JOHNSON & JOHNSON - Quarter Report: 2018 April (Form 10-Q)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

þ | Quarterly Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the quarterly period ended April 1, 2018 | |

or

o | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the transition period from to | |

Commission file number 1-3215

(Exact name of registrant as specified in its charter)

NEW JERSEY (State or other jurisdiction of incorporation or organization) | 22-1024240 (I.R.S. Employer Identification No.) | |

One Johnson & Johnson Plaza

New Brunswick, New Jersey 08933

(Address of principal executive offices)

Registrant’s telephone number, including area code (732) 524-0400

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. þ Yes o No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). þ Yes o No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer þ | Accelerated filer o | |||

Non-accelerated filer o | (Do not check if a smaller reporting company) | |||

Smaller reporting company o | Emerging growth company o | |||

If an emerging growth company, indicated by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). o Yes þ No

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

On April 26, 2018, 2,682,149,964 shares of Common Stock, $1.00 par value, were outstanding.

JOHNSON & JOHNSON AND SUBSIDIARIES

TABLE OF CONTENTS

Page | ||

No. | ||

EX-10.1 | ||

EX-10.2 | ||

EX-10.3 | ||

EX-31.1 | ||

EX-32.1 | ||

EX-101 INSTANCE DOCUMENT | ||

EX-101 SCHEMA DOCUMENT | ||

EX-101 CALCULATION LINKBASE DOCUMENT | ||

EX-101 LABELS LINKBASE DOCUMENT | ||

EX-101 PRESENTATION LINKBASE DOCUMENT | ||

EX-101 DEFINITION LINKBASE DOCUMENT | ||

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q and Johnson & Johnson's other publicly available documents contain “forward-looking statements” within the meaning of the safe harbor provisions of the United States Private Securities Litigation Reform Act of 1995. Management and representatives of Johnson & Johnson and its subsidiaries (the Company) also may from time to time make forward-looking statements. Forward-looking statements do not relate strictly to historical or current facts and reflect management’s assumptions, views, plans, objectives and projections about the future. Forward-looking statements may be identified by the use of words such as “plans,” “expects,” “will,” “anticipates,” “estimates,” and other words of similar meaning in conjunction with, among other things: discussions of future operations, expected operating results, financial performance; impact of planned acquisitions and dispositions; impact and timing of restructuring initiatives including associated cost savings and other benefits; the Company's strategy for growth; product development activities; regulatory approvals; market position and expenditures.

Because forward-looking statements are based on current beliefs, expectations and assumptions regarding future events, they are subject to uncertainties, risks and changes that are difficult to predict and many of which are outside of the Company's control. Investors should realize that if underlying assumptions prove inaccurate, or known or unknown risks or uncertainties materialize, the Company’s actual results and financial condition could vary materially from expectations and projections expressed or implied in its forward-looking statements. Investors are therefore cautioned not to rely on these forward-looking statements. Risks and uncertainties include, but are not limited to:

Risks Related to Product Development, Market Success and Competition

• | Challenges and uncertainties inherent in innovation and development of new and improved products and technologies on which the Company’s continued growth and success depend, including uncertainty of clinical outcomes, obtaining regulatory approvals, health plan coverage and customer access, and initial and continued commercial success; |

• | Challenges to the Company’s ability to obtain and protect adequate patent and other intellectual property rights for new and existing products and technologies in the United States and other important markets; |

• | The impact of patent expirations, typically followed by the introduction of competing biosimilars and generics and resulting revenue and market share losses; |

• | Increasingly aggressive and frequent challenges to the Company’s patents by competitors and others seeking to launch competing generic, biosimilar or other products and increased receptivity of courts, the United States Patent and Trademark Office and other decision makers to such challenges, potentially resulting in loss of market exclusivity and rapid decline in sales for the relevant product sooner than expected; |

• | Competition in research and development of new and improved products, processes and technologies, which can result in product and process obsolescence; |

• | Competition to reach agreement with third parties for collaboration, licensing, development and marketing agreements for products and technologies; |

• | Competition on the basis of cost-effectiveness, product performance, technological advances and patents attained by competitors; and |

• | Allegations that the Company’s products infringe the patents and other intellectual property rights of third parties, which could adversely affect the Company’s ability to sell the products in question and require the payment of money damages and future royalties. |

Risks Related to Product Liability, Litigation and Regulatory Activity

• | Product efficacy or safety concerns, whether or not based on scientific evidence, potentially resulting in product withdrawals, recalls, regulatory action on the part of the United States Food and Drug Administration (or international counterparts), declining sales and reputational damage; |

• | Impact of significant litigation or government action adverse to the Company, including product liability claims and allegations related to pharmaceutical marketing practices and contracting strategies; |

• | Increased scrutiny of the health care industry by government agencies and state attorneys general resulting in investigations and prosecutions, which carry the risk of significant civil and criminal penalties, including, but not limited to, debarment from government business; |

• | Failure to meet compliance obligations in the McNEIL-PPC, Inc. Consent Decree or the Corporate Integrity Agreements of the Johnson & Johnson Pharmaceutical Affiliates, or any other compliance agreements with governments or government agencies, which could result in significant sanctions; |

• | Potential changes to applicable laws and regulations affecting United States and international operations, including relating to: approval of new products; licensing and patent rights; sales and promotion of health care products; access to, and reimbursement and pricing for, health care products and services; environmental protection and sourcing of raw materials; |

• | Changes in tax laws and regulations, including changes related to The Tax Cuts and Jobs Act in the United States, increasing audit scrutiny by tax authorities around the world and exposures to additional tax liabilities potentially in excess of existing reserves; and |

• | Issuance of new or revised accounting standards by the Financial Accounting Standards Board and regulations by the Securities and Exchange Commission. |

Risks Related to the Company’s Strategic Initiatives and Health Care Market Trends

• | Pricing pressures resulting from trends toward health care cost containment, including the continued consolidation among health care providers, trends toward managed care, the shift toward governments increasingly becoming the primary payers of health care expenses and significant new entrants to the health care markets seeking to reduce costs; |

• | Restricted spending patterns of individual, institutional and governmental purchasers of health care products and services due to economic hardship and budgetary constraints; |

• | Challenges to the Company’s ability to realize its strategy for growth including through externally sourced innovations, such as development collaborations, strategic acquisitions, licensing and marketing agreements, and the potential heightened costs of any such external arrangements due to competitive pressures; |

• | The potential that the expected strategic benefits and opportunities from any planned or completed acquisition or divestiture by the Company, including the integration of Actelion Ltd., may not be realized or may take longer to realize than expected; and |

• | The potential that the expected benefits and opportunities related to past and future restructuring actions may not be realized or may take longer to realize than expected, including due to any required consultation procedures relating to restructuring of workforce. |

Risks Related to Economic Conditions, Financial Markets and Operating Internationally

• | Impact of inflation and fluctuations in interest rates and currency exchange rates and the potential effect of such fluctuations on revenues, expenses and resulting margins; |

• | Potential changes in export/import and trade laws, regulations and policies of the United States and other countries, including any increased trade restrictions or tariffs and potential drug reimportation legislation; |

• | The impact on international operations from financial instability in international economies, sovereign risk, possible imposition of governmental controls and restrictive economic policies, and unstable international governments and legal systems; |

• | Changes to global climate, extreme weather and natural disasters that could affect demand for the Company's products and services, cause disruptions in manufacturing and distribution networks, alter the availability of goods and services within the supply chain, and affect the overall design and integrity of the Company's products and operations; and |

• | The impact of armed conflicts and terrorist attacks in the United States and other parts of the world including social and economic disruptions and instability of financial and other markets. |

Risks Related to Supply Chain and Operations

• | Difficulties and delays in manufacturing, internally or within the supply chain, that may lead to voluntary or involuntary business interruptions or shutdowns, product shortages, withdrawals or suspensions of products from the market, and potential regulatory action; |

• | Interruptions and breaches of the Company's information technology systems, and those of the Company's vendors, could result in reputational, competitive, operational or other business harm as well as financial costs and regulatory action; |

• | Reliance on global supply chains and production and distribution processes that are complex and subject to increasing regulatory requirements that may adversely affect supply, sourcing and pricing of materials used in the Company’s products; and |

• | The potential that the expected benefits and opportunities related to restructuring actions contemplated for the global supply chain may not be realized or may take longer to realize than expected, including due to any required consultation procedures relating to restructuring of workforce and any required approvals from applicable regulatory authorities. Disruptions associated with the recently announced global supply chain actions may adversely affect supply and sourcing of materials used in the Company's products. |

Investors also should carefully read the Risk Factors described in Item 1A of the Company's Annual Report on Form 10-K for the fiscal year ended December 31, 2017, for a description of certain risks that could, among other things, cause the Company’s actual results to differ materially from those expressed in its forward-looking statements. Investors should understand that it is not possible to predict or identify all such factors and should not consider the risks described above to be a complete statement of all potential risks and uncertainties. The Company does not undertake to publicly update any forward-looking statement that may be made from time to time, whether as a result of new information or future events or developments.

