INTEL CORP - Quarter Report: 2018 September (Form 10-Q)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

þ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the quarterly period ended September 29, 2018. | ||

Or

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from to | ||

Commission File Number 000-06217

INTEL CORPORATION

(Exact name of registrant as specified in its charter)

Delaware | 94-1672743 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

2200 Mission College Boulevard, Santa Clara, California | 95054-1549 | |

(Address of principal executive offices) | (Zip Code) | |

(408) 765-8080

(Registrant’s telephone number, including area code)

N/A

(Former name, former address and former fiscal year, if changed since last report)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer þ | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ | Emerging growth company ¨ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

Shares outstanding of the Registrant’s common stock:

Class | Outstanding as of September 29, 2018 | |

Common stock, $0.001 par value | 4,564 million | |

TABLE OF CONTENTS

THE ORGANIZATION OF OUR QUARTERLY REPORT ON FORM 10-Q

The order and presentation of content in our Quarterly Report on Form 10-Q (Form 10-Q) differs from the traditional U.S. Securities and Exchange Commission (SEC) Form 10-Q format. We believe this format improves readability and better presents how we organize and manage our business. See "Form 10-Q Cross-Reference Index" within Other Key Information for a cross-reference index to the traditional SEC Form 10-Q format.

We have included key metrics that we use to measure our business, some of which are non-GAAP measures. See these "Non-GAAP Financial Measures" within Other Key Information.

Page | |||

FORWARD-LOOKING STATEMENTS | |||

A QUARTER IN REVIEW | |||

CONSOLIDATED CONDENSED FINANCIAL STATEMENTS AND SUPPLEMENTAL DETAILS | |||

Consolidated Condensed Statements of Income | |||

Consolidated Condensed Statements of Comprehensive Income | |||

Consolidated Condensed Balance Sheets | |||

Consolidated Condensed Statements of Cash Flows | |||

Notes to Consolidated Condensed Financial Statements | |||

MANAGEMENT'S DISCUSSION AND ANALYSIS (MD&A) - RESULTS OF OPERATIONS | |||

Overview | |||

Revenue, Gross Margin, and Operating Expenses | |||

Business Unit Trends and Results | |||

Other Consolidated Results of Operations | |||

Liquidity and Capital Resources | |||

Quantitative and Qualitative Disclosures about Market Risk | |||

OTHER KEY INFORMATION | |||

Risk Factors | |||

Controls and Procedures | |||

Non-GAAP Financial Measures | |||

Issuer Purchases of Equity Securities | |||

Exhibits | |||

Form 10-Q Cross-Reference Index | |||

FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q contains forward-looking statements that involve a number of risks and uncertainties. Words such as "anticipates," "expects," "intends," "goals," "plans," "believes," "seeks," "estimates," "continues," "may," "will," "would," "should," "could," and variations of such words and similar expressions are intended to identify such forward-looking statements. In addition, any statements that refer to projections of our future financial performance, our anticipated growth and trends in our businesses, projected growth of markets relevant to our businesses, uncertain events or assumptions, and other characterizations of future events or circumstances are forward-looking statements. Such statements are based on management's expectations as of the date of this filing and involve many risks and uncertainties that could cause our actual results to differ materially from those expressed or implied in our forward-looking statements. Such risks and uncertainties include those described throughout this report and our Annual Report on Form 10-K for the year ended December 30, 2017, particularly the "Risk Factors" sections of such reports. Given these risks and uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements. Readers are urged to carefully review and consider the various disclosures made in this Form 10-Q and in other documents we file from time to time with the Securities and Exchange Commission that disclose risks and uncertainties that may affect our business. The forward-looking statements in this Form 10-Q do not reflect the potential impact of any divestitures, mergers, acquisitions, or other business combinations that had not been completed as of the date of this filing. In addition, the forward-looking statements in this Form 10-Q are made as of the date of this filing, including expectations based on third-party information and projections that management believes to be reputable, and Intel does not undertake, and expressly disclaims any duty, to update such statements, whether as a result of new information, new developments or otherwise, except to the extent that disclosure may be required by law.

INTEL UNIQUE TERMS

We use specific terms throughout this document to describe our business and results. Below are key terms and how we define them:

PLATFORM PRODUCTS | A microprocessor (processor or central processing unit (CPU)) and chipset, a stand-alone System-on-Chip (SoC), or a multichip package. Platform products, or platforms, are primarily used in solutions sold through Client Computing Group (CCG), Data Center Group (DCG), and Internet of Things Group (IOTG) segments. | |

ADJACENT PRODUCTS | All of our non-platform products, for CCG, DCG, and IOTG like modem, ethernet and silicon photonics, as well as Non-Volatile Memory Solutions Group (NSG), Programmable Solutions Group (PSG), and Mobileye products. Combined with our platform products, adjacent products form comprehensive platform solutions to meet customer needs. | |

PC-CENTRIC BUSINESS | Is made up of our CCG business, both platform and adjacent products. | |

DATA-CENTRIC BUSINESSES | Includes our DCG, IOTG, NSG, PSG, and all other businesses, which includes Mobileye | |

Intel, the Intel logo, Intel Inside, Intel Optane, Intel Core, Xeon, and 3D XPoint are trademarks of Intel Corporation or its subsidiaries in the U.S. and/or other countries.

*Other names and brands may be claimed as the property of others.

1 | ||

A QUARTER IN REVIEW |

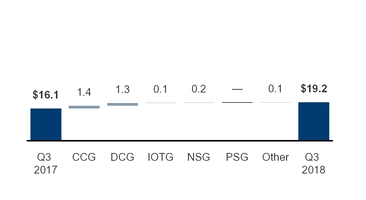

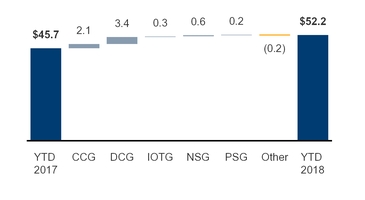

The third quarter was a record quarter in revenue, operating income, and net income, driven by strong customer demand for the performance of our leadership products across the business. Data Center Group (DCG), Client Computing Group (CCG), Internet of Things Group (IOTG), Non-Volatile Memory Solutions Group (NSG), and Mobileye each achieved record revenue. Strong business performance, operating margin leverage, and lower tax rate resulted in net income of $6.4 billion in the third quarter. From a capital allocation perspective, in the first nine months we generated $22.5 billion of cash flow from operations and returned $12.6 billion to shareholders, including $4.2 billion in dividends and $8.5 billion in buybacks.

REVENUE | OPERATING INCOME | DILUTED EPS | ||||||||

$19.2B | $7.3B | $7.6B | $1.38 | $1.40 | ||||||

GAAP | GAAP | non-GAAP1 | GAAP | non-GAAP1 | ||||||

up $3.0B or 19% from Q3 2017 | up $2.2B or 43% from Q3 2017 | up $2.0B or 36% from Q3 2017 | up $0.44 or 47% from Q3 2017 | up $0.39 or 39% from Q3 2017 | ||||||

Strong performance across all businesses and record revenue from DCG, CCG, IOTG, NSG, and Mobileye | Demand for leadership product and continued operating margin leverage while investing in key opportunities such as artificial intelligence and autonomous driving | Growing demand for higher performance products, growth in adjacent businesses, lower tax rate, and lower share outstanding | ||||||||

■ Data-centric $B | ■ PC-centric $B | ■ GAAP $B | ■ Non-GAAP $B | ■ GAAP | ■ Non-GAAP | |||||

BUSINESS SUMMARY

• | Five years ago, we set a course to transform to a data-centric company. Today our strategy, products, and employees are delivering on that ambition with strong growth, record results, and new opportunities. We are gaining share in an expanded total addressable market (TAM) opportunity, which is now expected to be over $300 billion2 as our transformation accelerates. |

• | Our data-centric businesses collectively grew 22% led by the growth in the cloud and communication service provider market segments. To extend the growth momentum, we are now shipping Intel® Optane™ data center persistent memory, which combines the speed of traditional memory with the capacity and native persistence of storage. |

• | Our focus on performance leadership and differentiation in client computing is producing outstanding results. In addition, we expect modest PC TAM2 growth this year and continued share gain in modems. To extend product leadership and to deliver more value to customers, we launched new 9th Gen Intel® Core™ processors, targeting the growing gaming market segment. |

• | The return to PC TAM growth put pressure on our factory network. In addition to prioritizing production to serve server and high-performance PC market segments, we are investing additional capital expenditure to increase our supply, working with customers to align demand with available supply, and making good progress to improve 10nm yields. |

• | 30 years ago, in September, 1988, Gordon Moore helped establish the Intel Foundation, a public charity funded by our company. From investing in science, technology, engineering, and mathematics (STEM) programs, providing disaster relief, and amplifying the philanthropy of Intel employees, the Intel Foundation has been committed to improving lives around the world. |

1 See "Non-GAAP Financial Measures" within Other Key Information.

2 Source: Intel calculated 2022 TAM and current year PC TAM derived from industry analyst reports and internal estimates.

