DNOW Inc. - Quarter Report: 2019 March (Form 10-Q)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark one)

|

☒ |

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE QUARTERLY PERIOD ENDED March 31, 2019

OR

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 001-36325

NOW INC.

(Exact name of registrant as specified in its charter)

|

Delaware |

|

46-4191184 |

|

(State or other jurisdiction of |

|

(I.R.S. Employer |

|

incorporation or organization) |

|

Identification No.) |

7402 North Eldridge Parkway,

Houston, Texas 77041

(Address of principal executive offices)

(281) 823-4700

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer |

|

☒ |

|

Accelerated filer |

|

☐ |

|

|

|

|

|

|||

|

Non-accelerated filer |

|

☐ |

|

Small reporting company |

|

☐ |

|

|

|

|

|

|

|

|

|

Emerging growth company |

|

☐ |

|

|

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of April 25, 2019 the registrant had 108,720,185 shares of common stock (excluding 1,348,147 unvested restricted shares), par value $0.01 per share, outstanding.

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

|

Common Stock, par value $0.01 |

|

DNOW |

|

New York Stock Exchange |

TABLE OF CONTENTS

2

NOW INC.

(In millions, except share data)

|

|

|

March 31, 2019 |

|

|

December 31, 2018 |

|

||

|

|

|

(Unaudited) |

|

|

|

|

|

|

|

ASSETS |

|

|

|

|

|

|||

|

Current assets: |

|

|

|

|

|

|

|

|

|

Cash and cash equivalents |

|

$ |

87 |

|

|

$ |

116 |

|

|

Receivables, net |

|

|

513 |

|

|

|

482 |

|

|

Inventories, net |

|

|

634 |

|

|

|

602 |

|

|

Prepaid and other current assets |

|

|

18 |

|

|

|

19 |

|

|

Total current assets |

|

|

1,252 |

|

|

|

1,219 |

|

|

Property, plant and equipment, net |

|

|

110 |

|

|

|

106 |

|

|

Deferred income taxes |

|

|

2 |

|

|

|

2 |

|

|

Goodwill |

|

|

318 |

|

|

|

314 |

|

|

Intangibles, net |

|

|

140 |

|

|

|

144 |

|

|

Other assets |

|

|

74 |

|

|

|

10 |

|

|

Total assets |

|

$ |

1,896 |

|

|

$ |

1,795 |

|

|

LIABILITIES AND STOCKHOLDERS' EQUITY |

|

|

|

|

|

|||

|

Current liabilities: |

|

|

|

|

|

|

|

|

|

Accounts payable |

|

$ |

339 |

|

|

$ |

329 |

|

|

Accrued liabilities |

|

|

130 |

|

|

|

110 |

|

|

Other current liabilities |

|

|

6 |

|

|

|

2 |

|

|

Total current liabilities |

|

|

475 |

|

|

|

441 |

|

|

Long-term debt |

|

|

124 |

|

|

|

132 |

|

|

Long-term operating lease liabilities |

|

|

40 |

|

|

|

— |

|

|

Deferred income taxes |

|

|

5 |

|

|

|

6 |

|

|

Other long-term liabilities |

|

|

7 |

|

|

|

2 |

|

|

Total liabilities |

|

|

651 |

|

|

|

581 |

|

|

Commitments and contingencies |

|

|

|

|

|

|

|

|

|

Stockholders' equity: |

|

|

|

|

|

|

|

|

|

Preferred stock—par value $0.01; 20 million shares authorized; no shares issued and outstanding |

|

|

— |

|

|

|

— |

|

|

Common stock - par value $0.01; 330 million shares authorized; 108,708,922 and 108,426,962 shares issued and outstanding at March 31, 2019 and December 31, 2018, respectively |

|

|

1 |

|

|

|

1 |

|

|

Additional paid-in capital |

|

|

2,037 |

|

|

|

2,034 |

|

|

Accumulated deficit |

|

|

(660 |

) |

|

|

(678 |

) |

|

Accumulated other comprehensive loss |

|

|

(133 |

) |

|

|

(143 |

) |

|

Total stockholders' equity |

|

|

1,245 |

|

|

|

1,214 |

|

|

Total liabilities and stockholders' equity |

|

$ |

1,896 |

|

|

$ |

1,795 |

|

See notes to unaudited consolidated financial statements.

3

NOW INC.

CONSOLIDATED STATEMENTS OF OPERATIONS (UNAUDITED)

(In millions, except per share data)

|

|

|

Three Months Ended March 31, |

|

|||||

|

|

|

2019 |

|

|

2018 |

|

||

|

Revenue |

|

$ |

785 |

|

|

$ |

764 |

|

|

Operating expenses: |

|

|

|

|

|

|

|

|

|

Cost of products |

|

|

627 |

|

|

|

616 |

|

|

Warehousing, selling and administrative |

|

|

135 |

|

|

|

141 |

|

|

Operating profit |

|

|

23 |

|

|

|

7 |

|

|

Other expense |

|

|

(4 |

) |

|

|

(4 |

) |

|

Income before income taxes |

|

|

19 |

|

|

|

3 |

|

|

Income tax provision |

|

|

1 |

|

|

|

1 |

|

|

Net income |

|

$ |

18 |

|

|

$ |

2 |

|

|

Earnings per share: |

|

|

|

|

|

|

|

|

|

Basic earnings per common share |

|

$ |

0.17 |

|

|

$ |

0.02 |

|

|

Diluted earnings per common share |

|

$ |

0.16 |

|

|

$ |

0.02 |

|

|

Weighted-average common shares outstanding, basic |

|

|

109 |

|

|

|

108 |

|

|

Weighted-average common shares outstanding, diluted |

|

|

109 |

|

|

|

108 |

|

See notes to unaudited consolidated financial statements.

4

NOW INC.

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (UNAUDITED)

(In millions)

|

|

Three Months Ended March 31, |

|

|||||

|

|

2019 |

|

|

2018 |

|

||

|

Net income |

$ |

18 |

|

|

$ |

2 |

|

|

Other comprehensive income: |

|

|

|

|

|

|

|

|

Foreign currency translation adjustments |

|

10 |

|

|

|

1 |

|

|

Comprehensive income |

$ |

28 |

|

|

$ |

3 |

|

See notes to unaudited consolidated financial statements.

