|

|

|

|

|

|

|

| ERGs | | Employee Resource Groups |

|

| ESPP | | Employee Stock Purchase Plan |

| EVP | | Employee Value Proposition |

| Exchange Act | | Securities Exchange Act of 1934, as amended |

| E.U. | | European Union |

| FAR | | Federal Acquisition Regulation |

| FASB | | Financial Accounting Standards Board |

| FCA | | False Claims Act |

| FCPA | | United States Foreign Corrupt Practices Act |

|

| FKTC | | First Kuwaiti Trading Company |

|

|

|

|

| G&A | | General and administrative |

| GAAP | | Generally Accepted Accounting Principles |

|

| GS | | Government Solutions |

| HETs | | Heavy equipment transporters |

| HR | | Human Resources |

|

| I&D | | Inclusion & Diversity |

| IRS | | Internal Revenue Service |

| JKC | | JKC Australia LNG, an Australian joint venture executing the Ichthys LNG Project |

| LIBOR | | London interbank offered rate |

| LNG | | Liquefied natural gas |

| MD&A | | Management's Discussion and Analysis of Financial Condition and Results of Operations |

|

|

| MoD | | Ministry of Defence |

| NCI | | Noncontrolling interests |

| NYSE | | The New York Stock Exchange |

|

|

| OAW | | Operation Allies Welcome |

| PCAOB | | Public Company Accounting Oversight Board |

| PFIs | | Private financed initiatives and projects |

| PIC | | Paid-in capital in excess of par |

| | | | | | | | |

| Acronym | | Definition |

| PPE | | Property, Plant and Equipment |

|

|

|

| RPA | | Master Accounts Receivable Purchase Agreement |

| SEC | | U.S. Securities and Exchange Commission |

| Securities Act | | Securities Act of 1933, as amended |

|

|

| SOFR | | Secured Overnight Financing Rate |

| SONIA | | Sterling Overnight Index Average |

| STS | | Sustainable Technology Solutions |

| Tax Act | | Tax Cuts and Jobs Act |

|

| U.K. | | United Kingdom |

| U.S. | | United States |

| U.S. GAAP | | Accounting principles generally accepted in the United States |

| UKMFTS | | U.K. Military Flying Training System |

| VIEs | | Variable interest entities |

|

|

|

|

|

|

|

|

|

|

|

|

| | | |

| | | |

|

|

|

|

|

|

|

|

|

| | | |

| | | |

|

|

|

|

|

|

|

|

| | | |

| | | |

|

| | | |

| | | |

|

| | | |

| | | |

|

|

We also own or lease numerous small facilities that include sales, administrative and offices as well as warehouses and equipment yards located throughout the world. Our owned Leatherhead property is pledged to secure certain pension obligations in the U.K., and we believe all properties that we currently occupy are suitable for their intended use.

Item 3.Legal Proceedings

Information relating to various commitments and contingencies is described in “Item 1A. Risk Factors” contained in Part I of this Annual Report on Form 10-K and in Notes 6, 13 and 14 to our consolidated financial statements in Part II, Item 8 of this Annual Report on Form 10-K and the information discussed therein is incorporated by reference into this Part I, Item 3.

Item 4.Mine Safety Disclosures

Not applicable.

PART II

Item 5.Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Our common stock is listed on the NYSE and trades under the symbol “KBR.” We have declared a dividend in each quarter during the years ended December 29, 2023 and December 31, 2022, and we currently expect that comparable quarterly cash dividends will continue to be paid for the foreseeable future. The declaration, payment and amount of future cash dividends will be at the discretion of our Board of Directors. On February 19, 2024, the Board of Directors declared a dividend of $0.15 per share, which will be paid on April 15, 2024.

At January 31, 2024, there were 59 shareholders of record. In calculating the number of shareholders, we consider clearing agencies and security position listings as one shareholder for each agency or listing.

Share Repurchases

On February 25, 2014, the Board of Directors authorized a $350 million share repurchase program. On October 18, 2022, the Board of Directors authorized an increase to the total authorization level to $500 million. As of December 29, 2023, $326 million remains available for repurchase under this authorization. On February 19, 2024, the Board of Directors authorized $174 million of share repurchases to be added to the prior authorizations. After the authorization on February 19, 2024, $500 million remains authorized and available for repurchase under this program. The authorization does not obligate the Company to acquire any particular number of shares of common stock and may be commenced, suspended or discontinued without prior notice. The share repurchases are intended to be funded through the Company’s current and future cash flows and the authorization does not have an expiration date.

The following is a summary of share repurchases of our common stock settled during the three months ended December 29, 2023, and the amount available to be repurchased under the authorized share repurchase program:

| | | | | | | | | | | | | | | | | | | | | | | |

| Purchase Period | Total Shares Repurchased (1) | | Average

Price Paid

per Share | |

Shares Repurchased

as Part of Publicly

Announced Plan | | Dollar Value of Maximum Number of Shares that May Yet Be

Purchased Under the Plan |

| September 30, 2023 | — | | | $ | — | | | — | | | $ | 326,215,513 | |

| October 1 - 31, 2023 | 72 | | | $ | 58.15 | | | — | | | $ | 326,215,513 | |

| November 1 - 30, 2023 | 10,088 | | | $ | 58.24 | | | — | | | $ | 326,215,513 | |

| December 1 - 29, 2023 | 11,096 | | | $ | 53.30 | | | — | | | $ | 326,215,513 | |

| Total | 21,256 | | | $ | — | | | — | | | $ | 326,215,513 | |

(1)Included within the shares repurchased herein are 21,256 shares acquired from employees in connection with the settlement of income tax and related benefit withholding obligations arising from issuance of share-based equity awards under the KBR Stock and Incentive Plan at an average price of $55.66 per share.

Performance Graph

The following performance graph and related information shall not be deemed “soliciting material” or to be “filed” with the SEC, nor shall the information be incorporated by reference into any future filing under the Securities Act or the Exchange Act, except to the extent that the Company specifically incorporates it by reference into such filing.