A QUARTER IN REVIEW | 2 | |

INTEL CORPORATION CONSOLIDATED CONDENSED STATEMENTS OF INCOME |

Three Months Ended | Nine Months Ended | |||||||||||||||

(In Millions, Except Per Share Amounts; Unaudited) | Sep 29, 2018 | Sep 30, 2017 | Sep 29, 2018 | Sep 30, 2017 | ||||||||||||

Net revenue | $ | 19,163 | $ | 16,149 | $ | 52,191 | $ | 45,708 | ||||||||

Cost of sales | 6,803 | 6,085 | 19,681 | 17,388 | ||||||||||||

Gross margin | 12,360 | 10,064 | 32,510 | 28,320 | ||||||||||||

Research and development | 3,428 | 3,209 | 10,110 | 9,782 | ||||||||||||

Marketing, general and administrative | 1,605 | 1,661 | 5,230 | 5,610 | ||||||||||||

Restructuring and other charges | (72 | ) | 4 | (72 | ) | 189 | ||||||||||

Amortization of acquisition-related intangibles | 50 | 49 | 150 | 124 | ||||||||||||

Operating expenses | 5,011 | 4,923 | 15,418 | 15,705 | ||||||||||||

Operating income | 7,349 | 5,141 | 17,092 | 12,615 | ||||||||||||

Gains (losses) on equity investments, net | (75 | ) | 846 | 365 | 1,440 | |||||||||||

Interest and other, net | (132 | ) | (57 | ) | 225 | 262 | ||||||||||

Income before taxes | 7,142 | 5,930 | 17,682 | 14,317 | ||||||||||||

Provision for taxes | 744 | 1,414 | 1,824 | 4,029 | ||||||||||||

Net income | $ | 6,398 | $ | 4,516 | $ | 15,858 | $ | 10,288 | ||||||||

Earnings per share – Basic | $ | 1.40 | $ | 0.96 | $ | 3.42 | $ | 2.19 | ||||||||

Earnings per share – Diluted | $ | 1.38 | $ | 0.94 | $ | 3.35 | $ | 2.12 | ||||||||

Cash dividends declared per share of common stock | $ | 0.60 | $ | 0.5450 | $ | 1.20 | $ | 1.0775 | ||||||||

Weighted average shares of common stock outstanding: | ||||||||||||||||

Basic | 4,574 | 4,688 | 4,632 | 4,707 | ||||||||||||

Diluted | 4,648 | 4,821 | 4,728 | 4,849 | ||||||||||||

See accompanying notes.

FINANCIAL STATEMENTS | Consolidated Condensed Statements of Income | 3 |

INTEL CORPORATION CONSOLIDATED CONDENSED STATEMENTS OF COMPREHENSIVE INCOME |

Three Months Ended | Nine Months Ended | |||||||||||||||

(In Millions; Unaudited) | Sep 29, 2018 | Sep 30, 2017 | Sep 29, 2018 | Sep 30, 2017 | ||||||||||||

Net income | $ | 6,398 | $ | 4,516 | $ | 15,858 | $ | 10,288 | ||||||||

Changes in other comprehensive income, net of tax: | ||||||||||||||||

Net unrealized holding gains (losses) on available-for-sale equity investments | — | 399 | — | 408 | ||||||||||||

Net unrealized holding gains (losses) on derivatives | (25 | ) | 19 | (199 | ) | 350 | ||||||||||

Actuarial valuation and other pension benefits (expenses), net | 13 | 13 | 39 | 233 | ||||||||||||

Translation adjustments and other | (2 | ) | 5 | (15 | ) | 513 | ||||||||||

Other comprehensive income (loss) | (14 | ) | 436 | (175 | ) | 1,504 | ||||||||||

Total comprehensive income | $ | 6,384 | $ | 4,952 | $ | 15,683 | $ | 11,792 | ||||||||

See accompanying notes.

FINANCIAL STATEMENTS | Consolidated Condensed Statements of Comprehensive Income | 4 |

INTEL CORPORATION CONSOLIDATED CONDENSED BALANCE SHEETS |

(In Millions) | Sep 29, 2018 | Dec 30, 2017 | ||||||

(unaudited) | ||||||||

Assets | ||||||||

Current assets: | ||||||||

Cash and cash equivalents | $ | 3,407 | $ | 3,433 | ||||

Short-term investments | 2,641 | 1,814 | ||||||

Trading assets | 7,138 | 8,755 | ||||||

Accounts receivable | 5,457 | 5,607 | ||||||

Inventories | 7,401 | 6,983 | ||||||

Other current assets | 3,546 | 2,908 | ||||||

Total current assets | 29,590 | 29,500 | ||||||

Property, plant and equipment, net of accumulated depreciation of $63,684 ($59,286 as of December 30, 2017) | 47,071 | 41,109 | ||||||

Equity investments | 7,551 | 8,579 | ||||||

Other long-term investments | 3,562 | 3,712 | ||||||

Goodwill | 24,506 | 24,389 | ||||||

Identified intangible assets, net | 12,007 | 12,745 | ||||||

Other long-term assets | 3,955 | 3,215 | ||||||

Total assets | $ | 128,242 | $ | 123,249 | ||||

Liabilities, temporary equity, and stockholders’ equity | ||||||||

Current liabilities: | ||||||||

Short-term debt | $ | 3,051 | $ | 1,776 | ||||

Accounts payable | 3,593 | 2,928 | ||||||

Accrued compensation and benefits | 3,095 | 3,526 | ||||||

Deferred income | — | 1,656 | ||||||

Other accrued liabilities | 9,835 | 7,535 | ||||||

Total current liabilities | 19,574 | 17,421 | ||||||

Debt | 24,823 | 25,037 | ||||||

Contract liabilities | 2,220 | — | ||||||

Income taxes payable, non-current | 4,879 | 4,069 | ||||||

Deferred income taxes | 1,485 | 3,046 | ||||||

Other long-term liabilities | 3,263 | 3,791 | ||||||

Contingencies (Note 16) | ||||||||

Temporary equity | 515 | 866 | ||||||

Stockholders’ equity: | ||||||||

Preferred stock | — | — | ||||||

Common stock and capital in excess of par value, 4,564 issued and outstanding (4,687 issued and outstanding as of December 30, 2017) | 25,492 | 26,074 | ||||||

Accumulated other comprehensive income (loss) | (1,103 | ) | 862 | |||||

Retained earnings | 47,094 | 42,083 | ||||||

Total stockholders’ equity | 71,483 | 69,019 | ||||||

Total liabilities, temporary equity, and stockholders’ equity | $ | 128,242 | $ | 123,249 | ||||

See accompanying notes.

FINANCIAL STATEMENTS | Consolidated Condensed Balance Sheets | 5 |

INTEL CORPORATION CONSOLIDATED CONDENSED STATEMENTS OF CASH FLOWS |

Nine Months Ended | ||||||||

(In Millions; Unaudited) | Sep 29, 2018 | Sep 30, 2017 | ||||||

Cash and cash equivalents, beginning of period | $ | 3,433 | $ | 5,560 | ||||

Cash flows provided by (used for) operating activities: | ||||||||

Net income | 15,858 | 10,288 | ||||||

Adjustments to reconcile net income to net cash provided by operating activities: | ||||||||

Depreciation | 5,420 | 4,990 | ||||||

Share-based compensation | 1,203 | 1,051 | ||||||

Amortization of intangibles | 1,172 | 999 | ||||||

(Gains) losses on equity investments, net | (329 | ) | (1,372 | ) | ||||

(Gains) losses on divestitures | (497 | ) | (387 | ) | ||||

Loss on debt conversion and extinguishment | 211 | — | ||||||

Deferred taxes | 18 | 570 | ||||||

Changes in assets and liabilities: | ||||||||

Accounts receivable | (449 | ) | (1,128 | ) | ||||

Inventories | (362 | ) | (1,245 | ) | ||||

Accounts payable | 430 | 171 | ||||||

Accrued compensation and benefits | (801 | ) | (362 | ) | ||||

Customer deposits and prepaid supply agreements | 1,472 | — | ||||||

Income taxes payable and receivable | (1,075 | ) | 979 | |||||

Other assets and liabilities | 261 | 315 | ||||||

Total adjustments | 6,674 | 4,581 | ||||||

Net cash provided by operating activities | 22,532 | 14,869 | ||||||

Cash flows provided by (used for) investing activities: | ||||||||

Additions to property, plant and equipment | (11,291 | ) | (7,709 | ) | ||||

Acquisitions, net of cash acquired | (183 | ) | (14,499 | ) | ||||

Purchases of available-for-sale debt investments | (3,090 | ) | (1,959 | ) | ||||

Sales of available-for-sale debt investments | 135 | 1,511 | ||||||

Maturities of available-for-sale debt investments | 2,232 | 3,488 | ||||||

Purchases of trading assets | (8,316 | ) | (9,792 | ) | ||||

Maturities and sales of trading assets | 9,705 | 11,806 | ||||||

Purchases of equity investments | (667 | ) | (744 | ) | ||||

Sales of equity investments | 1,646 | 3,173 | ||||||

Proceeds from divestitures | 548 | 3,124 | ||||||

Other investing | (138 | ) | 1,069 | |||||

Net cash used for investing activities | (9,419 | ) | (10,532 | ) | ||||

Cash flows provided by (used for) financing activities: | ||||||||

Increase (decrease) in short-term debt, net | 1,707 | (5 | ) | |||||

Issuance of long-term debt, net of issuance costs | 423 | 7,716 | ||||||

Repayment of debt and debt conversion | (1,928 | ) | (1,502 | ) | ||||

Proceeds from sales of common stock through employee equity incentive plans | 545 | 637 | ||||||

Repurchase of common stock | (8,464 | ) | (3,611 | ) | ||||

Restricted stock unit withholdings | (492 | ) | (424 | ) | ||||

Payment of dividends to stockholders | (4,173 | ) | (3,794 | ) | ||||

Other financing | (757 | ) | 161 | |||||

Net cash provided by (used for) financing activities | (13,139 | ) | (822 | ) | ||||

Net increase (decrease) in cash and cash equivalents | (26 | ) | 3,515 | |||||

Cash and cash equivalents, end of period | $ | 3,407 | $ | 9,075 | ||||

Supplemental disclosures of noncash investing activities and cash flow information: | ||||||||

Acquisition of property, plant, and equipment included in accounts payable and accrued liabilities | $ | 1,988 | $ | 1,736 | ||||

Non-marketable equity investment in McAfee from divestiture | $ | — | $ | 1,078 | ||||

Cash paid during the period for: | ||||||||

Interest, net of capitalized interest | $ | 316 | $ | 386 | ||||

Income taxes, net of refunds | $ | 2,854 | $ | 2,328 | ||||

See accompanying notes.

