Philip Morris International Inc. - Quarter Report: 2023 March (Form 10-Q)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

| ☑ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||

For the quarterly period ended March 31, 2023

OR

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||

For the transition period from to

Commission File Number 001-33708

Philip Morris International Inc. | ||||||||||||||

(Exact name of registrant as specified in its charter)

| Virginia | 13-3435103 | ||||

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||

| 677 Washington Blvd, Suite 1100 | Stamford | Connecticut | 06901 | ||||||||

| (Address of principal executive offices) | (Zip Code) | ||||||||||

| Registrant’s telephone number, including area code | (203) | 905-2410 | ||||||

Former name, former address and former fiscal year, if changed since last report

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

| Common Stock, no par value | PM | New York Stock Exchange | ||||||||||||

| 2.125% Notes due 2023 | PM23B | New York Stock Exchange | ||||||||||||

| 3.600% Notes due 2023 | PM23A | New York Stock Exchange | ||||||||||||

| 2.875% Notes due 2024 | PM24 | New York Stock Exchange | ||||||||||||

| 2.875% Notes due 2024 | PM24C | New York Stock Exchange | ||||||||||||

| 0.625% Notes due 2024 | PM24B | New York Stock Exchange | ||||||||||||

| 3.250% Notes due 2024 | PM24A | New York Stock Exchange | ||||||||||||

| 2.750% Notes due 2025 | PM25 | New York Stock Exchange | ||||||||||||

| 3.375% Notes due 2025 | PM25A | New York Stock Exchange | ||||||||||||

| 2.750% Notes due 2026 | PM26A | New York Stock Exchange | ||||||||||||

| 2.875% Notes due 2026 | PM26 | New York Stock Exchange | ||||||||||||

| 0.125% Notes due 2026 | PM26B | New York Stock Exchange | ||||||||||||

| 3.125% Notes due 2027 | PM27 | New York Stock Exchange | ||||||||||||

| 3.125% Notes due 2028 | PM28 | New York Stock Exchange | ||||||||||||

| 2.875% Notes due 2029 | PM29 | New York Stock Exchange | ||||||||||||

| 3.375% Notes due 2029 | PM29A | New York Stock Exchange | ||||||||||||

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

| 0.800% Notes due 2031 | PM31 | New York Stock Exchange | ||||||||||||

| 3.125% Notes due 2033 | PM33 | New York Stock Exchange | ||||||||||||

| 2.000% Notes due 2036 | PM36 | New York Stock Exchange | ||||||||||||

| 1.875% Notes due 2037 | PM37A | New York Stock Exchange | ||||||||||||

| 6.375% Notes due 2038 | PM38 | New York Stock Exchange | ||||||||||||

| 1.450% Notes due 2039 | PM39 | New York Stock Exchange | ||||||||||||

| 4.375% Notes due 2041 | PM41 | New York Stock Exchange | ||||||||||||

| 4.500% Notes due 2042 | PM42 | New York Stock Exchange | ||||||||||||

| 3.875% Notes due 2042 | PM42A | New York Stock Exchange | ||||||||||||

| 4.125% Notes due 2043 | PM43 | New York Stock Exchange | ||||||||||||

| 4.875% Notes due 2043 | PM43A | New York Stock Exchange | ||||||||||||

| 4.250% Notes due 2044 | PM44 | New York Stock Exchange | ||||||||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer þ Accelerated filer ☐

Non-accelerated filer ☐ Smaller reporting company ☐

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No þ

At April 21, 2023, there were 1,552,196,682 shares outstanding of the registrant’s common stock, no par value per share.

1

PHILIP MORRIS INTERNATIONAL INC.

TABLE OF CONTENTS

| Page No. | ||||||||

| PART I - | ||||||||

| Item 1. | ||||||||

| Condensed Consolidated Statements of Earnings for the | ||||||||

Three Months Ended March 31, 2023 and 2022 | ||||||||

| Condensed Consolidated Statements of Comprehensive Earnings for the | ||||||||

| Three Months Ended March 31, 2023 and 2022 | ||||||||

| Condensed Consolidated Balance Sheets at | ||||||||

March 31, 2023 and December 31, 2022 | ||||||||

| Condensed Consolidated Statements of Cash Flows for the | ||||||||

| Three Months Ended March 31, 2023 and 2022 | ||||||||

| Condensed Consolidated Statements of Stockholders’ (Deficit) Equity for the | ||||||||

| Three Months Ended March 31, 2023 and 2022 | ||||||||

| Item 2. | ||||||||

| Item 4. | ||||||||

| PART II - | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 2. | ||||||||

| Item 6. | ||||||||

In this report, “PMI,” “we,” “us” and “our” refer to Philip Morris International Inc. and its subsidiaries.

Trademarks and service marks in this report are the registered property of, or licensed by, the subsidiaries of Philip Morris International Inc. and are italicized.

2

PART I – FINANCIAL INFORMATION

Item 1. Financial Statements.

Philip Morris International Inc. and Subsidiaries

Condensed Consolidated Statements of Earnings

(in millions of dollars, except per share data)

(Unaudited)

| For the Three Months Ended March 31, | |||||||||||

| 2023 | 2022 | ||||||||||

Revenues including excise taxes (includes $1,845 in 2023 and $1,629 in 2022 from related parties) | $ | 19,318 | $ | 19,341 | |||||||

| Excise taxes on products | 11,299 | 11,595 | |||||||||

Net revenues (includes $873 in 2023 and $678 in 2022 from related parties) (Note 14) | 8,019 | 7,746 | |||||||||

| Cost of sales (Note 3) | 3,038 | 2,608 | |||||||||

| Gross profit | 4,981 | 5,138 | |||||||||

| Marketing, administration and research costs (Notes 3 & 17) | 2,250 | 1,840 | |||||||||

| Operating income | 2,731 | 3,298 | |||||||||

| Interest expense, net | 230 | 154 | |||||||||

| Pension and other employee benefit costs (Note 5) | 22 | 4 | |||||||||

| Earnings before income taxes | 2,479 | 3,140 | |||||||||

| Provision for income taxes | 428 | 619 | |||||||||

| Equity investments and securities (income)/loss, net | (51) | 56 | |||||||||

| Net earnings | 2,102 | 2,465 | |||||||||

| Net earnings attributable to noncontrolling interests | 107 | 134 | |||||||||

| Net earnings attributable to PMI | $ | 1,995 | $ | 2,331 | |||||||

Per share data (Note 8): | |||||||||||

| Basic earnings per share | $ | 1.28 | $ | 1.50 | |||||||

| Diluted earnings per share | $ | 1.28 | $ | 1.50 | |||||||

See notes to condensed consolidated financial statements.

3

Philip Morris International Inc. and Subsidiaries

Condensed Consolidated Statements of Comprehensive Earnings

(in millions of dollars)

(Unaudited)

| For the Three Months Ended March 31, | ||||||||||||||

| 2023 | 2022 | |||||||||||||

| Net earnings | $ | 2,102 | $ | 2,465 | ||||||||||

| Other comprehensive earnings (losses), net of income taxes: | ||||||||||||||

Change in currency translation adjustments: | ||||||||||||||

Unrealized gains (losses), net of income taxes of $52 in 2023 and $(31) in 2022 | (255) | (194) | ||||||||||||

Change in net loss and prior service cost: | ||||||||||||||

Net gains (losses) and prior service costs, net of income taxes of $(1) in 2023 and $0 in 2022 | 2 | — | ||||||||||||

Amortization of net losses, prior service costs and net transition costs, net of income taxes of $(7) in 2023 and $(13) in 2022 | 25 | 55 | ||||||||||||

Change in fair value of derivatives accounted for as hedges: | ||||||||||||||

Gains (losses) recognized, net of income taxes of $(16) in 2023 and $(20) in 2022 | 59 | 110 | ||||||||||||

(Gains) losses transferred to earnings, net of income taxes of $6 in 2023 and $2 in 2022 | (29) | (9) | ||||||||||||

| Total other comprehensive earnings (losses) | (198) | (38) | ||||||||||||

Total comprehensive earnings | 1,904 | 2,427 | ||||||||||||

| Less comprehensive earnings (losses) attributable to: | ||||||||||||||

| Noncontrolling interests | (36) | 279 | ||||||||||||

| Comprehensive earnings attributable to PMI | $ | 1,940 | $ | 2,148 | ||||||||||

See notes to condensed consolidated financial statements.

