LINDE PLC - Annual Report: 2019 (Form 10-K)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

___________________________________

FORM 10-K

_______________________________________________

☑ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2019

OR

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 001-38730

LINDE PLC

(Exact name of registrant as specified in its charter)

Ireland | 98-1448883 | ||||

(State or other jurisdiction of incorporation) | (I.R.S. Employer Identification No.) | ||||

The Priestley Centre | |||||

10 Priestley Road, | |||||

Surrey Research Park, | |||||

Guildford, | Surrey | GU2 7XY | |||

United Kingdom | |||||

(Address of principal executive offices) (Zip Code) | |||||

+44 | 14 | 83 242200 | |||

(Registrant's telephone number, including area code) | |||||

Securities registered pursuant to Section 12(b) of the Act:

Title of each class: | Trading Symbol(s) | Name of each exchange on which registered: |

Ordinary shares (€0.001 nominal value per share) | LIN | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

___________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," " smaller reporting company, " and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☑ Accelerated filer ☐ Non- accelerated filer ☐ Smaller reporting company ☐ Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☑

The aggregate market value of the voting and non-voting common stock held by non-affiliates as of June 30, 2019, was approximately $108 billion (based on the closing sale price of the stock on that date as reported on the New York Stock Exchange).

At January 31, 2020, 532,959,736 ordinary shares of €0.001 nominal value per share of the Registrant were outstanding.

Documents incorporated by reference:

Portions of the Proxy Statement of Linde plc for its 2020 Annual General Meeting of Shareholders, are incorporated in Part III of this report.

LINDE PLC

ANNUAL REPORT ON FORM 10-K

For the fiscal year ended December 31, 2019

TABLE OF CONTENTS

Page | ||

Part I | ||

Item 1: | ||

Item 1A: | ||

Item 1B: | ||

Item 2: | ||

Item 3: | ||

Item 4: | ||

Part II | ||

Item 5: | ||

Item 6: | ||

Item 7: | ||

Item 7A: | ||

Item 8: | ||

Item 9: | ||

Item 9A: | ||

Item 9B: | ||

Part III | ||

Item 10: | ||

Item 11: | ||

Item 12: | ||

Item 13: | ||

Item 14: | ||

Part IV | ||

Item 15: | ||

Item 16: | ||

2

FORWARD-LOOKING STATEMENTS

This document contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are identified by terms and phrases such as: anticipate, believe, intend, estimate, expect, continue, should, could, may, plan, project, predict, will, potential, forecast, and similar expressions. They are based on management’s reasonable expectations and assumptions as of the date the statements are made but involve risks and uncertainties. These risks and uncertainties include, without limitation: the ability to successfully integrate the Praxair and Linde AG businesses; regulatory or other requirements imposed as a result of the business combination of Praxair and Linde AG that could reduce anticipated benefits of the transaction; the risk that Linde plc may be unable to achieve expected synergies or that it may take longer or be more costly than expected to achieve those synergies; the performance of stock markets generally; developments in worldwide and national economies and other international events and circumstances, including trade conflicts and tariffs; changes in foreign currencies and in interest rates; the cost and availability of electric power, natural gas and other raw materials; the ability to achieve price increases to offset cost increases; catastrophic events including natural disasters, epidemics and acts of war and terrorism; the ability to attract, hire, and retain qualified personnel; the impact of changes in financial accounting standards; the impact of changes in pension plan liabilities; the impact of tax, environmental, healthcare and other legislation and government regulation in jurisdictions in which the company operates, including the impact of the U.S. Tax Cuts and Jobs Act of 2017; the cost and outcomes of investigations, litigation and regulatory proceedings; the impact of potential unusual or non-recurring items; continued timely development and market acceptance of new products and applications; the impact of competitive products and pricing; future financial and operating performance of major customers and industries served; the impact of information technology system failures, network disruptions and breaches in data security; and the effectiveness and speed of integrating new acquisitions into the business. These risks and uncertainties may cause actual future results or circumstances to differ materially from accounting principles generally accepted in the United States of America, International Financial Reporting Standards or adjusted projections, estimates or other forward-looking statements.

Linde plc assumes no obligation to update or provide revisions to any forward-looking statement in response to changing circumstances. The above listed risks and uncertainties are further described in Item 1A (Risk Factors) in this report, which should be reviewed carefully. Please consider Linde plc’s forward-looking statements in light of those risks.

3

Linde plc and Subsidiaries

PART I

ITEM 1. BUSINESS

General

Linde plc is a public limited company formed under the laws of Ireland with its principal offices in the United Kingdom. Linde plc was formed in 2017 in accordance with the requirements of the business combination agreement, dated June 1, 2017, as amended, between Linde plc, Praxair, Inc. ("Praxair") and Linde Aktiengesellschaft ("Linde AG"). Effective October 31, 2018, the business combination was completed and Linde plc is comprised of the businesses of Praxair and Linde AG (hereinafter the combined group will be referred to as "the company" or "Linde").

The business combination brought together two leading companies in the global industrial gases industry, leveraging the proven strengths of each. Linde believes the merger will combine Linde AG’s long-held expertise in technology with Praxair’s efficient operating model, thus creating a global leader. The company is expected to have strong positions in key geographies and end markets that will create a more diverse and balanced global portfolio.

Linde is the largest industrial gas company worldwide and is a major technological innovator in the industrial gases industry. Its primary products in its industrial gases business are atmospheric gases (oxygen, nitrogen, argon, and rare gases) and process gases (carbon dioxide, helium, hydrogen, electronic gases, specialty gases, and acetylene). The company also designs and builds equipment that produces industrial gases primarily for internal use and offers customers a wide range of gas production and processing services such as olefin plants, natural gas plants, air separation plants, hydrogen and synthesis gas plants and other types of plants.

Linde serves a diverse group of industries including healthcare, petroleum refining, manufacturing, food, beverage carbonation, fiber-optics, steel making, aerospace, chemicals, electronics and water treatment.

In 2018, the company, Praxair and Linde AG entered into various agreements with regulatory authorities to satisfy antitrust requirements to secure approval to consummate the business combination. These agreements required the sale of the majority of Praxair's European industrial gases business (completed on December 3, 2018), the majority of Linde AG's Americas industrial gases business (completed on March 1, 2019), select assets of Linde AG's South Korea industrial gases business (completed April 30, 2019), select assets of Praxair's Indian industrial gases business (completed July 12, 2019), select assets of Linde AG's Indian industrial gases business (completed December 16, 2019) as well as certain divestitures of other Praxair and Linde AG businesses in Asia that are expected to be sold in 2020. As of December 31, 2018 and until the completion of the majority of such divestitures, Linde AG and Praxair were obligated to operate their businesses globally as separate and independent companies, and not coordinate any of their commercial operations. The U.S. Federal Trade Commission's (“FTC”) hold separate order (“HSO”) restrictions were lifted March 1, 2019, concurrent with the sale of the required merger-related divestitures in the United States. See Note 4 to the consolidated financial statements for additional information relating to divestitures.

Praxair was determined to be the accounting acquirer in the business combination. Accordingly, the historical financial statements of Praxair for the periods prior to the business combination are considered to be the historical financial statements of the company. The results of Linde AG are included in Linde's consolidated results from the date of the completion of the business combination forward. During 2018, the company reported its continuing operations in six reporting segments under which it managed its operations, assessed performance, and reported earnings: North America, South America, Asia, Europe, Surface Technologies and Linde AG. Effective with the lifting of the hold separate order on March 1, 2019, new operating segments were established. Linde’s industrial gases operations are managed on a geographic basis, which represents three of the company's new reportable segments - Americas, EMEA (Europe/Middle East/Africa), and APAC (Asia/South Pacific); a fourth reportable segment which represents the company's Engineering business, designs and manufactures equipment for air separation and other industrial gas applications specifically for end customers and is managed on a worldwide basis operating in all geographic segments. Other consists of corporate costs and a few smaller businesses, which individually do not meet the quantitative thresholds for separate presentation.