FINANCIAL STATEMENTS | Consolidated Condensed Statements of Cash Flows | 6 |

INTEL CORPORATION NOTES TO CONSOLIDATED CONDENSED FINANCIAL STATEMENTS |

NOTE 1: BASIS OF PRESENTATION

We prepared our interim consolidated condensed financial statements that accompany these notes in conformity with U.S. generally accepted accounting principles, consistent in all material respects with those applied in our Annual Report on Form 10-K for the fiscal year ended December 30, 2017 (2017 Form 10-K), except for changes associated with recent accounting standards for retirement benefits, revenue recognition, and financial instruments as detailed in "Note 2: Recent Accounting Standards and Accounting Policies." We have reclassified certain prior period amounts to conform to current period presentation.

We have made estimates and judgments affecting the amounts reported in our consolidated condensed financial statements and the accompanying notes. The actual results that we experience may differ materially from our estimates. The interim financial information is unaudited, but reflects all normal adjustments that are, in our opinion, necessary to provide a fair statement of results for the interim periods presented. This report should be read in conjunction with the consolidated financial statements in our 2017 Form 10-K.

NOTE 2: RECENT ACCOUNTING STANDARDS AND ACCOUNTING POLICIES

We assess the adoption impacts of recently issued accounting standards by the Financial Accounting Standards Board on our financial statements. The sections below describe impacts from newly adopted standards as well as material updates to our previous assessments, if any, from our 2017 Form 10-K.

ACCOUNTING STANDARDS ADOPTED

Retirement Benefits - Improving the Presentation of Net Periodic Pension Cost and Net Periodic Postretirement Benefit Cost

Standard/Description: This amended standard was issued to provide additional guidance on the presentation of net periodic benefit cost in the income statement and on the components eligible for capitalization in assets. In accordance with the revised standard, we have separated the different components of net periodic benefit cost, presenting service cost components within operating income and other non-service components separately outside of operating income on the income statement. In addition, only service costs are now eligible for inventory capitalization.

Effective Date and Adoption Considerations: Effective in the first quarter of 2018. Changes to the presentation of benefit costs were required to be adopted retrospectively, while changes to the capitalization of service costs into inventories were required to be adopted prospectively. The standard permits, as a practical expedient, use of the amounts disclosed in the Retirement Benefit Plans footnote for the prior comparative periods as the estimation basis for applying the retrospective presentation requirement.

Effect on Financial Statements or Other Significant Matters: Adoption of the amended standard resulted in the reclassification of approximately $114 million of non-service net periodic benefit costs from line items within operating income to interest and other, net, for the year ended December 30, 2017 ($259 million for the year ended December 31, 2016).

Revenue Recognition - Contracts with Customers

Standard/Description: This standard was issued to achieve a consistent application of revenue recognition within the U.S., resulting in a single revenue model to be applied by all companies. Under the new model, recognition of revenue occurs when a customer obtains control of promised goods or services in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. In addition, the new standard requires that companies disclose the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers.

Effective Date and Adoption Considerations: Effective in the first quarter of 2018. This standard was adopted using a modified retrospective approach through a cumulative adjustment to retained earnings for the fiscal year beginning December 31, 2017.

Effect on Financial Statements or Other Significant Matters: Our adoption assessments identified a change in revenue recognition timing on our component sales made to distributors. Under the new standard we now recognize revenue when we deliver to the distributor rather than deferring recognition until the distributor sells the components.

On the date of initial application, we removed the deferred income and related receivables on component sales made to distributors through a cumulative adjustment to retained earnings. The revenue deferral that was historically recognized in the following period is expected to be primarily offset by the acceleration of revenue recognition in the current period as control of the product transfers to our customer.

FINANCIAL STATEMENTS | Notes to Financial Statements | 7 |

Our assessment also identified a change in expense recognition timing related to payments we make to our customers for distinct services they perform as part of cooperative advertising programs, which were previously recorded as operating expenses. We now recognize the expense for cooperative advertising in the period the marketing activities occur. Previously we recognized the expense in the period the customer was entitled to participate in the program, which coincided with the period of sale. On the date of initial adoption, we capitalized the expense of cooperative advertising not performed through a cumulative adjustment to retained earnings.

We have completed our adoption and implemented policies, processes, and controls to support the standard's measurement and disclosure requirements. Refer to the tables below, which summarize the impacts of the changes discussed above to our financial statements recorded as an adjustment to opening balances for the fiscal year beginning December 31, 2017, and also provide comparative reporting of the impacts of adopting the standard.

Accounting Policy Updates: We recognize net product revenue when we satisfy performance obligations as evidenced by the transfer of control of our products or services to customers. Substantially all of our revenue is derived from product sales. In accordance with contract terms, revenue for product sales is recognized at the time of product shipment from our facilities or delivery to the customer location, as determined by the agreed upon shipping terms. We include shipping charges billed to customers in net revenue, and include the related shipping costs in cost of sales.

We measure revenue based on the amount of consideration we expect to be entitled to in exchange for products or services. Any variable consideration is recognized as a reduction of net revenue at the time of revenue recognition. We determine variable consideration, which consists primarily of sales price concessions, by estimating the most likely amount of consideration we expect to receive from the customer based on historical analysis of customer purchase volumes. The impacts of distributor sales price reductions resulting from price protection agreements are also estimated based on historical analysis of such activity and are reflected as a reduction in net revenue.

We make payments to our customers through cooperative advertising programs, such as our Intel Inside® program, for marketing activities for certain of our products. We generally record the payment as a reduction in revenue in the period that the revenue is earned, unless the payment is for a distinct service, which we record as expense when the marketing activities occur.

Financial Instruments - Recognition and Measurement

Standard/Description: Requires changes to the accounting for financial instruments that primarily affect equity securities, financial liabilities measured using the fair value option, and the presentation and disclosure requirements for such instruments.

Effective Date and Adoption Considerations: Effective in the first quarter of 2018. Changes to our marketable equity securities were required to be adopted using a modified retrospective approach through a cumulative effect adjustment to retained earnings for the fiscal year beginning December 31, 2017. Since management has elected to apply the measurement alternative to non-marketable equity securities, changes to these securities were adopted prospectively.

Effect on Financial Statements or Other Significant Matters: Marketable equity securities previously classified as available-for-sale equity investments are now measured and recorded at fair value with changes in fair value recorded through the income statement.

All non-marketable equity securities formerly classified as cost method investments are measured and recorded using the measurement alternative. Equity securities measured and recorded using the measurement alternative are recorded at cost minus impairment, if any, plus or minus changes resulting from qualifying observable price changes. Adjustments resulting from impairments and qualifying observable price changes are recorded in the income statement.

Beginning in the first quarter of 2018, in accordance with the standard, recurring fair value disclosures are no longer provided for equity securities measured using the measurement alternative. In addition, the existing impairment model has been replaced with a new one-step qualitative impairment model. No initial adoption adjustment was recorded for these instruments since the standard was required to be applied prospectively for securities measured using the measurement alternative.

We have completed our adoption and implemented policies, processes, and controls to support the standard's measurement and disclosure requirements. Refer to the table below, which summarizes impacts, net of tax, of the changes discussed above to our financial statements. This reflects an adjustment to opening balances for the fiscal year beginning December 31, 2017.

Accounting Policy Updates: We regularly invest in equity securities of public and private companies to promote business and strategic objectives. Equity investments are measured and recorded as follows:

• | Marketable equity securities are equity securities with readily determinable fair value (RDFV) that are measured and recorded at fair value. Prior to fiscal 2018, these securities were measured and recorded at fair value and classified as available-for-sale securities. |

• | Non-marketable equity securities are equity securities without RDFV that are measured and recorded using a measurement alternative which measures the securities at cost minus impairment, if any, plus or minus changes resulting from qualifying observable price changes. These securities were previously accounted for using the cost method of accounting, measured at cost less other-than-temporary impairment. |

• | Equity method investments are equity securities in investees we do not control but over which we have the ability to exercise significant influence. Equity method investments are measured at cost minus impairment, if any, plus or minus our share of equity method investee income or loss. Our proportionate share of the income or loss from equity method investments is recognized on a one-quarter lag. |

FINANCIAL STATEMENTS | Notes to Financial Statements | 8 |

Realized and unrealized gains or losses resulting from changes in value and sale of our equity investments are recorded in gains (losses) on equity investments, net. We previously recorded unrealized gains and losses through other comprehensive income (loss) and realized gains and losses on the sale, exchange or impairment of these equity investments through gains (losses) on equity investments, net.