5

NOW INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

(In millions)

|

|

Three Months Ended March 31, |

|

|||||

|

|

2019 |

|

|

2018 |

|

||

|

Cash flows from operating activities: |

|

|

|

|

|

|

|

|

Net income |

$ |

18 |

|

|

$ |

2 |

|

|

Adjustments to reconcile net income to net cash used in operating activities: |

|

|

|

|

|

|

|

|

Depreciation and amortization |

|

10 |

|

|

|

11 |

|

|

Deferred income taxes |

|

— |

|

|

|

— |

|

|

Stock-based compensation |

|

4 |

|

|

|

4 |

|

|

Provision for inventory |

|

4 |

|

|

|

2 |

|

|

Other, net |

|

5 |

|

|

|

1 |

|

|

Change in operating assets and liabilities: |

|

|

|

|

|

|

|

|

Receivables |

|

(26 |

) |

|

|

(74 |

) |

|

Inventories |

|

(34 |

) |

|

|

(22 |

) |

|

Prepaid and other current assets |

|

— |

|

|

|

(3 |

) |

|

Accounts payable and accrued liabilities |

|

(1 |

) |

|

|

48 |

|

|

Income taxes receivable / payable |

|

1 |

|

|

|

1 |

|

|

Other assets / liabilities, net |

|

(1 |

) |

|

|

— |

|

|

Net cash used in operating activities |

|

(20 |

) |

|

|

(30 |

) |

|

Cash flows from investing activities: |

|

|

|

|

|

|

|

|

Purchases of property, plant and equipment |

|

— |

|

|

|

(1 |

) |

|

Net cash used in investing activities |

|

— |

|

|

|

(1 |

) |

|

Cash flows from financing activities: |

|

|

|

|

|

|

|

|

Borrowings under the revolving credit facility |

|

106 |

|

|

|

85 |

|

|

Repayments under the revolving credit facility |

|

(114 |

) |

|

|

(72 |

) |

|

Other |

|

(2 |

) |

|

|

— |

|

|

Net cash provided by (used in) financing activities |

|

(10 |

) |

|

|

13 |

|

|

Effect of exchange rates on cash and cash equivalents |

|

1 |

|

|

|

— |

|

|

Net change in cash and cash equivalents |

|

(29 |

) |

|

|

(18 |

) |

|

Cash and cash equivalents, beginning of period |

|

116 |

|

|

|

98 |

|

|

Cash and cash equivalents, end of period |

$ |

87 |

|

|

$ |

80 |

|

|

Supplemental disclosure of cash flow information: |

|

|

|

|

|

|

|

|

Accrued purchases of property, plant and equipment |

$ |

1 |

|

|

$ |

— |

|

See notes to unaudited consolidated financial statements.

6

NOW INC.

CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY (UNAUDITED)

($ In millions)

|

|

|

|

Common Stock |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

Shares |

|

|

|

|

|

|

Additional |

|

|

Retained |

|

|

Accum. Other |

|

|

Total |

|

|||||

|

|

|

|

Outstanding |

|

|

Par |

|

|

Paid-In |

|

|

Earnings |

|

|

Comprehensive |

|

|

Stockholders’ |

|

||||||

|

|

|

|

(in thousands) |

|

|

Value |

|

|

Capital |

|

|

(Deficit) |

|

|

Income (Loss) |

|

|

Equity |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

December 31, 2017 |

|

|

|

108,030 |

|

|

$ |

1 |

|

|

$ |

2,019 |

|

|

$ |

(730 |

) |

|

$ |

(105 |

) |

|

$ |

1,185 |

|

|

Net income |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

2 |

|

|

|

— |

|

|

|

2 |

|

|

Stock-based compensation |

|

|

|

— |

|

|

|

— |

|

|

|

4 |

|

|

|

— |

|

|

|

— |

|

|

|

4 |

|

|

Vesting of restricted stock |

|

|

|

158 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

Shares withheld for taxes |

|

|

|

(47 |

) |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

Other comprehensive income |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

1 |

|

|

|

1 |

|

|

March 31, 2018 |

|

|

|

108,141 |

|

|

$ |

1 |

|

|

$ |

2,023 |

|

|

$ |

(728 |

) |

|

$ |

(104 |

) |

|

$ |

1,192 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

December 31, 2018 |

|

|

|

108,427 |

|

|

$ |

1 |

|

|

$ |

2,034 |

|

|

$ |

(678 |

) |

|

$ |

(143 |

) |

|

$ |

1,214 |

|

|

Net income |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

18 |

|

|

|

— |

|

|

|

18 |

|

|

Stock-based compensation |

|

|

|

— |

|

|

|

— |

|

|

|

4 |

|

|

|

— |

|

|

|

— |

|

|

|

4 |

|

|

Exercise of stock options |

|

|

|

70 |

|

|

|

— |

|

|

|

1 |

|

|

|

— |

|

|

|

— |

|

|

|

1 |

|

|

Vesting of restricted stock |

|

|

|

305 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

Shares withheld for taxes |

|

|

|

(93 |

) |

|

|

— |

|

|

|

(2 |

) |

|

|

— |

|

|

|

— |

|

|

|

(2 |

) |

|

Other comprehensive income |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

10 |

|

|

|

10 |

|

|

March 31, 2019 |

|

|

|

108,709 |

|

|

$ |

1 |

|

|

$ |

2,037 |

|

|

$ |

(660 |

) |

|

$ |

(133 |

) |

|

$ |

1,245 |

|

|

|

|

||||||||||||||||||||||||

|

See notes to unaudited consolidated financial statements. |

|

||||||||||||||||||||||||

7

NOW INC.

Notes to Unaudited Consolidated Financial Statements

1. Organization and Basis of Presentation

Nature of Operations

NOW Inc. (“NOW” or the “Company”) is a holding company headquartered in Houston, Texas that was incorporated in Delaware on November 22, 2013. NOW operates primarily under the DistributionNOW and Wilson Export brands. NOW is a global distributor of energy products as well as products for industrial applications through its locations in the U.S., Canada and internationally which are geographically positioned to serve the energy and industrial markets in over 80 countries. NOW’s energy product offerings are used in the oil and gas industry including upstream drilling and completion, exploration and production, midstream infrastructure development and downstream petroleum refining – as well as in other industries, such as chemical processing, power generation and industrial manufacturing operations. The industrial distribution portion of NOW’s business targets a diverse range of manufacturing and other facilities across numerous industries and end markets. NOW also provides supply chain management to drilling contractors, E&P operators, midstream operators, downstream energy and industrial manufacturing companies. NOW’s supplier network consists of thousands of vendors in approximately 40 countries.

Basis of Presentation

All significant intercompany transactions and accounts have been eliminated. The unaudited consolidated financial information included in this report has been prepared in accordance with accounting principles generally accepted in the United States (“GAAP”) for interim financial information and Article 10 of SEC Regulation S-X. The principles for interim financial information do not require the inclusion of all the information and footnotes required by generally accepted accounting principles for complete financial statements. Therefore, these financial statements should be read in conjunction with the financial statements included in the Company’s most recent Annual Report on Form 10-K. In the opinion of the Company’s management, the consolidated financial statements include all adjustments, all of which are of a normal recurring nature, necessary for a fair presentation of the results for the interim periods. The results of operations for the three months ended March 31, 2019 are not necessarily indicative of the results to be expected for the full year.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect reported and contingent amounts of assets and liabilities as of the date of the financial statements and reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Reclassification

Certain amounts in the prior periods presented have been reclassified to conform to the current period financial statement presentation. These reclassifications have no effect on previously reported results of operations.

Fair Value of Financial Instruments

The carrying amounts of cash and cash equivalents, receivables and payables approximated fair value because of the relatively short maturity of these instruments. Cash equivalents include only those investments having a maturity date of three months or less at the time of purchase. See Note 12 “Derivative Financial Instruments” for the fair value of derivative financial instruments.

