TED until the inflammation subsides, after which they are often left with permanent and vision-impairing consequences and may require multiple surgeries that do not completely return the patient to their pre-disease state.

Our comprehensive post-launch commercial strategy for TEPEZZA aims to enable more TED patients to benefit from TEPEZZA. We are doing this by: (i) facilitating continued TEPEZZA uptake in the treatment of TED through continued promotion of TEPEZZA to treating physicians; (ii) continuing to develop the TED market by increasing physician awareness of the disease severity and the urgency to diagnose and treat it, as well as the benefits of treatment with TEPEZZA; (iii) driving accelerated disease identification and time to treatment through our digital and broadcast marketing campaigns; (iv) enhancing the patient journey with our high-touch, patient-centric model as well as support for the patient and site-of-care referral processes; and (v) pursuing more timely access to TEPEZZA for TED patients.

To advance the continued strong growth and adoption of TEPEZZA, we are continuing to invest in significant expansion efforts in multiple areas: our commercial and field-based organization for TEPEZZA; our marketing initiatives; our long-term supply capacity; and our efforts to expand outside the United States.

With the U.S. launch of TEPEZZA in 2020 and the demonstrated benefit to U.S. patients with TED, we are pursuing a global expansion strategy to bring TEPEZZA to patients with TED in other parts of the world. Japan is one of the countries we are pursuing and, in February 2022, we initiated a Phase 3 randomized, placebo-controlled clinical trial for the treatment of moderate-to-severe active TED patients in Japan.

As the only FDA-approved medication for the treatment of TED, TEPEZZA has no direct approved competition. We believe that the results of the TEPEZZA Phase 3 and Phase 2 clinical trials present a significantly high hurdle for potential competitors, given that potentially competitive medicines would be expected to demonstrate similar or greater efficacy and safety in the treatment of TED. In addition, we have a biologic exclusivity in the United States covering TEPEZZA that will expire in 2032. Further, the complexity of manufacturing TEPEZZA could pose a barrier to potential biosimilar competition. Although TEPEZZA does not face direct competition, other therapies, such as corticosteroids, have been used on an off-label basis to alleviate some of the symptoms of TED. While these therapies have not proved effective in treating the underlying disease, and carry with them potential significant side effects, their off-label use could reduce or delay treatment with TEPEZZA among the addressable patient population. Immunovant Inc., or Immunovant, is conducting Phase 2 clinical trials of a fully human anti-FcRn monoclonal antibody candidate for the treatment of active TED, also referred to as Graves’ ophthalmopathy. On February 2, 2021, Immunovant announced a voluntary pause in the clinical dosing of the candidate due to elevated total cholesterol and low-density lipoprotein levels in patients treated with the candidate. Immunovant has indicated it intends to continue developing the candidate but did not provide an estimate of when the dosing might resume. Viridian Therapeutics, Inc. is pursuing development of two anti-IGF-1R monoclonal antibodies for TED and initiated a Phase 1/2 trial in the fourth quarter of 2021.

7

KRYSTEXXA

A PEGylated uric acid specific enzyme (uricase), KRYSTEXXA is the first and only FDA approved medicine for the treatment of uncontrolled gout. Uncontrolled gout occurs in patients who have failed to normalize serum uric acid, or sUA, and whose signs and symptoms are inadequately controlled with conventional therapies, such as xanthine oxidase inhibitors, or XOIs, at the maximum medically appropriate dose, or for whom these drugs are contraindicated.

KRYSTEXXA has a unique mechanism of action that can rapidly reverse disease progression. Unlike conventional XOI therapies, which address the over-production or under-excretion of uric acid, KRYSTEXXA converts uric acid into allantoin, a water-soluble molecule, which the body can easily eliminate through the urine. Renal excretion of allantoin is ten times more efficient than uric acid excretion. Additionally, many chronic kidney disease, or CKD, patients have gout, and the disease tends to be more prevalent as CKD advances. While conventional XOI gout therapies can place additional burden on the kidneys and have dosing limitations, KRYSTEXXA has been proven effective and safe for uncontrolled gout patients with CKD without the need to adjust dosing.

Gout is one of the most common forms of inflammatory arthritis and can be assessed by a simple blood test for the amounts of uric acid in the blood (sUA levels). Typically in gout, when uric acid levels are greater than 6.8 milligrams per deciliter, urate will crystallize and deposit. These hard deposits are known as tophi and may occur anywhere in the body, including joints, as well as organs, such as the kidney and heart. When under-treated medically, tophi often lead to bone erosions and loss of functional ability. Gout flares, a common characteristic of uncontrolled gout, are intensely painful. They may or may not be accompanied by tophi. A systemic disease, uncontrolled gout frequently causes crippling disabilities and significant joint damage. Of the 9.5 million gout sufferers in the United States, we estimate that greater than 100,000 patients have uncontrolled gout.

