PFIZER INC - Quarter Report: 2019 June (Form 10-Q)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended June 30, 2019

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13

OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _______ to _______

COMMISSION FILE NUMBER 1-3619

----

PFIZER INC.

(Exact name of registrant as specified in its charter)

Delaware | 13-5315170 |

(State of Incorporation) | (I.R.S. Employer Identification No.) |

235 East 42nd Street, New York, New York 10017

(Address of principal executive offices) (zip code)

(212) 733-2323

(Registrant’s telephone number)

Securities registered pursuant to Section 12(b) of the Act: | ||||

Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

Common Stock, $.05 par value | PFE | New York Stock Exchange | ||

0.000% Notes due 2020 | PFE20A | New York Stock Exchange | ||

0.250% Notes due 2022 | PFE22 | New York Stock Exchange | ||

1.000% Notes due 2027 | PFE27 | New York Stock Exchange | ||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes | x | No | ☐ |

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes | x | No | ☐ |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

Large Accelerated filer x Accelerated filer ☐ Non-accelerated filer ☐ Smaller reporting company ☐ Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes | ☐ | No | x |

At August 5, 2019, 5,531,048,353 shares of the issuer’s voting common stock were outstanding.

Table of Contents

Page | |

Condensed Consolidated Statements of Income for the three and six months ended June 30, 2019 and July 1, 2018 | |

Condensed Consolidated Statements of Comprehensive Income for the three and six months ended June 30, 2019 and July 1, 2018 | |

Condensed Consolidated Balance Sheets as of June 30, 2019 and December 31, 2018 | |

Condensed Consolidated Statements of Equity for the three and six months ended June 30, 2019 and July 1, 2018 | |

Condensed Consolidated Statements of Cash Flows for the six months ended June 30, 2019 and July 1, 2018 | |

2

GLOSSARY OF DEFINED TERMS

Unless the context requires otherwise, references to “Pfizer,” “the Company,” “we,” “us” or “our” in this Quarterly Report on Form 10-Q (defined below) refer to Pfizer Inc. and its subsidiaries. We also have used several other terms in this Quarterly Report on Form 10-Q, most of which are explained or defined below:

2018 Financial Report | Financial Report for the fiscal year ended December 31, 2018, which was filed as Exhibit 13 to the Annual Report on Form 10-K for the fiscal year ended December 31, 2018 |

2018 Form 10-K | Annual Report on Form 10-K for the fiscal year ended December 31, 2018 |

ACA (Also referred to as U.S. Healthcare Legislation) | U.S. Patient Protection and Affordable Care Act, as amended by the Health Care and Education Reconciliation Act |

ACIP | Advisory Committee on Immunization Practices |

ALK | anaplastic lymphoma kinase |

Alliance revenues | Revenues from alliance agreements under which we co-promote products discovered or developed by other companies or us |

Allogene | Allogene Therapeutics, Inc. |

Anacor | Anacor Pharmaceuticals, Inc. |

AOCI | Accumulated Other Comprehensive Income |

Array | Array BioPharma Inc. |

Astellas | Astellas Pharma Inc., Astellas US LLC and Astellas Pharma US, Inc. |

Bamboo | Bamboo Therapeutics, Inc. |

Biopharma | Pfizer Biopharmaceuticals Group |

BMS | Bristol-Myers Squibb Company |

BRCA | BReast CAncer susceptibility gene |

CAR T | chimeric antigen receptor T cell |

CDC | U.S. Centers for Disease Control and Prevention |

cGMP | current Good Manufacturing Practices |

Citibank | Citibank, N.A. |

Developed Markets | U.S., Western Europe, Japan, Canada, South Korea, Australia, Scandinavian countries, Finland and New Zealand |

EGFR | epidermal growth factor receptor |

EH | Essential Health |

EMA | European Medicines Agency |

Emerging Markets | Includes, but is not limited to, the following markets: Asia (excluding Japan and South Korea), Latin America, Eastern Europe, the Middle East, Africa, Central Europe and Turkey |

EPS | earnings per share |

EU | European Union |

Exchange Act | Securities Exchange Act of 1934, as amended |

FASB | Financial Accounting Standards Board |

FDA | U.S. Food and Drug Administration |

GAAP | Generally Accepted Accounting Principles |

GIST | gastrointestinal stromal tumors |

GPD | Global Product Development organization |

GSK | GlaxoSmithKline plc |

GS&Co. | Goldman, Sachs & Co. LLC |

hGH-CTP | human growth hormone |

HIS | Hospira Infusion Systems |

Hisun Pfizer | Hisun Pfizer Pharmaceuticals Company Limited |

Hospira | Hospira, Inc. |

HR+ | hormone receptor-positive |

ICU Medical | ICU Medical, Inc. |

IH | Innovative Health |

IPR&D | in-process research and development |

IRS | U.S. Internal Revenue Service |

IV | intravenous |

Janssen | Janssen Biotech Inc. |

J&J | Johnson & Johnson |

King | King Pharmaceuticals LLC (formerly King Pharmaceuticals, Inc.) |

LDL | low density lipoprotein |

3

LEP | Legacy Established Products |

LIBOR | London Interbank Offered Rate |

Lilly | Eli Lilly & Company |

LOE | loss of exclusivity |

MCC | Merkel cell carcinoma |

MCO | managed care organization |

mCRC | metastatic colorectal cancer |

MD&A | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

Medivation | Medivation LLC (formerly Medivation, Inc.) |

Merck | Merck & Co., Inc. |

Meridian | Meridian Medical Technologies, Inc. |

Moody’s | Moody’s Investors Service |

Mylan | Mylan N.V. |

NDA | new drug application |

NSCLC | non-small cell lung cancer |

NYSE | New York Stock Exchange |

OPKO | OPKO Health, Inc. |

OTC | over-the-counter |

PARP | poly ADP ribose polymerase |

PBM | pharmacy benefit manager |

Pharmacia | Pharmacia Corporation |

PP&E | property, plant & equipment |

PsA | psoriatic arthritis |

Quarterly Report on Form 10-Q | Quarterly Report on Form 10-Q for the quarterly period ended June 30, 2019 |

RA | rheumatoid arthritis |

RCC | renal cell carcinoma |

R&D | research and development |

ROU | right of use |

Sandoz | Sandoz, Inc., a division of Novartis AG |

SEC | U.S. Securities and Exchange Commission |

SFJ | SFJ Pharmaceuticals Group |

Shire | Shire International GmbH |

SI&A | selling, informational and administrative |

S&P | Standard and Poor’s |

TCJA | legislation commonly referred to as the U.S. Tax Cuts and Jobs Act of 2017 |

Therachon | Therachon Holding AG |

UC | ulcerative colitis |

U.K. | United Kingdom |

U.S. | United States |

ViiV | ViiV Healthcare Limited |

WRDM | Worldwide Research, Development and Medical |

4

PART I - FINANCIAL INFORMATION

Item 1. Financial Statements

PFIZER INC. AND SUBSIDIARY COMPANIES

CONDENSED CONSOLIDATED STATEMENTS OF INCOME

(UNAUDITED)

Three Months Ended | Six Months Ended | |||||||||||||||

(MILLIONS, EXCEPT PER COMMON SHARE DATA) | June 30, 2019 | July 1, 2018 | June 30, 2019 | July 1, 2018 | ||||||||||||

Revenues | $ | 13,264 | $ | 13,466 | $ | 26,382 | $ | 26,373 | ||||||||

Costs and expenses: | ||||||||||||||||

Cost of sales(a) | 2,576 | 2,916 | 5,009 | 5,479 | ||||||||||||

Selling, informational and administrative expenses(a) | 3,511 | 3,542 | 6,850 | 6,954 | ||||||||||||

Research and development expenses(a) | 1,842 | 1,797 | 3,544 | 3,540 | ||||||||||||

Amortization of intangible assets | 1,184 | 1,191 | 2,367 | 2,387 | ||||||||||||

Restructuring charges and certain acquisition-related costs | (115 | ) | 44 | (69 | ) | 87 | ||||||||||

Other (income)/deductions––net | 126 | (551 | ) | 218 | (728 | ) | ||||||||||

Income from continuing operations before provision/(benefit) for taxes on income | 4,141 | 4,527 | 8,463 | 8,654 | ||||||||||||

Provision/(benefit) for taxes on income | (915 | ) | 648 | (481 | ) | 1,204 | ||||||||||

Income from continuing operations | 5,056 | 3,879 | 8,945 | 7,450 | ||||||||||||

Discontinued operations––net of tax | — | — | — | (1 | ) | |||||||||||

Net income before allocation to noncontrolling interests | 5,056 | 3,879 | 8,945 | 7,449 | ||||||||||||

Less: Net income attributable to noncontrolling interests | 10 | 7 | 15 | 16 | ||||||||||||

Net income attributable to Pfizer Inc. | $ | 5,046 | $ | 3,872 | $ | 8,929 | $ | 7,432 | ||||||||

Earnings per common share––basic: | ||||||||||||||||

Income from continuing operations attributable to Pfizer Inc. common shareholders | $ | 0.91 | $ | 0.66 | $ | 1.59 | $ | 1.26 | ||||||||

Discontinued operations––net of tax | — | — | — | — | ||||||||||||

Net income attributable to Pfizer Inc. common shareholders | $ | 0.91 | $ | 0.66 | $ | 1.59 | $ | 1.26 | ||||||||

Earnings per common share––diluted: | ||||||||||||||||

Income from continuing operations attributable to Pfizer Inc. common shareholders | $ | 0.89 | $ | 0.65 | $ | 1.56 | $ | 1.24 | ||||||||

Discontinued operations––net of tax | — | — | — | — | ||||||||||||

Net income attributable to Pfizer Inc. common shareholders | $ | 0.89 | $ | 0.65 | $ | 1.56 | $ | 1.24 | ||||||||

Weighted-average shares––basic | 5,562 | 5,866 | 5,598 | 5,911 | ||||||||||||

Weighted-average shares––diluted | 5,672 | 5,952 | 5,711 | 6,004 | ||||||||||||

(a) | Excludes amortization of intangible assets, except as disclosed in Note 9A. Identifiable Intangible Assets and Goodwill: Identifiable Intangible Assets. |

Amounts may not add due to rounding.