Recently Issued Accounting Standards

In June 2016, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) 2016-13, Measurement of Credit Losses on Financial Instruments (Topic 326), which replaces the incurred loss impairment methodology in current GAAP with a methodology that reflects expected credit losses and requires consideration of a broader range of reasonable and supportable information to determine credit loss estimates. ASU 2016-13 requires entities to measure all expected credit losses for financial assets held at the reporting date based on historical experience, current conditions and reasonable and supportable forecasts. Entities will now use forward-looking information to better form their credit loss estimates. ASU 2016-13 is effective for annual and interim periods in fiscal years beginning after December 15, 2019, with early adoption permitted as of December 15, 2018, and requires the modified retrospective transition method. The Company is currently assessing the impact of ASU 2016-13 on its consolidated financial statements.

8

In August 2018, the FASB issued ASU 2018-13, Disclosure Framework-Changes to the Disclosure Requirements for Fair Value Measurement (Topic 820), which modified the disclosure requirements on fair value measurements. ASU 2018-13 is effective for annual and interim periods in fiscal years beginning after December 15, 2019, with early adoption permitted for removed or modified disclosures. The Company is currently assessing the impact of ASU 2018-13 on its consolidated financial statements.

Recently Adopted Accounting Standards

In February 2016, the Financial Accounting Standards Board (“FASB”) issued ASU 2016-02, Leases (Topic 842), which requires lessees to recognize a lease liability and a right-of-use (“ROU”) asset for all leases, including operating leases, with a term greater than twelve months in its balance sheets. In July 2018, the FASB issued ASU 2018-11, Targeted Improvements, which provided entities with an additional (and optional) transition method, allowing an entity to apply the new lease standard at the adoption date and to recognize a cumulative-effect adjustment to the opening balance of retained earnings in the period of adoption. On January 1, 2019, the Company adopted ASC 842 using the modified retrospective method allowed under ASU 2018-11. The Company has utilized the package of practical expedients permitted under the transition guidance within ASC 842 which, among other things, allow an entity to carry forward its historical lease classifications. The adoption of ASC 842 resulted in the recognition of $66 million of ROU assets, net of $1 million deferred rent, and $67 million of lease liabilities related to leases that were previously not required to be presented in the consolidated balance sheets. See Note 13 “Leases” for additional information.

2. Revenue

The Company’s primary source of revenue is the sale of energy products and an extensive selection of products for industrial applications based upon purchase orders or contracts with customers. The majority of revenue is recognized at a point in time once the Company has determined that the customer has obtained control over the product. Control is typically deemed to have been transferred to the customer when the product is shipped, delivered, or picked up by the customer. The Company does not grant extended payment terms. Revenue is recognized net of any taxes collected from customers, which are subsequently remitted to government authorities. Shipping and handling costs for product shipments occur prior to the customer obtaining control of the goods and are recorded in cost of products.

The amount of revenue recognized reflects the consideration to which the Company expects to be entitled to receive in exchange for products sold. Revenue is recorded at the transaction price net of estimates of variable consideration, which may include product returns, trade discounts and allowances. The Company accrues for variable consideration using the expected value method. Estimates of variable consideration are included in revenue to the extent that it is probable that a significant reversal in the amount of cumulative revenue recognized will not occur.

See Note 7 “Business Segments” for disaggregation of revenue by reporting segments. The Company believes this disaggregation best depicts how the nature, amount, timing and uncertainty of revenue and cash flows are affected by economic factors.

Remaining Performance Obligations

Remaining performance obligations represent the transaction price of firm orders for which work has not been performed on contracts with an original expected duration of more than one year. The Company’s contracts are predominantly short-term in nature with a contract term of one year or less. For those contracts, the Company has utilized the practical expedient in ASC Topic 606 exempting the Company from disclosure of the transaction price allocated to remaining performance obligations when the performance obligation is part of a contract that has an original expected duration of one year or less.

Receivables

Receivables are recorded when the Company has an unconditional right to consideration.

Contract Assets and Liabilities

Contract assets primarily consist of retainage amounts held as a form of security by customers until the Company satisfies its remaining performance obligations. As of March 31, 2019, contract assets were approximately $2 million and were included in receivables, net in the consolidated balance sheets. The Company generally accounts for the incremental costs of obtaining a contract as an expense when incurred if the amortization period of the asset that the entity otherwise would have been recognized is one year or less. These expenses were not material for the three months ended March 31, 2019.

9

Contract liabilities primarily consist of deferred revenues recorded when customer payments are received or due in advance of satisfying performance obligations, including amounts which are refundable, and other accrued customer liabilities. Revenue recognition is deferred to a future period until the Company completes its obligations contractually agreed with customers. The increase in contract liabilities for the quarter ended March 31, 2019 was primarily related to customer deposits of approximately $14 million, partially offset by approximately $9 million of revenue that was deferred at December 31, 2018.

3. Property, Plant and Equipment, net

Property, plant and equipment consist of (in millions):

|

|

|

Estimated Useful Lives |

|

March 31, 2019 |

|

|

December 31, 2018 |

|

||

|

Information technology assets |

|

1-7 Years |

|

$ |

45 |

|

|

$ |

45 |

|

|

Operating equipment (1) |

|

2-15 Years |

|

|

100 |

|

|

|

92 |

|

|

Buildings and land (2) |

|

5-35 Years |

|

|

99 |

|

|

|

99 |

|

|

Construction in progress |

|

|

|

|

1 |

|

|

|

— |

|

|

Total property, plant and equipment |

|

|

|

|

245 |

|

|

|

236 |

|

|

Less: accumulated depreciation |

|

|

|

|

(135 |

) |

|

|

(130 |

) |

|

Property, plant and equipment, net |

|

|

|

$ |

110 |

|

|

$ |

106 |

|

|

|

(1) |

Includes finance lease ROU assets. |

|

|

(2) |

Land has an indefinite life. |

4. Accrued Liabilities

Accrued liabilities consist of (in millions):

|

|

|

March 31, 2019 |

|

|

December 31, 2018 |

|

||

|

Compensation and other related expenses |

|

$ |

33 |

|

|

$ |

38 |

|

|

Contract liabilities |

|

|

33 |

|

|

|

29 |

|

|

Taxes (non-income) |

|

|

12 |

|

|

|

14 |

|

|

Current portion of operating lease liabilities |

|

|

22 |

|

|

|

— |

|

|

Other |

|

|

30 |

|

|

|

29 |

|

|

Total |

|

$ |

130 |

|

|

$ |

110 |

|

5. Debt

On April 30, 2018, the Company replaced its existing senior secured revolving credit facility and entered into a senior secured revolving credit facility (the “Credit Facility”) with a syndicate of lenders with Wells Fargo Bank, National Association serving as the administrative agent. The five-year Credit Facility provides for a $750 million global revolving credit facility (with a letter of credit subfacility of $60 million and a swing line subfacility of 10% of the facility amount), of which up to $100 million is available for the Company’s Canadian subsidiaries and $40 million for the Company’s UK subsidiaries. The Company has the right, subject to certain conditions, to increase the aggregate principal amount of commitments under the credit facility by $250 million. The obligations under the Credit Facility are secured by substantially all the assets of the Company and its subsidiaries. The Credit Facility contains customary covenants, representations and warranties and events of default. The Company will be required to maintain a fixed charge coverage ratio of at least 1.00:1.00 as of the end of each fiscal quarter if excess availability under the Credit Facility falls below the greater of 12.5% of the borrowing base or $60 million.