We are focused on optimizing and maximizing the benefit the medicine offers for patients as well as driving toward its peak U.S. net sales potential. Our growth strategy for KRYSTEXXA includes: (i) supporting the continued adoption of the use of KRYSTEXXA with immunomodulators to increase the complete response rate of KRYSTEXXA; (ii) increasing uptake by rheumatologists; and (iii) accelerating uptake of the medicine by nephrologists. Following positive data from our Phase 4 randomized, placebo-controlled MIRROR clinical trial that evaluated the use of KRYSTEXXA plus methotrexate, an immunomodulator frequently used by rheumatologists, we submitted a supplemental biologics license application to the FDA in the first quarter of 2022 to expand the label for KRYSTEXXA to include co-treatment with methotrexate.

In 2019, we added a separate group of sales representatives to call exclusively on nephrologists. We believe KRYSTEXXA offers a solution to a clinical need experienced by many nephrologists in dealing with uncontrolled gout patients with CKD.

As the only FDA-approved medication for the treatment of uncontrolled gout, KRYSTEXXA faces limited direct competition. We believe that the complexity of manufacturing KRYSTEXXA provides a barrier to potential biosimilar competition. In addition, we submitted a supplemental BLA for KRYSTEXXA in the first quarter of 2022 as a result of our topline clinical results of our MIRROR randomized controlled trial evaluating KRYSTEXXA and methotrexate versus KRYSTEXXA alone. However, a number of competitors have medicines in clinical trials, including Selecta Biosciences Inc., or Selecta, which has initiated a Phase 3 clinical program of a candidate for the treatment of chronic refractory gout. In September 2020, Selecta announced topline clinical data that did not meet the primary endpoint or demonstrate statistical superiority for its Phase 2 trial that compared its candidate, which includes an immunomodulator, to KRYSTEXXA alone without an immunomodulator. In July 2020, Selecta and Swedish Orphan Biovitrum AB, or Sobi, entered into a strategic licensing agreement under which Sobi will assume responsibility for certain development, regulatory, and commercial activities for this candidate. In December 2021, Selecta and Sobi announced the completion of enrollment for DISSOLVE I, the first of two clinical studies of the Phase 3 DISSOLVE development program of SEL-212 for chronic refractory gout. SEL-212 is a combination of Selecta’s ImmTOR immune tolerance platform and a therapeutic uricase enzyme (pegadricase).

RAVICTI

RAVICTI is indicated for use as a nitrogen-binding agent for chronic management of adult and pediatric patients (beginning at birth) with urea cycle disorders, or UCDs, that cannot be managed by dietary protein restriction and/or amino acid supplementation alone. UCDs are rare, life-threatening genetic disorders. RAVICTI must be used with dietary protein restriction and, in some cases, dietary supplements (for example, essential amino acids, arginine, citrulline or protein-free calorie supplements).

8

UCDs are inherited metabolic diseases caused by a deficiency of one of the enzymes or transporters that constitute the urea cycle. The urea cycle involves a series of biochemical steps in which ammonia, a potent neurotoxin, is converted to urea, which is excreted in the urine. UCD patients may experience episodes during which the ammonia levels in their blood become excessively high, called hyperammonemic crises, which may result in irreversible brain damage, coma or death. We estimate that there are approximately 2,600 patients with UCDs living in the United States, including approximately 1,000 diagnosed patients. RAVICTI is not indicated for treatment of acute hyperammonemia or for N-acetylglutamate synthase (NAGS) deficiency.

UCD symptoms may first occur at any age depending on the severity of the disorder, with more severe defects presenting earlier in life. However, a prompt diagnosis and careful management of the disease can lead to good clinical outcomes.

RAVICTI competes with older-generation nitrogen scavenger medicines. In the United States, RAVICTI competes with all forms of sodium phenylbutyrate, including BUPHENYL. RAVICTI has advantages over older-generation medicines leading to better patient adherence and compliance rates, such as its better tolerability for patients. It is ingested by mouth, requires little preparation and has little taste and lower sodium content than other nitrogen scavenger medications. A few competitors have alternative medicine and treatment options in development, including a gene-therapy candidate by Ultragenyx Pharmaceutical Inc., a generic taste-masked formulation option of sodium phenylbutyrate by ACER Therapeutics Inc., an enzyme replacement for a specific UCD subtype (ARG) by Aeglea Bio Therapeutics Inc., and a mRNA-based therapeutic for a specific UCD subtype (OTC) by Arcturus Therapeutics Holdings Inc. If successful, these medicine and treatment option candidates could compete with RAVICTI.

Our strategy for RAVICTI is to drive growth through increased awareness and diagnosis of UCDs; to drive conversion to RAVICTI from older-generation nitrogen scavengers, such as generic forms of sodium phenylbutyrate, based on the medicine’s differentiated benefits; to position RAVICTI as the first line of therapy; and to increase compliance rates.

In December 2018 and October 2020, we sold our rights to develop and commercialize RAVICTI outside of North America to Immedica. We previously distributed RAVICTI through a commercial partner in Europe and other non-U.S. markets. We have retained rights to RAVICTI in North America.