4

Philip Morris International Inc. and Subsidiaries

Condensed Consolidated Balance Sheets

(in millions of dollars)

(Unaudited)

| March 31, 2023 | December 31, 2022 | ||||||||||

| ASSETS | |||||||||||

| Cash and cash equivalents | $ | 2,428 | $ | 3,207 | |||||||

Trade receivables (less allowances of $52 in 2023 and $42 in 2022) (1) | 3,642 | 3,850 | |||||||||

Other receivables (less allowances of $33 in 2023 and $32 in 2022) | 957 | 906 | |||||||||

Inventories: | |||||||||||

| Leaf tobacco | 1,848 | 1,674 | |||||||||

| Other raw materials | 2,276 | 2,028 | |||||||||

| Finished product | 6,588 | 6,184 | |||||||||

| 10,712 | 9,886 | ||||||||||

| Other current assets | 1,832 | 1,770 | |||||||||

Total current assets | 19,571 | 19,619 | |||||||||

Property, plant and equipment, at cost | 15,777 | 15,443 | |||||||||

| Less: accumulated depreciation | 8,989 | 8,733 | |||||||||

| 6,788 | 6,710 | ||||||||||

| Goodwill (Note 6) | 19,866 | 19,655 | |||||||||

| Other intangible assets, net (Note 6) | 6,732 | 6,732 | |||||||||

| Equity investments (Note 14) | 4,504 | 4,431 | |||||||||

| Deferred income taxes | 585 | 603 | |||||||||

Other assets (less allowances of $20 in 2023 and $20 in 2022) (Note 2) | 4,014 | 3,931 | |||||||||

| TOTAL ASSETS | $ | 62,060 | $ | 61,681 | |||||||

(1) Includes trade receivables from related parties of $708 million and $688 million as of March 31, 2023, and December 31, 2022, respectively (less allowances of $17 million as of March 31, 2023 and $7 million as of December 31, 2022). For further details, see Note 14. Related Parties - Equity Investments and Other.

See notes to condensed consolidated financial statements.

Continued

5

Philip Morris International Inc. and Subsidiaries

Condensed Consolidated Balance Sheets (Continued)

(in millions of dollars, except share data)

(Unaudited)

| March 31, 2023 | December 31, 2022 | ||||||||||

| LIABILITIES | |||||||||||

| Short-term borrowings (Note 12) | $ | 4,803 | $ | 5,637 | |||||||

| Current portion of long-term debt (Note 12) | 1,902 | 2,611 | |||||||||

| Accounts payable | 3,945 | 4,076 | |||||||||

| Accrued liabilities: | |||||||||||

| Marketing and selling | 662 | 695 | |||||||||

| Taxes, except income taxes | 5,133 | 7,440 | |||||||||

| Employment costs | 939 | 1,168 | |||||||||

| Dividends payable | 1,991 | 1,990 | |||||||||

| Other | 2,675 | 2,679 | |||||||||

| Income taxes | 935 | 1,040 | |||||||||

| Total current liabilities | 22,985 | 27,336 | |||||||||

Long-term debt (Note 12) | 40,416 | 34,875 | |||||||||

| Deferred income taxes | 1,822 | 1,956 | |||||||||

| Employment costs | 1,977 | 1,984 | |||||||||

| Income taxes and other liabilities | 1,913 | 1,841 | |||||||||

| Total liabilities | 69,113 | 67,992 | |||||||||

Contingencies (Note 10) | |||||||||||

STOCKHOLDERS’ (DEFICIT) EQUITY | |||||||||||

Common stock, no par value (2,109,316,331 shares issued in 2023 and 2022) | — | — | |||||||||

| Additional paid-in capital | 2,188 | 2,230 | |||||||||

| Earnings reinvested in the business | 34,303 | 34,289 | |||||||||

| Accumulated other comprehensive losses (Note 13) | (9,614) | (9,559) | |||||||||

| 26,877 | 26,960 | ||||||||||

Less: cost of repurchased stock (557,164,352 and 559,098,620 shares in 2023 and 2022, respectively) | 35,801 | 35,917 | |||||||||

| Total PMI stockholders’ deficit | (8,924) | (8,957) | |||||||||

| Noncontrolling interests | 1,871 | 2,646 | |||||||||

| Total stockholders’ deficit | (7,053) | (6,311) | |||||||||

| TOTAL LIABILITIES AND STOCKHOLDERS’ (DEFICIT) EQUITY | $ | 62,060 | $ | 61,681 | |||||||

See notes to condensed consolidated financial statements.

6

Philip Morris International Inc. and Subsidiaries

Condensed Consolidated Statements of Cash Flows

(in millions of dollars)

(Unaudited)

| For the Three Months Ended March 31, | |||||||||||

| 2023 | 2022 | ||||||||||

| CASH PROVIDED BY (USED IN) OPERATING ACTIVITIES | |||||||||||

| Net earnings | $ | 2,102 | $ | 2,465 | |||||||

| Adjustments to reconcile net earnings to operating cash flows: | |||||||||||

| Depreciation, amortization and impairment of intangibles | 299 | 253 | |||||||||

| Deferred income tax (benefit) provision | (96) | (1) | |||||||||

| Asset impairment and exit costs, net of cash paid (Note 17) | 102 | (28) | |||||||||

| Cash effects of changes, net of the effects from acquired companies: | |||||||||||

Receivables, net (1) | 245 | (553) | |||||||||

| Inventories | (783) | (232) | |||||||||

| Accounts payable | (145) | 14 | |||||||||

| Accrued liabilities and other current assets | (2,705) | (835) | |||||||||

| Income taxes | (88) | (93) | |||||||||

| Pension plan contributions (Note 5) | (45) | (34) | |||||||||

| Other | 159 | 162 | |||||||||

| Net cash provided by (used in) operating activities | (955) | 1,118 | |||||||||

| CASH PROVIDED BY (USED IN) INVESTING ACTIVITIES | |||||||||||

| Capital expenditures | (279) | (229) | |||||||||

| Equity investments | (8) | (20) | |||||||||

| Net investment hedges and other derivatives (Note 7) | (164) | 121 | |||||||||

| Other | (140) | (68) | |||||||||

| Net cash used in investing activities | (591) | (196) | |||||||||

(1) Includes amounts from related parties of $(76) million and $(202) million for March 31, 2023 and 2022, respectively

See notes to condensed consolidated financial statements.

Continued

7

Philip Morris International Inc. and Subsidiaries

Condensed Consolidated Statements of Cash Flows (Continued)

(in millions of dollars)

(Unaudited)

| For the Three Months Ended March 31, | |||||||||||

| 2023 | 2022 | ||||||||||

| CASH PROVIDED BY (USED IN) FINANCING ACTIVITIES | |||||||||||

| Short-term borrowing activity by original maturity: | |||||||||||

| Net issuances (repayments) - maturities of 90 days or less | $ | 3,361 | $ | 1,916 | |||||||

| Issuances - maturities longer than 90 days | 358 | 305 | |||||||||

| Repayments - maturities longer than 90 days | (138) | — | |||||||||

| Repayments under credit facilities related to Swedish Match AB acquisition | (4,430) | — | |||||||||

| Long-term debt proceeds | 5,203 | — | |||||||||

| Long-term debt repaid | (682) | (496) | |||||||||

| Repurchases of common stock | — | (209) | |||||||||

| Dividends paid | (1,987) | (1,952) | |||||||||

| Payments to acquire Swedish Match AB noncontrolling interests (Note 2) | (883) | — | |||||||||

Noncontrolling interests activity and Other (Note 2) | 62 | (265) | |||||||||

| Net cash provided by (used in) financing activities | 864 | (701) | |||||||||

| Effect of exchange rate changes on cash, cash equivalents and restricted cash | (89) | (95) | |||||||||

Cash, cash equivalents and restricted cash (1): | |||||||||||

| Increase (Decrease) | (771) | 126 | |||||||||

| Balance at beginning of period | 3,217 | 4,500 | |||||||||

| Balance at end of period | $ | 2,446 | $ | 4,626 | |||||||

(1) The amounts for cash, cash equivalents and restricted cash shown above include restricted cash of $18 million and $4 million as of March 31, 2023 and 2022, respectively, and $10 million and $4 million as of December 31, 2022 and 2021, respectively, which were included in other current assets in the condensed consolidated balance sheets.

See notes to condensed consolidated financial statements.

