DNOW Inc. - Annual Report: 2020 (Form 10-K)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark one)

|

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE YEAR ENDED DECEMBER 31, 2020

OR

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number 001-36325

NOW INC.

(Exact name of registrant as specified in its charter)

|

Delaware |

|

46-4191184 |

|

(State of Incorporation) |

|

(IRS Identification No.) |

7402 North Eldridge Parkway, Houston, Texas 77041

(Address of principal executive offices)

(281) 823-4700

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

|

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

|

|

|

Common Stock, par value $0.01 |

|

DNOW |

|

New York Stock Exchange |

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15 (d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

☒ |

Large accelerated filer |

|

|

|

|

☐ |

Accelerated filer |

|

☐ |

Non-accelerated filer |

|

|

|

|

☐ |

Smaller reporting company |

|

|

|

|

|

|

|

☐ |

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of common stock held by non-affiliates of the registrant as of June 30, 2020 was $0.9 billion. As of February 10, 2021, there were 109,951,610 shares of the Company’s common stock (excluding 574,022 unvested restricted shares) outstanding.

Documents Incorporated by Reference

Portions of the Proxy Statement in connection with the 2021 Annual Meeting of Stockholders are incorporated in Part III of this report.

NOW INC.

TABLE OF CONTENTS

|

|

|

|

|

Page |

|

|

|

|

|

|

|

|

|

|

||

|

ITEM 1. |

|

|

3 |

|

|

|

|

|

||

|

ITEM 1A. |

|

|

10 |

|

|

|

|

|

||

|

ITEM 1B. |

|

|

22 |

|

|

|

|

|

|

|

|

ITEM 2. |

|

|

22 |

|

|

|

|

|

||

|

ITEM 3. |

|

|

22 |

|

|

|

|

|

||

|

ITEM 4. |

|

|

22 |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

||

|

ITEM 5. |

|

|

23 |

|

|

|

|

|

||

|

ITEM 6. |

|

|

24 |

|

|

|

|

|

|

|

|

ITEM 7. |

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

|

25 |

|

|

|

|

||

|

ITEM 7A. |

|

|

37 |

|

|

|

|

|

||

|

ITEM 8. |

|

|

37 |

|

|

|

|

|

||

|

ITEM 9. |

|

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE |

|

38 |

|

|

|

|

||

|

ITEM 9A. |

|

|

38 |

|

|

|

|

|

||

|

ITEM 9B. |

|

|

38 |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

||

|

ITEM 10. |

|

|

39 |

|

|

|

|

|

||

|

ITEM 11. |

|

|

39 |

|

|

|

|

|

||

|

ITEM 12. |

|

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS |

|

39 |

|

|

|

|

||

|

ITEM 13. |

|

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE |

|

39 |

|

|

|

|

||

|

ITEM 14. |

|

|

39 |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

||

|

ITEM 15. |

|

|

40 |

|

2

FORM 10-K

Note About Forward-Looking Statements

This report includes estimates, projections, statements relating to our business plans, objectives and expected operating results that are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Forward-looking statements may appear throughout this report, including the following sections: “Business,” “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” These forward-looking statements generally are identified by the words “may,” “believe,” “anticipate,” “expect,” “plan,” “predict,” “estimate,” “will be” or other similar words and phrases. Forward-looking statements are based on current expectations and assumptions that are subject to risks and uncertainties that may cause actual results to differ materially. We describe risks and uncertainties that could cause actual results and events to differ materially in “Risk Factors” (Part I, Item 1A of this Form 10-K), “Management’s Discussion and Analysis of Financial Condition and Results of Operations” (Part II, Item 7) and “Quantitative and Qualitative Disclosures about Market Risk” (Part II, Item 7A). We undertake no obligation to update or revise publicly any forward-looking statements, whether because of new information, future events or otherwise, except to the extent required by applicable law.

PART I

ITEM 1.BUSINESS

Corporate Structure

NOW Inc. (“NOW” or the “Company”), headquartered in Houston, Texas, was incorporated in Delaware on November 22, 2013. On May 30, 2014, the spin-off from NOV Inc., formerly National Oilwell Varco, Inc. (“NOV”) was completed and NOW became an independent, publicly traded company (the “Spin-Off” or “Separation”). In accordance with a separation and distribution agreement between NOV and NOW, the two companies were separated by NOV distributing to its stockholders 107,053,031 shares of common stock of NOW Inc. with each NOV stockholder receiving one share of NOW common stock for every four shares of NOV common stock held at the close of business on the record date of May 22, 2014 and not sold prior to close of business on May 30, 2014. We filed a registration statement on Form 10, as amended through the time of its effectiveness, describing the Spin-Off, which was declared effective by the U.S. Securities and Exchange Commission (“SEC”) on May 13, 2014. On June 2, 2014, NOW stock began trading “regular-way” on the New York Stock Exchange under the ticker symbol “DNOW”. Following the Spin-Off, NOW became an independent, publicly traded company as NOV had no ownership interest in NOW. Each company has separate public ownership, boards of directors and management.

Overview

We are a global distributor to the oil and gas and industrial markets with a legacy of over 150 years. We operate primarily under the DistributionNOW and DNOW brands. Through a network of approximately 195 locations and approximately 2,500 employees worldwide, we offer a complementary suite of digital procurement channels, in conjunction with our locations, that provides products to the energy and industrial markets around the world.

Additionally, through our growing DigitalNOW® platform, customers can leverage world-class technology across ecommerce, data management and supply chain optimization applications to solve a wide array of complex operational and product sourcing challenges to assist in maximizing their return on assets.

Our energy product offering is consumed throughout all sectors of the energy industry – from upstream drilling and completion, exploration and production (“E&P”), midstream infrastructure development to downstream petroleum refining and petrochemicals – as well as in other industries, such as chemical processing, mining, utilities and renewables. The industrial distribution end markets include engineering and construction firms that perform capital and maintenance projects for their end user clients. We also provide supply chain and materials management solutions to the same markets where we sell products.

Our global product offering includes consumable maintenance, repair and operating (“MRO”) supplies, pipe, valves, fittings, flanges, gaskets, fasteners, electrical, instrumentation, artificial lift, pumping solutions, valve actuation and modular process, measurement and control equipment. We also offer procurement, warehouse and inventory management solutions as part of our supply chain and materials management offering. We have developed expertise in providing application systems, work processes, parts integration, optimization solutions and after-sales support.

Our solutions include outsourcing portions or entire functions of our customers’ procurement, warehouse and inventory management, logistics, point of issue technology, project management, business process and performance metrics reporting. These solutions allow us to leverage the infrastructure of our SAP™ Enterprise Resource Planning (“ERP”) system and other technologies to streamline our

3

customers’ purchasing process, from requisition to procurement to payment, by digitally managing workflow, improving approval routing and providing robust reporting functionality.

We support land and offshore operations for the major oil and gas producing regions around the world through our network of locations. Our key markets, beyond North America, include Latin America, the North Sea, the Middle East, Asia Pacific and the Former Soviet Union (“FSU”). Products sold through our locations support greenfield expansion upstream capital projects, midstream infrastructure and transmission and MRO consumables used in day-to-day production. We provide downstream energy and industrial products for petroleum refining, chemical processing, liquefied natural gas (“LNG”) terminals, power generation utilities and customer on-site locations.