PROCYSBI

PROCYSBI is indicated for nephropathic cystinosis, or NC, a rare lysosomal storage disorder that results in the amino acid cystine accumulating inside the lysosomes of nearly every cell. Cystine accumulation results in the formation of crystals that lead to cell damage and death in tissues and organs throughout the body. PROCYSBI (cysteamine bitartrate) delayed-release capsules and delayed-release oral granules is the first and only FDA-approved treatment for NC with 12-hour dosing. PROCYSBI uses proprietary technology that releases cysteamine gradually, providing 12-hour continuous cystine control in adults and children 1 year of age and older. PROCYSBI granules, also called “microbeads,” are composed of cysteamine bitartrate surrounded by an acid-resistant enteric coating. To work properly, PROCYSBI microbeads must dissolve and release cysteamine bitartrate in the small intestine. The coating on the microbeads helps to control where and how medicine is released by allowing the cysteamine bitartrate to pass through the acidic stomach to the alkaline environment of the small intestine. Once in the small intestine, the coating begins to dissolve and the microbeads release cysteamine bitartrate gradually. This allows PROCYSBI to control cystine levels continuously over the dosing interval. Randomized controlled clinical trials and extended treatment with PROCYSBI therapy demonstrated consistent cystine depletion as monitored by levels of the biomarker (and surrogate marker), white blood cell cystine concentration.

In NC patients, elevated cystine can lead to cellular dysfunction and death; without treatment, the disease is usually fatal by the end of the first decade of life. Cystinosis is progressive, eventually causing irreversible tissue damage and multi-organ failure, including kidney failure, blindness, muscle wasting and premature death. NC is usually diagnosed in infancy after children display symptoms to physicians, including markedly increased urination, thirst, dehydration, gastrointestinal distress, failure to thrive, rickets, photophobia and kidney symptoms specific to Fanconi syndrome. Management of cystinosis requires lifelong therapy.

In February 2020, the FDA approved PROCYSBI Delayed-Release Oral Granules in Packets for adults and children one year of age and older living with nephropathic cystinosis. The PROCYSBI Delayed-Release Oral Granules in Packets product is the same as the PROCYSBI capsules product except in respect of the packaging format. This granules in packets dosage form provides another administration option for patients, in addition to the PROCYSBI capsules. PROCYSBI Delayed-Release Oral Granules in Packets were made commercially available in April 2020.

9

PROCYSBI is differentiated by its ability to control cystine concentration continuously over twelve hours. Older therapies require administration of medicine every six hours. By taking PROCYSBI, patients have to dose only twice a day, providing them greater control over their medication schedule and lifestyle. Additionally, because PROCYSBI can be administered through a feeding tube or mixed with approved foods and liquids, the patient can choose a more flexible dosing regimen. PROCYSBI may also have fewer known side effects, such as less severe bad breath (halitosis) and body odor, than older-generation therapies.

We estimate that there are approximately 500-550 patients diagnosed with NC living in the United States. In addition to patients who have already been identified, we believe that a number of patients with atypical phenotypic presentation and end-stage renal disease have their condition as a result of undiagnosed late-onset NC and would benefit from treatment with PROCYSBI.

Other than PROCYSBI, three pharmaceutical products are currently approved to treat cystinosis, Cystagon®, Cystadrops® and Cystaran®. Cystagon, an immediate-release cysteamine bitartrate capsule, is an older-generation systemic cystine-depleting therapy for cystinosis in the United States marketed by Mylan N.V., and by Orphan Europe SARL in markets outside of the United States. Cystagon is PROCYSBI’s primary competitor. Cystadrops is a recently approved (2020) cysteamine ophthalmic solution indicated for the treatment of corneal cystine crystal deposits and is marketed by Recordati Rare Disease Inc. Cystaran, a cysteamine ophthalmic solution, is approved in the United States for treatment of corneal crystal accumulation in patients with cystinosis and is marketed by Leadiant Biosciences, Inc. Additionally, we are aware of an early-stage gene therapy candidate in development by AVROBIO, Inc. for the treatment of cystinosis. We believe that PROCYSBI will continue to be well received in the market and continue to expect Cystagon to be the primary competitor for PROCYSBI for the foreseeable future.

Our strategy for PROCYSBI is to drive conversion of patients from older-generation immediate-release capsules of cysteamine bitartrate; to increase the uptake of the medicine by diagnosed but untreated patients; to position PROCYSBI as a first line of therapy; and to increase compliance rates.

ACTIMMUNE

ACTIMMUNE is indicated for chronic granulomatous disease, or CGD, and severe, malignant osteopetrosis, or SMO. It is a biologically manufactured protein called interferon gamma-1b that is similar to a protein the human body makes naturally. Interferon gamma helps prevent infection in CGD patients and enhances osteoclast function in SMO patients. ACTIMMUNE is the only medicine approved by the FDA to reduce the frequency and severity of serious infections associated with CGD and for delaying disease progression in patients with SMO. ACTIMMUNE is believed to work by modifying the cellular function of various cells, including those in the immune system and those that help form bones.

