Stem Holdings, Inc. - Annual Report: 2021 (Form 10-K)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended September 30, 2021

Or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ___________ to ___________

Commission file number: 000-55751

STEM HOLDINGS, INC.

(Exact name of registrant as specified in charter)

| Nevada | 61-1794883 | |

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification No.) |

2201 NW Corporate Blvd., Suite 205

Boca Raton, FL 33431

(Address of principal executive offices) (Zip Code)

Registrant’s telephone Number: (561) 948-5410

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of exchange on which registered | ||

| Common Stock par value $0.001 | STMH | OTCQX |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☒ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ☒ Yes ☐ No

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☐ Yes ☒ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer”, “non-accelerated filer”, and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large Accelerated Filer ☐ | Accelerated Filer ☐ |

| Non-accelerated Filer ☒ | Smaller Reporting Company ☒ |

| Emerging Growth Company ☒ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒ No

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter. $112,532,221 at $0.649 per share.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date: shares of common stock par value $0.001 as of January 6, 2022.

DOCUMENTS INCORPORATED BY REFERENCE: NONE

TABLE OF CONTENTS

PART I

This Form 10-K contains some forward-looking statements. Forward-looking statements give our current expectations or forecasts of future events. You can identify these statements by the fact that they do not relate strictly to historical or current facts. Forward-looking statements involve risks and uncertainties. Forward-looking statements include statements regarding, among other things, (a) our projected sales, profitability, and cash flows, (b) our growth strategies, (c) anticipated trends in our industries, (d) our future financing plans and (e) our anticipated needs for working capital. They are generally identifiable by use of the words “may,” “will,” “should,” “anticipate,” “estimate,” “plans,” “potential,” “projects,” “continuing,” “ongoing,” “expects,” “management believes,” “we believe,” “we intend” or the negative of these words or other variations on these words or comparable terminology. These statements may be found under “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Business,” as well as in this Form 10-K generally. In particular, these include statements relating to future actions, prospective products or product approvals, future performance or results of current and anticipated products, sales efforts, expenses, the outcome of contingencies such as legal proceedings, and financial results.

Any or all of our forward-looking statements in this report may turn out to be inaccurate. They can be affected by inaccurate assumptions we might make or by known or unknown risks or uncertainties. Consequently, no forward-looking statement can be guaranteed. Actual future results may vary materially as a result of various factors, including, without limitation, the risks outlined under “Risk Factors” and matters described in this Form 10-K generally. In light of these risks and uncertainties, there can be no assurance that the forward-looking statements contained in this filing will in fact occur. You should not place undue reliance on these forward-looking statements.

The forward-looking statements speak only as of the date on which they are made, and, except to the extent required by federal securities laws, we undertake no obligation to publicly update any forward-looking statements, whether as the result of new information, future events, or otherwise.

ITEM 1. DESCRIPTION OF BUSINESS.

Corporate Structure

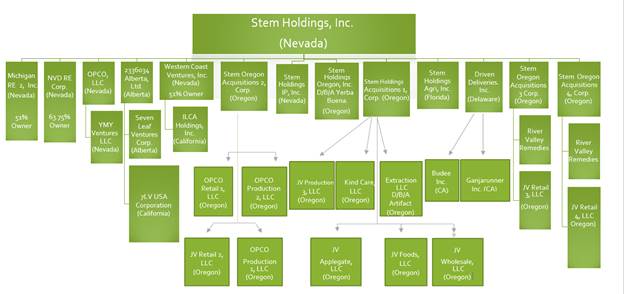

Stem Holdings, Inc. was organized on June 7, 2016, as a Nevada corporation under Chapter 78 of the Nevada Revised Statutes. The Company’s principal office is located at 2201 NW Corporate Blvd, Suite 205, Boca Raton, FL 33431.

The following chart illustrates the Companies corporate structure including details of the jurisdiction of formation of each subsidiary. Stem, through its subsidiaries, is currently in the process of finalizing the investment in and acquisition of entities that engage directly in the production and sale of cannabis.

| 2 |

Overview of the Business

Stem is a multi-state, vertically integrated, cannabis company that, through its subsidiaries and its investments, is engaged in the manufacture, possession, use, sale, distribution or branding of cannabis and/or holds licenses in the adult use and/or medical cannabis marketplace in the states of Oregon, Nevada, California, and Massachusetts. Stem has ownership interests in 29 state issued cannabis licenses including nine (9) licenses for cannabis cultivation, three (3) licenses for cannabis processing, two (2) licenses for cannabis wholesale distribution, three (3) licenses for hemp production, five (5) adult-use medical retailers (non-storefront) which were subsequently divested and seven (7) cannabis dispensary licenses.

The Company is also currently working towards acquiring one additional entity and assisting certain joint ventures with obtaining licenses and permits for cannabis production, distribution and sale in additional US states. Should it be successful in these endeavors, the Company will transform into a multi-state, vertically integrated, cannabis company that purchases, improves, leases, operates and invests in properties for use in the production, distribution and sales of cannabis and cannabis-infused products licensed under the laws of the states of Oregon, Nevada, California, and Colorado.

Stem’s partner consumer brands are award-winning, nationally known and include: cultivators, TJ’s Gardens, Travis X James, and Yerba Buena; retail brands, Stem and TJ’s; infused product manufacturers, Cannavore and Supernatural Honey; and a CBD company, Dose-ology. As of September 30, 2021, the Company owns five properties and leases eight other properties, located in Oregon, Nevada and California. As of September 30, 2021, the buildout of these properties to support cannabis related operations was either complete or near completion.

The Company has ten wholly-owned subsidiaries, including Driven Deliveries, Inc. (subsequently divested on December 17, 2021), Stem Holdings Oregon, Inc., Stem Holdings IP, Inc., Opco, LLC, Stem Agri, Inc., Stem Holdings Oregon Acquisitions 1, Corp., Stem Holdings Oregon Acquisitions 2, Corp., Stem Holdings Oregon Acquisitions 3, Corp., Stem Holdings Oregon Acquisitions 4 Corp., 2336034 Alberta Ltd., Stem, through its subsidiaries, is currently in the process of finalizing the investment in and acquisition of entities that engage directly in the production and sale of cannabis.

The Company’s stock is publicly traded and is listed on the Canadian Securities Exchange under the symbol “STEM” and the OTCQX exchange under the symbol “STMH”.

Recent Developments

COVID-19

On March 12, 2020, the World Health Organization (“WHO”) declared a global pandemic as a result of the spread of a virus known as COVID-19. The impacts on global commerce are expected to be far reaching. This has largely limited the Company’s workforce from travelling to its various state specific jurisdictions. This will likely impact demand for the Company’s products in the near term and will also likely impact the Company’s supply chains. It may also impact expected credit losses on trade receivables and may cause staffing shortages and increased government regulations or interventions, which may negatively impact the financial condition or results of the Company. The Company has taken effective steps to ensure frequent sanitization, social distancing, and abstention from duty for employees with illnesses.

As of the date of this report, the Company has experienced minimal disruptions in staffing and one of the Company’s facilities have been forced to close for a shortened period of time. The Company experienced significant retail revenue growth during 2021 despite this crisis. Overall demand in Oregon has been consistent through the date of this report and the Company expects that, without further restrictions from the government, its Oregon business will continue to remain open and service its customers. To date the Company has proven to be compliant with the Governors Guidelines and the updated OSHA requirements in response to COVID-19.

