Summit Materials, Inc. - Quarter Report: 2023 September (Form 10-Q)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM | 10-Q | ||||

(Mark One) | |||||||||||

| ☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||||

For the quarterly period ended September 30, 2023

OR

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||

For the transition period from to

Commission file numbers:

001-36873 (Summit Materials, Inc.)

333-187556 (Summit Materials, LLC)

| SUMMIT MATERIALS, INC. | ||

SUMMIT MATERIALS, LLC | ||

(Exact name of registrants as specified in their charters) | ||

Delaware (Summit Materials, Inc.) | 47-1984212 | |||||||

Delaware (Summit Materials, LLC) | 26-4138486 | |||||||

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

1801 California Street, Suite 3500 | 80202 | |||||||

Denver, Colorado | (Zip Code) | |||||||

| (Address of principal executive offices) | ||||||||

Registrants’ telephone number, including area code: (303) 893-0012

Not Applicable

(Former name, former address and former fiscal year, if changed since last report)

| Securities registered pursuant to Section 12(b) of the Act: | ||||||||||||||

| Title of each class | Trading symbol(s) | Name of each exchange on which registered | ||||||||||||

| Class A Common Stock (par value $.01 per share) | SUM | New York Stock Exchange | ||||||||||||

| Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | ||||||||||||||||||||||||||||||||

| Summit Materials, Inc. | Yes | ☒ | No | ☐ | Summit Materials, LLC | Yes | ☒ | No | ☐ | |||||||||||||||||||||||

| Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S‑T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). | ||||||||||||||||||||||||||||||||

| Summit Materials, Inc. | Yes | ☒ | No | ☐ | Summit Materials, LLC | Yes | ☒ | No | ☐ | |||||||||||||||||||||||

| Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. | ||||||||||||||||||||||||||||||||

| Summit Materials, Inc. | ||||||||||||||||||||||||||||||||

| Large accelerated filer | ☒ | Accelerated filer | ☐ | |||||||||||||||||||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ☐ | |||||||||||||||||||||||||||||

| Emerging growth company | ☐ | |||||||||||||||||||||||||||||||

| If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. | ☐ | |||||||||||||||||||||||||||||||

| Summit Materials, LLC | ||||||||||||||||||||||||||||||||

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||||||||||||||||||||||||||||

| Non-accelerated filer | ☒ | Smaller reporting company | ☐ | |||||||||||||||||||||||||||||

| Emerging growth company | ☐ | |||||||||||||||||||||||||||||||

| If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. | ☐ | |||||||||||||||||||||||||||||||

| Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). | ||||||||||||||||||||||||||||||||

| Summit Materials, Inc. | Yes | ☐ | No | ☒ | Summit Materials, LLC | Yes | ☐ | No | ☒ | |||||||||||||||||||||||

As of October 31, 2023, the number of shares of Summit Materials, Inc.’s outstanding Class A and Class B common stock, par value $0.01 per share for each class, was 119,460,587 and 99, respectively.

As of October 31, 2023, 100% of Summit Materials, LLC’s outstanding limited liability company interests were held by Summit Materials Intermediate Holdings, LLC, its sole member and an indirect subsidiary of Summit Materials, Inc.

EXPLANATORY NOTE

This quarterly report on Form 10-Q (this “report”) is a combined quarterly report being filed separately by two registrants: Summit Materials, Inc. and Summit Materials, LLC. Each registrant hereto is filing on its own behalf all of the information contained in this report that relates to such registrant. Each registrant hereto is not filing any information that does not relate to such registrant, and therefore makes no representation as to any such information. We believe that combining the quarterly reports on Form 10-Q of Summit Materials, Inc. and Summit Materials, LLC into this single report eliminates duplicative and potentially confusing disclosure and provides a more streamlined presentation since a substantial amount of the disclosure applies to both registrants.

Unless stated otherwise or the context requires otherwise, references to “Summit Inc.” mean Summit Materials, Inc., a Delaware corporation, and references to “Summit LLC” mean Summit Materials, LLC, a Delaware limited liability company. The references to Summit Inc. and Summit LLC are used in cases where it is important to distinguish between them. We use the terms “we,” “our,” “us” or “the Company” to refer to Summit Inc. and Summit LLC together with their respective subsidiaries, unless otherwise noted or the context otherwise requires.

Summit Inc. was formed on September 23, 2014 to be a holding company. As of September 30, 2023, its sole material asset was a 99.1% economic interest in Summit Materials Holdings L.P., a Delaware limited partnership (“Summit Holdings”). Summit Inc. has 100% of the voting rights of Summit Holdings, which is the indirect parent of Summit LLC. Summit LLC is a co-issuer of our outstanding 6 1/2 % senior notes due 2027 (“2027 Notes”) and our 5 1/4% senior notes due 2029 (“2029 Notes” and collectively with the 2027 Notes, the “Senior Notes”). Summit Inc.’s only revenue for the three and nine months ended September 30, 2023 was that generated by Summit LLC and its consolidated subsidiaries. Summit Inc. controls all of the business and affairs of Summit Holdings and, in turn, Summit LLC.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This report includes “forward-looking statements” within the meaning of the federal securities laws, which involve risks and uncertainties. Forward-looking statements include all statements that do not relate solely to historical or current facts, and you can identify forward-looking statements because they contain words such as “believes,” “expects,” “may,” “will,” “should,” “seeks,” “intends,” “trends,” “plans,” “estimates,” “projects” or “anticipates” or similar expressions that concern our strategy, plans, expectations or intentions. All statements made relating to our estimated and projected earnings, margins, costs, expenditures, cash flows, growth rates and financial results are forward-looking statements. These forward-looking statements are subject to risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from future results, performance or achievements expressed or implied by such forward-looking statements. We derive many of our forward-looking statements from our operating budgets and forecasts, which are based upon many detailed assumptions. While we believe that our assumptions are reasonable, it is very difficult to predict the effect of known factors, and, of course, it is impossible to anticipate all factors that could affect our actual results. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation by us or any other person that the results or conditions described in such statements or our objectives and plans will be realized. Important factors could affect our results and could cause results to differ materially from those expressed in our forward-looking statements, including but not limited to the factors discussed in the section entitled “Risk Factors” in Summit Inc.’s Annual Report on Form 10-K for the fiscal year ended December 31, 2022 (the “Annual Report”), as filed with the Securities and Exchange Commission (the “SEC”), the factors discussed in the section entitled “Risk Factors” of this report and the following:

•our dependence on the construction industry and the strength of the local economies in which we operate, including residential;

•the cyclical nature of our business;

•risks related to weather and seasonality;

•risks associated with our capital-intensive business;

•competition within our local markets;

•our ability to execute on our acquisition strategy and portfolio optimization strategy, successfully integrate acquisitions with our existing operations and retain key employees of acquired businesses;

•our dependence on securing and permitting aggregate reserves in strategically located areas;

•the impact of rising interest rates, and diminished liquidity and credit availability in the market broadly;

•declines in public infrastructure construction and delays or reductions in governmental funding, including the funding by transportation authorities, the federal government and other state agencies particularly;

•our reliance on private investment in infrastructure, which may be adversely affected by periods of economic stagnation and recession;

•environmental, health, safety and climate change laws or governmental requirements or policies concerning zoning and land use;

•rising prices for, or more limited availability of, commodities, labor and other production and delivery inputs as a result of inflation, supply chain challenges or otherwise;

•conditions in the credit markets;

•our ability to accurately estimate the overall risks, requirements or costs when we bid on or negotiate contracts that are ultimately awarded to us;

•material costs and losses as a result of claims that our products do not meet regulatory requirements or contractual specifications;

•cancellation of a significant number of contracts or our disqualification from bidding for new contracts;

•special hazards related to our operations that may cause personal injury or property damage not covered by insurance;

•unexpected factors affecting self-insurance claims and reserve estimates;

•our current level of indebtedness, including our exposure to variable interest rate risk;

•our dependence on senior management and other key personnel, and our ability to retain and attract qualified personnel;

•supply constraints or significant price fluctuations in the electricity and petroleum-based resources that we use, including diesel and liquid asphalt;

•climate change and climate change legislation or other regulations;

•unexpected operational difficulties;

•costs associated with pending and future litigation;

•interruptions in our information technology systems and infrastructure, including cybersecurity and data leakage risks;

•potential labor disputes, strikes, other forms of work stoppage or other union activities;

•the impact of the COVID-19 pandemic, and responses to it, including vaccine mandates, or any similar crisis, on our activities; and

•material or adverse effects related to the pending Argos USA combination.

All subsequent written and oral forward-looking statements attributable to us, or persons acting on our behalf, are expressly qualified in their entirety by these cautionary statements.

Any forward-looking statement that we make herein speaks only as of the date of this report. We undertake no obligation to publicly update or revise any forward-looking statement as a result of new information, future events or otherwise, except as required by law.