We stock or sell more than 300,000 stock keeping units (“SKUs”) through our branch network. Our supplier network consists of thousands of vendors in approximately 40 countries. From our operations in over 20 countries, we sell to customers operating in approximately 80 countries. The supplies and equipment stocked by each of our branches are customized to meet varied and changing local customer demands. The breadth and scale of our offering enhances our value proposition to our customers, suppliers and shareholders.

We employ advanced information technologies, including a common ERP platform across most of our business, to provide complete procurement, warehouse and inventory management and logistics coordination to our customers around the globe. Having a common ERP platform allows immediate visibility into our inventory assets, operations and financials worldwide, enhancing decision making and efficiency.

Global Operations

Demand for our products is driven primarily by the level of oil and gas drilling, completions, servicing, production, transmission, refining and petrochemical activities. It is also influenced by the global supply and demand for energy, the economy in general and geopolitics. Several factors drive spending, such as investment in energy infrastructure, the North American conventional and shale plays, market expectations of future developments in the oil, natural gas, liquids, refined products, petrochemical, plant maintenance and other industrial, manufacturing and energy sectors.

We have expanded globally, through acquisitions and organic investments, into Australia, Azerbaijan, Brazil, Canada, China, Colombia, Egypt, England, India, Indonesia, Kazakhstan, Kuwait, Mexico, Netherlands, Norway, Oman, Russia, Saudi Arabia, Scotland, Singapore, the United Arab Emirates (“UAE”) and the United States.

4

Summary of Reportable Segments

We operate through three reportable segments: United States (“U.S.”), Canada and International. The segment data included in our Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) are presented on a basis consistent with our internal management reporting. Segment information appearing in Note 15 “Business Segments” of the Notes to Consolidated Financial Statements (Part IV, Item 15 of this Form 10-K) is also presented on this basis.

United States

We have approximately 130 locations in the U.S., which are geographically positioned to best serve the upstream, midstream and downstream energy and industrial markets.

We offer higher value solutions in key product lines in the U.S. which broaden and deepen our customer relationships and related product line value. Examples of these include artificial lift, pumps, valves and valve actuation, process and production equipment, fluid transfer products, measurement and controls, spoolable and coated steel-pipe and composite pipe, along with many other products required by our customers, which enable them to focus on their core business while we manage varying degrees of their supply chain. We also provide additional value to our customers through the design, assembly, fabrication and optimization of products and equipment essential to the safe and efficient production, transportation and processing of oil and gas.

During 2020, in order to align with the updates to the operational and management structure, we combined the U.S. Supply Chain and U.S. Energy operating segments within the U.S. reportable segment.

Canada

We have a network of approximately 40 locations in the Canadian oilfield, predominately in the oil rich provinces of Alberta, Saskatchewan, Manitoba and other targeted locations across the country. Our Canada segment primarily serves energy exploration, production, mining and drilling business, offering customers many of the same products and value-added solutions that we perform in the U.S. In Canada, we also provide training for, and supervise the installation of, jointed and spoolable composite pipe. This product line is supported by inventory and product and installation expertise to serve our customers.

International

We operate in approximately 20 countries and serve the needs of our international customers from approximately 25 locations outside the U.S. and Canada, which are strategically located in major oil and gas development areas. Our approach in these markets is similar to our approach in North America, as our customers turn to us to provide products and supply chain solutions support closer to their drilling and exploration activities. Our long legacy of operating in many international regions, combined with significant expansion into several key markets, provides a competitive advantage as few of our competitors have a presence in most of the global energy producing regions.

Distribution Industry Overview

The distribution industry is highly fragmented, comprised of large companies with global reach and numerous small, local and regional competitors. Distribution companies act both as supply stores and supply chain management providers for their customers. Distributors deliver value to their customers by serving as a supply chain partner by managing vendor networks and aggregating, carrying and distributing a wide range of product inventory from numerous vendors in locations close to the end user. As a distributor of energy and industrial markets, we offer a wide array of products and supply chain services.

We offer our products, services and supply chain solutions across the entire energy value chain, from onshore and offshore drilling of oil and gas, to the exploration and production of oil and gas, the separation, transfer, and disposal of produced water, to the midstream gathering, processing and transmission of oil, gas, water, natural gas liquids (“NGLs”), LNG, and refined petroleum products, to the downstream refining of oil, and the manufacturing of petrochemicals and specialty chemicals. In addition, we provide our products, services and supply chain solutions to other end markets including mining and minerals, municipal water and wastewater and industrial manufacturing.

We provide drilling products, MRO consumables, safety and original equipment manufacturer (“OEM”) equipment for land drilling rigs, workover rigs and initial offshore drilling rig load outs. Once rigs are contracted, commissioned and deployed, we seek to replace material and inventory consumed during drilling operations. We couple the sale of products with supply chain services in the form of inventory planning, inventory management and warehouse management. We provide a full suite of process and production equipment, pumps and compressor packages, artificial lift, steel, fiberglass and composite pipe, valves and fittings (“PVF”), instrumentation and measurement, and safety and personal protective equipment (“PPE”) in the exploration, production, separation, storage and gathering of oil and gas, as well as the separation, removal, storage and transfer of produced water.

5

To minimize air emissions, we provide vapor recovery systems to capture and transfer gas and volatile organic compounds during the separation and storage of oil, gas and water from operating reservoirs. For produced water, we provide fluid movement products that help our customers environmentally dispose of water. For oil streams, we provide products that measure the quality and quantity of oil and gas through the separation process and prior to distribution to the midstream sector. We offer a variety of fluid movement solutions ranging from standard to engineered pump packages and a wide variety of American Society of Mechanical Engineers (“ASME”) fabricated process and production equipment to remove water and contaminants prior to the midstream transfer of oil, NGLs and other refined products within the midstream sector. For gas processing and gas conditioning, we offer a full suite of PVF and ASME coded fabricated process equipment to efficiently and economically process and condition gas for transfer to end markets. Many of the terminals and tank farms used in the midstream space to facilitate the storage and distribution of oil, gas, NGLs, LNG, and other hydrocarbon-based fluids utilize our products. Across many of the process industries where we provide valves, we offer low emission stem packing options to help reduce emissions. We provide PVF, pumps, safety, PPE, supply chain and safety services to the refining, petrochemical, chemical and industrial industries. Our products are consumed from industrial customer’s daily MRO expenditures, customer capital projects in the form of existing plant expansions, new plant facilities, as well as planned and unplanned maintenance of processing units.

Our Distribution Channels

We offer a diverse range of products across the energy and industrial markets in the U.S., Canada and internationally. There are thousands of manufacturers of the products used in the markets in which we operate and customers demand a high level of service, responsiveness and availability across a broad set of products and vendors. These market dynamics make the distributor an essential element in the value chain for our customers. Our product offering is aligned to meet the needs of our customer base.

Energy

Energy branches are brick and mortar supply store operations that provide products to multiple upstream, midstream and downstream customers from a single location. These branches serve repeat account and walk-in retail customers. Products are inventoried in branch warehouses based on local market needs and are delivered or available for pick-up as needed. These branches serve a geographical radius and provide delivery of products and solutions. A number of locations that service these same customers provide a complementary and expanded set of supply chain services in conjunction with the sale of products.