CGD is a genetic disorder of the immune system. It is described as a primary immunodeficiency disorder, which means it is not caused by another disease or disorder. In people who have CGD, a type of white blood cell called a phagocyte is defective. These defective phagocytes cannot generate superoxide, leading to an inability to kill harmful microorganisms such as bacteria and fungi. As a result, the immune system is weakened. People with CGD are more likely to have certain problems, such as recurrent severe and potentially life-threatening bacterial and fungal infections and chronic inflammatory conditions. These patients are prone to developing masses called granulomas, which can occur repeatedly in organs throughout the body and cause a variety of problems. We estimate that there are approximately 1,200 patients with CGD in the United States, based on an estimated incidence of 1:200,000 live births.

SMO is a form of osteopetrosis and is sometimes referred to as marble bone disease or malignant infantile osteopetrosis because it occurs in very young children. While exact numbers are not known, it has been estimated that one out of 250,000 children are born with SMO.

ACTIMMUNE currently faces limited competition. There are additional or alternative approaches used to treat patients with CGD and SMO, including the increasing trend towards the use of bone marrow transplants in patients with CGD, however, there are currently no medicines on the market that compete directly with ACTIMMUNE. Orchard Therapeutics plc has an early-stage ex-vivo autologous hematopoietic stem cell gene therapy candidate in development for the treatment of X-linked chronic granulomatous disease.

10

Our strategy for ACTIMMUNE is to increase awareness and diagnosis of CGD; to drive utilization of ACTIMMUNE prophylaxis in newly-diagnosed CGD patients as recommended in current treatment guidelines; encourage use of ACTIMMUNE in CGD patients prior to bone marrow transplant and in symptomatic carriers of x-linked CGD; and increase compliance rates overall.

UPLIZNA

UPLIZNA is a humanized monoclonal antibody that works by binding to CD19, a cell-surface molecule broadly expressed on the surface of B cells, including plasmablasts and some plasma cells. In some autoimmune diseases, autoantibodies secreted by plasmablasts and plasma cells attack native tissues as opposed to foreign pathogens. UPLIZNA depletes these plasmablasts that may produce pathogenic autoantibodies. UPLIZNA was approved for the treatment of NMOSD by the FDA in June 2020 and by the Japanese Ministry of Health, Labour and Welfare in March 2021.

NMOSD is a rare, severe autoimmune disease in which autoantibodies produced by B cells attack the optic nerve, spinal cord and brain/brainstem, often causing permanent blindness, weakness, and/or paralysis. NMOSD is characterized by unpredictable attacks and severe disability that often occurs following the first attack, accumulating with each subsequent relapse. Thus, preventing these attacks is the primary goal for disease management. NMOSD is often misdiagnosed as multiple sclerosis, or MS, which can be problematic since some MS treatments may exacerbate NMOSD. UPLIZNA is an infused medicine that works by depleting B-cells in a targeted manner and is proven to reduce NMOSD attacks.

In Japan, our strategic partner, MTPC has the rights for development and commercialization of UPLIZNA. UPLIZNA was launched in Japan during the second quarter of 2021. In November 2021, we announced that the Committee for Medicinal Products for Human Use of the European Medicines Agency, or EMA, adopted a positive opinion recommending grant of a Centralised Marketing Authorisation, or CMA, for UPLIZNA as a monotherapy for the treatment of adult patients with NMOSD who are anti-aquaporin-4 immunoglobulin G seropositive (AQP4-IgG+). While the Committee for Orphan Medicinal Products did not recommend maintenance of the orphan designation for UPLIZNA following its review, we are continuing to invest in our European infrastructure to support a potential European launch of UPLIZNA for NMOSD, which we anticipate would begin with Germany in the second quarter of 2022, assuming the grant of a CMA by the European Commission, or EC. If granted, the CMA would be valid throughout the European Economic Area (which consists of the Member States of the European Union, Iceland, Liechtenstein and Norway).

UPLIZNA is the only approved NMOSD therapy in the United States that has demonstrated a clinically relevant and durable effect on delaying worsening of disability, with a significant reduction in hospitalization. Long-term UPLIZNA treatment has been shown to be well tolerated and provide a sustained reduction in NMOSD attack risk for four or more years. UPLIZNA faces competition from eculizumab, marketed as Soliris® by AstraZeneca plc, and satralizumab, marketed as EnspryngTM by Chugai Pharmaceuticals Co., Ltd., a subsidiary of F. Hoffmann-La Roche Ltd., each for the treatment of patients with NMOSD. AstraZeneca is also conducting a Phase 3 trial with Ultomiris® (ravulizumab) in NMOSD and, if approved for this indication, UPLIZNA could face additional competition. UPLIZNA also faces competition from rituximab, an off-label treatment that has been used for years to treat NMOSD given the lack of an approved medicine for this disease prior to 2019.