8

Philip Morris International Inc. and Subsidiaries

Condensed Consolidated Statements of Stockholders’ (Deficit) Equity

For the Three Months Ended March 31, 2023 and 2022

(in millions of dollars, except per share amounts)

(Unaudited)

| PMI Stockholders’ (Deficit) Equity | |||||||||||||||||||||||||||||||||||||||||

| Common Stock | Additional Paid-in Capital | Earnings Reinvested in the Business | Accumulated Other Comprehensive Losses | Cost of Repurchased Stock | Noncontrolling Interests | Total | |||||||||||||||||||||||||||||||||||

| Balances, January 1, 2022 | $ | — | $ | 2,225 | $ | 33,082 | $ | (9,577) | $ | (35,836) | $ | 1,898 | $ | (8,208) | |||||||||||||||||||||||||||

| Net earnings | 2,331 | 134 | 2,465 | ||||||||||||||||||||||||||||||||||||||

| Other comprehensive earnings (losses), net of income taxes | (12) | (26) | (38) | ||||||||||||||||||||||||||||||||||||||

| Issuance of stock awards | (77) | 111 | 34 | ||||||||||||||||||||||||||||||||||||||

Dividends declared ($1.25 per share) | (1,945) | (1,945) | |||||||||||||||||||||||||||||||||||||||

| Dividends paid to noncontrolling interests | (101) | (101) | |||||||||||||||||||||||||||||||||||||||

| Common stock repurchased | (199) | (199) | |||||||||||||||||||||||||||||||||||||||

| Purchase of subsidiary shares from noncontrolling interests (Note 2) | (30) | (171) | (10) | (211) | |||||||||||||||||||||||||||||||||||||

| Balances, March 31, 2022 | $ | — | $ | 2,118 | $ | 33,468 | $ | (9,760) | $ | (35,924) | $ | 1,895 | $ | (8,203) | |||||||||||||||||||||||||||

| Balances, January 1, 2023 | $ | — | $ | 2,230 | $ | 34,289 | $ | (9,559) | $ | (35,917) | $ | 2,646 | $ | (6,311) | |||||||||||||||||||||||||||

| Net earnings | 1,995 | 107 | 2,102 | ||||||||||||||||||||||||||||||||||||||

| Other comprehensive earnings (losses), net of income taxes | (234) | 36 | (198) | ||||||||||||||||||||||||||||||||||||||

| Issuance of stock awards | (63) | 116 | 53 | ||||||||||||||||||||||||||||||||||||||

Dividends declared ($1.27 per share) | (1,981) | (1,981) | |||||||||||||||||||||||||||||||||||||||

| Dividends paid to noncontrolling interests | (93) | (93) | |||||||||||||||||||||||||||||||||||||||

| Sale (purchase) of subsidiary shares to/(from) noncontrolling interests (Note 2) | 21 | 179 | (825) | (625) | |||||||||||||||||||||||||||||||||||||

| Balances, March 31, 2023 | $ | — | $ | 2,188 | $ | 34,303 | $ | (9,614) | $ | (35,801) | $ | 1,871 | $ | (7,053) | |||||||||||||||||||||||||||

See notes to condensed consolidated financial statements.

9

Philip Morris International Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Note 1. Background and Basis of Presentation:

Background

Philip Morris International Inc. is a holding company incorporated in Virginia, U.S.A. (also referred to herein as the U.S., the United States or the United States of America), whose subsidiaries and affiliates and their licensees are primarily engaged in the manufacture and sale of cigarettes and smoke-free products. Throughout these financial statements, the term "PMI" refers to Philip Morris International Inc. and its subsidiaries.

Smoke-free products ("SFPs") is the term PMI primarily uses to refer to all of its products that are not combustible tobacco products, such as heat-not-burn, e-vapor, and oral nicotine. In addition, SFPs include wellness and healthcare products, as well as consumer accessories such as lighters and matches.

Reduced-risk products ("RRPs") is the term PMI uses to refer to products that present, are likely to present, or have the potential to present less risk of harm to smokers who switch to these products versus continuing smoking. PMI has a range of RRPs in various stages of development, scientific assessment and commercialization. PMI's RRPs are smoke-free products that contain and/or generate far lower quantities of harmful and potentially harmful constituents than found in cigarette smoke.

"Platform 1" is the term PMI uses to refer to PMI’s reduced-risk product that uses a precisely controlled heating device into which a specially designed and proprietary tobacco unit is inserted and heated to generate an aerosol.

Basis of Presentation

The interim condensed consolidated financial statements of PMI are unaudited. These interim condensed consolidated financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America ("U.S. GAAP") and such principles are applied on a consistent basis. Certain information and footnote disclosures normally included in annual financial statements prepared in accordance with U.S.GAAP have been omitted. It is the opinion of PMI’s management that all adjustments necessary for a fair statement of the interim results presented have been reflected therein. All such adjustments were of a normal recurring nature. Net revenues and net earnings attributable to PMI for any interim period are not necessarily indicative of results that may be expected for the entire year.

In the fourth quarter of 2022, PMI acquired a controlling interest of the total issued shares in Swedish Match AB (“Swedish Match”). The operating results of Swedish Match are included in a separate segment. For further details, see Note 2. Acquisitions and Note 9. Segment Reporting.

In the third quarter of 2021, PMI acquired Fertin Pharma A/S, Vectura Group plc. and OtiTopic, Inc. On March 31, 2022, PMI launched a Wellness and Healthcare business consolidating these entities, Vectura Fertin Pharma. The operating results of this business are reported in the Wellness and Healthcare segment. For further details, see Note 9. Segment Reporting.

To further support the growth of PMI's smoke-free business, reinforce consumer centricity, and increase the speed of innovation and deployment, in January 2023, PMI began managing its business in four geographical segments, down from six previously, in addition to its continuing Swedish Match and Wellness and Healthcare segments. The four geographical segments are as follows: Europe Region; South and Southeast Asia, Commonwealth of Independent States, Middle East and Africa Region ("SSEA, CIS & MEA"); East Asia, Australia, and PMI Duty Free Region ("EA, AU & PMI DF"); and Americas Region.

Certain prior years' amounts have been reclassified to conform with the current year's presentation. As a result of the new regional structure discussed above, certain goodwill amounts under the former six geographical segments were reallocated to the four geographical segments under the new structure. For further details, see Note 6. Goodwill and Other Intangible Assets, net. Following the Swedish Match acquisition and a review of PMI and Swedish Match’s combined product portfolio, PMI reclassified certain of its own products previously reported under its combustible tobacco product category to the newly created smoke-free product category to better reflect the characteristics of these products. For further details, see Note 9. Segment Reporting. These reclassifications did not impact PMI’s consolidated financial position, results of operations or cash flows in any of the periods presented.

These statements should be read in conjunction with the audited consolidated financial statements and related notes, which appear in PMI’s Annual Report on Form 10-K for the year ended December 31, 2022.

10

Philip Morris International Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Note 2. Acquisitions:

Transactions With Noncontrolling Interests

Turkey – In the first quarter of 2022, PMI acquired the remaining 25% stake of its holding in Philip Morris Tütün Mamulleri Sanayi ve Ticaret A.Ş. ("PMTM") (formerly Philsa Philip Morris Sabanci Sigara ve Tütüncülük Sanayi ve Ticaret A.Ş.) and 24.75% stake in Philip Morris Pazarlama ve Satiş A.Ş. ("PMPS") (formerly Philip Morris SA, Philip Morris Sabanci Pazarlama ve Satiş A.Ş.) from its Turkish partners, Sabanci Holding for a total acquisition price including transaction costs and remaining dividend entitlements of approximately $223 million. As a result of this acquisition, PMI owned 100% of these Turkish subsidiaries as of December 31, 2022. The purchase of the remaining stakes in these holdings resulted in a decrease to PMI's additional paid-in capital of $30 million and an increase to accumulated other comprehensive losses of $171 million primarily following the reclassification of accumulated currency translation losses from noncontrolling interests to PMI’s accumulated other comprehensive losses during the first quarter of 2022.

In January 2023, PMI sold the acquired stakes of its holdings in PMTM and PMPS to Pioneers Tutun Yatirim Anonim Sirketi (“Pioneers”) for a consideration of approximately $258 million, including transaction costs and dividend entitlements. The sale resulted in an increase to PMI's additional paid-in capital of $36 million and a decrease to accumulated other comprehensive losses of $179 million, following the reclassification of accumulated other comprehensive losses from PMI’s accumulated other comprehensive losses to noncontrolling interests.

Business Combinations

Swedish Match AB – On November 11, 2022 (the acquisition date), Philip Morris Holland Holdings B.V. (“PMHH”), a wholly owned subsidiary of PMI, acquired a controlling interest of 85.87% of the total issued shares in Swedish Match AB (“Swedish Match”) and acquired 94.81% of its outstanding shares as of December 31, 2022. The shares were acquired through acceptances of the tender offer and a series of open market and over-the-counter purchases. PMI funded the acquisition through cash on-hand and debt proceeds, as described in Note 12. Indebtedness. The aggregate cash paid as of the acquisition date was $14,460 million (or $13,976 million net of cash acquired), which was included in investing activities in the consolidated statements of cash flows for the year ended December 31, 2022. The cash paid in connection with the additional purchases of the noncontrolling interests after the acquisition date and through December 31, 2022 amounted to $1,495 million and was included in financing activities in the consolidated statements of cash flows for the year ended December 31, 2022.

