NITCHES INC - Annual Report: 2007 (Form 10-K)

SECURITIES AND EXCHANGE

COMMISSION

Washington, D.C. 20549

Form 10-K

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||

| For the fiscal year ended August 31, 2007 | |||

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||

| For the transition period from ______ to______. |

| Commission File Number 0-13851 |

| NITCHES, INC. |

| (Exact name of registrant as specified in its charter) |

| California | 95-2848021 |

| (State of Incorporation) | (I.R.S. Employer Identification No.) |

| 10280 Camino Santa Fe | |

| San Diego, California | 92121 |

| (Address of principal executive offices) | (Zip Code) |

Registrant's telephone number: (858) 625-2633

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered |

| Common Stock, no par value | NASDAQ Capital Market |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of "accelerated filer and large accelerated filer" in Rule 12b-2 of the Act. (Check one):

| Large Accelerated Filer o | Accelerated Filer o | Non-Accelerated Filer x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [ ] No [X]

As of November 30, 2007, 5,659,644 shares of the Registrant’s common stock were outstanding.

The aggregate market value of all equity securities held by non-affiliates of the registrant as of the last business day of the most recently completed second fiscal quarter (February 28, 2007) based on the closing price of the registrant’s stock in the NASDAQ Capital Market on that date was $28,316,403.

| TABLE OF CONTENTS | |||

| PART I | 3 | ||

| Item 1. BUSINESS | 3 | ||

| Item 1A. RISK FACTORS | 8 | ||

| Item 1B. UNRESOLVED STAFF COMMENTS | 13 | ||

| Item 2. PROPERTIES | 13 | ||

| Item 3. LEGAL PROCEEDINGS | 13 | ||

| Item 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS | 13 | ||

| PART II | 14 | ||

| Item 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES | 14 | ||

| Item 6. SELECTED FINANCIAL DATA | 16 | ||

| Item 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATION | 17 | ||

| Item 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 23 | ||

| Item 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA | 24 | ||

| Item 9. CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE | 43 | ||

| Item 9A. CONTROLS AND PROCEDURES | 43 | ||

| Item 9B. OTHER INFORMATION | 43 | ||

| PART III | 44 | ||

| Item 10. DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE | 44 | ||

| Item 11. EXECUTIVE COMPENSATION | 45 | ||

| Item 12. SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS | 51 | ||

| Item 13. CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE | 52 | ||

| Item 14. PRINCIPAL ACCOUNTING FEES AND SERVICES | 52 | ||

| PART IV | 53 | ||

| Item 15. EXHIBITS AND FINANCIAL STATEMENT SCHEDULES | 53 | ||

| SIGNATURES | 54 | ||

| EXHIBIT INDEX | 57 | ||

2

PART I

Item 1 - Business

Cautionary Statement Under the Private Securities Litigation Reform Act of 1995

Statements in this annual report on Form 10-K including statements under the caption "Business", as well as oral statements that may be made by the Company or by officers, directors or employees of the Company acting on the Company's behalf, that are not historical fact constitute "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements involve known and unknown risks and uncertainties that may cause the Company's actual results in future periods to differ materially from forecasted results. You can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expects,” “intends,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” “potential,” “continues” or the negative of these terms or other comparable terminology. These risks and other factors include those listed under “Risk Factors” and elsewhere in this report. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. You should not place undue reliance on any forward-looking statements as they reflect our management’s view only as of the date of this report. We will not update any forward-looking statements to reflect events or circumstances that occur after the date on which such statement is made.

General

Nitches, Inc. and subsidiaries ("we," "our," "us," or the "Company") is a wholesale importer and distributor of clothing and home décor products manufactured to our specifications and distributed in the United States under our brand labels and retailer-owned private labels. We distribute clothing primarily in three categories: women's sleepwear and loungewear, women's sportswear and outerwear, and men's casual wear and performance apparel. We market women's sleepwear and loungewear under the following brands: Princesse tam tam®, Derek Rose®, Crabtree & Evelyn®, Disney Couture®, The Anne Lewin® Collection, The Claire Murray® Collection and Gossard®. We market women's sportswear and outerwear under the following brands: Adobe Rose®, Country Tease®, Saguaro® and Southwest Canyon®. We market men's casual wear and performance apparel under the following brands: Nat Nast®, Newport Blue®, Dockers®, The Skins Game®, and ZOIC®. We distribute home décor products under the Bill Blass® and Newport Blue® brands. We sell our branded products to better department stores, specialty boutiques, moderate department stores, and national and regional discount department stores and chains. We also develop and manufacture private label products for many leading retailers and catalogs. The Company provides fashionable clothing to the popularly priced market segment that generally retails between $10 and $35 per item. For 35 years the Company has competed on the basis of price, quality, the desirability of its fabrics and designs, and the reliability of its delivery and service.

The apparel market continues to be marked by deflation and modest profit margins in many markets. The consolidation of retail stores among a small number of national chains has given these chains leverage to seek lower pricing and thereby reduce profit margins for suppliers such as the Company. In recent years, many vertical retailers who design, produce and sell their own product direct to consumers through physical stores, catalogs and the internet have emerged or expanded. Management has responded by developing products in categories that are underserved or where the Company retains an advantage in sources of supply, design or distribution. Management has also sought alliances and acquisitions as a means to increase sales to new and existing customers and improve margins by achieving operational efficiencies across a broader product portfolio.

Recent Developments

We have engaged in several recent business or asset acquisitions:

(1) On October 24, 2005, we acquired Designer Intimates, Inc., a New York City based importer and distributor of both branded and private label women's sleepwear, robes, loungewear, swimwear and intimate apparel; men's sleepwear, robes, and loungewear; and infant's and children's sleepwear and robes. The aggregate purchase price for the acquisition was $1,800,000, which we paid to the sellers with 180,000 restricted shares of our common stock at a value of $5.10 per share and 8,820 shares of our Series A preferred stock valued at $100 per share. With the Designer Intimates acquisition, we became a diversified supplier of women's intimate apparel at multiple levels of retail distribution. The purchase added significant revenues, further strengthened our product mix, and added to our portfolio of brands.

3

(2) On July 1, 2006 we acquired the home décor product line of Taresha LLC (“Taresha”). Home décor products include candles, candle holders and other home decorating accessories. We paid $2,730,000 in the form of 600,000 restricted shares of our common stock valued at $4.55 per share (based on the average closing price for our common stock for the ten trading days between June 7 and June 20, 2006, inclusive). Home décor products are sold under the Bill Blass® and Newport Blue® brands primarily to the same retailers to which we sell our apparel products. The purchase added new sources of revenue and diversified our product offerings to retailers beyond apparel.

(3) On October 24, 2006, we completed our acquisition of the Saguaro® mark and related trademarks from Impex Inc., a leading manufacturer of branded and non-branded specialty, western and private-label women's apparel. We paid consideration of $3,030,000 to Impex in the form of 600,000 restricted shares of our common stock valued at $4.55 per share (based on the average closing price for our common stock for the ten trading days between June 7 and June 20, 2006, inclusive) and a $300,000 promissory note. Since January 2005, we had been manufacturing and distributing Saguaro® apparel products to specialty and catalog retailers under the terms of a strategic alliance with Impex. Under this alliance, we recorded the revenue from such sales and remitted royalties and design fees to Impex as part of our operating expenses. As a result of this acquisition, we no longer pay royalties and design fees to Impex.