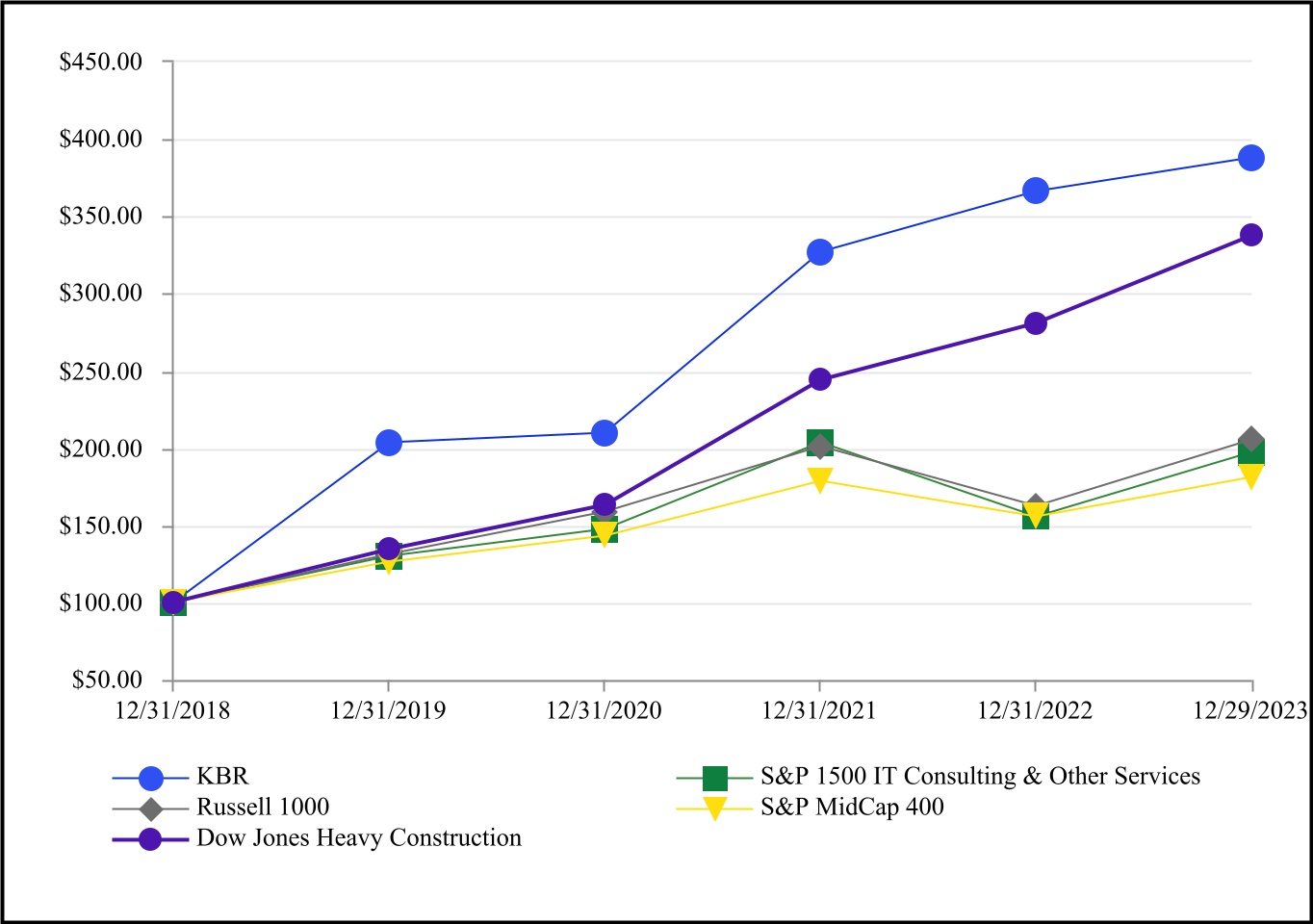

The following performance graph compares the cumulative total shareholder return on shares of our common stock for the five-year period ended December 29, 2023, with the cumulative total return on the S&P 1500 IT Consulting & Other Services Index, the Russell 1000 Index, the S&P MidCap 400 Index and the Dow Jones Heavy Construction Industry Index for the same period. The comparisons assume the investment of $100 on December 31, 2018 and reinvestment of all dividends. The shareholder return is not necessarily indicative of future performance.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 12/31/2018 | | 12/31/2019 | | 12/31/2020 | | 12/31/2021 | | 12/31/2022 | | 12/29/2023 |

| KBR | $ | 100.00 | | | $ | 203.62 | | | $ | 210.06 | | | $ | 327.00 | | | $ | 366.03 | | | $ | 387.71 | |

| S&P 1500 IT Consulting & Other Services | $ | 100.00 | | | $ | 130.23 | | | $ | 147.73 | | | $ | 203.78 | | | $ | 155.69 | | | $ | 197.65 | |

| Russell 1000 | $ | 100.00 | | | $ | 131.43 | | | $ | 158.98 | | | $ | 201.03 | | | $ | 162.58 | | | $ | 205.72 | |

| S&P MidCap 400 | $ | 100.00 | | | $ | 126.20 | | | $ | 143.44 | | | $ | 178.95 | | | $ | 155.58 | | | $ | 181.15 | |

| Dow Jones Heavy Construction | $ | 100.00 | | | $ | 134.15 | | | $ | 162.88 | | | $ | 243.89 | | | $ | 280.60 | | | $ | 337.69 | |

Item 6.[Reserved]

Item 7.Management’s Discussion and Analysis of Financial Condition and Results of Operations

Introduction

The purpose of the MD&A is to provide our stockholders and other interested parties with information necessary to gain an understanding of our financial condition and disclose changes in our financial condition since the most recent fiscal year-end and results of operations during the current fiscal period as compared to the corresponding period of the preceding fiscal year. The MD&A should be read in conjunction with Part I of this Annual Report on Form 10-K as well as the consolidated financial statements and related notes included in Part II, Item 8 of this Annual Report on Form 10-K.

Company Overview

KBR Inc., a Delaware corporation ("KBR"), delivers science, technology, engineering and logistics support solutions to governments and companies around the world. Drawing from its rich 100-year history and culture of innovation and mission focus, KBR creates sustainable value by combining deep domain expertise with its full life cycle capabilities to help clients meet their most pressing challenges. Our capabilities and offerings include the following:

•Scientific research such as quantum science and computing; health and human performance; materials science; life science research; and earth sciences;

•Defense systems engineering such as rapid prototyping; test and evaluation; aerospace acquisition support; systems and platform integration; and sustainment engineering;

•Operational support such as space domain awareness; C5ISR; human spaceflight and satellite operations; integrated supply chain and logistics; and military aviation support;

•Information operations such as cyber analytics and cybersecurity; data analytics; mission planning systems; virtual/augmented reality and technical training; and artificial intelligence and machine learning;

•Professional advisory services across the defense, renewable energy and critical infrastructure sectors; and

•Sustainable decarbonization solutions that accelerate and enable energy transition and climate change solutions such as proprietary, sustainability-focused process licensing; advisory services focused on energy transition; high-end engineering, design and management program offerings; and digitally-enabled asset optimization solutions.

KBR's strategic growth vectors include:

•Defense modernization;

•Space superiority;

•Health and human performance;

•Sustainable technology;

•High-end engineering;

•Energy transition and security; and

•Technology-led asset optimization

Key customers include U.S. DoD agencies such as the U.S. Army, U.S. Navy and U.S. Air Force, Missile Defense Agency, National Geospatial-Intelligence Agency, National Reconnaissance Office and other intelligence agencies; U.S. civilian agencies such as NASA, U.S. Geological Survey and National Oceanic and Atmospheric Administration; the U.K. MoD, London Metropolitan Police, and other U.K. Crown Services; the Royal Australian Air Force, Navy and Army; other national governments; and a wide range of commercial and industrial companies.

Our deployment priorities are to fund organic growth, maintain responsible leverage, maintain an attractive dividend, make strategic, accretive acquisitions and repurchase shares. As demonstrated by our acquisitions of Frazer Nash Consultancy Limited, VIMA Group and others in the past few years, our acquisition thesis is centered around moving upmarket, expanding capabilities and broadening customer sets across strategic growth vectors. KBR also develops and prioritizes investment in technologies that are disruptive, innovative and sustainability- and safety-focused. These technologies and engineering solutions enable clients to achieve a cleaner, greener, more energy efficient global future.

Our Business Segments

KBR's business is organized into two core business segments and one non-core business segment as follows:

Core business segments

•Government Solutions

•Sustainable Technology Solutions

Non-core business segment

•Other

See additional information on our business segments in Note 2 to our consolidated financial statements and under "Item 1. Business" in this Annual Report on Form 10-K.

Business Environment and Trends

Government Outlook

On June 3, 2023, President Biden signed into law the Fiscal Responsibility Act of 2023, which suspends the public debt ceiling limit through January 2, 2025. This law includes provisions that will impact future fiscal year budgets for the United States. Key provisions in this law include statutory caps on discretionary funding in 2024 and 2025 and limits on discretionary funding for the years 2026 through 2029. The 2024 statutory cap on discretionary funding totals $1.6 trillion, which included $886 million for defense spending and $704 million for non-defense spending. The 2024 statutory cap on defense spending does not impact President Biden's proposed fiscal 2024 budget; however, the 2024 statutory cap on non-defense spending is 14% lower than President Biden's proposed fiscal 2024 budget. The effect of the non-defense discretionary spending statutory cap on individual programs or KBR cannot be predicted at this time.

In December 2023, President Biden signed into law the National Defense Authorization Act ("NDAA") for fiscal year 2024. The NDAA authorizes programs, projects and policies to be carried out with funds appropriated by Congress as part of the annual budgetary process. The NDAA supports approximately $874 billion in fiscal year 2024 funding for national defense, $841 billion of which is for the DoD. The requested amount is an increase of $27 billion when compared to the authorized defense spending for fiscal year 2023.

The U.S. government has not yet enacted an annual budget for fiscal year 2024; these proposed 2024 budgetary amounts are subject to change. To avert a government shutdown, three continuing resolution funding measures have been enacted to finance all U.S. government activities. The most recent "laddered" continuing resolution passed in January 2024 funds the government through March 2024, depending on the appropriation bill. Under the continuing resolution, partial-year funding at amounts consistent with appropriated levels for fiscal year 2023 are available, subject to certain restrictions, but new spending initiatives are not authorized. Uncertainty continues to exist regarding whether a divided Congress will be able to pass appropriation bills or additional continuing resolutions once the current continuing resolutions expire in March 2024. We believe our key programs will continue to be supported and funded in the continuing resolution financing mechanism. The effect of a potential government shutdown or the finalized fiscal year 2024 budget on KBR or our individual programs cannot be predicted at this time. However, if a government shutdown were to occur and were to continue for an extended period, we could be at risk of program cancellations, schedule delays and other disruptions and nonpayment, which could adversely affect our results of operations. We anticipate the federal budget will continue to be subject to debate and compromise shaped by, among other things, heightened political tensions, the global security environment, inflationary pressures and macroeconomic conditions. The result may be shifting funding priorities, which could have material impacts on defense spending broadly and our programs.