The distribution channel includes sales and operations professionals trained in the products, applications and customer service required to support customers as they drill, explore, produce, transport and refine oil and gas and other products. The primary product offering includes line pipe, valves, fabrication, valve actuation, fittings and flanges, pumps, OEM equipment, electrical products, mill supplies, tools, safety supplies, PPE, applied products and applications, such as artificial lift systems, coatings and miscellaneous expendable items. We couple the sale of products with supply chain services in the form of inventory planning, inventory management and warehouse management. Supply chain services can be customized to a customer’s requirements and guided by a strategic framework to reduce direct material expenditures and supply chain costs, improve maintenance productivity, reduce inventory-related working capital, streamline time to revenue and manage the risk of material availability affecting business continuity.

Process Solutions

Process Solutions has a team of distribution experts, technical professionals and licensed engineers who provide expertise related to pumps, compressors and fluid movement packages, fabricated liquid and gas measurement systems and process and production equipment. Process Solutions distributes OEM equipment including pumps, generator sets, air and gas compressors, dryers, blowers, mixers and valves. Within our process and production equipment category, we produce customer lease automatic custody transfer (“LACT”) units, vapor recovery units, gas meter runs, ASME code vessels in the form of separators, heater treaters, gas conditioning systems, towers, reactors, condensate stabilizers, slug catchers and pressurized bullet tanks, pig launchers and receivers and water transfer and disposal units. After-market services include rental, machining and repair service from a team of field mechanics located throughout the central U.S.

Process Solutions serves the upstream, midstream and downstream oil and gas markets as well as the municipal industrial, mining, power generation and general industries. Process Solutions also provides modular oil and gas tank battery solutions that positively impact our operator customers by enabling them to design a modular tank battery that enables flexibility and scalability for current and future production, while expediting revenue generation by reducing the time to complete a tank battery and getting oil and gas into the pipeline earlier. This solution saves our customers time and expense related to well hookup and tank battery commissioning and reduces field incident exposures due to a reduced labor requirement for battery construction.

6

Customers

Our primary customers are companies active in the upstream, midstream and downstream sectors of the energy industry, including drilling contractors, well servicing companies, independent and national oil and gas companies, midstream operators, refineries, petrochemical, chemical, utilities and other downstream energy processors. We also serve a diverse range of industrial and manufacturing companies across a broad spectrum of industries and end markets. We partner with our customers to continually meet or exceed their expectations and add value as a supply chain partner in the locations where they operate. Our products are typically critical to our customers’ operations, yet represent only a small fraction of their total project or facility cost. As a result, our customers seek suppliers with established qualifications and an operational history to deliver high quality and reliable products that meet their requirements in a timely manner.

As customers increasingly aggregate purchases to improve efficiency and reduce costs, they partner with large distributors who can meet their needs for products in multiple locations around the world. Customers can procure products through our direct branch model or through our ecommerce site, http://shop.dnow.com. We believe we could benefit from consolidation among the companies we serve, as the larger resulting companies look to global distributors as their source for products and related solutions.

No single customer represents more than 10% of our revenue.

Competition

The distribution companies serving the energy and industrial end markets are both numerous and competitive. This industry is highly fragmented, comprised of large distributors, each with many locations and with online ecommerce sites, who aggregate and distribute several product lines, and includes numerous smaller regional and local companies, many of which operate from a single location and either aggregate and distribute several product lines or focus on a single product line. While some large distributors compete in both markets, most companies focus on either the energy or industrial end market. In the energy market, some of the larger companies against whom we compete include Ferguson Enterprises, Inc., MRC Global, Inc., Russel Metals, Inc., DXP Enterprises, Inc. and FloWorks International LLC. In the industrial market, some of the larger companies against whom we compete include Ferguson Enterprises, Inc., W.W. Grainger Inc., HD Supply, Inc., Wesco International Inc., MSC Industrial Direct Co., Inc., Applied Industrial Technologies, Inc., DXP Enterprises, Inc. and Fastenal Company.

Seasonal Nature of the Company’s Business

A portion of our business has experienced seasonal trends, to some degree, which have varied by geographic region. In the U.S., activity has historically been higher during the summer and fall months. In Canada, certain E&P activities have declined in the spring due to seasonal thaws and regulatory restrictions limiting the ability of drilling rigs and transportation to operate effectively and safely during these periods.

Human Capital Resources

At December 31, 2020, we had approximately 2,500 employees, of which approximately 100 were temporary employees. Some of our employees in various foreign locations are subject to collective bargaining agreements. Less than one percent of our employees in the U.S. are subject to collective bargaining agreements. We offer market-competitive benefits for employees and opportunities for growth and advancement. We place a strong emphasis on employee growth and development and provide opportunities for valued contribution and innovation.

Training and Development Programs

The skills, knowledge and capabilities of our people are central to our success. We have developed training courses and programs, including a robust online learning platform providing our employees an opportunity for professional development.

We recognize that the advancement and empowerment of our workforce drives a better quality of work and life for our employees, ultimately resulting in the delivery of exceptional service to our customers. As such, we have designed a range of professional and leadership development programs focused on helping our employees reach their career goals.

Recognizing Employees

Recognition of individual achievements and contributions is an important part of our culture. Our Customer Priority One program encourages customers, peers and leaders to recognize DNOW employees, customers or vendors who exemplify DNOW’s commitment to customer service. We also award Milestone Service Awards to employees for their years of service and dedication of time to our Company, which recognize employees at each five-year service anniversary.

7

Workforce Diversity and Inclusion

We are committed to advancing an inclusive environment where diversity is appreciated and encouraged, and everyone has a sense of belonging throughout our organization. We recognize the opportunity to drive diversity in our workforce through talent acquisition and retention because we know that one of our greatest strengths is the diversity of our team. We recognize that having a team with a broad range of experience, cultural characteristics and varying perspectives fortifies our brand. We believe in advocating for diversity within our workforce by employing women and men of varying cultures, nationalities and backgrounds to work together to achieve a common goal.

To find the best employees, we must have a diverse pipeline of talent. We have expanded recruiting efforts with diverse organizations so we can reach a broader pool of candidates. We create a culture where all employees can strive to be their best, to achieve company goals and to deliver superior service to our customers. As of December 31, 2020, our U.S. workforce was comprised of approximately 25% female and 31% racial minorities.

We recognize that we are an integral part of the communities in which we operate. By directly engaging people in the communities we serve, we create a transparent dialogue to try and listen and learn from alternative views in how we conduct our business. The strengthening of minority- and women-owned businesses contributes to the overall economic growth of DNOW and the expansion of our markets.

Workforce Health and Safety

Safety is at the center of our actions. Simply put, we act with high priority on health and safety in our workplace and in the communities where we operate. Our safety culture is driven through our health, safety and environment (“HSE”) management system beginning with our HSE Policy Statement, which sets the tone for our company’s commitment to safety. A one-page, top-level document, expressly approved by our senior management team, the HSE Policy Statement outlines our expectations for all employees, vendors, customers, contractors, subcontractors and third parties. This HSE Policy Statement, combined with our HSE guiding principles, corporate policies and procedures and our business level HSE policies and procedures, makes up our management system, which is overseen both with corporate supervision and field level management to ensure emphasis is consistent on proper and safe behaviors.