With respect to our strategy for UPLIZNA, which leverages the successful strategies we have employed with TEPEZZA and KRYSTEXXA, our aim is to (i) increase physician awareness of the benefits of UPLIZNA for the treatment of NMOSD, and what differentiates UPLIZNA from other medicines by generating additional trial data analyses and clinical evidence; (ii) drive patient initiation and adherence, and cultivate a positive patient experience; and (iii) maximize the potential of UPLIZNA through additional indications and global expansion.

11

BUPHENYL

BUPHENYL tablets and BUPHENYL powder are made from granules that contain sodium phenylbutyrate as the active (chemically synthesized) ingredient and microcrystalline cellulose as a diluent.

BUPHENYL tablets for oral administration and BUPHENYL powder for oral, nasogastric, or gastrostomy tube administration are indicated as adjunctive therapy in the chronic management of patients with UCDs involving deficiencies of carbamoyl phosphate synthetase, ornithine transcarbamylase or argininosuccinic acid synthetase.

BUPHENYL is indicated for treatment of all patients with neonatal-onset deficiency (complete enzymatic deficiency, presenting within the first twenty-eight days of life). It is also indicated for treatment of patients with late-onset disease (partial enzymatic deficiency, presenting after the first month of life) who have a history of hyperammonemic encephalopathy. It is important that the diagnosis be made early and treatment initiated immediately to improve clinical outcomes. BUPHENYL must be combined with dietary protein restriction and, in some cases, essential amino acid supplementation. We distribute BUPHENYL in the United States.

QUINSAIR

QUINSAIR is a formulation of the antibiotic drug levofloxacin, suitable for inhalation via a nebulizer and indicated for the management of chronic pulmonary infections due to Pseudomonas aeruginosa in adult patients with cystic fibrosis, or CF. CF is a rare, life-threatening genetic disease affecting approximately 70,000 people worldwide, and results in build-up of abnormally thick secretions that can cause chronic lung infections and progressive lung damage in many patients that eventually leads to death.

INFLAMMATION SEGMENT

Our inflammation segment includes PENNSAID 2% w/w, or PENNSAID 2%, DUEXIS, RAYOS and VIMOVO.

PENNSAID 2%

PENNSAID 2% is indicated for the treatment of pain of osteoarthritis, or OA, of the knee(s). OA is a type of arthritis that is caused by the breakdown and eventual loss of the cartilage of one or more joints.

An analgesic that is easy-to-apply topically directly to the knee, PENNSAID 2% contains diclofenac sodium, a commonly prescribed nonsteroidal anti-inflammatory drug, or NSAID, to treat OA pain, and dimethyl sulfoxide, a penetrating agent that helps ensure that diclofenac sodium is absorbed through the skin to the site of inflammation and pain. Topical NSAIDs such as PENNSAID 2% are generally viewed as safer alternatives to oral NSAID treatment because they reduce systemic exposure to a fraction of that of an oral NSAID. PENNSAID 2% is the only topical NSAID offered with the convenience of a metered-dose pump, which ensures that the patient receives the correct amount of PENNSAID 2% solution with each use. PENNSAID 2% competes primarily with the generic version of Voltaren Gel 1%, a market leader in the topical NSAID category.

DUEXIS

DUEXIS is indicated for the relief of signs and symptoms of rheumatoid arthritis, or RA, and OA and to decrease the risk of developing upper-gastrointestinal, or upper-GI, ulcers in patients who are taking ibuprofen for these indications. RA is a chronic disease that causes pain, stiffness and swelling, primarily in the joints.

DUEXIS provides a fixed-dose combination in tablet form of ibuprofen, the most widely prescribed NSAID, and famotidine, a well-established upper-GI agent used to treat dyspepsia, gastroesophageal reflux disease and active ulcers.

Fixed-dose combination therapy provides significant advantages over multiple-pill regimens: fixed-dose combinations can reduce the number of pills taken; ensure that the correct dose of each component is taken at the correct time, improving compliance; and is often associated with better treatment outcomes.

12

In general, DUEXIS faces competition from the separate use of NSAIDs for pain relief and upper-GI medications to address the risk of NSAID-induced ulcers. However, the prescribing information for DUEXIS states that DUEXIS should not be substituted with the single-ingredient products of ibuprofen and famotidine. DUEXIS competes with other NSAIDs, including Celebrex®, manufactured by Pfizer Inc., and celecoxib, a generic form of the medicine supplied by other pharmaceutical companies. DUEXIS also competes with TIVORBEX™ (indomethacin) capsules, VIVLODEX® (meloxicam) capsules and ZORVOLEX ® (diclofenac) capsules marketed by Iroko Pharmaceuticals, LLC.

On August 4, 2021, following a judgment in the District Court of Delaware, which was subsequently affirmed by the Federal Circuit Court of Appeals on November 16, 2021, Alkem Laboratories, Inc., or Alkem, launched a generic version of DUEXIS in the United States. As a result, we have repositioned our promotional efforts previously directed to DUEXIS to the other inflammation segment medicines and expect that our DUEXIS net sales will continue to decrease in future periods.