Part I — FINANCIAL INFORMATION

Item 1 — FINANCIAL STATEMENTS

JOHNSON & JOHNSON AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

(Unaudited; Dollars in Millions Except Share and Per Share Data)

April 1, 2018 | December 31, 2017 | ||||||

ASSETS | |||||||

Current assets: | |||||||

Cash and cash equivalents | $ | 14,639 | 17,824 | ||||

Marketable securities | 565 | 472 | |||||

Accounts receivable, trade, less allowances for doubtful accounts $281 (2017, $291) | 14,166 | 13,490 | |||||

Inventories (Note 2) | 9,014 | 8,765 | |||||

Prepaid expenses and other | 2,641 | 2,537 | |||||

Assets held for sale (Note 10) | 1,743 | — | |||||

Total current assets | 42,768 | 43,088 | |||||

Property, plant and equipment at cost | 41,996 | 41,466 | |||||

Less: accumulated depreciation | (24,956 | ) | (24,461 | ) | |||

Property, plant and equipment, net | 17,040 | 17,005 | |||||

Intangible assets, net (Note 3) | 52,365 | 53,228 | |||||

Goodwill (Note 3) | 31,149 | 31,906 | |||||

Deferred taxes on income | 8,785 | 7,105 | |||||

Other assets | 4,518 | 4,971 | |||||

Total assets | $ | 156,625 | 157,303 | ||||

LIABILITIES AND SHAREHOLDERS’ EQUITY | |||||||

Current liabilities: | |||||||

Loans and notes payable | $ | 2,696 | 3,906 | ||||

Accounts payable | 6,443 | 7,310 | |||||

Accrued liabilities | 6,535 | 7,304 | |||||

Accrued rebates, returns and promotions | 7,956 | 7,210 | |||||

Accrued compensation and employee related obligations | 1,892 | 2,953 | |||||

Accrued taxes on income | 1,559 | 1,854 | |||||

Total current liabilities | 27,081 | 30,537 | |||||

Long-term debt (Note 4) | 29,837 | 30,675 | |||||

Deferred taxes on income | 8,057 | 8,368 | |||||

Employee related obligations | 10,066 | 10,074 | |||||

Long-term taxes payable | 9,453 | 8,472 | |||||

Other liabilities | 8,876 | 9,017 | |||||

Total liabilities | 93,370 | 97,143 | |||||

Shareholders’ equity: | |||||||

Common stock — par value $1.00 per share (authorized 4,320,000,000 shares; issued 3,119,843,000 shares) | $ | 3,120 | 3,120 | ||||

Accumulated other comprehensive income (loss) (Note 7) | (12,608 | ) | (13,199 | ) | |||

Retained earnings | 104,339 | 101,793 | |||||

Less: common stock held in treasury, at cost (437,654,000 and 437,318,000 shares) | 31,596 | 31,554 | |||||

Total shareholders’ equity | 63,255 | 60,160 | |||||

Total liabilities and shareholders' equity | $ | 156,625 | 157,303 | ||||

See Notes to Consolidated Financial Statements

1

JOHNSON & JOHNSON AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF EARNINGS

(Unaudited; Dollars & Shares in Millions Except Per Share Amounts)

Fiscal First Quarters Ended | ||||||||||||||

April 1, 2018 | Percent to Sales | April 2, 2017 | Percent to Sales | |||||||||||

Sales to customers (Note 9) | $ | 20,009 | 100.0 | % | $ | 17,766 | 100.0 | % | ||||||

Cost of products sold | 6,614 | 33.1 | 5,409 | 30.4 | ||||||||||

Gross profit | 13,395 | 66.9 | 12,357 | 69.6 | ||||||||||

Selling, marketing and administrative expenses | 5,263 | 26.3 | 4,763 | 26.8 | ||||||||||

Research and development expense | 2,404 | 12.0 | 2,070 | 11.7 | ||||||||||

Interest income | (114 | ) | (0.6 | ) | (121 | ) | (0.7 | ) | ||||||

Interest expense, net of portion capitalized | 259 | 1.3 | 204 | 1.2 | ||||||||||

Other (income) expense, net | 60 | 0.3 | (219 | ) | (1.3 | ) | ||||||||

Restructuring (Note 12) | 42 | 0.2 | 85 | 0.5 | ||||||||||

Earnings before provision for taxes on income | 5,481 | 27.4 | 5,575 | 31.4 | ||||||||||

Provision for taxes on income (Note 5) | 1,114 | 5.6 | 1,153 | 6.5 | ||||||||||

NET EARNINGS | $ | 4,367 | 21.8 | % | $ | 4,422 | 24.9 | % | ||||||

NET EARNINGS PER SHARE (Note 8) | ||||||||||||||

Basic | $ | 1.63 | $ | 1.63 | ||||||||||

Diluted | $ | 1.60 | $ | 1.61 | ||||||||||

CASH DIVIDENDS PER SHARE | $ | 0.84 | $ | 0.80 | ||||||||||

AVG. SHARES OUTSTANDING | ||||||||||||||

Basic | 2,682.2 | 2,706.6 | ||||||||||||

Diluted | 2,731.9 | 2,754.5 | ||||||||||||

Prior year amounts have been reclassified to conform to current year presentation

See Notes to Consolidated Financial Statements

2

JOHNSON & JOHNSON AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(Unaudited; Dollars in Millions)

Fiscal Three Months Ended | ||||||

April 1, 2018 | April 2, 2017 | |||||

Net earnings | $ | 4,367 | 4,422 | |||

Other comprehensive income (loss), net of tax | ||||||

Foreign currency translation | 623 | 395 | ||||

Securities:(1) | ||||||

Unrealized holding gain (loss) arising during period | — | 89 | ||||

Reclassifications to earnings | — | (179 | ) | |||

Net change | — | (90 | ) | |||

Employee benefit plans: | ||||||

Prior service cost amortization during period | (6 | ) | (4 | ) | ||

Gain (loss) amortization during period | 192 | 123 | ||||

Net change | 186 | 119 | ||||

Derivatives & hedges: | ||||||

Unrealized gain (loss) arising during period | (164 | ) | (224 | ) | ||

Reclassifications to earnings | 178 | 179 | ||||

Net change | 14 | (45 | ) | |||

Other comprehensive income (loss) | 823 | 379 | ||||

Comprehensive income | $ | 5,190 | 4,801 | |||

(1) 2018 includes the impact from the adoption of ASU 2016-01. For further details see Note 1 to the Consolidated Financial Statements | ||||||

See Notes to Consolidated Financial Statements

The tax effects in other comprehensive income for the fiscal first quarters were as follows for 2018 and 2017, respectively: Foreign Currency Translation: $163 million in 2018 due to the enactment of the U.S. Tax Cuts and Jobs Act; Securities: $0 million and $48 million; Employee Benefit Plans: $52 million and $60 million; Derivatives & Hedges: $4 million and $24 million. |

3

JOHNSON & JOHNSON AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF CASH FLOWS (Unaudited; Dollars in Millions) | |||||||

Fiscal Three Months Ended | |||||||

April 1, 2018 | April 2, 2017 | ||||||

CASH FLOWS FROM OPERATING ACTIVITIES | |||||||

Net earnings | $ | 4,367 | 4,422 | ||||

Adjustments to reconcile net earnings to cash flows from operating activities: | |||||||

Depreciation and amortization of property and intangibles | 1,746 | 912 | |||||

Stock based compensation | 268 | 229 | |||||

Asset write-downs | — | 37 | |||||

Deferred tax provision | 44 | (27 | ) | ||||

Accounts receivable allowances | (20 | ) | (13 | ) | |||

Changes in assets and liabilities, net of effects from acquisitions and divestitures: | |||||||

Increase in accounts receivable | (479 | ) | (96 | ) | |||

Increase in inventories | (322 | ) | (368 | ) | |||

Decrease in accounts payable and accrued liabilities | (1,686 | ) | (2,030 | ) | |||

Increase in other current and non-current assets | (907 | ) | (424 | ) | |||

Increase in other current and non-current liabilities | 595 | 271 | |||||

NET CASH FLOWS FROM OPERATING ACTIVITIES | 3,606 | 2,913 | |||||

CASH FLOWS FROM INVESTING ACTIVITIES | |||||||

Additions to property, plant and equipment | (658 | ) | (560 | ) | |||

Proceeds from the disposal of assets/businesses, net | 20 | 31 | |||||

Acquisitions, net of cash acquired | (82 | ) | (4,852 | ) | |||

Purchases of investments | (548 | ) | (4,550 | ) | |||

Sales of investments | 341 | 8,994 | |||||

Other | 2 | 1 | |||||

NET CASH USED BY INVESTING ACTIVITIES | (925 | ) | (936 | ) | |||

CASH FLOWS FROM FINANCING ACTIVITIES | |||||||

Dividends to shareholders | (2,253 | ) | (2,171 | ) | |||

Repurchase of common stock | (1,444 | ) | (3,342 | ) | |||

Proceeds from short-term debt | 26 | 719 | |||||

Retirement of short-term debt | (2,484 | ) | (195 | ) | |||

Proceeds from long-term debt, net of issuance costs | 2 | 4,464 | |||||

Retirement of long-term debt | (8 | ) | (2 | ) | |||

Proceeds from the exercise of stock options/employee withholding tax on stock awards, net | 66 | 402 | |||||