Borrowings under the Credit Facility will bear an interest rate at the Company’s option, at (i) the base rate plus an applicable margin based on the Company’s fixed charge coverage ratio (and if applicable, the Company’s leverage ratio); or (ii) the greater of LIBOR for the applicable interest period and zero, plus an applicable margin based on the Company’s fixed charge coverage ratio (and if applicable, the Company’s leverage ratio). The Credit Facility includes a commitment fee on the unused portion of commitments that ranges from 25 to 37.5 basis points. Commitment fees incurred during the period were included in other expense in the consolidated statements of operations.

10

Availability under the Credit Facility is determined by a borrowing base comprised of eligible receivables and eligible inventory in the U.S and Canada. As of March 31, 2019, the Company borrowed $124 million against the Credit Facility and had approximately $444 million in availability (as defined in the Credit Facility) resulting in the excess availability (as defined in the Credit Facility) of 77% subject to certain limitations. The Company was not obligated to pay back the borrowing against the Credit Facility until the expiration date, as such the outstanding borrowing is classified as long-term debt in the consolidated balance sheets.

The Company issued $7 million in letters of credit under the Credit Facility primarily for casualty insurance expiring in July 2019.

6. Accumulated Other Comprehensive Income (Loss)

The components of accumulated other comprehensive income (loss) are as follows (in millions):

|

|

|

Foreign |

|

|

|

|

|

Currency |

|

|

|

|

|

Translation |

|

|

|

|

|

Adjustments |

|

|

|

Balance at December 31, 2018 |

|

$ |

(143 |

) |

|

Other comprehensive income |

|

|

10 |

|

|

Balance at March 31, 2019 |

|

$ |

(133 |

) |

The Company’s reporting currency is the U.S. dollar. A majority of the Company’s international entities in which there is a substantial investment have the local currency as their functional currency. As a result, foreign currency translation adjustments resulting from the process of translating the entities’ financial statements into the reporting currency are reported in other comprehensive income or loss in accordance with ASC Topic 830, “Foreign Currency Matters.”

7. Business Segments

Operating results by reportable segment are as follows (in millions):

|

|

Three Months Ended March 31, |

|

|||||

|

|

2019 |

|

|

2018 |

|

||

|

Revenue: |

|

|

|

|

|

|

|

|

United States |

$ |

600 |

|

|

$ |

562 |

|

|

Canada |

|

86 |

|

|

|

102 |

|

|

International |

|

99 |

|

|

|

100 |

|

|

Total revenue |

$ |

785 |

|

|

$ |

764 |

|

|

Operating profit: |

|

|

|

|

|

|

|

|

United States |

$ |

19 |

|

|

$ |

3 |

|

|

Canada |

|

2 |

|

|

|

4 |

|

|

International |

|

2 |

|

|

|

— |

|

|

Total operating profit |

$ |

23 |

|

|

$ |

7 |

|

|

Operating profit % of revenue: |

|

|

|

|

|

|

|

|

United States |

|

3.2 |

% |

|

|

0.5 |

% |

|

Canada |

|

2.3 |

% |

|

|

3.9 |

% |

|

International |

|

2.0 |

% |

|

|

0.0 |

% |

|

Total operating profit % |

|

2.9 |

% |

|

|

0.9 |

% |

8. Income Taxes

The effective tax rate for the three months ended March 31, 2019 was 6.5% compared to 24.1% for the same period in 2018. Compared to the U.S. statutory rate, the effective tax rate was impacted by recurring items, such as differing tax rates on income earned in foreign jurisdictions that is permanently reinvested, nondeductible expenses, state income taxes and the change in valuation allowance recorded against deferred tax assets. Due to the continuing uncertainty in the Company’s industry, the Company continues to utilize the method of recording income taxes on a year-to-date effective tax rate for the three months ended March 31, 2019. The Company will evaluate its use of this method each quarter until such time as a return to the annualized estimated effective tax rate method is deemed appropriate.

11

The Company is subject to taxation in the United States, various states and foreign jurisdictions. The Company has significant operations in the United States and Canada and to a lesser extent in various other international jurisdictions. Tax years that remain subject to examination by major tax jurisdictions vary by legal entity, but are generally open in the U.S. for the tax years ending after 2014 and outside the U.S. for the tax years ending after 2012.

9. Earnings Per Share (“EPS”)

For the three months ended March 31, 2019 and 2018, approximately 3 million and 6 million, respectively, of potentially dilutive shares were excluded from the computation of diluted earnings per share due to their antidilutive effect.

Basic and diluted earnings per share follows (in millions, except share data):

|

|

Three Months Ended March 31, |

|

|||||

|

|

2019 |

|

|

2018 |

|

||

|

Numerator: |

|

|

|

|

|

|

|

|

Net income attributable to the Company |

$ |

18 |

|

|

$ |

2 |

|

|

Less: net income attributable to participating securities |

|

— |

|

|

|

— |

|

|

Net income attributable to the Company's stockholders |

$ |

18 |

|

|

$ |

2 |

|

|

Denominator: |

|

|

|

|

|

|

|

|

Weighted average basic common shares outstanding |

|

108,556,369 |

|

|

|

108,074,718 |

|

|

Effect of dilutive securities |

|

504,426 |

|

|

|

98,041 |

|

|

Weighted average diluted common shares outstanding |

|

109,060,795 |

|

|

|

108,172,759 |

|

|

Earnings per share attributable to the Company's stockholders: |

|

|

|

|

|

|

|

|

Basic |

$ |

0.17 |

|

|

$ |

0.02 |

|

|

Diluted |

$ |

0.16 |

|

|

$ |

0.02 |

|

Under ASC Topic 260, “Earnings Per Share”, the two-class method requires a portion of net income attributable to the Company to be allocated to participating securities, which are unvested awards of share-based payments with non-forfeitable rights to receive dividends or dividend equivalents, if declared. For the periods that the Company recognized net income, net income attributable to these participating securities was excluded from net income attributable to the Company’s stockholders in the numerator of the earnings per share computation.

10. Stock-based Compensation and Outstanding Awards

The Company has a stock-based compensation plan known as the NOW Inc. Long-Term Incentive Plan (the “Plan”). Under the Plan, the Company’s employees are eligible to be granted stock options, restricted stock awards (“RSAs”), restricted stock units (“RSUs”), and performance stock awards (“PSAs”).