RAYOS

RAYOS is a corticosteroid indicated for the treatment of multiple conditions: RA; ankylosing spondylitis, or AS; polymyalgia rheumatica, or PMR; systemic lupus erythematosus, or SLE; and a number of other conditions. We focus our promotion of RAYOS on rheumatology indications, including RA and PMR.

RAYOS is composed of an active core containing prednisone that is encapsulated by an inactive porous shell, and acts as a barrier between the medicine’s active core and the patient’s gastrointestinal, or GI, fluids. RAYOS was developed using Vectura’s proprietary GeoClock™ and GeoMatrix™ technologies, for which we hold an exclusive U.S. license for the delivery of glucocorticoid, a class of corticosteroid. The delivery system enables a delayed release, synchronizing the prednisone delivery time with the patient’s elevated cytokine levels, thereby taking effect at a physiologically optimal point to inhibit cytokine production, and thus significantly reducing the signs and symptoms of RA and PMR.

RA is a chronic disease that causes pain, stiffness and swelling, primarily in the joints; PMR is an inflammatory disorder that causes significant muscle pain and stiffness; SLE is a chronic autoimmune disease that primarily affects women and causes inflammation and pain in the joints and muscles as well as overall fatigue.

RAYOS competes with a number of medicines in the market to treat RA, including corticosteroids, such as prednisone; traditional disease-modifying anti-rheumatic drugs, or DMARDs, such as methotrexate; and biologic agents, such as Humira and Enbrel. The majority of RA patients are treated with DMARDs, which are typically used as initial therapy in patients with RA. Biologic agents are typically added to DMARDs as combination therapy. It is common for an RA patient to take a combination of a DMARD, an oral corticosteroid, a NSAID and/or a biologic agent. We have an exclusive license to U.S. patents and patent applications from Vectura covering RAYOS. Under our settlement agreement with Teva Pharmaceuticals Industries Limited (formerly known as Actavis Laboratories FL, Inc., which itself was formerly known as Watson Laboratories, Inc. – Florida), or Teva, Teva may enter the market on December 23, 2022, or earlier under certain circumstances. As a result, we expect our net sales for RAYOS to decline in future periods.

Outside the United States, RAYOS is sold and marketed as LODOTRA. Effective January 1, 2019, we amended our license and supply agreements with Jagotec AG and Skyepharma AG, which are affiliates of Vectura. Under these amendments, our rights to LODOTRA in Europe were transferred to Vectura. We ceased recording LODOTRA revenue from January 1, 2019. See “Manufacturing, Commercial, Supply and License Agreements” below for further details of the amendments.

13

VIMOVO

VIMOVO is indicated for the relief of signs and symptoms of OA, RA and AS and to decrease the risk of developing gastric ulcers in patients at risk of developing NSAID-associated gastric ulcers. It is a proprietary, fixed-dose, delayed-release tablet that combines enteric-coated naproxen, an NSAID, surrounded by a layer of immediate-release esomeprazole magnesium. Naproxen has proven anti-inflammatory and analgesic properties, and esomeprazole magnesium reduces the stomach acid secretions that can cause upper-GI ulcers. Both naproxen and esomeprazole magnesium have well-documented and excellent long-term safety profiles, and both medicines have been used by millions of patients worldwide. VIMOVO has been shown to decrease the risk of developing gastric ulcers in patients at risk of developing NSAID associated gastric ulcers.

On February 27, 2020, following a judgment in federal court invalidating certain patents covering VIMOVO, Dr. Reddy’s Laboratories Inc. and Dr. Reddy’s Laboratories Ltd, or collectively, Dr. Reddy’s, launched a generic version of VIMOVO in the United States. While patent litigation against Dr. Reddy’s for infringement continues on additional patents in the New Jersey District Court, we now face generic competition for VIMOVO, which has negatively impacted net sales of VIMOVO. As a result, we have repositioned our promotional efforts previously directed to VIMOVO to the other inflammation segment medicines and expect that our VIMOVO net sales will continue to decrease in future periods.

In addition, similar to DUEXIS, VIMOVO faces competition from the separate use of NSAIDs for pain relief and GI medications to address the risk of NSAID-induced ulcers. However, the prescribing information for VIMOVO states that VIMOVO should not be substituted with the single-ingredient products of naproxen and esomeprazole magnesium. In addition to the generic version of VIMOVO launched by Dr. Reddy’s, VIMOVO also competes with other NSAIDs, including Celebrex, TIVORBEX, VIVLODEX and ZORVOLEX.