In accordance with the Swedish Companies Act, PMI subsequently exercised its right to compulsorily redeem the remaining shares for which acceptances were not received and obtained legal title to 100% of the shares in Swedish Match on February 17, 2023. Cash paid in connection with such legal title, together with an immaterial amount attributable to open market purchases that were executed in December 2022 but settled in January 2023, amounted to $883 million and was included in financing activities in the condensed consolidated statements of cash flows for the three months ended March 31, 2023. While we have paid the referenced amounts and have acquired legal title to the shares, the redemption process will not be complete under the Swedish Companies Act until a final redemption price is determined by an arbitral tribunal. This process may take 6 to 12 months to complete, but we believe the likelihood it will result in additional payments to be remote.

Swedish Match is a market leader in oral nicotine delivery with a significant presence in the United States market. The acquisition will accelerate PMI’s transformation to become a smoke-free company with a comprehensive global smoke-free portfolio with leadership positions in heat-not-burn, and the fastest growing category of oral nicotine, with the potential for accelerated international expansion.

11

Philip Morris International Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Due to the timing of the acquisition, and limited access to detailed and disaggregated financial information of Swedish Match, the purchase price allocation is preliminary and it is likely subject to change, including the valuation of property, plant and equipment, intangible assets, income taxes and legal contingencies among other items. During the first quarter of 2023, PMI did not record any measurement period adjustments to the preliminary purchase price allocation. The following table summarizes the preliminary purchase price allocation for the fair value of assets acquired and liabilities assumed as of the acquisition date:

| (in millions) | |||||

| Cash and cash equivalents | $ | 484 | |||

| Trade receivables | 135 | ||||

| Other receivables | 53 | ||||

| Inventories | 444 | ||||

| Other current assets | 524 | ||||

| Property, plant and equipment | 627 | ||||

| Other intangible assets | 4,512 | ||||

| Other non-current assets | 214 | ||||

| Current portion of long-term debt | 224 | ||||

| Accounts payable | 120 | ||||

| Other current liabilities | 531 | ||||

| Income taxes | 14 | ||||

| Long-term debt | 1,126 | ||||

| Deferred income taxes | 1,253 | ||||

| Other non-current liabilities | 187 | ||||

| Identifiable net assets acquired | 3,538 | ||||

| Noncontrolling interest | 2,379 | ||||

| Goodwill | 13,301 | ||||

| Total consideration transferred | $ | 14,460 | |||

The total fair value step-up adjustment for inventories was $146 million, of which $125 million was recognized in cost of sales in the fourth quarter of 2022 and the remaining balance in the first quarter of 2023.

The fair value of long-term debt was determined using readily available market prices as of the acquisition date and the total purchase price adjustment of $(102) million is being amortized as an increase to interest expense, net over the lives of the related debt.

Goodwill is primarily attributable to future growth opportunities, anticipated synergies in the U.S. and intangible assets that did not qualify for separate recognition. The goodwill is not deductible for income tax purposes.

Identifiable intangible assets of Swedish Match consist of:

| Type | Useful Life | Estimated Fair Value (in millions) | |||||||||

| Trademarks | Non-amortizable | $ | 2,077 | ||||||||

| Trademarks | Amortizable | 20 years | 904 | ||||||||

| Developed technology, including patents | 10 years | 367 | |||||||||

| Customer relationships | 10 years | 1,164 | |||||||||

| Total identifiable intangible assets | $ | 4,512 | |||||||||

The significant assumptions used in determining the preliminary fair values of the identifiable intangible assets included royalty rates, revenue growth rates, profit margins, customer attrition rate and discount rates.

12

Philip Morris International Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Trademarks primarily relate to $2,077 million for the ZYN trademark, which has been determined to have an indefinite life due to the fast growth and the leading position of the brand in the market. All other trademarks have been preliminarily determined to have a 20 years useful life. The preliminary fair values of the trademarks have been determined using the relief from royalty method supported by revenue growth rates assumptions and royalty rates benchmarking analysis at product category level (smoke-free brands, including ZYN, cigar brands and lights). In 2023, during the measurement period, the useful life, revenue growth rate and the royalty rate of each individual trademark will be reassessed to determine its final purchase price.

Developed technology, including patents, relates to the nicotine pouch technology of $367 million. The patent has been assigned a useful life of 10 years, which is in line with the patent's protection. The preliminary fair value of the patent has been determined using the relief from royalty method.

Customer relationships have been valued separately by geographic locations, namely for the U.S. market, Scandinavia, and other markets using the multiple periods excess earnings method, preliminarily reflecting a general market attrition rate for retail and revenue allocation and profit margin assumptions by customer type, which will be further assessed during the measurement period.

PMI consolidated statements of earnings for the year ended December 31, 2022, include $316 million of net revenues and $(26) million of net losses associated with the results of operations of Swedish Match from the acquisition date to December 31, 2022. The operating results of Swedish Match are included in a separate segment.

Acquisition related transaction costs, which were comprised primarily of regulatory, financial advisory and legal fees, totaled $59 million for the year ended December 31, 2022, and were included in marketing, administration and research costs in the consolidated statements of earnings. Bridge and term loan credit agreement related fees associated with the issuance of debt amounted to $54 million, of which $37 million were capitalized at the acquisition date. The fair value of the noncontrolling interest was based on the tender offer as of the acquisition date.

PMI’s approval of the acquisition by the European Commission, under the EU Merger Regulation, was subject to PMHH’s divestiture of Swedish Match’s subsidiary, SMD Logistics AB, following the completion of the offer to tender all shares in Swedish Match to PMHH. As a result, these assets have been accounted for as assets held for sale and included within other current assets and other accrued liabilities in PMI’s condensed consolidated balance sheets at March 31, 2023 and December 31, 2022.

The unaudited pro forma combined financial information was prepared using the acquisition method of accounting and was based on the historical financial information of PMI and Swedish Match. In order to reflect the occurrence of the acquisition on January 1, 2021, as required, the unaudited pro forma financial information includes adjustments to reflect the following:

•incremental amortization expense to be incurred based on the current preliminary fair values of the identifiable intangible assets acquired;

•incremental cost of products sold related to the fair value adjustments associated with acquisition date inventory;

•additional interest expense associated with the issuance of debt to finance the acquisition, including the effects of the related derivative financial instruments designated to hedge interest rate risks as well as economic hedges;

•reclassification of non-recurring acquisition-related costs incurred during the year ended December 31, 2022, to the year ended December 31, 2021;

•impact of a deferred tax cost of $430 million in 2022 and $321 million in 2021 related to the theoretical unrealized foreign currency gains on intercompany loans related to the acquisition financing. These theoretical unrealized pre-tax foreign currency movements were fully offset in the consolidated statements of earnings and were reflected as currency translation adjustments in PMI's consolidated statements of stockholders' (deficit) equity, while the corresponding deferred tax impacts were reflected in PMI's consolidated statements of earnings; and

•other immaterial items (i.e., the alignment of accounting policies from IFRS to US GAAP.)

13

Philip Morris International Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

The unaudited pro forma financial information is not necessarily indicative of what the consolidated results of operations would have been had the acquisition been completed on January 1, 2021. In addition, the unaudited pro forma financial information is not a projection of future results of operations of the combined company, nor does it reflect the expected realization of any synergies or cost savings associated with the acquisition.

The unaudited pro forma financial information is as follows:

| For the Years Ended December 31, | ||||||||

| (in millions) | 2022 | 2021 | ||||||

| Net revenues | $ | 33,690 | $ | 33,577 | ||||

| Net earnings attributable to PMI | $ | 8,875 | $ | 8,610 | ||||

Altria Group, Inc. Agreement

On October 20, 2022, PMI announced that it had reached an agreement with Altria Group, Inc. to end the companies' relationship regarding the IQOS commercialization rights in the U.S. as of April 30, 2024. As a result of PMI reacquiring these rights, effective May 1, 2024, PMI will have the full rights to commercialize IQOS in the U.S. As part of the agreement, PMI agreed to pay a total cash consideration of $2.7 billion, with $1.0 billion paid at the inception of the agreement and the remaining $1.7 billion (plus interest, at a per annum rate equal to six percent (6%)), to be paid by July 2023 at the latest. The cash consideration paid at the inception of the agreement of $1.0 billion has been accounted for within other assets in PMI’s condensed consolidated balance sheets as of March 31, 2023 and December 31, 2022. As of May 2024, when PMI can exercise its ability to commercialize IQOS in the U.S., PMI will finalize the accounting for this transaction by assigning the consideration to the respective assets.

14

Philip Morris International Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Note 3. War in Ukraine:

Since the onset of the war in Ukraine in February 2022, PMI's main priority has been the safety and security of its more than 1,300 employees and their families in the country.