Oregon is utilizing a 4-tiered risk level rubric, based on hospitalizations and percent increase in 7-day positive test rates. The levels are Lower Risk, Moderate Risk, High Risk, and Extreme Risk. As of the date of this report, 1 of the companies 5 dispensaries are located in counties with a “High Risk” rating. This will not affect the Company’s retail stores and the Company does not anticipate a significant impact in demand due to these ratings; however, the existence of more widespread cases of COVID-19 generally increases the risk of infection at a Company facility which could require downtime resulting in lost revenue, supply chain disruptions, testing and sanitization costs, and other potential unforeseen liabilities.

| 3 |

The Company has to date demonstrated resilience in managing its business through the pandemic by taking all recommended safety precautions including personal protective equipment, sanitization, working from home when possible and periodic testing. The Company also demonstrated strength by increasing headcount in its retail stores at the beginning of the pandemic rather than trimming headcount and shutting down stores. This decision significantly contributed to the Company’s growth and success in its Oregon business during the first half of 2021.

Industrial Hemp

Industrial hemp is now legal in the U.S., which advocates hope could eventually loosen laws around the popular marijuana extract CBD.

The 2018 farm bill which legalized hemp including a variety of cannabis that does not produce the psychoactive component of marijuana, paved the way to legitimacy for an agricultural sector that has been operating on the fringe of the law. Industrial hemp has made investors and executives swoon because of the potential multibillion-dollar market for cannabidiol, or CBD, a non-psychoactive compound that has started to turn up in beverages, health products and pet snacks, among other products.

Currently, it appears that CBD will remain largely off-limits for ingestible products. The Food and Drug Administration issued a statement saying that despite the new status of hemp, CBD is still considered a drug ingredient and remains illegal to add to food or health products without the agency’s approval, disappointing many hemp advocates, who said they will continue to work to convince the FDA to loosen its CBD rules. The FDA said some hemp ingredients, such as hulled hemp seeds, hemp seed protein and hemp seed oil, are safe in food and won’t require additional approvals.

The farm bill places industrial hemp, which is defined as a cannabis plant with under 0.3% of tetrahydrocannabinol, or THC, under the supervision of the Agriculture Department and removes CBD from the purview of the Controlled Substances Act, which covers marijuana. The law also “explicitly” preserved the Food and Drug Administration’s authority to regulate products containing cannabis, or cannabis-derived compounds.

Regulation of Cannabis in the United States Federally

The cultivation, production, distribution and sale of cannabis and cannabis extracts is illegal under U.S. federal law, and it is listed as a Schedule I substance under the U.S. Controlled Substances Act. A Schedule I drug or substance is deemed to have a high potential for abuse, to have no accepted medical use in the United States, and to lack an acceptable safe use of the drug under medical supervision. The Company believes the U.S. Controlled Substances Act categorization as a Schedule I drug is not reflective of cannabis’ medicinal properties and numerous related studies support rescheduling. Over the past decade, cannabis policy has been moving towards legalization and liberalization of cannabis laws.

In September 2018, Congress approved the Medical Cannabis Research Act. This bill requires the Department of Justice to issue additional cultivation licenses to grow marijuana for federal research. The bill also clarifies that Department of Veterans Affairs (“VA”) doctors can discuss medical marijuana with their patients and can refer them to participate in scientific studies on the drug’s effects.

| 4 |

The District of Columbia (“D.C.”) and 36 U.S. states, including the states of Oregon, Nevada and California, have legalized cannabis for medical use. D.C. and 15 U.S. states, including the states of Oregon, Nevada and California, have also legalized adult recreational use of cannabis.

As discussed above, marijuana remains a Schedule I substance under U.S. federal law. However, the Treasury Department’s Financial Crimes Enforcement Network (“FinCEN”) has issued guidance advising prosecutors of money laundering and other financial crimes not to focus their enforcement efforts on banks that serve marijuana-related businesses (“MRBs”), so long as that business is legal in the bank’s respective state and none of the federal enforcement priorities are being violated (such as keeping marijuana away from children and out of the hands of organized crime). This guidance was published on February 14, 2014 and requires banks providing such services to monitor strict compliance with FinCEN’s guidance. This requires investment in monitoring and compliance staff, and large national banks don’t appear to want to make such an investment, nor expose themselves to potential risk of prosecution from non-compliant businesses they might serve. At the end of 2020 FinCEN reported 684 banks and financial institutions doing business with MRB’s.

The few credit unions who have agreed to service marijuana businesses are limiting those accounts to no more than 5% of their total deposits to avoid creating a liquidity risk. Because the federal government could change the banking laws as it relates to marijuana businesses at any time and without notice, these credit unions must keep sufficient cash on hand to be able to return the full value of all deposits from marijuana businesses in a single day, while also servicing the needs of their other customers.

In March 2019, a congressional committee approved the Secure and Fair Enforcement (SAFE) Banking Act. Draft legislation of the SAFE Banking Act received a historic hearing in the House Consumer Protection and Financial Institutions Subcommittee in February 2019, where the National Cannabis Industry Association submitted written testimony along with the personal stories about the burdens and safety concerns created by the current banking situation from nearly 100 cannabis industry professionals. On September 25, 2019 the U.S House of Representatives passed the landmark legislation to reform federal cannabis laws and reduce the public safety risk in communities across the country. H.R. 1595, the SAFE Banking Act of 2019 passed by a vote of 321 to 103. This bill generally prohibits a federal banking regulator from penalizing a depository institution for providing banking services to a legitimate marijuana-related business. The Company believes this progressive banking reform for the U.S. cannabis industry reflects a positive trajectory for marijuana banking reform.

The Marijuana Opportunity Reinvestment and Expungement Act, also known as the MORE Act, is a proposed 2019 United States federal legislation to legalize cannabis and expunge prior cannabis related convictions that was introduced into the U.S. House of Representatives on July 23, 2019. This would remove cannabis from the Controlled Substances Act and impose a 5% tax on cannabis and cannabis products manufactured in or imported into the United States. This tax will be collected by the Treasury of the United States to create a trust fund to be known as the Opportunity Trust Fund. The trust funds the Act would create include the Community Reinvestment Grant, which would provide funding for services such as job training, re-entry services and legal aid; the Cannabis Opportunity Grant, which would provide funds to assist small businesses in the cannabis industry; and the Equitable Licensing Grant, which minimizes barriers to gain access to marijuana licensing and employment for those most impacted by the so-called war on drugs. The act would also establish a Cannabis Justice Office within the Department of Justice Office of Justice Programs, responsible for administering the grants. On December 4, 2020, the U.S. House of Representatives passed this legislation by a vote of 228-164.

Both the MORE and SAFE Banking Acts have yet to receive action in the U.S. Senate. However, in late 2020 incoming Senate Majority Leader Charles Schumer made multiple comments suggesting that passage of these bills and large-scale federal legalization of cannabis are on his agenda. The Company continues to monitor both of these bills and the general status of cannabis legalization at the U.S. federal level.

On December 14, 2020, former President Trump announced that William Barr would be resigning from his post as Attorney General, effective December 23, 2020. Merrick Garland, President Biden’s nominee to succeed Mr. Barr, has served as the current attorney since March 2021. It is unclear what specific impact the new Biden administration will have on U.S. federal government enforcement policy. There is no guarantee that state laws legalizing and regulating the sale and use of cannabis will not be repealed or overturned, or that local governmental authorities will not limit the applicability of state laws within their respective jurisdictions. Unless and until the United States Congress amends the CSA with respect to cannabis (and as to the timing or scope of any such potential amendments there can be no assurance), there is a risk that federal authorities may enforce current U.S. federal law.

| 5 |

The Company believes it is too soon to determine if any prosecutorial policy at the federal level will be forthcoming or if the Biden administration will reinstitute the prior posture of the Department of Justice or a similar guidance document for United States attorneys or by executive order. The sheer size of the cannabis industry, in addition to various level of legalization at the State and local governments, suggests that a largescale enforcement operation would possibly create unwanted political backlash for the Department of Justice. Moreover, State and local tax revenues generated by the cannabis business has become an increasingly important source of funding for State and local government programs.