14

Research and Development

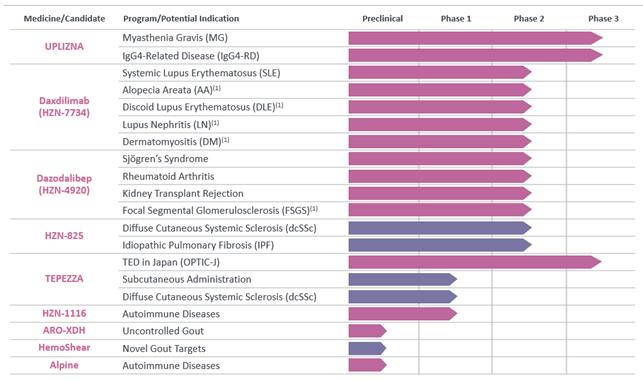

Our R&D programs include preclinical and clinical development of new medicine candidates, as well as development programs intended to maximize the benefit and value of our existing medicines. We devote significant resources to R&D activities that address critical unmet medical needs for people impacted by rare, autoimmune and severe inflammatory diseases. Our pipeline includes more than 20 programs, the majority of which were added in 2021. We initiated seven clinical trials in 2021 and expect to initiate seven more in 2022, including the HZN-825 IPF clinical trial initiated in January 2022 and the TEPEZZA in Japan (OPTIC-J) clinical trial initiated in February 2022. The graphic below summarizes our R&D programs ranging from preclinical to Phase 3 as of March 1, 2022.

|

|

|

|

(1) Program expected to initiate in 2022. |

|

We also have four Phase 4 programs: TEPEZZA chronic TED, KRYSTEXXA shorter infusion duration, KRYSTEXXA monthly dosing and KRYSTEXXA retreatment.

UPLIZNA Clinical Programs

UPLIZNA (inebilizumab-cdon) is an anti-CD19 humanized monoclonal antibody that depletes B cells, including the pathogenic cells that produce autoantibodies. UPLIZNA is approved by the FDA for the treatment of NMOSD. We are currently evaluating UPLIZNA in three additional indications: myasthenia gravis (a Phase 3 randomized, placebo-controlled clinical trial) and IgG4-related disease (a Phase 3 randomized, placebo-controlled clinical trial).

Daxdilimab (HZN-7734) Clinical Programs

Daxdilimab, or HZN-7734, is an anti-ILT7 human monoclonal antibody that depletes certain dendritic cells. Depleting these cells may interrupt the cycle of inflammation that causes tissue damage in diseases such as lupus, and a variety of other autoimmune conditions. We are currently evaluating daxdilimab in a Phase 2 randomized, placebo-controlled clinical trial in systemic lupus erythematosus. We expect to initiate four Phase 2 clinical trials in additional potential indications in 2022 – alopecia areata, discoid lupus erythematosus, lupus nephritis and dermatomyositis.

15

Dazodalibep (HZN-4920) Clinical Programs

Dazodalibep, or HZN-4920, is a CD40 ligand antagonist that blocks T cell interaction with the CD40-expressing B cells, disrupting the overactivation of the CD40 ligand co-stimulatory pathway. Several autoimmune diseases are associated with the overactivation of this pathway. Clinical trials in three indications are currently underway: a Phase 2b randomized, placebo-controlled clinical trial in Sjögren’s syndrome, a Phase 2 randomized, placebo-controlled clinical trial in rheumatoid arthritis and a Phase 2 open-label clinical trial in kidney transplant rejection. We expect to initiate a Phase 2 clinical trial in focal segmental glomerulosclerosis in 2022.

HZN-825 Clinical Programs

HZN-825 is an oral selective LPAR1 antagonist that prevents gene activation and has demonstrated antifibrotic activity. We are pursuing Phase 2b pivotal trials of HZN-825 in two potential indications – diffuse cutaneous systemic sclerosis and idiopathic pulmonary fibrosis.

TEPEZZA Clinical Programs

TEPEZZA (teprotumumab-trbw) is an IGF-1R antagonist monoclonal antibody. It is the first and only medicine approved by the FDA for the treatment of TED. Two of our three TEPEZZA clinical programs are underway: a Phase 1 pharmacokinetic clinical trial for subcutaneous administration of TED and a Phase 1 exploratory clinical trial in diffuse cutaneous systemic sclerosis. OPTIC-J, a Phase 3 randomized, placebo-controlled clinical trial for the treatment of moderate-to-severe active TED patients in Japan, was initiated in February 2022.

HZN-1116 Autoimmune Disease Program

HZN-1116 is a human monoclonal antibody designed to neutralize the FLT3-ligand, thereby reducing both conventional and plasmacytoid dendritic cells that play a key role in driving inflammatory processes. We are currently evaluating HZN-1116 in a Phase 1 clinical trial for autoimmune diseases.

Preclinical Programs

Our agreements with Arrowhead Pharmaceuticals, Inc., or Arrowhead, and HemoShear Therapeutics, LLC are both exploring the potential for novel therapeutics to address the unmet need for the more than 500,000 gout patients who do not respond to the current standard of conventional care and are not good candidates for KRYSTEXXA. Our preclinical program with Alpine Immune Sciences, Inc., or Alpine, is focused on developing novel protein-based therapies for autoimmune and inflammatory diseases. We are leveraging external collaborations for our three programs, using their specialized technologies in combination with our internal expertise.