Sustainability

We can assist in reducing emissions of greenhouse gases in our operations by creating a more efficient supply chain. An efficient supply chain can help reduce the carbon footprint of deliveries to our distribution centers and branches and, ultimately to our customers. Use of our large centralized and regional distribution centers allow us to aggregate product across multiple suppliers and customers, which, in turn, prevents each customer from separately creating duplicative supply chains that require fuel for deliveries and resources to manage.

As a distributor, we perform minimal manufacturing operations. We do not utilize large amounts of water. Our energy inputs are primarily electricity for lighting, heating and office and warehouse equipment, natural gas for heating and gasoline for company sales and delivery vehicles. We strive to make our operations more efficient, and in turn try to work to reduce use of these resources and resulting emissions. We have recycling programs to try and reduce waste from used cardboard, office paper and other recyclables. However, recycling programs are sometimes limited by the unavailability of users, haulers or purchasers for recyclable materials at reasonable costs.

We are a distributor of products that contain and control the movement of gases and fluids in an efficient and sustainable manner. The products we sell are designed by the manufacturers of those products to prevent and minimize accidental leaks of hydrocarbons. Additionally, we offer product lines that further aid in the mitigation of environmental impact. Examples of such products include: domestically produced goods; low emission rated valves; steel piping products produced from recycled scrap; and pipe produced using wind power, recycled water, and wood pellet inputs.

Environmental Matters

We are subject to a variety of federal, state, local, foreign and provincial environmental, health and safety laws, regulations and permitting requirements, including those governing the discharge of pollutants or hazardous substances into the air, soil or water, the generation, handling, use, management, storage and disposal of, or exposure to, hazardous substances and wastes, the responsibility to investigate, remediate, monitor and clean up contamination and occupational health and safety. Fines and penalties may be imposed for non-compliance with applicable environmental, health and safety requirements and the failure to have or to comply with the terms and conditions of required permits. Historically, the costs to comply with environmental and health and safety requirements have not been material to our financial position, results of operations or cash flows. We are not aware of any pending environmental compliance or remediation matters that, in the opinion of management, are reasonably likely to have a material effect on our business, financial position or results of operations or cash flows.

8

Available Information

Our website address is www.dnow.com. The information found on our website is not part of this or any other report we file with, or furnish to, the SEC and is expressly not incorporated by reference into this document. Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, proxy statements and any amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 are available on our website, free of charge, as soon as reasonably practicable after such reports are filed with, or furnished to, the SEC. Alternatively, you may access these reports at the SEC’s website at www.sec.gov.

9

ITEM 1A.RISK FACTORS

You should carefully consider each of the following risks in addition to all other information contained or incorporated herein. These risks relate principally to our business and the industry in which we operate or to the securities markets generally and ownership of our common stock. Our business, prospects, financial condition, results of operations or cash flows could be materially and adversely affected by any of these risks, and, as a result, the trading price of our common stock could decline. This information should be read in conjunction with Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, Item 7A, Quantitative and Qualitative Disclosures about Market Risk and the consolidated financial statements and related notes included in this Form 10-K.

Risks Relating to Our Business

The COVID-19 pandemic has adversely affected our business, and the ultimate effect on our operations and financial condition will depend on future developments, which are highly uncertain and cannot be predicted.

The COVID-19 pandemic has adversely affected the global economy, disrupted global supply chains and created significant volatility in the financial markets. In addition, the pandemic has resulted in travel restrictions, business closures and the institution of quarantining and other restrictions on movement in many communities. As a result, there has been a significant reduction in demand for and prices of crude oil, natural gas and natural gas liquids (“NGLs”). If the reduced demand for and prices of crude oil, natural gas and NGLs continue for a prolonged period, our operations, financial condition and cash flows may be materially and adversely affected. Our operations also may be adversely affected if significant portions of our workforce are unable to work effectively, including because of illness, quarantines, government actions, or other restrictions in connection with the pandemic. We have already implemented workplace restrictions, including guidance for our employees to work remotely if able, in our offices and work sites for health and safety reasons and are continuing to monitor national, state and local government directives where we have operations or offices. The extent to which the COVID-19 pandemic adversely affects our business, results of operations, and financial condition will depend on future developments, which are highly uncertain and cannot be predicted, including the scope and duration of the pandemic and actions taken by governmental authorities and other third parties in response to the pandemic, the resurgence of cases, stay-at-home orders and other similar restrictions.

Decreased capital and other expenditures in the energy industry, which can result from decreased oil and natural gas prices, among other things, can adversely impact our customers’ demand for our products and our revenue.

A large portion of our revenue depends upon the level of capital and operating expenditures in the oil and natural gas industry, including capital and other expenditures in connection with exploration, drilling, production, gathering, transportation, refining and processing operations. Demand for the products we distribute is particularly sensitive to the level of exploration, development and production activity of, and the corresponding capital and other expenditures by, oil and natural gas companies. In addition, after a well is drilled, there can be a lag between when the well is drilled and when it is completed, which causes a delay in the demand for some of our products. Oil and natural gas prices have been extremely volatile since 2014. Continued volatility and weakness in oil or natural gas prices could depress levels of exploration, development and production activity and, therefore, could lead to a decrease in our customers’ capital and other expenditures.

The willingness of oil and gas operators to make capital and operating expenditures to explore for and produce oil and natural gas and the willingness of oilfield service companies to invest in capital and operating equipment will continue to be influenced by numerous factors over which we have no control, including:

|

|

• |

the ability of the members of the Organization of Petroleum Exporting Countries (“OPEC”) and certain non-OPEC countries, such as Russia, to maintain price stability through voluntary production limits, the level of production by other non-OPEC countries, such as the United States, and worldwide demand for oil and gas; |

|

|

• |

the impact of public health crises, such as the COVID-19 pandemic, on worldwide demand for oil and gas; |

|

|

• |

the level of production from known reserves; |

|

|

• |

the cost of exploring for and producing oil and gas; |

|

|

• |

limits on access to capital and investor demands for capital discipline; |

|

|

• |

the level of drilling activity and drilling rig day rates; |

|

|

• |

worldwide economic activity; |

|

|

• |

national government political requirements; |

10

|

|

• |

changes in governmental regulations; |

|

|

• |

the development of alternate energy sources; and |

|

|

• |

environmental regulations. |

If there is a significant reduction in demand for drilling services, in cash flows of drilling contractors, well servicing companies or production companies, or in drilling or well servicing rig utilization rates, then demand for our products will decline.

Volatile oil and gas prices affect demand for our products.

Demand for our products is largely determined by current and anticipated oil and natural gas prices, and the related spending and level of activity by our customers, including spending on production and the level of drilling activities. Volatility or weakness in oil or natural gas prices (or the perception that oil or natural gas prices will decrease) affects the spending pattern of our customers, and may result in the drilling of fewer new wells or lower production spending on existing wells. This, in turn, could result in lower demand for our products. Any sustained decrease in capital expenditures in the oil and natural gas industry could have a material adverse effect on us.