In addition, during the year ended August 31, 2007 we completed two financing transactions:

(1) On April 27, 2007, pursuant to the terms of a stock purchase agreement we issued to Sojitz Corporation, a Japanese corporation, 406,137 restricted shares of our common stock for $1.5 million. The number of shares of our common stock issued under the agreement was determined by (i) dividing $1.5 million by $3.88, which was the average of the closing prices of a share of our common stock on the NASDAQ Capital Market for the 10 trading days that immediately preceded the closing date, plus (ii) an additional number of shares determined by multiplying that number of shares calculated in (i) by 5%. Concurrently with the execution of the stock purchase agreement, we entered into a manufacturing agreement with Sojitz pursuant to which Sojitz agreed to manufacture products on our behalf.

(2) On June 21, 2007, we entered into a Securities Purchase Agreement with Birchten Investments, Ltd., an unaffiliated institutional investor, and Granite Financial Group, LLC, an unaffiliated investment bank, for the sale of 12.0% Subordinated Convertible Debentures and Common Stock Purchase Warrants. We refer to this transaction as our June 2007 Private Placement. In this transaction, we issued an aggregate of $3.15 million principal amount of debentures and warrants to purchase up to 577,500 shares of our common stock in exchange for net proceeds of $2.95 million, after deduction of fees and expenses. Interest on the debentures accrues at the rate of 12% per annum and is payable quarterly on February 28, May 31, August 31, and November 30, commencing on August 31, 2007. The debentures are due December 31, 2009. The warrants are exercisable at any time within five years from the date of issuance at an exercise price of $4.12 per share, subject to adjustment, including full-ratchet anti-dilution protection.

Furthermore, on June 1, 2007 we took possession of 76,000 square feet of warehouse space in Reno, Nevada under the terms of a 5 year lease. This facility is intended to primarily handle distribution of our sleepwear and home décor products as well as seasonal overflow of products historically shipped from our San Diego location. Our Reno warehouse replaced approximately 70,000 square feet of warehouse we had utilized in Bayonne, New Jersey through a service agreement with a third party logistics provider. Key logistics personnel from the third party operation were hired and relocated from Bayonne to Reno to form the nucleus of the permanent staff that manages and operates our Reno facility.

Product Development and Design

Our in-house design and merchandising staff develops high quality lines of clothing for each of our brands. Using computer-based design and illustration technology, designers create original garment bodies (styles) with unique fabric prints and designs. From time to time we also incorporate prints and concepts purchased from freelance artists and independent design services. The use of advanced design tools allows us to simulate a wide variety of product for development and presentation to retailers on printed storyboards and in catalogs. The time and expense of sample production is thereby avoided or reduced as merchandisers narrow and refine product lines.

4

We respond to frequent style changes in women's and men’s clothing by maintaining a program of evaluating current trends in style and fabric. In an effort to continually stay abreast of fashion trends, Company representatives shop at department and specialty stores in the United States, Europe, Japan and other countries that are known to sell merchandise with advanced styling direction. We may also seek input from selected customers and other industry resources. Design teams then select styles, fabrics, and colors that interpret current fashion trends for their respective product lines.

Retail store buyers may also provide specifications to us or may select for sale through their private label apparel programs styles from product lines our designers have developed. We then manufacture and import these goods which are generally sold under a label owned by or exclusive to a retailer. Retailers rely on our established reputation for arranging for foreign manufacture on a reliable, expeditious and cost-effective basis.

Sources of Supply

Over 96% of the garments we sell are manufactured abroad. Contracting with foreign manufacturers enables us to take advantage of prevailing lower labor rates, with the consequent ability to produce a quality garment that can be retailed in the popular, value and moderate price ranges. We arrange for the production of garments with suppliers on a purchase order basis, with each order generally backed by an irrevocable letter of credit. We do not have any long-term contractual commitments with manufacturers. This provides us with flexibility in the selection of manufacturers for future production of goods. We believe that we could replace the loss of any particular manufacturer in any country within a reasonable time period.

As a result of import restrictions on certain garments imposed by bilateral trade agreements between the United States and certain foreign countries, we have sought diversity in the number of countries in which we have manufacturing arrangements. The percentage of total purchases from particular countries varies from period to period based upon quota availability and price considerations. We have arranged, and will continue to arrange, for production in the United States when economically feasible to meet specific needs.

The following table shows the percentage of the Company's total purchases, not including freight charges, duties and commissions, from each country for the years ended August 31, 2007, 2006, and 2005.

| Percent of Total Purchases by Country | |||||

| Year ended August 31, | |||||

| 2007 | 2006 | 2005 | |||

| China | 56.2 | 22.7 | 2.7 | ||

| Pakistan | 10.3 | 7.8 | 16.4 | ||

| Hong Kong | 7.9 | 9.3 | 15.4 | ||

| Turkey | 6.3 | 13.3 | - | ||

| India | 5.3 | 9.7 | 16.7 | ||

| Macau | 4.2 | 13.7 | - | ||

| United States | 3.2 | 1.8 | 4.9 | ||

| Sri Lanka | 1.8 | 2.3 | 5.7 | ||

| Countries <1.0% each in the current year | 4.8 | 19.4 | 38.2 | ||

| 100.0 | 100.0 | 100.0 | |||

We own 100% of the outstanding capital stock of Nitches Far East Ltd., a Hong Kong corporation that performs production coordination, quality control and sample production services for the Company. Furthermore, we work with independent agents specializing in sourcing and production control in Cambodia, China, India, Pakistan, Sri Lanka and Turkey. We do not, and our subsidiary does not, perform material manufacturing or maintain significant assets outside the United States.

5

In some cases, the manufacturer or agent with whom we contract for production may subcontract work. Most of the listed countries have numerous suppliers that have the technical capability to manufacture the type of garments we sell. The availability of alternate sources tends to offset the risk associated with the loss of a major manufacturer.

We believe that the production capacity of foreign manufacturers with which we have developed, or are developing, a relationship is adequate to meet our production requirements for the foreseeable future. However, because of existing and potential import restrictions, we continue to attempt to diversify our sources of supply.

When management believes, based on previous experience and market performance, that additional orders for certain garments will be received, we may place production runs in amounts in excess of firm customer orders. This may allow us to achieve overall lower costs as well as to be able to respond more quickly to customer delivery requirements. However, we bear the consequent risk if garments purchased in advance of receipt of customer purchase orders do not sell.

Raw Materials

The clothing we sell is made of l00% cotton, cotton blends, polyester, rayon and leather fabrics. All of these fabrics are readily available in most countries in which we contract for production and are easily imported to those countries that do not have an internal supply of such fabric. The majority of the fabrics that we use comes from multiple sources of supply in many countries including China, Pakistan and India. We are not dependent on a single source of supply for fabric that is not readily replaceable.

Quality Control

Company representatives regularly visit manufacturers to inspect garments and monitor production facilities in order to assure timely delivery, maintain quality control and issue inspection certificates. Furthermore, through these representatives and independent inspectors from major retailers, we ensure that the factories we use for production adhere to policies consistent with prevailing labor laws. A sample of garments from a percentage of each production run is inspected before each shipment. Letters of credit we arrange require, as a condition to the release of funds to the supplier, that a representative of the Company sign an inspection certificate.

Marketing and Distribution

We sell our products through an established sales network consisting of both in-house sales personnel and independent sale representatives. We do not generally advertise, although customers sometimes feature our products in their advertisements. Employees in our showrooms in New York City, Dallas and Los Angeles represent us in soliciting orders nationally. In addition, our senior managers have primary responsibility for sales to certain key accounts. Our products are also marketed by 54 independent commissioned sales representatives.