Regulation of the Cannabis Market at State and Local Levels

The following chart sets out, for each of the subsidiaries and other entities through which the Company conducts is operations, the U.S. state(s) in which it operates, the nature of its operations (adult-use/medicinal), whether such activities carried on are direct, indirect or ancillary in nature (as such terms are defined in Staff Notice 51-352), the number of sales, cultivation and other licenses held by such entity and whether such entity has any operational cultivation or processing facilities.

| State | Entities | Adult-Use / Medical |

Direct / Indirect / Ancillary |

Dispensary Licenses |

Cultivation / Processing / Distribution Licenses |

|||||||

| California | 7LV USA | Medical | Direct (1) | 1 | N/A | |||||||

| Massachusetts | CGP | Adult-Use | Indirect(2) | 1 | ||||||||

| Nevada | YMY | Both | Indirect(3) | N/A | 4 | |||||||

| Oregon | Various | Both | Direct and Ancillary(4) | 5 | 5 |

Notes:

| (1) | The Company’s wholly-owned subsidiary, 7LV USA, operates a cannabis dispensary in Sacramento, California. |

| (2) | The Company holds a 13% interest in CGP, which operates a cannabis dispensary in Great Barrington, Massachusetts. CGP is also building a cannabis facility in Northampton, Massachusetts. |

| (3) | The Company holds a 50% interest in YMY, which operates a cannabis facility in North Las Vegas, Nevada. |

| (4) | The Company holds all licenses in Oregon directly, through wholly-owned subsidiaries. |

California

History

In 1996, California voters passed a medical cannabis law allowing physicians to recommend cannabis for an inclusive set of qualifying conditions including chronic pain and providing immunity/defense to criminal proceedings. The law was amended in 2003 to expand the criminal defense to groups of patients/caregivers, but there was no state licensing authority to oversee the businesses that emerged as a result of the system. In September 2015, the California legislature passed three bills, collectively known as the “Medical Marijuana Regulation and Safety Act” (“MMRSA” later referred to as MCRSA after an amendment changed the word “Marijuana” to “Cannabis”). In 2016, California voters passed the “Adult Use of Marijuana Act” (“AUMA”), which legalized adult-use cannabis for adults 21 years of age and older and created a licensing system for commercial cannabis business. On June 27, 2017, Governor Brown signed SB-94 into law. SB-94 combines California’s medicinal and adult-use regulatory framework into one licensing structure under the Medicinal and Adult-Use of Cannabis Regulation and Safety Act (“MAUCRSA”).

| 6 |

Regulatory Summary

Pursuant to MAUCRSA: (i) the California Department of Food and Agriculture, via CalCannabis, issues licenses to cannabis cultivators, (ii) the California Department of Public Health, via the Manufactured Cannabis Safety Branch (the “MCSB”) issues licenses to cannabis manufacturers and (iii) the California Department of Consumer Affairs, via the Bureau of Cannabis Control (the “BCC”), issues licenses to cannabis distributors, testing laboratories, retailers, and micro-businesses. These agencies also oversee the various aspects of implementing and maintaining California’s cannabis landscape, including the statewide track and trace system. All three agencies released their emergency rulemakings at the end of 2017 and have begun issuing licenses.

In July, 2017, the State of California established the MCSB to develop statewide standards, regulations, and licensing procedures in relation to cannabis, and is addressing policy issues in support of cannabis manufacturers. MCSB is responsible for issuing licenses to manufacturers of cannabis products.

To operate legally under state law, cannabis operators must obtain the requisite state licensure and local approval. Local authorization is a prerequisite to obtaining state licensure, and local governments are permitted to prohibit or otherwise regulate the types and number of cannabis businesses allowed in their locality. The state license approval process is not competitive and there is no limit on the number of state licenses an entity may hold. Although vertical integration across multiple license types is allowed under the MAUCRSA, testing laboratory licensees may not hold any other licenses aside from a laboratory license. However, a licensee is not prohibited from performing testing on the licensee’s premises for the purposes of quality assurance of a cannabis product in conjunction with reasonable business operations (testing conducted on a licensee’s premises by the licensee does not meet the testing requirements required under the MAUCRSA). There are also no residency requirements for ownership under MAUCRSA.

California License Types

Once an operator obtains local approval, the operator must obtain state licenses before conducting any commercial cannabis activity. There are 12 different license types that cover all commercial activity. License types 1-3 and 5 authorize the cultivation of medical and/or adult use cannabis plants. Type 4 licenses are for nurseries that cultivate and sell clones and “teens” (immature cannabis plants that have established roots but require further vegetation prior to being sent into the flowering period). Type 6 and 7 licenses authorize manufacturers to process cannabis biomass into certain value-added products such as shatter or cannabis distillate oil with the use of volatile or non-volatile solvents, depending on the license type. Type 8 licenses are held by testing facilities who test samples of cannabis products and generate “certificates of analysis,” which include important information regarding the potency of products and whether products have passed or failed certain threshold tests for pesticide and microbiological contamination. Type 9 licenses are issued to “non-storefront” retailers, commonly called delivery services, who bring cannabis products directly to customers and patients at their residences or other chosen deliver location. Type 10 licenses are known as “Transport-Only” distribution licenses, and they allow the distributor to transport cannabis and cannabis products between licensees, but not to retailers. Type 12 licenses are issued to distributors who move cannabis and cannabis products to all license types, including retailers.

Company Licenses

On March 29, 2019, the Company executed a definitive agreement to acquire Western Coast Ventures, Inc. (“WCV”), an arm’s length private corporation incorporated under the laws of Nevada. Other than approximately $2,000,000 in cash, WCV’s sole asset was a 51% ownership interest in ILCA. ILCA was issued a limited conditional use permit for a cannabis production facility by the City of San Diego. Upon issuance of the final cannabis production facility permit and the completed construction of the facility, the ILCA will: (i) operate an advanced cannabis facility to grow and cultivate cannabis; (ii) manufacture cannabis-derived products; and (iii) distribute cannabis and cannabis-derived products state-wide throughout California. During the year ended September 30, 2021 the Company determined the investment in ILCA was impaired and recognized an impairment expense of $2.2 million for the year ended September 30, 2021.

| 7 |

On March 6, 2020, the Company closed the acquisition of Seven Leaf Ventures Corp. (“7LV”), an arm’s length private corporation incorporated under the laws of Alberta, and its subsidiaries, pursuant to the terms of a share purchase agreement dated March 6, 2020. A subsidiary of 7LV, 7LV USA, owns Foothills Health and Wellness, a medical dispensary, in the greater Sacramento, California area.

The table below lists the licenses directly and indirectly held by the Company in the State of California:

| Holding Entity | Permit/License | City, State | Expiration Date | Description | ||||

| 7LV USA | C10-0000679-LIC | Sacramento, California | January 14, 2023 | Medicinal Retailer License |

California Agencies Regulating the Commercial Cannabis Industry

From 2015 through July 2021, three agencies were tasked with regulating the cannabis industry in California. The California Department of Food and Agriculture (“CDFA”) which oversaw nurseries and cultivators; the California Department of Public Health (“CDPH”) which oversaw manufacturers, and the Bureau of Cannabis Control (BCC) which oversaw distributors, retailers, delivery services and testing laboratories.

In an effort to centralize and simplify regulatory and licensing oversight of the cannabis market, Gov. Gavin Newsom signed AB-141 into law on July 12, 2021, creating the Department of Cannabis Control (DCC). Assembly Bill 141 consolidates three state cannabis programs – the Bureau of Cannabis Control (BCC), the California Department of Food and Agriculture’s (CDFA) CalCannabis Cultivation Licensing Division, and the California Department of Public Health’s (CDPH) Manufactured Cannabis Safety Branch into the DCC. The law transfers to the DCC all of the “powers, duties, purposes, functions, responsibilities, and jurisdiction” of the BCC, CDFA and CDPH.