Linde’s sales were $28,228 million, $14,836 million, and $11,358 million for 2019, 2018, and 2017, respectively. Refer to Item 7, Management's Discussion and Analysis, for a discussion of consolidated sales and Note 20 to the consolidated financial statements for additional information related to Linde’s reportable segments.

Industrial Gases Products and Manufacturing Processes

Atmospheric gases are the highest volume products produced by Linde. Using air as its raw material, Linde produces oxygen, nitrogen and argon through several air separation processes of which cryogenic air separation is the most prevalent. Rare gases, such as krypton, neon and xenon, are also produced through cryogenic air separation. As a pioneer

4

in the industrial gases industry, Linde is a leader in developing a wide range of proprietary and patented applications and supply systems technology. Linde also led the development and commercialization of non-cryogenic air separation technologies for the production of industrial gases. These technologies open important new markets and optimize production capacity for the company by lowering the cost of supplying industrial gases. These technologies include proprietary vacuum pressure swing adsorption (“VPSA”) and membrane separation to produce gaseous oxygen and nitrogen, respectively.

Process gases, including carbon dioxide, hydrogen, carbon monoxide, helium, specialty gases and acetylene are produced by methods other than air separation. Most carbon dioxide is purchased from by-product sources, including chemical plants, refineries and industrial processes or is recovered from carbon dioxide wells. Carbon dioxide is processed in Linde’s plants to produce commercial and food-grade carbon dioxide. Hydrogen and carbon monoxide can be produced by either steam methane reforming or auto-thermal reforming of natural gas or other feed streams such as naphtha. Hydrogen is also produced by purifying by-product sources obtained from the chemical and petrochemical industries. Acetylene is primarily sourced as a chemical by-product, but may also be produced from calcium carbide and water.

Industrial Gases Distribution

There are three basic distribution methods for industrial gases: (i) on-site or tonnage; (ii) merchant or bulk liquid; and (iii) packaged or cylinder gases. These distribution methods are often integrated, with products from all three supply modes coming from the same plant. The method of supply is generally determined by the lowest cost means of meeting the customer’s needs, depending upon factors such as volume requirements, purity, pattern of usage, and the form in which the product is used (as a gas or as a cryogenic liquid).

On-site. Customers that require the largest volumes of product (typically oxygen, nitrogen and hydrogen) and that have a relatively constant demand pattern are supplied by cryogenic and process gas on-site plants. Linde constructs plants on or adjacent to these customers’ sites and supplies the product directly to customers by pipeline. On-site product supply contracts generally are total requirement contracts with terms typically ranging from 10-20 years and containing minimum purchase requirements and price escalation provisions. Many of the cryogenic on-site plants also produce liquid products for the merchant market. Therefore, plants are typically not dedicated to a single customer. Advanced air separation processes allow on-site delivery to customers with smaller volume requirements. Customers using these systems usually enter into requirement contracts with terms typically ranging from ten to twenty years.

Merchant. The merchant business is generally associated with distributable liquid oxygen, nitrogen, argon, carbon dioxide, hydrogen and helium. The deliveries generally are made from Linde’s plants by tanker trucks to storage containers at the customer's site which are owned and maintained by Linde and leased to the customer. Due to distribution cost, merchant oxygen and nitrogen generally have a relatively small distribution radius from the plants at which they are produced. Merchant argon, hydrogen and helium can be shipped much longer distances. The customer agreements used in the merchant business are usually three to seven-year requirement contracts.

Packaged Gases. Customers requiring small volumes are supplied products in metal containers called cylinders, under medium to high pressure. Packaged gases include atmospheric gases, carbon dioxide, hydrogen, helium, acetylene and related products. Linde also produces and distributes in cylinders a wide range of specialty gases and mixtures. Cylinders may be delivered to the customer’s site or picked up by the customer at a packaging facility or retail store. Packaged gases are generally sold under one to three-year supply contracts and through purchase orders.

A substantial amount of the cylinder gases sold in the United States are distributed by independent distributors that buy merchant gases in liquid form and repackage the products in their facilities. Packaged gas distributors, including Linde, also distribute hardgoods and welding equipment purchased from independent manufacturers. Over time, Linde has acquired a number of independent industrial gases and welding products distributors at various locations in the United States and continues to sell merchant gases to other independent distributors. Between its own distribution business, joint ventures and sales to independent distributors, Linde is represented in 48 states, the District of Columbia and Puerto Rico.

Engineering

Linde’s Engineering business has a global presence, with its focus on market segments such as olefin, natural gas, air separation, hydrogen and synthesis gas plants. The company utilizes its own extensive process engineering know-how in the planning, project development and construction of turnkey industrial plants and associated services. Linde plants are used in a wide variety of fields: in the petrochemical and chemical industries, in refineries and fertilizer plants, to recover air gases, to produce hydrogen and synthesis gases, to treat natural gas and to produce noble gases. The Engineering business either supplies plant components and services directly to the customer or to the industrial gas business of Linde which operates the plants on behalf of the customer under a long-term gases supply contract.

5

Inventories – Linde carries inventories of merchant and cylinder gases, hardgoods and coatings materials to supply products to its customers on a reasonable delivery schedule. On-site plants and pipeline complexes have limited inventory. Inventory obsolescence is not material to Linde’s business.

Customers – Linde is not dependent upon a single customer or a few customers.

International – Linde is a global enterprise with approximately 70% of its 2019 sales outside of the United States. The company also has majority or wholly owned subsidiaries that operate in approximately 45 European, Middle Eastern and African countries (including Germany, France, Sweden, the Republic of South Africa, and the United Kingdom); approximately 20 Asian and South Pacific countries (including China, Taiwan, India and Australia); and approximately 20 countries in North and South America (including Canada, Mexico and Brazil).

The company also has equity method investments operating in Europe, Asia, Africa, the Middle East, and North America.

Linde’s international business is subject to risks customarily encountered in foreign operations, including fluctuations in foreign currency exchange rates, import and export controls, and other economic, political and regulatory policies of local governments. Also, see Item 1A. “Risk Factors” and Item 7A. “Quantitative and Qualitative Disclosures About Market Risk.”

Seasonality – Linde’s business is generally not subject to seasonal fluctuations to any significant extent.

Research and Development – Linde’s research and development is directed toward development of gas processing, separation and liquefaction technologies, improving distribution of industrial gases and the development of new markets and applications for these gases. This results in the development of new advanced air separation, hydrogen, synthesis gas, natural gas, adsorption and chemical process technologies as well as the frequent introduction of new industrial gas applications. Research and development is primarily conducted at Pullach, Germany, Tonawanda, New York, Burr Ridge, Illinois and Shanghai, China.

Patents and Trademarks – Linde owns or licenses a large number of patents that relate to a wide variety of products and processes. Linde’s patents expire at various times over the next 20 years. While these patents and licenses are considered important to its individual businesses, Linde does not consider its business as a whole to be materially dependent upon any one particular patent, or patent license, or family of patents. Linde also owns a large number of trademarks, of which the "Linde" trademark is the most significant.

Raw Materials and Energy Costs – Energy is the single largest cost item in the production and distribution of industrial gases. Most of Linde’s energy requirements are in the form of electricity, natural gas and diesel fuel for distribution. The company mitigates electricity, natural gas, and hydrocarbon price fluctuations contractually through pricing formulas, surcharges, and cost pass–through and tolling arrangements.