CERTAIN DEFINITIONS

As used in this report, unless otherwise noted or the context otherwise requires:

•“EBITDA” refers to net income (loss) before interest expense (income), income tax expense (benefit) and depreciation, depletion and amortization;

•“Finance Corp.” refers to Summit Materials Finance Corp., an indirect wholly-owned subsidiary of Summit LLC and the co-issuer of the Senior Notes;

•“LP Units” refers to the Class A limited partnership units of Summit Holdings; and

•“TRA” refers to a tax receivable agreement between Summit Inc. and certain current and former holders of LP Units and their permitted assignees.

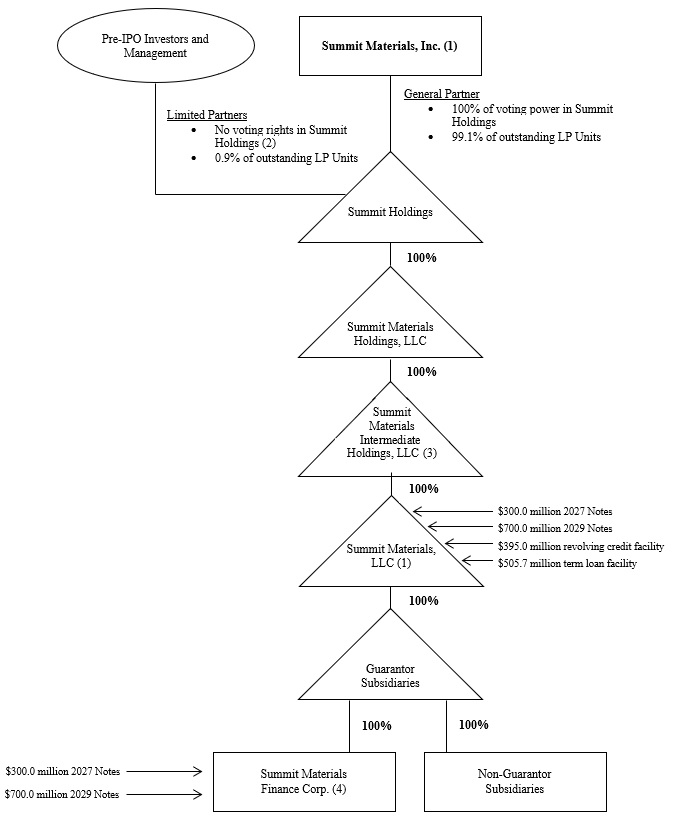

Corporate Structure

The following chart summarizes our organizational structure, equity ownership and our principal indebtedness as of September 30, 2023. This chart is provided for illustrative purposes only and does not show all of our legal entities or all obligations of such entities.

(1)SEC registrant.

(2)The shares of Class B Common Stock are currently held by pre-IPO investors, including certain members of management or their family trusts that directly hold LP Units. A holder of Class B Common Stock is entitled, without regard to the number of shares of Class B Common Stock held by such holder, to a number of votes that is equal to the aggregate number of LP Units held by such holder.

(3)Guarantor under the senior secured credit facilities, but not the Senior Notes.

(4)Summit LLC and Finance Corp are the issuers of the Senior Notes and Summit LLC is the borrower under our senior secured credit facilities. Finance Corp. was formed solely for the purpose of serving as co-issuer or guarantor of certain indebtedness, including the Senior Notes. Finance Corp. does not and will not have operations of any kind and does not and will not have revenue or assets other than as may be incidental to its activities as a co-issuer or guarantor of certain indebtedness.

SUMMIT MATERIALS, INC.

SUMMIT MATERIALS, LLC

FORM 10-Q

TABLE OF CONTENTS

| Page No. | ||||||||

PART I—Financial Information | ||||||||

Consolidated Balance Sheets as of September 30, 2023 (unaudited) and December 31, 2022 | ||||||||

Unaudited Consolidated Statements of Operations for the three and nine months ended September 30, 2023 and October 1, 2022 | ||||||||

Unaudited Consolidated Statements of Comprehensive Income for the three and nine months ended September 30, 2023 and October 1, 2022 | ||||||||

Unaudited Consolidated Statements of Cash Flows for the nine months ended September 30, 2023 and October 1, 2022 | ||||||||

Unaudited Consolidated Statements of Changes in Stockholders’ Equity for the three and nine months ended September 30, 2023 and October 1, 2022 | ||||||||

PART II — Other Information | ||||||||

PART I—FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

SUMMIT MATERIALS, INC. AND SUBSIDIARIES

Consolidated Balance Sheets

(In thousands, except share and per share amounts)

| September 30, 2023 | December 31, 2022 | ||||||||||

| (unaudited) | (audited) | ||||||||||

| Assets | |||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | 197,475 | $ | 520,451 | |||||||

| Accounts receivable, net | 375,929 | 256,669 | |||||||||

| Costs and estimated earnings in excess of billings | 40,985 | 6,510 | |||||||||

| Inventories | 243,136 | 212,491 | |||||||||

| Other current assets | 17,976 | 20,787 | |||||||||

| Current assets held for sale | 1,702 | 1,468 | |||||||||

| Total current assets | 877,203 | 1,018,376 | |||||||||

Property, plant and equipment, less accumulated depreciation, depletion and amortization (September 30, 2023 - $1,387,348 and December 31, 2022 - $1,267,557) | 1,974,532 | 1,813,702 | |||||||||

| Goodwill | 1,241,472 | 1,132,546 | |||||||||

Intangible assets, less accumulated amortization (September 30, 2023 - $18,115 and December 31, 2022 - $15,503) | 68,814 | 71,384 | |||||||||

Deferred tax assets, less valuation allowance (September 30, 2023 - $1,113 and December 31, 2022 - $1,113) | 113,362 | 136,986 | |||||||||

| Operating lease right-of-use assets | 38,380 | 37,889 | |||||||||

| Other assets | 51,201 | 44,809 | |||||||||

| Total assets | $ | 4,364,964 | $ | 4,255,692 | |||||||

| Liabilities and Stockholders’ Equity | |||||||||||

| Current liabilities: | |||||||||||

| Current portion of debt | $ | 3,822 | $ | 5,096 | |||||||

| Current portion of acquisition-related liabilities | 7,028 | 13,718 | |||||||||

| Accounts payable | 173,127 | 104,031 | |||||||||

| Accrued expenses | 147,619 | 119,967 | |||||||||

| Current operating lease liabilities | 8,745 | 7,296 | |||||||||

| Billings in excess of costs and estimated earnings | 8,539 | 5,739 | |||||||||

| Total current liabilities | 348,880 | 255,847 | |||||||||

| Long-term debt | 1,488,069 | 1,488,569 | |||||||||

| Acquisition-related liabilities | 27,633 | 29,051 | |||||||||

| Tax receivable agreement liability | 52,143 | 327,812 | |||||||||

| Noncurrent operating lease liabilities | 34,838 | 35,737 | |||||||||

| Other noncurrent liabilities | 105,668 | 106,686 | |||||||||

| Total liabilities | 2,057,231 | 2,243,702 | |||||||||

| Commitments and contingencies (see note 12) | |||||||||||

| Stockholders’ equity: | |||||||||||

Class A common stock, par value $0.01 per share; 1,000,000,000 shares authorized, 119,112,950 and 118,408,655 shares issued and outstanding as of September 30, 2023 and December 31, 2022, respectively | 1,192 | 1,185 | |||||||||

Class B common stock, par value $0.01 per share; 250,000,000 shares authorized, 99 shares issued and outstanding as of September 30, 2023 and December 31, 2022 | — | — | |||||||||

| Additional paid-in capital | 1,415,320 | 1,404,122 | |||||||||

| Accumulated earnings | 873,773 | 590,895 | |||||||||

| Accumulated other comprehensive income | 3,296 | 3,084 | |||||||||

| Stockholders’ equity | 2,293,581 | 1,999,286 | |||||||||

| Noncontrolling interest in Summit Holdings | 14,152 | 12,704 | |||||||||

| Total stockholders’ equity | 2,307,733 | 2,011,990 | |||||||||

| Total liabilities and stockholders’ equity | $ | 4,364,964 | $ | 4,255,692 | |||||||

See notes to unaudited consolidated financial statements.