Other | 125 | (25 | ) | ||||

NET CASH USED BY FINANCING ACTIVITIES | (5,970 | ) | (150 | ) | |||

Effect of exchange rate changes on cash and cash equivalents | 104 | 110 | |||||

(Decrease)/Increase in cash and cash equivalents | (3,185 | ) | 1,937 | ||||

Cash and Cash equivalents, beginning of period | 17,824 | 18,972 | |||||

CASH AND CASH EQUIVALENTS, END OF PERIOD | $ | 14,639 | 20,909 | ||||

Acquisitions | |||||||

Fair value of assets acquired | $ | 119 | 5,250 | ||||

Fair value of liabilities assumed and noncontrolling interests | (37 | ) | (398 | ) | |||

Net cash paid for acquisitions | $ | 82 | 4,852 | ||||

Prior year amounts have been reclassified to conform to current year presentation

See Notes to Consolidated Financial Statements

4

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

NOTE 1 — The accompanying unaudited interim consolidated financial statements and related notes should be read in conjunction with the audited Consolidated Financial Statements of Johnson & Johnson and its subsidiaries (the Company) and related notes as contained in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2017. The unaudited interim financial statements include all adjustments (consisting only of normal recurring adjustments) and accruals necessary in the judgment of management for a fair statement of the results for the periods presented.

New Accounting Standards

Recently Adopted Accounting Standards

ASU 2014-09: Revenue from Contracts with Customers

On January 1, 2018, the Company adopted the new accounting standard, ASC 606, Revenue from Contracts with Customers and all the related amendments (new revenue standard) to all contracts using the modified retrospective method. The cumulative effect of initially applying the new standard was recognized as an adjustment to the opening balance of retained earnings. The comparative information has not been restated and continues to be reported under the accounting standards in effect for those periods. The adoption of the new revenue standard has not had a material impact to either reported Sales to customers or Net earnings. Additionally, the Company will continue to recognize revenue from product sales as goods are shipped or delivered to the customer, as control of goods occurs at the same time.

In accordance with the new standard requirements, the disclosure of the impact of adoption on the Company's Consolidated Statement of Earnings and Balance Sheet was as follows:

Statement of Earnings - For the fiscal three months ended April 1, 2018 | |||||||||

(Dollars in millions) | As Reported | Effect of change | Balance without adoption of ASC 606 | ||||||

Sales to customers | $ | 20,009 | (29 | ) | 19,980 | ||||

Net earnings | 4,367 | (25 | ) | 4,342 | |||||

Balance Sheet - As of April 1, 2018 | |||||||||

As Reported | Effect of change | Balance without adoption of ASC 606 | |||||||

Assets | 156,625 | 19 | 156,644 | ||||||

Liabilities | 93,370 | (3 | ) | 93,367 | |||||

Equity | $ | 63,255 | 22 | 63,277 | |||||

The Company made a cumulative effect adjustment to the 2018 opening balance of retained earnings upon adoption of ASU 2014-09, which decreased beginning retained earnings by $47 million.

As part of the adoption of ASC 606 see Note 9 to the Consolidated Financial Statements for further disaggregation of revenue.

The Company recognizes revenue from product sales when obligations under the terms of a contract with the customer are satisfied; generally, this occurs with the transfer of control of the goods to customers. The Company's global payment terms are typically between 30 to 90 days. Provisions for certain rebates, sales incentives, trade promotions, coupons, product returns and discounts to customers are accounted as variable consideration and recorded as a reduction in sales.

Product discounts granted are based on the terms of arrangements with direct, indirect and other market participants, as well as market conditions, including prices charged by competitors. Rebates, which include the Medicaid rebate provision, are estimated based on contractual terms, historical experience, patient outcomes, trend analysis and projected market conditions in the various markets served. The Company evaluates market conditions for products or groups of products primarily through the analysis of wholesaler and other third-party sell-through and market research data, as well as internally generated information.

Sales returns are estimated and recorded based on historical sales and returns information. Products that exhibit unusual sales or return patterns due to dating, competition or other marketing matters are specifically investigated and analyzed as part of the accounting for sales return accruals.

5

Sales returns allowances represent a reserve for products that may be returned due to expiration, destruction in the field, or in specific areas, product recall. The sales returns reserve is based on historical return trends by product and by market as a percent to gross sales. In accordance with the Company’s accounting policies, the Company generally issues credit to customers for returned goods. The Company’s sales returns reserves are accounted for in accordance with the U.S. GAAP guidance for revenue recognition when right of return exists. Sales returns reserves are recorded at full sales value. Sales returns in the Consumer and Pharmaceutical segments are almost exclusively not resalable. Sales returns for certain franchises in the Medical Devices segment are typically resalable but are not material. The Company infrequently exchanges products from inventory for returned products. The sales returns reserve for the total Company has been approximately 1.0% of annual net trade sales during the fiscal reporting years 2017, 2016 and 2015.

Promotional programs, such as product listing allowances and cooperative advertising arrangements, are recorded in the same period as related sales. Continuing promotional programs include coupons and volume-based sales incentive programs. The redemption cost of consumer coupons is based on historical redemption experience by product and value. Volume-based incentive programs are based on the estimated sales volumes for the incentive period and are recorded as products are sold. The Company also earns service revenue for co-promotion of certain products, which is included in sales to customers. These arrangements are evaluated to determine the appropriate amounts to be deferred or recorded as a reduction of revenue.

ASU 2016-01: Financial Instruments: Recognition and Measurement of Financial Assets and Financial Liabilities

The Company adopted this standard as of the beginning of the fiscal year 2018 on a modified retrospective basis. The amendments in this update supersede the guidance to classify equity securities with readily determinable fair values into different categories (that is, trading or available-for-sale) and require equity securities to be measured at fair value with changes in the fair value recognized through net earnings. The standard amends financial reporting by providing relevant information about an entity’s equity investments and reducing the number of items that are recognized in other comprehensive income.

The Company made a cumulative effect adjustment to the opening balance of retained earnings upon adoption of ASU 2016-01 that increased retained earnings by $232 million net of tax and decreased accumulated other comprehensive income for previously unrealized gains from equity investments. For additional details see Note 4 to the Consolidated Financial Statements.

ASU 2016-16: Income Taxes: Intra-Entity Transfers of Assets Other Than Inventory

The Company adopted this standard as of the beginning of the fiscal year 2018. This update removes the current exception in U.S. GAAP prohibiting entities from recognizing current and deferred income tax expenses or benefits related to transfer of assets, other than inventory, within the consolidated entity. The current exception to defer the recognition of any tax impact on the transfer of inventory within the consolidated entity until it is sold to a third party remains unaffected. The Company recorded net adjustments to deferred taxes of approximately $2.0 billion, a decrease to Other Assets of approximately $0.7 billion and an increase to retained earnings of approximately $1.3 billion. The Company does not expect the adoption of this standard to have a significant impact on the Company's 2018 financial results.

ASU 2017-01: Clarifying the Definition of a Business

The Company adopted this standard as of the beginning of the fiscal year 2018. This update narrows the definition of a business by providing a screen to determine when an integrated set of assets and activities is not a business. The screen specifies that an integrated set of assets and activities is not a business if substantially all of the fair value of the gross assets acquired or disposed of is concentrated in a single or a group of similar identifiable assets. This update was applied prospectively. The adoption of this standard did not have a material impact on the Company's consolidated financial statements.

ASU 2017-07: Improving the Presentation of Net Periodic Pension Cost and Net Periodic Postretirement Benefit Cost

The Company adopted this standard as of the beginning of the fiscal year 2018. This update requires that an employer disaggregate the service cost component from the other components of net periodic benefit cost (“NPBC”). In addition, only the service cost component will be eligible for capitalization. The amendments in this update are required to be applied retrospectively for the presentation of the service cost component and the other components of NPBC in the Consolidated Statement of Earnings and prospectively, on and after the adoption date, for the capitalization of the service cost component of NPBC in assets. As required by the transition provisions of this update, the Company made the following reclassifications to the 2017 fiscal first quarter Consolidated Statement of Earnings to retroactively apply classification of the service cost component and the other components of NPBC:

6

(Dollars In millions) | Increase (Decrease) to Net Expense | ||

Cost of products sold | $ | 23 | |

Selling, marketing and administrative expenses | 26 | ||

Research and development expense | 10 | ||

Other (income) expense, net | (59 | ) | |

Earnings before provision for taxes on income | $ | — | |

The following table summarizes the cumulative effect adjustments made to the 2018 opening balance of retained earnings upon adoption of the new accounting standards mentioned above:

(Dollars in Millions) | Cumulative Effect Adjustment Increase (Decrease) to Retained Earnings | |||

ASU 2014-09 - Revenue from Contracts with Customers | $ | (47 | ) | |

ASU 2016-01 - Financial Instruments | 232 | |||

ASU 2016-16 - Income Taxes: Intra-Entity Transfers | 1,311 | |||

Total | $ | 1,496 | ||

Recently Issued Accounting Standards

Not Adopted as of April 1, 2018

ASU 2018-02: Reclassification of Certain Tax Effects from Accumulated Other Comprehensive Income

This update allows a reclassification from accumulated other comprehensive income to retained earnings for stranded tax effects resulting from the Tax Cuts and Job Act enacted in December 2017. This update will be effective for the Company for fiscal years beginning after December 15, 2018 and interim periods within those fiscal years. Early adoption is permitted. The Company does not expect this standard to have a material impact on the Company's consolidated financial statements.