Prices for oil and natural gas are subject to large fluctuations in response to relatively minor changes in the supply of and demand for oil and natural gas, market uncertainty and a variety of other factors that are beyond our control. Any such reduction in operating budgets, reduction in activity and/or pricing pressures, would adversely affect our revenue and operating performance.

Many factors affect the supply of and demand for energy and, therefore, influence oil and natural gas prices, including:

|

|

• |

the level of domestic and worldwide oil and natural gas production and inventories; |

|

|

• |

the level of drilling activity and the availability of attractive oil and natural gas field prospects, which governmental actions may affect, such as regulatory actions or legislation, or other restrictions on drilling, including those related to environmental concerns (e.g., a temporary moratorium on deepwater drilling in the Gulf of Mexico following a rig accident or oil spill); |

|

|

• |

the discovery rate of new oil and natural gas reserves and the expected cost of developing new reserves; |

|

|

• |

the actual cost of finding and producing oil and natural gas; |

|

|

• |

depletion rates; |

|

|

• |

domestic and worldwide refinery over capacity or under capacity and utilization rates; |

|

|

• |

the availability of transportation infrastructure and refining capacity; |

|

|

• |

increases in the cost of products that the oil and gas industry uses, such as those that we provide, which may result from increases in the cost of raw materials such as steel; |

|

|

• |

shifts in end-customer preferences toward fuel efficiency and the use of natural gas; |

|

|

• |

the economic or political attractiveness of alternative fuels, such as coal, hydrocarbon, battery power, wind, solar energy and biomass-based fuels; |

|

|

• |

increases in oil and natural gas prices or historically high oil and natural gas prices, which could lower demand for oil and natural gas products; |

|

|

• |

worldwide economic activity including growth in non-Organization for Economic Co-operation and Development countries, including China and India; |

|

|

• |

interest rates and the cost of capital; |

|

|

• |

national government policies, including government policies that could nationalize or expropriate oil and natural gas, E&P, refining or transportation assets; |

|

|

• |

the ability of OPEC and non-OPEC countries, such as Russia, to set and maintain production levels and prices for oil; |

|

|

• |

the level of production by non-OPEC countries; |

|

|

• |

the impact of armed hostilities, or the threat or perception of armed hostilities; |

|

|

• |

public health crises, such as the COVID-19 pandemic that began in 2020; |

|

|

• |

environmental regulation; |

|

|

• |

import duties and tariffs; |

11

|

|

• |

technological advances; |

|

|

• |

global weather conditions and natural disasters; |

|

|

• |

currency fluctuations; and |

|

|

• |

tax policies. |

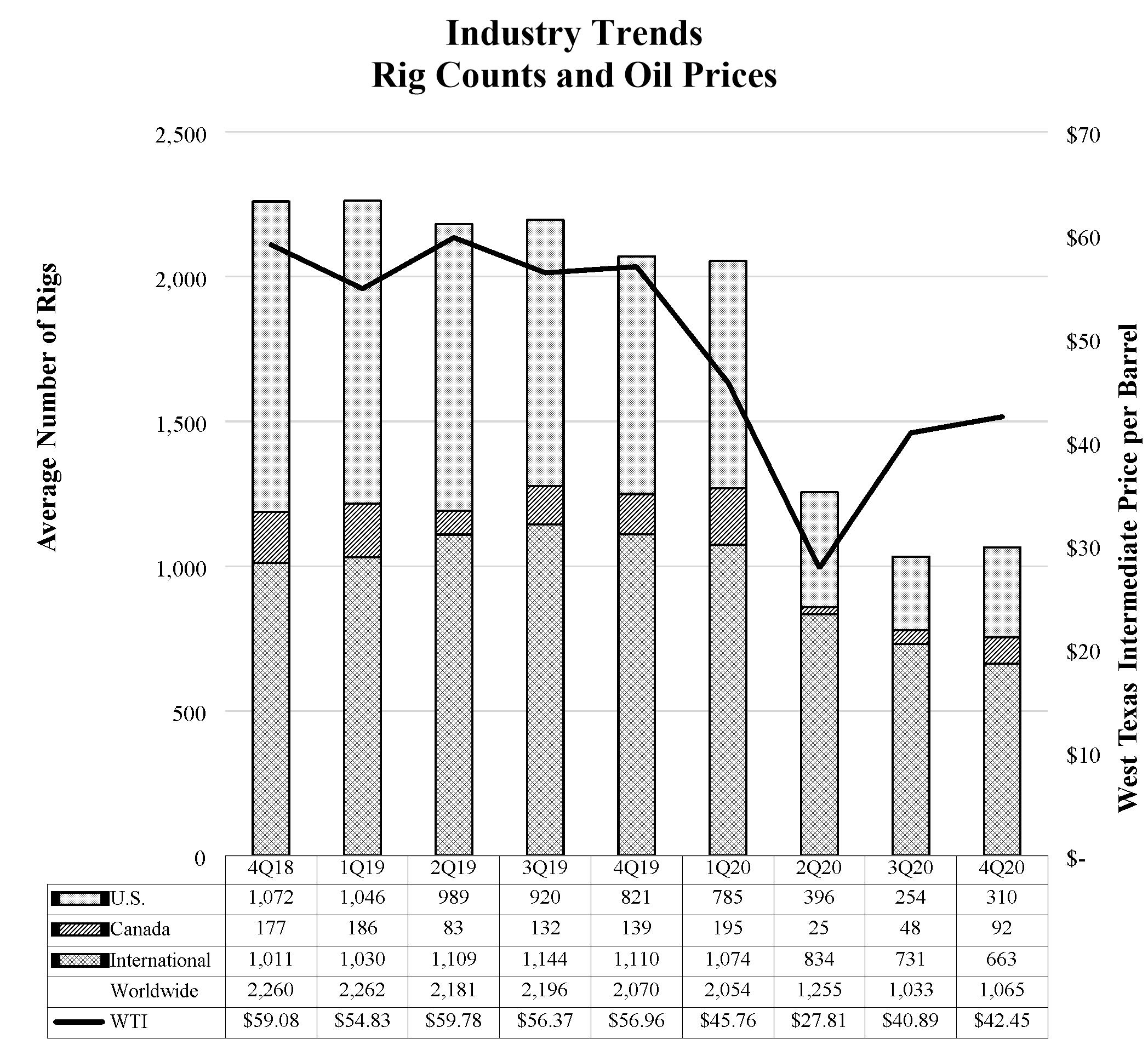

Oil and natural gas prices have been and are expected to remain volatile. U.S. rig count decreased from 796 rigs on January 3, 2020 to 351 rigs on December 31, 2020. U.S. rig count averaged 436 rigs in 2020. U.S. rig count at January 22, 2021 was 378 rigs. The price for West Texas Intermediate crude was $47.47 per barrel at January 4, 2021, $61.17 per barrel on January 2, 2020 and $46.31 per barrel on January 2, 2019. This type of volatility has historically caused oil and natural gas companies to change their strategies and expenditure levels from year to year. We have experienced in the past, and we will likely experience in the future, significant fluctuations in operating results based on these changes.

General economic conditions may adversely affect our business.