The presence of a national brand has emerged as a principle factor in apparel buying decisions. In response, we have sought ownership or control of recognized brands for the categories of apparel that we distribute. We market sleepwear, robes, loungewear, and daywear under the following brands: Derek Rose®, Princesse tam tam®, Crabtree & Evelyn®, Disney Couture®, The Anne Lewin® Collection, The Bill Blass® Lifestyle Collection, The Claire Murray® Collection and Gossard®. We design and distribute men’s casual wear and performance apparel under the Nat Nast®, Newport Blue®, Dockers®, The Skins Game® and ZOIC® labels through agreements with third parties. We distribute women’s western wear shirts under our own labels Adobe Rose® and Southwest Canyon®. Western jeans are sold under the label Posted® through a licensing agreement with a third party supplier. We also import and distribute sweater-knit tops and leather and suede apparel under the brands Saguaro® and Saguaro West®, which we own. We distribute home décor products under the Bill Blass® and Newport Blue® brands through agreements with third parties. We sell our branded products to better department stores, specialty boutiques, moderate department stores and national and regional discount department stores and chains. We also develop and manufacture private label products for many leading retailers and catalogs.

Most garments are shipped by suppliers in bulk form to our warehouses in San Diego and Reno, where they are sorted, stored and packed for distribution to customers. From time to time, we may rent additional short-term warehouse space as needed to accommodate our requirements during peak shipping periods. In addition, to facilitate shipping to customers, some of our overseas suppliers perform sorting, price ticketing, hanging, and packing functions.

6

Customers

We sell to better department stores, specialty boutiques, moderate department stores, and national and regional discount department stores and chains. Sales are made against customer issued purchase orders.

Purchase orders may be canceled by our customers in the event of late delivery or in the event of receipt of nonconforming goods. Late deliveries usually are attributable to production or shipping delays beyond our control. In the event of canceled purchase orders, rejections or returns, we will sell garments to other retailers, off-price discount stores or garment jobbers. In the past we have often been able to recover from our manufacturers some portion of our expenses or losses associated with sales below cost for causes attributable to manufacturing problems. We have also historically experienced losses on merchandise that is rejected or returned, but past losses on rejected and returned merchandise have not been material to our overall operations.

Our business is concentrated on certain significant customers. Sales to three customers accounted for 17.7%, 15.3% and 12.8% respectively, of the Company’s net sales during fiscal 2007. While three customers accounted for 21.6%, 10.9% and 11.2% respectively of the Company’s net sales in fiscal 2006. One customer accounted for 53.1% of the Company’s net sales in fiscal 2005. While we believe our relationships with our major customers are good, because of competitive changes and availability of the types of garments we sell from a number of other suppliers, there is the possibility that any customer could alter the amount of business it does with us. If we experience a significant decrease in sales to any of our major customers, and are unable to replace such sales volume with sales to other major customers, there could be a material adverse financial effect on our operations.

Imports and Import Restrictions

Our ability to import garments is subject to the risks of international commerce. Imports into the United States are affected by, among other things, the cost of transportation and import restrictions that limit the specific number of garments that may be imported from any country during a specific period. Countries from which we purchase garments may impose or alter quotas, duties or other restrictions on substantially all of the products that we import. Because of this uncertainty, we have sought diversity in the number of countries in which we have garments manufactured.

Import restrictions have, in some cases, increased the cost of finished goods to us as a result of increased competition for a restricted supply of goods. Our future results may also be affected by additional bilateral or unilateral trade restrictions, a significant change in existing quotas, political instability resulting in the disruption of trade from exporting countries, or the imposition of additional duties, taxes and other charges on imports.

Because of import restrictions and quotas, embargos, and political instability in some countries of origin, we may be unable, from time to time, to import certain types of garments. Because of our dependence on foreign suppliers, a significant tightening or utilization of import quotas for the types of garments we import, applicable to a substantial number of countries from which we import, could force us to seek other sources of supply and to take other actions which could increase costs of production. This could also cause delays in production and result in cancellation of orders. Any of these factors could result in a material adverse financial impact on the Company.

We believe that we have the ability to locate, establish relationships with and develop manufacturing sources in countries where we have not previously operated. The time required to commence contract production in supplier countries ranges from several weeks in the case of a country with a relatively well developed garment manufacturing industry to four months or more for a country in which there are less developed capabilities. The cost to us of arranging for production in a country generally involves management time and associated travel expenses.

Backlog

At August 31, 2007 and August 31, 2006 we had unfilled customer orders of $42.3 million and $44.7 million, respectively, with such orders generally scheduled for delivery by March 2008 and 2007, respectively. The decrease in backlog of $2.4 million is due to a decline in sleepwear orders. The amount of unfilled orders at any given time is affected by a number of factors, including the timing of the receipt and processing of customer orders and the scheduling of the manufacture and shipping of the product, which may be dependent on customer requirements.

7

As of November 30, 2007, we had on-hand unfilled customer orders of $36.3 million as compared to $26.4 million at November 30, 2006, with such orders generally scheduled for delivery by May 2008 and 2007, respectively. The increase in backlog of $9.9 million is primarily due to increases in orders for men’s sportswear, women’s sleepwear and home décor items. Backlog amounts include both confirmed orders and unconfirmed orders that we believe, based on industry practice and past experience, will be confirmed. While cancellations, rejections and returns have generally not been material in the past, there can be no assurance that such action by customers will not reduce the amount of sales realized from the backlog of orders at either August 31, 2007 or November 30, 2007.

Competition

The apparel industry is highly competitive and consists of many manufacturers and distributors, none of which account for a significant percentage of total sales, but many of which are larger and have substantially greater resources than the Company. We compete with a number of companies which import clothing from abroad for wholesale distribution, with domestic retailers having established foreign manufacturing capabilities and with domestically produced goods. Management believes that we compete upon the basis of price, quality, the desirability of its fabrics and styles, and the reliability of its service and delivery. In addition, we have developed long-term working relationships with manufacturers and agents, which presently provide us with reliable sources of supply. Increasingly we compete directly with agents or with retailers’ own sourcing affiliates who own factories or have established production relationships that allow these companies to directly supply retailers with the desired product at a lower cost.

Employees

Our ability to compete effectively is dependent, in part, on our ability to retain managerial personnel with experience in locating, developing and maintaining reliable sources of supply and to retain experienced sales and product development personnel. As of August 31, 2007, we had 80 full-time employees, of whom 15 worked in executive, administrative or clerical capacities, 58 worked in sales, design, and production, and 7 worked in warehousing and logistics. Additionally, we employ eight individuals in our Hong Kong office who are responsible for fabric and trim sourcing, product development and quality control. We also contract with an unrelated entity to provide warehouse services. We may also employ temporary personnel on a seasonal basis. None of our employees is represented by a union. We consider our working relationships with our employees to be good and have never experienced an interruption of our operations due to any kind of labor dispute.

Available Information

Our annual reports on Form 10-K, along with all other reports and amendments filed with or furnished to the Securities and Exchange Commission (“SEC”), are publicly available free of charge on the Investor Relations section of our website at www.nitches.com as soon as reasonably practicable after these materials are filed with or furnished to the SEC. Our corporate governance policies, code of ethics and Board of Directors’ committee charters are also posted within this section of the website. The information on our website is not part of this or any other report we file with, or furnish to, the SEC. The SEC also maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. The address of that site is www.sec.gov.

Item 1A – Risk Factors

Our ability to implement our business strategy and achieve the intended operating results is subject to a number of risks and uncertainties, including the ones identified below, and additional risks not currently known to us or that we currently believe are immaterial.

We rely on a few key customers, and the loss of any one key customer would substantially reduce our revenues.