Ukraine

PMI temporarily suspended its commercial and manufacturing operations in Ukraine, including the closing of its factory in Kharkiv at the end of February 2022, in order to preserve the safety of its employees. PMI subsequently resumed some retail activities where safety allowed, in order to provide product availability and service to adult consumers, and began to supply the market from production centers outside Ukraine, as well as through a contract manufacturing arrangement. Production at the factory in Kharkiv remains suspended. While the effects of the war are unpredictable and could trigger impairment reviews for long-lived assets, as of March 31, 2023, PMI is unable to estimate the information required to perform impairment analyses (i.e., forecast of revenues, manufacturing and commercial plans). PMI is not aware of any major damage to its production facilities, inventories or other assets in Ukraine. As a result, PMI has not recorded an impairment of long-lived assets. As of March 31, 2023, PMI’s Ukrainian operations had approximately $485 million in total assets, excluding intercompany balances. These total assets included $69 million, $324 million and $30 million in receivables, inventories and property, plant and equipment, respectively.

Russia

PMI has suspended its planned investments in the Russian Federation including all new product launches and commercial, innovation, and manufacturing investments. PMI has also taken steps to scale down its manufacturing operations in Russia amid ongoing supply chain disruptions and the evolving regulatory environment. PMI is continuously assessing the evolving situation in Russia, including: recent regulatory constraints in the market that entail very complex terms and conditions that must be met for any divestment transaction to be granted approval by the authorities; and restrictions resulting from international regulations. As a result of PMI continuing operations within Russia as of March 31, 2023, it has not recorded an impairment of long-lived and other assets. However, PMI recorded specific asset write downs as referred to in the table below. PMI’s Russian operations as of March 31, 2023 had approximately $2.4 billion in total assets, excluding intercompany balances. These total assets included $393 million, $560 million, $932 million, $307 million and $164 million in cash (primarily held in local currency), receivables, inventories, property, plant and equipment and goodwill, respectively. In addition, there was approximately $928 million of cumulative foreign currency translation losses reflected in accumulated other comprehensive losses in the condensed consolidated statement of stockholders’ equity as of March 31, 2023.

During the three months ended March 31, 2023, PMI did not record any material charges related to the war in Ukraine. During the three months ended March 31, 2022, PMI recorded in its condensed consolidated statements of earnings pre-tax charges related to circumstances driven by the war as follows:

| (in millions) | For the Three Months Ended March 31, 2022 | ||||||||||

| Cost of sales | Marketing, administration and research costs | Total | |||||||||

Ukraine 1 | $ | 11 | $ | 16 | $ | 27 | |||||

Russia 2 | 15 | — | 15 | ||||||||

| Total | $ | 26 | $ | 16 | $ | 42 | |||||

1 The pre-tax charges were primarily due to an inventory write down, additional allowance for receivables and the cost of PMI’s humanitarian efforts, which includes salary continuation for its employees.

2 The pre-tax charges were primarily due to inventory write downs related to the commercial decisions noted above.

PMI will continue to monitor the situation as it evolves and will determine if further charges are needed.

15

Philip Morris International Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Note 4. Stock Plans:

In May 2022, PMI’s shareholders approved the Philip Morris International Inc. 2022 Performance Incentive Plan (the “2022 Plan”). Under the 2022 Plan, PMI may grant to eligible employees restricted shares and restricted share units, performance-based cash incentive awards and performance-based equity awards. Up to 25 million shares of PMI’s common stock may be issued under the 2022 Plan. At March 31, 2023, shares available for grant under the 2022 Plan were 22,158,790.

In May 2017, PMI’s shareholders approved the Philip Morris International Inc. 2017 Stock Compensation Plan for Non-Employee Directors (the “2017 Non-Employee Directors Plan”). A non-employee director is defined as a member of the PMI Board of Directors who is not a full-time employee of PMI or of any corporation in which PMI owns, directly or indirectly, stock possessing at least 50% of the total combined voting power of all classes of stock entitled to vote in the election of directors in such corporation. Up to 1 million shares of PMI common stock may be awarded under the 2017 Non-Employee Directors Plan. At March 31, 2023, shares available for grant under the plan were 894,346.

Restricted share unit (RSU) awards

During the three months ended March 31, 2023 and 2022, shares granted to eligible employees, the weighted-average grant date fair value per share and the recorded compensation expense related to RSU awards were as follows:

| Number of Shares Granted | Weighted-Average Grant Date Fair Value Per RSU Award Granted | Compensation Expense Related to RSU Awards (in millions) | |||||||||||||||

| 2023 | 1,732,910 | $ 102.01 | $ | 50 | |||||||||||||

| 2022 | 1,551,050 | $ 105.04 | $ | 39 | |||||||||||||

As of March 31, 2023, PMI had $277 million of total unrecognized compensation cost related to non-vested RSU awards. The cost is recognized over the original restriction period of the awards, which is typically three years after the date of the award, or upon death, disability or reaching the age of 58.

During the three months ended March 31, 2023, 1,274,379 RSU awards vested. The grant date fair value of all the vested awards was approximately $110 million. The total fair value of RSU awards that vested during the three months ended March 31, 2023 was approximately $128 million.

Performance share unit (PSU) awards

During the three months ended March 31, 2023 and 2022, PMI granted PSU awards to certain executives. The PSU awards require the achievement of certain performance metrics, which are predetermined at the time of grant, typically over a three-year performance cycle. The performance metrics for such PSU's granted during the three months ended March 31, 2023 and 2022 consisted of PMI's Total Shareholder Return ("TSR") relative to a predetermined peer group and on an absolute basis (40% weight), PMI’s currency-neutral compound annual adjusted diluted earnings per share growth rate (30% weight), and a Sustainability Index, which consists of two drivers:

•Product Sustainability (20% weight) measuring progress on PMI's efforts to maximize the benefits of smoke-free products, purposefully phase out cigarettes, seek net positive impact in wellness and healthcare, and reduce post-consumer waste; and

•Operational Sustainability (10% weight) measuring progress on PMI's efforts to tackle climate change, preserve nature, improve the quality of life of people in its supply chain, and foster an empowered, and inclusive workplace.

The aggregate of the weighted performance factors for the three metrics in each such PSU award determines the percentage of PSUs that will vest at the end of the three-year performance cycle. The minimum percentage of such PSUs that can vest is zero, with a target percentage of 100 and a maximum percentage of 200. Each such vested PSU entitles the participant to one share

16

Philip Morris International Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

of common stock. An aggregate weighted PSU performance factor of 100 will result in the targeted number of PSUs being vested. At the end of the performance cycle, participants are entitled to an amount equivalent to the accumulated dividends paid on common stock during the performance cycle for the number of shares earned.

During the three months ended March 31, 2023 and 2022, shares granted to eligible employees, the grant date fair value per share and the recorded compensation expense related to PSU awards were as follows:

| Number of Shares Granted | Weighted- Average PSU Grant Date Fair Value Subject to Other Performance Factors | Weighted- Average PSU Grant Date Fair Value Subject to TSR Performance Factors | Compensation Expense Related to PSU Awards (in millions) | |||||||||||

| (Per Share) | (Per Share) | |||||||||||||

| 2023 | 482,360 | $ 102.02 | $ 133.54 | $ | 27 | |||||||||

| 2022 | 451,790 | $ 105.07 | $ 143.94 | $ | 21 | |||||||||

The grant date fair value of the PSU awards subject to the other performance factors was determined by using the market price of PMI’s stock on the date of the grant. The grant date fair value of the PSU market-based awards subject to the TSR performance factor was determined by using the Monte Carlo simulation model. The following assumptions were used to determine the grant date fair value of the PSU awards subject to the TSR performance factor:

| 2023 | 2022 | ||||||||||

Average risk-free interest rate (a) | 4.1 | % | 1.6 | % | |||||||

Average expected volatility (b) | 24.3 | % | 28.6 | % | |||||||

(a) Based on the U.S. Treasury yield curve.

(b) Determined using the observed historical volatility.

As of March 31, 2023, PMI had $62 million of total unrecognized compensation cost related to non-vested PSU awards. The cost is recognized over the performance cycle of the awards, or upon death, disability or reaching the age of 58.

During the three months ended March 31, 2023, 902,232 PSU awards vested. The grant date fair value of all the vested awards was approximately $83 million. The total fair value of PSU awards that vested during the three months ended March 31, 2023 was approximately $91 million.

Note 5. Benefit Plans:

Pension coverage for employees of PMI’s subsidiaries is provided, to the extent deemed appropriate, through separate plans, many of which are governed by local statutory requirements. In addition, PMI provides health care and other benefits to certain U.S. retired employees and certain non-U.S. retired employees. In general, health care benefits for non-U.S. retired employees are covered through local government plans.