U.S. and global general economic conditions affect many aspects of our business, including demand for the products we distribute and the pricing and availability of supplies. General economic conditions and predictions regarding future economic conditions also affect our forecasts. A decrease in demand for the products we distribute or other adverse effects resulting from an economic downturn may cause us to fail to achieve our anticipated financial results. General economic factors beyond our control that affect our business and customers include public health crises, interest rates, recession, inflation, deflation, customer credit availability, consumer credit availability, consumer debt levels, performance of housing markets, energy costs, tariffs, tax rates and policy, unemployment rates, commencement or escalation of war or hostilities, the threat or possibility of war, terrorism or other global or national unrest, political or financial instability, and other matters that influence our customers’ spending. Increasing volatility in financial markets may cause these factors to change with a greater degree of frequency or increase in magnitude. In addition, worldwide economic conditions could have an adverse effect on our business, prospects, operating results, financial condition and cash flows.

We may be unable to compete successfully with other companies in our industry.

We sell products in very competitive markets. In some cases, we compete with large companies with substantial resources. In other cases, we compete with smaller regional companies that may increasingly be willing to provide similar products at lower prices. Certain of these competitors may have greater financial, technical and marketing resources than us, and may be in a better competitive position. The following competitive actions can each adversely affect our revenues and earnings:

|

|

• |

price changes; |

|

|

• |

vendors with better terms; |

|

|

• |

consolidation in the industry; |

|

|

• |

investments in technology and fulfillment; and |

|

|

• |

improvements in availability and delivery. |

We could experience a material adverse effect to the extent that our competitors are successful in reducing our customers’ purchases of products from us. Competition could also cause us to lower our prices, which could reduce our margins and profitability. Furthermore, consolidation in our industry could heighten the impacts of the competition on our business and results of operations discussed above, particularly if consolidation results in competitors with stronger financial and strategic resources, and could also result in increases to the prices we are required to pay for acquisitions we may make in the future. In addition, certain foreign jurisdictions and government-owned petroleum companies located in some of the countries in which we operate have adopted policies or regulations which may give local nationals in these countries competitive advantages. Competition in our industry could lead to lower revenues and earnings.

Demand for the products we distribute could decrease if the manufacturers of those products were to sell a substantial amount of goods directly to end users in the sectors we serve.

Historically, users of pipes, valves and fittings and related products have purchased certain amounts of these products through distributors and not directly from manufacturers. If customers were to purchase the products that we sell directly from manufacturers, or if manufacturers sought to increase their efforts to sell directly to end users, we could experience a significant decrease in profitability. These or other developments that remove us from, or limit our role in, the distribution chain, may harm our competitive position in the marketplace and reduce our sales and earnings and adversely affect our business.

12

We may need additional capital in the future, and it may not be available on acceptable terms, or at all.

We may require more capital in the future to:

|

|

• |

fund our operations (including, but not limited to, working capital requirements such as inventory); |

|

|

• |

finance investments in equipment and infrastructure needed to maintain and expand our distribution capabilities; |

|

|

• |

enhance and expand the range of products we offer; and |

|

|

• |

respond to potential strategic opportunities, such as investments, acquisitions and international expansion. |

We can give no assurance that additional financing will be available on terms favorable to us, or at all. The terms of available financing may place limits on our financial and operating flexibility. If adequate funds are not available on acceptable terms, we may be forced to reduce our operations or delay, limit or abandon expansion opportunities. Moreover, even if we are able to continue our operations, the failure to obtain additional financing could reduce our competitiveness.

We do not have long-term contracts or agreements with many of our customers. The contracts and agreements that we do have generally do not commit our customers to any minimum purchase volume. The loss of a significant customer may have a material adverse effect on us.

Given the nature of our business, and consistent with industry practice, we do not have long-term contracts with many of our customers. In addition, our contracts generally do not commit our customers to any minimum purchase volume. Therefore, a significant number of our customers may terminate their relationships with us or reduce their purchasing volume at any time. Furthermore, the long-term customer contracts that we do have are generally terminable without cause on short notice. The products that we may sell to any particular customer depend in large part on the size of that customer’s capital expenditure budget in a particular year and on the results of competitive bids for major projects. Consequently, a customer that accounts for a significant portion of our sales in one fiscal year may represent an immaterial portion of our sales in subsequent fiscal years. The loss of a significant customer, or a substantial decrease in a significant customer’s orders, may have an adverse effect on our sales and revenue.

In addition, we are subject to customer audit clauses in many of our multi-year contracts. If we are not able to provide the proper documentation or support for invoices per the contract terms, we may be subject to negotiated settlements with our major customers.

Changes in our customer and product mix could cause our product margin to fluctuate.

From time to time, we may experience changes in our customer mix or in our product mix. Changes in our customer mix may result from geographic expansion, daily selling activities within current geographic markets and targeted selling activities to new customer segments. Changes in our product mix may result from marketing activities to existing customers and needs communicated to us from existing and prospective customers. If customers begin to require more lower-margin products from us and fewer higher-margin products, our business, results of operations and financial condition may suffer.

Customer credit risks could result in losses.

The concentration of our customers in the energy industry may impact our overall exposure to credit risk as customers may be similarly affected by prolonged changes in economic and industry conditions. Further, laws in some jurisdictions in which we operate could make collection difficult or time consuming. We perform ongoing credit evaluations of our customers and do not generally require collateral in support of our trade receivables. While we maintain reserves for expected credit losses, we cannot assure these reserves will be sufficient to meet write-offs of uncollectible receivables or that our losses from such receivables will be consistent with our expectations.

We may be unable to successfully execute or effectively integrate acquisitions.

One of our key operating strategies is to selectively pursue acquisitions, including large scale acquisitions, to continue to grow and increase profitability. However, acquisitions, particularly of a significant scale, involve numerous risks and uncertainties, including intense competition for suitable acquisition targets, the potential unavailability of financial resources necessary to consummate acquisitions in the future, increased leverage due to additional debt financing that may be required to complete an acquisition, dilution of our stockholders’ net current book value per share if we issue additional equity securities to finance an acquisition, difficulties in identifying suitable acquisition targets or in completing any transactions identified on sufficiently favorable terms, assumption of undisclosed or unknown liabilities and the need to obtain regulatory or other governmental approvals that may be necessary to complete acquisitions. In addition, any future acquisitions may entail significant transaction costs and risks associated with entry into new markets.

13

Even when acquisitions are completed, integration of acquired entities can involve significant difficulties, such as:

|

|

• |

failure to achieve cost savings or other financial or operating objectives with respect to an acquisition; |

|

|

• |

complications and issues resulting from the integration/conversion of ERP systems; |

|

|

• |

strain on the operational and managerial controls and procedures of our business, and the need to modify systems or to add management resources; |

|

|

• |

difficulties in the integration and retention of customers or personnel and the integration and effective deployment of operations or technologies; |

|

|

• |

amortization of acquired assets, which would reduce future reported earnings; |

|

|

• |

possible adverse short-term effects on our cash flows or operating results; |

|

|

• |

diversion of management’s attention from the ongoing operations of our business; |

|

|

• |

integrating personnel with diverse backgrounds and organizational cultures; |

|

|

• |

coordinating sales and marketing functions; |

|

|

• |

failure to obtain and retain key personnel of an acquired business; and |

|

|

• |

assumption of known or unknown material liabilities or regulatory non-compliance issues. |

Failure to manage these acquisition risks could have an adverse effect on us.