We derive a significant amount of our revenues from a few major customers. A significant decrease in business from or loss of any of our major customers could harm our financial condition by causing a significant decline in revenues attributable to such customers.

The Company’s business is concentrated on certain significant customers. Sales to three customers accounted for 17.7%, 15.3% and 12.8% respectively, of the Company’s net sales during fiscal 2007. Three customers accounted for 21.6%, 10.9% and 11.2% respectively of the Company’s net sales in fiscal 2006. One customer accounted for 53.1% of the Company’s net sales in fiscal 2005. While the Company believes its relationships with its major customers are good, we do not have long-term contracts with any of them and purchases generally occur on an order-by-order basis. Because of competitive changes and the availability of the types of garments sold by the Company from a number of other suppliers, there is the possibility that any customer could alter the amount of business it does with the Company. If the Company experiences a significant decrease in sales to any of its major customers, and is unable to replace such sales volume with orders from other customers, there could be a material adverse financial effect on the Company.

8

Our business depends on consumer spending patterns.

Our business is sensitive to a number of factors that influence the levels of consumer spending, including political and economic conditions such as recessionary environments, the levels of disposable consumer income, consumer debt, interest rates and consumer confidence. Reduced consumer spending on apparel and accessories could have an adverse effect on our operating results.

We operate in a highly competitive and fragmented industry and our failure to successfully compete could result in a loss of one or more significant customers.

The retail apparel industry is highly competitive. As an apparel company, we face competition on many fronts including the following:

- establishing and maintaining favorable brand recognition;

- developing products that appeal to consumers;

- pricing products appropriately; and

- obtaining access to and sufficient floor space in retail outlets.

Our competitors include numerous apparel and home décor designers, manufacturers, importers and licensors, many of which have greater financial and marketing resources than us. The competitive responses encountered from these larger, more established companies may be more aggressive and comprehensive than anticipated and we may not be able to compete effectively. The aggressive and competitive nature of the apparel and home furnishings industries may result in lower prices for our products and decreased gross profit margins, either of which may materially adversely affect sales and profitability. We believe that the principal competitive factors in the apparel industry are:

- timeliness, reliability and quality of services provided,

- pricing that supports retailers’ targeted gross margins,

- product designs that appeal to current consumer tastes and preferences,

- brand name and brand identity, and

- the ability to anticipate customer requirements and consumer demand.

If we do not continue to provide high quality and reliable services on a timely basis at competitive prices, we may not be able to continue to compete successfully in our industry. If we are unable to compete successfully, we could lose one or more of our significant customers which, if not replaced, could negatively impact our sales and financial performance.

We must successfully gauge fashion trends and changing consumer preferences to succeed.

Our failure to anticipate, identify and respond effectively to changing consumer demands and fashion trends could adversely affect acceptance of our products by retailers and consumers and may result in a significant decrease in net sales or leave us with a substantial amount of unsold inventory. We believe that our success depends on our ability to anticipate, identify and respond to changing fashion trends in a timely manner. Our products must appeal to a broad range of consumers whose preferences cannot be predicted with certainty and are subject to rapid change. If our products are not successfully received by retailers and consumers and we are left with a substantial amount of unsold inventory, we may be forced to rely on markdowns or promotional sales to dispose of excess, slow-moving inventory. If this occurs, our business, financial condition, results of operations and prospects may be harmed.

The apparel industry has relatively long lead times for the design and production of products. Consequently, we must in some cases commit to production in advance of orders based on forecasts of customer and consumer demand. If we fail to forecast demand accurately, we may under-produce or over-produce a product and encounter difficulty in filling customer orders or in liquidating excess inventory. Additionally, if we over-produce a product based on an aggressive forecast of demand, retailers may not be able to sell the product and cancel future orders or require retrospective price adjustments. These outcomes could have a material adverse effect on sales and brand image and adversely affect sales and profitability.

9

We depend on our key personnel.

Our success depends to a large extent upon the continued services of our officers and managers. The loss of the services of any key member of management could have a material adverse effect on our ability to manage our business. Our continued success is dependent upon our ability to attract and retain qualified management, administrative and sales personnel to support our future growth. Our inability to do so may have a significant negative impact on our ability to manage our business.

Consolidation and change in the retail industry may eliminate existing or potential customers.

A number of apparel retailers have experienced significant changes and difficulties over the past several years, including consolidation of ownership, increased centralization of buying decisions, restructurings, bankruptcies and liquidations. During past years, various apparel retailers, including some of our customers, have experienced financial problems that have increased the risk of extending credit to those retailers. Financial problems with respect to any of our customers could cause us to reduce or discontinue business with those customers or require us to assume more credit risk relating to those customers' receivables, either of which could have a material adverse effect on our business, results of operations and financial condition.

There has been and continues to be merger, acquisition and consolidation activity in the retail industry. Future consolidation could reduce the number of our customers and potential customers. A smaller market for our products could have a material adverse impact on our business and results of operations. In addition, it is possible that the larger customers, which result from mergers or consolidations, could decide to perform many of the services that we currently provide. If that were to occur, it could cause our business to suffer.

With increased consolidation in the retail industry, we are increasingly dependent upon key retailers whose bargaining strength and share of our business is growing. Accordingly, we face greater pressure from these customers to provide more favorable trade terms. We could be negatively affected by changes in the policies or negotiating positions of our customers. Our inability to develop satisfactory programs and systems to satisfy these customers could adversely affect operating results in any reporting period.

Fluctuations in the price, availability and quality of raw materials could cause delays and increase costs.

Fluctuations in the price, availability and quality of the fabrics or other raw materials used in our manufactured apparel could have a material adverse effect on cost of sales or our ability to meet customer demands. The prices for fabrics depend largely on the market prices for the raw materials used to produce them, particularly cotton. The price and availability of the raw materials and, in turn, the fabrics used in our apparel may fluctuate significantly, depending on many factors, including crop yields, weather patterns and changes in oil prices. We may not be able to pass higher raw materials prices and related transportation costs on to our customers.

The extent of our foreign sourcing and manufacturing may adversely affect our business.

Substantially all of our products are manufactured outside the United States. As a result of the magnitude of our foreign sourcing and manufacturing, our business is subject to all of the following risks:

- Uncertainty caused by the elimination of import quotas in China. Such quotas have been replaced by safeguard provisions that continue to provide limits on importation of apparel on China. The operation and effects of these safeguard provisions are uncertain and could result in delays in imports and supplies. As a result, we will have to monitor and manage our sourcing of products and develop alternative sourcing plans, if necessary, to alleviate the impact of any anticipated impact of safeguard provisions.

- Political and economic instability in foreign countries, including heightened terrorism and other security concerns, which could subject imported or exported goods to additional or more frequent inspections, leading to delays in deliveries or impoundment of goods.

- Imposition of regulations and quotas relating to imports, including quotas imposed by bilateral textile agreements between the United States and foreign countries.

10

- Imposition of duties, taxes and other charges on imports.

- Significant fluctuation of the value of the dollar against foreign currencies.

- Restrictions on the transfer of funds to or from foreign countries.

- Political instability, military conflict, or terrorism involving the United States, or any of the many countries where our products are manufactured, which could cause a delay in transportation, or an increase in transportation costs of raw materials or finished product.

- Disease epidemics and health related concerns, such as SARS or the mad cow or bird flu disease outbreaks in recent years, which could result in closed factories, reduced workforces, scarcity of raw materials and scrutiny or embargoing of goods produced in infected areas.

- Reduced manufacturing flexibility because of geographic distance between us and our foreign manufacturers, increasing the risk that we may have to mark down unsold inventory as a result of misjudging the market for a foreign-made product.