The supply of energy has not been a significant issue in the geographic areas where the company conducts business. However, energy availability and price is unpredictable and may pose unforeseen future risks.

For carbon dioxide, carbon monoxide, helium, hydrogen, specialty gases and surface technologies, raw materials are largely purchased from outside sources. Linde has contracts or commitments for, or readily available sources of, most of these raw materials; however, their long-term availability and prices are subject to market conditions.

Competition – Linde participates in highly competitive markets in the industrial gases, engineering and healthcare businesses, which are characterized by a mixture of local, regional and global players, all of which exert competitive pressure on the parties. In locations where Linde has pipeline networks, which enable the company to provide reliable and economic supply of products to larger customers, Linde derives a competitive advantage.

Competitors in the industrial and medical gases industry include global and regional companies such as L’Air Liquide S.A., Air Products and Chemicals, Inc., Messer Group GmbH, Mitsubishi Chemical Holdings Corporation (through Taiyo Nippon Sanso Corporation) as well as an extensive number of small to medium size independent industrial gas companies which compete locally as producers or distributors. In addition, a significant portion of the international gases market relates to customer-owned plants.

Employees and Labor Relations – As of December 31, 2019, Linde had 79,886 employees worldwide. Linde has collective bargaining agreements with unions at numerous locations throughout the world, which expire at various dates. Linde considers relations with its employees to be satisfactory.

Environment – Information required by this item is incorporated herein by reference to the section captioned “Management’s Discussion and Analysis – Environmental Matters” in Item 7 of this 10-K.

6

Available Information – The company makes its periodic and current reports available, free of charge, on or through its website, www.linde.com, as soon as practicable after such material is electronically filed with, or furnished to, the Securities and Exchange Commission ("SEC"). Investors may also access from the company website other investor information such as press releases and presentations. Information on the company’s website is not incorporated by reference herein. In addition, the public may read and copy any materials filed with the SEC free of charge at the SEC’s website, www.sec.gov, that contains reports, proxy information statements and other information regarding issuers that file electronically.

Executive Officers – The following Executive Officers have been elected by the Board of Directors and serve at the pleasure of the Board. It is expected that the Board will elect officers annually following each annual meeting of shareholders.

Stephen F. Angel, 64, is Chief Executive Officer of Linde. Prior to that, Mr. Angel was Chairman, President and CEO of Praxair, Inc. since 2007. Angel joined Praxair in 2001 as an executive vice president and was named president and chief operating officer in February 2006. Prior to joining Praxair, Angel spent 22 years in a variety of management positions with General Electric. Angel serves on the board of directors of PPG Industries and the U.S.-China Business Council and is a member of The Business Council. Angel received a bachelor of science degree in civil engineering from North Carolina State University and an MBA from Loyola College in Baltimore.

Dr. Christian Bruch, age 49, became an executive officer and a member of the Management Committee of Linde in connection with the business combination in October 2018. He is also the Head of Engineering for Linde and is a member of the Executive Board of Linde AG. Dr. Bruch joined The Linde Group's Gases Division in 2004 as a Business Development Manager for Airgases. In 2006 he became the Head of Tonnage Business Development for air separation projects in Europe, the Middle East and Africa. In 2009 he transferred to the Engineering Division, where he was responsible for the product line Air Separation Plants. In 2013 he was appointed a member of the Board of Directors at the Engineering Division, a position he held until becoming a member of the Executive Board of Linde AG at the beginning of 2015 responsible for the Linde Engineering Division and the Corporate & Support Function Technology & Innovation. Prior to joining The Linde Group, Dr. Bruch worked for the Swiss Institute of Technology in Zürich and for the RWE Group in Essen, Germany.

Kelcey E. Hoyt, age 50, became the Chief Accounting Officer of Linde in connection with the business combination in October 2018. Prior to this, she served as Vice President and Controller of Praxair, Inc. effective August 1, 2016. Prior to becoming Controller, she served as Praxair’s Director of Investor Relations since 2010. She joined Praxair in 2002 and served as Director of Corporate Accounting and SEC Reporting through 2008, and later served as Controller for various divisions within Praxair’s North American Industrial Gas business. Previously, she had five years of experience in audit at KPMG, LLP.

Sanjiv Lamba age 55, became an executive officer and a member of the Management Committee of Linde in connection with the business combination in October 2018. He is the Head of APAC. Mr. Lamba was appointed a Member of the Executive Board of Linde AG in 2011, responsible for the Asia, Pacific segment of the Gases Division, for Global Gases Businesses Helium & Rare Gases, Electronics as well as Asia Joint Venture Management. Mr. Lamba started his career 1989 with BOC India in Finance where he progressed to become Director of Finance. He was appointed Managing Director for BOC’s India’s business in 2001. Throughout his years with BOC/Linde, he has worked in a number of geographies including Germany, the UK, Singapore and India where he has held numerous roles across the organization.

Eduardo F. Menezes, age 56, became an executive officer and a member of the Management Committee of Linde in connection with the business combination in October 2018. He is the Head of EMEA. Mr. Menezes previously served as Executive Vice President of Praxair, Inc. since 2012, responsible for Praxair Europe, Praxair Mexico, Praxair South America and Praxair Asia. From 2010 to March 2011, he was a Vice President of Praxair with responsibility for the North American Industrial Gases business and was named senior vice president in 2011. From 2007 to 2010, he was President of Praxair Europe. He served as Managing Director of Praxair’s business in Mexico from 2004 to 2007, as Vice President and General Manager for Praxair Distribution, Inc. from 2003 to 2004 and as Vice President, U.S. West Region, for North American Industrial Gases, from 2000 to 2003.

Dr. Andreas Opfermann, 48, became Executive Vice President of Americas and a member of the Management Committee of Linde in November 2019. Prior to this, from 2016-2019, he was the regional business unit leader for Linde’s North European region. Dr. Opfermann joined Linde in 2005 initially in Corporate Strategy. He has subsequently served as Head of Innovation Management from 2008 to 2010, Head of Clean Energy and Innovation Management from 2010 to 2014, and Head of Technology and Innovation from 2015 to 2016, responsible for all Linde research and development. Before joining Linde, he held positions at McKinsey & Company.

7

Anne K. Roby, age 55, became an executive officer and a member of the Management Committee of Linde in connection with the business combination in October 2018. She is the Head of Global Functions. Prior to this, Dr. Roby served as Senior Vice President of Praxair, Inc. since January 1, 2014, responsible for Global Supply Systems, R&D, Global Market Development, Global Operations Excellence, Global Strategic Sales, Global Procurement, Sustainability and Safety, Health and Environment. From 2011to 2013, she served as President of Praxair Asia, responsible for Praxair’s industrial gases business in China, India, South Korea and Thailand as well as the electronics market globally. In 2010, Dr. Roby became President of Praxair Electronics, after having served as Vice President, Global Sales, for Praxair from 2009 to 2010. Prior to this, she was Vice President of the Praxair U.S. South Region from 2006 to 2009. Dr. Roby joined Praxair in 1991 as a development associate in the company’s R&D organization and was promoted to other positions of increasing responsibility.

Matt J. White, age 47, became an executive officer and a member of the Management Committee of Linde in connection with the business combination in October 2018. He is the Chief Financial Officer for Linde. He previously served as the Senior Vice President and Chief Financial Officer of Praxair, Inc. since January 1, 2014. Prior to this, Mr. White was President of Praxair Canada from 2011-2014. He joined Praxair in 2004 as finance director for the company’s largest business unit, North American Industrial Gases. In 2008, he became Vice President and Controller of Praxair, Inc., then was named Vice President and Treasurer in 2010. Before joining Praxair, White was vice president, finance, at Fisher Scientific and before that he held various financial positions, including group controller, at GenTek, a manufacturing and performance chemicals company.