1

SUMMIT MATERIALS, INC. AND SUBSIDIARIES

Unaudited Consolidated Statements of Operations

(In thousands, except share and per share amounts)

| Three months ended | Nine months ended | ||||||||||||||||||||||

| September 30, 2023 | October 1, 2022 | September 30, 2023 | October 1, 2022 | ||||||||||||||||||||

| Revenue: | |||||||||||||||||||||||

| Product | $ | 641,778 | $ | 587,138 | $ | 1,609,664 | $ | 1,485,746 | |||||||||||||||

| Service | 100,182 | 98,871 | 219,939 | 224,676 | |||||||||||||||||||

| Net revenue | 741,960 | 686,009 | 1,829,603 | 1,710,422 | |||||||||||||||||||

| Delivery and subcontract revenue | 52,837 | 66,738 | 129,732 | 149,826 | |||||||||||||||||||

| Total revenue | 794,797 | 752,747 | 1,959,335 | 1,860,248 | |||||||||||||||||||

| Cost of revenue (excluding items shown separately below): | |||||||||||||||||||||||

| Product | 412,784 | 392,187 | 1,086,299 | 1,042,888 | |||||||||||||||||||

| Service | 77,538 | 76,011 | 173,568 | 179,807 | |||||||||||||||||||

| Net cost of revenue | 490,322 | 468,198 | 1,259,867 | 1,222,695 | |||||||||||||||||||

| Delivery and subcontract cost | 52,837 | 66,738 | 129,732 | 149,826 | |||||||||||||||||||

| Total cost of revenue | 543,159 | 534,936 | 1,389,599 | 1,372,521 | |||||||||||||||||||

| General and administrative expenses | 50,895 | 39,232 | 150,731 | 136,897 | |||||||||||||||||||

| Depreciation, depletion, amortization and accretion | 57,452 | 52,133 | 163,133 | 150,483 | |||||||||||||||||||

| Transaction costs | 17,442 | 727 | 19,518 | 2,637 | |||||||||||||||||||

| Gain on sale of property, plant and equipment | (2,134) | (1,343) | (5,787) | (6,293) | |||||||||||||||||||

| Operating income | 127,983 | 127,062 | 242,141 | 204,003 | |||||||||||||||||||

| Interest expense | 28,013 | 21,980 | 83,335 | 62,728 | |||||||||||||||||||

| Loss on debt financings | — | — | 493 | — | |||||||||||||||||||

| Tax receivable agreement (benefit) expense | (153,080) | — | (153,080) | 954 | |||||||||||||||||||

| Gain on sale of businesses | — | (4,115) | — | (174,373) | |||||||||||||||||||

| Other income, net | (3,583) | (3,283) | (14,771) | (4,956) | |||||||||||||||||||

| Income from operations before taxes | 256,633 | 112,480 | 326,164 | 319,650 | |||||||||||||||||||

| Income tax expense | 23,908 | 24,829 | 39,923 | 74,033 | |||||||||||||||||||

| Net income | 232,725 | 87,651 | 286,241 | 245,617 | |||||||||||||||||||

| Net income attributable to noncontrolling interest in Summit Holdings | 2,680 | 1,162 | 3,363 | 3,307 | |||||||||||||||||||

| Net income attributable to Summit Inc. | $ | 230,045 | $ | 86,489 | $ | 282,878 | $ | 242,310 | |||||||||||||||

| Earnings per share of Class A common stock: | |||||||||||||||||||||||

| Basic | $ | 1.93 | $ | 0.72 | $ | 2.38 | $ | 2.01 | |||||||||||||||

| Diluted | $ | 1.92 | $ | 0.72 | $ | 2.37 | $ | 2.00 | |||||||||||||||

| Weighted average shares of Class A common stock: | |||||||||||||||||||||||

| Basic | 119,013,331 | 119,896,272 | 118,874,967 | 120,345,015 | |||||||||||||||||||

| Diluted | 119,725,693 | 120,383,312 | 119,558,974 | 121,078,150 | |||||||||||||||||||

See notes to unaudited consolidated financial statements.

2

SUMMIT MATERIALS, INC. AND SUBSIDIARIES

Unaudited Consolidated Statements of Comprehensive Income

(In thousands)

| Three months ended | Nine months ended | ||||||||||||||||||||||

| September 30, 2023 | October 1, 2022 | September 30, 2023 | October 1, 2022 | ||||||||||||||||||||

| Net income | $ | 232,725 | $ | 87,651 | $ | 286,241 | $ | 245,617 | |||||||||||||||

| Other comprehensive income (loss): | |||||||||||||||||||||||

| Foreign currency translation adjustment | (3,810) | (10,247) | 295 | (14,113) | |||||||||||||||||||

| Less tax effect of other comprehensive income (loss) items | 738 | 2,470 | (80) | 3,404 | |||||||||||||||||||

| Other comprehensive (loss) income | (3,072) | (7,777) | 215 | (10,709) | |||||||||||||||||||

| Comprehensive income | 229,653 | 79,874 | 286,456 | 234,908 | |||||||||||||||||||

| Less comprehensive income attributable to Summit Holdings | 2,638 | 1,048 | 3,366 | 3,151 | |||||||||||||||||||

| Comprehensive income attributable to Summit Inc. | $ | 227,015 | $ | 78,826 | $ | 283,090 | $ | 231,757 | |||||||||||||||

See notes to unaudited consolidated financial statements.

3

SUMMIT MATERIALS, INC. AND SUBSIDIARIES

Unaudited Consolidated Statements of Cash Flows

(In thousands)

| Nine months ended | |||||||||||

| September 30, 2023 | October 1, 2022 | ||||||||||

| Cash flows from operating activities: | |||||||||||

| Net income | $ | 286,241 | $ | 245,617 | |||||||

| Adjustments to reconcile net income to net cash provided by operating activities: | |||||||||||

| Depreciation, depletion, amortization and accretion | 168,758 | 160,162 | |||||||||

| Share-based compensation expense | 15,116 | 15,058 | |||||||||

| Net gain on asset and business disposals | (5,790) | (180,240) | |||||||||

| Non-cash loss on debt financings | 161 | — | |||||||||

| Change in deferred tax asset, net | 23,540 | 58,318 | |||||||||

| Other | (105) | (396) | |||||||||

| Decrease (increase) in operating assets, net of acquisitions and dispositions: | |||||||||||

| Accounts receivable, net | (107,349) | (96,724) | |||||||||

| Inventories | (23,935) | (53,762) | |||||||||

| Costs and estimated earnings in excess of billings | (34,463) | (32,042) | |||||||||

| Other current assets | 4,438 | (6,961) | |||||||||

| Other assets | 2,208 | 3,432 | |||||||||

| (Decrease) increase in operating liabilities, net of acquisitions and dispositions: | |||||||||||

| Accounts payable | 48,524 | 44,510 | |||||||||

| Accrued expenses | 19,034 | (21,780) | |||||||||

| Billings in excess of costs and estimated earnings | 2,812 | 646 | |||||||||

| Tax receivable agreement benefit | (153,080) | 954 | |||||||||

| Other liabilities | (2,486) | (4,601) | |||||||||

| Net cash provided by operating activities | 243,624 | 132,191 | |||||||||

| Cash flows from investing activities: | |||||||||||

| Acquisitions, net of cash acquired | (239,508) | (1,933) | |||||||||

| Purchases of property, plant and equipment | (182,182) | (189,008) | |||||||||

| Proceeds from the sale of property, plant and equipment | 9,760 | 8,298 | |||||||||

| Proceeds from sale of businesses | — | 373,790 | |||||||||

| Other | (3,602) | (2,214) | |||||||||

| Net cash (used in) provided by investing activities | (415,532) | 188,933 | |||||||||

| Cash flows from financing activities: | |||||||||||

| Debt issuance costs | (1,566) | — | |||||||||

| Payments on debt | (8,520) | (113,769) | |||||||||

| Purchase of tax receivable agreement interests | (122,935) | — | |||||||||

| Payments on acquisition-related liabilities | (12,203) | (12,964) | |||||||||

| Distributions from partnership | (60) | (399) | |||||||||

| Repurchases of common stock | — | (100,980) | |||||||||

| Proceeds from stock option exercises | 112 | 199 | |||||||||

| Other | (6,011) | (774) | |||||||||

| Net cash used in financing activities | (151,183) | (228,687) | |||||||||

| Impact of foreign currency on cash | 115 | (1,732) | |||||||||

| Net (decrease) increase in cash | (322,976) | 90,705 | |||||||||

| Cash and cash equivalents—beginning of period | 520,451 | 380,961 | |||||||||

| Cash and cash equivalents—end of period | $ | 197,475 | $ | 471,666 | |||||||

See notes to unaudited consolidated financial statements.