California Transportation

Transporting cannabis goods between licensees and a licensed facility may only be performed by persons holding a distributor license. The vehicle or trailer used must not contain any markings or features on the exterior which may indicate or identify the contents or purpose. All cannabis products must be locked in a box, container, or cage that is secured to the inside of the vehicle or trailer. When left unattended, vehicles must be locked and secured. At a minimum, the vehicle must be equipped with an alarm system, motion detectors, pressure switches, duress, panic, and hold-up alarms.

California Inventory/Storage

Each licensee is required to assign an account manager to oversee the track and trace system. The account manager is fully trained on the system and is accountable to record all commercial cannabis activities accurately and completely. The licensee is expected to correct any data that is entered into the track and trace system in error within three business days of discovery of the error. The licensee is required to report information in the track and trace system for each transfer of cannabis or non-manufactured cannabis products to, or cannabis or non-manufactured cannabis products received from, other licensed operators. Licensees must use the track and trace system for all inventory tracking activities at a licensed premise, including, but not limited to, reconciling all on-premise and in-transit cannabis or non-manufactured cannabis product inventories at least once every 14 business days. The licensee must store cannabis and cannabis products in a secure place with locked doors.

| 8 |

California Record-keeping/Reporting

The cultivation, processing, and movement of cannabis within the state is tracked by the METRC system, into which all licensees are required to input their track and trace data (either manually or using another software that automatically uploads to METRC). Immature plants are assigned a Unique Identifier number (UID), and this number follows the flowers and biomass resulting from that plant through the supply chain, all the way to the consumer. Each licensee in the supply chain is required to meticulously log any processing, packaging, and sales associated with that UID.

Retail Compliance in California

California requires that certain warnings, images and content information be printed on all cannabis packaging. BCC regulations also include certain requirements about tamper-evident and child-resistant packaging. Distributors and retailers are responsible for confirming that products are properly labeled and packaged before they are sold to a customer.

Consumers aged 21 and up may purchase cannabis in California from a dispensary with an “adult-use” license. Some localities still only allow medicinal dispensaries. Consumers aged 18 and up with a valid physician’s recommendation may purchase cannabis from a medicinal-only dispensary or an adult-use dispensary. Consumers without valid physician’s recommendations may not purchase cannabis from a medicinal-only dispensary. All cannabis businesses are prohibited from hiring employees under the age of 21.

California Security

Each local government in California has its own security requirements for cannabis businesses, which usually include comprehensive video surveillance, intrusion detection and alarms and limited-access areas where only employees and other authorized individuals may enter. All licensee employees must wear employee badges. The limited-access areas must be locked with “commercial-grade, non-residential door locks on all points of entry and exit to the licensed premises.”

Each licensed premises must have a digital video surveillance system that can “effectively and clearly” record images of the area under surveillance. Cameras must be “in a location that allows the camera to clearly record activity occurring within 20 feet of all points of entry and exit on the licensed premises.” The regulations list specific areas which must be under surveillance, including places where cannabis goods are weighed, packed, stored loaded and unloaded, security rooms and entrances and exits to the premises. Retailers must record point of sale areas on the video surveillance system.

Licensed retailers must hire security personnel to provide on-site security services for the licensed retails premises during hours of operation. All security personnel must be licensed by the Bureau of Security and Investigate Services.

California Inspections

All licensees are subject to annual and random inspections of their premises. Cultivators may be inspected by the California Department of Fish and Wildlife, the California Regional Water Quality Control Boards, and the California Department of Food and Agriculture. Manufacturers are subject to inspection by the California Department of Public Health, and Retailers, Distributors, Testing Laboratories, and Delivery services are subject to inspection by the Department of Cannabis Control. Inspections can result in notices to correct, or notices of violation, fines, or other disciplinary action by the inspecting agency.

Cannabis taxes in California

Several taxes are imposed at the point of sale and are required to be collected by the retailer. The State imposes an excise tax of 15%, and a sales and use tax is assessed on top of that. Cities and Counties apply their sales tax along with the State’s sales and use tax, and many cities and counties have also authorized the imposition of special cannabis business taxes which can range from 2% to 10% of gross receipts of the business.

| 9 |

U.S. Attorney Statements in California

To the knowledge of management of Stem, other than as disclosed in this Document, there have not been any statements or guidance made by federal authorities or prosecutors regarding the risk of enforcement action in California. See “Risk Factors”.

Massachusetts

History

The Massachusetts Medical Use of Marijuana Program (the “MA Program”) was formed pursuant to the Act for the Humanitarian Medical Use of Marijuana (the “MA ACT”). The MA Program allows registered persons to purchase medical cannabis and applies to any patient, personal caregiver, Registered Marijuana Dispensary (each, a “RMD”), and RMD agent that qualifies and registers under the MA Program. To qualify, patients must suffer from a debilitating condition as defined by the MA Program. Currently there are eight conditions that allow a patient to acquire cannabis in Massachusetts, including AIDS/HIV, ALS, cancer and Crohn’s disease. The MA Program is administrated by the Department of Public Health, Bureau of Health Care Safety and Quality. In November 2016, Massachusetts voted affirmatively on a ballot petition to legalize and regulate cannabis for adult-use. The Massachusetts legislature amended the law on December 28, 2016, delaying the date adult-use cannabis sales would begin by six months. The delay allowed the legislature to clarify how municipal land-use regulations would treat the cultivation of cannabis and authorized a study of related issues. After further debate, the state House of Representatives and state Senate approved H.3818 which became Chapter 55 of the Acts of 2017, An Act to Ensure Safe Access to Marijuana, and established the Cannabis Control Commission (the “MA CCC”). The MA CCC consists of five commissioners and regulates the Massachusetts Recreational Marijuana Program. Adult-use of cannabis in Massachusetts started in July 2018.

Regulatory Summary (Medical)

Under the MA Program, RMDs are heavily regulated. Vertically integrated RMDs grow, process, and dispense their own cannabis. As such, each RMD is required to have a retail facility as well as cultivation and processing operations, although retail operations may be separate from grow and cultivation operations. A RMD’s cultivation location may be in a different municipality or county than its retail facility. RMD’s are required to be Massachusetts non-profit corporations.

The MA Program mandates a comprehensive application process for RMDs. Each RMD applicant must submit a Certificate of Good Standing, comprehensive financial statements, a character competency assessment, and employment and education histories of the senior partners and individuals responsible for the day-to-day security and operation of the RMD. Municipalities may individually determine what local permits or licenses are required if an RMD wishes to establish an operation within its boundaries.

Each Massachusetts dispensary, grower and processor license is valid for one year and must be renewed no later than 60 calendar days prior to expiration. As in other states where cannabis is legal, the MA CCC can deny or revoke licenses and renewals for multiple reasons, including (a) submission of materially inaccurate, incomplete, or fraudulent information, (b) failure to comply with any applicable law or regulation, including laws relating to taxes, child support, workers compensation and insurance coverage, (c) failure to submit or implement a plan of correction (d) attempting to assign registration to another entity, (e) insufficient financial resources, (f) committing, permitting, aiding, or abetting of any illegal practices in the operation of the RMD, (g) failure to cooperate or give information to relevant law enforcement related to any matter arising out of conduct at an RMD, and (h) lack of responsible RMD operations, as evidenced by negligence, disorderly or unsanitary facilities or permitting a person to use a registration card belonging to another person. Additionally, license holders must ensure that no cannabis is sold, delivered, or distributed by a producer from or to a location outside of this state.