Internationally, our Government Solutions work is performed primarily for the U.K. MoD and the Australian Department of Defence. In March 2023, the U.K. government announced its intent to increase its defense budget by £11 billion over the next five years, increasing the defense budget to 2.25% of GDP by 2025. Recognizing the importance of strong defense and the role the U.K. plays across the globe, the U.K. has prioritized investment in military research and investment in key areas to advance and develop capabilities around artificial intelligence, cyber security and space superiority. It is expected the next general election in the United Kingdom will occur in 2024 (and no later than January 28, 2025). The effect of the next general election in the United Kingdom on KBR or our individual programs cannot be predicted at this time. The Australian government continues to invest in defense spending, with particular focus on enhancing regional security, modernizing defense capabilities, strengthening cyber defenses and promoting broader economic stability. The fiscal year budget for Australia for the

2023 - 2024 financial year was finalized, with the Australian government increasing defense spending by 5% to AUD 51.0 billion, or approximately 2.00% of GDP.

In 2021, the U.S., U.K. and Australia announced AUKUS, a security pact that will promote a free and open Indo-Pacific through a shared long-term investment to strengthen their combined capabilities and enhance their ability to deter aggression. AUKUS’ first major initiative (Pillar 1) is a joint effort to provide Australia with conventionally armed, nuclear powered submarine ("NPS") capability and strengthen the capacity of the submarine workforce and industrial base. In 2023, these countries announced an arrangement for Australia to acquire a NPS through the AUKUS security pact. This arrangement outlines an approach that will provide Australia with the capability to operate and maintain a NPS before the expected sale of these submarines from the United States to Australia in the early 2030s (subject to Congressional approval). Pillar 2 of this security pact will focus on enabling technologies to maintain a secure and stable trade through the region including undersea technologies, quantum technologies, advanced cyber, artificial intelligence and autonomy, hypersonic research and development, electronic warfare and innovation.

With defense and civil budgets driven in part by political instability, military conflicts, aging platforms and infrastructure and the need for technology advances, we expect continued opportunities to provide solutions and technologies to mission critical work aligned with our customers’ and our nation’s critical priorities.

Sustainable Technology Outlook

Long-range commercial market fundamentals are supported by global population growth, expanding global development and an acceleration of demand for energy transition, renewable energy sources and climate change solutions. The globe is in search of the solution to the energy trilemma, the balance between energy affordability, ensuring energy security and achieving environmental sustainability. Clients are prioritizing their efforts to solve the energy trilemma by investing in digital solutions to optimize operations, increase end-product flexibility and energy efficiency, reduce unplanned downtime and minimize environmental footprint. As the global focus on energy security intensifies and companies continue to commit to near-term carbon neutrality and longer-range net-zero carbon emissions, we expect spending to continue in areas such as decarbonization; carbon capture, utilization and sequestration; biofuels; and circular economy. Further, leading companies across the world are proactively evaluating clean energy alternatives, including hydrogen and green ammonia which complements KBR's proprietary process technologies, solutions and capabilities.

We expect climate change and energy transition to continue to be areas of priority and investment as many countries, including the U.S., look to boost their economies and invest in a cleaner future. Specifically, on August 16, 2022, the President signed the Inflation Reduction Act into law which includes provisions intended to, among other things, incentivize domestic clean energy, manufacturing and production. Additionally, in March 2023, the Canadian government announced its federal budget which includes billions of dollars for investment in the transition to a low-carbon economy.

Change in Fiscal Year End

On December 13, 2022, the Board of Directors approved a change in the fiscal year end from a calendar year ending on December 31 to a 52 – 53 week year ending on the Friday closest to December 31, effective as of the commencement of the Company's fiscal year on January 1, 2023. In a 52 week fiscal year, each of the Company’s quarterly periods will comprise 13 weeks. The additional week in a 53 week fiscal year is added to the fourth quarter, making such quarter consist of 14 weeks. The Company’s first 53 week fiscal year will occur in fiscal year 2024. The Company made the fiscal year change on a prospective basis and will not adjust operating results for prior periods. The change will impact the prior year comparability of each of the fiscal quarters and the annual period for the year ending December 29, 2023; however, the impact will not be material. The Company believes this change will improve comparability between periods by eliminating the year-over-year variability in calendar month productive days and provide a more consistent reporting cadence for operational leaders to aid in strategic decision making.

Due to this change in fiscal year, our fiscal year ended on December 29 in 2023 as compared to December 31 in 2022. The years ended December 29, 2023 and December 31, 2022 contained 363 days and 365 days, respectively.

Overview of 2023 Financial Results and Significant Bookings

2023 was a year of significant achievement for KBR as we continued to execute toward our long-term vision. The Company benefits from a significant base of long-term enduring contracts in our government business, a diverse portfolio of high quality proprietary process technologies, market tailwinds that benefit our capabilities and technologies in areas such as defense modernization, energy transition, energy security and high-end engineering and a truly global client base. Together, these attributes distinguish KBR and have contributed directly to the Company’s growth in earnings during the year.

In 2023, revenues and operating income increased for KBR when compared to 2022. These increases were driven by both our GS and STS business segments. Our GS business segment increased revenues in 2023 with contract growth and increased activity to support exercises, training and other activities within the European Command during the year, despite being partially offset by revenue recognized in the previous year related to the OAW program. Our STS business segment increased revenues in 2023 due to increases in technology sales and engineering and professional services. Our teams continued to deliver operational performance, healthy profitability and strong cash flow. Importantly, we drove innovation and extended our footprint through new program wins and technology advances, developments and investments, such as our additional investment in Mura Technology in 2023. 2023 was also an important year for KBR with multiple obligations resolved during the year including the settlement of a legacy legal matter and the maturity and settlement of our Convertible Notes. Our outstanding warrants were also terminated in 2023, with final payment for the warrant terminations being made in January 2024.

Our GS business landed new awards, including a $1.9 billion ceiling, 5-year Integrated Mission Operations Contract for the continued support of NASA's human spaceflight programs which includes the International Space Station, Artemis and Low Earth Orbit Commercialization. Additional new awards included an award to a KBR joint venture for the Omnibus Multidiscipline Engineering Services III contract, worth up to $719 million, to aid NASA's development of space orbital systems in its Engineering and Technology Directorate at Goddard Space Flight Center in Maryland. Our STS business landed various awards during the year, including an award for modifications to the Pluto LNG facility in Australia and numerous projects across the ammonia landscape and various projects spanning carbon capture, utilization and storage, hydrogen, biofuels and renewables.

Results of Operations

The following tables set forth our results of operations for the periods presented, including by segment. A discussion regarding our financial condition and results of operations for the years ended December 31, 2022 and 2021 is included in Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations of our Annual Report on Form 10-K for the year ended December 31, 2022, as filed with the SEC on February 17, 2023.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Consolidated Results |

| Year Ended | | Change |

| December 29, | | December 31, | | December 31, | | 2023 vs. 2022 | | 2022 vs. 2021 |

| Dollars in millions | 2023 | | 2022 | | 2021 | | $ | | % | | $ | | % |

| Revenues | $ | 6,956 | | | $ | 6,564 | | | $ | 7,339 | | | $ | 392 | | | 6 | % | | $ | (775) | | | (11) | % |

| Cost of revenues | $ | (5,979) | | | $ | (5,736) | | | $ | (6,533) | | | $ | 243 | | | 4 | % | | $ | (797) | | | (12) | % |

| Gross profit | $ | 977 | | | $ | 828 | | | $ | 806 | | | $ | 149 | | | 18 | % | | $ | 22 | | | 3 | % |

| Equity in earnings (losses) of unconsolidated affiliates | $ | 114 | | | $ | (80) | | | $ | (170) | | | $ | 194 | | | n/m | | $ | 90 | | | 53 | % |

| Selling, general and administrative expenses | $ | (488) | | | $ | (420) | | | $ | (393) | | | $ | 68 | | | 16 | % | | $ | 27 | | | 7 | % |

| | | | | | | | | | |

| Legal settlement of legacy matter | $ | (144) | | | $ | — | | | $ | — | | | $ | 144 | | | n/m | | $ | — | | | — | % |

| Gain (loss) on disposition of assets and investments | $ | (7) | | | $ | 19 | | | $ | 2 | | | $ | (26) | | | n/m | | $ | 17 | | | n/m |

| | | | | | | | | | |

| Other | $ | (4) | | | $ | (4) | | | $ | (14) | | | $ | — | | | — | % | | $ | (10) | | | (71) | % |

| Operating income | $ | 448 | | | $ | 343 | | | $ | 231 | | | $ | 105 | | | 31 | % | | $ | 112 | | | 48 | % |

| Interest expense | $ | (115) | | | $ | (87) | | | $ | (80) | | | $ | 28 | | | 32 | % | | $ | 7 | | | 9 | % |

| Unrealized gain on other investment | $ | — | | | $ | 16 | | | $ | 4 | | | $ | (16) | | | n/m | | $ | 12 | | | 300 | % |