ASU 2017-12: Targeted Improvements to Accounting for Hedging Activities

This update makes more financial and nonfinancial hedging strategies eligible for hedge accounting. It also amends the presentation and disclosure requirements and changes how companies assess effectiveness. This update will be effective for the Company for fiscal years beginning after December 15, 2018, and interim periods within those fiscal years. Early adoption is permitted. The Company is planning to early adopt this standard in the fiscal second quarter of 2018 and does not expect the adoption to have a material impact on its financial statements.

ASU 2016-02: Leases

This update requires the recognition of lease assets and lease liabilities on the balance sheet for all lease obligations and disclosing key information about leasing arrangements. This update requires the recognition of lease assets and lease liabilities by lessees for those leases classified as operating leases under current generally accepted accounting principles. This update will be effective for the Company for all annual periods beginning after December 15, 2018, including interim periods within those fiscal years. Early application is permitted. The Company anticipates that most of its operating leases will result in the recognition of additional assets and the corresponding liabilities on its Consolidated Balance Sheets, however it does not expect the standard to have a material impact on the financial position. The actual impact will depend on the Company's lease portfolio at the time of adoption. The Company continues to assess all implications of the standard and related financial disclosures.

NOTE 2 — INVENTORIES

(Dollars in Millions) | April 1, 2018 | December 31, 2017 | |||||

Raw materials and supplies | $ | 1,200 | 1,140 | ||||

Goods in process | 2,339 | 2,317 | |||||

Finished goods | 5,475 | 5,308 | |||||

Total inventories(1) | $ | 9,014 | 8,765 | ||||

(1) Net of approximately $0.1 billion classified as assets held for sale on the Consolidated Balance Sheet, related to the divestiture of the LifeScan business which was pending as of April 1, 2018

7

NOTE 3 — INTANGIBLE ASSETS AND GOODWILL

Intangible assets that have finite useful lives are amortized over their estimated useful lives. The latest annual impairment assessment of goodwill and indefinite lived intangible assets was completed in the fiscal fourth quarter of 2017. Future impairment tests for goodwill and indefinite lived intangible assets will be performed annually in the fiscal fourth quarter, or sooner, if warranted.

(Dollars in Millions) | April 1, 2018 | December 31, 2017 | |||||

Intangible assets with definite lives: | |||||||

Patents and trademarks — gross | $ | 35,980 | 36,427 | ||||

Less accumulated amortization | 7,594 | 7,223 | |||||

Patents and trademarks — net (1) | 28,386 | 29,204 | |||||

Customer relationships and other intangibles — gross | 21,141 | 20,204 | |||||

Less accumulated amortization | 7,748 | 7,463 | |||||

Customer relationships and other intangibles — net | 13,393 | 12,741 | |||||

Intangible assets with indefinite lives: | |||||||

Trademarks | 7,113 | 7,082 | |||||

Purchased in-process research and development | 3,473 | 4,201 | |||||

Total intangible assets with indefinite lives | 10,586 | 11,283 | |||||

Total intangible assets — net | $ | 52,365 | 53,228 | ||||

(1) Net of approximately $0.6 billion classified as assets held for sale on the Consolidated Balance Sheet. $0.5 billion is related to the divestiture of Valchlor and $0.1 billion is related to the divestiture of the LifeScan business, both of which were pending as of April 1, 2018.

Goodwill as of April 1, 2018 was allocated by segment of business as follows:

(Dollars in Millions) | Consumer | Pharm | Med Devices | Total | |||||||||

Goodwill, net at December 31, 2017 | $ | 8,875 | 9,109 | 13,922 | 31,906 | ||||||||

Goodwill, related to acquisitions | — | — | 53 | 53 | |||||||||

Goodwill, related to divestitures | — | — | — | — | |||||||||

Currency translation/Other | 24 | 147 | (981 | ) | (1) | (810 | ) | ||||||

Goodwill, net at April 1, 2018 | $ | 8,899 | 9,256 | 12,994 | 31,149 | ||||||||

(1) Net of approximately $1.0 billion classified as assets held for sale on the Consolidated Balance Sheet, related to the divestiture of the LifeScan business which was pending as of April 1, 2018.

The weighted average amortization periods for patents and trademarks and customer relationships and other intangible assets are 11 years and 22 years, respectively. The amortization expense of amortizable intangible assets included in cost of products sold was $1.1 billion and $0.3 billion for the fiscal three months ended April 1, 2018 and April 2, 2017, respectively. The estimated amortization expense for the five succeeding years approximates $4.4 billion, before tax, per year. Intangible asset write-downs are included in Other (income) expense, net.

See Note 10 to the Consolidated Financial Statements for additional details related to acquisitions and divestitures.

NOTE 4 — FAIR VALUE MEASUREMENTS

The Company uses forward foreign exchange contracts to manage its exposure to the variability of cash flows, primarily related to the foreign exchange rate changes of future intercompany products and third-party purchases of materials denominated in a foreign currency. The Company uses cross currency interest rate swaps to manage currency risk primarily related to borrowings.

The Company also uses equity collar contracts to manage exposure to market risk associated with certain equity investments.

All three types of derivatives are designated as cash flow hedges.

The Company uses interest rate swaps as an instrument to manage interest rate risk related to fixed rate borrowings. These derivatives are designated as fair value hedges. The Company uses forward foreign exchange contracts designated as net investment hedges. Additionally, the Company uses forward foreign exchange contracts to offset its exposure to certain foreign currency assets and liabilities. These forward foreign exchange contracts are not designated as hedges, and therefore, changes in

8

the fair values of these derivatives are recognized in earnings, thereby offsetting the current earnings effect of the related foreign currency assets and liabilities.

The Company does not enter into derivative financial instruments for trading or speculative purposes, or that contain credit risk related contingent features. During the fiscal second quarter of 2017, the Company entered into credit support agreements (CSA) with certain derivative counterparties establishing collateral thresholds based on respective credit ratings and netting agreements. As of April 1, 2018, the total amount of collateral paid under the credit support agreements amounted to $32 million, net. For equity collar contracts, the Company pledged the underlying hedged marketable equity securities to the counter-party as collateral. On an ongoing basis, the Company monitors counter-party credit ratings. The Company considers credit non-performance risk to be low, because the Company primarily enters into agreements with commercial institutions that have at least an investment grade credit rating. Refer to the table on significant financial assets and liabilities measured at fair value contained in this footnote for receivables and payables with these commercial institutions. As of April 1, 2018, the Company had notional amounts outstanding for forward foreign exchange contracts, cross currency interest rate swaps and interest rate swaps of $35.3 billion, $2.3 billion and $1.1 billion, respectively. As of December 31, 2017, the Company had notional amounts outstanding for forward foreign exchange contracts, cross currency interest rate swaps and interest rate swaps of $34.5 billion, $2.3 billion and $1.1 billion, respectively.

All derivative instruments are recorded on the balance sheet at fair value. Changes in the fair value of derivatives are recorded each period in current earnings or other comprehensive income, depending on whether the derivative is designated as part of a hedge transaction, and if so, the type of hedge transaction.

The designation as a cash flow hedge is made at the entrance date of the derivative contract. At inception, all derivatives are expected to be highly effective. Changes in the fair value of a derivative that is designated as a cash flow hedge and is highly effective are recorded in accumulated other comprehensive income until the underlying transaction affects earnings, and are then reclassified to earnings in the same account as the hedged transaction. Gains and losses associated with interest rate swaps and changes in fair value of hedged debt attributable to changes in interest rates are recorded to interest expense in the period in which they occur. Gains and losses on net investment hedges are accounted for through the currency translation account. On an ongoing basis, the Company assesses whether each derivative continues to be highly effective in offsetting changes of hedged items. If a derivative is no longer expected to be highly effective, hedge accounting is discontinued. Hedge ineffectiveness, if any, is included in current period earnings in Other (income) expense, net for forward foreign exchange contracts, cross currency interest rate swaps, net investment hedges and equity collar contracts. For interest rate swaps designated as fair value hedges, hedge ineffectiveness, if any, is included in current period earnings within interest expense. For the current reporting period, hedge ineffectiveness associated with interest rate swaps was not material.

During the fiscal second quarter of 2016, the Company designated its Euro denominated notes issued in May 2016 with due dates ranging from 2022 to 2035 as a net investment hedge of the Company's investments in certain of its international subsidiaries that use the Euro as their functional currency in order to reduce the volatility caused by changes in exchange rates.

The change in the carrying value due to remeasurement of these Euro notes resulted in a $150 million unrealized pretax loss for the fiscal first quarter of April 1, 2018 reflected in foreign currency translation adjustment, within the Consolidated Statements of Comprehensive Income. The change in the carrying value due to remeasurement of these Euro notes resulted in a cumulative $372 million unrealized pretax loss from hedge inception through the fiscal first quarter of 2018, reflected in foreign currency translation adjustment, within the Consolidated Statements of Comprehensive Income.