Regulatory Summary (Adult-Use)

Many of the same application requirements exist for a marijuana establishment license as a RMD application, and each owner, officer or member must undergo background checks and fingerprinting with the CCC. Applicants must submit the location and identification of each site, and must establish a property interest in the same, and the applicant and the local municipality must have entered into a host agreement authorizing the location of the adult-use marijuana establishment within the municipality and said agreement must be included in the application. Applicants must include disclosure of any regulatory actions against it by the Commonwealth of Massachusetts, as well as the civil and criminal history of the applicant and its owners, officers, principals or members. The application must include the RMD applicant’s plans for separating medical and adult-use operations, proposed timeline for achieving operations, liability insurance, business plan, and a detailed summary describing and/or updating or modifying the RMD’s existing medical marijuana operating policies and procedures for adult-use including security, prevention of diversion, storage, transportation, inventory procedures, quality control, dispensing procedures, personnel policies, record keeping, maintenance of financial records and employee training protocols.

| 10 |

No person or entity may own more than 10% or “control” more than three licenses in each marijuana establishment class (i.e., marijuana retailer, marijuana cultivator, marijuana product manufacturer). Additionally, there is a 100,000 square foot cultivation canopy for adult-use licenses; however, there is no canopy restriction for RMD license holders relative to their cultivation facility.

Company Licenses

The Company holds a minority interest in an entity that holds one cultivation and one dispensary license in the State of Massachusetts. The table below lists the licenses indirectly held by the Company:

| Holding Entity | Permit/License | City, State | Expiration Date | Description | ||||

| CGP(1) | MR282695 | Massachusetts | January 13, 2022 | Dispensary and Cultivation License |

Note:

| (1) | The Company holds a 13% interest in CGP, which operates a cannabis dispensary in Great Barrington, Massachusetts. CGP is also building a cannabis facility in Northampton, Massachusetts. |

Massachusetts Transportation

A licensee transporting cannabis must ensure the product is in a secure, locked storage compartment. If a cannabis establishment, pursuant to a cannabis transporter license is transporting cannabis products for more than one cannabis establishment at a time, the cannabis products for each cannabis establishment must be kept in separate locked storage compartments during transportation and separate manifests are required for each cannabis establishment. Vehicles transporting cannabis must be equipped with an approved alarm system and functioning heating and air conditioning systems appropriate for maintaining correct temperatures for storage of cannabis products.

Massachusetts Inventory

Through the track and trace system, licensees are required to record all actions related to each individual cannabis plant. This robust inventorying requirement includes tracking how each plant is handled and processed from seed and cultivation, through growth, harvest and preparation of cannabis infused products, if any, to final sale of finished products. To meet this tracking requirement, the inventory tracking process is mandated to utilize unique plant and batch identification numbers. Besides capturing all processes associated with each cannabis plant, licensees must also establish and abide by inventory controls and procedures for conducting inventory reviews and comprehensive inventories of cultivating, finished, and stored cannabis products.

Massachusetts Security

Adequate security systems that prevent and detect diversion, theft, or loss of cannabis are required of each licensee.

To ensure licensees meet the rigorous security standards, use of surveillance cameras is mandated. Video cameras must be appropriate for the lighting conditions of the area under surveillance. Interior video cameras must be directed at all safes, vaults, sales areas, and areas where cannabis is cultivated, harvested, processed, prepared, stored, handled, or dispensed.

Massachusetts Record-keeping/Reporting

Massachusetts uses METRC as the track and trace system. Individual licensees, whether directly or through a third-party application programming interface, are required to push data to the state to meet all reporting requirements.

| 11 |

Massachusetts Inspections

The CCC or its agents may inspect a licensee and affiliated vehicles at any time without prior notice. A licensee shall immediately upon request make available to the CCC information that may be relevant to a CCC inspection, and the CCC may direct a licensee to test cannabis for contaminants.

U.S. Attorney Statements in Massachusetts

On July 10, 2018, the U.S. Attorney for the District of Massachusetts, Andrew Lelling, issued a statement regarding the legalization of adult-use cannabis in Massachusetts. Mr. Lelling stated that since he has a constitutional obligation to enforce the laws passed by Congress, he would not immunize the residents of Massachusetts from federal law enforcement. He did state, however, that his office’s resources would be primarily focused on combating the opioid epidemic. He stated that considering those factors and the experiences of other states that have legalized adult-use cannabis, his office’s enforcement efforts would focus on the areas of (i) overproduction, (ii) targeted sales to minors and (iii) organized crime and interstate transportation of drug proceeds.

To the knowledge of management of the Company, other than as disclosed in this Document, there have not been any statements or guidance made by federal authorities or prosecutors regarding the risk of enforcement action in Massachusetts.

Nevada

History

Nevada’s medical cannabis market was introduced in June 2013 when the legislature passed SB374, legalizing the medicinal use of cannabis for certified patients. The first dispensaries opened to patients in August 2015.

The Nevada Division of Public and Behavioral Health licensed medical cannabis establishments up until July 1, 2017, when the State’s medical cannabis program merged with adult-use cannabis enforcement under the State of Nevada Department of Taxation, Marijuana Enforcement Division (the “Nevada Taxation Department”). In 2014, Nevada accepted medical cannabis business applications and a few months later the division approved 182 cultivation licenses, 118 licenses for the production of edibles and infused products, 17 independent testing laboratories, and 55 medical cannabis dispensary licenses. The number of dispensary licenses was then increased to 66 by legislative action in 2015. The application process is merit-based, competitive, and is currently closed. Residency is not required to own or invest in a Nevada medical cannabis business. In addition, vertical integration is neither required nor prohibited. Nevada’s medical law includes patient reciprocity, which permits medical patients from other States to purchase cannabis from Nevada dispensaries. Nevada also allows for dispensaries to deliver medical cannabis to patients.

Each medical cannabis establishment must register with the Nevada Taxation Department and apply for a medical cannabis establishment registration certificate. As noted above, the application process is competitive, and, among other requirements, there are minimum liquidity requirements and restrictions on the geographic location of a medical cannabis establishment as well as restrictions relating to the age and criminal background of employees, owners, officers and board members of the establishment. All employees must be over 21 and all owners, officers and board members must not have any previous felony convictions or had a previously granted medical cannabis registration revoked. Additionally, each volunteer, employee, officer, board member, and owner of an effective 5% or greater interest of a medical cannabis establishment must be individually registered with the Nevada Taxation Department as a medical cannabis agent and hold a valid medical cannabis establishment agent card. The establishment must have adequate security measures and use an electronic verification system and inventory control system. If the proposed medical cannabis establishment will sell or deliver edible cannabis products or cannabis-infused products, the proposed establishment must establish operating procedures for handling such products, which must be preapproved by the Nevada Taxation Department.

| 12 |

In response to the rescission of the Cole Memo, Nevada Attorney General Adam Laxalt had issued a public statement, pledging to defend the law after it was approved by voters. Then-Governor Brian Sandoval also stated, “Since Nevada voters approved the legalization of recreational cannabis in 2016, I have called for a well-regulated, restricted and respected industry. My administration has worked to ensure these priorities are met while implementing the will of the voters and remaining within the guidelines of both the Cole and Wilkinson federal memos,” and that he would like for Nevada to follow in the footsteps of Colorado, where the U.S. attorneys do not plan to change the approach to prosecuting crimes involving recreational cannabis.