- Violations by foreign contractors of labor and wage standards and resulting adverse publicity.

If these risks limit or prevent us from manufacturing products in any significant international market, prevent us from acquiring products from foreign suppliers, or significantly increase the cost of our products, our operations could be seriously disrupted until alternative suppliers are found or alternative markets are developed, which could negatively impact our business.

Our success depends in part on the value of licensed brands.

Many of our products are produced under license agreements with third parties. Similarly, we license some of our brand names to other companies. Our success depends on the value of the brands and trademarks that we license and sell. Brands that we license from third parties are integral to our business as is the implementation of our strategies for growing and expanding these brands and trademarks. We market some of our products under the names and brands of recognized designers. Our sales of these products could decline if any of those designer's images or reputations were to be negatively impacted. Additionally, we rely on continued good relationships with both licensees and licensors, of certain trademarks and brand names. Adverse actions by any of these third parties could damage the brand equity associated with these trademarks and brands, which could have a material adverse effect on our business, results of operations and financial condition.

We may not address successfully the problems encountered in connection with any potential and completed acquisitions.

We expect to continue to consider opportunities to acquire or make investments in other technologies, products and businesses that could enhance our capabilities, complement our current products or expand the breadth of our markets or customer base. We have limited experience in acquiring other businesses and technologies. Potential and completed acquisitions and strategic investments involve numerous risks, including:

- problems assimilating the purchased products or business operations;

- problems maintaining uniform standards, procedures, controls and policies;

- unanticipated costs associated with the acquisition;

- failure to adequately integrate operations or obtain anticipated operative efficiencies;

- diversion of management’s attention from our core business;

- adverse effects on existing business relationships with suppliers and customers;

- risks associated with entering new markets in which we have no or limited prior experience; and

- potential loss of key employees of acquired businesses.

If we fail to properly evaluate and execute acquisitions and strategic investments, our management team may be distracted from our day-to-day operations, our business may be disrupted and our operating results may suffer. In addition, if we finance acquisitions by issuing equity or convertible securities, our stockholders would be diluted.

Our competitive position could suffer, if our intellectual property rights are not protected.

We believe that our trademarks and designs are of great value. From time to time, third parties have challenged, and may in the future try to challenge, our ownership of our intellectual property. We are susceptible to others imitating our products and infringing our intellectual property rights. Imitation or counterfeiting of our products or infringement of our intellectual property rights could diminish the value of our brands or otherwise adversely affect our revenues. We cannot assure you that the actions we have taken to establish and protect our trademarks and other intellectual property rights will be adequate to prevent imitation of our products by others or to prevent others from seeking to invalidate our trademarks or block sales of our products as a violation of the trademarks and intellectual property rights of others. In addition, we cannot assure you that others will not assert rights in, or ownership of, our trademarks and other intellectual property rights or in similar marks or marks that we license and/or market or that we will be able to successfully resolve these conflicts to our satisfaction. We may need to resort to litigation to enforce our intellectual property rights, which could result in substantial costs and diversion of resources. At the time of any such infringement, we may not have adequate financial resources to prosecute or defend a lengthy trademark or copyright case.

11

Our reliance on independent manufacturers could cause delays and damage customer relationships.

We rely on independent manufacturers to assemble or produce a substantial portion of our products. We are dependent on the ability of these independent manufacturers to adequately finance the production of goods ordered and maintain sufficient manufacturing capacity. The use of independent manufacturers to produce finished goods and the resulting lack of direct control could subject us to difficulty in obtaining timely delivery of products of acceptable quality. We generally do not have long-term contracts with any independent manufacturers. Alternative manufacturers, if available, may not be able to provide us with products or services of a comparable quality, at an acceptable price or on a timely basis. There can be no assurance that there will not be a disruption in the supply of our products from independent manufacturers or, in the event of a disruption, that we would be able to substitute suitable alternative manufacturers in a timely manner, if at all. The failure of any independent manufacturer to perform or the loss of any independent manufacturer could have a material adverse effect on our business, results of operations and financial condition.

We do not control our independent manufacturers or their labor and other business practices. If any of our manufacturers violates labor or other laws or implements labor or other business practices that are generally regarded as unethical in the United States, the shipment of finished products could be interrupted, orders could be cancelled, relationships could be terminated and our reputation could be damaged. Any of these events could have a material adverse effect on our revenues and, consequently, our results of operations.

The apparel business is subject to seasonal volatility and our operating results may fluctuate on a quarterly and annual basis, which could cause our stock price to fluctuate or decline.

Our operating results may fluctuate substantially from quarter-to-quarter and year-to-year for a variety of reasons, many of which are beyond our control. Factors that could affect our quarterly and annual operating results include those listed below as well as others listed in this "Risk Factors" section:

- changes in our pricing policies or those of our competitors;

- our current reliance on large-volume orders from only a few customers;

- the receipt and shipment of large orders or reductions in these orders;

- variability between customer and product mix;

- delays or failures to fulfill orders for our products on a timely basis;

- the availability and cost of raw materials and components for our products; and

- operational disruptions, such as transportation delays or failures of our order processing system.

As a result of these factors, period-to-period comparisons of our operating results may not be meaningful, and you should not rely on them as an indication of our future performance. In addition, our operating results may fall below the expectations of public market analysts or investors. In this event, our stock price could decline significantly.

If we need additional financing in the future and are required to issue securities which are priced at less than the conversion price of our convertible debentures or the exercise price of warrants sold in our June 2007 Private Placement, it will result in additional dilution.

In our June 2007 Private Placement, in the aggregate, we issued a total of $3.15 million principal amount of debentures (convertible into 764,563 shares of common stock based on the current conversion price) and warrants to purchase 577,500 shares of our common stock. Both the debentures and warrants contain provisions that will require us to reduce the conversion price of the debentures (currently $4.12 per share) and the exercise price of the warrants (currently $4.12 per share) if we issue any securities while such debentures and warrants are outstanding with a purchase price, conversion price or exercise price that is less than the conversion price of the debentures or the exercise price of the warrants issued in our June 2007 Private Placement. If this were to occur, current investors, other than the investors in our June 2007 Private Placement, would sustain dilution in their ownership interest.

12

Our former auditors have only tail professional liability insurance to allow it to meet any responsibility to discharge its liabilities, if any, with respect to its audits of our financial statements for our fiscal years ended August 31, 2006 and 2005.

In May 2007, J.H. Cohn LLP acquired Berenson LLP in a transaction that was structured as an asset sale. As such, J.H.Cohn LLP did not succeed to the liabilities of Berenson LLP. Berenson LLP continues to exist with ongoing responsibility to discharge its liabilities for work performed prior to May 3, 2007. Berenson LLP has purchased tail professional liability insurance to allow it to meet any such ongoing responsibilities.

Berenson LLP was our independent registered public accounting firm during our fiscal years ended August 31, 2006 and 2005. If we have any claim against Berenson LLP with respect to its audits of our financial statements for our fiscal years ended August 31, 2006 and 2005, our ability to seek redress may be limited to the tail professional liability insurance that Berenson LLP purchased to meet its ongoing responsibilities. There can be no assurances that such insurance will be enough to cover our claims, if any.

Our chief executive officer beneficially owns approximately 23% of our outstanding common stock, and will be able to exert substantial influence over us and our major corporate decisions.

As of November 30, 2007, our chief executive officer, Steven P. Wyandt, beneficially owns approximately 23% of our outstanding common stock. As a result of his ownership interest, Mr. Wyandt will have substantial influence over who is elected to our board of directors each year as well as whether we enter into any significant corporate transactions that require stockholders approval.