4

SUMMIT MATERIALS, INC. AND SUBSIDIARIES

Unaudited Consolidated Statements of Changes in Stockholders’ Equity

(In thousands, except share amounts)

| Summit Materials, Inc. | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Accumulated | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other | Class A | Class B | Additional | Noncontrolling | Total | ||||||||||||||||||||||||||||||||||||||||||||||||

| Accumulated | Comprehensive | Common Stock | Common Stock | Paid-in | Interest in | Stockholders’ | |||||||||||||||||||||||||||||||||||||||||||||||

| Earnings | income | Shares | Dollars | Shares | Dollars | Capital | Summit Holdings | Equity | |||||||||||||||||||||||||||||||||||||||||||||

| Balance - December 31, 2022 | $ | 590,895 | $ | 3,084 | 118,408,655 | $ | 1,185 | 99 | $ | — | $ | 1,404,122 | $ | 12,704 | $ | 2,011,990 | |||||||||||||||||||||||||||||||||||||

| Net loss | (30,804) | — | — | — | — | — | — | (408) | (31,212) | ||||||||||||||||||||||||||||||||||||||||||||

| LP Unit exchanges | — | — | 2,000 | — | — | — | 21 | (21) | — | ||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive income, net of tax | — | 161 | — | — | — | — | — | 3 | 164 | ||||||||||||||||||||||||||||||||||||||||||||

| Stock option exercises | — | — | 902 | — | — | — | 15 | — | 15 | ||||||||||||||||||||||||||||||||||||||||||||

| Share-based compensation | — | — | — | — | — | — | 4,708 | — | 4,708 | ||||||||||||||||||||||||||||||||||||||||||||

| Shares redeemed to settle taxes and other | — | — | 407,114 | 4 | — | — | (5,680) | (43) | (5,719) | ||||||||||||||||||||||||||||||||||||||||||||

| Balance — April 1, 2023 | $ | 560,091 | $ | 3,245 | 118,818,671 | $ | 1,189 | 99 | $ | — | $ | 1,403,186 | $ | 12,235 | $ | 1,979,946 | |||||||||||||||||||||||||||||||||||||

| Net income | 83,637 | — | — | — | — | — | — | 1,091 | 84,728 | ||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive income, net of tax | — | 3,081 | — | — | — | — | — | 42 | 3,123 | ||||||||||||||||||||||||||||||||||||||||||||

| Stock option exercises | — | — | 3,338 | — | — | — | 69 | — | 69 | ||||||||||||||||||||||||||||||||||||||||||||

| Share-based compensation | — | — | — | — | — | — | 5,216 | — | 5,216 | ||||||||||||||||||||||||||||||||||||||||||||

| Shares redeemed to settle taxes and other | — | — | 64,265 | 1 | — | — | 893 | (12) | 882 | ||||||||||||||||||||||||||||||||||||||||||||

| Balance — July 1, 2023 | $ | 643,728 | $ | 6,326 | 118,886,274 | $ | 1,190 | 99 | $ | — | $ | 1,409,364 | $ | 13,356 | $ | 2,073,964 | |||||||||||||||||||||||||||||||||||||

| Net income | 230,045 | — | — | — | — | — | — | 2,680 | 232,725 | ||||||||||||||||||||||||||||||||||||||||||||

| LP Unit exchanges | — | — | 174,258 | 2 | — | — | 1,776 | (1,778) | — | ||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive loss, net of tax | — | (3,030) | — | — | — | — | — | (42) | (3,072) | ||||||||||||||||||||||||||||||||||||||||||||

| Stock option exercises | — | — | 1,167 | — | — | — | 28 | — | 28 | ||||||||||||||||||||||||||||||||||||||||||||

| Share-based compensation | — | — | — | — | — | — | 5,192 | — | 5,192 | ||||||||||||||||||||||||||||||||||||||||||||

| Distributions from partnership | — | — | — | — | — | — | — | (60) | (60) | ||||||||||||||||||||||||||||||||||||||||||||

| Shares redeemed to settle taxes and other | — | — | 51,251 | — | — | — | (1,040) | (4) | (1,044) | ||||||||||||||||||||||||||||||||||||||||||||

| Balance - September 30, 2023 | $ | 873,773 | $ | 3,296 | 119,112,950 | $ | 1,192 | 99 | $ | — | $ | 1,415,320 | $ | 14,152 | $ | 2,307,733 | |||||||||||||||||||||||||||||||||||||

5

| Summit Materials, Inc. | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Accumulated | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other | Class A | Class B | Additional | Noncontrolling | Total | ||||||||||||||||||||||||||||||||||||||||||||||||

| Accumulated | Comprehensive | Common Stock | Common Stock | Paid-in | Interest in | Stockholders’ | |||||||||||||||||||||||||||||||||||||||||||||||

| Earnings | income | Shares | Dollars | Shares | Dollars | Capital | Summit Holdings | Equity | |||||||||||||||||||||||||||||||||||||||||||||

| Balance — January 1, 2022 | $ | 478,956 | $ | 7,083 | 118,705,108 | $ | 1,188 | 99 | $ | — | $ | 1,326,340 | $ | 9,645 | $ | 1,823,212 | |||||||||||||||||||||||||||||||||||||

| Net loss | (34,292) | — | — | — | — | — | — | (508) | (34,800) | ||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive income, net of tax | — | 1,306 | — | — | — | — | — | 19 | 1,325 | ||||||||||||||||||||||||||||||||||||||||||||

| Stock option exercises | — | — | 1,589 | — | — | — | 27 | — | 27 | ||||||||||||||||||||||||||||||||||||||||||||

| Share-based compensation | — | — | — | — | — | — | 5,422 | — | 5,422 | ||||||||||||||||||||||||||||||||||||||||||||

| Repurchases of common stock | (47,494) | — | (1,506,878) | (15) | — | — | (121) | 121 | (47,509) | ||||||||||||||||||||||||||||||||||||||||||||

| Shares redeemed to settle taxes and other | — | — | 842,029 | 8 | — | — | (1,120) | (68) | (1,180) | ||||||||||||||||||||||||||||||||||||||||||||

| Balance — April 2, 2022 | $ | 397,170 | $ | 8,389 | 118,041,848 | $ | 1,181 | 99 | $ | — | $ | 1,330,548 | $ | 9,209 | $ | 1,746,497 | |||||||||||||||||||||||||||||||||||||

| Net income | 190,113 | — | — | — | — | — | — | 2,653 | 192,766 | ||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive loss, net of tax | — | (4,196) | — | — | — | — | — | (61) | (4,257) | ||||||||||||||||||||||||||||||||||||||||||||

| Stock option exercises | — | — | 4,929 | — | — | — | 96 | — | 96 | ||||||||||||||||||||||||||||||||||||||||||||

| Share-based compensation | — | — | — | — | — | — | 4,734 | — | 4,734 | ||||||||||||||||||||||||||||||||||||||||||||

| Distributions from partnership | — | — | — | — | — | — | — | (25) | (25) | ||||||||||||||||||||||||||||||||||||||||||||

| Shares redeemed to settle taxes and other | — | — | 67,835 | 1 | — | — | 997 | (7) | 991 | ||||||||||||||||||||||||||||||||||||||||||||

| Balance — July 2, 2022 | $ | 587,283 | $ | 4,193 | 118,114,612 | $ | 1,182 | 99 | $ | — | $ | 1,336,375 | $ | 11,769 | $ | 1,940,802 | |||||||||||||||||||||||||||||||||||||

| Net income | 86,489 | — | — | — | — | — | — | 1,162 | 87,651 | ||||||||||||||||||||||||||||||||||||||||||||

| LP Unit exchanges | — | — | 2,000 | — | — | — | 34 | (34) | — | ||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive loss, net of tax | — | (7,663) | — | — | — | — | — | (114) | (7,777) | ||||||||||||||||||||||||||||||||||||||||||||

| Stock option exercises | — | — | 3,580 | — | — | — | 76 | — | 76 | ||||||||||||||||||||||||||||||||||||||||||||

| Share-based compensation | — | — | — | — | — | — | 4,902 | — | 4,902 | ||||||||||||||||||||||||||||||||||||||||||||

| Repurchases of common stock | (53,452) | — | (1,920,632) | (19) | — | — | (198) | 198 | (53,471) | ||||||||||||||||||||||||||||||||||||||||||||

| Distributions from partnership | — | — | — | — | — | — | — | (374) | (374) | ||||||||||||||||||||||||||||||||||||||||||||

| Shares redeemed to settle taxes and other | — | — | 187,409 | 2 | — | — | (587) | — | (585) | ||||||||||||||||||||||||||||||||||||||||||||

| Balance — October 1, 2022 | $ | 620,320 | $ | (3,470) | 116,386,969 | $ | 1,165 | 99 | $ | — | $ | 1,340,602 | $ | 12,607 | $ | 1,971,224 | |||||||||||||||||||||||||||||||||||||

See notes to unaudited consolidated financial statements.

6

SUMMIT MATERIALS, INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in tables in thousands, except per share amounts or otherwise noted)

1.SUMMARY OF ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES

Summit Materials, Inc. (“Summit Inc.” and, together with its subsidiaries, “Summit,” “we,” “us,” “our” or the “Company”) is a vertically-integrated construction materials company. The Company is engaged in the production and sale of aggregates, cement, ready-mix concrete, asphalt paving mix and concrete products and owns and operates quarries, sand and gravel pits, two cement plants, cement distribution terminals, ready-mix concrete plants, asphalt plants and landfill sites. It is also engaged in paving and related services. The Company’s three operating and reporting segments are the West, East and Cement segments.

Substantially all of the Company’s construction materials, products and services are produced, consumed and performed outdoors, primarily in the spring, summer and fall. Seasonal changes and other weather-related conditions can affect the production and sales volumes of its products and delivery of services. Therefore, the financial results for any interim period are typically not indicative of the results expected for the full year. Furthermore, the Company’s sales and earnings are sensitive to national, regional and local economic conditions, weather conditions and to cyclical changes in construction spending, among other factors.