See Notes to Condensed Consolidated Financial Statements.

5

PFIZER INC. AND SUBSIDIARY COMPANIES

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(UNAUDITED)

Three Months Ended | Six Months Ended | |||||||||||||||

(MILLIONS OF DOLLARS) | June 30, 2019 | July 1, 2018 | June 30, 2019 | July 1, 2018 | ||||||||||||

Net income before allocation to noncontrolling interests | $ | 5,056 | $ | 3,879 | $ | 8,945 | $ | 7,449 | ||||||||

Foreign currency translation adjustments, net | (485 | ) | (699 | ) | (161 | ) | 59 | |||||||||

Reclassification adjustments | — | (35 | ) | 2 | (20 | ) | ||||||||||

(485 | ) | (734 | ) | (159 | ) | 39 | ||||||||||

Unrealized holding gains/(losses) on derivative financial instruments, net | (176 | ) | 127 | 91 | 13 | |||||||||||

Reclassification adjustments for (gains)/losses included in net income(a) | (81 | ) | 310 | (343 | ) | 354 | ||||||||||

(256 | ) | 437 | (252 | ) | 367 | |||||||||||

Unrealized holding gains/(losses) on available-for-sale securities, net | (7 | ) | (374 | ) | 33 | (214 | ) | |||||||||

Reclassification adjustments for (gains)/losses included in net income(a) | 26 | 143 | 37 | (31 | ) | |||||||||||

Reclassification adjustments for unrealized gains included in Retained earnings(b) | — | — | — | (462 | ) | |||||||||||

19 | (231 | ) | 70 | (707 | ) | |||||||||||

Benefit plans: actuarial gains/(losses), net | (4 | ) | (57 | ) | (4 | ) | 106 | |||||||||

Reclassification adjustments related to amortization | 60 | 61 | 121 | 123 | ||||||||||||

Reclassification adjustments related to settlements, net | 2 | 30 | 2 | 67 | ||||||||||||

Other | 41 | 107 | 18 | 21 | ||||||||||||

100 | 141 | 137 | 316 | |||||||||||||

Benefit plans: prior service costs and other, net | (1 | ) | — | (1 | ) | — | ||||||||||

Reclassification adjustments related to amortization of prior service costs and other, net | (46 | ) | (46 | ) | (93 | ) | (92 | ) | ||||||||

Reclassification adjustments related to curtailments of prior service costs and other, net | — | (7 | ) | — | (13 | ) | ||||||||||

Other | 1 | (1 | ) | 2 | 1 | |||||||||||

(46 | ) | (53 | ) | (92 | ) | (104 | ) | |||||||||

Other comprehensive loss, before tax | (669 | ) | (440 | ) | (296 | ) | (88 | ) | ||||||||

Tax provision/(benefit) on other comprehensive loss | (59 | ) | 173 | (34 | ) | 605 | ||||||||||

Other comprehensive loss before allocation to noncontrolling interests | $ | (610 | ) | $ | (613 | ) | $ | (262 | ) | $ | (693 | ) | ||||

Comprehensive income before allocation to noncontrolling interests | $ | 4,446 | $ | 3,266 | $ | 8,683 | $ | 6,755 | ||||||||

Less: Comprehensive income/(loss) attributable to noncontrolling interests | 12 | (4 | ) | 13 | 6 | |||||||||||

Comprehensive income attributable to Pfizer Inc. | $ | 4,434 | $ | 3,270 | $ | 8,669 | $ | 6,750 | ||||||||

(a) | Reclassified into Other (income)/deductions—net and Cost of sales in the condensed consolidated statements of income. For additional information on amounts reclassified into Cost of sales, see Note 7E. Financial Instruments: Derivative Financial Instruments and Hedging Activities. |

(b) | For additional information, see Notes to Consolidated Financial Statements—Note 1B. Basis of Presentation and Significant Accounting Policies: Adoption of New Accounting Standards in 2018 in our 2018 Financial Report. |

Amounts may not add due to rounding.

See Notes to Condensed Consolidated Financial Statements.

6

PFIZER INC. AND SUBSIDIARY COMPANIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(MILLIONS OF DOLLARS) | June 30, 2019 | December 31, 2018 | ||||||

(Unaudited) | ||||||||

Assets | ||||||||

Cash and cash equivalents | $ | 1,784 | $ | 1,139 | ||||

Short-term investments | 11,128 | 17,694 | ||||||

Trade accounts receivable, less allowance for doubtful accounts: 2019—$540; 2018—$541 | 9,793 | 8,025 | ||||||

Inventories | 8,233 | 7,508 | ||||||

Current tax assets | 3,723 | 3,374 | ||||||

Other current assets | 2,535 | 2,461 | ||||||

Assets held for sale | 9,877 | 9,725 | ||||||

Total current assets | 47,073 | 49,926 | ||||||

Long-term investments | 2,905 | 2,767 | ||||||

Property, plant and equipment, less accumulated depreciation: 2019—$16,389; 2018—$16,591 | 13,521 | 13,385 | ||||||

Identifiable intangible assets, less accumulated amortization | 33,024 | 35,211 | ||||||

Goodwill | 53,352 | 53,411 | ||||||

Noncurrent deferred tax assets and other noncurrent tax assets | 1,935 | 1,924 | ||||||

Other noncurrent assets | 4,388 | 2,799 | ||||||

Total assets | $ | 156,199 | $ | 159,422 | ||||

Liabilities and Equity | ||||||||

Short-term borrowings, including current portion of long-term debt: 2019—$2,139; 2018—$4,776 | $ | 10,507 | $ | 8,831 | ||||

Trade accounts payable | 4,002 | 4,674 | ||||||

Dividends payable | 1,991 | 2,047 | ||||||

Income taxes payable | 1,536 | 1,265 | ||||||

Accrued compensation and related items | 1,875 | 2,397 | ||||||

Other current liabilities | 10,110 | 10,753 | ||||||

Liabilities held for sale | 2,009 | 1,890 | ||||||

Total current liabilities | 32,030 | 31,858 | ||||||

Long-term debt | 36,168 | 32,909 | ||||||

Pension benefit obligations, net | 4,982 | 5,272 | ||||||

Postretirement benefit obligations, net | 1,310 | 1,338 | ||||||

Noncurrent deferred tax liabilities | 3,180 | 3,700 | ||||||

Other taxes payable | 12,421 | 14,737 | ||||||

Other noncurrent liabilities | 6,183 | 5,850 | ||||||

Total liabilities | 96,274 | 95,664 | ||||||

Commitments and Contingencies | ||||||||

Preferred stock | 18 | 19 | ||||||

Common stock | 468 | 467 | ||||||

Additional paid-in capital | 86,963 | 86,253 | ||||||

Treasury stock | (110,786 | ) | (101,610 | ) | ||||

Retained earnings | 94,440 | 89,554 | ||||||

Accumulated other comprehensive loss | (11,535 | ) | (11,275 | ) | ||||

Total Pfizer Inc. shareholders’ equity | 59,568 | 63,407 | ||||||

Equity attributable to noncontrolling interests | 357 | 351 | ||||||

Total equity | 59,924 | 63,758 | ||||||

Total liabilities and equity | $ | 156,199 | $ | 159,422 | ||||

Amounts may not add due to rounding.

See Notes to Condensed Consolidated Financial Statements.