Charges associated with Convertible Notes

| $ | (494) | | | $ | — | | | $ | — | | | $ | 494 | | | n/m | | $ | — | | | — | % |

| Other non-operating income (expense) | $ | (5) | | | $ | 12 | | | $ | (9) | | | $ | (17) | | | n/m | | $ | 21 | | | n/m |

| Income (loss) before income taxes | $ | (166) | | | $ | 284 | | | $ | 146 | | | $ | (450) | | | n/m | | $ | 138 | | | 95 | % |

| Provision for income taxes | $ | (95) | | | $ | (92) | | | $ | (111) | | | $ | 3 | | | 3 | % | | $ | (19) | | | (17) | % |

| Net income (loss) | $ | (261) | | | $ | 192 | | | $ | 35 | | | $ | (453) | | | n/m | | $ | 157 | | | 449 | % |

Less: Net income attributable to noncontrolling interests | $ | 4 | | | $ | 2 | | | $ | 8 | | | $ | 2 | | | 100 | % | | $ | (6) | | | (75) | % |

| Net income (loss) attributable to KBR | $ | (265) | | | $ | 190 | | | $ | 27 | | | $ | (455) | | | n/m | | $ | 163 | | | 604 | % |

n/m - not meaningful

Revenues. Revenues increased by $392 million, or 6%, to $6,956 million in 2023, compared to $6,564 million in 2022. The increase was primarily attributed to contract growth across our GS business and increased revenues from technology sales and engineering and professional services in our STS business. Additionally, there was increased activity to support exercises, training and other activities within the European Command. These increases in revenue were offset by approximately $313 million of revenue recognized in 2022 from contingency work associated with the OAW program that wound down and substantially completed in early 2022 and decreases in revenue due to the ramp down of construction work for the Aspire program.

Gross profit. The increase in overall gross profit of $149 million, or 18%, was primarily driven by items increasing revenues discussed above, favorable STS licensing mix and resolutions on various legacy matters in the current year. These increases were offset by reduced volume from contingency work associated with the OAW program.

Equity in earnings (losses) of unconsolidated affiliates. Equity in earnings (losses) of unconsolidated affiliates increased by $194 million to $114 million in earnings for the year ended December 29, 2023 compared to $80 million in losses for the year ended December 31, 2022. In 2022, a non-cash charge in the amount of $137 million was recorded associated with the settlement agreement with the consortium of subcontractors of the Combined Cycle Power Plant for the Ichthys LNG Project that did not recur in 2023. In 2022, we also recorded a charge on a joint venture in our GS business segment that did not recur in 2023. Further, the increase in 2023 is attributed to equity in earnings from services on an LNG project that commenced in the second quarter of 2022.

Selling, general and administrative expenses. Selling, general and administrative expenses were $68 million higher in 2023 compared to 2022, which was primarily driven by growth in the business and favorable settlements and credits received in the first quarter of 2022 that did not recur in 2023.

Legal settlement of legacy matter. In 2023 we recorded a charge of $144 million related to the settlement of a legacy legal matter.

Gain (loss) on disposition of assets and investments. In 2023, we recognized a loss on disposition of assets and investments of $7 million related to the sale of our operations in Russia. This loss was primarily due to $10 million in accumulated foreign currency adjustments that were reclassified from AOCL. In 2022, we recognized a gain on disposition of assets and investments of $16 million primarily from the sale of our investment interest in three U.K. Road investments.

Interest Expense. The increase in interest expense was primarily driven by increases in the U.S. federal reserve funds rate from 2022 to 2023.

Unrealized gain on other investment. In 2022, we recognized an unrealized gain on other investment of $16 million related to the appreciation in the fair value of our Mura Technology investment as a result of a revaluation triggered by our incremental investment commitment. We did not record an unrealized gain on other investment in 2023.

Charges associated with Convertible Notes. In 2023, we recognized a loss of $494 million related to the cash election and repurchase of Convertible Notes and Warrant Unwind Agreements.

Other non-operating income (expense). Other non-operating income (expense) includes interest income, foreign exchange gains and losses and other non-operating income or expense items. The net decrease is primarily driven by foreign exchange gains and losses. In 2023, we recorded approximately $6 million in net foreign exchange losses. In 2022, we recorded approximately $8 million in net foreign exchanges gains primarily related to foreign exchange impacts from the Australian dollar tranche of Term Loan A that was redenominated into U.S. dollars following the execution of an amendment to our existing Credit Agreement in the fourth quarter of 2022.

Provision for income taxes. The provision for income taxes for the year ended December 29, 2023 reflects a (57)% tax rate as compared to a 32% tax rate for the year ended December 31, 2022. The effective tax rate of (57)%, as compared to the U.S. statutory rate of 21%, for the year ended December 29, 2023 was primarily impacted by the non-deductible portion of a legal settlement on a legacy matter and the non-deductible charge associated with the cash election and Convertible Notes repurchase discussed in Note 22. The implication of these non-deductible items were partially offset by the release of a previously reserved position based on developments associated with the ongoing IRS examination and appeals process for certain years. The effective tax rate of 32% for the year ended December 31, 2022 was primarily driven by the non-deductibility of losses incurred with respect to the settlement of outstanding matters related to the Ichthys LNG project to which KBR is a JV partner. Excluding the tax impact of these items, our tax rate would be 26% and 24% for the year ended December 29, 2023 and December 31, 2022, respectively. See Note 12 "Income Taxes" to our consolidated financial statements for further discussion on income taxes, including our reconciliation of the U.S. statutory tax rate to our effective tax rate.

Results of Operations by Business Segment

We analyze the financial results of our two core business segments and one non-core business segment. The business segments presented are consistent with our reportable segments discussed in Note 2 to our consolidated financial statements.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Years Ended | | Change |

| December 29, | | December 31, | | December 31, | | 2023 vs. 2022 | | 2022 vs. 2021 |

| Dollars in millions | 2023 | | 2022 | | 2021 | | $ | | % | | $ | | % |

| Revenues | | | | | | | | | | | |

| Government Solutions | $ | 5,353 | | | $ | 5,320 | | | $ | 6,149 | | | $ | 33 | | | 1 | % | | $ | (829) | | | (13) | % |

| Sustainable Technology Solutions | 1,603 | | | 1,244 | | | 1,190 | | | 359 | | | 29 | % | | 54 | | | 5 | % |

| Total revenues | $ | 6,956 | | | $ | 6,564 | | | $ | 7,339 | | | $ | 392 | | | 6 | % | | $ | (775) | | | (11) | % |

| | | | | | | | | | | | | |

| Operating income | | | | | | | | | | | | | |

| Government Solutions | $ | 285 | | | $ | 441 | | | $ | 414 | | | $ | (156) | | | (35) | % | | $ | 27 | | | 7 | % |

| Sustainable Technology Solutions | 324 | | | 47 | | | (30) | | | 277 | | | n/m | | 77 | | | n/m |

| Other | (161) | | | (145) | | | (153) | | | (16) | | | (11) | % | | 8 | | | 5 | % |

| Operating income | $ | 448 | | | $ | 343 | | | $ | 231 | | | $ | 105 | | | 31 | % | | $ | 112 | | | 48 | % |

n/m - not meaningful

Government Solutions

GS revenues increased by $33 million, or 1%, to $5,353 million in 2023 compared to $5,320 million in 2022. This increase was primarily attributable to activity to support exercises, training and other activities within the European Command and continued contract growth across our GS business segment. These increases were partially offset by approximately $313 million of revenue recognized in 2022 from contingency work associated with the OAW program that was wound down and substantially completed in early 2022. Additionally, the increase was offset by the ramp down of construction work for the Aspire program.