For the three months ended March 31, 2019, the Company granted 521,157 stock options with a weighted average fair value of $6.02 per share and 191,995 shares of RSAs and RSUs with a weighted average fair value of $15.30 per share. In addition, the Company granted PSAs to senior management employees with potential payouts varying from zero to 331,372 shares. These options vest over a three-year period from the grant date on a straight-line basis over the requisite service period for each separately vesting portion of the award as if the award was, in-substance, multiple awards. The RSAs and RSUs vest on the third anniversary of the date of grant. The PSAs can be earned based on performance against established metrics over a three-year performance period. The PSAs are divided into three independent parts that are subject to separate performance metrics: (i) one-half of the PSAs have a Total Shareholder Return (“TSR”) metric, (ii) one-quarter of the PSAs have an EBITDA metric, and (iii) one-quarter of the PSAs have a Return on Capital Employed (“ROCE”) metric.

Performance against the TSR metric is determined by comparing the performance of the Company’s TSR with the TSR performance of designated peer companies for the three-year performance period. Performance against the EBITDA metric is determined by comparing the performance of the Company’s actual EBITDA average for each of the three-years of the performance period against the EBITDA metrics set by the Company’s Compensation Committee of the Board of Directors. Performance against the ROCE metric is determined by comparing the performance of the Company’s actual ROCE average for each of the three-years of the performance period against the ROCE metrics set by the Company’s Compensation Committee of the Board of Directors.

Stock-based compensation expense totaled $4 million for the three months ended March 31 in both 2019 and 2018.

12

11. Commitments and Contingencies

The Company is involved in various claims, regulatory agency audits and pending or threatened legal actions involving a variety of matters. The Company has also assessed the potential for additional losses above the amounts accrued as well as potential losses for matters that are not probable, but are reasonably possible. The total potential loss on these matters cannot be determined; however, in the Company’s opinion, any ultimate liability, to the extent not otherwise recorded or accrued for, will not materially affect the Company’s financial position, cash flow or results of operations. These estimated liabilities are based on the Company’s assessment of the nature of these matters, their progress toward resolution, the advice of legal counsel and outside experts as well as management’s intention and experience.

The Company’s business is affected both directly and indirectly by governmental laws and regulations relating to the oilfield service industry in general, as well as by environmental and safety regulations that specifically apply to the Company’s business. Although the Company has not incurred material costs in connection with its compliance with such laws, there can be no assurance that other developments, such as new environmental laws, regulations and enforcement policies hereunder may not result in additional, presently unquantifiable, costs or liabilities to the Company. The Company does not accrue for contingent losses that, in its judgment, are considered to be reasonably possible, but not probable. Estimating reasonably possible losses also requires the analysis of multiple possible outcomes that often depend on judgments about potential actions by third parties.

The Company maintains credit arrangements with several banks providing for short-term borrowing capacity, overdraft protection and other bonding requirements. As of March 31, 2019, the Company was contingently liable for approximately $10 million of outstanding standby letters of credit and surety bonds. The Company does not believe, based on historical experience and information currently available, that it is probable that any amounts will be required to be paid.

12. Derivative Financial Instruments

The Company is exposed to certain risks relating to its ongoing business operations. The primary risk managed by using derivative instruments is foreign currency exchange rate risk. The Company has entered into certain financial derivative instruments to manage this risk.

The derivative financial instruments the Company has entered into are forward exchange contracts which have terms of less than one year to economically hedge foreign currency exchange rate risk on recognized non-functional currency monetary accounts. The purpose of the Company’s foreign currency economic hedging activities is to economically hedge the Company’s risk from changes in the fair value of non-functional currency denominated monetary accounts.

The Company records all derivative financial instruments at their fair value in its consolidated balance sheets. None of the derivative financial instruments that the Company holds are designated as either a fair value hedge or cash flow hedge and the gain or loss on the derivative instrument is recorded in earnings. The Company has determined that the fair value of its derivative financial instruments are computed using level 2 inputs (inputs other than quoted prices in active markets for identical assets and liabilities that are observable either directly or indirectly for substantially the full term of the asset or liability) in the fair value hierarchy as the fair value is based on publicly available foreign exchange rates at each financial reporting date. As of March 31, 2019, and December 31,

2018, the fair value of the Company’s foreign currency forward contracts totaled an asset of less than $1 million, respectively, and is included in prepaid and other current assets in the consolidated balance sheets; a liability of less than $1 million, respectively, and is included in other current liabilities in the consolidated balance sheets.

For the three months ended March 31, 2019 and 2018, the Company recorded a loss of less than $1 million and a gain of less than $1 million, respectively, related to changes in fair value. All gains and losses are included in other expense in the consolidated statements of operations. The notional principal associated with those contracts was $21 million and $20 million as of March 31, 2019 and December 31, 2018, respectively.

As of March 31, 2019, the Company’s financial instruments do not contain any credit-risk-related or other contingent features that could cause accelerated payments when the Company’s financial instruments are in net liability positions. The Company does not use derivative financial instruments for trading or speculative purposes.

13

13. Leases

The Company leases certain facilities, vehicles and equipment. The Company determines if an arrangement contains a lease at contract inception and recognizes ROU assets and lease liabilities for leases with terms greater than twelve months. Leases with an initial term of twelve months or less are accounted for as short-term leases and are not recognized in the balance sheet. Operating fixed lease expenses and finance lease depreciation expense are recognized on a straight-line basis over the lease term. Variable lease payments which cannot be determined at the lease commencement date, such as reimbursement of lessor expenses, are not included in the ROU assets or lease liabilities.

Many leases include both lease and non-lease components which are primarily related to management services provided by lessors for the underlying assets. The Company elected the practical expedient to account for lease and non-lease components as a single lease component for all leases as well as the practical expedient that allows to carry forward the historical lease classifications. For all new and modified leases entered into after the adoption of ASC 842, the Company reassesses the lease classification and lease term on the effective date of modification. Lease term includes renewal periods if the Company is reasonably certain to exercise any renewal options per the lease contract. The Company’s leases do not contain any material residual value guarantees or restrictive covenants. The Company subleases certain real estate to third parties, however, this activity is not material.

As most leases do not have readily determinable implicit rates, the Company estimates the incremental borrowing rates based on prevailing financial market conditions, comparable companies and credit analysis and management judgments to determine the present values of its lease payments. The Company also applies the portfolio approach to account for leases with similar terms. As of March 31, 2019, the weighted-average remaining lease terms were approximately 4 years for operating leases and 7 years for finance leases. The weighted-average discount rates were 6.1% for operating leases and 5.8% for finance leases.