7

PFIZER INC. AND SUBSIDIARY COMPANIES

CONDENSED CONSOLIDATED STATEMENTS OF EQUITY

PFIZER INC. SHAREHOLDERS | |||||||||||||||||||||||||||||||||||||||||||||

Preferred Stock | Common Stock | Treasury Stock | |||||||||||||||||||||||||||||||||||||||||||

(MILLIONS, EXCEPT PREFERRED SHARES) | Shares | Stated Value | Shares | Par Value | Add’l Paid-In Capital | Shares | Cost | Retained Earnings | Accum. Other Comp. Loss | Share- holders’ Equity | Non-controlling interests | Total Equity | |||||||||||||||||||||||||||||||||

Balance, March 31, 2019 | 466 | $ | 19 | 9,358 | $ | 468 | $ | 86,635 | (3,801 | ) | $ | (110,781 | ) | $ | 93,388 | $ | (10,923 | ) | $ | 58,806 | $ | 352 | $ | 59,158 | |||||||||||||||||||||

Net income | 5,046 | 5,046 | 10 | 5,056 | |||||||||||||||||||||||||||||||||||||||||

Other comprehensive income/(loss), net of tax | (613 | ) | (613 | ) | 3 | (610 | ) | ||||||||||||||||||||||||||||||||||||||

Cash dividends declared: | |||||||||||||||||||||||||||||||||||||||||||||

Common stock | (3,994 | ) | (3,994 | ) | (3,994 | ) | |||||||||||||||||||||||||||||||||||||||

Preferred stock | — | — | — | ||||||||||||||||||||||||||||||||||||||||||

Noncontrolling interests | — | (8 | ) | (8 | ) | ||||||||||||||||||||||||||||||||||||||||

Share-based payment transactions | 5 | — | 329 | — | (6 | ) | 324 | 324 | |||||||||||||||||||||||||||||||||||||

Purchases of common stock | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||

Preferred stock conversions and redemptions | (8 | ) | — | (1 | ) | — | — | (1 | ) | (1 | ) | ||||||||||||||||||||||||||||||||||

Other | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||

Balance, June 30, 2019 | 458 | $ | 18 | 9,363 | $ | 468 | $ | 86,963 | (3,801 | ) | $ | (110,786 | ) | $ | 94,440 | $ | (11,535 | ) | $ | 59,568 | $ | 357 | $ | 59,924 | |||||||||||||||||||||

PFIZER INC. SHAREHOLDERS | |||||||||||||||||||||||||||||||||||||||||||||

Preferred Stock | Common Stock | Treasury Stock | |||||||||||||||||||||||||||||||||||||||||||

(MILLIONS, EXCEPT PREFERRED SHARES) | Shares | Stated Value | Shares | Par Value | Add’l Paid-In Capital | Shares | Cost | Retained Earnings | Accum. Other Comp. Loss | Share- holders’ Equity | Non-controlling interests | Total Equity | |||||||||||||||||||||||||||||||||

Balance April 1, 2018 | 513 | $ | 21 | 9,299 | $ | 465 | $ | 84,599 | (3,437 | ) | $ | (95,460 | ) | $ | 89,961 | $ | (9,402 | ) | $ | 70,184 | $ | 358 | $ | 70,541 | |||||||||||||||||||||

Net income | 3,872 | 3,872 | 7 | 3,879 | |||||||||||||||||||||||||||||||||||||||||

Other comprehensive income/(loss), net of tax | (602 | ) | (602 | ) | (11 | ) | (613 | ) | |||||||||||||||||||||||||||||||||||||

Cash dividends declared: | |||||||||||||||||||||||||||||||||||||||||||||

Common stock | (3,970 | ) | (3,970 | ) | (3,970 | ) | |||||||||||||||||||||||||||||||||||||||

Preferred stock | — | — | — | ||||||||||||||||||||||||||||||||||||||||||

Noncontrolling interests | — | (7 | ) | (7 | ) | ||||||||||||||||||||||||||||||||||||||||

Share-based payment transactions | 4 | — | 300 | — | (4 | ) | 297 | 297 | |||||||||||||||||||||||||||||||||||||

Purchases of common stock | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||

Preferred stock conversions and redemptions | (11 | ) | — | (1 | ) | — | — | (1 | ) | (1 | ) | ||||||||||||||||||||||||||||||||||

Other | — | — | — | (2 | ) | — | (2 | ) | — | (2 | ) | ||||||||||||||||||||||||||||||||||

Balance, July 1, 2018 | 502 | $ | 20 | 9,303 | $ | 465 | $ | 84,898 | (3,438 | ) | $ | (95,463 | ) | $ | 89,860 | $ | (10,003 | ) | $ | 69,778 | $ | 346 | $ | 70,124 | |||||||||||||||||||||

Amounts may not add due to rounding.

See Notes to Condensed Consolidated Financial Statements.

8

PFIZER INC. AND SUBSIDIARY COMPANIES

CONDENSED CONSOLIDATED STATEMENTS OF EQUITY

PFIZER INC. SHAREHOLDERS | |||||||||||||||||||||||||||||||||||||||||||||

Preferred Stock | Common Stock | Treasury Stock | |||||||||||||||||||||||||||||||||||||||||||

(MILLIONS, EXCEPT PREFERRED SHARES) | Shares | Stated Value | Shares | Par Value | Add’l Paid-In Capital | Shares | Cost | Retained Earnings | Accum. Other Comp. Loss | Share- holders’ Equity | Non-controlling interests | Total Equity | |||||||||||||||||||||||||||||||||

Balance, January 1, 2019 | 478 | $ | 19 | 9,332 | $ | 467 | $ | 86,253 | (3,615 | ) | $ | (101,610 | ) | $ | 89,554 | $ | (11,275 | ) | $ | 63,407 | $ | 351 | $ | 63,758 | |||||||||||||||||||||

Net income | 8,929 | 8,929 | 15 | 8,945 | |||||||||||||||||||||||||||||||||||||||||

Other comprehensive income/(loss), net of tax | (260 | ) | (260 | ) | (2 | ) | (262 | ) | |||||||||||||||||||||||||||||||||||||

Cash dividends declared: | |||||||||||||||||||||||||||||||||||||||||||||

Common stock | (4,062 | ) | (4,062 | ) | (4,062 | ) | |||||||||||||||||||||||||||||||||||||||

Preferred stock | (1 | ) | (1 | ) | (1 | ) | |||||||||||||||||||||||||||||||||||||||

Noncontrolling interests | — | (8 | ) | (8 | ) | ||||||||||||||||||||||||||||||||||||||||

Share-based payment transactions | 31 | 2 | 712 | (7 | ) | (312 | ) | 402 | 402 | ||||||||||||||||||||||||||||||||||||

Purchases of common stock | (180 | ) | (8,865 | ) | (8,865 | ) | (8,865 | ) | |||||||||||||||||||||||||||||||||||||

Preferred stock conversions and redemptions | (20 | ) | (1 | ) | (1 | ) | — | — | (2 | ) | (2 | ) | |||||||||||||||||||||||||||||||||

Other(a) | — | — | — | 19 | — | 19 | — | 19 | |||||||||||||||||||||||||||||||||||||

Balance, June 30, 2019 | 458 | $ | 18 | 9,363 | $ | 468 | $ | 86,963 | (3,801 | ) | $ | (110,786 | ) | $ | 94,440 | $ | (11,535 | ) | $ | 59,568 | $ | 357 | $ | 59,924 | |||||||||||||||||||||

PFIZER INC. SHAREHOLDERS | |||||||||||||||||||||||||||||||||||||||||||||

Preferred Stock | Common Stock | Treasury Stock | |||||||||||||||||||||||||||||||||||||||||||

(MILLIONS, EXCEPT PREFERRED SHARES) | Shares | Stated Value | Shares | Par Value | Add’l Paid-In Capital | Shares | Cost | Retained Earnings | Accum. Other Comp. Loss | Share- holders’ Equity | Non-controlling interests | Total Equity | |||||||||||||||||||||||||||||||||

Balance, January 1, 2018 | 524 | $ | 21 | 9,275 | $ | 464 | $ | 84,278 | (3,296 | ) | $ | (89,425 | ) | $ | 85,291 | $ | (9,321 | ) | $ | 71,308 | $ | 348 | $ | 71,656 | |||||||||||||||||||||

Net income | 7,432 | 7,432 | 16 | 7,449 | |||||||||||||||||||||||||||||||||||||||||

Other comprehensive income/(loss), net of tax | (682 | ) | (682 | ) | (11 | ) | (693 | ) | |||||||||||||||||||||||||||||||||||||

Cash dividends declared: | |||||||||||||||||||||||||||||||||||||||||||||

Common stock | (4,035 | ) | (4,035 | ) | (4,035 | ) | |||||||||||||||||||||||||||||||||||||||

Preferred stock | (1 | ) | (1 | ) | (1 | ) | |||||||||||||||||||||||||||||||||||||||

Noncontrolling interests | — | (7 | ) | (7 | ) | ||||||||||||||||||||||||||||||||||||||||

Share-based payment transactions | 28 | 1 | 621 | 3 | 25 | 648 | 648 | ||||||||||||||||||||||||||||||||||||||

Purchases of common stock | (145 | ) | (6,063 | ) | (6,063 | ) | (6,063 | ) | |||||||||||||||||||||||||||||||||||||

Preferred stock conversions and redemptions | (22 | ) | (1 | ) | (1 | ) | — | — | (2 | ) | (2 | ) | |||||||||||||||||||||||||||||||||

Other(b) | — | — | — | 1,172 | — | 1,173 | — | 1,172 | |||||||||||||||||||||||||||||||||||||

Balance, July 1, 2018 | 502 | $ | 20 | 9,303 | $ | 465 | $ | 84,898 | (3,438 | ) | $ | (95,463 | ) | $ | 89,860 | $ | (10,003 | ) | $ | 69,778 | $ | 346 | $ | 70,124 | |||||||||||||||||||||

(a) | Represents the cumulative effect of the adoption of a new accounting standard for leases in the first quarter of 2019. For additional information, see Note 1B. Basis of Presentation and Significant Accounting Policies: Adoption of New Accounting Standards. |

(b) | Represents the cumulative effect of the adoption of new accounting standards in the first quarter of 2018 for revenues, financial assets and liabilities, income tax accounting, and the reclassification of certain tax effects from Accumulated other comprehensive income. For additional information, see Notes to Consolidated Financial Statements––Note 1B. Basis of Presentation and Significant Accounting Policies: Adoption of New Accounting Standards in 2018 in our 2018 Financial Report. |

Amounts may not add due to rounding.

See Notes to Condensed Consolidated Financial Statements.