Item 1B – Unresolved Staff Comments

Not applicable.

Item 2 - Properties

We currently lease properties in California, Nevada, Texas, Hong Kong and New York. We lease one showroom in New York City, one in Los Angeles, one in Dallas, and an office in Hong Kong, along with approximately 76,000 square feet for warehousing and administrative offices in Reno and approximately 28,000 square feet for warehousing and administrative offices in San Diego. We may lease additional short-term warehouse space from time to time as needed.

Each of our facilities is covered by insurance and we believe them to be suitable for their respective uses and adequate for our present needs. We believe that suitable additional or substitute space will be available to accommodate the foreseeable expansion of our operations.

Item 3 - Legal Proceedings

From time to time, we may be involved in litigation relating to claims arising out of our operations in the normal course of business. As of the date of this report, we are not a party to any such litigation which we believe would have a material adverse effect on us.

Item 4 - Submission of Matters to a Vote of Security Holders

On August 29, 2007, we held our Annual Meeting of Stockholders (the “Annual Meeting”) to elect a board of five directors.

13

The following votes were cast with respect to such election:

| NAME | FOR |

WITHHELD | ||

| Steven P. Wyandt | 4,394,827 | 327,359 | ||

| Paul M. Wyandt | 4,406,458 | 315,728 | ||

| Eugene B. Price II | 4,396,628 | 325,588 | ||

| Michael D. Sholtis | 4,396,628 | 325,588 | ||

| T. Jefferson Straub | 4,404,355 | 313,831 |

The foregoing action is described in further detail in our Definitive Proxy Statement on Schedule 14A filed with the SEC on August 1, 2007.

PART II

Item 5 - Market for the Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Market information

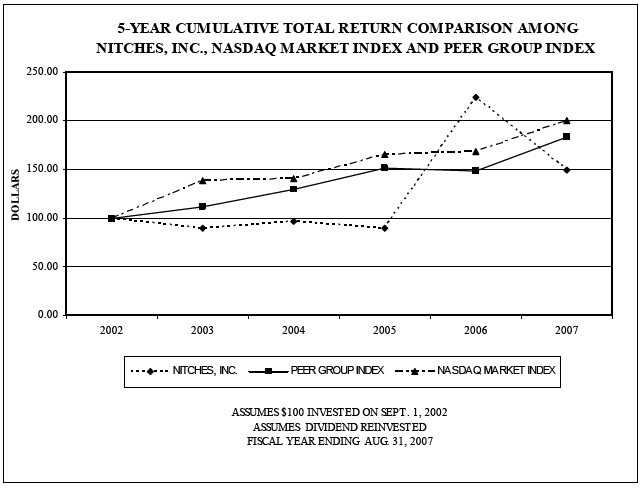

The following graph compares the performance of the Company for the five-year period ending August 31, 2007 with the performance of the NASDAQ market index and the average performance of companies comprising the Dow Jones Industry Group CLO – Clothing & Accessories, which for this year numbered 12 companies, and which is published by Dow Jones & Company. The index reflects reinvested dividends and is weighted by the sum of the closing price times the shares outstanding divided by the total shares outstanding for the group.

14

Our common stock trades on The NASDAQ Capital Market under the symbol NICH. The high and low closing sale prices, adjusted for stock dividends, for each fiscal quarter during the last two fiscal years were as follows:

| High | Low | ||||

| FISCAL YEAR ENDED AUGUST 31, 2007 | |||||

| Fourth Quarter | $ | 4.11 | $ | 2.25 | |

| Third Quarter | $ | 5.84 | $ | 3.54 | |

| Second Quarter | $ | 7.80 | $ | 4.79 | |

| First Quarter | $ | 6.67 | $ | 4.19 | |

| FISCAL YEAR ENDED AUGUST 31, 2006 | |||||

| Fourth Quarter | $ | 6.03 | $ | 3.09 | |

| Third Quarter | $ | 8.64 | $ | 4.53 | |

| Second Quarter | $ | 7.94 | $ | 1.63 | |

| First Quarter | $ | 1.80 | $ | 1.67 | |

Holders

The number of shareholders of record of our common stock on November 30, 2007 was 89. The Company believes that there are a significant number of beneficial owners of its Common Stock whose shares are held in "street name".

Dividends

We do not have a stated dividend policy and did not pay or declare any cash dividends during fiscal year 2007 or 2006. On January 20, 2006 the Company issued a 200% stock dividend to shareholders of record as of January 3, 2006. This stock dividend had the effect of tripling the outstanding number of shares common stock of the Company.

Securities authorized for issuance under Equity Compensation Plans.

The table below sets forth information as of August 31, 2007, with respect to compensation plans under which our common stock is authorized for issuance. The figures related to the equity compensation plan approved by security holders relate to our 2006 Equity Incentive Plan. We do not have any equity compensation plans that have not been approved by security holders.

Equity Compensation Plan Information

| Number of securities remaining | |||||||

| Number of securities to | Weighted-average | available for future issuance | |||||

| be issued upon exercise | exercise price of | under equity compensation | |||||

| of outstanding options, | outstanding options, | plans (excluding securities | |||||

| warrants and rights | warrants and rights | reflected in column (a)) | |||||

| Plan Category | (a) | (b) | (c) | ||||

| Equity Compensation Plans | |||||||

| Approved by Security Holders | 440,000 | $4.35 | 160,000 | ||||

15

Item 6 - Selected Financial Data (In thousands, except per share amounts)

| Years Ended August 31, | ||||||||||||||||||||

| 2007 | 2006 | 2005 | 2004 | 2003 | ||||||||||||||||

| (In thousands, except per share amounts) | ||||||||||||||||||||

| CONSOLIDATED STATEMENTS OF OPERATIONS DATA: | ||||||||||||||||||||

| Net sales | $ | 84,943 | $ | 54,832 | $ | 26,320 | $ | 32,179 | $ | 28,440 | ||||||||||

| Cost of goods sold | 64,586 | 39,985 | 20,534 | 22,783 | 21,856 | |||||||||||||||

| Gross profit | 20,357 | 14,847 | 5,786 | 9,396 | 6,584 | |||||||||||||||

| Selling, general and administrative expenses | 20,618 | 13,763 | 8,175 | 8,389 | 7,663 | |||||||||||||||

| Operating income (loss) | (261 | ) | 1,084 | (2,389 | ) | 1,007 | (1,079 | ) | ||||||||||||

| Other income | - | 2 | 460 | - | 3 | |||||||||||||||

| Interest expense | (1,037 | ) | (486 | ) | (102 | ) | (93 | ) | (83 | ) | ||||||||||

| Income (loss) from equity investment | - | (11 | ) | (64 | ) | 14 | (236 | ) | ||||||||||||

| Income (loss) before income taxes | (1,298 | ) | 589 | (2,095 | ) | 928 | (1,395 | ) | ||||||||||||

| Provision for (benefit from) income taxes | (362 | ) | 121 | (894 | ) | 371 | (425 | ) | ||||||||||||

| Net income (loss) | $ | (936 | ) | $ | 468 | $ | (1,201 | ) | $ | 557 | $ | (970 | ) | |||||||

| Basic earnings (loss) per share | $ | (0.18 | ) | $ | 0.11 | $ | (0.34 | ) | $ | 0.16 | $ | (0.28 | ) | |||||||

| Diluted earnings (loss) per share | $ | (0.18 | ) | $ | 0.11 | $ | (0.34 | ) | $ | 0.16 | $ | (0.28 | ) | |||||||

| Cash dividends per common share | $ | - | $ | - | $ | - | $ | - | $ | 0.10 | ||||||||||