In determining whether to issue a medical cannabis establishment registration certificate pursuant to NRS 453A.322, the Nevada Taxation Department, in addition the application requirements set out, considers the following criteria of merit:

| ● | the total financial resources of the applicant, both liquid and illiquid; | |

| ● | the previous experience of the persons who are proposed to be owners, officers of board members of the proposed medical cannabis establishment at operating other businesses or non-profit organizations; | |

| ● | the educational achievements of the persons who are proposed to be owners, officers of board members of the proposed medical cannabis establishment; | |

| ● | any demonstrated knowledge or expertise on the part of the persons who are proposed to be owners, officers or board members of the proposed medical cannabis establishment with respect to the compassionate use of cannabis to treat medical conditions; | |

| ● | whether the proposed location of the proposed medical cannabis establishment would be convenient to serve the needs of persons who are authorized to engage in the medical use of cannabis; | |

| ● | whether the applicant has an integrated plan for the care, quality and safekeeping of medical cannabis from seed to sale; | |

| ● | the amount of taxes paid to, or other beneficial financial contributions made to, the State of Nevada or its political subdivisions by the applicant or the persons who are proposed to be the owners, officers or board members of the proposed medical cannabis establishment; and | |

| ● | any other criteria of merit that the Nevada Taxation Department determines to be relevant. |

A medical cannabis establishment registration certificate expires 1 year after the date of issuance and may be renewed upon resubmission of the application information and renewal fee to the Nevada Taxation Department.

The sale of cannabis for adult-use in Nevada was approved by ballot initiative on November 8, 2016, and Nevada Revised Statute 453D exempts a person who is 21 years of age or older from state or local prosecution for possession, use, consumption, purchase, transportation or cultivation of certain amounts of cannabis and requires the Nevada Taxation Department to begin receiving applications for the licensing of cannabis establishments on or before January 1, 2018. The legalization of retail cannabis does not change the medical cannabis program.

In February 2017, the Nevada Taxation Department announced plans to issue “early start” recreational cannabis establishment licenses in the summer of 2017. These licenses, which began on July 1, 2017, allowed cannabis establishments holding both a retail cannabis store and dispensary license to sell their existing medical cannabis inventory as either medical or adult-use cannabis, and expired at the end of the year. As of July 1, 2017, medical and adult-use cannabis have incurred a 15% excise tax on the first wholesale sale (calculated on the fair market value) and adult-use cannabis has incurred an additional 10% special retail cannabis sales tax in addition to any general State and local sales and use taxes.

On January 16, 2018, the Nevada Taxation Department issued final rules governing its adult-use cannabis program, pursuant to which up to sixty-six (66) permanent adult-use cannabis dispensary licenses will be issued. Existing adult-use cannabis licensees under the “early start” regulations must re-apply for licensure under the permanent rules in order to continue adult-use sales.

| 13 |

Under Nevada’s adult-use cannabis law, the Nevada Taxation Department licenses cannabis cultivation facilities, product manufacturing facilities, distributors, retail stores and testing facilities. For the first 18 months, applications to the Nevada Taxation Department for adult-use distribution establishment licenses can only be accepted from existing medical cannabis establishments and existing liquor distributors.

In September 2018, the Nevada Taxation Department accepted applications from existing Nevada medical cannabis establishment certificate owners to be awarded licenses for approximately 65 retail cannabis stores throughout the State. The application period closed on September 20, 2018, and the additional retail store licenses were awarded by the Nevada Taxation Department on December 5, 2018.

Regulatory Overview

The State of Nevada utilizes Metrc as its statewide seed-to-sale tracking system for all cannabis and cannabis products. All licensees within the State system are required, either directly or through third-party software systems that are capable of data integration, to report to the State all creation and transfers of such inventory to other licensees and sales to consumers. CSAC intends to designate a third-party computerized seed-to-sale inventory software tracking system designed to integrate with Metrc via an application programming interface.

Licensing Requirements

There are five certificate/license types issued in the State of Nevada:

“Marijuana cultivation facility” means an entity licensed to cultivate, process, and package cannabis, to have cannabis tested by a cannabis testing facility, and to sell cannabis to retail cannabis stores, to cannabis product manufacturing facilities, and to other cannabis cultivation facilities, but not to consumers. NRS 453D.030(9).

“Marijuana product manufacturing facility” means an entity licensed to purchase cannabis, manufacture, process, and package cannabis and cannabis products, and sell cannabis and cannabis products to other cannabis product manufacturing facilities and to retail cannabis stores, but not to consumers. NRS 453D.030(12).

“Retail marijuana store” means an entity licensed to purchase cannabis from cannabis cultivation facilities, to purchase cannabis and cannabis products from cannabis product manufacturing facilities and retail cannabis stores, and to sell cannabis and cannabis products to consumers. NRS 453D.030(18).

“Marijuana distributor” means an entity licensed to transport cannabis from a cannabis establishment to another cannabis establishment. NRS 453D.030(10).

“Marijuana testing facility” means an entity licensed to test cannabis and cannabis products, including for potency and contaminants. NRS 453D.030(15).

Administration of the regular retail program in Nevada is governed by Nevada Revised Statutes Section 453D and the Adopted Regulation of the Nevada Department of Taxation, LCB File R092-17 (the “Nevada Adult-Use Regulation”). The Nevada Adult-Use Regulation was adopted on February 27, 2018 and is a regulation relating to cannabis responsible for: (i) revising requirements relating to independent testing laboratories; (ii) providing for the licensing of cannabis establishments and registration of cannabis establishment agents; (iii) providing requirements concerning the operation of cannabis establishments; (iv) providing additional requirements concerning the operation of marijuana cultivation facilities, marijuana distributors, marijuana product manufacturing facilities, marijuana testing facilities and retail marijuana stores; (v) providing standards for the packaging and labeling cannabis and cannabis products; (vi) providing requirements relating to the production of edible cannabis products and other cannabis products; (vii) providing standards for the cultivation and production of cannabis; (viii) establishing requirements relating to advertising by cannabis establishments; (ix) establishing provisions relating to the collection of excise taxes from cannabis establishments; (x) establishing provisions relating to dual licensees; and (xi) providing other matters properly relating thereto.

| 14 |

In the State of Nevada, only cannabis that is grown or produced in the state by a licensed establishment may be sold in the state. The Nevada regulatory regime does not mandate or prohibit vertically integrated facilities and only permits the holder of a retail dispensary license and registration certificate to purchase cannabis from cultivation facilities, cannabis and cannabis products from product manufacturing facilities and cannabis from other retail stores, for the sale of such products to consumers.

A medical cultivation license permits its holder to acquire, possess, cultivate, deliver, transfer, have tested, transport, supply or sell cannabis and related supplies to medical cannabis dispensaries, facilities for the production of edible medical cannabis products and/or medical cannabis-infused products, or other medical cannabis cultivation facilities.

The medical product manufacturing license permits its holder to acquire, possess, manufacture, deliver, transfer, transport, supply, or sell edible cannabis products or cannabis infused products to other medical cannabis production facilities or medical cannabis dispensaries.

Medical marijuana establishment certificates and recreational cannabis facility licenses are issued independently to specific owners and at identified locations. Ownership of certificates and licenses is transferable in accordance with the Nevada Taxation Department’s policies and procedures, including completion of a background investigation. Establishment certificates and facility licenses may only be relocated to a new location within the identified local jurisdiction.

All licenses expire one year after the date of issue. The Nevada Taxation Department shall issue a renewal license within 10 days after the receipt of a renewal application and applicable fee if the license is not then under suspension or has not been revoked.