The carrying value of our portfolio of non-marketable equity securities totaled $2.9 billion as of September 29, 2018 ($2.6 billion as of December 30, 2017). The carrying value of our non-marketable equity securities is adjusted for qualifying observable price changes resulting from the issuance of similar or identical securities by the same issuer. Determining whether an observed transaction is similar to a security within our portfolio requires judgment based on the rights and preferences of the securities. Recording upward and downward adjustments to the carrying value of our equity securities as a result of observable price changes requires quantitative assessments of the fair value of our securities using various valuation methodologies and involves the use of estimates.

Non-marketable equity securities and equity method investments are also subject to periodic impairment reviews. Our quarterly impairment analysis considers both qualitative and quantitative factors that may have a significant impact on the investee's fair value. Qualitative factors considered include industry and market conditions, the financial performance and near-term prospects of the investee, and other relevant events and factors affecting the investee. When indicators of impairment exist, we prepare quantitative assessments of the fair value of our equity investments using both the market and income approaches which require judgment and the use of estimates, including discount rates, investee revenues and costs, and comparable market data of private and public companies, among others. Prior to fiscal 2018, non-marketable equity securities were tested for impairment using the other-than-temporary impairment model which considered the severity and duration of a decline in fair value below cost and our ability and intent to hold the investment for a sufficient period of time to allow for recovery. Impairments of equity investments were $372 million in the first nine months of 2018 and $613 million in the first nine months of 2017.

Opening Balance Adjustments

The following table summarizes the effects of adopting Revenue Recognition - Contracts with Customers, Financial Instruments - Recognition and Measurement, and other accounting standards on our financial statements for the fiscal year beginning December 31, 2017 as an adjustment to the opening balance:

Adjustments from | ||||||||||||||||||||

(In Millions) | Balance as of Dec 30, 2017 | Revenue Standard | Financial Instruments Standard | Other1 | Opening Balance as of Dec 31, 2017 | |||||||||||||||

Assets: | ||||||||||||||||||||

Accounts receivable | $ | 5,607 | $ | (530 | ) | $ | — | $ | — | $ | 5,077 | |||||||||

Inventories | $ | 6,983 | $ | 47 | $ | — | $ | — | $ | 7,030 | ||||||||||

Other current assets | $ | 2,908 | $ | 64 | $ | — | $ | (8 | ) | $ | 2,964 | |||||||||

Equity investments | $ | — | $ | — | $ | 8,579 | $ | — | $ | 8,579 | ||||||||||

Marketable equity securities | $ | 4,192 | $ | — | $ | (4,192 | ) | $ | — | $ | — | |||||||||

Other long-term assets | $ | 7,602 | $ | — | $ | (4,387 | ) | $ | (43 | ) | $ | 3,172 | ||||||||

Liabilities: | ||||||||||||||||||||

Deferred income | $ | 1,656 | $ | (1,356 | ) | $ | — | $ | — | $ | 300 | |||||||||

Other accrued liabilities | $ | 7,535 | $ | 81 | $ | — | $ | — | $ | 7,616 | ||||||||||

Deferred income taxes | $ | 3,046 | $ | 191 | $ | — | $ | (20 | ) | $ | 3,217 | |||||||||

Stockholders' equity: | ||||||||||||||||||||

Accumulated other comprehensive income (loss) | $ | 862 | $ | — | $ | (1,745 | ) | $ | (45 | ) | $ | (928 | ) | |||||||

Retained earnings | $ | 42,083 | $ | 665 | $ | 1,745 | $ | 14 | $ | 44,507 | ||||||||||

1 | Includes adjustments from adoption of "Income Taxes - Intra-Entity Transfers of Assets Other Than Inventory" and "Income Statement—Reporting Comprehensive Income - Reclassification of Certain Tax Effects from Accumulated Other Comprehensive Income." |

FINANCIAL STATEMENTS | Notes to Financial Statements | 9 |

The following table summarizes the impacts of adopting the new revenue standard on our consolidated condensed statements of income and balance sheets:

Three Months Ended September 29, 2018 | Nine Months Ended September 29, 2018 | |||||||||||||||||||||||

(In Millions) | As reported | Adjustments | Without new revenue standard | As reported | Adjustments | Without new revenue standard | ||||||||||||||||||

Income Statement | ||||||||||||||||||||||||

Net revenue | $ | 19,163 | $ | 118 | $ | 19,281 | $ | 52,191 | $ | (266 | ) | $ | 51,925 | |||||||||||

Cost of sales | 6,803 | 46 | 6,849 | 19,681 | (136 | ) | 19,545 | |||||||||||||||||

Gross margin | 12,360 | 72 | 12,432 | 32,510 | (130 | ) | 32,380 | |||||||||||||||||

Marketing, general and administrative | 1,605 | — | 1,605 | 5,230 | (70 | ) | 5,160 | |||||||||||||||||

Operating income | 7,349 | 72 | 7,421 | 17,092 | (60 | ) | 17,032 | |||||||||||||||||

Income before taxes | 7,142 | 72 | 7,214 | 17,682 | (60 | ) | 17,622 | |||||||||||||||||

Provision for taxes | 744 | 20 | 764 | 1,824 | (4 | ) | 1,820 | |||||||||||||||||

Net income | $ | 6,398 | $ | 52 | $ | 6,450 | $ | 15,858 | $ | (56 | ) | $ | 15,802 | |||||||||||

As of September 29, 2018 | ||||||||||||||||||||||||

(In Millions) | As reported | Adjustments | Without new revenue standard | |||||||||||||||||||||

Balance Sheet | ||||||||||||||||||||||||

Assets: | ||||||||||||||||||||||||

Accounts receivable | $ | 5,457 | $ | 446 | $ | 5,903 | ||||||||||||||||||

Inventories | $ | 7,401 | $ | 23 | $ | 7,424 | ||||||||||||||||||

Other current assets | $ | 3,546 | $ | 4 | $ | 3,550 | ||||||||||||||||||

Liabilities: | ||||||||||||||||||||||||

Deferred income | $ | — | $ | 1,668 | $ | 1,668 | ||||||||||||||||||

Other accrued liabilities | $ | 9,835 | $ | (334 | ) | $ | 9,501 | |||||||||||||||||

Deferred income taxes | $ | 1,485 | $ | (140 | ) | $ | 1,345 | |||||||||||||||||

Equity: | ||||||||||||||||||||||||

Retained earnings | $ | 47,094 | $ | (721 | ) | $ | 46,373 | |||||||||||||||||

ACCOUNTING STANDARDS NOT YET ADOPTED

Leases

Standard/Description: This new lease accounting standard requires that we recognize leased assets and corresponding liabilities on the balance sheet and provide enhanced disclosure of lease activity.

Effective Date and Adoption Considerations: Effective in the first quarter of 2019. The standard requires a modified retrospective adoption. We can choose to apply the provisions at the beginning of the earliest comparative period presented in the financial statements or at the beginning of the period of adoption. We have elected to apply the guidance at the beginning of the period of adoption.

Effect on Financial Statements or Other Significant Matters: We expect the valuation of our right-of-use assets and lease liabilities, previously described as operating leases, to approximate the present value of our forecasted future lease commitments. We are currently implementing processes to comply with the measurement and disclosure requirements.

Cloud Computing Implementation Costs

Standard/Description: The standard requires implementation costs incurred in cloud computing (i.e. hosting) arrangements that are service contracts to be assessed under existing guidance to determine which costs to capitalize as assets or expense as incurred.

Effective Date and Adoption Considerations: Effective in the first quarter of 2020. The standard requires adoption either retrospectively or prospectively.

Effect on Financial Statements or Other Significant Matters: We have not yet determined the impact of this standard on our financial statements.

FINANCIAL STATEMENTS | Notes to Financial Statements | 10 |

NOTE 3: OPERATING SEGMENTS

We manage our business through the following operating segments:

• | Client Computing Group (CCG) |

• | Data Center Group (DCG) |

• | Internet of Things Group (IOTG) |

• | Non-Volatile Memory Solutions Group (NSG) |

• | Programmable Solutions Group (PSG) |

• | All Other |

During the third quarter of 2018, we made an organizational change to combine our artificial intelligence investments in edge computing with IOTG; accordingly, approximately $480 million of goodwill was reallocated from "all other" to the IOTG operating segment.

We offer platform products that incorporate various components and technologies, including a microprocessor and chipset, a stand-alone System-on-Chip (SoC), or a multichip package. A platform product may be enhanced by additional hardware, software, and services offered by Intel. Platform products are used in various form factors across our CCG, DCG, and IOTG operating segments. We derive a substantial majority of our revenue from platform products, which are our principal products and considered as one class of product.

CCG and DCG are our reportable operating segments. IOTG, NSG, and PSG do not meet the quantitative thresholds to qualify as reportable operating segments; however, we have elected to disclose the results of these non-reportable operating segments.