GS operating income decreased by $156 million, or 35%, to $285 million in 2023 compared to $441 million in 2022. The decrease was primarily driven by the $144 million charge recorded in the second quarter of 2023 related to the settlement of a legacy legal matter. Additionally, operating income decreased $19 million primarily due to the gain on sale of our investment interest in three U.K. Road investments.

Sustainable Technology Solutions

STS revenues increased by $359 million, or 29%, to $1,603 million in 2023 compared to $1,244 million in 2022. The increase from 2022 to 2023 was primarily driven by increased revenues from technology sales and engineering and professional services.

STS operating income increased by $277 million to $324 million in 2023 compared to $47 million in 2022. The increase was primarily related to the Ichthys LNG project. In 2022, a non-cash charge in the amount of $137 million was recorded for the settlement agreement with the consortium of subcontractors of the Combined Cycle Power Plant that did not recur in 2023. Additionally, the increase was related to increased technology sales and engineering and professional services, increased equity in earnings from services on an LNG project, a favorable resolution on a legacy matter in 2023 and a non-cash impact in 2022 that did not recur in 2023. The increases in 2023 were offset by a $7 million loss related to the sale of our operations in Russia. This loss was primarily due to $10 million in accumulated foreign currency adjustments that were reclassified from AOCL.

Other

Other operating loss remained materially consistent between the years ended December 29, 2023 and December 31, 2022.

Backlog of Unfilled Orders

Backlog represents the estimated dollar amount of revenues we expect to realize in the future as a result of performing work on contracts and our pro-rata share of work to be performed by our unconsolidated joint ventures. We include total estimated revenues in backlog when a contract is awarded under a legally binding agreement. In many instances, arrangements included in backlog are complex, nonrepetitive and may fluctuate over the contract period due to the release of contracted work in phases by the customer. Additionally, nearly all contracts allow customers to terminate the agreement at any time for convenience, and from time to time customers may dispute or try to renegotiate existing contracts. These and other factors may result in delays in our recognition of revenue from our backlog, and in differences between the amounts we book as backlog and the amounts we recognize as revenue. Certain contracts provide maximum dollar limits, with actual authorization to perform work under the contract agreed upon on a periodic basis with the customer. In these arrangements, only the amounts authorized are included in backlog. For projects where we act solely in a project management capacity, we only include the expected value of our services in backlog.

We define backlog, as it relates to U.S. government contracts, as our estimate of the remaining future revenue from existing signed contracts over the remaining base contract performance period (including customer approved option periods) for which work scope and price have been agreed with the customer. We define funded backlog as the portion of backlog for which funding currently is appropriated, less the amount of revenue we have previously recognized. We define unfunded backlog as the total backlog less the funded backlog. Our GS backlog does not include any estimate of future potential delivery orders that might be awarded under our government-wide acquisition contracts, agency-specific indefinite delivery/indefinite quantity contracts or other multiple-award contract vehicles, nor does it include option periods that have not been exercised by the customer.

Within our GS business segment, we calculate estimated backlog for long-term contracts associated with the U.K. government's PFIs based on the aggregate amount that our client would contractually be obligated to pay us over the life of the project. We update our estimates of the future work to be executed under these contracts on a quarterly basis and adjust backlog if necessary.

Refer to "Item 1A. Risk Factors" contained in Part 1 of this Annual Report on Form 10-K for a discussion of other factors that may cause backlog to ultimately convert into revenues at different amounts.

We have included in the table below our proportionate share of unconsolidated joint ventures' estimated backlog. As these projects are accounted for under the equity method, only our share of future earnings from these projects will be recorded in our results of operations. Our proportionate share of backlog for projects related to unconsolidated joint ventures totaled $4.1 billion at December 29, 2023, and $3.9 billion at December 31, 2022.

As a result of U.S. Transportation Command lifting the stop work order on the HomeSafe contract in November 2022, we have recognized $54 million and $39 million in backlog as of December 29, 2023 and December 31, 2022, respectively, for our transition work. Additionally, for the year ended December 29, 2023, we recognized $0.8 billion for our proportionate share of KZJV's backlog and for KBR services to be provided to KZJV as a result of receiving a full notice to proceed with Phase 2 of the Plaquemines LNG project.

The following table summarizes our backlog by business segment for the years ended December 29, 2023 and December 31, 2022, respectively:

| | | | | | | | | | | |

| Dollars in millions | December 29, 2023 | | December 31, 2022 |

| Government Solutions | $ | 12,790 | | | $ | 11,543 | |

| Sustainable Technology Solutions | 4,545 | | | 4,012 | |

| Total backlog | $ | 17,335 | | | $ | 15,555 | |

We estimate that as of December 29, 2023, 30% of our backlog will be executed within one year. Of this amount, we estimate that 87% will be recognized in revenues on our consolidated statement of operations and 13% will be recorded by our unconsolidated joint ventures. As of December 29, 2023, $164 million of our backlog relates to active contracts that are in a loss position.

As of December 29, 2023, 10% of our backlog was attributable to fixed-price contracts, 39% was attributable to PFIs, 36% was attributable to cost-reimbursable contracts and 15% was attributable to time-and-materials contracts. For contracts that contain fixed-price, cost-reimbursable and time-and-materials components, we classify the individual components as either fixed-price, cost-reimbursable or time-and materials according to the composition of the contract; however, for smaller contracts, we characterize the entire contract based on the predominant component. As of December 29, 2023, $9.2 billion of our GS backlog was currently funded by our customers.

As of December 29, 2023, we had approximately $4.4 billion of priced option periods not yet exercised by the customer for U.S. government contracts that are not included in the backlog amounts presented above.

The difference between backlog of $17.3 billion and the remaining performance obligations as defined by ASC 606 of $12.7 billion is primarily due to our proportionate share of backlog related to unconsolidated joint ventures which is not included in our remaining performance obligations. See Note 3 "Revenue" to our consolidated financial statements for discussion of the remaining performance obligations.

Liquidity and Capital Resources

Liquidity is provided by available cash and cash equivalents, cash generated from operations, our Senior Credit Facility (as defined below) and access to capital markets. Our operating cash flow can vary significantly from year to year and is affected by the mix, terms, timing and stage of completion of our projects. We often receive cash in advance on certain of our sustainable technology projects. On time-and-material and cost reimbursable contracts, we may utilize cash on hand or availability under our Senior Credit Facility to satisfy any periodic operating cash requirements for working capital, as we incur costs and subsequently invoice our customers.

Certain STS services projects may require us to provide credit support for our performance obligations to our customers in the form of letters of credit, surety bonds or guarantees. Our ability to obtain new project awards in the future may be dependent on our ability to maintain or increase our letter of credit and surety bonding capacity, which may be further dependent on the timely release of existing letters of credit and surety bonds. As the need for credit support arises, letters of credit may be issued under the Revolver (as defined below) or with lending counterparties on a bilateral, syndicated or other basis.

As discussed in Note 11 "Debt and Other Credit Facilities" of our consolidated financial statements, we entered into Amendment No. 8 on February 6, 2023, to our existing Credit Agreement, dated as of April 25, 2018, as amended ("Credit Agreement"), consisting of a $1 billion revolving credit facility (the "Revolver"), a Term Loan A ("Term Loan A") with debt tranches denominated in U.S. dollars and British pound sterling and a Term Loan B ("Term Loan B" and together with the Revolver and Term Loan A, the "Senior Credit Facility"). Amendment No. 8 (i) replaces the LIBOR-based reference borrowing rate with a SOFR-based reference borrowing rate for the U.S. dollar tranche of Term Loan A and the Revolver and (ii) implements the Company’s recent fiscal year change from a calendar year ending on December 31 to a 52-53 week year ending on the Friday closest to December 31, effective beginning with fiscal year 2023.

We entered into Amendment No. 9 to our Credit Agreement on June 6, 2023. Amendment No. 9 replaces the LIBOR-based reference borrowing rate with a SOFR-based reference borrowing rate for Term Loan B. We entered into Amendment No. 10 to our Credit Agreement on July 26, 2023. Amendment No. 10 provided for an additional $200 million loan tranche under Term Loan A. We borrowed the full $200 million principal amount available under this additional loan tranche, and this $200 million borrowing was applied as a partial repayment of the outstanding amounts of principal and accrued interest under the Revolver.