9

PFIZER INC. AND SUBSIDIARY COMPANIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

Six Months Ended | ||||||||

(MILLIONS OF DOLLARS) | June 30, 2019 | July 1, 2018 | ||||||

Operating Activities | ||||||||

Net income before allocation to noncontrolling interests | $ | 8,945 | $ | 7,449 | ||||

Adjustments to reconcile net income before allocation to noncontrolling interests to net cash provided by operating activities: | ||||||||

Depreciation and amortization | 3,073 | 3,129 | ||||||

Asset write-offs and impairments | 178 | 41 | ||||||

TCJA impact(a) | (285 | ) | (68 | ) | ||||

Deferred taxes from continuing operations | (160 | ) | (500 | ) | ||||

Share-based compensation expense | 384 | 379 | ||||||

Benefit plan contributions in excess of income | (313 | ) | (826 | ) | ||||

Other adjustments, net | (462 | ) | (523 | ) | ||||

Other changes in assets and liabilities, net of acquisitions and divestitures | (7,051 | ) | (3,250 | ) | ||||

Net cash provided by operating activities | 4,309 | 5,830 | ||||||

Investing Activities | ||||||||

Purchases of property, plant and equipment | (939 | ) | (810 | ) | ||||

Purchases of short-term investments | (4,063 | ) | (3,122 | ) | ||||

Proceeds from redemptions/sales of short-term investments | 6,001 | 10,497 | ||||||

Net proceeds from redemptions/sales of short-term investments with original maturities of three months or less | 4,717 | 1,231 | ||||||

Purchases of long-term investments | (123 | ) | (1,070 | ) | ||||

Proceeds from redemptions/sales of long-term investments | 142 | 1,361 | ||||||

Acquisitions of intangible assets | (267 | ) | (32 | ) | ||||

Other investing activities, net | 179 | 138 | ||||||

Net cash provided by investing activities | 5,648 | 8,193 | ||||||

Financing Activities | ||||||||

Proceeds from short-term borrowings | 3,956 | 1,746 | ||||||

Principal payments on short-term borrowings | (2,375 | ) | (2,921 | ) | ||||

Net proceeds from short-term borrowings with original maturities of three months or less | 2,719 | 2,092 | ||||||

Proceeds from issuance of long-term debt | 4,942 | — | ||||||

Principal payments on long-term debt | (5,355 | ) | (3,104 | ) | ||||

Purchases of common stock | (8,865 | ) | (6,063 | ) | ||||

Cash dividends paid | (4,047 | ) | (4,021 | ) | ||||

Proceeds from exercise of stock options | 248 | 474 | ||||||

Other financing activities, net | (541 | ) | (831 | ) | ||||

Net cash used in financing activities | (9,318 | ) | (12,628 | ) | ||||

Effect of exchange-rate changes on cash and cash equivalents and restricted cash and cash equivalents | (28 | ) | (15 | ) | ||||

Net increase in cash and cash equivalents and restricted cash and cash equivalents | 612 | 1,381 | ||||||

Cash and cash equivalents and restricted cash and cash equivalents, beginning | 1,225 | 1,431 | ||||||

Cash and cash equivalents and restricted cash and cash equivalents, end | $ | 1,837 | $ | 2,811 | ||||

Supplemental Cash Flow Information | ||||||||

Non-cash transactions: | ||||||||

Equity investment in Allogene received in exchange for Pfizer's allogeneic CAR T developmental program assets(b) | $ | — | $ | 92 | ||||

Cash paid (received) during the period for: | ||||||||

Income taxes | 2,136 | 1,197 | ||||||

Interest paid | 809 | 724 | ||||||

Interest rate hedges | (72 | ) | (71 | ) | ||||

(a) | As a result of the enactment of the TCJA in December 2017, Pfizer’s Provision for taxes on income for (i) the six months ended June 30, 2019 was favorably impacted by approximately $285 million, primarily as a result of additional guidance issued by the U.S. Department of Treasury and (ii) the six months ended July 1, 2018 was favorably impacted by approximately $68 million, primarily related to certain tax initiatives associated with the lower U.S. tax rate as a result of the TCJA. |

(b) | For additional information, see Notes to Consolidated Financial Statements––Note 2B. Acquisitions, Divestitures, Assets and Liabilities Held for Sale, Licensing Arrangements, Research and Development and Collaborative Arrangements, Equity-Method Investments and Privately Held Investment: Divestitures in our 2018 Financial Report. |

Amounts may not add due to rounding.

See Notes to Condensed Consolidated Financial Statements.

10

PFIZER INC. AND SUBSIDIARY COMPANIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

Note 1. Basis of Presentation and Significant Accounting Policies

A. Basis of Presentation

See the Glossary of Defined Terms at the beginning of this Quarterly Report on Form 10-Q for terms used throughout the condensed consolidated financial statements and related notes in this Quarterly Report on Form 10-Q.

We prepared the condensed consolidated financial statements following the requirements of the SEC for interim reporting. As permitted under those rules, certain footnotes or other financial information that are normally required by U.S. GAAP can be condensed or omitted.

The financial information included in our condensed consolidated financial statements for subsidiaries operating outside the U.S. is as of and for the three and six months ended May 26, 2019 and May 27, 2018. The financial information included in our condensed consolidated financial statements for U.S. subsidiaries is as of and for the three and six months ended June 30, 2019 and July 1, 2018.

Revenues, expenses, assets and liabilities can vary during each quarter of the year. Therefore, the results and trends in these interim financial statements may not be representative of those for the full year.

We are responsible for the unaudited financial statements included in this Quarterly Report on Form 10-Q. The interim financial statements include all normal and recurring adjustments that are considered necessary for the fair statement of results for the interim periods presented. The information included in this Quarterly Report on Form 10-Q should be read in conjunction with the consolidated financial statements and accompanying notes included in our 2018 Financial Report.

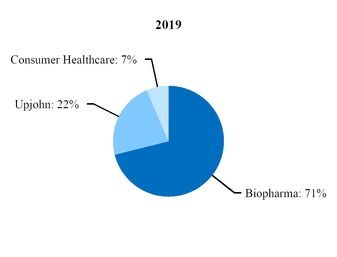

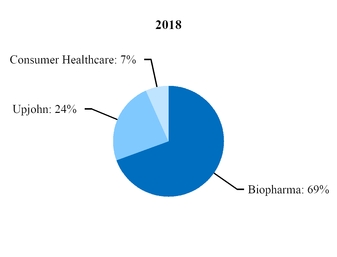

At the beginning of our 2019 fiscal year, we began to manage our commercial operations through a new global structure consisting of three business segments––Pfizer Biopharmaceuticals Group (Biopharma), Upjohn and through July 31, 2019, Consumer Healthcare. Biopharma and Upjohn are the only reportable segments. We have revised prior-period segment information to reflect the reorganization. For additional information, see Note 13.

Certain amounts in the condensed consolidated financial statements and associated notes may not add due to rounding. All percentages have been calculated using unrounded amounts.

In the first quarter of 2019, as of January 1, 2019, we adopted four new accounting standards. See Note 1B for further information.

Our recent significant business development activities include:

• | Formation of a New Consumer Healthcare Joint Venture––On July 31, 2019, which fell in the third fiscal quarter of 2019, we closed the transaction in which we and GSK combined our respective consumer healthcare businesses into a new consumer healthcare joint venture that operates globally under the GSK Consumer Healthcare name. Assets and liabilities associated with our Consumer Healthcare business were reclassified as held for sale in the consolidated balance sheets as of June 30, 2019 and December 31, 2018. |

• | Acquisition of Array BioPharma Inc.––On July 30, 2019, which fell in the third fiscal quarter of 2019, we acquired Array, a commercial stage biopharmaceutical company focused on the discovery, development and commercialization of targeted small molecule medicines to treat cancer and other diseases of high unmet need, for $48 per share in cash, for a total enterprise value of approximately $11.4 billion. We financed the majority of the transaction with debt and the balance with existing cash. |

• | Agreement to Combine Upjohn with Mylan––On July 29, 2019, which fell in the third fiscal quarter of 2019, we announced that we entered into a definitive agreement to combine Upjohn with Mylan, creating a new global pharmaceutical company. Under the terms of the agreement, which is structured as an all-stock, Reverse Morris Trust transaction, Upjohn is expected to be spun off or split off to Pfizer’s shareholders and simultaneously combined with Mylan. Pfizer shareholders would own 57% of the combined new company, and Mylan shareholders would own 43%. The transaction is expected to be tax free to Pfizer and Pfizer shareholders. The transaction is anticipated to close in mid-2020, subject to Mylan shareholder approval and customary closing conditions, including receipt of regulatory approvals. |

11

PFIZER INC. AND SUBSIDIARY COMPANIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

• | Acquisition of Therachon Holding AG––On July 1, 2019, which fell in the third fiscal quarter of 2019, we acquired all the remaining shares of Therachon, a privately-held clinical-stage biotechnology company focused on rare diseases, with assets in development for the treatment of achondroplasia, a genetic condition and the most common form of short-limb dwarfism, for $340 million upfront, plus potential milestone payments of up to $470 million, contingent on the achievement of key milestones in the development and commercialization of the lead asset TA-46. In 2018, Pfizer acquired 3% of Therachon’s outstanding shares. |

For additional information, see Note 2 below and Notes to Consolidated Financial Statements––Note 2. Acquisitions, Divestitures, Assets and Liabilities Held for Sale, Licensing Arrangements, Research and Development and Collaborative Arrangements, Equity-Method Investments and Privately Held Investment in Pfizer’s 2018 Financial Report.