8

ITEM 1A. RISK FACTORS

Due to the size and geographic reach of the company’s operations, a wide range of factors, many of which are outside of the company’s control, could materially affect the company’s future operations and financial performance. Management believes the following risks may significantly impact the company:

The company may fail to realize the anticipated strategic and financial benefits sought from the business combination.

The company may not realize all of the anticipated benefits of the business combination between Praxair, Inc. and Linde AG, which was completed on October 31, 2018. The success of the business combination will depend on, among other things, the company’s ability to combine Praxair, Inc.’s and Linde AG’s businesses in a manner that facilitates growth and realizes the anticipated annual synergies and cost reductions without adversely affecting current revenues and investments in future growth. The actual integration will continue to involve complex operational, technological and personnel-related challenges. Difficulties in the integration of the businesses, which may result in significant costs and delays, include:

• | managing a significantly larger combined group; |

• | aligning and executing the strategy of the company; |

• | integrating and unifying the offerings and services available to customers and coordinating distribution and marketing efforts in geographically separate organizations; |

• | coordinating corporate and administrative infrastructures and aligning insurance coverage; |

• | coordinating accounting, reporting, information technology, communications, administration and other systems; |

• | addressing possible differences in corporate cultures and management philosophies; |

• | the company being subject to Irish laws and regulations and legal action in Ireland; |

• | coordinating the compliance program and uniform financial reporting, information technology and other standards, controls, procedures and policies; |

• | the implementation, ultimate impact and outcome of post-completion reorganization transactions, which may be delayed; |

• | unforeseen and unexpected liabilities related to the business combination or the combined businesses; |

• | managing tax costs or inefficiencies associated with integrating operations; |

• | identifying and eliminating redundant and underperforming functions and assets; and |

• | effecting actions that may be required in connection with obtaining regulatory approvals. |

These and other factors could result in increased costs and diversion of management’s time and energy, as well as decreases in the amount of expected revenue and earnings. The integration process and other disruptions resulting from the business combination may also adversely affect the company’s relationships with employees, suppliers, customers, distributors, licensors and others with whom Praxair, Inc. and Linde AG have business or other dealings, and difficulties in integrating the businesses could harm the reputation of the company.

If the company is not able to successfully integrate the businesses of Praxair, Inc. and Linde AG in an efficient, cost-effective and timely manner, the anticipated benefits and cost savings of the business combination may not be realized fully, or at all, or may take longer to realize than expected.

Weakening economic conditions in markets in which Linde does business may adversely impact its financial results and/or cash flows.

Linde serves a diverse group of industries across more than 100 countries, which generally leads to financial stability through various business cycles. However, a broad decline in general economic or business conditions in the industries served by its customers could adversely affect the demand for Linde’s products and impair the ability of its customers to satisfy their obligations to Linde, resulting in uncollected receivables and/or unanticipated contract terminations or project delays. For example, global political and economic uncertainty could reduce investment activities of Linde’s customers, which could adversely affect Linde’s business.

In addition, many of Linde’s customers are in businesses that are cyclical in nature, such as the chemicals, electronics, metals and energy industries. Downturns in these industries may adversely impact Linde during these cycles. Additionally, such conditions could impact the utilization of Linde’s manufacturing capacity which may require it to

9

recognize impairment losses on tangible assets such as property, plant and equipment, as well as intangible assets such as goodwill, customer relationships or intellectual property.

Increases in the cost of energy and raw materials and/or disruption in the supply of these materials could result in lost sales or reduced profitability.

Energy is the single largest cost item in the production and distribution of industrial gases. Most of Linde’s energy requirements are in the form of electricity, natural gas and diesel fuel for distribution. Linde attempts to minimize the financial impact of variability in these costs through the management of customer contracts and reducing demand through operational productivity and energy efficiency. Large customer contracts typically have escalation and pass-through clauses to recover energy and feedstock costs. Such attempts may not successfully mitigate cost variability, which could negatively impact Linde’s financial condition or results of operations. The supply of energy has not been a significant issue in the geographic areas where Linde conducts business. However, regional energy conditions are unpredictable and may pose future risk.

For carbon dioxide, carbon monoxide, helium, hydrogen, specialty gases and surface technologies, raw materials are largely purchased from outside sources. Where feasible, Linde sources several of these raw materials, including carbon dioxide, hydrogen and calcium carbide, as chemical or industrial byproducts. In addition, Linde has contracts or commitments for, or readily available sources of, most of these raw materials; however, their long-term availability and prices are subject to market conditions. A disruption in supply of such raw materials could impact Linde’s ability to meet contractual supply commitments.

Linde’s international operations are subject to the risks of doing business abroad and international events and circumstances may adversely impact its business, financial condition or results of operations.

Linde has substantial international operations which are subject to risks including devaluations in currency exchange rates, transportation delays and interruptions, political and economic instability and disruptions, restrictions on the transfer of funds, trade conflicts and the imposition of duties and tariffs, import and export controls, changes in governmental policies, labor unrest, possible nationalization and/or expropriation of assets, domestic and international tax laws and compliance with governmental regulations. These events could have an adverse effect on the international operations of Linde in the future by reducing the demand for its products, decreasing the prices at which it can sell its products, reducing the revenue from international operations or otherwise having an adverse effect on its business. For example, Linde has a meaningful presence in the U.K. and the U.K.’s ongoing exit process from the EU has continued to cause, and may in the future cause, political and economic uncertainty, which could have an adverse impact on the markets which Linde supplies.

Currency exchange rate fluctuations and other related risks may adversely affect Linde's results.

Because a significant portion of Linde's revenue is denominated in currencies other than its reporting currency, the U.S. dollar, changes in exchange rates will produce fluctuations in revenue, costs and earnings and may also affect the book value of assets and liabilities and related equity. Although the company from time to time utilizes foreign exchange forward contracts to hedge these exposures, its efforts to minimize currency exposure through such hedging transactions may not be successful depending on market and business conditions. As a result, fluctuations in foreign currency exchange rates could adversely affect Linde’s financial condition, results of operations or cash flows.

Macroeconomic factors may impact Linde’s ability to obtain financing or increase the cost of obtaining financing which may adversely impact Linde’s financial results and/or cash flows.

Volatility and disruption in the U.S., European and global credit and equity markets, from time to time, could make it more difficult for Linde to obtain financing for its operations and/or could increase the cost of obtaining financing. In addition, Linde’s borrowing costs can be affected by short- and long-term debt ratings assigned by independent rating agencies which are based, in significant part, on its performance as measured by certain criteria such as interest coverage and leverage ratios. A decrease in these debt ratings could increase the cost of borrowing or make it more difficult to obtain financing.

10

An impairment of goodwill or intangible assets could negatively impact the company's financial results.

As of December 31, 2019, the net carrying value of goodwill and other indefinite-lived intangible assets was $27 billion and $2 billion, respectively, primarily as a result of the business combination and the related acquisition method of accounting applied to Linde AG. In accordance with generally accepted accounting principles, the company periodically assesses these assets to determine if they are impaired. Significant negative industry or economic trends, disruptions to business, unexpected significant changes or planned changes in use of the assets, divestitures and sustained market capitalization declines may result in recognition of impairments to goodwill or other indefinite-lived assets. Any charges relating to such impairments could have a material adverse impact on Linde's results of operations in the periods recognized.