As of April 1, 2018, the balance of deferred net gains on derivatives included in accumulated other comprehensive income was $84 million after-tax. For additional information, see the Consolidated Statements of Comprehensive Income and Note 7. The Company expects that substantially all of the amounts related to forward foreign exchange contracts will be reclassified into earnings over the next 12 months as a result of transactions that are expected to occur over that period. The maximum length of time over which the Company is hedging transaction exposure is 18 months, excluding interest rate contracts, net investment hedges and equity collar contracts. The amount ultimately realized in earnings may differ as foreign exchange rates change. Realized gains and losses are ultimately determined by actual exchange rates at maturity of the derivative.

9

The following table is a summary of the activity related to derivatives designated as cash flow hedges for the fiscal first quarters in 2018 and 2017:

Gain/(Loss) Recognized In Accumulated OCI (1) | Gain/(Loss) Reclassified From Accumulated OCI Into Income (1) | Gain/(Loss) Recognized In Other Income/Expense (2) | |||||||||||||||||

(Dollars in Millions) | Fiscal First Quarters Ended | ||||||||||||||||||

Cash Flow Hedges By Income Statement Caption | April 1, 2018 | April 2, 2017 | April 1, 2018 | April 2, 2017 | April 1, 2018 | April 2, 2017 | |||||||||||||

Sales to customers (3) | $ | 31 | (13 | ) | 29 | (33 | ) | — | — | ||||||||||

Cost of products sold (3) | 3 | (97 | ) | 2 | (31 | ) | 12 | (17 | ) | ||||||||||

Research and development expense (3) | (237 | ) | (109 | ) | (238 | ) | (102 | ) | — | 5 | |||||||||

Interest (income)/Interest expense, net (4) | 57 | 28 | 40 | 22 | — | — | |||||||||||||

Other (income) expense, net (3) (5) | (18 | ) | (33 | ) | (11 | ) | (35 | ) | 5 | 1 | |||||||||

Total | $ | (164 | ) | (224 | ) | (178 | ) | (179 | ) | 17 | (11 | ) | |||||||

All amounts shown in the table above are net of tax.

(1) Effective portion

(2) Ineffective portion

(3) Forward foreign exchange contracts

(4) Cross currency interest rate swaps

(5) Includes equity collar contracts. The equity collar contracts expired in December of 2017

For the fiscal first quarters ended April 1, 2018 and April 2, 2017, a loss of $19 million and $29 million, respectively, was recognized in Other (income) expense, net, relating to forward foreign exchange contracts not designated as hedging instruments.

10

The Company adopted ASU 2016-01: Financial Instruments: Recognition and Measurement of Financial Assets and Financial Liabilities as of the beginning of the fiscal year 2018. This ASU amends prior guidance to classify equity investments with readily determinable market values into different categories (that is, trading or available-for-sale) and require equity investments to be measured at fair value with changes in fair value recognized through net earnings. The Company made a cumulative effect adjustment to the opening balance of retained earnings upon adoption of ASU 2016-01 which increased retained earnings by $232 million, net of tax, and decreased accumulated other comprehensive income for previously net unrealized gains from equity investments.

The Company holds equity investments with readily determinable fair values and equity investments without readily determinable fair values. The Company has elected to measure equity investments that do not have readily determinable fair values at cost minus impairment, if any, plus or minus changes resulting from observable price changes in orderly transactions for the identical or a similar investment of the same issuer.

The following table is a summary of the activity related to equity investments for the fiscal first quarter of 2018:

(Dollars in Millions) | December 31, 2017 | April 1, 2018 | ||||||||||||||

Carrying Value | Changes in Fair Value Reflected in Net Income (1) | Sales/ Purchases/Other (2) | Carrying Value | Non Current Other Assets | ||||||||||||

Equity Investments with readily determinable value | $ | 751 | (27 | ) | 7 | 731 | 731 | |||||||||

Equity Investments without readily determinable value | $ | 510 | (20 | ) | 83 | 573 | 573 | |||||||||

(1) Recorded in Other Income/Expense

(2) Other includes impact of currency

For equity investments without readily determinable market values, $20 million of the changes in fair value reflected in net income that were the result of impairments. There were no changes related to adjustments due to changes in observable prices.

For the fiscal first quarter ended April 2, 2017, changes in fair value reflected within other comprehensive income due to previously unrealized gains on equity investments with readily determinable fair values net of tax was a net gain of $349 million

Fair value is the exit price that would be received to sell an asset or paid to transfer a liability. Fair value is a market-based measurement determined using assumptions that market participants would use in pricing an asset or liability. The authoritative literature establishes a three-level hierarchy to prioritize the inputs used in measuring fair value. The levels within the hierarchy are described below with Level 1 inputs having the highest priority and Level 3 inputs having the lowest.

The fair value of a derivative financial instrument (i.e. forward foreign exchange contracts, interest rate contracts) is the aggregation by currency of all future cash flows discounted to its present value at the prevailing market interest rates and subsequently converted to the U.S. Dollar at the current spot foreign exchange rate. The Company does not believe that fair values of these derivative instruments materially differ from the amounts that could be realized upon settlement or maturity, or that the changes in fair value will have a material effect on the Company’s results of operations, cash flows or financial position. The Company also holds equity investments which are classified as Level 1 and debt securities which are classified as Level 2. The Company did not have any other significant financial assets or liabilities which would require revised valuations under this standard that are recognized at fair value.

The following three levels of inputs are used to measure fair value:

Level 1 — Quoted prices in active markets for identical assets and liabilities.

Level 2 — Significant other observable inputs.

Level 3 — Significant unobservable inputs.

11

The Company’s significant financial assets and liabilities measured at fair value as of April 1, 2018 and December 31, 2017 were as follows:

April 1, 2018 | December 31, 2017 | |||||||||||||||

(Dollars in Millions) | Level 1 | Level 2 | Level 3 | Total | Total(1) | |||||||||||

Derivatives designated as hedging instruments: | ||||||||||||||||

Assets: | ||||||||||||||||

Forward foreign exchange contracts(7) (8) | $ | — | 351 | — | 351 | 342 | ||||||||||

Interest rate contracts (2)(4) | — | 3 | — | 3 | 7 | |||||||||||

Total | — | 354 | — | 354 | 349 | |||||||||||

Liabilities: | ||||||||||||||||

Forward foreign exchange contracts(7) (9) | — | 269 | — | 269 | 314 | |||||||||||

Interest rate contracts (3)(4)(7) (10) | — | 19 | — | 19 | 15 | |||||||||||

Total | — | 288 | — | 288 | 329 | |||||||||||

Derivatives not designated as hedging instruments: | ||||||||||||||||

Assets: | ||||||||||||||||

Forward foreign exchange contracts | — | 25 | — | 25 | 38 | |||||||||||

Liabilities: | ||||||||||||||||

Forward foreign exchange contracts | — | 53 | — | 53 | 38 | |||||||||||

Other Investments: | ||||||||||||||||

Equity investments (5) | 731 | — | — | 731 | 751 | |||||||||||

Debt securities(6) | $ | — | 2,967 | — | 2,967 | 5,310 | ||||||||||

(1) | 2017 assets and liabilities are all classified as Level 2 with the exception of equity investments of $751 million, which are classified as Level 1. |

(2) | Includes $2 million and $7 million of non-current other assets for April 1, 2018 and December 31, 2017, respectively. |

(3) | Includes $14 million and $9 million of non-current other liabilities for April 1, 2018 and December 31, 2017, respectively. |

(4) | Includes cross currency interest rate swaps and interest rate swaps. |

(5) | Classified as non-current other assets. The carrying amount of the equity investments were $731 million and $751 million as of April 1, 2018 and December 31, 2017, respectively. |

(6) | Classified as cash equivalents and current marketable securities. |

(7) | Includes collateral exchanged on the credit support agreements on derivatives |

(8) | Forward foreign exchange contracts excluding CSA were $478 million and $418 million for April 1, 2018 and December 31, 2017, respectively. |

(9) | Forward foreign exchange contracts excluding CSA were $364 million and $402 million for April 1, 2018 and December 31, 2017, respectively. |

(10) | Interest rate contracts excluding CSA were $83 million and $165 million for April 1, 2018 and December 31, 2017, respectively. |

12

The Company's cash, cash equivalents and current marketable securities as of April 1, 2018 comprised:

April 1, 2018 | ||||||||||||

(Dollars in Millions) | Carrying Amount | Estimated Fair Value | Cash & Cash Equivalents | Current Marketable Securities | ||||||||

Cash | $ | 2,656 | 2,656 | 2,656 | ||||||||

Other Sovereign Securities(1) | 529 | 529 | 529 | |||||||||

U.S. Reverse repurchase agreements | 2,682 | 2,682 | 2,682 | |||||||||

Other Reverse repurchase agreements | 398 | 398 | 398 | |||||||||

Corporate debt securities(1) | 1,869 | 1,869 | 1,864 | 5 | ||||||||

Money market funds | 2,944 | 2,944 | 2,944 | |||||||||

Time deposits(1) | 1,159 | 1,159 | 1,159 | |||||||||

Subtotal | 12,237 | 12,237 | 12,232 | 5 | ||||||||

Gov't securities | 2,705 | 2,705 | 2,370 | 335 | ||||||||

Other Sovereign Securities | 2 | 2 | — | 2 | ||||||||

Corporate debt securities | 260 | 260 | 37 | 223 | ||||||||

Subtotal available for sale debt(2) | $ | 2,967 | 2,967 | 2,407 | 560 | |||||||

Total cash, cash equivalents and current marketable securities | 14,639 | 565 | ||||||||||

(1) Held to maturity investments are reported at amortized cost and gains or losses are reported in earnings.