The “all other” category includes revenue, expenses, and charges such as:

• | results of operations from non-reportable segments not otherwise presented, including Mobileye results; |

• | historical results of operations from divested businesses, including Intel Security Group (ISecG) results; |

• | results of operations of start-up businesses that support our initiatives, including our foundry business; |

• | amounts included within restructuring and other charges; |

• | a portion of employee benefits, compensation, and other expenses not allocated to the operating segments; and |

• | acquisition-related costs, including amortization and any impairment of acquisition-related intangibles and goodwill. |

The Chief Operating Decision Maker (CODM), which is our interim Chief Executive Officer, does not evaluate operating segments using discrete asset information. Operating segments do not record inter-segment revenue. We do not allocate gains and losses from equity investments, interest and other income, or taxes to operating segments. Although the CODM uses operating income to evaluate the segments, operating costs included in one segment may benefit other segments. Except for these differences, the accounting policies for segment reporting are the same as for Intel as a whole.

FINANCIAL STATEMENTS | Notes to Financial Statements | 11 |

Net revenue and operating income (loss) for each period were as follows:

Three Months Ended | Nine Months Ended | |||||||||||||||

(In Millions) | Sep 29, 2018 | Sep 30, 2017 | Sep 29, 2018 | Sep 30, 2017 | ||||||||||||

Net revenue: | ||||||||||||||||

Client Computing Group | ||||||||||||||||

Platform | $ | 9,023 | $ | 8,132 | $ | 24,703 | $ | 23,163 | ||||||||

Adjacent | 1,211 | 728 | 2,479 | 1,886 | ||||||||||||

10,234 | 8,860 | 27,182 | 25,049 | |||||||||||||

Data Center Group | ||||||||||||||||

Platform | 5,637 | 4,439 | 15,561 | 12,344 | ||||||||||||

Adjacent | 502 | 439 | 1,361 | 1,138 | ||||||||||||

6,139 | 4,878 | 16,922 | 13,482 | |||||||||||||

Internet of Things Group | ||||||||||||||||

Platform | 855 | 680 | 2,319 | 1,926 | ||||||||||||

Adjacent | 64 | 169 | 320 | 364 | ||||||||||||

919 | 849 | 2,639 | 2,290 | |||||||||||||

Non-Volatile Memory Solutions Group | 1,081 | 891 | 3,200 | 2,631 | ||||||||||||

Programmable Solutions Group | 496 | 469 | 1,511 | 1,334 | ||||||||||||

All other | 294 | 202 | 737 | 922 | ||||||||||||

Total net revenue | $ | 19,163 | $ | 16,149 | $ | 52,191 | $ | 45,708 | ||||||||

Operating income (loss): | ||||||||||||||||

Client Computing Group | $ | 4,532 | $ | 3,600 | $ | 10,557 | $ | 9,656 | ||||||||

Data Center Group | 3,082 | 2,255 | 8,421 | 5,403 | ||||||||||||

Internet of Things Group | 321 | 146 | 791 | 390 | ||||||||||||

Non-Volatile Memory Solutions Group | 160 | (52 | ) | 14 | (291 | ) | ||||||||||

Programmable Solutions Group | 106 | 113 | 304 | 302 | ||||||||||||

All other | (852 | ) | (921 | ) | (2,995 | ) | (2,845 | ) | ||||||||

Total operating income | $ | 7,349 | $ | 5,141 | $ | 17,092 | $ | 12,615 | ||||||||

Disaggregated net revenue for each period was as follows:

Three Months Ended | Nine Months Ended | |||||||||||||||

(In Millions) | Sep 29, 2018 | Sep 30, 2017 | Sep 29, 2018 | Sep 30, 2017 | ||||||||||||

Platform revenue | ||||||||||||||||

Desktop platform | $ | 3,225 | $ | 2,967 | $ | 9,087 | $ | 8,598 | ||||||||

Notebook platform | 5,774 | 5,123 | 15,549 | 14,437 | ||||||||||||

DCG platform | 5,637 | 4,439 | 15,561 | 12,344 | ||||||||||||

Other platform1 | 879 | 722 | 2,386 | 2,054 | ||||||||||||

15,515 | 13,251 | 42,583 | 37,433 | |||||||||||||

Adjacent revenue2 | 3,648 | 2,898 | 9,608 | 7,741 | ||||||||||||

ISecG divested business | — | — | — | 534 | ||||||||||||

Total revenue | $ | 19,163 | $ | 16,149 | $ | 52,191 | $ | 45,708 | ||||||||

1 | Includes our tablet, service provider, and IOTG platform revenue. |

2 | Includes all of our non-platform products for CCG, DCG, and IOTG like modem, ethernet, and silicon photonics, as well as NSG, PSG, and Mobileye products. |

FINANCIAL STATEMENTS | Notes to Financial Statements | 12 |

NOTE 4: EARNINGS PER SHARE

We computed basic earnings per share of common stock based on the weighted average number of shares of common stock outstanding during the period. We computed diluted earnings per share of common stock based on the weighted average number of shares of common stock outstanding plus potentially dilutive shares of common stock outstanding during the period.

Three Months Ended | Nine Months Ended | |||||||||||||||

(In Millions, Except Per Share Amounts) | Sep 29, 2018 | Sep 30, 2017 | Sep 29, 2018 | Sep 30, 2017 | ||||||||||||

Net income available to common stockholders | $ | 6,398 | $ | 4,516 | $ | 15,858 | $ | 10,288 | ||||||||

Weighted average shares of common stock outstanding – basic | 4,574 | 4,688 | 4,632 | 4,707 | ||||||||||||

Dilutive effect of employee equity incentive plans | 40 | 34 | 52 | 43 | ||||||||||||

Dilutive effect of convertible debt | 34 | 99 | 44 | 99 | ||||||||||||

Weighted average shares of common stock outstanding – diluted | 4,648 | 4,821 | 4,728 | 4,849 | ||||||||||||

Earnings per share – Basic | $ | 1.40 | $ | 0.96 | $ | 3.42 | $ | 2.19 | ||||||||

Earnings per share – Diluted | $ | 1.38 | $ | 0.94 | $ | 3.35 | $ | 2.12 | ||||||||

Potentially dilutive shares of common stock from employee equity incentive plans are determined by applying the treasury stock method to the assumed exercise of outstanding stock options, the assumed vesting of outstanding restricted stock units (RSUs), and the assumed issuance of common stock under the stock purchase plan. In December 2017, we paid cash to satisfy the conversion of our 2035 debentures, which we excluded from our dilutive earnings per share computation starting in the fourth quarter of 2017 and are no longer dilutive. Our 2039 debentures require settlement of the principal amount of the debt in cash upon conversion. Since the conversion premium is paid in cash or stock at our option, we determined the potentially dilutive shares of common stock by applying the treasury stock method. For the nine months ended September 29, 2018, we paid cash to satisfy the conversion of a portion of our 2039 debentures. The potentially dilutive shares associated with the converted portion are excluded from our diluted earnings per share computation in 2018 as they are no longer dilutive.

In all periods presented, potentially dilutive outstanding securities which would have been antidilutive are insignificant and are excluded from the computation of diluted earnings per share. In all periods presented, we included our outstanding 2039 debentures in the calculation of diluted earnings per share of common stock because the average market price was above the conversion price. We could potentially exclude the 2039 debentures in the future if the average market price is below the conversion price.

NOTE 5: CONTRACT LIABILITIES

(In Millions) | Sep 29, 2018 | Opening Balance as of Dec 31, 2017 | ||||||

Contract liabilities from prepaid supply agreements | $ | 2,692 | $ | 105 | ||||

Contract liabilities from software, services and other | 93 | 195 | ||||||

Total contract liabilities | $ | 2,785 | $ | 300 | ||||

Contract liabilities are primarily related to partial prepayments received from customers on long-term supply agreements towards future NSG product delivery. As new prepaid supply agreements are entered into and performance obligations are negotiated, this component of the contract liability balance will increase, and as customers purchase product and utilize their prepaid balances, the balance will decrease. The short-term portion of prepayments from supply agreements is reported on the consolidated condensed balance sheets within other accrued liabilities.

The following table shows the changes in contract liability balances relating to prepaid supply agreements during the first nine months of 2018:

(In Millions) | ||||

Prepaid supply agreements balance as of December 31, 2017 | $ | 105 | ||

Additions and adjustments | 2,753 | |||

Revenue recognized | (166 | ) | ||

Prepaid supply agreements balance as of September 29, 2018 | $ | 2,692 | ||

Additions and adjustments in the first nine months of 2018 include a $1.0 billion reclassification from customer deposits previously included in other long-term liabilities. The long-term supply agreements represent $4.8 billion in future anticipated revenues with 2% expected to be recognized during the fourth quarter of the year and the remainder ratably over the next five years.