Summit Inc. is a holding corporation operating and controlling all of the business and affairs of Summit Materials Holdings L.P. (“Summit Holdings”) and its subsidiaries, and through Summit Holdings conducts its business. Summit Inc. owns the majority of the partnership interests of Summit Holdings (see Note 9, Stockholders’ Equity). Summit Materials, LLC (“Summit LLC”), an indirect wholly owned subsidiary of Summit Holdings, conducts the majority of our operations. Summit Materials Finance Corp. (“Summit Finance”), an indirect wholly owned subsidiary of Summit LLC, has jointly issued our Senior Notes as described below.

Basis of Presentation—These unaudited consolidated financial statements were prepared in accordance with U.S. generally accepted accounting principles (“U.S. GAAP”) for interim financial information, without audit, pursuant to the rules and regulations of the Securities and Exchange Commission (“SEC”). Certain information and footnote disclosures typically included in financial statements prepared in accordance with U.S. GAAP have been condensed or omitted pursuant to such rules and regulations. These unaudited consolidated financial statements should be read in conjunction with the Company's audited consolidated financial statements and the notes thereto as of and for the year ended December 31, 2022. The Company continues to follow the accounting policies set forth in those audited consolidated financial statements.

Management believes that these consolidated interim financial statements include all adjustments, normal and recurring in nature, that are necessary to present fairly the financial position of the Company as of September 30, 2023, the results of operations for the three and nine months ended September 30, 2023 and October 1, 2022 and cash flows for the nine months ended September 30, 2023 and October 1, 2022.

Principles of Consolidation—The consolidated financial statements include the accounts of Summit Inc. and its majority owned subsidiaries. All intercompany balances and transactions have been eliminated.

For a summary of the changes in Summit Inc.’s ownership of Summit Holdings, see Note 9, Stockholders’ Equity.

Use of Estimates—Preparation of these consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions. These estimates and the underlying assumptions affect the amounts of assets and liabilities reported, disclosures about contingent assets and liabilities and reported amounts of revenue and expenses. Such estimates include the valuation of accounts receivable, inventories, valuation of deferred tax assets, goodwill, intangibles and other long-lived assets, tax receivable agreement ("TRA") liability, pension and other postretirement obligations and asset retirement obligations. Estimates also include revenue earned on contracts and costs to complete contracts. Most of the Company’s paving and related services are performed under fixed unit-price contracts with state and local governmental entities. Management regularly evaluates its estimates and assumptions based on historical experience and other factors, including the current economic environment. As future events and their effects cannot be determined with precision, actual results can differ significantly from estimates made. Changes in estimates, including

7

those resulting from continuing changes in the economic environment, are reflected in the Company’s consolidated financial statements when the change in estimate occurs.

Business and Credit Concentrations—The Company’s operations are conducted primarily across 21 U.S. states and in British Columbia, Canada, with the most significant revenue generated in Texas, Utah, Kansas and Missouri. The Company’s accounts receivable consist primarily of amounts due from customers within these areas. Therefore, collection of these accounts is dependent on the economic conditions in the aforementioned states, as well as specific situations affecting individual customers. Credit granted within the Company’s trade areas has been granted to many customers, and management does not believe that a significant concentration of credit exists with respect to any individual customer or group of customers. No single customer accounted for more than 10% of the Company’s total revenue in the three and nine months ended September 30, 2023 or October 1, 2022.

Revenue Recognition—We earn revenue from the sale of products, which primarily include aggregates, cement, ready-mix concrete and asphalt, but also include concrete products and plastics components, and from the provision of services, which are primarily paving and related services, but also include landfill operations, the receipt and disposal of waste that is converted to fuel for use in our cement plants.

Products: Revenue for product sales is recognized when the performance obligation is satisfied, which generally is when the product is shipped.

Services: We earn revenue from the provision of services, which are primarily paving and related services, which are typically calculated using monthly progress based on a method similar to percentage of completion or a customer’s engineer review of progress.

The majority of our construction service contracts are completed within one year, but may occasionally extend beyond this time frame. The majority of our construction service contracts are for work that occurs mostly during the spring, summer and fall. We generally measure progress toward completion on long-term paving and related services contracts based on the proportion of costs incurred to date relative to total estimated costs at completion.

Estimating costs to be incurred for revenue recognition involves the use of various estimating techniques to project costs at completion, and in some cases includes estimates of recoveries asserted against the customer for changes in specifications or other disputes.

Earnings per Share—The Company computes basic earnings per share attributable to stockholders by dividing income attributable to Summit Inc. by the weighted-average shares of Class A common stock outstanding. Diluted earnings per share reflects the potential dilution beyond shares for basic earnings per share that could occur if securities or other contracts to issue common stock were exercised, converted into common stock, or resulted in the issuance of common stock that would have shared in the Company’s earnings. Since the Class B common stock has no economic value, those shares are not included in the weighted-average common share amount for basic or diluted earnings per share. In addition, as the shares of Class A common stock are issued by Summit Inc., the earnings and equity interests of noncontrolling interests are not included in basic earnings per share.

Prior Year Reclassifications — We have reclassified transaction costs of $0.7 million and $2.6 million for the three and nine months ended October 1, 2022, respectively, from general and administrative expenses to a separate line item included in operating income to conform to the current year presentation.

2.ACQUISITIONS, DISPOSITIONS, GOODWILL AND INTANGIBLES

The financial results of each acquisition have been included in the Company’s consolidated results of operations beginning on the respective closing dates of the acquisitions. The Company measures all assets acquired and liabilities assumed at their acquisition-date fair value. Goodwill acquired during a business combination has an indefinite life and is not amortized.

The following table summarizes the Company’s acquisitions by region and period:

| Nine months ended | Year ended | ||||||||||

| September 30, 2023 | December 31, 2022 | ||||||||||

| West | 3 | — | |||||||||

| East | 1 | 2 | |||||||||

8

The purchase price allocation, primarily the valuation of property, plant and equipment for the acquisitions completed during the nine months ended September 30, 2023, as well as the acquisitions completed during 2022 that occurred after October 1, 2022, have not yet been finalized due to the recent timing of the acquisitions, status of the valuation of property, plant and equipment and finalization of related tax returns. The following table summarizes aggregated information regarding the fair values of the assets acquired and liabilities assumed as of the respective acquisition dates:

| Nine months ended | Year ended | ||||||||||

| September 30, 2023 | December 31, 2022 | ||||||||||

| Financial assets | $ | 12,747 | $ | 297 | |||||||

| Inventories | 6,694 | 161 | |||||||||

| Property, plant and equipment | 124,051 | 30,041 | |||||||||

| Other assets | 1,550 | 1,116 | |||||||||

| Financial liabilities | (11,973) | (1,120) | |||||||||

| Other long-term liabilities | (768) | (1,589) | |||||||||

| Net assets acquired | 132,301 | 28,906 | |||||||||

| Goodwill | 108,803 | — | |||||||||

| Purchase price | 241,104 | 28,906 | |||||||||

| Acquisition-related liabilities | — | (6,176) | |||||||||

| Other | (1,596) | — | |||||||||

| Net cash paid for acquisitions | $ | 239,508 | $ | 22,730 | |||||||

Changes in the carrying amount of goodwill, by reportable segment, from December 31, 2022 to September 30, 2023 are summarized as follows:

| West | East | Cement | Total | ||||||||||||||||||||

| Balance—December 31, 2022 | $ | 566,389 | $ | 361,501 | $ | 204,656 | $ | 1,132,546 | |||||||||||||||

| Acquisitions (1) | 108,803 | — | — | 108,803 | |||||||||||||||||||

| Foreign currency translation adjustments | 123 | — | — | 123 | |||||||||||||||||||

| Balance—September 30, 2023 | $ | 675,315 | $ | 361,501 | $ | 204,656 | $ | 1,241,472 | |||||||||||||||

_______________________________________________________________________

(1) Reflects goodwill from 2023 acquisitions.