Supplemental balance sheet information (in millions):

|

|

Classification |

March 31, 2019 |

|

|

|

Assets |

|

|

|

|

|

Operating |

Other assets |

$ |

63 |

|

|

Finance |

Property, plant and equipment, net |

|

7 |

|

|

Total ROU assets |

|

$ |

70 |

|

|

Liabilities |

|

|

|

|

|

Current |

|

|

|

|

|

Operating |

Accrued liabilities |

$ |

22 |

|

|

Finance |

Other current liabilities |

|

3 |

|

|

Long-term |

|

|

|

|

|

Operating |

Long-term operating lease liabilities |

|

40 |

|

|

Finance |

Other long-term liabilities |

|

5 |

|

|

Total lease liabilities |

|

$ |

70 |

|

Components of lease expense (in millions):

|

|

Classification |

Three Months Ended March 31, 2019 |

|

|

|

Operating lease cost |

Warehousing, selling and administrative |

$ |

8 |

|

|

Finance lease ROU asset depreciation (1) |

Warehousing, selling and administrative |

|

1 |

|

|

Short-term lease cost |

Warehousing, selling and administrative |

|

2 |

|

|

Variable lease cost |

Warehousing, selling and administrative |

|

1 |

|

|

|

(1) |

Included in depreciation and amortization in the consolidated statement of cash flows. Interest on finance lease liabilities is less than $1 million. |

14

Supplemental cash flow information (in millions):

|

|

Three Months Ended March 31, 2019 |

|

|

|

Cash paid for amounts included in the measurement of lease liabilities |

|

|

|

|

Operating cash flows from operating leases |

$ |

8 |

|

|

Financing cash flows from finance leases (1) |

|

1 |

|

|

ROU assets obtained in exchange for new lease liabilities |

|

|

|

|

Operating |

|

4 |

|

|

Finance |

|

8 |

|

|

|

(1) |

Interest payments from finance lease liabilities is less than $1 million. |

Maturity of lease liabilities as of March 31, 2019 were as follows (in millions):

|

|

Operating Lease |

|

Finance Lease |

|

||

|

2019 |

$ |

19 |

|

$ |

2 |

|

|

2020 |

|

20 |

|

|

3 |

|

|

2021 |

|

12 |

|

|

2 |

|

|

2022 |

|

8 |

|

|

1 |

|

|

2023 |

|

6 |

|

|

— |

|

|

Thereafter |

|

4 |

|

|

2 |

|

|

Total future lease payments |

|

69 |

|

|

10 |

|

|

Less: interest |

|

(7 |

) |

|

(2 |

) |

|

Present value of lease liabilities |

$ |

62 |

|

$ |

8 |

|

15

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Forward-Looking Statements

Some of the information in this document contains, or has incorporated by reference, forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Statements that are not historical facts, including statements about our beliefs and expectations, are forward-looking statements. Forward-looking statements typically are identified by use of terms such as “may,” “believe,” “anticipate,” “expect,” “plan,” “predict,” “estimate,” “will be” or other similar words and phrases, although some forward-looking statements are expressed differently. You should be aware that our actual results could differ materially from results anticipated in the forward-looking statements due to a number of factors, including, but not limited to, changes in oil and gas prices, changes in the energy markets, customer demand for our products, significant changes in the size of our customers, difficulties encountered in integrating mergers and acquisitions, general volatility in the capital markets, changes in applicable government regulations, increased borrowing costs, competition between us and our former parent company, NOV, the triggering of rights and obligations in connection with our spin-off and separation from NOV or any litigation arising out of or related thereto, impairments in goodwill or other intangible assets and worldwide economic activity. You should also consider carefully the statements under “Risk Factors,” as disclosed in our Form 10-K, which address additional factors that could cause our actual results to differ from those set forth in the forward-looking statements. Given these uncertainties, current or prospective investors are cautioned not to place undue reliance on any such forward-looking statements. We undertake no obligation to update any such factors or forward-looking statements to reflect future events or developments.

Company Overview

We are a global distributor to the oil and gas and industrial markets with a legacy of over 150 years. We operate primarily under the DistributionNOW and Wilson Export brands. Through our network of approximately 260 locations and approximately 4,500 employees worldwide, we stock and sell a comprehensive offering of energy products as well as an extensive selection of products for industrial applications. Our energy product offering is consumed throughout all sectors of the oil and gas industry – from upstream drilling and completion, exploration and production (“E&P”), midstream infrastructure development to downstream petroleum refining – as well as in other industries, such as chemical processing, mining, utilities and industrial manufacturing operations. The industrial distribution end markets include manufacturing, aerospace, automotive, refineries and engineering and construction firms. We also provide supply chain and materials management solutions to the same markets where we sell products.

Our global product offering includes consumable maintenance, repair and operating (“MRO”) supplies, pipe, valves, fittings, flanges, gaskets, fasteners, electrical, instrumentation, artificial lift, pumping solutions, valve actuation and modular process, measurement and control equipment. We also offer warehouse and inventory management solutions as part of our supply chain and materials management offering. We have developed expertise in providing application systems, work processes, parts integration, optimization solutions and after-sales support.

Our solutions include outsourcing the functions of procurement, inventory and warehouse management, logistics, point of issue technology, project management, business process and performance metrics reporting. These solutions allow us to leverage the infrastructure of our SAP™ Enterprise Resource Planning (“ERP”) system and other technologies to streamline our customers’ purchasing process, from requisition to procurement to payment, by digitally managing workflow, improving approval routing and providing robust reporting functionality.

We support land and offshore operations for all the major oil and gas producing regions around the world through our network of locations. Our key markets, beyond North America, include Latin America, the North Sea, the Middle East, Asia Pacific and the Former Soviet Union (“FSU”). Products sold through our locations support greenfield expansion upstream capital projects, midstream infrastructure and transmission and MRO consumables used in day-to-day production. We provide downstream energy and industrial products for petroleum refining, chemical processing, LNG terminals, power generation utilities and industrial manufacturing operations and customer on-site locations.

We stock or sell more than 300,000 stock keeping units (“SKUs”) through our branch network. Our supplier network consists of thousands of vendors in approximately 40 countries. From our operations in over 20 countries we sell to customers operating in approximately 80 countries. The supplies and equipment stocked by each of our branches are customized to meet varied and changing local customer demands. The breadth and scale of our offering enhances our value proposition to our customers, suppliers and shareholders.

16

We employ advanced information technologies, including a common ERP platform across most of our business, to provide complete procurement, materials management and logistics coordination to our customers around the globe. Having a common ERP platform allows immediate visibility into the Company’s inventory assets, operations and financials worldwide, enhancing decision making and efficiency.

Demand for our products is driven primarily by the level of oil and gas drilling, completions, servicing, production, transmission, refining and petrochemical and industrial manufacturing activities. It is also influenced by the global supply and demand for energy, the economy in general and geopolitics. Several factors drive spending, such as investment in energy infrastructure, the North American conventional and shale plays, market expectations of future developments in the oil, natural gas, liquids, refined products, petrochemical, plant maintenance and other industrial, manufacturing and energy sectors.

We have expanded globally, through acquisitions and organic investments, into Australia, Azerbaijan, Brazil, Canada, China, Colombia, Egypt, England, India, Indonesia, Kazakhstan, Kuwait, Mexico, Netherlands, Norway, Oman, the Philippines, Russia, Saudi Arabia, Scotland, Singapore, the United Arab Emirates and the United States.

Summary of Reportable Segments

We operate through three reportable segments: United States (“U.S.”), Canada and International. The segment data included in our Management’s Discussion and Analysis (“MD&A”) are presented on a basis consistent with our internal management reporting. Segment information appearing in Note 7 “Business Segments” of the notes to the unaudited consolidated financial statements (Part I, Item 1 of this Form 10-Q) is also presented on this basis.