We entered into Amendment No.11 to our Credit Agreement on January 19, 2024. This amendment provides for an incremental Term Loan B facility in an aggregate principal amount of $1 billion and extends the Term Loan B maturity date to January 2031. We borrowed the full $1 billion principal amount available under this loan and primarily used the proceeds to repay all amounts of outstanding principal and accrued interest under the Company’s Term Loan B facility at December 29, 2023 and to partially repay outstanding principal and accrued interest under the Company’s Revolver. We entered into Amendment No.12 to our Credit Agreement on February 7, 2024. This amendment consolidated the USD denominated Term A-1, Term A-2 and Term A-4 loan facilities under our Credit Agreement into the amended USD denominated Term A-1 loan facility and continued the GBP denominated Term A-3 loan facility outstanding at December 29, 2023. Additionally, this amendment extended the maturity date of the $1 billion Revolver, amended Term A-1 loan facility and Term A-3 loan facility to February 2029. Immediately following execution of Amendment No. 12, we had approximately $500 million outstanding related to the remaining Term Loan A facilities and $117 million outstanding on our Revolver.

We believe that existing cash balances, internally generated cash flows, availability under our Senior Credit Facility and other lines of credit are sufficient to support our business operations for the next 12 months. As of December 29, 2023, we were in compliance with all financial covenants related to our debt agreements.

Cash and cash equivalents totaled $304 million at December 29, 2023 and $389 million at December 31, 2022 and consisted of the following:

| | | | | | | | | | | |

| | December 29, | | December 31, |

| Dollars in millions | 2023 | | 2022 |

| Domestic U.S. cash | $ | 44 | | | $ | 27 | |

| International cash | 128 | | | 255 | |

| Joint venture and Aspire Defence project cash | 132 | | | 107 | |

| Total | $ | 304 | | | $ | 389 | |

Our cash balances are held in numerous accounts throughout the world to fund our global activities, including acquisitions, joint ventures and other business partnerships. Domestic cash relates to cash balances held by U.S. entities and is largely used to support project activities of those businesses as well as general corporate needs such as the payment of dividends to shareholders, repayment of debt and potential repurchases of our outstanding common stock.

Our international cash balances may be available for general corporate purposes but are subject to local restrictions, such as capital adequacy requirements and maintaining sufficient cash balances to support our U.K. pension plan and other obligations incurred in the normal course of business by those foreign entities. Repatriations of our undistributed foreign earnings are generally free of U.S. tax but may incur withholding and/or state taxes. We consider our future non-U.S. cash needs as 1) our anticipated foreign working capital requirements, including funding of our U.K. pension plan, 2) the expected growth opportunities across all geographical markets and 3) our plans to invest in strategic growth opportunities, which may include acquisitions, joint ventures and other business partnerships around the world, including whether foreign earnings are permanently reinvested. If management were to completely remove the indefinite investment assertion on all foreign subsidiaries, the exposure to local withholding taxes would be less than $7 million.

Joint venture cash and Aspire Defence project cash balances reflect the amounts held by joint venture entities that we consolidate for financial reporting purposes. These amounts are limited to those entities' activities and are not readily available for general corporate purposes; however, portions of such amounts may become available to us in the future should there be a distribution of dividends to the joint venture partners. We expect that the majority of the joint venture cash balances will be utilized for the corresponding joint venture purposes or for paying dividends.

As of December 29, 2023, substantially all of our excess cash was held in interest bearing operating accounts or short-term investment accounts with the primary objectives of preserving capital and maintaining liquidity.

Cash Flows

The following table summarizes our cash flows for the periods indicated:

| | | | | | | | | | | | | | | | | | | | |

| | | Years ended, |

| | December 29, | | December 31, | | December 31, |

| Dollars in millions | | 2023 | | 2022 | | 2021 |

| Cash flows provided by operating activities | | $ | 331 | | | $ | 396 | | | $ | 278 | |

| Cash flows provided by (used in) investing activities | | (70) | | | 37 | | | (428) | |

| Cash flows provided by (used in) financing activities | | (359) | | | (399) | | | 87 | |

| Effect of exchange rate changes on cash | | 13 | | | (15) | | | (3) | |

| Increase (decrease) in cash and cash equivalents | | $ | (85) | | | $ | 19 | | | $ | (66) | |

Operating Activities. Cash provided by operations totaled $331 million and $396 million in 2023 and 2022, respectively, as compared to a net loss of $261 million and net income of $192 million in 2023 and 2022, respectively. Cash flows from operating activities result primarily from earnings and are affected by changes in operating assets and liabilities, which consist primarily of working capital balances for projects. Working capital levels vary from year to year and are primarily affected by the Company's volume of work. These levels are also impacted by the mix, stage of completion and commercial terms of projects. Working capital requirements also vary by project depending on the type of client and location throughout the world.

The decrease in operating cash flows in 2023 compared to 2022 is primarily attributed to the $144 million payment made in the third quarter of 2023 related to the settlement of a legacy legal matter. This decrease was offset by increases in operating cash flows from changes in our pension funding amounts in the 2023. In 2022, we made an advance payment in October 2022 to our U.K. pension plan for approximately £29 million of the £33 million required minimum annual contributions. No similar advance payments were made in 2023. Additionally, there were increases in operating cash flows from changes in the primary components of our working capital. The primary components of our working capital accounts are accounts receivable, contract assets, accounts payable and contract liabilities. These components are impacted by the size and changes in the mix of our cost-reimbursable and time-and-materials projects versus fixed price projects, and as a result, fluctuations in these components are not uncommon in our business.

Investing Activities. Cash used in investing activities totaled $70 million in 2023 and was primarily related to the second payment for an additional investment of $39 million in Mura Technology and capital expenditures of $80 million. This was offset by a return of investment of approximately $61 million from JKC resulting from the receipt of the second payment from the Subcontractor Settlement Agreement. See Note 9 "Equity Method Investments and Variable Interest Entities" for further details.

Cash provided by investing activities totaled $37 million in 2022 and was primarily due to a return of investment of approximately $190 million from JKC resulting from the receipt of the first payment from the Subcontractor Settlement Agreement, a return of investment from BRIS of $10 million as our cumulative distributions from inception of the joint venture exceeded our cumulative earnings and proceeds of $55 million from the sale of our investment interest in three U.K. Road Projects. See Note 9 "Equity Method Investments and Variable Interest Entities" for further details. This was partially offset by our first payment related to an additional investment of $61 million in Mura Technology, $71 million in capital expenditures, $13 million net cash paid upon divestiture of a joint venture acquired as part of a historical GS acquisition and $73 million net cash used for the acquisition of VIMA. See Note 4 "Acquisitions" for further details

Financing activities. Cash used in financing activities totaled $359 million in 2023 and was primarily due to a net cash outflow of $567 million for the settlement and maturity of our outstanding Convertible Notes, corresponding Note Hedge and warrants settled and paid during the year. Cash used in financing activities also included $72 million of dividend payments to common shareholders, $125 million for the repurchase of common stock under our share repurchase program, $13 million for the repurchase of common stock under our "withhold to cover" program, $340 million in payments on our revolving credit facility and $17 million of principal payments related to our Senior Credit Facility. These decreases were partially offset by $785 million in borrowings related to our revolving credit facility and $5 million in net proceeds from the issuance of common stock. See Note 11 "Debt and Other Credit Facilities" for further discussion of our Senior Credit Facility.

Cash used in financing activities totaled $399 million in 2022 and was primarily due to $193 million of repurchases of common stock under our share repurchase program, $66 million of dividend payments to common shareholders, $116 million in net payments on borrowings related to our Senior Credit Facility, $11 million repayment on our finance lease obligations, $10 million for the repurchase of common stock under our "withheld to cover" program and dividends paid to NCI shareholders of $4 million. These decreases were partially offset by $5 million in net proceeds received from the issuance of common stock and $3 million in investments from NCI shareholders.

Future sources of cash. We believe that future sources of cash include cash flows from operations (including accounts receivable monetization arrangements), cash derived from working capital management and cash borrowings under the Senior Credit Facility.

Future uses of cash. We believe that future uses of cash include working capital requirements, joint venture capital calls, capital expenditures, dividends, pension funding obligations, repayments of borrowings, share repurchases, legal settlements of any currently outstanding legal matter or any future legal proceeding and strategic investments including acquisitions, joint ventures and other business partnerships. Our capital expenditures will be focused primarily on facilities and equipment to support our businesses. In addition, we will use cash to make payments under leases and various other obligations, including potential litigation payments, as they arise.