FINANCIAL STATEMENTS | Notes to Financial Statements | 13 |

NOTE 6: OTHER FINANCIAL STATEMENT DETAILS

INVENTORIES

(In Millions) | Sep 29, 2018 | Dec 30, 2017 | ||||||

Raw materials | $ | 932 | $ | 738 | ||||

Work in process | 4,507 | 4,213 | ||||||

Finished goods | 1,962 | 2,032 | ||||||

Total inventories | $ | 7,401 | $ | 6,983 | ||||

INTEREST AND OTHER, NET

The components of interest and other, net for each period were as follows:

Three Months Ended | Nine Months Ended | |||||||||||||||

(In Millions) | Sep 29, 2018 | Sep 30, 2017 | Sep 29, 2018 | Sep 30, 2017 | ||||||||||||

Interest income | $ | 109 | $ | 137 | $ | 308 | $ | 349 | ||||||||

Interest expense | (109 | ) | (191 | ) | (337 | ) | (493 | ) | ||||||||

Other, net | (132 | ) | (3 | ) | 254 | 406 | ||||||||||

Total interest and other, net | $ | (132 | ) | $ | (57 | ) | $ | 225 | $ | 262 | ||||||

Interest expense in the preceding table is net of $142 million of interest capitalized in the third quarter of 2018 and $381 million in the first nine months of 2018 ($77 million in the third quarter of 2017 and $212 million in the first nine months of 2017).

In the second quarter of 2018, we completed the divestiture of Wind River Systems, Inc. and recognized a pre-tax gain of $494 million. For the first nine months of 2018, we have settled conversion requests for our 2039 convertible debentures totaling $793 million in principal, resulting in a cumulative loss of $211 million.

NOTE 7: INCOME TAXES

During the third quarter of 2018, we adjusted our provisional tax estimates related to the U.S. Tax Cuts and Jobs Act (Tax Reform) that we recorded in the fourth quarter of 2017 to reflect the impact of additional analysis related to the transition tax liability and the refinement of our measurement of deferred income taxes. Our estimated annual effective tax rate for the first nine months of 2018 includes provisional tax estimates for certain Tax Reform provisions related to foreign-derived intangible income and low-taxed intangible income. Our accounting remains incomplete as of the third quarter of 2018. We could receive additional data and regulatory guidance during the fourth quarter of 2018 that may impact our provisional estimates.

Our effective income tax rate was 10.3% in the first nine months of 2018 compared to 28.1% in the first nine months of 2017. Tax Reform reduced the U.S. statutory federal tax rate from 35.0% to 21.0%, which favorably impacted our effective tax rate in the first nine months of 2018 by approximately nine percentage points. Further, the Tax Reform provisions related to foreign-derived intangible income favorably impacted our effective tax rate by approximately four percentage points, and the provision related to low-taxed intangible income and the repeal of the domestic manufacturing deduction each unfavorably impacted our effective tax rate by approximately one percentage point. The decrease in the first nine months of 2018 was also driven by non-recurring items, primarily our divestiture of ISecG in the second quarter of 2017, which increased our effective tax rate in the first nine months of 2017 by approximately five percentage points, and the adjustment to our provisional estimates for Tax Reform in the first nine months of 2018, which reduced our effective tax rate by approximately two percentage points.

FINANCIAL STATEMENTS | Notes to Financial Statements | 14 |

NOTE 8: INVESTMENTS

DEBT INVESTMENTS

Trading Assets

Trading assets still held at the reporting date incurred net losses of $4 million in the third quarter of 2018 and net losses of $169 million in the first nine months of 2018 (net gains of $81 million in the third quarter of 2017 and net gains of $433 million in the first nine months of 2017). Related derivatives incurred net losses of $11 million in the third quarter of 2018 and net gains of $159 million in the first nine months of 2018 (net losses of $75 million in the third quarter of 2017 and net losses of $402 million in the first nine months of 2017).

Available-for-Sale Debt Investments

September 29, 2018 | December 30, 2017 | |||||||||||||||||||||||||||||||

(In Millions) | Adjusted Cost | Gross Unrealized Gains | Gross Unrealized Losses | Fair Value | Adjusted Cost | Gross Unrealized Gains | Gross Unrealized Losses | Fair Value | ||||||||||||||||||||||||

Corporate debt | $ | 2,647 | $ | 2 | $ | (29 | ) | $ | 2,620 | $ | 2,294 | $ | 4 | $ | (13 | ) | $ | 2,285 | ||||||||||||||

Financial institution instruments | 3,647 | 3 | (18 | ) | 3,632 | 3,387 | 3 | (9 | ) | 3,381 | ||||||||||||||||||||||

Government debt | 940 | — | (14 | ) | 926 | 961 | — | (6 | ) | 955 | ||||||||||||||||||||||

Total available-for-sale debt investments | $ | 7,234 | $ | 5 | $ | (61 | ) | $ | 7,178 | $ | 6,642 | $ | 7 | $ | (28 | ) | $ | 6,621 | ||||||||||||||

Government debt includes instruments such as non-U.S. government bonds and U.S. agency securities. Financial institution instruments include instruments issued or managed by financial institutions in various forms such as commercial paper, fixed and floating rate bonds, money market fund deposits, and time deposits. Substantially all time deposits were issued by institutions outside the U.S. as of September 29, 2018 and December 30, 2017.

The fair value of available-for-sale debt investments, by contractual maturity, as of September 29, 2018, was as follows:

(In Millions) | Fair Value | |||

Due in 1 year or less | $ | 3,138 | ||

Due in 1–2 years | 782 | |||

Due in 2–5 years | 2,662 | |||

Due after 5 years | 118 | |||

Instruments not due at a single maturity date | 478 | |||

Total | $ | 7,178 | ||

EQUITY INVESTMENTS

(In Millions) | Sep 29, 2018 | Dec 30, 2017 | ||||||

Marketable equity securities | $ | 3,039 | $ | 4,192 | ||||

Non-marketable equity securities | 2,878 | 2,613 | ||||||

Equity method investments | 1,634 | 1,774 | ||||||

Total | $ | 7,551 | $ | 8,579 | ||||

FINANCIAL STATEMENTS | Notes to Financial Statements | 15 |

The components of gains (losses) on equity investments, net for each period were as follows:

Three Months Ended | Nine Months Ended | |||||||||||||||

(In Millions) | Sep 29, 2018 | Sep 30, 2017 | Sep 29, 2018 | Sep 30, 2017 | ||||||||||||

Initial mark to market adjustments on marketable equity securities1 2 | $ | — | $ | — | $ | 46 | $ | — | ||||||||

Ongoing mark to market adjustments on marketable equity securities1 2 | 8 | — | 379 | — | ||||||||||||

Gains (losses) on sales2 | 57 | 944 | 68 | 2,020 | ||||||||||||

Observable price adjustments on non-marketable equity securities2 | 43 | — | 191 | — | ||||||||||||

Impairments | (328 | ) | (10 | ) | (372 | ) | (613 | ) | ||||||||

Share of equity method investee gains (losses) | — | (110 | ) | (152 | ) | (129 | ) | |||||||||

Dividends | 1 | — | 39 | 68 | ||||||||||||

Other | 144 | 22 | 166 | 94 | ||||||||||||

Total gains (losses) on equity investments, net | $ | (75 | ) | $ | 846 | $ | 365 | $ | 1,440 | |||||||

1 | Initial mark to market adjustments refers to the fair value adjustment recorded upon a security becoming marketable, generally as a result of an initial public offering (IPO), whereas ongoing mark to market adjustments refers to all post-IPO mark to market adjustments. |

2 Both initial and ongoing mark to market adjustments and observable price adjustments relate to the new financial instruments standard adopted in the first quarter of 2018, and are not applicable in prior periods. Gains (losses) on sales includes realized gains (losses) on sales of non-marketable equity securities and equity method investments, and in 2017 also includes realized gains (losses) on sales of available-for-sale equity securities which are now reflected in ongoing mark to market adjustments on marketable equity securities.

Three Months Ended | Nine Months Ended | |||||||

(In Millions) | Sep 29, 2018 | Sep 29, 2018 | ||||||

Net gains (losses) recognized during the period on equity securities | $ | (75 | ) | $ | 518 | |||

Less: Net (gains) losses recognized during the period on equity securities sold during the period | (225 | ) | (463 | ) | ||||

Unrealized gains (losses) recognized during the reporting period on equity securities still held at the reporting date | $ | (300 | ) | $ | 55 | |||

Cloudera, Inc.

On April 28, 2017, Cloudera, Inc. (Cloudera) completed its initial public offering and we designated our previous equity and cost method investments in Cloudera as available-for-sale. During the second quarter of 2017, we determined we had an other-than-temporary decline in the fair value of our investment and recognized an impairment charge of $278 million.

Beijing UniSpreadtrum Technology Ltd.

During 2014, we entered into a series of agreements with Tsinghua Unigroup Ltd. (Tsinghua Unigroup), an operating subsidiary of Tsinghua Holdings Co. Ltd., to, among other things, jointly develop Intel® architecture- and communications-based solutions for phones. We agreed to invest up to 9.0 billion Chinese yuan (approximately $1.5 billion as of the date of the agreement) for a minority stake of approximately 20% of Beijing UniSpreadtrum Technology Ltd., a holding company under Tsinghua Unigroup. During 2015, we invested $966 million to complete the first phase of the equity investment and accounted for our interest using the cost method of accounting. During 2017, we reduced our expectation of the company's future operating performance due to competitive pressures, which resulted in an impairment charge of $308 million.