Company Licenses

YMY, in which the Company owns a 50% interest, holds one medical cultivation license and one recreational cultivation license and one medical product manufacturing license and one recreational product manufacturing license in the State of Nevada. The table below lists the licenses indirectly held by the Company:

| Holding Entity | Permit/License | City, State | Expiration Date | Description | ||||

| YMY(1) | 18897864143987354009 | Las Vegas, Nevada | June 30, 2022 | Medical Cultivation License | ||||

| YMY(1) | 49988620104464639364 | Las Vegas, Nevada | June 30, 2022 | Recreational Cultivation License | ||||

| YMY(1) | 78715576282428558550 | Las Vegas, Nevada | June 30, 2022 | Medical Product Manufacturing License | ||||

| YMY(1) | 32704290606712932888 | Las Vegas, Nevada | June 30, 2022 | Recreational Product Manufacturing License |

Note:

| (1) | The Company holds a 50% interest in YMY, which operates a cannabis facility in North Las Vegas, Nevada. |

Nevada Transportation

In Nevada, cannabis may only be transported from a licensed cultivation or production facility to a licensed retail cannabis establishment by a licensed marijuana distributor. Prior to transporting the cannabis or cannabis products, the distributor must complete a trip plan which includes: the agent name and registration number providing and receiving the cannabis; the date and start time of the trip; a description, including the amount, of the cannabis or cannabis products being transported; and the anticipated route of transportation.

| 15 |

During the transportation of cannabis or cannabis products, the licensed marijuana distributor agent must: (a) carry a copy of the trip plan with him or her for the duration of the trip; (b) have his or her cannabis establishment agent card in his or her immediate possession; (c) use a vehicle without any identification relating to cannabis and which is equipped with a secure lockbox or locking cargo area which must be used for the sanitary and secure transportation of cannabis, or cannabis products; (d) have a means of communicating with the cannabis establishment for which he or she is providing the transportation; and (e) ensure that all cannabis or cannabis products are not visible. After transporting cannabis or cannabis products a licensed marijuana distributor agent must enter the end time of the trip and any changes to the trip plan that was completed.

Each licensed marijuana distributor agent transporting cannabis or cannabis products must report any: (a) vehicle accident that occurs during the transportation to a person designated by the marijuana distributor to receive such reports within two (2) hours after the accident occurs; and (b) loss or theft of cannabis or cannabis products that occurs during the transportation to a person designated by the marijuana distributor to receive such reports immediately after the cannabis establishment agent becomes aware of the loss or theft. A marijuana distributor that receives a report of loss or theft pursuant to this paragraph must immediately report the loss or theft to the appropriate law enforcement agency and to the Nevada Taxation Department. The distributor must report any unauthorized stop that lasts longer than two (2) hours to the Nevada Taxation Department.

A marijuana distributor shall maintain the required documents and provide a copy of the documents required to the Nevada Taxation Department for review upon request. Each marijuana distributor shall maintain a log of all received reports.

Employees of licensed marijuana distributors, including drivers transporting cannabis and cannabis products, must be 21 years of age or older and must obtain a valid cannabis establishment agent registration card issued by the Nevada Taxation Department. If a marijuana distributor is co-located with another type of business, all employees of co-located businesses must have cannabis establishment agent registration cards unless the co-located business does not include common entrances, exits, break room, restrooms, locker rooms, loading docks, and other areas as are expedient for business and appropriate for the site as determined and approved by Nevada Taxation Department inspectors. While engaged in the transportation of cannabis and cannabis products, any person that occupies a transport vehicle when it is loaded with cannabis or cannabis products must have their physical cannabis establishment agent registration card in their possession.

All drivers must carry in the vehicle valid driver’s insurance at the limits required by the State of Nevada and the Nevada Taxation Department. All drivers must be bonded in an amount sufficient to cover any claim that could be brought or disclose to all parties that their drivers are not bonded. Cannabis establishment agent registration cardholders and the licensed marijuana distributor they work for are responsible for the cannabis and cannabis product once they take control of the product and leave the premises of the cannabis establishment.

There is no load limit on the amount or weight of cannabis and cannabis products that are being transported by a licensed marijuana distributor. Cannabis distributors are required to adhere to Nevada Taxation Department regulations and those required through their insurance coverage. When transporting by vehicle, cannabis and cannabis product must be in a lockbox or locked cargo area. A trunk of a vehicle is not considered secure storage unless there is no access from within the vehicle and it is not the same key access as the vehicle. Live plants can be transported in a fully enclosed, windowless locked trailer or secured area inside the body/compartment of a locked van or truck so that they are not visible to the outside. If the value of the cannabis and cannabis products being transported by vehicle is in excess of $10,000 (the insured value per the shipping manifest), the transporting vehicle must be equipped with a car alarm with sound or have no less than two (2) of the marijuana distributor’s cannabis establishment agent registration cardholders involved in the transportation. All cannabis and cannabis product must be tagged for purposes of inventory tracking with a unique identifying label as required by the Nevada Taxation Department and remain tagged during transport. This unique identifying label should be similar to the stamp for cigarette distribution. All cannabis and cannabis product when transported by vehicle must be transported in sealed packages and containers and remain unopened during transport. All cannabis and cannabis product transported by vehicle should be inventoried and accounted for in the inventory tracking system. Loading and unloading of cannabis and cannabis products from the transporting vehicle must be within view of existing video surveillance systems prior to leaving the origination location. Security requirements are required for the transportation of cannabis and cannabis products.

| 16 |

Nevada Inventory

Each cannabis establishment must maintain an inventory control system to monitor and report on chain of custody of cannabis in real-time, from the point of harvest at a cultivation facility until it is sold at a dispensary, or it is processed at a facility for the production of edible cannabis products or cannabis-infused products. For this purpose, Nevada tracks information through METRC which maintains the name of each person or cannabis establishment to cannabis is sold, for dispensaries, the date of sales, quantity, and potency. Cannabis establishments must exercise vigilance to ensure personal identifying information contained in the inventory control system is encrypted, protected and not divulged for any purpose not specifically authorized by law.

Nevada Security

To prevent unauthorized access to cannabis at a Nevada-licensed cannabis establishment, the cannabis establishment must have security equipment to deter and prevent unauthorized entrance into limited access areas. This includes devices or a series of devices interconnected with a radio frequency, such as cellular or private radio signals, or other mechanical device, covering the entirety of the facility. Exterior lighting to facilitate surveillance, video cameras with a recording rate of at least 15 frames per second covering all entrances and exits of the building, any room or area that hold a vault or point-of-sale location and which records 24 hours per day. Recordings must be accessible remotely by law enforcement in real time upon request. Video quality providing coverage of a point-of-sale location must allow for the identification of any person purchasing cannabis. Video recording must be restored for at least 30 days in a secure off-site location or other service that provides on-demand access to the Department Nevada Taxation Department.

Department Inspections

Each establishment that has been granted a provisional operating certificate by the Nevada Taxation Department must undergo facility and audit inspections by the Nevada Taxation Department prior to the issuance of a final registration certificate. Additionally, the issuance of a registration certificate is considered provisional until the establishment is in compliance with all applicable local government requirements including, without limitation, the issuance of a local business licenses.

After an establishment registration certificate has been issued, the cannabis establishment is subject to reasonable inspection from the Nevada Taxation Department and a licensee must make himself or herself, or an agent, available and present for any inspection required by the Nevada Taxation Department.

Delivery and Online Distribution

There are specific situations in which the delivery of cannabis to customers is allowed under the Nevada Taxation Department regulations. Delivery services to customers may only be carried out by retail stores that are licensed properly by the Nevada Taxation Department. Deliveries can only be brought to the residential addresses of customers and only within the State of Nevada. Delivery was allowed as soon as retail cannabis sales began on July 1, 2017, although those regulations were only temporary. Drivers may not deliver more than the legal amount of cannabis, which is currently one ounce, in compliance with the existing seed-to-sale tracking system. Cannabis or cannabis products may not be shipped via the US Postal Service or via any private courier.

U.S. Attorney Statements in Nevada

In response to the rescission of the Cole Memo, Nevada Attorney General Adam Laxalt had issued a public statement, pledging to defend the law after it was approved by voters. Then-Governor Brian Sandoval also stated, “Since Nevada voters approved the legalization of recreational cannabis in 2016, I have called for a well-regulated, restricted and respected industry. My administration has worked to ensure these priorities are met while implementing the will of the voters and remaining within the guidelines of both the Cole and Wilkinson federal memos,” and that he would like for Nevada to follow in the footsteps of Colorado, where the U.S. attorneys do not plan to change the approach to prosecuting crimes involving recreational cannabis.

| 17 |

In June 2019, incoming U.S. Attorney of the District of Nevada Nicholas Trutanich stated to the Reno Gazette Journal that he would not rule out the possibility of prosecuting cases related to cannabis, but did emphasize that it also was not a priority. He stated cannabis remains illegal under federal law, and his job is to enforce federal law. He stated, however, that one of his main priorities was to tackle the opioid crisis and human trafficking. He further stated that he is following orders from the DOJ.