B. Adoption of New Accounting Standards

On January 1, 2019, we adopted four new accounting standards.

Leases––On January 1, 2019, we adopted a new accounting standard for leases and changed our lease policies accordingly. Under the new standard, the most significant change is the requirement of balance sheet recognition of ROU assets and lease liabilities by lessees for those leases classified as operating leases. We adopted the new accounting standard utilizing the modified retrospective method using a simplified transition approach, and, therefore, no adjustments were made to our prior period financial statements. We have elected the package of practical expedients for transition which are permitted in the new standard. Accordingly, we did not reassess whether (i) any expired or existing contracts are or contain leases under the new standard, (ii) classification of leases as operating leases or capital leases would be different under the new standard, or (iii) any initial direct costs would have met the definition of initial direct costs under the new standard. Additionally, we did not elect to use hindsight in determining the lease term for existing leases as of January 1, 2019. We recorded noncurrent ROU assets of $1.4 billion and current and noncurrent operating lease liabilities of $1.4 billion as of January 1, 2019. We also recorded the cumulative effect of adopting the standard as an adjustment to increase the opening balance of Retained earnings by $30 million on a pre-tax basis ($20 million after-tax), relating to previously deferred sale-leaseback gains that can be recognized under the new rules.

Adopting the standard related to leases impacted our prior period condensed consolidated balance sheet as follows: | ||||||||||||

(MILLIONS OF DOLLARS) | As Previously Reported Balance at December 31, 2018 | Effect of Change Higher/(Lower) | Balance at January 1, 2019 | |||||||||

Other current assets | $ | 2,461 | $ | (1 | ) | $ | 2,460 | |||||

Noncurrent deferred tax assets and other noncurrent tax assets | 1,924 | (11 | ) | 1,913 | ||||||||

Other noncurrent assets | 2,799 | 1,351 | 4,149 | |||||||||

Other current liabilities | 10,753 | 258 | 11,011 | |||||||||

Other noncurrent liabilities | 5,850 | 1,060 | 6,910 | |||||||||

Retained earnings | 89,554 | 20 | 89,574 | |||||||||

Adoption of the standard related to leases did not have a material impact on our condensed consolidated statements of income or condensed consolidated statements of cash flows for the six months ended June 30, 2019. For additional information, see Note 1D.

Amortization Period for Certain Callable Debt Securities Held at a Premium––We prospectively adopted the standard, which shortens the amortization period for certain callable debt securities held at a premium. The new guidance requires the premium to be amortized to the earliest call date. We do not have any investments with features subject to this standard and, therefore, there was no impact to our condensed consolidated financial statements from the adoption of this new standard.

Accounting for Certain Financial Instruments with Characteristics of Liabilities and Equity and Accounting for Certain Financial Instruments with Down Round Features––We prospectively adopted the standard, which changes the accounting for warrants or convertible instruments that include a down round feature. We do not have any financial instruments with features subject to this standard and, therefore, there was no impact to our condensed consolidated financial statements from the adoption of this new standard.

Accounting for Share-Based Payments to Nonemployees––We prospectively adopted the standard, which simplifies the accounting for share-based payments to nonemployees by aligning it with the accounting for share-based payments to employees, with certain exceptions. Under the guidance, the measurement of equity-classified nonemployee awards will be

12

PFIZER INC. AND SUBSIDIARY COMPANIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

fixed at the grant date. We do not have any share-based awards issued to nonemployees and, therefore, there was no impact to our condensed consolidated financial statements from the adoption of this new standard.

On January 1, 2018, we adopted eleven new accounting standards. For additional information, see Notes to Consolidated Financial Statements––Note 1B. Basis of Presentation and Significant Accounting Policies: Adoption of New Accounting Standards in 2018 included in our 2018 Financial Report.

C. Revenues and Trade Accounts Receivable

Our accruals for Medicare rebates, Medicaid and related state program rebates, performance-based contract rebates, chargebacks, sales allowances and sales returns and cash discounts totaled $5.6 billion as of June 30, 2019 and $5.4 billion as of December 31, 2018.

The following table provides information about the balance sheet classification of these accruals: | ||||||||

(MILLIONS OF DOLLARS) | June 30, 2019 | December 31, 2018 | ||||||

Reserve against Trade accounts receivable, less allowance for doubtful accounts | $ | 1,226 | $ | 1,288 | ||||

Other current liabilities: | ||||||||

Accrued rebates | 3,256 | 3,208 | ||||||

Other accruals | 620 | 531 | ||||||

Other noncurrent liabilities | 472 | 399 | ||||||

Total accrued rebates and other accruals | $ | 5,574 | $ | 5,426 | ||||

D. Leases

On January 1, 2019, we adopted a new accounting standard for leases. For further information, see Note 1B.

We lease real estate, fleet, and equipment for use in our operations. Our leases generally have lease terms of 1 to 30 years, some of which include options to terminate or extend leases for up to 5 to 10 years or on a month-to-month basis. We include options that are reasonably certain to be exercised as part of the determination of lease terms. We may negotiate termination clauses in anticipation of any changes in market conditions, but generally these termination options are not exercised. Residual value guarantees are generally not included within our operating leases with the exception of some fleet leases. In addition to base rent payments, the leases may require us to pay directly for taxes and other non-lease components, such as insurance, maintenance and other operating expenses, which may be dependent on usage or vary month-to-month. Variable lease payments amounted to $59 million for the three months ended June 30, 2019 and $118 million for the six months ended June 30, 2019. We have elected the practical expedient in the new standard to not separate non-lease components from lease components in calculating the amounts of ROU assets and lease liabilities for all underlying asset classes.

We determine if an arrangement is a lease at inception of the contract in accordance with guidance detailed in the new standard and we perform the lease classification test as of the lease commencement date. ROU assets represent our right to use an underlying asset for the lease term and lease liabilities represent our obligation to make lease payments arising from the lease. Operating lease ROU assets and liabilities are recognized at commencement date based on the present value of lease payments over the lease term. As most of our leases do not provide an implicit rate, we use our estimated incremental borrowing rate based on the information available at commencement date in determining the present value of future payments.

For operating leases, the ROU assets and liabilities are presented in our condensed consolidated balance sheet as follows: | ||||||

(MILLIONS OF DOLLARS) | Balance Sheet Classification | Balance at June 30, 2019 | ||||

ROU assets | Other noncurrent assets | $ | 1,273 | |||

Lease liabilities (short-term) | Other current liabilities | 263 | ||||

Lease liabilities (long-term) | Other noncurrent liabilities | 1,026 | ||||

13

PFIZER INC. AND SUBSIDIARY COMPANIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

Our total lease costs are as follows: | ||||||||

Three Months Ended | Six Months Ended | |||||||

(MILLIONS OF DOLLARS) | June 30, 2019 | June 30, 2019 | ||||||

Operating lease cost | $ | 100 | $ | 200 | ||||

Variable lease cost | 59 | 118 | ||||||

Sublease income | (11 | ) | (21 | ) | ||||

Total lease cost | $ | 148 | $ | 297 | ||||

Other supplemental information includes the following: | |||||||||

(MILLIONS OF DOLLARS) | Weighted-Average Remaining Contractual Lease Term (Years) as of June 30, 2019 | Weighted-Average Discount Rate as of June 30, 2019 | Six Months Ended June 30, 2019 | ||||||

Operating leases | 7.1 | 3.7 | % | ||||||

Cash paid for amounts included in the measurement of lease liabilities: | |||||||||

Operating cash flows from operating leases | $ | 156 | |||||||

ROU assets obtained in exchange for new operating lease liabilities | $ | 122 | |||||||

The table below reconciles the undiscounted cash flows for the first five years and total of the remaining years to the operating lease liabilities recorded in the condensed consolidated balance sheet as of June 30, 2019: | ||||

(MILLIONS OF DOLLARS) | ||||

Period | Operating Lease Liabilities | |||

Next one year(a) | $ | 302 | ||

1-2 years | 254 | |||

2-3 years | 216 | |||

3-4 years | 171 | |||

4-5 years | 122 | |||

Thereafter | 419 | |||

Total undiscounted lease payments | 1,483 | |||

Less: Imputed interest | 195 | |||

Present Value of Minimum Lease Payments | 1,288 | |||

Less: Current portion | 263 | |||

Noncurrent portion | $ | 1,026 | ||

(a) |

In April 2018, we entered an agreement to lease space in an office building in New York City. We expect to take control of the property in 2021 and relocate our global headquarters to this new office building in 2022. Our future minimum rental commitment under this 20-year lease is approximately $1.7 billion.

Prior to our adoption of the new lease standard, rental expense, net of sublease income, was $301 million in 2018, $314 million in 2017 and $292 million in 2016.