The Company’s intangible assets subject to amortization are primarily composed of operating permits, mineral lease agreements and reserve rights. Operating permits relate to permitting and zoning rights acquired outside of a business combination. The assets related to mineral lease agreements reflect the submarket royalty rates paid under agreements, primarily for extracting aggregates. The values were determined as of the respective acquisition dates by a comparison of market-royalty rates. The reserve rights relate to aggregate reserves to which the Company has certain rights of ownership, but does not own the reserves. The intangible assets are amortized on a straight-line basis over the lives of the leases or permits. The following table shows intangible assets by type and in total:

| September 30, 2023 | December 31, 2022 | ||||||||||||||||||||||||||||||||||

| Gross Carrying Amount | Accumulated Amortization | Net Carrying Amount | Gross Carrying Amount | Accumulated Amortization | Net Carrying Amount | ||||||||||||||||||||||||||||||

| Operating permits | $ | 38,677 | $ | (5,291) | $ | 33,386 | $ | 38,677 | $ | (4,109) | $ | 34,568 | |||||||||||||||||||||||

| Mineral leases | 17,778 | (7,452) | 10,326 | 18,091 | (7,056) | 11,035 | |||||||||||||||||||||||||||||

| Reserve rights | 25,586 | (4,814) | 20,772 | 25,242 | (3,872) | 21,370 | |||||||||||||||||||||||||||||

| Other | 4,888 | (558) | 4,330 | 4,877 | (466) | 4,411 | |||||||||||||||||||||||||||||

| Total intangible assets | $ | 86,929 | $ | (18,115) | $ | 68,814 | $ | 86,887 | $ | (15,503) | $ | 71,384 | |||||||||||||||||||||||

Amortization expense totaled $0.8 million and $2.6 million for the three and nine months ended September 30, 2023, respectively, and $0.8 million and $2.6 million for the three and nine months ended October 1, 2022, respectively. The estimated amortization expense for the intangible assets for each of the five years subsequent to September 30, 2023 is as follows:

9

| 2023 (three months) | $ | 1,001 | |||

| 2024 | 4,011 | ||||

| 2025 | 3,969 | ||||

| 2026 | 3,920 | ||||

| 2027 | 3,908 | ||||

| 2028 | 3,910 | ||||

| Thereafter | 48,095 | ||||

| Total | $ | 68,814 | |||

In September 2023, the Company entered into a definitive agreement to acquire all of the outstanding equity interests of Argos North America Corp. (“Argos USA”) in a cash and stock transaction valued at $3.2 billion. Argos USA is among the largest cement producers with four integrated cement plants and approximately 140 ready-mix plants in the Southeast, Mid-Atlantic and Texas geographies. Under the terms of the agreement, the shareholders of Argos USA will receive approximately $1.2 billion in cash subject to closing adjustments and approximately 54.7 million shares of the Company's Class A common stock. In connection with the agreement, the Company has obtained committed financing in the form of a $1.3 billion 364-day term loan bridge facility to finance the cash consideration to be paid to the shareholders of Argos USA. The Company expects to enter into permanent financing agreements prior to the transaction closing, which would reduce any amounts that may ultimately be borrowed under the term loan bridge facility. The transaction closing is expected to occur prior to the end of the first quarter of 2024, subject to customary closing conditions, including regulatory approvals and approval by the Company's stockholders.

3.REVENUE RECOGNITION

We derive our revenue predominantly by selling construction materials, products and providing paving and related services. Construction materials consist of aggregates and cement. Products consist of related downstream products, including ready-mix concrete, asphalt paving mix and concrete products. Paving and related service revenue is generated primarily from the asphalt paving services that we provide.

Revenue by product for the three and nine months ended September 30, 2023 and October 1, 2022 is as follows:

| Three months ended | Nine months ended | ||||||||||||||||||||||

| September 30, 2023 | October 1, 2022 | September 30, 2023 | October 1, 2022 | ||||||||||||||||||||

| Revenue by product*: | |||||||||||||||||||||||

| Aggregates | $ | 179,819 | $ | 163,524 | $ | 505,984 | $ | 448,397 | |||||||||||||||

| Cement | 115,135 | 112,489 | 267,755 | 241,858 | |||||||||||||||||||

| Ready-mix concrete | 213,325 | 189,081 | 551,673 | 530,001 | |||||||||||||||||||

| Asphalt | 117,896 | 106,804 | 236,340 | 218,083 | |||||||||||||||||||

| Paving and related services | 110,370 | 120,327 | 226,928 | 249,547 | |||||||||||||||||||

| Other | 58,252 | 60,522 | 170,655 | 172,362 | |||||||||||||||||||

| Total revenue | $ | 794,797 | $ | 752,747 | $ | 1,959,335 | $ | 1,860,248 | |||||||||||||||

*Revenue from liquid asphalt terminals is included in asphalt revenue.

Accounts receivable, net consisted of the following as of September 30, 2023 and December 31, 2022:

| September 30, 2023 | December 31, 2022 | ||||||||||

| Trade accounts receivable | $ | 305,436 | $ | 215,766 | |||||||

| Construction contract receivables | 64,438 | 37,067 | |||||||||

| Retention receivables | 13,165 | 11,048 | |||||||||

| Accounts receivable | 383,039 | 263,881 | |||||||||

| Less: Allowance for doubtful accounts | (7,110) | (7,212) | |||||||||

| Accounts receivable, net | $ | 375,929 | $ | 256,669 | |||||||

Retention receivables are amounts earned by the Company but held by customers until paving and related service contracts and projects are near completion or fully completed. Amounts are generally billed and collected within one year.

4.INVENTORIES

10

Inventories consisted of the following as of September 30, 2023 and December 31, 2022:

| September 30, 2023 | December 31, 2022 | ||||||||||

| Aggregate stockpiles | $ | 165,071 | $ | 148,347 | |||||||

| Finished goods | 43,316 | 33,622 | |||||||||

| Work in process | 11,220 | 8,191 | |||||||||

| Raw materials | 23,529 | 22,331 | |||||||||

| Total | $ | 243,136 | $ | 212,491 | |||||||

5.ACCRUED EXPENSES

Accrued expenses consisted of the following as of September 30, 2023 and December 31, 2022:

| September 30, 2023 | December 31, 2022 | ||||||||||

| Interest | $ | 10,677 | $ | 24,625 | |||||||

| Payroll and benefits | 48,595 | 34,485 | |||||||||

| Finance lease obligations | 3,399 | 6,959 | |||||||||

| Insurance | 23,874 | 18,127 | |||||||||

| Current portion of TRA liability and non-income taxes | 14,349 | 4,360 | |||||||||

| Deferred asset purchase payments | 5,892 | 5,131 | |||||||||

| Professional fees | 11,980 | 924 | |||||||||

| Other (1) | 28,853 | 25,356 | |||||||||

| Total | $ | 147,619 | $ | 119,967 | |||||||

(1)Consists primarily of current portion of asset retirement obligations and miscellaneous accruals.

6.DEBT

Debt consisted of the following as of September 30, 2023 and December 31, 2022:

| September 30, 2023 | December 31, 2022 | ||||||||||

| Term Loan, due 2027: | |||||||||||

$505.7 million and $509.6 million, net of $4.2 million and $5.0 million discount at September 30, 2023 and December 31, 2022, respectively | $ | 501,492 | $ | 504,549 | |||||||

61⁄2% Senior Notes, due 2027 | 300,000 | 300,000 | |||||||||

51⁄4% Senior Notes, due 2029 | 700,000 | 700,000 | |||||||||

| Total | 1,501,492 | 1,504,549 | |||||||||

| Current portion of long-term debt | 3,822 | 5,096 | |||||||||

| Long-term debt | $ | 1,497,670 | $ | 1,499,453 | |||||||

The contractual payments of long-term debt, including current maturities, for the five years subsequent to September 30, 2023, are as follows:

11

| 2023 (three months) | $ | 1,274 | |||

| 2024 | 3,822 | ||||

| 2025 | 6,369 | ||||

| 2026 | 5,096 | ||||

| 2027 | 789,177 | ||||

| 2028 | — | ||||

| Thereafter | 700,000 | ||||

| Total | 1,505,738 | ||||

| Less: Original issue net discount | (4,246) | ||||

| Less: Capitalized loan costs | (9,601) | ||||

| Total debt | $ | 1,491,891 | |||

Senior Notes— On August 11, 2020, Summit LLC and Summit Finance (together, the “Issuers”) issued $700.0 million in aggregate principal amount of 5.250% senior notes due January 15, 2029 (the “2029 Notes”). The 2029 Notes were issued at 100.0% of their par value with proceeds of $690.4 million, net of related fees and expenses. The 2029 Notes were issued under an indenture dated August 11, 2020 (the "2029 Notes Indenture"). The 2029 Notes Indenture contains covenants limiting, among other things, Summit LLC and its restricted subsidiaries’ ability to incur additional indebtedness or issue certain preferred shares, pay dividends, redeem stock or make other distributions, make certain investments, sell or transfer certain assets, create liens, consolidate, merge, sell or otherwise dispose of all or substantially all of its assets, enter into certain transactions with affiliates, and designate subsidiaries as unrestricted subsidiaries. The 2029 Notes Indenture also contains customary events of default. Interest on the 2029 Notes is payable semi-annually on January 15 and July 15 of each year commencing on January 15, 2021.

On March 15, 2019, the Issuers issued $300.0 million in aggregate principal amount of 6.500% senior notes due March 15, 2027 (the “2027 Notes”). The 2027 Notes were issued at 100.0% of their par value with proceeds of $296.3 million, net of related fees and expenses. The 2027 Notes were issued under an indenture dated March 25, 2019, the terms of which are generally consistent with the 2029 Notes Indenture. Interest on the 2027 Notes is payable semi-annually on March 15 and September 15 of each year commencing on September 15, 2019.

As of September 30, 2023 and December 31, 2022, the Company was in compliance with all covenants under the applicable indentures.

Senior Secured Credit Facilities— Summit LLC has credit facilities that provide for term loans in an aggregate amount of $505.7 million and revolving credit commitments in an aggregate amount of $395.0 million (the “Senior Secured Credit Facilities”). Under the Senior Secured Credit Facilities, required principal repayments of 0.25% of the refinanced aggregate amount of term debt are due on the last business day of each March, June, September and December commencing with the March 2023 payment. The interest rate on the term loan is a variable rate, it was 8.57% as of September 30, 2023. In 2022, the Company repaid $95.6 million of its term loan under provisions related to divestitures of businesses.