Catastrophic events could disrupt the operations of Linde and/or its customers and suppliers and may have a significant adverse impact on the results of operations.

The occurrence of catastrophic events or natural disasters such as extreme weather, including hurricanes and floods; health epidemics; and acts of war or terrorism, could disrupt or delay Linde’s ability to produce and distribute its products to customers and could potentially expose Linde to third-party liability claims. In addition, such events could impact Linde’s customers and suppliers resulting in temporary or long-term outages and/or the limitation of supply of energy and other raw materials used in normal business operations. Linde evaluates the direct and indirect business risks, consults with vendors, insurance providers and industry experts, makes investments in suitably resilient design and technology, and conducts regular reviews of the business risks with management. Despite these steps, however, these situations are outside Linde’s control and may have a significant adverse impact on its financial results.

The inability to attract and retain qualified personnel may adversely impact Linde’s business.

If Linde fails to attract, hire and retain qualified personnel, it may not be able to develop, market or sell its products or successfully manage its business. Linde is dependent upon a highly skilled, experienced and efficient workforce to be successful. Much of Linde’s competitive advantage is based on the expertise and experience of key personnel regarding marketing, technology, manufacturing and distribution infrastructure, systems and products. The inability to attract and hire qualified individuals or the loss of key employees in very skilled areas could have a negative effect on Linde’s financial results.

If Linde fails to keep pace with technological advances in the industry or if new technology initiatives do not become commercially accepted, customers may not continue to buy Linde’s products and results of operations could be adversely affected.

Linde’s research and development is directed toward developing new and improved methods for the production and distribution of industrial gases, the design and construction of plants and toward developing new markets and applications for the use of industrial and process gases. This results in the introduction of new applications and the development of new advanced air separation process technologies. As a result of these efforts, Linde develops new and proprietary technologies and employs necessary measures to protect such technologies within the global geographies in which Linde operates. These technologies help Linde to create a competitive advantage and to provide a platform to grow its business. If Linde’s research and development activities do not keep pace with competitors or if Linde does not create new technologies that benefit customers, future results of operations could be adversely affected.

Risks related to pension benefit plans may adversely impact Linde’s results of operations and cash flows.

Pension benefits represent significant financial obligations that will be ultimately settled in the future with employees who meet eligibility requirements. Because of the uncertainties involved in estimating the timing and amount of future payments and asset returns, significant estimates are required to calculate pension expense and liabilities related to Linde’s plans. Linde utilizes the services of independent actuaries, whose models are used to facilitate these calculations. Several key assumptions are used in the actuarial models to calculate pension expense and liability amounts recorded in the consolidated financial statements. In particular, significant changes in actual investment returns on pension assets, discount rates, or legislative or regulatory changes could impact future results of operations and required pension contributions.

11

Operational risks may adversely impact Linde’s business or results of operations.

Linde’s operating results are dependent on the continued operation of its production facilities and its ability to meet customer contract requirements and other needs. Insufficient or excess capacity threatens Linde’s ability to generate competitive profit margins and may expose Linde to liabilities related to contract commitments. Operating results are also dependent on Linde’s ability to complete new construction projects on time, on budget and in accordance with performance requirements. Failure to do so may expose Linde’s business to loss of revenue, potential litigation and loss of business reputation.

Also inherent in the management of Linde’s production facilities and delivery systems, including storage, vehicle transportation and pipelines, are operational risks that require continuous training, oversight and control. Material operating failures at production, storage facilities or pipelines, including fire, toxic release and explosions, or the occurrence of vehicle transportation accidents could result in loss of life, damage to the environment, loss of production and/or extensive property damage, all of which may negatively impact Linde’s financial results.

Linde may be subject to information technology system failures, network disruptions and breaches in data security.

Linde relies on information technology systems and networks for business and operational activities, and also stores and processes sensitive business and proprietary information in these systems and networks. These systems are susceptible to outages due to fire, flood, power loss, telecommunications failures, viruses, break-ins and similar events, or breaches of security.

Linde has taken steps to address these risks and concerns by implementing advanced security technologies, internal controls, network and data center resiliency and recovery process. Despite these steps, however, operational failures and breaches of security from increasingly sophisticated cyber threats could lead to the loss or disclosure of confidential information, result in business interruption or malfunction or regulatory actions and have a material adverse impact on Linde’s operations, reputation and financial results.

The inability to effectively integrate acquisitions or collaborate with joint venture partners could adversely impact Linde’s financial position and results of operations.

In addition to the business combination, Linde has evaluated and expects to continue to evaluate, a wide array of potential strategic acquisitions and joint ventures. Many of these transactions, if consummated, could be material to its financial condition and results of operations. In addition, the process of integrating an acquired company, business or group of assets may create unforeseen operating difficulties and expenditures. Although historically Linde has been successful with its acquisition strategy and execution, the areas where Linde may face risks include:

• | the need to implement or remediate controls, procedures and policies appropriate for a larger public company at companies that prior to the acquisition lacked these controls, procedures and policies; |

• | diversion of management time and focus from operating existing business to acquisition integration challenges; |

• | cultural challenges associated with integrating employees from the acquired company into the existing organization; |

• | the need to integrate each company’s accounting, management information, human resources and other administrative systems to permit effective management; |

• | difficulty with the assimilation of acquired operations and products; |

• | failure to achieve targeted synergies and cost reductions; and |

• | inability to retain key employees and business relationships of acquired companies. |

Foreign acquisitions and joint ventures involve unique risks in addition to those mentioned herein, including those related to integration of operations across different cultures and languages, currency risks and the particular economic, political and regulatory risks associated with specific countries.

Also, the anticipated benefit of potential future acquisitions may not materialize. Future acquisitions or dispositions could result in the incurrence of debt, contingent liabilities or amortization expenses, or impairments of goodwill, any of which could adversely impact Linde’s financial results.

12

Linde is subject to a variety of international laws and government regulations and changes in, or failure to comply with, these laws or regulations could have an adverse impact on the company’s business, financial position and results of operations.

Linde is subject to regulations in the following areas, among others:

• | environmental protection, including climate change and energy efficiency laws and policies; |

• | domestic and international tax laws and currency controls; |

• | safety; |

• | securities laws applicable in the United States, the European Union, Germany, Ireland, and other jurisdictions; |

• | trade and import/export restrictions, as well as economic sanctions laws; |

• | antitrust matters; |

• | data protection; |

• | global anti-bribery laws, including the U.S. Foreign Corrupt Practices Act; and |

• | healthcare regulations. |

Changes in these or other regulatory areas, such as evolving environmental legislation in China, may impact Linde’s profitability and may give rise to new or increased compliance risks: it may become more complex and costly to ensure compliance, and the level of sanctions in the event of non-compliance may rise. Such changes may also restrict Linde’s ability to compete effectively in the marketplace. Noncompliance with such laws and regulations could result in penalties or sanctions, cancellation of marketing rights or restrictions on participation in, or even exclusion from, public tender proceedings, all of which could have a material adverse impact on Linde’s financial results and/or reputation.

Doing business globally requires Linde to comply with anti-corruption, trade, compliance and economic sanctions and similar laws, and to implement policies and procedures designed to ensure that its employees and other intermediaries comply with the applicable restrictions. These restrictions include prohibitions on the sale or supply of certain products, services and any other economic resources to embargoed or sanctioned countries, governments, persons and entities. Compliance with these restrictions requires, among other things, screening of business partners. Despite its commitment to legal compliance and corporate ethics, the company cannot ensure that its policies and procedures will always protect it from intentional, reckless or negligent acts committed by employees or agents under the applicable laws. If Linde fails to comply with laws governing the conduct of international operations, Linde may be subject to criminal and civil penalties and other remedial measures, which could materially adversely affect its reputation, business and results of operations.