As of December 31, 2018, the future minimum rental commitments under non-cancelable operating leases follow: | ||||||||||||||||||||||||

(MILLIONS OF DOLLARS) | 2019 | 2020 | 2021 | 2022 | 2023 | After 2023 | ||||||||||||||||||

Lease commitments | $ | 300 | $ | 252 | $ | 210 | $ | 267 | $ | 248 | $ | 2,040 | ||||||||||||

Note 2. Assets and Liabilities Held for Sale

On July 31, 2019, which fell in the third fiscal quarter of 2019, we closed the transaction in which we and GSK combined our respective consumer healthcare businesses into a new consumer healthcare joint venture that operates globally under the GSK Consumer Healthcare name. In exchange for contributing our Consumer Healthcare business, we received a 32% equity stake in the new company and GSK owns the remaining 68%. Upon the closing of the transaction, we deconsolidated our

14

PFIZER INC. AND SUBSIDIARY COMPANIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

Consumer Healthcare business and expect to recognize a gain in our fiscal third quarter of 2019 for the difference in the fair value of our 32% equity stake in the new company and the carrying value of our Consumer Healthcare business. We will account for our 32% equity stake in the new company as an equity-method investment. Assets and liabilities associated with our Consumer Healthcare business were reclassified as held for sale in the consolidated balance sheets as of June 30, 2019 and December 31, 2018. The Consumer Healthcare business assets held for sale are reported in Assets held for sale and Consumer Healthcare business liabilities held for sale are reported in Liabilities held for sale. This includes the Consumer Healthcare business tax assets and liabilities related to fully dedicated consumer healthcare subsidiaries.

The amounts associated with the Consumer Healthcare business, as well as other assets classified as held for sale consisted of the following: | ||||||||

(MILLIONS OF DOLLARS) | June 30, 2019 | December 31, 2018 | ||||||

Assets Held for Sale | ||||||||

Cash and cash equivalents | $ | 53 | $ | 32 | ||||

Trade accounts receivable, less allowance for doubtful accounts | 555 | 532 | ||||||

Inventories | 580 | 538 | ||||||

Other current assets | 56 | 56 | ||||||

PP&E | 714 | 675 | ||||||

Identifiable intangible assets, less accumulated amortization | 5,753 | 5,763 | ||||||

Goodwill | 1,965 | 1,972 | ||||||

Noncurrent deferred tax assets and other noncurrent tax assets | 55 | 54 | ||||||

Other noncurrent assets | 91 | 57 | ||||||

Total Consumer Healthcare assets held for sale | 9,821 | 9,678 | ||||||

Other assets held for sale(a) | 56 | 46 | ||||||

Assets held for sale | $ | 9,877 | $ | 9,725 | ||||

Liabilities Held for Sale | ||||||||

Trade accounts payable | $ | 348 | $ | 406 | ||||

Income taxes payable | 63 | 39 | ||||||

Accrued compensation and related items | 79 | 93 | ||||||

Other current liabilities | 334 | 353 | ||||||

Pension benefit obligations, net | 41 | 39 | ||||||

Postretirement benefit obligations, net | 34 | 33 | ||||||

Noncurrent deferred tax liabilities | 1,036 | 870 | ||||||

Other noncurrent liabilities | 74 | 56 | ||||||

Total Consumer Healthcare liabilities held for sale | $ | 2,009 | $ | 1,890 | ||||

(a) | Other assets held for sale consist of PP&E. |

As a part of Pfizer, pre-tax income on a management business unit basis for the Consumer Healthcare business was $274 million for the second quarter of 2019 and $554 million for the six months ended June 30, 2019, and $249 million for the second quarter of 2018 and $514 million for the six months ended July 1, 2018.

Note 3. Restructuring Charges and Other Costs Associated with Acquisitions and Cost-Reduction/Productivity Initiatives

We incur significant costs in connection with acquiring, integrating and restructuring businesses and in connection with our global cost-reduction/productivity initiatives. For example:

• | In connection with acquisition activity, we typically incur costs associated with executing the transactions, integrating the acquired operations (which may include expenditures for consulting and the integration of systems and processes), and restructuring the combined company (which may include charges related to employees, assets and activities that will not continue in the combined company); and |

• | In connection with our cost-reduction/productivity initiatives, we typically incur costs and charges associated with site closings and other facility rationalization actions, workforce reductions and the expansion of shared services, including the development of global systems. |

All of our businesses and functions may be impacted by these actions, including sales and marketing, manufacturing and R&D, as well as groups such as information technology, shared services and corporate operations.

15

PFIZER INC. AND SUBSIDIARY COMPANIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

2017-2019 Initiatives and Organizing for Growth

During 2018, as we reviewed our business opportunities and challenges and the way in which we think about our business operations, we determined that at the start of our 2019 fiscal year, we would begin operating under our new commercial structure, which reorganized our operations into three businesses––Biopharma, a science-based innovative medicines business; Upjohn, a global, primarily off-patent branded and generic established medicines business; and through July 31, 2019, a Consumer Healthcare business (see Note 13). To operate effectively in this structure and position ourselves for future growth, we are focused on creating a simpler, more efficient operating structure within each business as well as the functions that support them. Beginning in the fourth quarter of 2018, we reviewed previously planned initiatives and new initiatives to ensure that there was alignment around our new structure and combined the 2017-2019 initiatives with our current Organizing for Growth initiatives to form one cohesive plan. Initiatives for the combined program include activities related to the optimization of our manufacturing plant network, the centralization of our corporate and platform functions, and the simplification and optimization of our operating business structure and functions that support them. From 2017 through June 30, 2019, we incurred approximately $774 million associated with manufacturing optimization, and approximately $871 million associated with other activities.

In 2019, we expect restructuring, implementation and additional depreciation charges of about $600 million and, of that amount, we expect approximately 20% of the total charges will be non-cash.

Current-Period Key Activities

For the first six months of 2019, we incurred costs of $32 million composed of $180 million associated with the 2017-2019 and Organizing for Growth initiatives, $51 million associated with the integration of Hospira and income of $199 million primarily due to the reversal of certain accruals upon the effective favorable settlement of a U.S. IRS audit for multiple tax years and other acquisition-related initiatives.

The following table provides the components of costs associated with acquisitions and cost-reduction/productivity initiatives: | ||||||||||||||||

Three Months Ended | Six Months Ended | |||||||||||||||

(MILLIONS OF DOLLARS) | June 30, 2019 | July 1, 2018 | June 30, 2019 | July 1, 2018 | ||||||||||||

Restructuring charges/(credits): | ||||||||||||||||

Employee terminations | $ | (166 | ) | $ | (21 | ) | $ | (167 | ) | $ | (29 | ) | ||||

Asset impairments | (9 | ) | (6 | ) | — | (4 | ) | |||||||||

Exit costs | 31 | 3 | 34 | — | ||||||||||||

Restructuring credits(a) | (144 | ) | (24 | ) | (134 | ) | (33 | ) | ||||||||

Integration costs(b) | 29 | 68 | 64 | 120 | ||||||||||||

Restructuring charges and certain acquisition-related costs | (115 | ) | 44 | (69 | ) | 87 | ||||||||||

Net periodic benefit costs recorded in Other (income)/deductions––net | 4 | 29 | 10 | 61 | ||||||||||||

Additional depreciation––asset restructuring recorded in our condensed consolidated statements of income as follows(c): | ||||||||||||||||

Cost of sales | 7 | 13 | 15 | 30 | ||||||||||||

Selling, informational and administrative expenses | 1 | — | 2 | — | ||||||||||||

Research and development expenses | 2 | — | 5 | — | ||||||||||||

Total additional depreciation––asset restructuring | 10 | 13 | 23 | 31 | ||||||||||||

Implementation costs recorded in our condensed consolidated statements of income as follows(d): | ||||||||||||||||

Cost of sales | 17 | 20 | 31 | 36 | ||||||||||||

Selling, informational and administrative expenses | 16 | 16 | 25 | 34 | ||||||||||||

Research and development expenses | 9 | 7 | 13 | 13 | ||||||||||||

Total implementation costs | 42 | 44 | 69 | 82 | ||||||||||||

Total costs associated with acquisitions and cost-reduction/productivity initiatives | $ | (59 | ) | $ | 131 | $ | 32 | $ | 262 | |||||||

(a) | In the second quarter and first six months of 2019, restructuring credits mostly represent the reversal of certain accruals related to our acquisition of Wyeth upon the effective favorable settlement of a U.S. IRS audit for multiple tax years (see Note 5B). In the three and six months ended July 1, 2018, restructuring credits were associated with cost-reduction and productivity initiatives not associated with acquisitions, as well as acquisition-related costs, primarily associated with Hospira. |

16

PFIZER INC. AND SUBSIDIARY COMPANIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

The restructuring activities for 2019 are associated with the following:

• | For the second quarter of 2019, Biopharma ($62 million credit); Upjohn ($9 million credit); and Other ($74 million credit). |

• | For the first six months of 2019, Biopharma ($48 million credit); Upjohn ($22 million credit); and Other ($63 million credit). |

The restructuring activities for 2018 are associated with the following:

• | For the second quarter of 2018, total reportable segments ($10 million credit); and Other ($13 million credit). |

• | For the first six months of 2018, total reportable segments ($24 million credit); and Other ($9 million credit). At the beginning of fiscal 2019, we revised our operating segments and are unable to directly associate these prior-period restructuring charges with the new individual segments. |

(b) | Integration costs represent external, incremental costs directly related to integrating acquired businesses, and primarily include expenditures for consulting and the integration of systems and processes. In the second quarter and first six months of 2019 and 2018, integration costs were primarily related to our acquisition of Hospira. |

(c) | Additional depreciation––asset restructuring represents the impact of changes in the estimated useful lives of assets involved in restructuring actions. |

(d) | Implementation costs represent external, incremental costs directly related to implementing our non-acquisition-related cost-reduction/productivity initiatives. |

The following table provides the components of and changes in our restructuring accruals: | ||||||||||||||||