(2) Available for sale debt securities are reported at fair value with unrealized gains and losses reported net of taxes in other comprehensive income.

In the fiscal first quarter ended April 1, 2018 and the fiscal year ended December 31, 2017 the carrying amount was the same as the estimated fair value.

Fair value of government securities and obligations and corporate debt securities was estimated using quoted broker prices and significant other observable inputs.

The Company classifies all highly liquid investments with stated maturities of three months or less from date of purchase as cash equivalents and all highly liquid investments with stated maturities of greater than three months from the date of purchase as current marketable securities. Available for sale securities with stated maturities of greater than one year from the date of purchase are available for current operations and are classified as cash equivalents and current marketable securities.

The contractual maturities of the available for sale securities at April 1, 2018 are as follows:

(Dollars in Millions) | Cost Basis | Fair Value | |||||

Due within one year | $ | 2,887 | 2,887 | ||||

Due after one year through five years | 80 | 80 | |||||

Due after five years through ten years | — | — | |||||

Total debt securities | $ | 2,967 | 2,967 | ||||

13

Financial Instruments not measured at Fair Value:

The following financial liabilities are held at carrying amount on the consolidated balance sheet as of April 1, 2018:

(Dollars in Millions) | Carrying Amount | Estimated Fair Value | |||||

Financial Liabilities | |||||||

Current Debt | $ | 2,696 | 2,696 | ||||

Non-Current Debt | |||||||

4.75% Notes due 2019 (1B Euro 1.2323) | 1,230 | 1,330 | |||||

1.875% Notes due 2019 | 495 | 492 | |||||

3% Zero Coupon Convertible Subordinated Debentures due in 2020 | 52 | 92 | |||||

1.950% Notes due 2020 | 499 | 492 | |||||

2.95% Debentures due 2020 | 547 | 553 | |||||

3.55% Notes due 2021 | 448 | 461 | |||||

2.45% Notes due 2021 | 349 | 347 | |||||

1.65% Notes due 2021 | 998 | 973 | |||||

0.250% Notes due 2022 (1B Euro 1.2323) | 1,229 | 1,236 | |||||

2.25% Notes due 2022 | 995 | 975 | |||||

6.73% Debentures due 2023 | 250 | 298 | |||||

3.375% Notes due 2023 | 806 | 827 | |||||

2.05% Notes due 2023 | 498 | 478 | |||||

0.650% Notes due 2024 (750MM Euro 1.2323) | 920 | 926 | |||||

5.50% Notes due 2024 (500 MM GBP 1.4063) | 697 | 865 | |||||

2.625% Notes due 2025 | 747 | 722 | |||||

2.45% Notes due 2026 | 1,991 | 1,877 | |||||

2.95% Notes due 2027 | 995 | 968 | |||||

2.90% Notes due 2028 | 1,492 | 1,443 | |||||

1.150% Notes due 2028 (750MM Euro 1.2323) | 916 | 923 | |||||

6.95% Notes due 2029 | 296 | 397 | |||||

4.95% Debentures due 2033 | 498 | 580 | |||||

4.375% Notes due 2033 | 856 | 938 | |||||

1.650% Notes due 2035 (1.5B Euro 1.2323) | 1,830 | 1,907 | |||||

3.55% Notes due 2036 | 987 | 978 | |||||

5.95% Notes due 2037 | 991 | 1,289 | |||||

3.625% Notes due 2037 | 1,486 | 1,479 | |||||

3.40% Notes due 2038 | 990 | 961 | |||||

5.85% Debentures due 2038 | 696 | 908 | |||||

4.50% Debentures due 2040 | 538 | 604 | |||||

4.85% Notes due 2041 | 296 | 340 | |||||

4.50% Notes due 2043 | 495 | 545 | |||||

3.70% Notes due 2046 | 1,971 | 1,966 | |||||

3.75% Notes due 2047 | 991 | 991 | |||||

3.50% Notes due 2048 | 742 | 716 | |||||

Other | 20 | 20 | |||||

Total Non-Current Debt | $ | 29,837 | 30,897 | ||||

The weighted average effective interest rate on non-current debt is 3.19%.

14

The excess of the estimated fair value over the carrying value of debt was $2.0 billion at December 31, 2017.

Fair value of the non-current debt was estimated using market prices, which were corroborated by quoted broker prices and significant other observable inputs.

NOTE 5 — INCOME TAXES

The worldwide effective income tax rates for the fiscal three months of 2018 and 2017 were 20.3% and 20.7%, respectively. The U.S. Tax Cuts and Jobs Act (TCJA) was enacted into law effective January 1, 2018. This law reduces the U.S. statutory corporate tax rate from 35% to 21%, eliminates or reduces certain corporate income tax deductions and introduces a tax on global intangible low-taxed income (GILTI). In December 2017, the Company recorded a provisional tax cost of $13.0 billion related to the enactment of the TCJA. Under the guidance in SEC Staff Accounting Bulletin 118 (SAB 118), the provisional amount was a reasonable estimate based on the most recent information and guidance available related to the calculation of the tax liability and the impact to its deferred tax assets and liabilities, including those recorded for foreign local and withholding taxes as of the 2017 assessment date of January 18, 2018. As noted below, the Company made adjustments in the first quarter of 2018. All amounts recorded remain provisional and may require further adjustments and changes to the Company’s estimates as new guidance is made available. The estimate is subject to the finalization of management’s analysis related to certain matters, such as developing interpretations of the provisions of the TCJA, changes to certain estimates and amounts related to the earnings and profits of certain subsidiaries and the filing of tax returns. Revisions to the provisional charge may be material to the Company's future financial results. See Note 8 to the Consolidated Financial Statements in the Annual Report on Form 10-K for the fiscal year ended December 31, 2017 for further details on the TCJA and SAB 118.

The Company completed its acquisition of AMO in the first fiscal quarter of 2017, and incurred incremental tax costs that were discretely recorded in the first quarter of 2017, which increased the effective tax rate by 3.8% for the first three months of 2017 compared to the same period in 2018. Additionally, in 2018 the Company had more income in higher tax jurisdictions relative to lower tax jurisdictions as compared to 2017. Remeasurement of deferred tax liabilities and assets recorded for the foreign withholding taxes and related U.S. foreign tax credits, respectively, increased the Company’s effective tax rate in 2018 by approximately 1.4% due to changes in the foreign currency exchange rates. Tax benefits received from stock-based compensation during the fiscal three months of 2018 and 2017, reduced the effective tax rate by 2.2% and 3.6%, respectively. The reduction of the U.S. statutory corporate tax rate, offset by the elimination of the corporate income tax deductions, measurement period adjustments(1) and the GILTI tax(2), decreased the Company’s worldwide effective rate as compared to the same period of the prior year. As previously disclosed, the Company has elected to provisionally treat the GILTI tax as a period expense, pending further analysis by management of this new tax provision.

(1)The following adjustments were made to the provisional tax amounts in the first fiscal quarter of 2018 due to issued Treasury guidance and revisions to the Company’s estimates since the assessment date:

• | $0.2 billion increase to the transition tax on previously undistributed foreign earnings as of December 31, 2017 due to U.S. Treasury Department’s issuance of Notice 2018-13 on January 19, 2018 |

• | $0.3 billion decrease to the deferred tax liability for foreign local taxes, partially offset by a decrease of $0.1 billion in deferred tax assets for U.S. foreign tax credits due to updated estimates from the amounts recorded in 2017. |

These measurement period adjustments decreased the Company’s effective tax rate by approximately 0.5% in the first fiscal quarter of 2018 as compared to the same period of the prior year.

(2) The impact of GILTI on the first quarter effective tax rate was an increase of 2.6%.

As of April 1, 2018, the Company had approximately $3.2 billion of liabilities from unrecognized tax benefits. The Company believes it is possible that audits may be completed by tax authorities in some jurisdictions over the next twelve months. The Company is not able to provide a reasonably reliable estimate of the timing of any future tax payments relating to uncertain tax positions.