The outcome of litigation or governmental investigations may adversely impact the company’s business or results of operations.

Linde’s subsidiaries are party to various lawsuits and governmental investigations arising in the ordinary course of business. Adverse outcomes in some or all of the claims pending may result in significant monetary damages or injunctive relief that could adversely affect Linde’s ability to conduct business. Linde and its subsidiaries may in the future become subject to further claims and litigation, which is impossible to predict. The litigation and other claims Linde faces are subject to inherent uncertainties. Legal or regulatory judgments or agreed settlements might give rise to expenses which are not covered, or are not fully covered, by insurance benefits and may also lead to negative publicity and reputational damage. An unfavorable outcome or determination could cause a material adverse impact on the company’s results of operations.

Potential product defects or inadequate customer care may adversely impact Linde’s business or results of operations.

Risks associated with products and services may result in potential liability claims, the loss of customers or damage to Linde’s reputation. Principal possible causes of risks associated with products and services are product defects or an inadequate level of customer care when Linde is providing services.

Linde is exposed to legal risks relating to product liability in the countries where it operates, including countries such as the United States, where legal risks (in particular through class actions) have historically been more significant than in other countries. The outcome of any pending or future products and services proceedings or investigations cannot be predicted and legal or regulatory judgments or agreed settlements may give rise to significant losses, costs and expenses.

The manufacturing and sale of products as well as the construction of plants by Linde may give rise to risks associated with the production, filling, storage, handling and transport of raw materials, goods or waste. Industrial gases are

13

potentially hazardous substances and medical gases and the related healthcare services must comply with the relevant specifications in order to not adversely affect the health of patients treated with them.

Linde’s products and services, if defective or not handled or performed appropriately, may lead to personal injuries, business interruptions, environmental damages or other significant damages, which may result, among other consequences, in liability, losses, monetary penalties or compensation payments, environmental clean-up costs or other costs and expenses, exclusion from certain market sectors deemed important for future development of the business and loss of reputation. All these consequences could have a material adverse effect on Linde’s business and results of operations.

U.S. civil liabilities may not be enforceable against Linde.

Linde is organized under the laws of Ireland and substantial portions of its assets will be located outside of the United States. In addition, certain directors and officers of Linde and its subsidiaries reside outside the United States. As a result, it may be difficult for investors to effect service of process within the United States upon Linde or such persons, or to enforce outside the United States judgments obtained against such persons in U.S. courts in any action, including actions predicated upon the civil liability provisions of the U.S. federal securities laws. In addition, it may be difficult for investors to enforce, in original actions brought in courts in jurisdictions located outside the United States, rights predicated upon the U.S. federal securities laws.

A judgment for the payment of money rendered by a court in the United States based on civil liability would not be automatically enforceable in Ireland. There is no treaty between Ireland and the United States providing for the reciprocal enforcement of foreign judgments. The following requirements must be met before the foreign judgment will be deemed to be enforceable in Ireland (i) the judgment must be for a definite sum, (ii) the judgment must be final and conclusive; and (iii) the judgment must be provided by a court of competent jurisdiction.

An Irish court will also exercise its right to refuse judgment if the foreign judgment (i) was obtained by fraud; (ii) violated Irish public policy; (iii) is in breach of natural justice; or (iv) if the judgment is irreconcilable with an earlier foreign judgment.

In addition, there is doubt as to whether an Irish court would accept jurisdiction and impose civil liability on Linde or such persons in an original action predicated solely upon the U.S. federal securities laws brought in a court of competent jurisdiction in Ireland against Linde or such member, officer or expert, respectively.

Changes in tax laws or policy could adversely impact the company’s financial position or results of operations.

Linde and its subsidiaries are subject to the tax rules and regulations in the U.S., Germany, Ireland, the U.K. and other countries in which they operate. Those tax rules and regulations are subject to change on a prospective or retroactive basis. Under current economic and political conditions, including the U.K.’s ongoing exit process from the EU, tax rates and policies in any jurisdiction, including the U.S., the U.K. and the EU, are subject to significant change. In particular, since Linde is currently treated as U.K. tax resident, any potential changes in the tax rules applying to U.K. tax-resident companies would directly affect Linde.

A change in Linde’s tax residency could have a negative effect on the company’s future profitability and may trigger taxes on dividends or exit charges. If Linde ceases to be resident in the United Kingdom and becomes resident in another jurisdiction, it may be subject to United Kingdom exit charges, and/or could become liable for additional tax charges in the other jurisdiction. If Linde were to be treated as resident in more than one jurisdiction, it could be subject to duplicative taxation. Furthermore, although Linde is incorporated in Ireland and is not expected to be treated as a domestic corporation for U.S. federal income tax purposes, it is possible that the IRS could disagree with this result or that changes in U.S. federal income tax law could alter this result. If the IRS successfully asserted such a position or the law were to change, significant adverse tax consequences may result for Linde, the company and Linde’s shareholders.

When tax rules change, this may result in a higher tax expense and the need to make higher tax payments. In addition, changes in tax legislation may have a significant impact on Linde’s and its subsidiaries’ tax receivables and tax liabilities as well as on their deferred tax assets and deferred tax liabilities and uncertainty about the tax environment in some regions may restrict their opportunities to enforce their respective rights under the law. Linde also operates in countries with complex tax regulations which could be interpreted in different ways. Interpretations of these regulations or changes in the tax system might have an adverse impact on the tax liabilities, profitability and business operations of

14

Linde. Linde and its subsidiaries are subject to periodic audits by the tax authorities in various jurisdictions or other review actions by the relevant financial or tax authorities. The ultimate tax outcome may differ from the amounts recorded in Linde’s or its subsidiaries’ financial statements and may materially affect their respective financial results for the period when such determination is made.

15

ITEM 1B. UNRESOLVED STAFF COMMENTS

Linde has received no written SEC staff comments regarding any of its Exchange Act reports which remain unresolved.

ITEM 2. PROPERTIES

Linde plc's principal executive offices are located in owned office space in Guildford, United Kingdom. Linde also owns principal administrative office space in Danbury, Connecticut and Houston, Texas, United States; Pullach, Germany; and Singapore.

Due to the nature of Linde’s industrial gas products, it is generally uneconomical to transport them distances greater than a few hundred miles from the production facility. As a result, Linde operates a significant number of production facilities spread globally throughout a number of geographic regions.

The following is a description of production facilities for Linde by segment. No significant portion of these assets was leased at December 31, 2019. Generally, these facilities are fully utilized and are sufficient to meet the company's manufacturing needs.

Americas

The Americas segment operates production facilities primarily in the U.S., Canada, Mexico and Brazil, approximately 350 of which are mainly cryogenic air separation plants, hydrogen plants and carbon dioxide plants. There are five major pipeline complexes in North America located in northern Indiana, Houston, along the Gulf Coast of Texas, Detroit and Louisiana. Many of the South American plants support one pipeline complex in Southern Brazil. Also located throughout the Americas are noncryogenic air separation plants, packaged gas facilities and other smaller plant facilities.

EMEA

The EMEA segment has production facilities primarily in Italy, Spain, Germany, the Benelux region, the United Kingdom, Scandinavia and Russia which include approximately 230 cryogenic air separation plants and carbon dioxide plants. Also located throughout Europe are noncryogenic air separation plants, packaged gas facilities and other smaller plant facilities.