On December 14, 2022, Summit Materials, LLC entered into Amendment No. 5 to the credit agreement governing the Senior Secured Credit Facilities (the “Credit Agreement”), which among other things, (a) refinanced the existing $509.6 million of existing term loans with new term loans under the Term Loan Facility bearing interest, at Summit LLC’s option, based on either the base rate or Term Secured Overnight Financing Rate ("SOFR") rate and an applicable margin of (i) 2.00% per annum with respect to base rate borrowings and a floor of 1.00% per annum or (ii) 3.00% per annum with respect to Term SOFR borrowings, with a SOFR adjustment of 0.10% per annum and a floor of zero, and (b) extended the maturity date to December 14, 2027.

On January 10, 2023, Summit Materials, LLC entered into Amendment No. 6 to the Credit Agreement, which among other things, increased the maximum amount available to $395.0 million and extended the maturity date to January 10, 2028. The revolving credit agreement bears interest per annum equal to a Term SOFR Rate with a SOFR adjustment of 0.10% per annum and a floor of zero.

There were no outstanding borrowings under the revolving credit facility as of September 30, 2023 and December 31, 2022, with borrowing capacity of $374.1 million remaining as of September 30, 2023, which is net of $20.9 million of outstanding letters of credit. The outstanding letters of credit are renewed annually and support required bonding on construction projects, large leases, workers compensation claims and the Company’s insurance liabilities.

12

Summit LLC’s Consolidated First Lien Net Leverage Ratio, as such term is defined in the Credit Agreement, should be no greater than 4.75:1.0 as of each quarter-end. As of September 30, 2023 and December 31, 2022, Summit LLC was in compliance with all financial covenants.

Summit LLC’s wholly-owned domestic subsidiary companies, subject to certain exclusions and exceptions, are named as subsidiary guarantors of the Senior Notes and the Senior Secured Credit Facilities. In addition, Summit LLC has pledged substantially all of its assets as collateral, subject to certain exclusions and exceptions, for the Senior Secured Credit Facilities.

In September 2023, in connection with our agreement to combine with Argos USA, we obtained a $1.3 billion 364-day term loan bridge facility commitment from various financial institutions. The term loan bridge facility may only be drawn to close the transaction. We expect to obtain permanent financing prior to our combination with Argos USA, at which time the term loan bridge facility commitment will expire.

The following table presents the activity for the deferred financing fees for the nine months ended September 30, 2023 and October 1, 2022:

| Deferred financing fees | |||||

| Balance—December 31, 2022 | $ | 11,489 | |||

| Loan origination fees | 1,566 | ||||

| Amortization | (1,838) | ||||

| Write off of deferred financing fees | (160) | ||||

| Balance—September 30, 2023 | $ | 11,057 | |||

| Balance—January 1, 2022 | $ | 13,049 | |||

| Amortization | (2,028) | ||||

| Balance—October 1, 2022 | $ | 11,021 | |||

Other—On January 15, 2015, the Company’s wholly-owned subsidiary in British Columbia, Canada entered into an agreement with HSBC Bank Canada, which was amended on November 30, 2020, for a (i) $6.0 million Canadian dollar (“CAD”) revolving credit commitment to be used for operating activities that bears interest per annum equal to the bank’s prime rate plus 0.20%, (ii) $0.5 million CAD revolving credit commitment to be used for capital equipment that bears interest per annum at the bank’s prime rate plus 0.20% and (iii) $1.5 million CAD revolving credit commitment to provide guarantees on behalf of that subsidiary and (iv) $10.0 million CAD revolving foreign exchange facility available to purchase foreign exchange forward contracts. There were no amounts outstanding under this agreement as of September 30, 2023 or December 31, 2022, which may be terminated upon demand.

7.INCOME TAXES

Summit Inc.’s tax provision includes its proportional share of Summit Holdings’ tax attributes. Summit Holdings’ subsidiaries are primarily limited liability companies but do include certain entities organized as C corporations and a Canadian subsidiary. The tax attributes related to the limited liability companies are passed on to Summit Holdings and then to its partners, including Summit Inc. The tax attributes associated with the C corporation and Canadian subsidiaries are fully reflected in the Company’s accounts.

Our income tax expense was $23.9 million and $39.9 million in the three and nine months ended September 30, 2023, respectively, and our income tax expense was $24.8 million and $74.0 million in the three and nine months ended October 1, 2022, respectively. The effective tax rate for Summit Inc. differs from the federal statutory tax rate primarily due to (1) the non-taxability of the tax receivable agreement benefit (2) tax depletion expense in excess of the expense recorded under U.S. GAAP, (3) basis differences in assets divested, (4) state taxes, (5) the minority interest in the Summit Holdings partnership that is allocated outside of the Company and (6) various other items such as limitations on meals and entertainment, certain stock compensation and other costs.

As of September 30, 2023 and December 31, 2022, Summit Inc. had a valuation allowance of $1.1 million in both periods, which relates to certain deferred tax assets in taxable entities where realization is not more likely than not.

13

No material interest or penalties were recognized in income tax expense during the three and nine months ended September 30, 2023 and October 1, 2022.

Tax Receivable Agreement—The Company is party to a TRA with certain current and former holders of LP Units that provides for the payment by Summit Inc. to exchanging holders of LP Units of 85% of the benefits, if any, that Summit Inc. actually realizes (or, under certain circumstances such as an early termination of the TRA, is deemed to realize) as a result of increases in the tax basis of tangible and intangible assets of Summit Holdings and certain other tax benefits related to entering into the TRA, including tax benefits attributable to payments under the TRA.

In the third quarter of 2023, Summit LLC reached an agreement to acquire all of the rights and interests in the TRA from affiliates of Blackstone Inc. and certain other TRA holders for cash consideration of $122.9 million. In connection with these transactions, Summit LLC and Summit Inc. reached an agreement whereby the maximum amount Summit Inc. is obligated to pay Summit LLC for the TRA interests acquired is limited to the amount Summit LLC paid for the TRA interests. As the cash paid for TRA interests acquired was less than their carrying value, Summit Inc. recognized a tax receivable agreement benefit of $153.1 million in the accompanying consolidated statement of operations.

In the nine months ended September 30, 2023, 176,258 LP Units were acquired by Summit Inc. in exchange for an equal number of newly-issued shares of Summit Inc.’s Class A common stock. Subsequent to quarter end, an additional 345,554 LP units were exchanged for an equal amount of newly issued shares of Summit Inc.'s Class A common stock, and Summit LLC. Summit LLC then acquired the interest in the TRA interests from certain of those holders for aggregate cash consideration of $9.5 million, resulting in further reduction of the TRA liability of approximately $19.3 million.

Changes in the balance of the TRA liability, from December 31, 2022 to September 30, 2023 are summarized as follows:

| TRA Liability | |||||

| Balance — December 31, 2022 | $ | 328,356 | |||

| LP unit exchanges during period | 1,146 | ||||

| Purchase of TRA interests | (122,935) | ||||

| TRA liability reduction | (153,080) | ||||

| TRA liability payments | (544) | ||||

| Total | 52,943 | ||||

| Less current portion | 800 | ||||

| Balance — September 30, 2023 | $ | 52,143 | |||

Tax Distributions – The holders of Summit Holdings’ LP Units, including Summit Inc., incur U.S. federal, state and local income taxes on their share of any taxable income of Summit Holdings. The limited partnership agreement of Summit Holdings provides for pro rata cash distributions (“tax distributions”) to the holders of the LP Units in an amount generally calculated to provide each holder of LP Units with sufficient cash to cover its tax liability in respect of the LP Units. In general, these tax distributions are computed based on Summit Holdings’ estimated taxable income allocated to Summit Inc. multiplied by an assumed tax rate equal to the highest effective marginal combined U.S. federal, state and local income tax rate in New York, New York. In the nine months ended September 30, 2023, Summit Holdings paid tax distributions of approximately $4.5 million, of which $0.1 million was paid to holders of its LP Units not owned by Summit Inc. In the nine months ended October 1, 2022, Summit Holdings made a tax distribution of approximately $34.2 million, of which $0.4 million went to LP units not owned by Summit Inc.

8.EARNINGS PER SHARE

Basic earnings per share is computed by dividing net earnings by the weighted average common shares outstanding and diluted net earnings is computed by dividing net earnings, adjusted for changes in the earnings allocated to Summit Inc. as a result of the assumed conversion of LP Units, by the weighted-average common shares outstanding assuming dilution.