15

NOTE 6 — PENSIONS AND OTHER BENEFIT PLANS

Components of Net Periodic Benefit Cost

Net periodic benefit cost for the Company’s defined benefit retirement plans and other benefit plans for the fiscal first quarters of 2018 and 2017 include the following components:

Fiscal First Quarters Ended | |||||||||||||

Retirement Plans | Other Benefit Plans | ||||||||||||

(Dollars in Millions) | April 1, 2018 | April 2, 2017 | April 1, 2018 | April 2, 2017 | |||||||||

Service cost | $ | 309 | 251 | 67 | 61 | ||||||||

Interest cost | 252 | 230 | 37 | 39 | |||||||||

Expected return on plan assets | (560 | ) | (505 | ) | (2 | ) | (2 | ) | |||||

Amortization of prior service cost/(credit) | 1 | — | (8 | ) | (7 | ) | |||||||

Recognized actuarial losses | 215 | 152 | 30 | 34 | |||||||||

Curtailments and settlements | (2 | ) | — | — | — | ||||||||

Net periodic benefit cost | $ | 215 | 128 | 124 | 125 | ||||||||

As per the adoption of ASU 2017-07, the service cost component of net periodic benefit cost was presented in the same line items on the Consolidated Statement of Earnings where other employee compensation costs are reported. All other components of net periodic benefit cost are presented as part of Other (income) expense, net on the Consolidated Statement of Earnings.

Company Contributions

For the fiscal three months ended April 1, 2018, the Company contributed $18 million and $9 million to its U.S. and international retirement plans, respectively. The Company plans to continue to fund its U.S. defined benefit plans to comply with the Pension Protection Act of 2006. International plans are funded in accordance with local regulations.

NOTE 7 — ACCUMULATED OTHER COMPREHENSIVE INCOME

Components of other comprehensive income (loss) consist of the following:

Foreign | Gain/(Loss) | Employee | Gain/(Loss) | Total Accumulated | ||||||||||||

Currency | On | Benefit | On Derivatives | Other Comprehensive | ||||||||||||

(Dollars in Millions) | Translation | Securities | Plans | & Hedges | Income (Loss) | |||||||||||

December 31, 2017 | $ | (7,351 | ) | 232 | (6,150 | ) | 70 | (13,199 | ) | |||||||

Net change | 623 | — | 186 | 14 | 823 | |||||||||||

Cumulative adjustment to retained earnings | (232 | ) | (1) | (232 | ) | |||||||||||

April 1, 2018 | $ | (6,728 | ) | — | (5,964 | ) | 84 | (12,608 | ) | |||||||

(1) See Note 1 to the Consolidated Financial Statements for additional details on the adoption of ASU 2016-01

Amounts in accumulated other comprehensive income are presented net of the related tax impact. Foreign currency translation is not adjusted for income taxes where it relates to permanent investments in international subsidiaries. For additional details on comprehensive income see the Consolidated Statements of Comprehensive Income.

Details on reclassifications out of Accumulated Other Comprehensive Income:

Gain/(Loss) On Securities - reclassifications released to Other (income) expense, net.

Employee Benefit Plans - reclassifications are included in net periodic benefit cost. See Note 6 for additional details.

Gain/(Loss) On Derivatives & Hedges - reclassifications to earnings are recorded in the same account as the underlying transaction. See Note 4 for additional details.

16

NOTE 8 — EARNINGS PER SHARE

The following is a reconciliation of basic net earnings per share to diluted net earnings per share for the fiscal first quarters ended April 1, 2018 and April 2, 2017:

Fiscal First Quarters Ended | |||||||

(Shares in Millions) | April 1, 2018 | April 2, 2017 | |||||

Basic net earnings per share | $ | 1.63 | 1.63 | ||||

Average shares outstanding — basic | 2,682.2 | 2,706.6 | |||||

Potential shares exercisable under stock option plans | 139.5 | 141.2 | |||||

Less: shares which could be repurchased under treasury stock method | (90.6 | ) | (94.6 | ) | |||

Convertible debt shares | 0.8 | 1.3 | |||||

Average shares outstanding — diluted | 2,731.9 | 2,754.5 | |||||

Diluted net earnings per share | $ | 1.60 | 1.61 | ||||

The diluted net earnings per share calculation for both the fiscal first quarters ended April 1, 2018 and April 2, 2017 included the dilutive effect of convertible debt that was offset by the related reduction in interest expense.

The diluted net earnings per share calculation for both the fiscal first quarters ended April 1, 2018 and April 2, 2017 included all shares related to stock options, as there were no options or other instruments which were anti-dilutive.