APAC

The APAC segment has production facilities located primarily in China, Korea, India and Thailand, approximately 230 of which are cryogenic air separation plants and carbon dioxide plants. Also located throughout Asia are noncryogenic air separation plants, hydrogen, packaged gas and other production facilities.

Engineering

The Linde Engineering business designs and constructs turnkey process plants for third-party customers as well as for the Linde gases businesses in many locations worldwide, such as olefin plants, natural gas plants, air separation plants, hydrogen and synthesis gas plants. Plant components are produced in owned factories in Pullach and Tacherting, Germany; Hesinque, France; Oklahoma, United States; and Dalian, China.

ITEM 3. LEGAL PROCEEDINGS

Information required by this item is incorporated herein by reference to the section captioned “Notes to Consolidated Financial Statements – 19. Commitments and Contingencies” in Item 8 of this 10-K.

ITEM 4. MINE SAFETY DISCLOSURES

Not Applicable

16

PART II

ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Linde plc shares trade on the New York Stock Exchange (“NYSE”) and the Frankfurt Stock Exchange (“FSE”) under the ticker symbol “LIN”. At December 31, 2019 there were 9,322 shareholders of record.

Purchases of Equity Securities – Certain information regarding purchases made by or on behalf of the company or any affiliated purchaser (as defined in Rule 10b-18(a)(3) under the Securities Exchange Act of 1934, as amended) of its ordinary shares during the three months ended December 31, 2019 is provided below:

Period | Total Number of Shares Purchased (Thousands) | Average Price Paid Per Share | Total Number of Shares Purchased as Part of Publicly Announced Program (1) (Thousands) | Approximate Dollar Value of Shares that May Yet be Purchased Under the Program (2) (Millions) | |||||||||

October 2019 | 716 | $ | 191.19 | 716 | $ | 4,322 | |||||||

November 2019 | 1,039 | $ | 205.74 | 1,039 | $ | 4,108 | |||||||

December 2019 | 1,896 | $ | 207.31 | 1,896 | $ | 3,715 | |||||||

Fourth Quarter 2019 | 3,651 | $ | 203.70 | 3,651 | $ | 3,715 | |||||||

________________________

(1) | On January 22, 2019 the company’s board of directors approved the repurchase of $6.0 billion of its ordinary shares ("2019 program") which could take place from time to time on the open market (and could include the use of 10b5-1 trading plans), subject to market and business conditions. The 2019 program has a maximum repurchase amount of 15% of outstanding shares and a stated expiration date of February 1, 2021. |

(2) | As of December 31, 2019, the company repurchased $2.3 billion of its ordinary shares pursuant to the 2019 program, leaving an additional $3.7 billion authorized. |

17

Peer Performance Table – The graph below compares the most recent five-year cumulative returns of the common stock of Praxair, the company's predecessor, through October 31, 2018 and Linde's ordinary shares from October 31, 2018 through December 31, 2019 with those of the Standard & Poor’s 500 Index ("SPX") and the S5 Materials Index ("S5MATR") which covers 22 companies, including Linde. The figures assume an initial investment of $100 on December 31, 2014 and that all dividends have been reinvested.

2014 | 2015 | 2016 | 2017 | 2018 | 2019 | |

LIN | $100 | $79 | $90 | $119 | $120 | $164 |

SPX | $100 | $99 | $109 | $130 | $122 | $157 |

S5MATR | $100 | $90 | $102 | $124 | $104 | $126 |

18

ITEM 6. SELECTED FINANCIAL DATA

FIVE-YEAR FINANCIAL SUMMARY

(Dollar amounts in millions, except per share data)

The year ended December 31, 2019 reflects the results of both Praxair and Linde AG for the entire year. The year ended December 31, 2018 reflects the results of Praxair for the entire year and the results of Linde AG for the period beginning after October 31, 2018 (the merger date), including the impacts of purchase accounting (See Notes 1, 3 and 4 to the consolidated financial statements). The historical periods prior to 2018 reflect the results of Praxair.

Year Ended December 31, | 2019(a) | 2018(a) | 2017(a) | 2016(a) | 2015(a) | ||||||||||||||

From the Consolidated Statements of Income | |||||||||||||||||||

Sales | $ | 28,228 | $ | 14,836 | $ | 11,358 | $ | 10,469 | $ | 10,710 | |||||||||

Cost of sales, exclusive of depreciation and amortization | 16,644 | 9,020 | 6,382 | 5,790 | 5,852 | ||||||||||||||

Selling, general and administrative | 3,457 | 1,629 | 1,207 | 1,145 | 1,152 | ||||||||||||||

Depreciation and amortization | 4,675 | 1,830 | 1,184 | 1,122 | 1,106 | ||||||||||||||

Research and development | 184 | 113 | 93 | 92 | 93 | ||||||||||||||

Cost reduction programs and other charges | 567 | 309 | 52 | 96 | 165 | ||||||||||||||

Net gain on sale of businesses | 164 | 3,294 | — | — | — | ||||||||||||||

Other income (expenses) – net | 68 | 18 | 4 | 23 | 28 | ||||||||||||||

Operating profit | 2,933 | 5,247 | 2,444 | 2,247 | 2,370 | ||||||||||||||

Interest expense – net | 38 | 202 | 161 | 190 | 161 | ||||||||||||||

Net pension and OPEB cost (benefit), excluding service cost | (32 | ) | (4 | ) | (4 | ) | 9 | 49 | |||||||||||

Income from continuing operations before income taxes and equity investments | 2,927 | 5,049 | 2,287 | 2,048 | 2,160 | ||||||||||||||

Income taxes on continuing operations | 769 | 817 | 1,026 | 551 | 612 | ||||||||||||||

Income from continuing operations before equity investments | 2,158 | 4,232 | 1,261 | 1,497 | 1,548 | ||||||||||||||

Income from equity investments | 114 | 56 | 47 | 41 | 43 | ||||||||||||||

Income from continuing operations (including noncontrolling interests) | 2,272 | 4,288 | 1,308 | 1,538 | 1,591 | ||||||||||||||

Noncontrolling interests from continuing operations | (89 | ) | (15 | ) | (61 | ) | (38 | ) | (44 | ) | |||||||||

Income from continuing operations | $ | 2,183 | $ | 4,273 | $ | 1,247 | $ | 1,500 | $ | 1,547 | |||||||||

Per Share Data – Linde plc Shareholders | |||||||||||||||||||

Basic earnings per share from continuing operations | $ | 4.03 | $ | 12.93 | $ | 4.36 | $ | 5.25 | $ | 5.39 | |||||||||

Diluted earnings per share from continuing operations | $ | 4.00 | $ | 12.79 | $ | 4.32 | $ | 5.21 | $ | 5.35 | |||||||||

Cash dividends per share | $ | 3.50 | $ | 3.30 | $ | 3.15 | $ | 3.00 | $ | 2.86 | |||||||||

Weighted Average Shares Outstanding (000’s) (b) | |||||||||||||||||||

Basic shares outstanding | 541,094 | 330,401 | 286,261 | 285,677 | 287,005 | ||||||||||||||

Diluted shares outstanding | 545,170 | 334,127 | 289,114 | 287,757 | 289,055 | ||||||||||||||

Other Information and Ratios | |||||||||||||||||||

Total assets | $ | 86,612 | $ | 93,386 | $ | 20,436 | $ | 19,332 | $ | 18,319 | |||||||||

Total debt | $ | 13,956 | $ | 15,296 | $ | 9,000 | $ | 9,515 | $ | 9,231 | |||||||||