IM Flash Technologies, LLC

Intel-Micron Flash Technologies (IMFT) was formed in 2006 by Micron Technology, Inc. (Micron) and Intel to jointly develop NAND flash memory and 3D XPoint™ technology products. IMFT is an unconsolidated variable interest entity and all costs of IMFT are passed on to Micron and Intel through sale of products or services in proportional share of ownership. As of September 29, 2018, we own a 49% interest in IMFT. Our portion of IMFT costs was approximately $97 million in the third quarter of 2018 and approximately $324 million in the first nine months of 2018 (approximately $115 million in the third quarter of 2017 and approximately $350 million in the first nine months of 2017).

IMFT depends on Micron and Intel for any additional cash needs to be provided in the form of cash calls or member debt financing (MDF). The MDF balance may be converted to a capital contribution at our request, or may be repaid upon availability of funds. The IMFT operating agreement continues through 2024 unless terminated earlier, and provides for certain buy-sell rights of the joint venture. Intel has the right to cause Micron to buy our interest in IMFT and, if exercised, Micron could elect to receive financing from us for one to two years. Commencing in January 2019, Micron has the right to call our interest in IMFT.

FINANCIAL STATEMENTS | Notes to Financial Statements | 16 |

On July 16, 2018, Intel and Micron announced that they agreed to complete joint development for the second generation of 3D XPoint technology, which is expected to occur in the first half of 2019. Technology development beyond the second generation of 3D XPoint technology will be pursued independently by the two companies in order to optimize the technology for their respective product and business needs. Intel continues to purchase jointly developed products from Micron under certain supply agreements.

On October 18, 2018, Micron publicly announced their intent to exercise the right to call our interest in IMFT. The timeline to close the transaction is between six and twelve months after the date Micron exercises the call. Following the closing date, we will continue to receive supply for a period of one year. We recognized an impairment charge of $290 million during the third quarter of 2018. This reduced the carrying value of our equity method investment in IMFT to $1.6 billion in line with our expectation of future cash flows and Micron exercising the call in January.

NOTE 9: IDENTIFIED INTANGIBLE ASSETS

September 29, 2018 | ||||||||||||

(In Millions) | Gross Assets | Accumulated Amortization | Net | |||||||||

Acquisition-related developed technology | $ | 9,611 | $ | (2,742 | ) | $ | 6,869 | |||||

Acquisition-related customer relationships | 2,036 | (433 | ) | 1,603 | ||||||||

Acquisition-related brands | 143 | (44 | ) | 99 | ||||||||

Licensed technology and patents | 3,052 | (1,505 | ) | 1,547 | ||||||||

Identified intangible assets subject to amortization | 14,842 | (4,724 | ) | 10,118 | ||||||||

In-process research and development | 1,497 | — | 1,497 | |||||||||

Other intangible assets | 392 | — | 392 | |||||||||

Identified intangible assets not subject to amortization | 1,889 | — | 1,889 | |||||||||

Total identified intangible assets | $ | 16,731 | $ | (4,724 | ) | $ | 12,007 | |||||

December 30, 2017 | ||||||||||||

(In Millions) | Gross Assets | Accumulated Amortization | Net | |||||||||

Acquisition-related developed technology | $ | 8,912 | $ | (1,922 | ) | $ | 6,990 | |||||

Acquisition-related customer relationships | 2,052 | (313 | ) | 1,739 | ||||||||

Acquisition-related brands | 143 | (29 | ) | 114 | ||||||||

Licensed technology and patents | 3,104 | (1,370 | ) | 1,734 | ||||||||

Identified intangible assets subject to amortization | 14,211 | (3,634 | ) | 10,577 | ||||||||

In-process research and development | 2,168 | — | 2,168 | |||||||||

Identified intangible assets not subject to amortization | 2,168 | — | 2,168 | |||||||||

Total identified intangible assets | $ | 16,379 | $ | (3,634 | ) | $ | 12,745 | |||||

Amortization expenses recorded in the consolidated condensed statements of income for each period were as follows:

Three Months Ended | Nine Months Ended | |||||||||||||||||

(In Millions) | Location | Sep 29, 2018 | Sep 30, 2017 | Sep 29, 2018 | Sep 30, 2017 | |||||||||||||

Acquisition-related developed technology | Cost of sales | $ | 276 | $ | 243 | $ | 826 | $ | 650 | |||||||||

Acquisition-related customer relationships | Amortization of acquisition-related intangibles | 45 | 45 | 135 | 113 | |||||||||||||

Acquisition-related brands | Amortization of acquisition-related intangibles | 5 | 4 | 15 | 11 | |||||||||||||

Licensed technology and patents | Cost of sales | 64 | 73 | 196 | 225 | |||||||||||||

Total amortization expenses | $ | 390 | $ | 365 | $ | 1,172 | $ | 999 | ||||||||||

FINANCIAL STATEMENTS | Notes to Financial Statements | 17 |

We expect future amortization expenses for the next five years to be as follows:

(In Millions) | Remainder of 2018 | 2019 | 2020 | 2021 | 2022 | |||||||||||||||

Acquisition-related developed technology | $ | 279 | $ | 1,114 | $ | 1,082 | $ | 1,047 | $ | 1,008 | ||||||||||

Acquisition-related customer relationships | 45 | 180 | 179 | 179 | 171 | |||||||||||||||

Acquisition-related brands | 5 | 20 | 20 | 20 | 6 | |||||||||||||||

Licensed technology and patents | 64 | 241 | 210 | 198 | 193 | |||||||||||||||

Total future amortization expenses | $ | 393 | $ | 1,555 | $ | 1,491 | $ | 1,444 | $ | 1,378 | ||||||||||

NOTE 10: OTHER LONG-TERM ASSETS

(In Millions) | Sep 29, 2018 | Dec 30, 2017 | ||||||

Non-current deferred tax assets | $ | 1,011 | $ | 840 | ||||

Pre-payments for property, plant and equipment | 1,383 | 714 | ||||||

Loans receivable | 544 | 860 | ||||||

Other | 1,017 | 801 | ||||||

Total other long-term assets | $ | 3,955 | $ | 3,215 | ||||

NOTE 11: BORROWINGS

For the first nine months of 2018, we paid $1.9 billion to satisfy conversion obligations for $793 million of our $2.0 billion 3.25% junior subordinated 2039 convertible debentures. We recognized a loss of $211 million in interest and other, net and a reduction of $1.3 billion in stockholders' equity related to the conversion feature.

During the third quarter of 2018, we remarketed $423 million principal of bonds issued by the Industrial Development Authority of the City of Chandler, Arizona (the Arizona bonds) and the State of Oregon Business Development Commission (the Oregon bonds). The bonds are our unsecured general obligations in accordance with loan agreements we entered into with the Industrial Development Authority of the City of Chandler, Arizona and the State of Oregon Business Development Commission. The bonds mature between 2035 and 2040 and carry interest rates of 2.4% - 2.7%. Each series of the Arizona bonds and the Oregon bonds are subject to mandatory tender in August 2023, at which time we can re-market the bonds as either fixed-rate bonds for a specified period or as variable-rate bonds until another fixed rate period is selected or until their final maturity date.

FINANCIAL STATEMENTS | Notes to Financial Statements | 18 |

NOTE 12: FAIR VALUE

For information about our fair value policies, and methods and assumptions used in estimating the fair value of our financial assets and liabilities, see "Note 2: Accounting Policies" and "Note 15: Fair Value" in our 2017 Form 10-K.

ASSETS AND LIABILITIES MEASURED AND RECORDED AT FAIR VALUE ON A RECURRING BASIS

September 29, 2018 | December 30, 2017 | |||||||||||||||||||||||||||||||

Fair Value Measured and Recorded at Reporting Date Using | Fair Value Measured and Recorded at Reporting Date Using | |||||||||||||||||||||||||||||||

(In Millions) | Level 1 | Level 2 | Level 3 | Total | Level 1 | Level 2 | Level 3 | Total | ||||||||||||||||||||||||

Assets | ||||||||||||||||||||||||||||||||

Cash equivalents: | ||||||||||||||||||||||||||||||||

Corporate debt | $ | — | $ | 179 | $ | — | $ | 179 | $ | — | $ | 30 | $ | — | $ | 30 | ||||||||||||||||

Financial institution instruments 1 | 478 | 318 | — | 796 | 335 | 640 | — | 975 | ||||||||||||||||||||||||

Government debt 2 | — | — | — | — | — | 90 | — | 90 | ||||||||||||||||||||||||

Reverse repurchase agreements | — | 1,949 | — | 1,949 | — | 1,399 | — | 1,399 | ||||||||||||||||||||||||

Short-term investments: | ||||||||||||||||||||||||||||||||

Corporate debt | — | 573 | — | 573 | — | 672 | 3 | 675 | ||||||||||||||||||||||||

Financial institution instruments 1 | — | 1,740 | — | 1,740 | — | 1,009 | — | 1,009 | ||||||||||||||||||||||||

Government debt 2 | — | 328 | — | 328 | — | 130 | — | 130 | ||||||||||||||||||||||||

Trading assets: | ||||||||||||||||||||||||||||||||

Asset-backed securities | — | — | — | — | — | 2 | — | 2 | ||||||||||||||||||||||||

Corporate debt | — | 2,562 | — | 2,562 | — | 2,842 | — | 2,842 | ||||||||||||||||||||||||

Financial institution instruments 1 | 29 | 1,299 | — | 1,328 | 59 | 1,064 | — | 1,123 | ||||||||||||||||||||||||