(MILLIONS OF DOLLARS) | Employee Termination Costs | Asset Impairment Charges | Exit Costs | Accrual | ||||||||||||

Balance, December 31, 2018(a) | $ | 1,203 | $ | — | $ | 49 | $ | 1,252 | ||||||||

Provision/(credit)(b) | (167 | ) | — | 34 | (134 | ) | ||||||||||

Utilization and other(c) | (303 | ) | — | (18 | ) | (321 | ) | |||||||||

Balance, June 30, 2019(d) | $ | 733 | $ | — | $ | 64 | $ | 797 | ||||||||

(a) | Included in Other current liabilities ($823 million) and Other noncurrent liabilities ($428 million). |

(b) | Includes the reversal of certain accruals related to our acquisition of Wyeth upon the effective favorable settlement of a U.S. IRS audit for multiple tax years. See Note 5B for additional information. |

(c) | Includes adjustments for foreign currency translation. |

(d) | Included in Other current liabilities ($593 million) and Other noncurrent liabilities ($204 million). |

Note 4. Other (Income)/Deductions—Net

The following table provides components of Other (income)/deductions––net: | ||||||||||||||||

Three Months Ended | Six Months Ended | |||||||||||||||

(MILLIONS OF DOLLARS) | June 30, 2019 | July 1, 2018 | June 30, 2019 | July 1, 2018 | ||||||||||||

Interest income(a) | $ | (59 | ) | $ | (80 | ) | (125 | ) | (157 | ) | ||||||

Interest expense(a) | 389 | 326 | 750 | 635 | ||||||||||||

Net interest expense | 330 | 245 | 625 | 478 | ||||||||||||

Royalty-related income(b) | (231 | ) | (121 | ) | (320 | ) | (217 | ) | ||||||||

Net gains on asset disposals | — | (15 | ) | (1 | ) | (22 | ) | |||||||||

Net gains recognized during the period on investments in equity securities(c) | (36 | ) | (257 | ) | (147 | ) | (375 | ) | ||||||||

Net realized losses on sales of investments in debt securities | — | 8 | — | 12 | ||||||||||||

Income from collaborations, out-licensing arrangements and sales of compound/product rights(d) | (22 | ) | (174 | ) | (104 | ) | (316 | ) | ||||||||

Net periodic benefit credits other than service costs(e) | (51 | ) | (84 | ) | (91 | ) | (166 | ) | ||||||||

Certain legal matters, net(f) | 15 | (88 | ) | 19 | (107 | ) | ||||||||||

Certain asset impairments(g) | 10 | 40 | 160 | 40 | ||||||||||||

Business and legal entity alignment costs(h) | 137 | 1 | 256 | 4 | ||||||||||||

Net losses on early retirement of debt(i) | — | — | 138 | 3 | ||||||||||||

Other, net(j) | (27 | ) | (106 | ) | (318 | ) | (64 | ) | ||||||||

Other (income)/deductions––net | $ | 126 | $ | (551 | ) | $ | 218 | $ | (728 | ) | ||||||

(a) | Interest income decreased in the second quarter and first six months of 2019, primarily driven by a lower investment balance. Interest expense increased in the second quarter and first six months of 2019, mainly as a result of higher short-term interest rates, as well as the retirement of lower-coupon debt and the issuance of new debt with a higher coupon than the debt outstanding for the comparative prior year periods. |

(b) | The increase in royalty-related income for the second quarter and first six months of 2019 is primarily due to a one-time favorable resolution in the second quarter of 2019 of a legal dispute for $82 million. |

(c) | The second quarter of 2018 included gains of $142 million and the first six months of 2018 included gains of $203 million related to our investment in ICU Medical stock. For additional information, see Note 7B. |

(d) | Includes income from upfront and milestone payments from our collaboration partners and income from out-licensing arrangements and sales of compound/product rights. In the first six months of 2019, mainly includes $68 million in milestone income from Mylan Pharmaceuticals Inc. related to the FDA’s approval and launch of Wixela Inhub®, a generic of Advair Diskus® (fluticasone propionate and salmeterol inhalation powder). In the second quarter of 2018, primarily included, among other things, $88 million in milestone income from multiple licensees and an upfront payment to us of $75 million for the sale of |

17

PFIZER INC. AND SUBSIDIARY COMPANIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

an α-amino-3-hydroxy-5-methyl-4-isoxazolepropionic acid (AMPA) receptor potentiator for cognitive impairment associated with schizophrenia (CIAS) to Biogen Inc. In the first six months of 2018, mainly includes, among other things, all of the factors discussed above for the second quarter of 2018, as well as a $75 million milestone payment received from Shire related to their first dosing of a patient in a Phase 3 clinical trial of a compound out-licensed by Pfizer to Shire for the treatment of ulcerative colitis, and a $40 million milestone payment from Merck in conjunction with the approval of ertugliflozin in the EU.

(e) | For additional information, see Note 10. |

(f) | In the second quarter and first six months of 2018, primarily represented the reversal of a legal accrual where a loss was no longer deemed probable. |

(g) | The second quarter and first six months of 2019 include an intangible asset impairment charge of $10 million and the second quarter and first six months of 2018 included an intangible asset impairment charge of $31 million, which are all related to a finite-lived developed technology right, acquired in connection with our acquisition of Anacor, for the treatment for toenail fungus marketed in the U.S. market only, associated with Biopharma and reflect, among other things, updated commercial forecasts. The first six months of 2019 also includes intangible asset impairment charges of: (i) $90 million related to WRDM IPR&D, which relates to a pre-clinical stage asset from our acquisition of Bamboo for gene therapies for the potential treatment of patients with certain rare diseases; and (ii) $40 million related to a Biopharma developed technology right, acquired in connection with our acquisition of King, for government defense products. The WRDM IPR&D intangible asset impairment charge was the result of a determination to not use certain Bamboo IPR&D acquired in future rare disease development. The intangible asset impairment charge related to the Biopharma developed technology right reflects, among other things, updated commercial forecasts including manufacturing cost assumptions. In addition, the first six months of 2019, includes other asset impairments of $20 million. |

(h) | In the second quarter and first six months of 2019, represents incremental costs associated with the design, planning and implementation of our new organizational structure, effective in the beginning of 2019, and primarily includes consulting, legal, tax and advisory services. In the second quarter and first six months of 2018, represents expenses for changes to our infrastructure to align our commercial operations that existed through December 31, 2018, including costs to internally separate our businesses into distinct legal entities, as well as to streamline our intercompany supply operations to better support each business. |

(i) | In the first six months of 2019, represents net losses due to the early retirement of debt in the first quarter of 2019, inclusive of the related termination of cross-currency swaps. |

(j) | The second quarter of 2019 includes, among other things, charges of $81 million, reflecting the change in the fair value of contingent consideration, dividend income of $76 million from our investment in ViiV and $25 million of income from insurance recoveries related to Hurricane Maria. The first six months of 2019 includes, among other things, dividend income of $140 million from our investment in ViiV and $50 million of income from insurance recoveries related to Hurricane Maria. The second quarter of 2018 included, among other things, dividend income of $76 million from our investment in ViiV, and charges of $23 million, reflecting the change in the fair value of contingent consideration. The first six months of 2018 included, among other things, dividend income of $135 million from our investment in ViiV, and charges of $135 million reflecting the change in the fair value of contingent consideration. The second quarter and first six months of 2018 also included a non-cash $50 million pre-tax gain on the contribution of Pfizer’s allogeneic CAR T development program assets obtained from Cellectis S.A. and Les Laboratoires Servier SAS in connection with our contribution agreement entered into with Allogene, and a non-cash $17 million gain on the cash settlement of a liability that we incurred in April 2018 upon the EU approval of Mylotarg. |

The following table provides additional information about the intangible assets that were impaired during 2019 in Other (income)/deductions: | ||||||||||||||||||||

Fair Value(a) | Six Months Ended June 30, 2019 | |||||||||||||||||||

(MILLIONS OF DOLLARS) | Amount | Level 1 | Level 2 | Level 3 | Impairment | |||||||||||||||

Intangible assets––IPR&D(b) | $ | — | $ | — | $ | — | $ | — | $ | 90 | ||||||||||

Intangible assets––Developed technology rights(b) | 13 | — | — | 13 | 50 | |||||||||||||||

Total | $ | 13 | $ | — | $ | — | $ | 13 | $ | 140 | ||||||||||

(a) | The fair value amount is presented as of the date of impairment, as these assets are not measured at fair value on a recurring basis. |

(b) | Reflects intangible assets written down to fair value in the first six months of 2019. Fair value was determined using the income approach, specifically the multi-period excess earnings method, also known as the discounted cash flow method. We started with a forecast of all the expected net cash flows associated with the asset and then applied an asset-specific discount rate to arrive at a net present value amount. Some of the more significant estimates and assumptions inherent in this approach include: the amount and timing of the projected net cash flows, which includes the expected impact of competitive, legal and/or regulatory forces on the product; the discount rate, which seeks to reflect the various risks inherent in the projected cash flows; and the tax rate, which seeks to incorporate the geographic diversity of the projected cash flows. |

Note 5. Tax Matters

A. Taxes on Income from Continuing Operations

During the second quarter of 2019, Pfizer reached settlement of disputed issues at the IRS Office of Appeals, thereby settling all issues related to U.S. tax returns of Pfizer for the years 2009-2010. As a result of settling these years, in the second quarter of 2019 we recorded a benefit of approximately $1.4 billion, representing tax and interest.