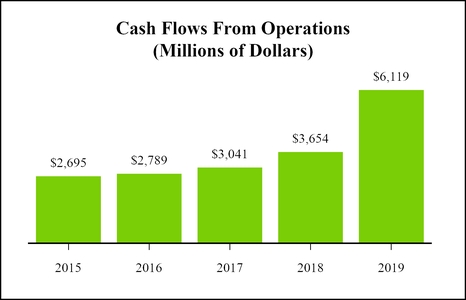

Cash flow from operations | $ | 6,119 | $ | 3,654 | $ | 3,041 | $ | 2,789 | $ | 2,695 | |||||||||

Net cash provided by (used for) investing activities | $ | 1,189 | $ | 5,363 | $ | (1,314 | ) | $ | (1,770 | ) | $ | (1,303 | ) | ||||||

Net cash used for financing activities | $ | (8,997 | ) | $ | (4,998 | ) | $ | (1,656 | ) | $ | (659 | ) | $ | (1,310 | ) | ||||

Capital expenditures | $ | 3,682 | $ | 1,883 | $ | 1,311 | $ | 1,465 | $ | 1,541 | |||||||||

Shares outstanding (000’s) | 534,381 | 547,242 | 286,777 | 284,901 | 284,879 | ||||||||||||||

Number of employees | 79,886 | 80,820 | 26,461 | 26,498 | 26,657 | ||||||||||||||

(a) | Amounts for 2019 include: (i) charges of $567 million for cost reduction programs and other charges primarily related to the merger and synergies, (ii) pension settlement charges of $97 million related to lump sum benefit payments made from pension plans, (iii) a net gain on sale of businesses of $164 million and (iv) the purchase accounting impacts of the merger of $1,952 million. |

19

Amounts for 2018 include: (i) charges of $309 million for transaction costs and other charges primarily related to the merger, (ii) pension settlement charges of $14 million related to lump sum benefit payments made from pension plans, (iii) income tax benefit, net of $17 million due to U.S. Tax Cuts and Jobs Act and other tax charges, (iv) a net gain on sale of businesses of $3,294 million, (v) bond redemption costs of $26 million, and (vi) the purchase accounting impacts of the merger of $714 million.

Amounts for 2017 include: (i) charges of $52 million for transaction costs related to the merger, (ii) a pension settlement charge of $2 million related to lump sum benefit payments made from an international pension plan, and (iii) income tax charges, net of $394 million due to U.S. Tax Cuts and Jobs Act.

Amounts for 2016 include: (i) a $16 million charge to interest expense related to the redemption of the $325 million 5.20% notes due 2017, (ii) a pre–tax pension settlement charge of $4 million related to lump sum benefit payments made from the U.S. supplemental pension plan, and (iii) pre–tax charges of $96 million primarily related to cost reduction actions.

Amounts for 2015 include: (i) a pre-tax charge of $165 million related to the cost reduction program and other charges; and (ii) a pre-tax charge of $7 million related to a pension settlement.

See Notes 1, 3, 4, 5, 7, 13 and 18 to the consolidated financial statements.

(b) As a result of the merger, share amounts for the year ended December 31, 2018 reflect the weighted averaging effect of Praxair shares outstanding prior to October 31, 2018 and Linde shares outstanding from October 31, 2018 through December 31, 2018.

20

ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

The following discussion of the company’s financial condition and results of operations should be read together with its consolidated financial statements and notes to the consolidated financial statements included in Item 8 of this Form 10-K.

Page | |

Merger of Praxair, Inc. and Linde AG | |

Business Overview | |

Executive Summary – Financial Results & Outlook | |

Consolidated Results and Other Information | |

Segment Discussion | |

Liquidity, Capital Resources and Other Financial Data | |

Contractual Obligations | |

Off-Balance Sheet Arrangements | |

Critical Accounting Policies | |

New Accounting Standards | |

Fair Value Measurements | |

Supplemental Pro Forma Income Statement Information | |

Non-GAAP Financial Measures | |

MERGER OF PRAXAIR, INC. AND LINDE AG

Linde plc ("Linde") is a public limited company formed under the laws of Ireland in 2017 in accordance with the requirements of the business combination agreement between Praxair, Inc. ("Praxair") and Linde Aktiengesellschaft ("Linde AG"). On October 31, 2018 Praxair and Linde AG combined their respective businesses through an all-stock transaction, and became subsidiaries of Linde plc (collectively referred to as the “business combination” or "merger"). The business combination of Praxair and Linde AG has been accounted for using the acquisition method of accounting under the provisions of Financial Accounting Standards Board (“FASB”) Accounting Standards Codification 805, “Business Combinations,” with Praxair representing the accounting acquirer under this guidance. Accordingly, the historical financial statements of Praxair for the periods prior to the merger are considered to be the historical financial statements of Linde. The results of Linde AG are included in Linde’s consolidated results from the merger date forward. The Linde shares trade on the New York Stock Exchange and the Frankfurt Stock Exchange under the ticker symbol “LIN”. See Notes 1 and 3 to the consolidated financial statements for additional information.

In connection with the business combination, the company, Praxair and Linde AG, entered into various agreements with regulatory authorities to satisfy anti-trust requirements to secure approval to consummate the business combination. These agreements required the sale of the majority of Praxair’s European businesses (completed on December 3, 2018), a significant portion of Linde AG’s Americas business (completed on March 1, 2019), select assets of Linde AG's South Korean industrial gases business (completed April 30, 2019), select assets of Praxair's Indian industrial gases business (completed July 12, 2019), select assets of Linde AG's Indian industrial gases business (completed December 16, 2019) as well as certain divestitures of other Praxair and Linde AG businesses in Asia that are currently expected to be sold in 2020 (collectively, the “merger-related divestitures”). In the consolidated financial statements included in Item 8, Praxair’s merger-related divestitures are included in the results of operations until sold and Linde AG’s merger-related divestitures are accounted for as discontinued operations. See Notes 1, 3 and 4 to the consolidated financial statements included in Item 8 for additional information relating to merger-related divestitures.

Additionally, to obtain merger approval in the United States Linde, Praxair and Linde AG entered into an agreement with the U.S. Federal Trade Commission dated October 1, 2018 (“hold separate order” or “HSO”). Under the HSO, the company, Praxair and Linde AG agreed to continue to operate Linde AG and Praxair as independent, ongoing, economically viable, competitive businesses held separate, distinct, and apart from each other’s operations; and not coordinate any aspect of their operations until certain divestitures in the United States were completed. Accordingly, Linde had accounted for Linde AG as a separate segment for 2018 reporting purposes effective with the merger date. Prior to the merger date, the company’s Linde AG segment did not exist. Since the FTC hold separate order restrictions were lifted effective March 1, 2019, the company subsequently implemented a new segment structure as follows: Americas; EMEA

21

(Europe/Middle East/Africa); APAC (Asia/South Pacific) and Engineering. This new management organization structure was implemented during the first quarter 2019 and, accordingly, segment information has been retrospectively recast for all prior periods.

ITEMS AFFECTING COMPARABILITY

Because Praxair and Linde AG combined their respective businesses effective with the merger date of October 31, 2018, the year ended December 31, 2019 reflects the results and cash flows of the combined business, while the year ended December 31, 2018 includes twelve months of Praxair and two months of Linde AG. Due to the size of Linde AG’s businesses prior to the merger, the reported results for 2019 and 2018 periods are not comparable. The balance sheets at December 31, 2019 and December 31, 2018 are comparable because both periods reflect the merger.

Pro Forma Income Statement Information

Therefore, to assist with a discussion of the 2019 and 2018 results on a comparable basis, certain supplemental unaudited pro forma income statement information is provided on both a consolidated and segment basis (referred to as "pro forma income statement information" or "pro forma information").