Pension and other employee benefit costs per the condensed consolidated statements of earnings consisted of the following:

| For the Three Months Ended March 31, | |||||||||||

| (in millions) | 2023 | 2022 | |||||||||

| Net pension costs (income) | $ | (12) | $ | (25) | |||||||

| Net postemployment costs | 30 | 27 | |||||||||

| Net postretirement costs | 4 | 2 | |||||||||

| Total pension and other employee benefit costs | $ | 22 | $ | 4 | |||||||

17

Philip Morris International Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Pension Plans

Components of Net Periodic Benefit Cost

Net periodic pension cost consisted of the following:

Pension (1) | |||||||||||

| For the Three Months Ended March 31, | |||||||||||

| (in millions) | 2023 | 2022 | |||||||||

| Service cost | $ | 43 | $ | 60 | |||||||

| Interest cost | 66 | 20 | |||||||||

| Expected return on plan assets | (90) | (92) | |||||||||

| Amortization: | |||||||||||

| Net loss | 12 | 48 | |||||||||

| Prior service cost (credit) | — | (1) | |||||||||

| Net periodic pension cost | $ | 31 | $ | 35 | |||||||

(1) Primarily non-U.S. based defined benefit retirement plans.

Employer Contributions

PMI makes, and plans to make, contributions, to the extent that they are tax deductible and meet specific funding requirements of its funded pension plans. Employer contributions of $45 million were made to the pension plans during the three months ended March 31, 2023. Currently, PMI anticipates making additional contributions during the remainder of 2023 of approximately $83 million to its pension plans, based on current tax and benefit laws. However, this estimate is subject to change as a result of changes in tax and other benefit laws, as well as asset performance significantly above or below the assumed long-term rate of return on pension assets, or changes in interest and currency rates.

Note 6. Goodwill and Other Intangible Assets, net:

The movements in goodwill were as follows:

| (in millions) | Europe | SSEA, CIS & MEA | EA, AU & PMI DF | Americas | Swedish Match | Wellness & Healthcare | Total | ||||||||||||||||

| Balances at December 31, 2022 | $ | 1,370 | $ | 2,869 | $ | 493 | $ | 615 | $ | 13,296 | $ | 1,012 | $ | 19,655 | |||||||||

| Changes due to: | |||||||||||||||||||||||

| Currency | 35 | 75 | 11 | 32 | 33 | 25 | 211 | ||||||||||||||||

| Balances, March 31, 2023 | $ | 1,405 | $ | 2,944 | $ | 504 | $ | 647 | $ | 13,329 | $ | 1,037 | $ | 19,866 | |||||||||

As discussed in Note 1. Background and Basis of Presentation, in January 2023, PMI began managing its business in four geographical segments, Swedish Match segment and Wellness and Healthcare segment. As a result, the December 31, 2022 goodwill balance in the table above included the reclassifications from the former six geographical segments to the four geographical segments under the new structure.

At March 31, 2023, goodwill primarily reflects PMI’s business combinations in Greece, Indonesia, Mexico, the Philippines and Serbia, as well as the goodwill from the 2021 acquisitions of Fertin Pharma A/S and Vectura Group plc. and the preliminary purchase price allocation of Swedish Match AB, which was acquired in the fourth quarter of 2022.

18

Philip Morris International Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Details of other intangible assets were as follows:

| March 31, 2023 | December 31, 2022 | |||||||||||||||||||||||||

| (in millions) | Weighted-Average Remaining Useful Life | Gross Carrying Amount | Accumulated Amortization | Net | Gross Carrying Amount | Accumulated Amortization | Net | |||||||||||||||||||

| Non-amortizable intangible assets | $ | 3,405 | $ | 3,405 | $ | 3,346 | $ | 3,346 | ||||||||||||||||||

| Amortizable intangible assets: | ||||||||||||||||||||||||||

| Trademarks | 15 years | 2,055 | $ | 696 | 1,359 | 2,050 | $ | 674 | 1,376 | |||||||||||||||||

| Developed technology, including patents | 8 years | 984 | 269 | 715 | 975 | 243 | 732 | |||||||||||||||||||

| Customer relationships and other | 10 years | 1,399 | 146 | 1,253 | 1,390 | 112 | 1,278 | |||||||||||||||||||

| Total other intangible assets | $ | 7,843 | $ | 1,111 | $ | 6,732 | $ | 7,761 | $ | 1,029 | $ | 6,732 | ||||||||||||||

Non-amortizable intangible assets substantially consist of trademarks from PMI’s acquisitions in Indonesia and Mexico, as well as the preliminary purchase price allocation associated with the Swedish Match acquisition in 2022, and PMI's business combinations in 2021 (primarily in-process research and development). The increase since December 31, 2022 was due to currency movements of $59 million.

The increase in the gross carrying amount of amortizable intangible assets from December 31, 2022, was due to currency movements of $23 million.

The change in the accumulated amortization from December 31, 2022, was mainly due to the 2023 amortization of $81 million, combined with currency movements of $1 million. The amortization of intangibles for the three months ended March 31, 2023 was recorded in cost of sales ($22 million) and in marketing, administration and research costs ($59 million) on PMI's condensed consolidated statements of earnings.

Amortization expense for each of the next five years is estimated to be $322 million or less, assuming no additional transactions occur that require the amortization of intangible assets. This estimate is subject to change based on the finalization of the preliminary purchase price allocation of the Swedish Match acquisition.

19

Philip Morris International Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Note 7. Financial Instruments:

Overview

PMI operates in markets primarily outside of the United States of America, with manufacturing and sales facilities in various locations around the world. PMI utilizes certain financial instruments to manage foreign currency and interest rate exposures. Derivative financial instruments are used by PMI principally to reduce exposures to market risks resulting from fluctuations in foreign currency exchange and interest rates by creating offsetting exposures. PMI is not a party to leveraged derivatives and, by policy, does not use derivative financial instruments for speculative purposes. Substantially all of PMI's derivative financial instruments are subject to master netting arrangements, whereby the right to offset occurs in the event of default by a participating party. While these contracts contain the enforceable right to offset through close-out netting rights, PMI elects to present them on a gross basis in the consolidated balance sheets. Collateral associated with these arrangements is in the form of cash and is unrestricted. Financial instruments qualifying for hedge accounting must maintain a specified level of effectiveness between the hedging instrument and the item being hedged, both at inception and throughout the hedged period. PMI formally documents the nature and relationships between the hedging instruments and hedged items, as well as its risk-management objectives, strategies for undertaking the various hedge transactions and method of assessing hedge effectiveness. Additionally, for hedges of forecasted transactions, the significant characteristics and expected terms of the forecasted transaction must be specifically identified, and it must be probable that each forecasted transaction will occur. If it were deemed probable that the forecasted transaction would not occur, the gain or loss would be recognized in earnings.

PMI uses deliverable and non-deliverable forward foreign exchange contracts, foreign currency swaps and foreign currency options, collectively referred to as foreign exchange contracts ("foreign exchange contracts"), and interest rate contracts to mitigate its exposure to changes in exchange and interest rates related to net investments in foreign operations, third-party and intercompany actual and forecasted transactions. Both foreign exchange contracts and interest rate contracts are collectively referred to as derivative contracts ("derivative contracts"). The primary currencies to which PMI is exposed include the Euro, Egyptian pound, Indonesian rupiah, Japanese yen, Mexican peso, Philippine peso, Russian ruble and Swiss franc.