We are a holding company and depend upon our subsidiaries for our cash flow.

We are a holding company. Our subsidiaries conduct all of our operations and own substantially all of our assets. Consequently, our cash flow and our ability to meet our obligations or to make other distributions in the future will depend upon the cash flow of our subsidiaries and our subsidiaries’ payment of funds to us in the form of dividends, tax sharing payments or otherwise.

The ability of our subsidiaries to make any payments to us will depend on their earnings, the terms of their current and future indebtedness, tax considerations and legal and contractual restrictions on the ability to make distributions.

Our subsidiaries are separate and distinct legal entities. Any right that we have to receive any assets of or distributions from any of our subsidiaries upon the bankruptcy, dissolution, liquidation or reorganization, or to realize proceeds from the sale of their assets, will be junior to the claims of that subsidiary’s creditors, including trade creditors and holders of debt that the subsidiary issued.

If we lose any of our key personnel, we may be unable to effectively manage our business or continue our growth.

Our future performance depends to a significant degree upon the continued contributions of our management team and our ability to attract, hire, train and retain qualified managerial, sales and marketing personnel. In particular, we rely on our sales and marketing teams to create innovative ways to generate demand for the products we distribute. The loss or unavailability to us of any member of our management team or a key sales or marketing employee could have a material adverse effect on us to the extent we are unable to timely find adequate replacements. We face competition for these professionals from our competitors, our customers and other companies operating in our industry. We may be unsuccessful in attracting, hiring, training and retaining qualified personnel.

Interruptions in the proper functioning of our information systems could disrupt operations and cause increases in costs or decreases in revenues.

The proper functioning of our information systems is critical to the successful operation of our business. We depend on our information management systems to process orders, track credit risk, manage inventory and monitor accounts receivable collections. Our information systems also allow us to efficiently purchase products from our vendors and ship products to our customers on a timely basis, maintain cost-effective operations and provide superior service to our customers. However, our information systems could be vulnerable to natural disasters, power losses, telecommunication failures, security breaches and other problems. If critical information systems fail or are otherwise unavailable, our ability to procure products to sell, process and ship customer orders, identify business opportunities, maintain proper levels of inventories, collect accounts receivable and pay accounts payable and expenses could be adversely affected. Our ability to integrate our systems with our customers’ systems would also be significantly affected. If our information systems are damaged or fail to function properly, we may incur substantial costs to repair or replace them, and may experience loss of critical data and interruptions or delays in our ability to manage inventories or process transactions, which could result in lost sales, inability to process purchase orders and/or a potential loss of customer loyalty, which could adversely affect our results of operations. We maintain information systems controls designed to protect against, among other things, unauthorized program changes and unauthorized access to data on our information systems. If our information systems controls do not function properly, we face increased risks of unexpected errors and unreliable financial data or theft of proprietary Company information.

14

The loss of third-party transportation providers upon whom we depend, or conditions negatively affecting the transportation industry, could increase our costs or cause a disruption in our operations.

We depend upon third-party transportation providers for delivery of products to our customers. Strikes, slowdowns, transportation disruptions or other conditions in the transportation industry, including, but not limited to, shortages of truck drivers, disruptions in rail service, increases in fuel prices and adverse weather conditions, could increase our costs and disrupt our operations and our ability to service our customers on a timely basis. We cannot predict whether or to what extent increases or anticipated increases in fuel prices may impact our costs or cause a disruption in our operations going forward.

Adverse weather events or natural disasters could negatively affect local economies and disrupt operations.

Certain areas in which we operate are susceptible to adverse weather conditions or natural disasters, such as hurricanes, tornadoes, floods and earthquakes. These events can disrupt our operations, result in damage to our properties and negatively affect the local economies in which we operate. Additionally, we may experience communication disruptions with our customers, vendors and employees. These events can cause physical damage to our locations and require us to close locations. Additionally, our sales orders and shipments can experience a temporary decline immediately following these events.

We cannot predict whether or to what extent damage caused by these events will affect our operations or the economies in regions where we operate. These adverse events could result in disruption of our purchasing or distribution capabilities, interruption of our business that exceeds our insurance coverage, our inability to collect from customers and increased operating costs. Our business or results of operations may be adversely affected by these and other negative effects of these events.

The occurrence of cyber incidents, or a deficiency in our cybersecurity, could negatively impact our business by causing a disruption to our operations, a compromise or corruption of our confidential information or damage to our Company’s image, all of which could negatively impact our financial results.

A cyber incident is considered to be any adverse event that threatens the confidentiality, integrity or availability of our information resources. More specifically, a cyber incident is an intentional attack or an unintentional event that can include gaining unauthorized access to systems to disrupt operations, corrupt data or steal confidential information. As our reliance on technology has increased, so have the risks posed to our systems, both internal and those we have outsourced. Our four primary risks that could directly result from the occurrence of a cyber incident include operational interruption, damage to our Company’s image, financial loss and private data exposure.

We have implemented solutions, processes, and procedures to help mitigate this risk, but these measures, as well as our organization’s increased awareness of our risk of a cyber incident, do not guarantee that our financial results will not be negatively impacted by such an incident. Our security measures may be undermined due to the actions of outside parties, employee error, malfeasance, or otherwise, and, as a result, an unauthorized party may obtain access to our data systems and misappropriate business and personal information. Our systems are subject to repeated attempts by third parties to access information or to disrupt our systems. Such disruptions or misappropriations and the resulting repercussions, including reputational damage and legal claims or proceedings, may adversely affect our results of operations, cash flows and financial condition, and the trading price of our common stock.

Privacy concerns relating to our personal and business information being potentially breached could damage our reputation and deter current and potential users or customers from using our products and services.

We have security measures and controls to protect personal and business information and continue to make investments to secure access to our information technology network. These measures may be undermined, however, due to the actions of outside parties, employee error, internal or external malfeasance, or otherwise, and, as a result an unauthorized party may obtain access to our data systems and misappropriate business and personal information. Because the techniques used to obtain unauthorized access, disable or degrade service, or sabotage systems change frequently and may not immediately produce signs of intrusion, we may be unable to anticipate these techniques, timely discover or counter them, or implement adequate preventative measures. Any such breach or unauthorized access could result in significant legal and financial exposure, damage to our reputation, and potentially have an adverse effect on our business and results of operations.

15

Certain of our borrowings based on the London Interbank Offered Rate (“LIBOR”) may be adversely impacted by the scheduled phase out of LIBOR.

The Financial Conduct Authority, which regulates LIBOR, has announced that it will not compel panel banks to contribute to LIBOR after 2021. It is likely that banks will not continue to provide submissions for the calculation of LIBOR after 2021 and possibly prior to then. Similarly, it is not possible to know whether LIBOR will continue to be viewed as an acceptable market benchmark, what rate or rates may become accepted alternatives to LIBOR, or what the effect of any such changes in views or alternatives may have on the financial markets for LIBOR-linked financial instruments.

Borrowings under our revolving credit facility bear an interest rate at the Company’s option, which includes LIBOR. There may be alternatives to this benchmark, but there are no assurances they will be available to the Company. The usage of interest rates other than LIBOR could result in increased borrowing costs to the Company.