Other factors potentially affecting liquidity

Ichthys LNG Project. As part of the settlement agreement between JKC and Ichthys LNG, Pty, Ltd (collectively, “the Parties”) in October 2021, KBR’s letters of credit were reduced to $82 million from $164 million. Additionally, as part of this settlement agreement, the Parties agreed to consult in good faith and to cooperate to seek maximum recovery from the insurance policies and paint manufacturer for the deterioration of paint and insulation on certain exterior areas of the plant. The Parties agreed to collectively pursue claims against the paint manufacturer, and JKC has assigned claims under the insurance policy regarding the paint and insulation matters to the client. The parties have agreed that if, at the date of final resolution of the above proceedings and claims with respect to the paint and insulation matters, the recovered amount from the paint manufacturer and insurance claim is less than the stipulated ceiling amount in the settlement agreement, JKC will pay the client the difference between the stipulated ceiling amount and the recovered amount. JKC has provided for and continues to maintain a provision for this contingent liability.

U.K. pension obligation. We have recognized on our consolidated balance sheets a funding deficit of approximately $15 million (calculated as the excess of the projected benefit obligations over the fair value of plan assets) as of December 29, 2023) for our frozen U.K. defined benefit pension plan. The total amount of employer pension contributions paid for the year ended December 29, 2023 is $9 million for our defined benefit plan in the U.K. On October 17, 2022, we made an advance payment to our U.K. pension plan for approximately £29 million of the £33 million required minimum annual contributions for the year ending December 29, 2023. The funding requirements for our U.K. pension plan are determined based on the U.K. Pensions Act 1995. Annual minimum funding requirements are based on a binding agreement with the Trustee of the U.K. pension plan that is negotiated on a triennial basis. In June 2022, KBR and the Trustee executed an agreement requiring minimum annual contributions of approximately £33 million (approximately $42 million at current exchange rates) for the period through March 2028. This schedule of contributions will be reviewed by the Trustee and KBR no later than 15 months after the effective date of each actuarial valuation, due every three years. In the future, pension funding may increase or decrease depending on changes in the levels of interest rates, pension plan asset return performance and other factors. A significant increase in our funding requirements for the U.K. pension plan could result in a material adverse impact on our financial position.

Sales of Receivables. From time to time, we sell certain receivables to unrelated third-party financial institutions under various accounts receivable monetization programs. One such program is with MUFG Bank, Ltd. (“MUFG”) under a Master Accounts Receivable Purchase Agreement (the “RPA”), which provides the sale to MUFG of certain of our designated eligible receivables, with a significant portion of such receivables being owed by the U.S. government. We plan to continue to utilize these programs to ensure we have flexibility in regards to meeting our capital needs. Refer to Note 20 "Fair Value of Financial Instruments and Risk Management" to our consolidated financial statements for further discussion on our sales of receivables.

Credit Agreement and Senior Credit Facility

Information relating to our Senior Credit Facility is described in Note 11 "Debt and Other Credit Facilities" to our consolidated financial statements in Part II, Item 8 of this Annual Report on Form 10-K and the information discussed therein is incorporated by reference into this Part II, Item 7.

Senior Notes

Information relating to our Senior Notes is described in Note 11 "Debt and Other Credit Facilities" to our consolidated financial statements in Part II, Item 8 of this Annual Report on Form 10-K and the information discussed therein is incorporated by reference into this Part II, Item 7.

Convertible Senior Notes

On November 15, 2018, we issued and sold $350 million of 2.50% Convertible Senior Notes due 2023 (the "Convertible Notes") pursuant to an indenture between us and Citibank, N.A., as trustee. Concurrent with the issuance of the Convertible Notes, we entered into privately negotiated convertible note hedge transactions (the "Note Hedge Transactions") and warrant transactions (the "Warrant Transactions") with the option counterparties. In 2023, we settled our outstanding Convertible Notes and corresponding Note Hedge and unwound the warrants.

For more information relating to our Convertible Notes, Note Hedge Transactions and Warrant Transactions, refer to Note 11 "Debt and Other Credit Facilities" and Note 22 "Cash Election and Repurchase of Convertible Notes and Warrant Unwind Agreements" to our consolidated financial statements in Part II, Item 8 of this Annual Report on Form 10-K and the information discussed therein is incorporated by reference into this Part II, Item 7.

Off-Balance Sheet Arrangements

Letters of credit, surety bonds and guarantees. In the ordinary course of business, we may enter into various arrangements providing financial or performance assurance to customers on behalf of certain consolidated and unconsolidated subsidiaries, joint ventures and other jointly executed contracts. Such off-balance sheet arrangements include letters of credit, surety bonds and corporate guarantees to support the creditworthiness or project execution commitments of these entities and typically have various expiration dates ranging from mechanical completion of the project being constructed to a period beyond completion in certain circumstances such as for warranties. We may also guarantee that a project, once completed, will achieve specified performance standards. If the project subsequently fails to meet guaranteed performance standards, we may incur additional costs, pay liquidated damages or be held responsible for the costs incurred by the client to achieve the required performance standards. The potential amount of future payments that we could be required to make under an outstanding performance arrangement is typically the remaining estimated cost of work to be performed by or on behalf of third parties. For cost-reimbursable contracts, amounts that may become payable pursuant to guarantee provisions are normally recoverable from the client for work performed under the contract. For fixed-price contracts, the performance guarantee amount is the cost to complete the contracted work, less amounts remaining to be billed to the client under the contract. Remaining billable amounts could be greater or less than the cost to complete the project. If costs exceed the remaining amounts payable under the contract, we may have recourse to third parties, such as owners, subcontractors or vendors for claims.

In our joint venture arrangements, the liability of each partner is usually joint and several. This means that each joint venture partner may become liable for the entire risk of performance guarantees provided by each partner to the customer. Typically, each joint venture partner indemnifies the other partners for any liabilities incurred in excess of the liabilities the other party is obligated to bear under the respective joint venture agreement. We are unable to estimate the maximum potential amount of future payments that we could be required to make under outstanding performance guarantees related to joint venture projects due to a number of factors, including but not limited to, the nature and extent of any contractual defaults by our joint venture partners, resource availability, potential performance delays caused by the defaults, the location of the projects and the terms of the related contracts. See “Item 1A. Risk Factors” contained in Part I of this Annual Report on Form 10-K for information regarding our fixed-price contracts and operations through joint ventures and partnerships.

In certain limited circumstances, we enter into financial guarantees in the ordinary course of business, with financial institutions and other credit grantors, which generally obligate us to make payment in the event of a default by the borrower. These arrangements generally require the borrower to pledge collateral to support the fulfillment of the borrower’s obligation. We account for both financial and performance guarantees at fair value at issuance in accordance with ASC 460-10 Guarantees and, as of December 29, 2023, we had no material guarantees of the work or obligations of third parties recorded.

As of December 29, 2023, we had $1 billion in a committed line of credit on the Revolver under our Senior Credit Facility and $392 million of bilateral and uncommitted lines of credit to support the issuance of letters of credit. As of December 29, 2023, with respect to our Revolver, we had $505 million of outstanding borrowings. We also have $14 million of outstanding letters of credit on our Senior Credit Facility. With respect to our $392 million of bilateral and uncommitted lines of credit, we utilized $298 million for letters of credit as of December 29, 2023. The total remaining capacity of these committed and uncommitted lines of credit was approximately $575 million. Information relating to our letters of credit is described in Note 11 "Debt and Other Credit Facilities" to our consolidated financial statements in Part II, Item 8 of this Annual Report on Form 10-K and the information discussed therein is incorporated by reference into this Part II, Item 7. Other than as discussed in this report, we have not engaged in any material off-balance sheet financing arrangements through special purpose entities.

Contractual Obligations and Commitments

Significant contractual obligations and commercial commitments as of December 29, 2023 are as follows:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Payments Due |

| Dollars in millions | 2024 | | 2025 | | 2026 | | 2027 | | 2028 | | Thereafter | | Total |

Debt obligations (a) | $ | 31 | | | $ | 31 | | | $ | 1,054 | | | $ | 485 | | | $ | 250 | | | $ | — | | | $ | 1,851 | |

Interest (a) (b) | 95 | | | 107 | | | 95 | | | 13 | | | 12 | | | — | | | 322 | |

| Operating leases | 55 | | | 49 | | | 36 | | | 31 | | | 30 | | | 70 | | | 271 | |

| Finance leases | 12 | | | 7 | | | 1 | | | 1 | | | 1 | | | — | | | 22 | |

Pension funding obligation (c) | 42 | | | 41 | | | 41 | | | 41 | | | 15 | | | — | | | 180 | |

Purchase obligations (d) | 51 | | | 35 | | | 11 | | | 6 | | | — | | | — | | | 103 | |

| | | | | | | | | | |

Total (e) | $ | 286 | | | $ | 270 | | | $ | 1,238 | | | $ | 577 | | | $ | 308 | | | $ | 70 | | | $ | 2,749 | |

(a)Subsequent to December 29, 2023, we entered into Amendment No.11 and Amendment No.12 to our Credit Agreement. See Note 11 "Debt and Other Credit Facilities" for additional information.