United States

We have approximately 170 locations in the U.S., which are geographically positioned to best serve the upstream, midstream and downstream energy and industrial markets.

We offer higher value solutions in key product lines in the U.S. which broaden and deepen our customer relationships and related product line value. Examples of these include artificial lift, pumps, valves and valve actuation, process equipment, fluid transfer products, measurement and controls, along with many other products required by our customers, which enable them to focus on their core business while we manage their supply chain. We also provide additional value to our customers through the design, assembly, fabrication and optimization of products and equipment essential to the safe and efficient production, transportation and processing of oil and gas and industrial manufacturing.

Canada

We have a network of approximately 55 locations in the Canadian oilfield, predominantly in the oil rich provinces of Alberta and Saskatchewan in Western Canada. Our Canada segment primarily serves the energy exploration, production, mining and drilling business, offering customers many of the same products and value-added solutions that we perform in the U.S. In Canada, we also provide training for, and supervise the installation of, jointed and spoolable composite pipe. This product line is supported by inventory and product and installation expertise to serve our customers.

International

We operate in approximately 20 countries and serve the needs of our international customers from approximately 35 locations outside of the U.S. and Canada, which are strategically located in major oil and gas development areas. Our approach in these markets is similar to our approach in North America, as our customers turn to us to provide inventory and support closer to their drilling and exploration activities. Our long legacy of operating in many international regions, combined with significant expansion into several key markets, provides a competitive advantage as few of our competitors have a presence in most of the global energy producing regions.

17

Basis of Presentation

All significant intercompany transactions and accounts have been eliminated. The unaudited consolidated financial information included in this report has been prepared in accordance with GAAP for interim financial information and Article 10 of SEC Regulation S-X. The principles for interim financial information do not require the inclusion of all the information and footnotes required by generally accepted accounting principles for complete financial statements. Therefore, these financial statements should be read in conjunction with the financial statements included in the Company’s most recent Annual Report on Form 10-K. In the opinion of our management, the consolidated financial statements include all adjustments, all of which are of a normal recurring nature, necessary for a fair presentation of the results for the interim periods. The results of operations for the three months ended March 31, 2019 are not necessarily indicative of the results to be expected for the full year.

Operating Environment Overview

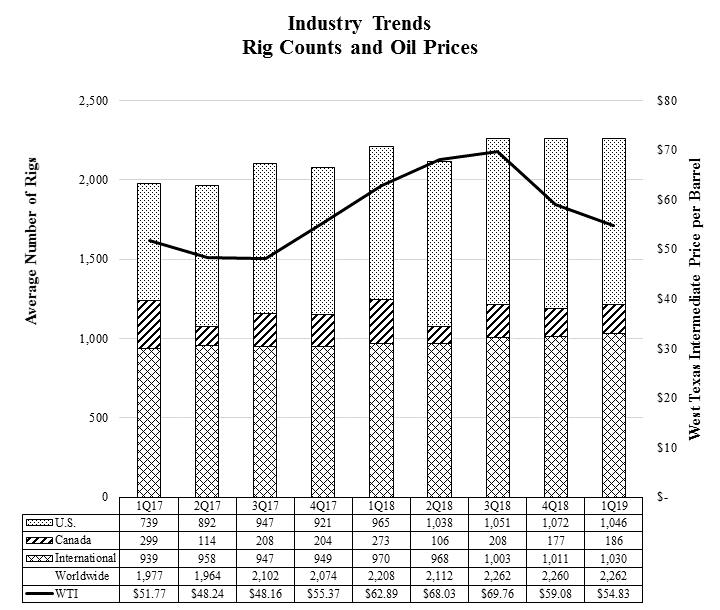

Our results are dependent on, among other factors, the level of worldwide oil and gas drilling and completions, well remediation activity, crude oil and natural gas prices, capital spending by operators, oilfield service companies and contractors and worldwide oil and gas inventory levels. Key industry indicators for the first quarter of 2019 and 2018 and the fourth quarter of 2018 include the following:

|

|

|

|

|

|

|

|

|

|

|

% |

|

|

|

|

|

|

% |

|

||

|

|

|

|

|

|

|

|

|

|

|

1Q19 v |

|

|

|

|

|

|

1Q19 v |

|

||

|

|

|

1Q19* |

|

|

1Q18* |

|

|

1Q18 |

|

|

4Q18* |

|

|

4Q18 |

|

|||||

|

Active Drilling Rigs: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

U.S. |

|

|

1,046 |

|

|

|

965 |

|

|

|

8.4 |

% |

|

|

1,072 |

|

|

|

(2.4 |

%) |

|

Canada |

|

|

186 |

|

|

|

273 |

|

|

|

(31.9 |

%) |

|

|

177 |

|

|

|

5.1 |

% |

|

International |

|

|

1,030 |

|

|

|

970 |

|

|

|

6.2 |

% |

|

|

1,011 |

|

|

|

1.9 |

% |

|

Worldwide |

|

|

2,262 |

|

|

|

2,208 |

|

|

|

2.4 |

% |

|

|

2,260 |

|

|

|

0.1 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

West Texas Intermediate Crude Prices (per barrel) |

|

$ |

54.83 |

|

|

$ |

62.89 |

|

|

|

(12.8 |

%) |

|

$ |

59.08 |

|

|

|

(7.2 |

%) |

|

Natural Gas Prices ($/MMBtu) |

|

$ |

2.92 |

|

|

$ |

3.08 |

|

|

|

(5.2 |

%) |

|

$ |

3.80 |

|

|

|

(23.2 |

%) |

|

Hot-Rolled Coil Prices (steel) ($/short ton) |

|

$ |

715.33 |

|

|

$ |

721.03 |

|

|

|

(0.8 |

%) |

|

$ |

818.50 |

|

|

|

(12.6 |

%) |

|

* |

Averages for the quarters indicated. See sources on following page. |

18

The following table details the U.S., Canadian and international rig activity and West Texas Intermediate oil prices for the past nine quarters ended March 31, 2019:

Sources: Rig count: Baker Hughes, Inc. (www.bhge.com); West Texas Intermediate Crude and Natural Gas Prices: Department of Energy, Energy Information Administration (www.eia.doe.gov); Hot-Rolled Coil Prices: SteelBenchmarker™ Hot Roll Coil USA (www.steelbenchmarker.com)

The worldwide quarterly average rig count increased 0.1% (from 2,260 rigs to 2,262 rigs) and the U.S. declined 2.4% (from 1,072 rigs to 1,046 rigs) in the first quarter of 2019 compared to the fourth quarter of 2018. The average price per barrel of West Texas Intermediate Crude declined 7.2% (from $59.08 per barrel to $54.83 per barrel) and natural gas prices declined 23.2% (from $3.80 per MMBtu to $2.92 per MMBtu) in the first quarter of 2019 compared to the fourth quarter of 2018. The average price per short ton of Hot-Rolled Coil declined 12.6% (from $818.50 per short ton to $715.33 per short ton) in the first quarter of 2019 compared to the fourth quarter of 2018.