The gross notional amounts for outstanding derivatives at the end of each period were as follows:

| (in millions) | At March 31, 2023 | At December 31, 2022 | ||||||

| Derivative contracts designated as hedging instruments: | ||||||||

| Foreign exchange contracts | $ | 21,831 | $ | 17,627 | ||||

| Interest rate contracts | 1,500 | 1,019 | ||||||

| Derivative contracts not designated as hedging instruments: | ||||||||

| Foreign exchange contracts | 20,270 | 21,755 | ||||||

| Total | $ | 43,601 | $ | 40,401 | ||||

20

Philip Morris International Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

The fair value of PMI’s derivative contracts included in the condensed consolidated balance sheets as of March 31, 2023 and December 31, 2022, were as follows:

| Derivative Assets | Derivative Liabilities | ||||||||||||||||||||||||||||||||||

| Fair Value | Fair Value | ||||||||||||||||||||||||||||||||||

| At | At | At | At | ||||||||||||||||||||||||||||||||

| (in millions) | Balance Sheet Classification | March 31, 2023 | December 31, 2022 | Balance Sheet Classification | March 31, 2023 | December 31, 2022 | |||||||||||||||||||||||||||||

| Derivative contracts designated as hedging instruments: | |||||||||||||||||||||||||||||||||||

| Foreign exchange contracts | Other current assets | $ | 338 | $ | 376 | Other accrued liabilities | $ | 263 | $ | 126 | |||||||||||||||||||||||||

| Other assets | 318 | 341 | Income taxes and other liabilities | 209 | 147 | ||||||||||||||||||||||||||||||

| Interest rate contracts | Other current assets | 5 | — | Other accrued liabilities | 34 | 27 | |||||||||||||||||||||||||||||

| Other assets | — | — | Income taxes and other liabilities | 46 | 56 | ||||||||||||||||||||||||||||||

| Derivative contracts not designated as hedging instruments: | |||||||||||||||||||||||||||||||||||

| Foreign exchange contracts | Other current assets | 104 | 156 | Other accrued liabilities | 150 | 165 | |||||||||||||||||||||||||||||

| Other assets | — | — | Income taxes and other liabilities | 74 | 16 | ||||||||||||||||||||||||||||||

| Total gross amount derivatives contracts presented in the condensed consolidated balance sheets | $ | 765 | $ | 873 | $ | 776 | $ | 537 | |||||||||||||||||||||||||||

| Gross amounts not offset in the condensed consolidated balance sheets | |||||||||||||||||||||||||||||||||||

| Financial instruments | (412) | (346) | (412) | (346) | |||||||||||||||||||||||||||||||

| Cash collateral received/pledged | (167) | (341) | (89) | (48) | |||||||||||||||||||||||||||||||

| Net amount | $ | 186 | $ | 186 | $ | 275 | $ | 143 | |||||||||||||||||||||||||||

PMI assesses the fair value of its foreign exchange contracts and interest rate contracts using standard valuation models that use, as their basis, readily observable market inputs. The fair value of PMI’s foreign exchange forward contracts, foreign currency swaps and interest rate contracts is determined by using the prevailing foreign exchange spot rates and interest rate differentials, and the respective maturity dates of the instruments. The fair value of PMI’s currency options is determined by using a Black-Scholes methodology based on foreign exchange spot rates and interest rate differentials, currency volatilities and maturity dates. PMI’s derivative contracts have been classified within Level 2 at March 31, 2023 and December 31, 2022.

21

Philip Morris International Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

For the three months ended March 31, 2023 and 2022, PMI's derivative contracts impacted the condensed consolidated statements of earnings and comprehensive earnings as follows:

| (pre-tax, in millions) | For the Three Months Ended March 31, | ||||||||||||||||||||||||||||||||||||||||

| Amount of Gain/(Loss) Recognized in Other Comprehensive Earnings/(Losses) on Derivatives | Statement of Earnings Classification of Gain/(Loss) on Derivatives | Amount of Gain/(Loss) Reclassified from Other Comprehensive Earnings/(Losses) into Earnings | Amount of Gain/(Loss) Recognized in Earnings | ||||||||||||||||||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||||||||||||||||||

| Derivative contracts designated as hedging instruments: | |||||||||||||||||||||||||||||||||||||||||

| Cash flow hedges: | |||||||||||||||||||||||||||||||||||||||||

| Foreign exchange contracts | $ | 10 | $ | 79 | Net revenues | $ | 12 | $ | 17 | ||||||||||||||||||||||||||||||||

| Cost of sales | — | — | |||||||||||||||||||||||||||||||||||||||

| Marketing, administration and research costs | 16 | (3) | |||||||||||||||||||||||||||||||||||||||

| Interest expense, net | (3) | (1) | |||||||||||||||||||||||||||||||||||||||

| Interest rate contracts | 65 | 51 | Interest expense, net | 10 | (2) | ||||||||||||||||||||||||||||||||||||

| Fair value hedges: | |||||||||||||||||||||||||||||||||||||||||

| Interest rate contracts | Interest expense, net (a) | $ | 3 | $ | (37) | ||||||||||||||||||||||||||||||||||||

Net investment hedges (b): | |||||||||||||||||||||||||||||||||||||||||

| Foreign exchange contracts | (258) | 105 | 63 | 33 | |||||||||||||||||||||||||||||||||||||

| Derivative contracts not designated as hedging instruments: | |||||||||||||||||||||||||||||||||||||||||

| Foreign exchange contracts | Interest expense, net | 90 | 8 | ||||||||||||||||||||||||||||||||||||||

Marketing, administration and research costs (d) | (16) | (1) | |||||||||||||||||||||||||||||||||||||||

| Total | $ | (183) | $ | 235 | $ | 35 | $ | 11 | $ | 140 | $ | 3 | |||||||||||||||||||||||||||||

(a) The gains (losses) from these contracts are offset by the changes in the fair value of the hedged item

(b) Amount of gains (losses) on hedges of net investments principally related to changes in exchange and interest rates between the Euro and U.S. dollar

(c) Represent the gains for amounts excluded from the effectiveness testing

(d) The gains (losses) from these contracts attributable to changes in foreign currency exchange rates are partially offset by the (losses) and gains generated by the underlying intercompany and third-party loans being hedged

Cash Flow Hedges

PMI has entered into derivative contracts to hedge the foreign currency exchange and interest rate risks related to certain forecasted transactions. Gains and losses associated with qualifying cash flow hedge contracts are deferred as components of accumulated other comprehensive losses until the underlying hedged transactions are reported in PMI’s condensed consolidated statements of earnings. As of March 31, 2023, PMI has hedged forecasted transactions with derivative contracts expiring at various dates through May 2028. The impact of these hedges is primarily included in operating cash flows on PMI’s condensed consolidated statements of cash flows.

22

Philip Morris International Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Fair Value Hedges

PMI has entered into fixed-to-floating interest rate contracts, designated as fair value hedges to minimize exposure to changes in the fair value of fixed rate U.S. dollar-denominated debt that results from fluctuations in benchmark interest rates. For derivative contracts that are designated and qualify as fair value hedges, the gain or loss on the derivative, as well as the offsetting gain or loss on the hedged items attributable to the hedged risk, is recognized in current earnings. The carrying amount of the debt hedged, which includes the cumulative adjustment for fair value gains/losses, as of March 31, 2023 was $916 million, and is recorded in long-term debt in the condensed consolidated balance sheets. The cumulative amount of fair value gains/(losses) included in the carrying amount of the debt hedged was $80 million as of March 31, 2023.

Hedges of Net Investments in Foreign Operations

PMI designates derivative contracts and certain foreign currency denominated debt and other financial instruments as net investment hedges, primarily of its Euro net assets. For the three months ended March 31, 2023 and 2022, the amount of pre-tax gain/(loss) related to the non-derivative financial instruments, that was reported as a component of accumulated other comprehensive losses within currency translation adjustments, was $1 million and $66 million, respectively. The premiums paid for, and settlements of, net investment hedges are included in investing cash flows on PMI’s condensed consolidated statements of cash flows.

Other Derivatives

PMI has entered into derivative contracts to hedge the foreign currency exchange and interest rate risks related to intercompany loans between certain subsidiaries, third-party loans and acquisition related transactions. While effective as economic hedges, no hedge accounting is applied for these contracts; therefore, the gains (losses) relating to these contracts are reported in PMI’s condensed consolidated statements of earnings. Acquisition related transactions are included in investing cash flows on PMI’s condensed consolidated statements of cash flows.

Qualifying Hedging Activities Reported in Accumulated Other Comprehensive Losses

Derivative gains or losses reported in accumulated other comprehensive losses are a result of qualifying hedging activity. Transfers of these gains or losses to earnings are offset by the corresponding gains or losses on the underlying hedged item. Hedging activity affected accumulated other comprehensive losses, net of income taxes, as follows:

| (in millions) | For the Three Months Ended March 31, | |||||||

| 2023 | 2022 | |||||||

| Gain/(loss) as of January 1, | $ | 266 | $ | 4 | ||||

| Derivative (gains)/losses transferred to earnings | (29) | (9) | ||||||

| Change in fair value | 59 | 110 | ||||||

| Gain/(loss) as of March 31, | $ | 296 | $ | 105 | ||||

At March 31, 2023, PMI expects $77 million of derivative gains that are included in accumulated other comprehensive losses to be reclassified to the condensed consolidated statement of earnings within the next 12 months. These gains are expected to be substantially offset by the statement of earnings impact of the respective hedged transactions.

Contingent Features

PMI’s derivative instruments do not contain contingent features.

Credit Exposure and Credit Risk

PMI is exposed to credit loss in the event of non-performance by counterparties. While PMI does not anticipate non-performance, its risk is limited to the fair value of the financial instruments less any cash collateral received or pledged. PMI actively monitors its exposure to credit risk through the use of credit approvals and credit limits and by selecting and continuously monitoring a diverse group of major international banks and financial institutions as counterparties.