To the knowledge of management of Stem, other than as disclosed in this Document, there have not been any statements or guidance made by federal authorities or prosecutors regarding the risk of enforcement action in Nevada. See “Risk Factors”.

New York (Industrial Hemp)

In December 2014, New York State enacted legislation authorizing a research-based industrial hemp program pursuant to authority granted in the Original Farm Bill (as defined herein) (predecessor to the Farm Bill in which industrial hemp was initially legalized in the U.S., though legalization extended to research-related activities only). The state of New York subsequently launched an Industrial Hemp Agricultural Research Pilot Program regulated by the New York Department of Agriculture (“NY DOH”). In December 2018, the state of New York opened an application period for “hemp cannabis,” or industrial hemp grown and processed for cannabinoid content, and particularly for CBD. In late 2019, the state of New York enacted legislation that made sweeping, structural changes to the hemp program. As is relevant to the Company, processing hemp for the purpose of extracting cannabinoids and manufacturing hemp-derived cannabinoid products was removed from NY DOA regulatory oversight and moved to the New York Department of Health (“NY DOA”), which regulates medical cannabis. State regulators have initiated the process of transitioning licensees, such as Sound Wellness, from NY DOA to NY DOH. This process is expected to continue through calendar year 2020. Once the transition is complete, NY DOH is expected to promulgate hemp regulations. No significant changes to the hemp program are expected between now and when NY DOH issues new regulations.

Company Licenses

The table below lists the licenses directly held by the Company:

| Holding Entity | Permit/License | City, State | Expiration Date | Description | ||||

| Stem Holdings Agri, Inc. | HEMP-G-000478 | New York | September 30, 2022 | Industrial Hemp Research Partner Authorization |

Oregon

History

Oregon’s medical cannabis program was introduced in November 1998 when voters approved Measure 67, the Oregon Medical Marijuana Act, with 55% of the vote. In November 2014, voters approved Measure 91, the ‘Oregon Legalized Marijuana Initiative,’ which legalized adult-use cannabis in the state. In October 2015, the first adult-use dispensaries opened for sale.

Regulatory Summary

There are four types of adult-use cannabis licenses: producer, processor, wholesaler and retail. Additionally, the Oregon Liquor Control Commission (“OLCC”) grants a certificate for research and a hemp certificate. A producer is permitted to cultivate cannabis. A processor is permitted to transform raw cannabis into another product (topicals, edibles, concentrates, or extracts). A wholesaler is permitted to buy cannabis in bulk and sell to licensees but not to consumers. A retailer is permitted to sell cannabis to consumers. A laboratory is permitted to test cannabis based on rules established by the Oregon Health Authority. To receive a laboratory license, the lab must be accredited by the Oregon Environmental Laboratory Accreditation program. The hemp certificate allows persons that are registered with the Oregon Department of Agriculture to transfer hemp flower, extracts, or concentrates to OLCC licensed processors who hold an industrial hemp processor endorsement.

| 18 |

Company Licenses

Pursuant to the purchase of the Operating Companies by the Company, Stem has acquired an interest in five retail licenses, five producer licenses, two wholesaler license and three processing licenses.

The table below lists the licenses that are: (i) directly held by the Company; and (ii) held by the Company’s operating partners:

| Holding Entity | Permit/License | City, State | License Expiration Date | Description | ||||

| JV Foods LLC | 030-1014658322F | Eugene, Oregon | September 3, 2022 | Recreational Processor | ||||

| JV Extraction LLC | 030-1014657D1EC | Eugene, Oregon | September 3, 2022 | Recreational Processor | ||||

| JV Extraction LLC/JV Wholesale LLC | 030-101742659A2 | Eugene, Oregon | September 16, 2022 | Recreational Processor | ||||

| JV Applegate LLC | 020-10146602629 | Jacksonville, Oregon | November 11, 2022 | Recreational Producer | ||||

| JV Wholesale LLC | 060-10146555C41 | Eugene, Oregon | September 3, 2022 | Recreational Wholesaler | ||||

| JV Extraction LLC/JV Wholesale LLC | 060-1017430C9B0 | Eugene, Oregon | September 16, 2022 | Recreational Wholesaler | ||||

| JV Wholesale LLC | 060-10118468E74 | Eugene, Oregon | June 2, 2022 | Recreational Wholesaler | ||||

| JV Production 3 LLC | 020-1014656E7A7 | Eugene, Oregon | September 3, 2022 | Recreational Producer | ||||

| OpCo Production 2 LLC | 020-10146517BD5 | Mulino, Oregon | September 3, 2022 | Recreational Producer | ||||

| OpCo Production 1 LLC | 020-10146613F29 | Springfield, Oregon | September 5, 2022 | Recreational Producer | ||||

| JV Retail 3 LLC | 050-1017428AB09 | Eugene, Oregon | September 16, 2022 | Recreational Retailer | ||||

| JV Retail 4 LLC | 050-1017432812F | Salem, Oregon | September 16, 2022 | Recreational Retailer | ||||

| OPCO Retail 1 LLC | 050-10146522DCF | Portland, Oregon | September 3, 2022 | Recreational Retailer | ||||

| JV Retail 2 LLC | 050-1014653D811 | Eugene, Oregon | September 3, 2022 | Recreational Retailer | ||||

| Kind Care, LLC | 050-10146546503 | Eugene, Oregon | September 3, 2022 | Recreational Retailer | ||||

| Stem Holdings Oregon, Inc. | 020-1013432D099 | Hillsboro, Oregon | June 23, 2022 | Recreational Producer |

Oregon Transportation

Licensed producers which transport cannabis to licensed retailers must comply with the following: (a) a licensee must keep cannabis items in transit shielded from public view, (b) the cannabis items must be of secured (locked-up) during transport, (c) the transport must be equipped with an alarm system, (d) the transport must be temperature controlled if perishable cannabis items are being transported, (e) the transport must provide arrival date and estimated time of arrival information, (f) all cannabis items must be packaged in shipping containers and labeled with a unique identifier, and (g) the transport must provide a copy of the printed manifest and any printed receipts for cannabis items delivered to law enforcement officers or other representatives of a government agency if requested to do so while in transit.

| 19 |

Oregon Inventory/Storage

OLCC licensees must report the following to Oregon’s Cannabis Tracking System (“CTS”) (a) a reconciliation of all on-premise and in-transit cannabis item inventories each day, (b) all information for seeds, usable cannabis, CBD concentrates and extracts by weight, (c) the wet weight of all harvested cannabis plants immediately after harvest, (d) all required information for CBD products by unit count, and (e) for retailer license holders, the price before tax and amount of each item sold to consumers and the date of each transaction. The data must be transmitted for each individual transaction before the retailer opens the next business day. All cannabis items on a licensed retailer’s premises must be held in a safe or vault. All usable cannabis, cut and drying mature cannabis plants, CBD concentrates, extracts or products on the licensed premises of a licensee other than a retailer are to be kept in a locked, enclosed area within the licensed premises that is secured with at a minimum, a steel door with a steel frame or equivalent, and a commercial grade, non-residential door lock. All licensees must keep all video recordings and archived required records not stored electronically in a locked storage area. Current records may be kept in a locked cupboard or desk outside the locked storage area during hours when the licensed business is open.

Oregon Record-keeping/Reporting