U.S. rig count at April 12, 2019 was 1,022 rigs, down 24 rigs compared to the first quarter of 2019 average of 1,046 rigs. The price for West Texas Intermediate Crude was $63.86 per barrel at April 12, 2019, up 16.5% from the first quarter average of 2019. The price for natural gas was $2.75 per MMBtu at April 12, 2019, down 5.8% from the first quarter average of 2019. The price for Hot-Rolled Coil was $701.00 per short ton at April 8, 2019, down 2.0% from the first quarter average of 2019.

19

Executive Summary

For the three months ended March 31, 2019, the Company generated net income of $18 million on $785 million in revenue. Revenue increased $21 million or 2.7% for the three months ended March 31, 2019 when compared to the corresponding period of 2018. For the three months ended March 31, 2019, net income improved $16 million when compared to the corresponding period of 2018.

For the three months ended March 31, 2019, the Company generated an operating profit of $23 million or 2.9% of revenue compared to $7 million or 0.9% of revenue for the corresponding period of 2018.

Outlook

Our outlook for the Company remains tied to global rig count and oil and gas spending, particularly in North America. Oil prices and U.S. oil storage levels are primary catalysts determining U.S. rig activity.

In 2019, activity should fluctuate as the industry addresses the vagaries of an over- or under-supplied market. Recent oil price volatility has created uncertainty around global exploration and production activity, with many customers still reassessing their budgets for the remainder of the year.

We will continue to advance our strategic goals and manage the Company based on market conditions. We will persist in optimizing our operations, scaling up or down to market activity as appropriate. We believe that our management history, paired with our resources and low capital expenditure requirements, enable us to maximize new opportunities.

20

Results of Operations

Operating results by reportable segment are as follows (in millions):

|

|

Three Months Ended March 31, |

|

|||||

|

|

2019 |

|

|

2018 |

|

||

|

Revenue: |

|

|

|

|

|

|

|

|

United States |

$ |

600 |

|

|

$ |

562 |

|

|

Canada |

|

86 |

|

|

|

102 |

|

|

International |

|

99 |

|

|

|

100 |

|

|

Total revenue |

$ |

785 |

|

|

$ |

764 |

|

|

Operating profit: |

|

|

|

|

|

|

|

|

United States |

$ |

19 |

|

|

$ |

3 |

|

|

Canada |

|

2 |

|

|

|

4 |

|

|

International |

|

2 |

|

|

|

— |

|

|

Total operating profit |

$ |

23 |

|

|

$ |

7 |

|

|

Operating profit % of revenue: |

|

|

|

|

|

|

|

|

United States |

|

3.2 |

% |

|

|

0.5 |

% |

|

Canada |

|

2.3 |

% |

|

|

3.9 |

% |

|

International |

|

2.0 |

% |

|

|

0.0 |

% |

|

Total operating profit % |

|

2.9 |

% |

|

|

0.9 |

% |

United States

For the three months ended March 31, 2019, revenue was $600 million, an increase of $38 million or 6.8% when compared to the corresponding period of 2018. This increase was primarily driven by a year over year improvement in U.S. rig count.

For the three months ended March 31, 2019, the U.S. generated an operating profit of $19 million or 3.2% of revenue, an improvement of $16 million when compared to the corresponding period of 2018. For the three months ended March 31, 2019, operating profit improved primarily due to the increases in volume discussed above, coupled with product margin gains.

Canada

For the three months ended March 31, 2019, revenue was $86 million, a decline of $16 million or 15.7% when compared to the corresponding period of 2018. For the three months ended March 31, 2019, the decrease was driven by a year over year decline in Canadian rig count activity, coupled with an unfavorable foreign exchange rate impact.

For the three months ended March 31, 2019, Canada generated an operating profit of $2 million or 2.3% of revenue, a decline of $2 million when compared to the corresponding period of 2018. For the three months ended March 31, 2019, operating profit decreased primarily due to the decline in revenue discussed above, offset by reduced operating expenses.

International

For the three months ended March 31, 2019, revenue was $99 million, a decline of $1 million or 1.0% when compared to the corresponding period of 2018. For the three months ended March 31, 2019, the decrease was driven by an unfavorable foreign exchange rate impact.

For the three months ended March 31, 2019, the international segment generated an operating profit of $2 million or 2.0% of revenue, an increase of $2 million when compared to the corresponding period of 2018. For the three months ended March 31, 2019, operating profit improved due to reduced bad debt charges in the period, partially offset by increased inventory charges.

21

Cost of products

For the three months ended March 31, 2019, cost of products was $627 million compared to $616 million for the corresponding period in 2018. The increase was primarily due to increases in revenue in the period. Cost of products includes the cost of inventory sold and related items, such as vendor consideration, inventory allowances, amortization of intangibles and inbound and outbound freight.

Warehousing, selling and administrative

For the three months ended March 31, 2019, warehousing, selling and administrative expenses were $135 million compared to $141 million for the corresponding period of 2018. Operating expenses declined due to reduced bad debt charges. Warehousing, selling and administrative expenses include general corporate expenses, depreciation and branch, distribution center and regional expenses (including costs such as compensation, benefits and rent).

Other expense

For the three months ended March 31, 2019 and 2018, other expense was $4 million for both periods. These charges were mainly attributable to interest and bank charges associated with the credit facilities.

The effective tax rate for the three months ended March 31, 2019 was 6.5% compared to 24.1% for the same period in 2018. Compared to the U.S. statutory rate, the effective tax rate was impacted by recurring items, such as differing tax rates on income earned in foreign jurisdictions that is permanently reinvested, nondeductible expenses, state income taxes and the change in valuation allowance recorded against deferred tax assets. The change in the effective tax rate when compared to the corresponding period in 2018 was primarily driven by an increase in income before taxes in 2019.

22

Non-GAAP Financial Measure and Reconciliation

In an effort to provide investors with additional information regarding our results as determined by GAAP, we disclose a non-GAAP financial measure in our quarterly earnings press releases and other public disclosures. The primary non-GAAP financial measure we focus on is earnings before interest, taxes, depreciation and amortization, excluding other costs (“EBITDA excluding other costs”). This financial measure excludes the impact of certain amounts as further identified below and has not been calculated in accordance with GAAP. A reconciliation of this non-GAAP financial measure to its most comparable GAAP financial measure is included below.

We use this non-GAAP financial measure internally to evaluate and manage the Company’s operations because we believe it provides useful supplemental information regarding the Company’s ongoing economic performance. We have chosen to provide this information to investors to enable them to perform more meaningful comparisons of operating results.

The following table sets forth the reconciliation of EBITDA excluding other costs to its most comparable GAAP financial measure (in millions):

EBITDA excluding other costs

|

|

|

Three Months Ended March 31, |

|

|||||

|

|

|

2019 |

|

|

2018 |

|

||

|

GAAP net income (1) |

|

$ |

18 |

|

|

$ |

2 |

|

|

Interest, net |

|

|

2 |

|

|

|

2 |

|

|

Income tax provision |

|

|

1 |

|

|

|

1 |

|

|

Depreciation and amortization |

|

|

10 |

|

|

|

11 |

|

|

Other costs (2) |

|

|

— |

|

|

|

— |

|

|