Our effective tax rate for continuing operations was (22.1)% for the second quarter of 2019, compared to 14.3% for the second quarter of 2018 and was (5.7)% for the first six months of 2019, compared to 13.9% for the first six months of 2018.

The lower effective tax rate for the second quarter and first six months of 2019 in comparison with the same periods in 2018 was primarily due to:

• | an increase in tax benefits associated with the resolution of certain tax positions pertaining to prior years, primarily resulting from the aforementioned favorable settlement with the IRS; |

18

PFIZER INC. AND SUBSIDIARY COMPANIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

• | the tax benefit recorded as a result of additional guidance issued by the U.S. Department of Treasury related to the enactment of the TCJA, as well as |

• | the favorable change in the jurisdictional mix of earnings as a result of operating fluctuations in the normal course of business. |

Our estimated $15 billion repatriation tax liability on accumulated post-1986 foreign earnings for which we plan to elect, with the filing of our 2018 U.S. Federal Consolidated Income Tax Return, payment over eight years through 2026 is reported in Income taxes payable (approximately $750 million) and the remaining liability is reported in Other taxes payable in our consolidated balance sheet as of June 30, 2019. The first installment of $750 million was paid in April 2019. Our obligations may vary as a result of changes in our uncertain tax positions and/or availability of attributes such as foreign tax and other credit carryforwards.

B. Tax Contingencies

We are subject to income tax in many jurisdictions, and a certain degree of estimation is required in recording the assets and liabilities related to income taxes. All of our tax positions are subject to audit by the local taxing authorities in each tax jurisdiction. These tax audits can involve complex issues, interpretations and judgments and the resolution of matters may span multiple years, particularly if subject to negotiation or litigation. Our assessments are based on estimates and assumptions that have been deemed reasonable by management, but our estimates of unrecognized tax benefits and potential tax benefits may not be representative of actual outcomes, and variation from such estimates could materially affect our financial statements in the period of settlement or when the statutes of limitations expire, as we treat these events as discrete items in the period of resolution.

The U.S. is one of our major tax jurisdictions, and we are regularly audited by the IRS:

• | During the second quarter of 2019, Pfizer reached settlement of disputed issues at the IRS Office of Appeals, thereby settling all issues related to U.S. tax returns of Pfizer for the years 2009-2010. As a result of settling these years, in the second quarter of 2019 we recorded a benefit of approximately $1.4 billion, representing tax and interest. |

• | With respect to Pfizer, tax years 2011-2015 are currently under audit. Tax years 2016-2019 are open, but not under audit. All other tax years are closed. |

In addition to the open audit years in the U.S., we have open audit years in other major tax jurisdictions, such as Canada (2013-2019), Japan (2017-2019), Europe (2011-2019, primarily reflecting Ireland, the United Kingdom, France, Italy, Spain and Germany), Latin America (1998-2019, primarily reflecting Brazil) and Puerto Rico (2014-2019).

19

PFIZER INC. AND SUBSIDIARY COMPANIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

C. Tax Provision/(Benefit) on Other Comprehensive Loss

The following table provides the components of Tax provision/(benefit) on other comprehensive loss: | ||||||||||||||||

Three Months Ended | Six Months Ended | |||||||||||||||

(MILLIONS OF DOLLARS) | June 30, 2019 | July 1, 2018 | June 30, 2019 | July 1, 2018 | ||||||||||||

Foreign currency translation adjustments, net(a) | $ | (17 | ) | $ | 101 | $ | 10 | $ | 67 | |||||||

Unrealized holding gains/(losses) on derivative financial instruments, net | (53 | ) | 8 | 6 | 4 | |||||||||||

Reclassification adjustments for (gains)/losses included in net income | (4 | ) | 72 | (59 | ) | 65 | ||||||||||

Reclassification adjustments of certain tax effects from AOCI to Retained earnings(b) | — | — | — | 1 | ||||||||||||

(57 | ) | 79 | (53 | ) | 70 | |||||||||||

Unrealized holding gains/(losses) on available-for-sale securities, net | (1 | ) | (48 | ) | 4 | (28 | ) | |||||||||

Reclassification adjustments for (gains)/losses included in net income | 3 | 20 | 5 | (2 | ) | |||||||||||

Reclassification adjustments for tax on unrealized gains from AOCI to Retained earnings(c) | — | — | — | (45 | ) | |||||||||||

2 | (29 | ) | 9 | (76 | ) | |||||||||||

Benefit plans: actuarial gains/(losses), net | (1 | ) | (13 | ) | (1 | ) | 25 | |||||||||

Reclassification adjustments related to amortization | 15 | 14 | 18 | 28 | ||||||||||||

Reclassification adjustments related to settlements, net | — | 7 | 1 | 15 | ||||||||||||

Reclassification adjustments of certain tax effects from AOCI to Retained earnings(b) | — | — | — | 637 | ||||||||||||

Other | 8 | 27 | 3 | 6 | ||||||||||||

23 | 34 | 21 | 712 | |||||||||||||

Benefit plans: prior service costs and other, net | — | — | — | — | ||||||||||||

Reclassification adjustments related to amortization of prior service costs and other, net | (11 | ) | (11 | ) | (22 | ) | (22 | ) | ||||||||

Reclassification adjustments related to curtailments of prior service costs and other, net | — | 4 | — | (3 | ) | |||||||||||

Reclassification adjustments of certain tax effects from AOCI to Retained earnings(b) | — | — | — | (144 | ) | |||||||||||

Other | — | (6 | ) | — | — | |||||||||||

(11 | ) | (13 | ) | (22 | ) | (168 | ) | |||||||||

Tax provision/(benefit) on other comprehensive loss | $ | (59 | ) | $ | 173 | $ | (34 | ) | $ | 605 | ||||||

(a) | Taxes are not provided for foreign currency translation adjustments relating to investments in international subsidiaries that will be held indefinitely. |

(b) | For additional information on the adoption of a new accounting standard related to reclassification of certain tax effects from AOCI, see Notes to Consolidated Financial Statements––Note 1B. Basis of Presentation and Significant Accounting Policies: Adoption of New Accounting Standards in 2018 in our 2018 Financial Report. |

(c) | For additional information on the adoption of a new accounting standard related to financial assets and liabilities, see Notes to Consolidated Financial Statements––Note 1B. Basis of Presentation and Significant Accounting Policies: Adoption of New Accounting Standards in 2018 in our 2018 Financial Report. |

Note 6. Accumulated Other Comprehensive Loss, Excluding Noncontrolling Interests

The following table provides the changes, net of tax, in Accumulated other comprehensive loss: | ||||||||||||||||||||||||

Net Unrealized Gains/(Losses) | Benefit Plans | |||||||||||||||||||||||

(MILLIONS OF DOLLARS) | Foreign Currency Translation Adjustments | Derivative Financial Instruments | Available-For-Sale Securities | Actuarial Gains/(Losses) | Prior Service (Costs)/Credits and Other | Accumulated Other Comprehensive Income/(Loss) | ||||||||||||||||||

Balance, December 31, 2018 | $ | (6,075 | ) | $ | 167 | $ | (68 | ) | $ | (6,027 | ) | $ | 728 | $ | (11,275 | ) | ||||||||

Other comprehensive income/(loss)(a) | (167 | ) | (200 | ) | 61 | 116 | (70 | ) | (260 | ) | ||||||||||||||

Balance, June 30, 2019 | $ | (6,242 | ) | $ | (33 | ) | $ | (8 | ) | $ | (5,911 | ) | $ | 658 | $ | (11,535 | ) | |||||||

(a) | Amounts do not include foreign currency translation adjustments attributable to noncontrolling interests of $2 million loss for the first six months of 2019. |

As of June 30, 2019, with respect to derivative financial instruments, the amount of unrealized pre-tax net gains on derivative financial instruments estimated to be reclassified into income within the next 12 months is approximately $153 million. The net gains are expected to be offset primarily by net losses from reclassification adjustments related to foreign currency exchange-denominated forecasted intercompany inventory sales and available-for-sale debt securities.

20

PFIZER INC. AND SUBSIDIARY COMPANIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

Note 7. Financial Instruments

A. Fair Value Measurements

Financial Assets and Liabilities Measured at Fair Value on a Recurring Basis

The following table presents the financial assets and liabilities measured at fair value using a market approach on a recurring basis by balance sheet categories and fair value hierarchy level as defined in Notes to Consolidated Financial Statements––Note 1E. Basis of Presentation and Significant Accounting Policies: Fair Value in Pfizer’s 2018 Financial Report: | ||||||||||||||||||||||||

June 30, 2019 | December 31, 2018 | |||||||||||||||||||||||

(MILLIONS OF DOLLARS) | Total | Level 1 | Level 2 | Total | Level 1 | Level 2 | ||||||||||||||||||

Financial assets measured at fair value on a recurring basis: | ||||||||||||||||||||||||

Short-term investments | ||||||||||||||||||||||||

Classified as equity securities: | ||||||||||||||||||||||||

Money market funds | $ | 4,727 | $ | — | $ | 4,727 | $ | 1,571 | $ | — | $ | 1,571 | ||||||||||||

Equity(a) | 26 | 15 | 12 | 29 | 17 | 11 | ||||||||||||||||||

4,753 | 15 | 4,739 | 1,600 | 17 | 1,583 | |||||||||||||||||||