23

Philip Morris International Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Other Investments

A certain PMI investment, which is comprised primarily of money market funds, has been classified within Level 1 and had a fair value of $173 million at March 31, 2023. For the three months ended March 31, 2023, the unrealized pre-tax gains on these investments were immaterial.

Note 8. Earnings Per Share:

Basic and diluted earnings per share (“EPS”) were calculated using the following:

| (in millions) | For the Three Months Ended March 31, | |||||||

| 2023 | 2022 | |||||||

| Net earnings attributable to PMI | $ | 1,995 | $ | 2,331 | ||||

Less distributed and undistributed earnings attributable to share-based payment awards | 6 | 7 | ||||||

| Net earnings for basic and diluted EPS | $ | 1,989 | $ | 2,324 | ||||

| Weighted-average shares for basic EPS | 1,552 | 1,550 | ||||||

| Plus contingently issuable performance stock units (PSUs) | 1 | 2 | ||||||

| Weighted-average shares for diluted EPS | 1,553 | 1,552 | ||||||

Unvested share-based payment awards that contain non-forfeitable rights to dividends or dividend equivalents are participating securities and therefore are included in PMI’s earnings per share calculation pursuant to the two-class method.

For the 2023 and 2022 computations, there were no antidilutive stock awards.

Note 9. Segment Reporting:

PMI’s subsidiaries and affiliates are primarily engaged in the manufacture and sale of cigarettes and smoke-free products, including heat-not-burn, e-vapor and oral nicotine products. Excluding the Wellness and Healthcare segment and the 2022 acquisition of Swedish Match, PMI's segments are generally organized by geographic region and managed by segment managers who are responsible for the operating and financial results of the regions inclusive of combustible tobacco and smoke-free product categories sold in the region. Effective in January 2023, PMI began managing its business in four geographical segments, down from six previously, in addition to its continuing Swedish Match and Wellness and Healthcare segments. The four geographical segments are as follows: Europe Region; South and Southeast Asia, Commonwealth of Independent States, Middle East and Africa Region ("SSEA, CIS & MEA"); East Asia, Australia, and PMI Duty Free Region ("EA, AU & PMI DF"); and Americas Region. PMI records net revenues and operating income to its geographical segments based upon the geographic area in which the customer resides.

PMI’s chief operating decision maker evaluates geographical segment performance and allocates resources based on regional operating income, which includes results from all product categories sold in each region, excluding Swedish Match and Wellness and Healthcare products. Business operations in the Swedish Match segment and the Wellness and Healthcare segment are evaluated separately.

PMI disaggregates its net revenues from contracts with customers by product category for each of PMI's four geographical segments and for the Swedish Match segment. For the Wellness and Healthcare business, Vectura Fertin Pharma, net revenues from contracts with customers are included in the Wellness and Healthcare segment. PMI believes this best depicts how the nature, amount, timing and uncertainty of its revenue and cash flows are affected by economic factors.

24

Philip Morris International Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Segment data were as follows:

| (in millions) | For the Three Months Ended March 31, | |||||||

| 2023 | 2022 | |||||||

| Net revenues: | ||||||||

| Europe | $ | 2,910 | $ | 3,224 | ||||

SSEA, CIS & MEA | 2,477 | 2,445 | ||||||

EA, AU & PMI DF | 1,520 | 1,587 | ||||||

| Americas | 445 | 424 | ||||||

| Swedish Match | 581 | — | ||||||

| Wellness and Healthcare | 86 | 66 | ||||||

| Net revenues | $ | 8,019 | $ | 7,746 | ||||

| Operating income (loss): | ||||||||

| Europe | $ | 1,175 | $ | 1,558 | ||||

SSEA, CIS & MEA | 712 | 965 | ||||||

EA, AU & PMI DF | 623 | 685 | ||||||

| Americas | 66 | 121 | ||||||

| Swedish Match | 193 | — | ||||||

| Wellness and Healthcare | (38) | (31) | ||||||

| Operating income | $ | 2,731 | $ | 3,298 | ||||

25

Philip Morris International Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

PMI's net revenues by product category were as follows:

| (in millions) | For the Three Months Ended March 31, | |||||||

| 2023 | 2022 | |||||||

| Net revenues: | ||||||||

| Combustible tobacco products: | ||||||||

| Europe | $ | 1,815 | $ | 1,937 | ||||

SSEA, CIS & MEA | 2,154 | 2,195 | ||||||

EA, AU & PMI DF | 689 | 769 | ||||||

| Americas | 430 | 402 | ||||||

| Swedish Match | 136 | — | ||||||

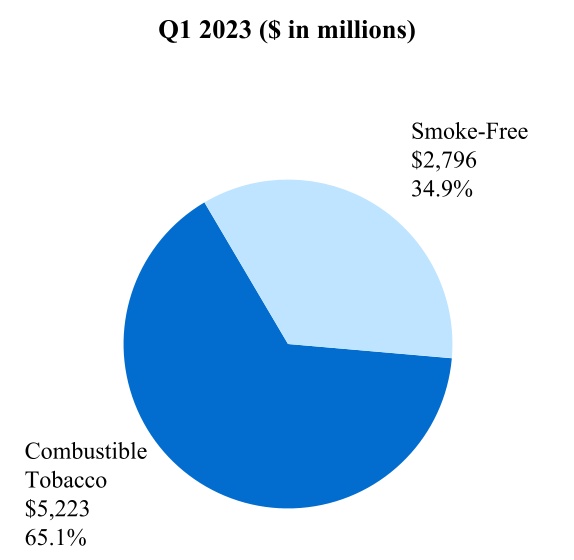

| Total combustible tobacco products | 5,223 | 5,303 | ||||||

| Smoke-free products: | ||||||||

| Smoke-free products excluding Wellness and Healthcare: | ||||||||

| Europe | 1,095 | 1,287 | ||||||

SSEA, CIS & MEA | 323 | 250 | ||||||

EA, AU & PMI DF | 831 | 818 | ||||||

| Americas | 15 | 22 | ||||||

| Swedish Match | 445 | — | ||||||

| Total smoke-free products excluding Wellness and Healthcare | 2,710 | 2,377 | ||||||

| Wellness and Healthcare | 86 | 66 | ||||||

| Total smoke-free products | 2,796 | 2,443 | ||||||

| Total PMI net revenues | $ | 8,019 | $ | 7,746 | ||||

Note: Sum of product categories or Regions might not foot to total PMI due to roundings.

Items affecting the comparability of results from operations were as follows:

•Termination of distribution arrangement in the Middle East - In the first quarter of 2023, PMI recorded a pre-tax charge of $80 million following the termination of a distribution arrangement in the Middle East. This pre-tax charge was recorded as a reduction of net revenues in the condensed consolidated statements of earnings, and was included in the SSEA, CIS & MEA segment results for the three months ended March 31, 2023.

•Charges related to the war in Ukraine - In the first quarter of 2022, PMI recorded a pre-tax charge of $42 million related to the war in Ukraine. This pre-tax charge was included in the Europe segment for the three months ended March 31, 2022. For further details, see Note 3. War in Ukraine.

•Swedish Match AB acquisition accounting related item - See Note 2. Acquisitions for details of the $18 million pre-tax purchase accounting adjustments related to the sale of acquired inventories stepped up to fair value included in the Swedish Match segment for the three months ended March 31, 2023.

•Asset impairment and exit costs - See Note 17. Asset Impairment and Exit Costs for details of the $109 million pre-tax charges for the three months ended March 31, 2023, as well as a breakdown of these costs by segment.

Following the Swedish Match acquisition and a review of PMI and Swedish Match’s combined product portfolio, PMI reclassified certain of its own products previously reported under its combustible tobacco product category to the newly created smoke-free product category to better reflect the characteristics of these products. This reclassification did not impact PMI’s consolidated financial position, results of operations or cash flows in any of the periods presented.

26

Philip Morris International Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Net revenues related to combustible tobacco products refer to the operating revenues generated from the sale of these products, including shipping and handling charges billed to customers, net of sales and promotion incentives, and excise taxes. These net revenue amounts consist of the sale of PMI's cigarettes and other tobacco products that are combusted. Other tobacco products primarily include roll-your-own and make-your-own cigarettes, pipe tobacco, cigars and cigarillos, and do not include smoke-free products.

Net revenues related to smoke-free products refer to the operating revenues generated from the sale of these products, including shipping and handling charges billed to customers, net of sales and promotion incentives, and excise taxes, if applicable. These net revenue amounts consist of the sale of all of PMI's products that are not combustible tobacco products, such as heat-not-burn, e-vapor, and oral nicotine, also including wellness and healthcare products, as well as consumer accessories such as lighters and matches.