| Weighted average number of common shares (000’s): | ||||||||||||||||||||

| Basic | 5,311 | 4,077 | 3,514 | 3,514 | 3,514 | |||||||||||||||

| Diluted | 5,311 | 4,077 | 3,514 | 3,514 | 3,514 | |||||||||||||||

| As of August 31 | ||||||||||||||||||||

| 2007 | 2006 | 2005 | 2004 | 2003 | ||||||||||||||||

| (In thousands) | ||||||||||||||||||||

| CONSOLIDATED BALANCE SHEETS DATA: | ||||||||||||||||||||

| Cash | $ | 353 | $ | 228 | $ | 192 | $ | 219 | $ | 110 | ||||||||||

| Total assets | 38,101 | 30,784 | 10,453 | 9,561 | 6,847 | |||||||||||||||

| Long-term debt | 1,627 | - | - | - | - | |||||||||||||||

| Other Financial Information: | ||||||||||||||||||||

| Gross margin | 24.0% | 27.1% | 22.0% | 29.2% | 23.2% | |||||||||||||||

| Operating margin (deficit) | (0.3% | ) | 2.0% | (9.1% | ) | 3.1% | (3.8% | ) | ||||||||||||

| Net income (loss) as a percent of sales | (1.1% | ) | 0.9% | (4.6% | ) | 1.7% | (3.4% | ) | ||||||||||||

| Liquidity: | ||||||||||||||||||||

| Current ratio | 1.33 | 1.17 | 1.72 | 2.45 | 3.94 | |||||||||||||||

| Working capital | $ | 7,199 | $ | 3,636 | $ | 4,341 | $ | 5,617 | $ | 5,014 | ||||||||||

16

Item 7 - Management's Discussion and Analysis of Financial Condition and Results of Operation

Cautionary Statement Under the Private Securities Litigation Reform Act of 1995

Statements in this annual report on Form 10-K including statements under the caption "Management's Discussion and Analysis of Financial Condition and Results of Operations", as well as oral statements that may be made by the Company or by officers, directors or employees of the Company acting on the Company's behalf, that are not historical fact constitute "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements involve known and unknown risks and uncertainties that may cause the Company's actual results in future periods to differ materially from forecasted results. You can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expects,” “intends,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” “potential,” “continues” or the negative of these terms or other comparable terminology. These risks and other factors include those listed under “Risk Factors” and elsewhere in this report. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. You should not place undue reliance on any forward-looking statements as they reflect our management’s view only as of the date of this report. We will not update any forward-looking statements to reflect events or circumstances that occur after the date on which such statement is made.

Critical Accounting Policies

Several of the Company’s accounting policies involve significant judgments and uncertainties. The policies with the greatest potential effect on the Company’s results of operations and financial position include the estimated collectibility of accounts receivable and the recovery value of obsolete or overstocked inventory. On an on-going basis, management evaluates its estimates and judgments, including those related to revenue recognition, intangible assets, and income taxes.

Revenue Recognition. The Company recognizes revenue at the time products are shipped based on its terms of F.O.B. shipping point, where risk of loss and title transfers to the buyer at time of shipment. The Company records sales in accordance with SEC Staff Accounting Bulletin No. 104, Revenue Recognition. Under these guidelines, revenue is recognized when all of the following exist: persuasive evidence of a sale arrangement exists, delivery of the product has occurred, the price is fixed or determinable and payment is reasonably assured. Provisions are made currently for estimated product returns and sales allowances.

Allowances for Sales Returns, Doubtful Accounts and Other. Sales are recorded net of estimated future returns, uncollectible accounts receivable and other customer related allowances. Management analyzes historical returns and bad debt expense, current economic trends, changes in customer demand and sell-through of our products when evaluating the adequacy of these allowances. In addition, the Company may provide warehousing credits and other allowances to certain customers in accordance with industry practice. These reserves are determined based on historical experience, budgeted customer allowances and existing commitments to customers. Although management believes it has established adequate reserves with respect to these items, actual activity could vary from management's estimates and such variances could have a material impact on reported results.

Inventory. In its ordinary course of operations, the Company generally makes some sales below its normal selling prices or below cost. Based on experience, management believes this will be true for some inventory held on or acquired after August 31, 2007. The amount of such sales depends on several factors, including general economic conditions, market conditions within the apparel industry, the desirability of the styles held in inventory and competitive pressures from other garment suppliers.

The Company's inventory increased to $14.1 million at August 31, 2007 from $12.4 million at August 31, 2006, reflective of higher stock levels due to earlier receipt in the current year as compared to the prior year of pre-sold goods held for shipments to customers in primarily September and October. The Company has established an inventory markdown reserve as of August 31, 2007, which management believes will be sufficient for current inventory that is expected to be sold below cost in the future. There can be no assurance that the Company will realize its expected selling prices or that the inventory markdown reserve will be adequate for items in inventory as of August 31, 2007 for which customer sales orders have not yet been received. The inventory markdown reserve is calculated based on specific identification of aged goods and styles that are slow-moving or selling off-price.

Deferred Taxes. Deferred taxes are determined, based on the differences between the financial statement and tax bases of assets and liabilities, as well as the future benefit of any net operating loss carryforward, using enacted tax rates in effect for the year in which the differences are expected to reverse. Valuation allowances are established when necessary to reduce deferred tax assets to the amounts expected to be realized. In assessing the need for a valuation allowance management considers estimates of future taxable income and ongoing prudent and feasible tax planning strategies.

Goodwill and Intangible Asset Impairment. Goodwill represents the excess of cost over the fair value of the net identifiable assets acquired in a business combination. In accordance with SFAS No. 142, Goodwill and Other Intangibles (“SFAS 142”), goodwill and intangible assets with an indefinite useful life are no longer amortized, but are tested for impairment at least annually.

17

We performed an annual test during the fourth quarter of this fiscal year to determine if the recorded goodwill and intangible assets were impaired. This process compared the fair value of the goodwill and intangible assets to their carrying values. We concluded that for fiscal year 2007, the fair value of our goodwill and intangible assets exceeded the carrying values and no impairment charge was required.

The determination of whether these assets are impaired involves significant judgment based on long-term and short-term projections of future performance. Changes in strategy and/or market conditions or if actual operating results or cash flows are different than our estimates and assumptions, may result in impairment charges in future periods.

Stock-Based Compensation. We adopted Statement of Financial Accounting Standards No. 123 (revised 2004), “Share-Based Payment,” (SFAS 123(R)) when we issued our first options in September 2006. Under SFAS 123 (R), stock-based compensation cost is measured at the grant date, based on the estimated fair value of the award, and is recognized as expense over the employee’s requisite service period. The valuation provisions of SFAS 123 (R) apply to these and new awards.

We utilize the Black-Scholes option valuation model for estimating the fair value of the stock-based compensation granted. The Black-Scholes model was developed for use in estimating the fair value of traded options, which have no vesting restrictions and are fully transferable. In addition, option valuation models require the input of highly subjective assumptions including the expected stock price volatility. Because our stock options have characteristics significantly different from those of traded options, and because changes in the subjective input assumptions can materially affect the fair value estimate, in our opinion, the existing models do not necessarily provide a reliable single measure of the fair value of our employee stock options.

Results of Operations

Years Ended August 31, 2007 and 2006

Net sales for the fiscal year ended August 31, 2007 increased $30.1 million or 54.9% as compared to the prior fiscal year ended August 31, 2006. This increase was attributable to increased shipments of our sleepwear and mens and women’s sportswear product lines, as well as the inclusion of a full year of shipping of home décor product in the current year as compared to only two months of shipping home décor at the end of the prior year.