Risks Relating to Our Supply Chain and International Trade Policies

We may experience unexpected supply shortages.

We distribute products from a wide variety of manufacturers and suppliers. Nevertheless, in the future we may have difficulty obtaining the products we need from suppliers and manufacturers as a result of unexpected demand or production difficulties that might extend lead times. Also, products may not be available to us in quantities sufficient to meet our customer demand. Our inability to obtain products from suppliers and manufacturers in sufficient quantities, or at all, could adversely affect our product offerings and our business.

We may experience cost increases from suppliers, which we may be unable to pass on to our customers.

In the future, we may face supply cost increases due to, among other things, unexpected increases in demand for supplies, decreases in production of supplies or increases in the cost of raw materials or transportation, or trade wars. Any inability to pass supply price increases on to our customers could have a material adverse effect on us. In addition, if supply costs increase, our customers may elect to purchase smaller amounts of products or may purchase products from other distributors. While we may be able to work with our customers to reduce the effects of unforeseen price increases because of our relationships with them, we may not be able to reduce the effects of the cost increases. In addition, to the extent that competition leads to reduced purchases of products from us or a reduction of our prices, and these reductions occur concurrently with increases in the prices for selected commodities which we use in our operations, the adverse effects described above would likely be exacerbated and could result in a prolonged downturn in profitability.

We do not have contracts with most of our suppliers. The loss of a significant supplier would require us to rely more heavily on our other existing suppliers or to develop relationships with new suppliers. Such a loss may have an adverse effect on our product offerings and our business.

Given the nature of our business, and consistent with industry practice, we do not have contracts with most of our suppliers. We generally make our purchases through purchase orders. Therefore, most of our suppliers have the ability to terminate their relationships with us at any time. Although we believe there are numerous manufacturers with the capacity to supply the products we distribute, the loss of one or more of our major suppliers could have an adverse effect on our product offerings and our business. Such a loss would require us to rely more heavily on our other existing suppliers or develop relationships with new suppliers, which may cause us to pay higher prices for products due to, among other things, a loss of volume discount benefits currently obtained from our major suppliers.

Changes in our credit profile may affect our relationship with our suppliers, which could have a material adverse effect on our liquidity.

Changes in our credit profile may affect the way our suppliers view our ability to make payments and may induce them to shorten the payment terms of their invoices. Given the large dollar amounts and volume of our purchases from suppliers, a change in payment terms may have a material adverse effect on our liquidity and our ability to make payments to our suppliers and, consequently, may have a material adverse effect on us.

16

Price reductions by suppliers of products that we sell could cause the value of our inventory to decline. Also, these price reductions could cause our customers to demand lower sales prices for these products, possibly decreasing our margins and profitability on sales to the extent that we purchased our inventory of these products at the higher prices prior to supplier price reductions.

The value of our inventory could decline as a result of manufacturer price reductions with respect to products that we sell. There is no assurance that a substantial decline in product prices would not result in a write-down of our inventory value. Such a write-down could have an adverse effect on our financial condition. Also, decreases in the market prices of products that we sell could cause customers to demand lower sales prices from us. These price reductions could reduce our margins and profitability on sales with respect to the lower-priced products. Reductions in our margins and profitability on sales could have a material adverse effect on us.

A substantial decrease in the price of steel could significantly lower our product margin or cash flow.

We distribute many products manufactured from steel. As a result, the price and supply of steel can affect our business and, in particular, our pipe product category. When steel prices are lower, the prices that we charge customers for products may decline, which affects our product margin and cash flow. At times pricing and availability of steel can be volatile due to numerous factors beyond our control, including general domestic and international economic conditions, labor costs, sales levels, competition, consolidation of steel producers, fluctuations in and the costs of raw materials necessary to produce steel, steel manufacturers’ plant utilization levels and capacities, import duties and tariffs and currency exchange rates. Increases in manufacturing capacity for steel-related products could put pressure on the prices we receive for such products. When steel prices decline, customer demands for lower prices and our competitors’ responses to those demands could result in lower sales prices and, consequently, lower product margin and cash flow.

If steel prices rise, we may be unable to pass along the cost increases to our customers.

We maintain inventories of steel products to accommodate the lead time requirements of our customers. Accordingly, we purchase steel products in an effort to maintain our inventory at levels that we believe to be appropriate to satisfy the anticipated needs of our customers based upon historic buying practices, contracts with customers and market conditions. Our commitments to purchase steel products are generally at prevailing market prices in effect at the time we place our orders. If steel prices increase between the time we order steel products and the time of delivery of the products to us, our suppliers may impose surcharges that require us to pay for increases in steel prices during the period. Demand for the products we distribute, the actions of our competitors and other factors will influence whether we will be able to pass on steel cost increases and surcharges to our customers, and we may be unsuccessful in doing so.

If tariffs and duties on imports into the U.S. of line pipe or certain of the other products that we sell are lifted, we could have too many of these products in inventory competing against less expensive imports.

U.S. law currently imposes tariffs and duties on imports from certain foreign countries of pipe and on other imports of certain steel products that we sell. If these tariffs and duties are lifted or reduced, and our U.S. customers accept these imported products, we could be materially and adversely affected to the extent that we would then have higher-cost products in our inventory or there would be increased supplies of these products which would drive down prices and affect our margins on our domestic or other alternate products that compete with the new imports that have tariffs or duties removed. If prices of these products were to decrease significantly, we might not be able to profitably sell these products we have in our inventory and the value would decline. In addition, significant price decreases could result in a significantly longer holding period for some of our inventory.

Changes in trade policies, including the imposition of additional tariffs, could negatively impact our business, financial condition and results of operations.

The current United States administration has signaled support for implementing, and in some instances, has already proposed or taken action with respect to, major changes to certain trade policies, such as the imposition of additional tariffs on imported products and the withdrawal from or renegotiation of certain trade agreements, including the North American Free Trade Agreement. On March 8, 2018, the President of the United States signed an order to impose a tariff of 25% on steel imported from certain countries under the Section 232 rule. The tariff did result in an increase in our cost of sales, and if removed could trigger a decrease in our cost of sales and inventory value. The U.S. has also imposed tariffs on China under section 301 that has affected the cost of certain products. These tariffs are subject to change as trade negotiations continue. If these tariffs were removed, it could drive down the costs of certain products and affect our inventory value which could affect our margin negatively. There can be no assurance that we will be able to pass any of the increases in raw material costs directly resulting from the tariffs to our customers.

In addition, there could be additional tariffs imposed by the United States and these could also result in additional retaliatory actions by the United States’ trade partners. Given that we procure many of the raw materials that we use to create our products directly or indirectly from outside of the United States, the imposition of tariffs and other potential changes in U.S. trade policy could increase the cost or limit the availability of such raw materials, which could hurt our competitive position and adversely impact our business, financial condition and results of operations. In addition, we sell a significant proportion of our products to customers outside of the

17

United States. Retaliatory actions by other countries could result in increases in the price of our products, which could limit demand for such products, hurt our global competitive position and have a material adverse effect on our business, financial condition and results of operations.

Risks Relating to Legal and Regulatory Matters

We are subject to strict environmental, health and safety laws and regulations that may lead to significant liabilities and negatively impact the demand for our products.