Phase 4 TEPEZZA and KRYSTEXXA Programs

Additional programs not shown on the pipeline above include our Phase 4 TEPEZZA and KRYSTEXXA programs. Our ongoing TEPEZZA Phase 4 randomized, placebo-controlled clinical trial in chronic TED is designed to better inform physicians and payers on the safety and efficacy of TEPEZZA in patients with chronic TED. Our three Phase 4 KRYSTEXXA open-label clinical trials underway are evaluating KRYSTEXXA plus the immunomodulator methotrexate in a shorter-infusion duration trial; a monthly dosing trial; and a retreatment trial for patients who were not complete responders to KRYSTEXXA monotherapy.

Clinical Programs Completed in 2021

In 2021, we successfully completed two KRYSTEXXA clinical trials, MIRROR and PROTECT:

KRYSTEXXA MIRROR: Our Phase 4 randomized, placebo-controlled MIRROR clinical trial evaluated the use of KRYSTEXXA plus methotrexate, an immunomodulator frequently used by rheumatologists. The trial results demonstrated that 71.0 percent (71 of 100) patients randomized to receive KRYSTEXXA plus methotrexate achieved a complete response rate, defined as serum uric acid <6 mg/dL at least 80% of the time during Month 6 (p<0.0001), a significant improvement from the 38.5 percent response rate in patients (20 of 52) who were randomized to receive KRYSTEXXA plus placebo. KRYSTEXXA plus immunomodulation is a core element of our strategy to maximize the value of KRYSTEXXA and enable more patients with uncontrolled gout to benefit from the medicine. We submitted a supplemental biologics license application to the FDA in the first quarter of 2022 to expand the label for KRYSTEXXA to include co-treatment with methotrexate.

16

KRYSTEXXA PROTECT: Our Phase 4 open-label PROTECT clinical trial evaluated the use of KRYSTEXXA in patients with uncontrolled gout who had received a kidney transplant and were treated with two to three immunosuppressive agents to prevent organ rejection. Gout is more common and often more severe among patients who have undergone kidney transplantation. 88.9 percent (16 of 18) of the patients achieved the primary endpoint, defined as sUA <6 mg/dL for at least 80 percent of time during Month 6, demonstrating that KRYSTEXXA provided a substantial and sustained decrease in sUA for these patients.

Distribution

We use central third-party logistics and FDA-compliant warehouses for storage and distribution of our medicines into the supply chain. Our third-party logistics provider specializes in integrated operations that include warehousing and transportation services that can be scaled and customized to our needs based on market conditions and the demands and delivery service requirements for our medicines and materials. Their services eliminate the need to build dedicated internal infrastructures that would be difficult to scale without significant capital investment. Our third-party logistics provider warehouses all medicines in controlled FDA-registered facilities. Incoming orders are prepared and shipped through an order entry system to ensure adequate supply and delivery of our medicines.

Sales and Marketing

As of December 31, 2021, our sales force was composed of approximately 480 sales representatives consisting of approximately 280 orphan sales representatives and 200 inflammation sales representatives.

Our orphan sales representatives focus on marketing our rare disease medicines to a limited number of healthcare practitioners who specialize in fields such as pediatric immunology, allergy, infectious diseases, metabolic disorders, rheumatology, nephrology, ophthalmology and endocrinology, to help them understand the potential benefits of our medicines. We have entered into, and may continue to enter into, agreements with third parties to commercialize our medicines outside the United States.

We offer discount card and other programs such as our HorizonCares program to patients under which the patient receives a discount on his or her prescription. In certain circumstances when a patient’s prescription is rejected by a managed care vendor, we will pay for the full cost of the prescription. Patients are able to fill prescriptions for our inflammation medicines through pharmacies participating in our HorizonCares patient assistance program, as well as other pharmacies. In addition, we have business arrangements with pharmacy benefit managers, or PBMs, and other payers to secure formulary status and reimbursement of our inflammation medicines. The business arrangements with the PBMs generally require us to pay administrative fees and rebates to the PBMs and other payers for qualifying prescriptions.

We have a comprehensive compliance program in place to address adherence with various laws and regulations relating to our sales, marketing, and manufacturing of our medicines, as well as certain third-party relationships, including pharmacies. Specifically with respect to pharmacies, the compliance program utilizes a variety of methods and tools to monitor and audit pharmacies, including those that participate in our patient assistance programs, to confirm their activities, adjudication and practices are consistent with our compliance policies and guidance.

17

Manufacturing, Commercial, Supply and License Agreements

We have agreements with third parties for active pharmaceutical ingredients, or APIs, biological drug substance, manufacture of our medicines, formulation and development services. We also have agreements for fill, finish and packaging services, transportation, and distribution and logistics services for certain medicines. In all cases, we retain certain levels of safety stock or maintain alternate supply relationships that we can utilize without undue disruption of our manufacturing processes if a third party fails to perform its contractual obligations.

In July 2021, we purchased a biologic drug product manufacturing facility in Waterford, Ireland, which is intended to be an additional source of manufacturing to supplement the capabilities of our third-party drug product manufacturers. We are in the process of completing the build-out and validation of this facility and assuming timely receipt of regulatory approvals, we expect that the first medicine manufactured at the facility to be approved for release in 2023.

TEPEZZA