17

NOTE 9 — SEGMENTS OF BUSINESS AND GEOGRAPHIC AREAS

SALES BY SEGMENT OF BUSINESS

Fiscal First Quarters Ended | ||||||||||

(Dollars in Millions) | April 1, 2018 | April 2, 2017 | Percent Change | |||||||

CONSUMER | ||||||||||

Baby Care | ||||||||||

U.S. | $ | 97 | 113 | (14.2 | )% | |||||

International | 360 | 342 | 5.3 | |||||||

Worldwide | 457 | 455 | 0.4 | |||||||

Beauty | ||||||||||

U.S. | 611 | 567 | 7.8 | |||||||

International | 473 | 414 | 14.3 | |||||||

Worldwide | 1,084 | 981 | 10.5 | |||||||

Oral Care | ||||||||||

U.S. | 157 | 156 | 0.6 | |||||||

International | 222 | 206 | 7.8 | |||||||

Worldwide | 379 | 362 | 4.7 | |||||||

OTC | ||||||||||

U.S. | 465 | 477 | (2.5 | ) | ||||||

International | 607 | 536 | 13.2 | |||||||

Worldwide | 1,072 | 1,013 | 5.8 | |||||||

Women's Health | ||||||||||

U.S. | 3 | 3 | 0.0 | |||||||

International | 240 | 239 | 0.4 | |||||||

Worldwide | 243 | 242 | 0.4 | |||||||

Wound Care/Other | ||||||||||

U.S. | 103 | 98 | 5.1 | |||||||

International | 60 | 77 | (22.1 | ) | ||||||

Worldwide | 163 | 175 | (6.9 | ) | ||||||

TOTAL CONSUMER | ||||||||||

U.S. | 1,436 | 1,414 | 1.6 | |||||||

International | 1,962 | 1,814 | 8.2 | |||||||

Worldwide | 3,398 | 3,228 | 5.3 | |||||||

PHARMACEUTICAL | ||||||||||

Immunology | ||||||||||

U.S. | 2,000 | 2,123 | (5.8 | ) | ||||||

International | 1,042 | 807 | 29.1 | |||||||

Worldwide | 3,042 | 2,930 | 3.8 | |||||||

REMICADE® | ||||||||||

U.S. | 916 | 1,182 | (22.5 | ) | ||||||

U.S. Exports | 142 | 165 | (13.9 | ) | ||||||

International | 331 | 325 | 1.8 | |||||||

Worldwide | 1,389 | 1,672 | (16.9 | ) | ||||||

SIMPONI / SIMPONI ARIA® | ||||||||||

18

U.S. | 224 | 229 | (2.2 | ) | ||||||

International | 294 | 199 | 47.7 | |||||||

Worldwide | 518 | 428 | 21.0 | |||||||

STELARA® | ||||||||||

U.S. | 652 | 547 | 19.2 | |||||||

International | 409 | 276 | 48.2 | |||||||

Worldwide | 1,061 | 823 | 28.9 | |||||||

OTHER IMMUNOLOGY | ||||||||||

U.S. | 66 | — | * | |||||||

International | 8 | 7 | 14.3 | |||||||

Worldwide | 74 | 7 | * | |||||||

Infectious Diseases | ||||||||||

U.S. | 333 | 326 | 2.1 | |||||||

International | 497 | 423 | 17.5 | |||||||

Worldwide | 830 | 749 | 10.8 | |||||||

EDURANT® / rilpivirine | ||||||||||

U.S. | 14 | 12 | 16.7 | |||||||

International | 196 | 137 | 43.1 | |||||||

Worldwide | 210 | 149 | 40.9 | |||||||

PREZISTA® / PREZCOBIX® / REZOLSTA® / SYMTUZA® | ||||||||||

U.S. | 273 | 259 | 5.4 | |||||||

International | 205 | 171 | 19.9 | |||||||

Worldwide | 478 | 430 | 11.2 | |||||||

OTHER INFECTIOUS DISEASES | ||||||||||

U.S. | 46 | 55 | (16.4 | ) | ||||||

International | 96 | 115 | (16.5 | ) | ||||||

Worldwide | 142 | 170 | (16.5 | ) | ||||||

Neuroscience | ||||||||||

U.S. | 624 | 664 | (6.0 | ) | ||||||

International | 935 | 833 | 12.2 | |||||||

Worldwide | 1,559 | 1,497 | 4.1 | |||||||

CONCERTA® / Methylphenidate | ||||||||||

U.S. | 66 | 108 | (38.9 | ) | ||||||

International | 107 | 101 | 5.9 | |||||||

Worldwide | 173 | 209 | (17.2 | ) | ||||||

INVEGA SUSTENNA® / XEPLION® / TRINZA® / TREVICTA® | ||||||||||

U.S. | 400 | 372 | 7.5 | |||||||

International | 296 | 232 | 27.6 | |||||||

Worldwide | 696 | 604 | 15.2 | |||||||

RISPERDAL CONSTA® | ||||||||||

U.S. | 82 | 95 | (13.7 | ) | ||||||

International | 114 | 112 | 1.8 | |||||||

Worldwide | 196 | 207 | (5.3 | ) | ||||||

OTHER NEUROSCIENCE | ||||||||||

U.S. | 76 | 89 | (14.6 | ) | ||||||

19

International | 418 | 388 | 7.7 | |||||||

Worldwide | 494 | 477 | 3.6 | |||||||

Oncology | ||||||||||

U.S. | 933 | 664 | 40.5 | |||||||

International | 1,378 | 930 | 48.2 | |||||||

Worldwide | 2,311 | 1,594 | 45.0 | |||||||

DARZALEX® | ||||||||||

U.S. | 264 | 201 | 31.3 | |||||||

International | 168 | 54 | * | |||||||

Worldwide | 432 | 255 | 69.4 | |||||||

IMBRUVICA® | ||||||||||

U.S. | 227 | 190 | 19.5 | |||||||

International | 360 | 219 | 64.4 | |||||||

Worldwide | 587 | 409 | 43.5 | |||||||

VELCADE® | ||||||||||

U.S. | — | — | — | |||||||

International | 313 | 280 | 11.8 | |||||||

Worldwide | 313 | 280 | 11.8 | |||||||

ZYTIGA® | ||||||||||

U.S. | 407 | 233 | 74.7 | |||||||

International | 438 | 290 | 51.0 | |||||||

Worldwide | 845 | 523 | 61.6 | |||||||

OTHER ONCOLOGY | ||||||||||

U.S. | 35 | 40 | (12.5 | ) | ||||||

International | 99 | 87 | 13.8 | |||||||

Worldwide | 134 | 127 | 5.5 | |||||||

Pulmonary Hypertension | ||||||||||

U.S. | 361 | — | * | |||||||

International | 224 | — | * | |||||||

Worldwide | 585 | — | * | |||||||

OPSUMIT® | ||||||||||

U.S. | 149 | — | * | |||||||

International | 122 | — | * | |||||||

Worldwide | 271 | — | * | |||||||

TRACLEER® | ||||||||||

U.S. | 68 | — | * | |||||||

International | 72 | — | * | |||||||

Worldwide | 140 | — | * | |||||||

UPTRAVI® | ||||||||||

U.S. | 124 | — | * | |||||||

International | 16 | — | * | |||||||

Worldwide | 140 | — | * | |||||||

OTHER | ||||||||||

U.S. | 20 | — | * | |||||||

International | 14 | — | * | |||||||

Worldwide | 34 | — | * | |||||||

20

Cardiovascular / Metabolism / Other | ||||||||||

U.S. | 1,103 | 1,095 | 0.7 | |||||||

International | 414 | 380 | 8.9 | |||||||

Worldwide | 1,517 | 1,475 | 2.8 | |||||||

XARELTO® | ||||||||||

U.S. | 578 | 513 | 12.7 | |||||||

International | — | — | — | |||||||

Worldwide | 578 | 513 | 12.7 | |||||||

INVOKANA® / INVOKAMET® | ||||||||||

U.S. | 204 | 247 | (17.4 | ) | ||||||

International | 44 | 37 | 18.9 | |||||||

Worldwide | 248 | 284 | (12.7 | ) | ||||||

PROCRIT® / EPREX® | ||||||||||

U.S. | 189 | 169 | 11.8 | |||||||

International | 87 | 78 | 11.5 | |||||||

Worldwide | 276 | 247 | 11.7 | |||||||

OTHER | ||||||||||

U.S. | 132 | 166 | (20.5 | ) | ||||||

International | 283 | 265 | 6.8 | |||||||

Worldwide | 415 | 431 | (3.7 | ) | ||||||

TOTAL PHARMACEUTICAL | ||||||||||

U.S. | 5,354 | 4,872 | 9.9 | |||||||

International | 4,490 | 3,373 | 33.1 | |||||||

Worldwide | 9,844 | 8,245 | 19.4 | |||||||

MEDICAL DEVICES | ||||||||||

Diabetes Care | ||||||||||

U.S. | 117 | 154 | (24.0 | ) | ||||||

International | 222 | 245 | (9.4 | ) | ||||||

Worldwide | 339 | 399 | (15.0 | ) | ||||||

Diagnostics | ||||||||||

U.S. | — | — | — | |||||||

International | — | 1 | * | |||||||

Worldwide | — | 1 | * | |||||||

Interventional Solutions | ||||||||||

U.S. | 304 | 279 | 9.0 | |||||||

International | 336 | 270 | 24.4 | |||||||

Worldwide | 640 | 549 | 16.6 | |||||||

Orthopaedics | ||||||||||

U.S. | 1,307 | 1,359 | (3.8 | ) | ||||||

International | 943 | 916 | 2.9 | |||||||

Worldwide | 2,250 | 2,275 | (1.1 | ) | ||||||

HIPS | ||||||||||

U.S. | 209 | 209 | 0.0 | |||||||

International | 154 | 143 | 7.7 | |||||||

Worldwide | 363 | 352 | 3.1 | |||||||

21

KNEES | ||||||||||

U.S. | 228 | 246 | (7.3 | ) | ||||||

International | 159 | 152 | 4.6 | |||||||

Worldwide | 387 | 398 | (2.8 | ) | ||||||

TRAUMA | ||||||||||

U.S. | 407 | 391 | 4.1 | |||||||

International | 289 | 251 | 15.1 | |||||||

Worldwide | 696 | 642 | 8.4 | |||||||

SPINE & OTHER | ||||||||||

U.S. | 463 | 513 | (9.7 | ) | ||||||

International | 341 | 370 | (7.8 | ) | ||||||

Worldwide | 804 | 883 | (8.9 | ) | ||||||

Surgery | ||||||||||

U.S. | 993 | 995 | (0.2 | ) | ||||||

International | 1,430 | 1,276 | 12.1 | |||||||

Worldwide | 2,423 | 2,271 | 6.7 | |||||||

ADVANCED | ||||||||||

U.S. | 393 | 392 | 0.3 | |||||||

International | 573 | 485 | 18.1 | |||||||

Worldwide | 966 | 877 | 10.1 | |||||||

GENERAL | ||||||||||

U.S. | 423 | 423 | 0.0 | |||||||

International | 704 | 651 | 8.1 | |||||||

Worldwide | 1,127 | 1,074 | 4.9 | |||||||

SPECIALTY | ||||||||||

U.S. | 177 | 180 | (1.7 | ) | ||||||

International | 153 | 140 | 9.3 | |||||||

Worldwide | 330 | 320 | 3.1 | |||||||

Vision Care | ||||||||||

U.S. | 440 | 305 | 44.3 | |||||||

International | 675 | 493 | 36.9 | |||||||

Worldwide | 1,115 | 798 | 39.7 | |||||||

CONTACT LENSES / OTHER | ||||||||||

U.S. | 309 | 256 | 20.7 | |||||||

International | 498 | 427 | 16.6 | |||||||

Worldwide | 807 | 683 | 18.2 | |||||||

SURGICAL | ||||||||||

U.S. | 131 | 49 | * | |||||||

International | 177 | 66 | * | |||||||

Worldwide | 308 | 115 | * | |||||||

TOTAL MEDICAL DEVICES | ||||||||||

U.S. | 3,161 | 3,092 | 2.2 | |||||||

International | 3,606 | 3,201 | 12.7 | |||||||

Worldwide | 6,767 | 6,293 | 7.5 | |||||||

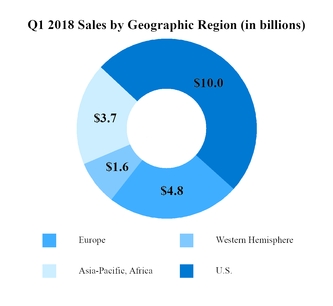

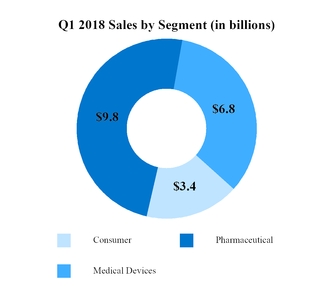

WORLDWIDE | ||||||||||

U.S. | 9,951 | 9,378 | 6.1 | |||||||

22

International | 10,058 | 8,388 | 19.9 | |||||||

Worldwide | $ | 20,009 | 17,766 | 12.6 | % | |||||

*Percentage greater than 100% or not meaningful

EARNINGS BEFORE PROVISION FOR TAXES BY SEGMENT

Fiscal First Quarters Ended | ||||||||||

(Dollars in Millions) | April 1, 2018 | April 2, 2017 | Percent Change | |||||||

Consumer (1) | $ | 548 | 596 | (8.1 | )% | |||||

Pharmaceutical(2) | 3,666 | 3,663 | 0.1 | |||||||

Medical Devices(3) | 1,579 | 1,563 | 1.0 | |||||||

Segment earnings before provision for taxes | 5,793 | 5,822 | (0.5 | ) | ||||||

Less: Expense not allocated to segments (4) | 312 | 247 | ||||||||

Worldwide income before tax | $ | 5,481 | 5,575 | (1.7 | )% | |||||

(1) Includes amortization expense of $0.1 billion in the fiscal first quarters of 2018 and 2017.