Government debt 2 | 28 | 3,220 | — | 3,248 | 30 | 4,758 | — | 4,788 | ||||||||||||||||||||||||

Other current assets: | ||||||||||||||||||||||||||||||||

Derivative assets | — | 150 | — | 150 | — | 279 | — | 279 | ||||||||||||||||||||||||

Loans receivable 3 | — | 304 | — | 304 | — | 30 | — | 30 | ||||||||||||||||||||||||

Marketable equity securities | 3,039 | — | — | 3,039 | 4,148 | 44 | — | 4,192 | ||||||||||||||||||||||||

Other long-term investments: | ||||||||||||||||||||||||||||||||

Corporate debt | — | 1,868 | — | 1,868 | — | 1,576 | 4 | 1,580 | ||||||||||||||||||||||||

Financial institution instruments 1 | — | 1,096 | — | 1,096 | — | 1,397 | — | 1,397 | ||||||||||||||||||||||||

Government debt 2 | — | 598 | — | 598 | — | 735 | — | 735 | ||||||||||||||||||||||||

Other long-term assets: | ||||||||||||||||||||||||||||||||

Derivative assets | — | 47 | — | 47 | — | 77 | 7 | 84 | ||||||||||||||||||||||||

Loans receivable 3 | — | 294 | — | 294 | — | 610 | — | 610 | ||||||||||||||||||||||||

Total assets measured and recorded at fair value | 3,574 | 16,525 | — | 20,099 | 4,572 | 17,384 | 14 | 21,970 | ||||||||||||||||||||||||

Liabilities | ||||||||||||||||||||||||||||||||

Other accrued liabilities: | ||||||||||||||||||||||||||||||||

Derivative liabilities | — | 464 | — | 464 | — | 454 | — | 454 | ||||||||||||||||||||||||

Other long-term liabilities: | ||||||||||||||||||||||||||||||||

Derivative liabilities | — | 761 | 106 | 867 | — | 297 | 6 | 303 | ||||||||||||||||||||||||

Total liabilities measured and recorded at fair value | $ | — | $ | 1,225 | $ | 106 | $ | 1,331 | $ | — | $ | 751 | $ | 6 | $ | 757 | ||||||||||||||||

1 | Level 1 investments consist of money market funds. Level 2 investments consist primarily of commercial paper, certificates of deposit, time deposits, and notes and bonds issued by financial institutions. |

2 | Level 1 investments consist primarily of U.S. Treasury securities. Level 2 investments consist primarily of U.S. Agency notes and non-U.S. government debt. |

3 | The fair value of our loans receivable for which we elected the fair value option did not significantly differ from the contractual principal balance based on the contractual currency. |

FINANCIAL STATEMENTS | Notes to Financial Statements | 19 |

ASSETS MEASURED AND RECORDED AT FAIR VALUE ON A NON-RECURRING BASIS

Our non-marketable equity securities, equity method investments, and certain non-financial assets, such as intangible assets and property, plant and equipment, are recorded at fair value only if an impairment or observable price adjustment is recognized in the current period. If an observable price adjustment or impairment is recognized on our non-marketable equity securities during the period, we classify these assets as Level 3 within the fair value hierarchy based on the nature of the fair value inputs.

FINANCIAL INSTRUMENTS NOT RECORDED AT FAIR VALUE ON A RECURRING BASIS

Financial instruments not recorded at fair value on a recurring basis include non-marketable equity securities (that have not been re-measured or impaired in the current period), equity method investments, grants receivable, loans receivable, reverse repurchase agreements and our short-term and long-term debt.

Prior to the adoption of the new financial instrument standard, our non-marketable cost method investments were disclosed at fair value on a recurring basis and the carrying amount and fair value as of December 30, 2017 was $2.6 billion and $3.6 billion, respectively. These assets were classified as Level 3 within the fair value hierarchy based on the nature of the fair value inputs.

As of September 29, 2018, the aggregate carrying value of grants receivable, loans receivable, and reverse repurchase agreements was $1.1 billion (the aggregate carrying amount as of December 30, 2017 was $935 million). The estimated fair value of these financial instruments approximates their carrying value and is categorized as Level 2 within the fair value hierarchy based on the nature of the fair value inputs.

As of September 29, 2018, the fair value of short and long-term debt (excluding drafts payable) was $29.3 billion (the fair value as of December 30, 2017 was $29.4 billion). These liabilities are classified as Level 2 within the fair value hierarchy based on the nature of the fair value inputs.

NOTE 13: OTHER COMPREHENSIVE INCOME (LOSS)

The changes in accumulated other comprehensive income (loss) by component and related tax effects in the first nine months of 2018 were as follows:

(In Millions) | Unrealized Holding Gains (Losses) on Available-for-Sale Equity Investments | Unrealized Holding Gains (Losses) on Derivatives | Actuarial Valuation and Other Pension Expenses | Translation adjustments and other | Total | |||||||||||||||

Balance as of December 30, 2017 | $ | 1,745 | $ | 106 | $ | (963 | ) | $ | (26 | ) | $ | 862 | ||||||||

Impact of change in accounting standards | (1,745 | ) | 24 | (65 | ) | (4 | ) | (1,790 | ) | |||||||||||

Opening Balance as of December 31, 2017 | $ | — | $ | 130 | $ | (1,028 | ) | $ | (30 | ) | $ | (928 | ) | |||||||

Other comprehensive income (loss) before reclassifications | — | (203 | ) | 3 | (31 | ) | (231 | ) | ||||||||||||

Amounts reclassified out of accumulated other comprehensive income (loss) | — | (55 | ) | 48 | 8 | 1 | ||||||||||||||

Tax effects | — | 59 | (12 | ) | 8 | 55 | ||||||||||||||

Other comprehensive income (loss) | — | (199 | ) | 39 | (15 | ) | (175 | ) | ||||||||||||

Balance as of September 29, 2018 | $ | — | $ | (69 | ) | $ | (989 | ) | $ | (45 | ) | $ | (1,103 | ) | ||||||

FINANCIAL STATEMENTS | Notes to Financial Statements | 20 |

The amounts reclassified out of accumulated other comprehensive income (loss) into the consolidated condensed statements of income for each period were as follows:

Income Before Taxes Impact (In Millions) | ||||||||||||||||||

Three Months Ended | Nine Months Ended | |||||||||||||||||

Comprehensive Income Components | Location | Sep 29, 2018 | Sep 30, 2017 | Sep 29, 2018 | Sep 30, 2017 | |||||||||||||

Unrealized holding gains (losses) on available-for-sale equity investments: | ||||||||||||||||||

Gains (losses) on equity investments, net | $ | — | $ | 916 | $ | — | $ | 1,962 | ||||||||||

— | 916 | — | 1,962 | |||||||||||||||

Unrealized holding gains (losses) on derivatives: | ||||||||||||||||||

Foreign currency contracts | Cost of sales | (14 | ) | (13 | ) | 5 | (60 | ) | ||||||||||

Research and development | (11 | ) | 24 | 60 | 10 | |||||||||||||

Marketing, general and administrative | (1 | ) | 4 | 31 | (2 | ) | ||||||||||||

Gains (losses) on equity investments, net | — | 12 | — | 28 | ||||||||||||||

Interest and other, net | (6 | ) | 17 | (41 | ) | 52 | ||||||||||||

(32 | ) | 44 | 55 | 28 | ||||||||||||||

Amortization of pension and postretirement benefit components: | ||||||||||||||||||

Actuarial valuation and other pension expenses | — | (18 | ) | (48 | ) | (46 | ) | |||||||||||

— | (18 | ) | (48 | ) | (46 | ) | ||||||||||||

Translation adjustments and other | Interest and other, net | (2 | ) | — | (8 | ) | (507 | ) | ||||||||||

Total amounts reclassified out of accumulated other comprehensive income (loss) | $ | (34 | ) | $ | 942 | $ | (1 | ) | $ | 1,437 | ||||||||

The amortization of pension and postretirement benefit components is included in the computation of net periodic benefit cost. For more information, see "Note 18: Retirement Benefit Plans" in our 2017 Form 10-K.

We estimate that we will reclassify approximately $143 million (before taxes) of net derivative losses included in accumulated other comprehensive income (loss) into earnings within the next 12 months.

FINANCIAL STATEMENTS | Notes to Financial Statements | 21 |

NOTE 14: DERIVATIVE FINANCIAL INSTRUMENTS

For further information on our derivative policies, see "Note 2: Accounting Policies" in our 2017 Form 10-K.

VOLUME OF DERIVATIVE ACTIVITY

Total gross notional amounts for outstanding derivatives (recorded at fair value) at the end of each period were as follows:

(In Millions) | Sep 29, 2018 | Dec 30, 2017 | ||||||

Foreign currency contracts | $ | 19,179 | $ | 19,958 | ||||

Interest rate contracts | 22,936 | 16,823 | ||||||

Other | 1,539 | 1,636 | ||||||

Total | $ | 43,654 | $ | 38,417 | ||||

FAIR VALUE OF DERIVATIVE INSTRUMENTS

September 29, 2018 | December 30, 2017 | |||||||||||||||

(In Millions) | Assets 1 | Liabilities 2 | Assets 1 | Liabilities 2 | ||||||||||||