Cost of sales as a percent of net sales increased 3.1% generating a lower gross profit margin of 24.0% for the year ended August 31, 2007 as compared to 27.1% for the prior year. The decrease in gross margin came primarily as the result of increased private label sales in several product categories and a high volume sale of branded sleepwear product to a national retailer, both at a lower average gross margin. Cost of sales also included approximately $317,000 related to the write-off of inventory from a discontinued product line in August 2007. Our product mix constantly changes to reflect customer mix, fashion trends and changing seasons. Consequently gross margin is likely to vary on a quarter-to-quarter basis and in comparison to gross margins generated in prior years.

Selling, general and administrative expenses for the fiscal year ended August 31, 2007 increased $6.9 million from a year ago, due primarily to the consolidation of full year selling, general and administrative expenses for both the home décor and Designer Intimates product lines.

Interest expense increased $551,000 during the current year to $1.0 million as compared to $486,000 for the year ended August 31, 2006. This increase was due primarily to increased advances under our factoring agreement in support of our increased sales and operating activity, higher interest rates charged on those advances, and interest on our convertible debentures which were issued in June 2007.

Our income tax provision for the year ended August 31, 2007, reflects a $362,000 tax benefit on a pretax loss of $1.3 million, an effective tax rate of 27.9%. Our income tax provision for the year ended August 31, 2006, reflected a $121,000 tax expense on pretax income of $589,000 at an effective rate of 20.5%.

Years Ended August 31, 2006 and 2005

Net sales for the fiscal year ended August 31, 2006 increased $28.5 million or 108.3% as compared to the prior fiscal year ended August 31, 2005. This increase was primarily attributable to the acquisition of Designer Intimates early in the current year. Increased shipments of the Company’s sleepwear and menswear product lines as well as the addition of private label women’s sportswear also contributed to the increase.

18

Cost of sales as a percent of net sales decreased 5.1% generating a higher gross profit margin of 27.1% for the year ended August 31, 2006 as compared to 22.0% for prior year. The increase in gross margin came primarily as the result of the addition of higher gross margin sales from Designer Intimates, as well as higher gross margins in the Company’s menswear product line. The Company’s product mix constantly changes to reflect customer mix, fashion trends and changing seasons. Consequently gross margin is likely to vary on a quarter-to-quarter basis and in comparison to gross margins generated in prior years.

Selling, general and administrative expenses for the fiscal year ended August 31, 2006 increased $5.6 million from a year ago, due primarily to the selling, general and administrative costs for Designer Intimates. Selling, general and administrative expense for 2006 included $6.0 million of selling and merchandising expense and $1.9 million of warehousing and distribution expense.

Other income for the fiscal year 2005 of $460,000 included $453,000 for the repayment of a note receivable that the Company issued related to the sale of product lines in 1995. This note had been written off by the Company in fiscal 2001 as part of a credit reorganization of the buyer. However due to improved financial performance of the buyer achieved in part through continued guidance and support from the Company, the buyer was able to repay the balance on the note.

Interest expense increased $384,000 for the year ended August 31, 2006 to $486,000 as compared to $102,000 for the year ended August 31, 2005. This increase was due to increased advances under the Company’s factoring agreement, higher interest rates charged on those advances, and the inclusion of the interest expense of Designer Intimates.

The Company’s income tax provision for the year ended August 31, 2006, reflects a $121,000 tax expense on the Company’s pretax income of $589,000, an effective tax rate of 20.5%. This lowered tax rate is primarily the result of the benefit of net operating loss carryforwards. The Company’s income tax provision for the year ended August 31, 2005, reflects an $894,000 tax benefit on the Company’s pretax loss of $2,095,000, which includes the recognized operating loss of $64,000 from the unconsolidated subsidiary.

Liquidity and Capital Resources

Working capital increased to $7.2 million at August 31, 2007 from $3.6 million at August 31, 2006 due primarily to higher receivables due from the factor and higher inventory levels, both as a result of higher sales. Working capital decreased to $3.6 million at August 31, 2006 as compared to $4.3 million at August 31, 2005, due to current liabilities increasing $700,000 more than current assets increased. Increases in both current assets and current liabilities are largely attributable to the effect of balances acquired in the acquisition of Designer Intimates. However current liabilities also increased in line with increased purchases in July and August 2006 due to increased customer orders for fall 2006.

For the fiscal years ended August 31, 2007, 2006 and 2005, cash used by operating activities was approximately $1.5 million, $3.6 million and $1.1 million. Cash used by operating activities in fiscal 2007 resulted from a higher level of invoice assignments to the factor at year end coupled with an increase in inventories, offset partially by an increase in accounts payable and accrued expenses. For the fiscal year ended August 31, 2006, cash used by operating activities includes the effect of the balances acquired in the acquisition of Designer Intimates. Cash used in 2006 was attributed to an increase in inventory in response to increased orders for fall 2006 as well as an increase in accounts receivable due to increased sales in July and August. For the fiscal year ended August 31, 2005, in addition to the net loss, cash used by operating activities was due primarily to an increase in inventories offset partially by a decrease in accounts receivable.

Net cash used by investing activities during the fiscal year ended August 31, 2007 totaled $185,000 expended primarily on equipment utilized in our recently opened warehouse in Reno, Nevada. Net cash used by investing activities during the fiscal year ended August 31, 2006 consisted of $103,000 in acquisition related expenses and $44,000 in purchases of office equipment offset partially by the cash balance acquired in the purchase of Designer Intimates. For the fiscal year ended August 31, 2005 net cash used by investing activities of $168,000 was primarily for a contribution of capital to Designer Intimates.

19

For the fiscal years ended August 31, 2007, 2006 and 2005, cash provided by financing activities was approximately $1.8 million, $3.7 million, and $1.2 million respectively. For fiscal year ended August 31, 2007 $2.95 million was provided by the issuance of convertible debt and $1.5 million was provided by the issuance of common stock, offset partially from the repayment of notes payable and a lower rate of advances from the factor. For each of the fiscal years 2006 and 2005, cash provided by financing activities was attributable to advances from the Company’s factor in accordance with the terms of the factoring agreement. The increase in advances from factor for 2006 was attributable to the effect of the balances acquired in the acquisition of Designer Intimates. A note payable was also utilized in the purchase of inventory in response to increased orders for fall 2006.

The Company sells substantially all of its trade receivables to a factor (CIT) on a pre-approved, non-recourse basis. The Company attempts to make any recourse shipments on a COD basis or ensure that the customers' payments are backed by a commercial or standby letter of credit issued by the customers’ bank. The amount of the Company’s receivables which were recourse and were not made on a COD basis or supported by commercial or standby letters of credit at August 31, 2007 was approximately $526,000 of which approximately $446,000 had been collected through November 30, 2007.

Payment for non-recourse factored receivables is made at the time customers make payment to CIT or, if a customer is financially unable to make payment, within approximately 180 days of the invoice due date. Under the factoring agreement, the Company can request advances in anticipation of customer collections at CIT’s prime rate (currently 8.25%) less one and one-half percent (1.5%). The amount of advances available to the Company is limited to eighty-five percent (85%) of non-recourse factored receivables.

The factoring agreement does not contain any financial covenants with which the Company must adhere. Advances are collateralized by all of the assets of the Company as well as a personal guaranty of the Company’s Chairman Steven Wyandt. This guaranty allows CIT to recover up to $1 million from Mr. Wyandt to offset any losses incurred in the event of liquidation. The factoring agreement can be terminated by CIT on 30-days written notice.