(b)Determined based on long-term debt borrowings outstanding at the end of 2023 using the interest rates in effect for the individual borrowings as of December 29, 2023, including the effects of interest rate swaps. The payments due for interest reflect the cash interest that will be paid, which includes interest on outstanding borrowings and commitment fees. These amounts exclude the amortization of discounts or debt issuance costs.

(c)Included in our pension funding obligations are payments related to our agreement with the trustees of our U.K. pension plan. The agreement for this plan calls for minimum annual contributions of £33 million ($42 million at current exchange rates) from 2024 through the next valuation.

(d)In the ordinary course of business, we enter into commitments to purchase software and related maintenance, materials, supplies and similar items. The purchase obligations disclosed above do not include purchase obligations that we enter into with vendors in the normal course of business that support direct project costs on existing contracting arrangements with our customers. We expect to recover such obligations from our customers.

(e)We have excluded uncertain tax positions totaling $74 million as of December 29, 2023. The ultimate timing of settlement of these obligations cannot be determined with reasonable assurance. See Note 12 to our consolidated financial statements for further discussion on income taxes.

Transactions with Joint Ventures

In the normal course of business, we form incorporated and unincorporated joint ventures to execute projects. In addition to participating as a joint venture partner, we often provide engineering, procurement, construction, operations or maintenance services to the joint venture as a subcontractor. Where we provide services to a joint venture that we control and therefore consolidate for financial reporting purposes, we eliminate intercompany revenues and expenses on such transactions. In situations where we account for our interest in the joint venture under the equity method of accounting, we do not eliminate any portion of our subcontractor revenues or expenses, however, we recognize profit on our subcontractor scope of work only to the extent the joint venture's scope of work to the end customer is complete. We recognize revenue over time on our services provided to joint ventures that we consolidate and our services provided to joint ventures that we record under the equity method of accounting. See Note 9 to our consolidated financial statements in Part II, Item 8 of this Annual Report on Form 10-K for more information. The information discussed therein is incorporated by reference into this Part II, Item 7.

Recent Accounting Pronouncements

Information relating to recent accounting pronouncements is described in Note 21 to our consolidated financial statements in Part II, Item 8 of this Annual Report on Form 10-K and the information discussed therein is incorporated by reference into this Part II, Item 7.

U.S. Government Matters

Information relating to U.S. government matters commitments and contingencies is described in Note 14 to our consolidated financial statements in Part II, Item 8 of this Annual Report on Form 10-K and the information discussed therein is incorporated by reference into this Part II, Item 7.

Legal Proceedings

Information relating to various commitments and contingencies is described in Notes 6, 13 and 14 to our consolidated financial statements in Part II, Item 8 of this Annual Report on Form 10-K and the information discussed therein is incorporated by reference into this Part II, Item 7.

Critical Accounting Policies and Estimates

The discussion and analysis of our financial condition and results of operations is based upon our consolidated financial statements which have been prepared in conformity with U.S. GAAP. The preparation of our consolidated financial statements requires us to make estimates and judgments that affect the determination of financial positions, results of operations, cash flows and related disclosures. Our significant accounting policies are described in Note 1 to our consolidated financial statements. The following discussion is intended to highlight and describe those accounting policies that are especially critical to the preparation of our consolidated financial statements and to provide a better understanding of our significant accounting estimates and assumptions about future events that affect the amounts reported in our consolidated financial statements. Significant accounting estimates are important to the representation of our financial position and results of operations and involve our most difficult, subjective or complex judgments. We base our estimates on historical experience and various other assumptions we believe to be reasonable according to the current facts and circumstances through the date of the issuance of our financial statements.

Contract Revenue and Contract Estimates. Our policy on revenue recognition is provided in Note 1 to our consolidated financial statements for the year ended December 29, 2023 and is also applied to the revenues of our equity method investments included in equity in earnings of unconsolidated affiliates. We recognize revenue on substantially all of our contracts over time, as performance obligations are satisfied, due to the continuous transfer of control to the customer. Our contracts are generally accounted for as a single performance obligation and are not segmented between types of services provided. We recognize revenue on those contracts over time using the cost-to-cost method, based primarily on contract costs incurred to date compared to total estimated contract costs at completion. Contract costs include all direct materials, labor and subcontractors costs and indirect costs related to contract performance. We believe this method is the most accurate measure of contract performance because it directly measures the value of the goods and services transferred to the customer. For all other contracts we recognize revenue when services are performed which generally coincides with our ability to bill.

The cost-to-cost method of revenue recognition requires us to prepare estimates of cost to complete for contracts in progress. Due to the nature of the work performed on many of our performance obligations, the estimates of total revenue and cost at completion is complex, subject to many variables and require significant judgment. In making such estimates, judgments are required to evaluate contingencies such as potential variances in schedule and the cost of materials, labor and productivity, the impact of change orders, liability claims, contract disputes and achievement of contractual performance standards. As a significant change in one or more of these estimates could affect the profitability of our contracts, we routinely review and update our significant contract estimates through a disciplined project review process in which management reviews the progress and execution of our performance obligations and estimates at completion. We have a long history of working with multiple types of projects and in preparing cost estimates. However, there are many factors that impact future cost as outlined in “Item 1A. Risk Factors” contained in Part I of this Annual Report on Form 10-K. These factors can affect the accuracy of our estimates and materially impact our future reported earnings. Changes in total estimated contract costs and losses, if any, are recognized on a cumulative catch-up basis in the period in which the changes are identified at the contract level. Such changes in contract estimates can result in the recognition of revenue in a current period for performance obligations which were satisfied or partially satisfied in a prior period. Changes in contract estimates may also result in the reversal of previously recognized revenue if the current estimate differs from the previous estimate.

It is common for our contracts to contain variable consideration in the form of incentive fees, performance bonuses, award fees, liquidated damages or penalties that may increase or decrease the transaction price. Variable consideration may be tied to our performance, cost targets, or achievement of milestones. Other contract provisions also give rise to variable consideration such as unapproved change orders and claims, and on certain contracts, index-based price adjustments. We estimate the amount of variable consideration at the most likely amount we expect to be entitled and include in the transaction price when it is probable that a significant reversal of cumulative revenue recognized will not occur. Variable consideration

associated with claims and unapproved change orders is included in the transaction price only to the extent of costs incurred. We recognize claims against suppliers and subcontractors as a reduction in recognized costs when enforceability is established by the contract and the amounts are reasonably estimable and probable of recovery. Reductions in costs are recognized to the extent of the lesser of the amounts management expects to recover or actual costs incurred.

Under cost-reimbursable contracts, the price is generally variable based upon our actual allowable costs incurred for materials, equipment, reimbursable labor hours, overhead and G&A expenses. The FAR provides guidance on types of costs that are allowable in establishing prices for goods and services provided to the U.S. government and its agencies. Pricing, including the types of costs that are allowable, for non-U.S. government agencies and commercial customers is based on specific negotiations with each customer. We recognize revenue on cost-reimbursable contracts to the extent it is not probable a significant reversal will occur.

Our estimates of variable consideration and determination of whether to include such amounts in the transaction price are based largely on our assessment of legal enforceability, anticipated performance and any other information (historical, current or forecasted) that is reasonably available to us.

Goodwill and Intangible Assets. Goodwill is tested annually for possible impairment as of the first day of the fourth fiscal quarter within our fiscal year, and on an interim basis when indicators of possible impairment exist. For purposes of impairment testing, goodwill is assigned to the applicable reporting units based on our current reporting structure. We have the option to first assess qualitative factors to determine whether it is more likely than not that the fair value of a reporting unit is less than its carrying value. Qualitative factors assessed for each of the applicable reporting units include, but are not limited to, changes in macroeconomic conditions, industry and market considerations, cost factors, discount rates, competitive environments and financial performance of the reporting units. If the qualitative assessment indicates that it is more likely than not that the carrying value of a reporting unit exceeds its estimated fair value, a quantitative test is required.