The following table shows the calculation of basic and diluted earnings per share:

14

| Three months ended | Nine months ended | ||||||||||||||||||||||

| September 30, 2023 | October 1, 2022 | September 30, 2023 | October 1, 2022 | ||||||||||||||||||||

| Net income attributable to Summit Inc. | $ | 230,045 | $ | 86,489 | $ | 282,878 | $ | 242,310 | |||||||||||||||

| Weighted average shares of Class A stock outstanding | 118,928,799 | 119,753,806 | 118,780,523 | 120,196,211 | |||||||||||||||||||

| Add: Nonvested restricted stock awards of retirement eligible shares | 84,532 | 142,466 | 94,444 | 148,804 | |||||||||||||||||||

| Weighted average shares outstanding | 119,013,331 | 119,896,272 | 118,874,967 | 120,345,015 | |||||||||||||||||||

| Basic earnings per share | $ | 1.93 | $ | 0.72 | $ | 2.38 | $ | 2.01 | |||||||||||||||

| Diluted net income attributable to Summit Inc. | $ | 230,045 | $ | 86,489 | $ | 282,878 | $ | 242,310 | |||||||||||||||

| Weighted average shares outstanding | 119,013,331 | 119,896,272 | 118,874,967 | 120,345,015 | |||||||||||||||||||

| Add: stock options | 122,753 | 78,799 | 108,024 | 93,993 | |||||||||||||||||||

| Add: warrants | 15,578 | 10,790 | 13,943 | 12,202 | |||||||||||||||||||

| Add: restricted stock units | 356,286 | 279,684 | 376,221 | 485,174 | |||||||||||||||||||

| Add: performance stock units | 217,745 | 117,767 | 185,819 | 141,766 | |||||||||||||||||||

| Weighted average dilutive shares outstanding | 119,725,693 | 120,383,312 | 119,558,974 | 121,078,150 | |||||||||||||||||||

| Diluted earnings per share | $ | 1.92 | $ | 0.72 | $ | 2.37 | $ | 2.00 | |||||||||||||||

Excluded from the above calculations were the shares noted below as they were antidilutive:

| Three months ended | Nine months ended | ||||||||||||||||||||||

| September 30, 2023 | October 1, 2022 | September 30, 2023 | October 1, 2022 | ||||||||||||||||||||

| Antidilutive shares: | |||||||||||||||||||||||

| LP Units | 1,303,990 | 1,312,795 | 1,308,417 | 1,313,601 | |||||||||||||||||||

9.STOCKHOLDERS’ EQUITY

During 2023, certain limited partners of Summit Holdings exchanged their LP Units for shares of Class A common stock of Summit Inc. Subsequent to September 30, 2023, an additional 345,554 LP units were exchanged for shares of Class A common stock.

In March 2022, our Board of Directors authorized a share repurchase program, whereby we can repurchase up to $250 million of our Class A common stock. As of September 30, 2023, there was $149.0 million available for purchase, upon which they will be retired.

The following table summarizes the changes in our ownership of Summit Holdings:

| Summit Inc. Shares (Class A) | LP Units | Total | Summit Inc. Ownership Percentage | ||||||||||||||||||||

| Balance — December 31, 2022 | 118,408,655 | 1,312,004 | 119,720,659 | 98.9 | % | ||||||||||||||||||

| Exchanges during period | 176,258 | (176,258) | — | ||||||||||||||||||||

| Stock option exercises | 5,407 | — | 5,407 | ||||||||||||||||||||

| Other equity transactions | 522,630 | — | 522,630 | ||||||||||||||||||||

| Balance — September 30, 2023 | 119,112,950 | 1,135,746 | 120,248,696 | 99.1 | % | ||||||||||||||||||

| Balance — January 1, 2022 | 120,684,322 | 1,314,006 | 121,998,328 | 98.9 | % | ||||||||||||||||||

| Exchanges during period | 2,000 | (2,000) | — | ||||||||||||||||||||

| Stock option exercises | 10,098 | — | 10,098 | ||||||||||||||||||||

| Repurchases of common stock | (3,427,510) | — | (3,427,510) | ||||||||||||||||||||

| Other equity transactions | 1,097,273 | — | 1,097,273 | ||||||||||||||||||||

| Balance — October 1, 2022 | 118,366,183 | 1,312,006 | 119,678,189 | 98.9 | % | ||||||||||||||||||

15

Summit Inc. is Summit Holdings’ primary beneficiary and thus consolidates Summit Holdings in its consolidated financial statements with a corresponding noncontrolling interest reclassification, which was 0.9% and 1.1% as of September 30, 2023 and December 31, 2022, respectively.

Accumulated other comprehensive income (loss) —The changes in each component of accumulated other comprehensive income (loss) consisted of the following:

| Change in retirement plans | Foreign currency translation adjustments | Accumulated other comprehensive income (loss) | |||||||||||||||

| Balance — December 31, 2022 | $ | 6,356 | $ | (3,272) | $ | 3,084 | |||||||||||

| Foreign currency translation adjustment, net of tax | — | 212 | 212 | ||||||||||||||

| Balance — September 30, 2023 | $ | 6,356 | $ | (3,060) | $ | 3,296 | |||||||||||

| Balance — January 1, 2022 | $ | 1,508 | $ | 5,575 | $ | 7,083 | |||||||||||

| Foreign currency translation adjustment, net of tax | — | (10,553) | (10,553) | ||||||||||||||

| Balance — October 1, 2022 | $ | 1,508 | $ | (4,978) | $ | (3,470) | |||||||||||

10.SUPPLEMENTAL CASH FLOW INFORMATION

Supplemental cash flow information is as follows:

| Nine months ended | |||||||||||

| September 30, 2023 | October 1, 2022 | ||||||||||

| Cash payments: | |||||||||||

| Interest | $ | 88,400 | $ | 70,184 | |||||||

| Payments for income taxes, net | 13,602 | 15,888 | |||||||||

| Operating cash payments on operating leases | 7,578 | 7,112 | |||||||||

| Operating cash payments on finance leases | 400 | 890 | |||||||||

| Finance cash payments on finance leases | 6,137 | 13,465 | |||||||||

| Non cash investing and financing activities: | |||||||||||

| Accrued liabilities for purchases of property, plant and equipment | $ | 22,244 | $ | 16,778 | |||||||

| Right of use assets obtained in exchange for operating lease obligations | 6,371 | 13,302 | |||||||||

| Right of use assets obtained in exchange for finance leases obligations | 413 | 258 | |||||||||

| Exchange of LP Units to shares of Class A common stock | 5,527 | 62 | |||||||||

16

11.LEASES

We lease construction and office equipment, distribution facilities and office space. Leases with an initial term of 12 months or less, including month to month leases, are not recorded on the balance sheet. Lease expense for short-term leases is recognized on a straight line basis over the lease term. For lease agreements we have entered into or reassessed, we combine lease and nonlease components. While we also own mineral leases for mining operations, those leases are outside the scope of Accounting Standards Update No. 2016-2, Leases (Topic 842). Assets acquired under finance leases are included in property, plant and equipment.

Many of our leases include options to purchase the leased equipment. The depreciable life of assets and leasehold improvements are limited by the expected lease term, unless there is a transfer of title or purchase option reasonably certain of exercise. Our lease agreements do not contain any material residual value guarantees or material restrictive covenants. The components of lease expense were as follows:

17

| Three months ended | Nine months ended | ||||||||||||||||||||||

| September 30, 2023 | October 1, 2022 | September 30, 2023 | October 1, 2022 | ||||||||||||||||||||

| Operating lease cost | $ | 2,903 | $ | 2,398 | $ | 8,241 | $ | 7,181 | |||||||||||||||

| Variable lease cost | 39 | 70 | 103 | 225 | |||||||||||||||||||

| Short-term lease cost | 13,238 | 11,916 | 30,692 | 31,097 | |||||||||||||||||||

| Financing lease cost: | |||||||||||||||||||||||

| Amortization of right-of-use assets | 483 | 1,235 | 2,015 | 4,598 | |||||||||||||||||||

| Interest on lease liabilities | 118 | 239 | 399 | 879 | |||||||||||||||||||

| Total lease cost | $ | 16,781 | $ | 15,858 | $ | 41,450 | $ | 43,980 | |||||||||||||||

| September 30, 2023 | December 31, 2022 | ||||||||||||||||||||||

| Supplemental balance sheet information related to leases: | |||||||||||||||||||||||

| Operating leases: | |||||||||||||||||||||||

| Operating lease right-of-use assets | $ | 38,380 | $ | 37,889 | |||||||||||||||||||

| Current operating lease liabilities | $ | 8,745 | $ | 7,296 | |||||||||||||||||||

| Noncurrent operating lease liabilities | 34,838 | 35,737 | |||||||||||||||||||||

| Total operating lease liabilities | $ | 43,583 | $ | 43,033 | |||||||||||||||||||

| Finance leases: | |||||||||||||||||||||||

| Property and equipment, gross | $ | 20,030 | $ | 32,119 | |||||||||||||||||||

| Less accumulated depreciation | (9,893) | (14,992) | |||||||||||||||||||||

| $ | 10,137 | $ | 17,127 | ||||||||||||||||||||

| $ | 3,399 | $ | 6,959 | ||||||||||||||||||||

| 5,180 | 7,167 | ||||||||||||||||||||||

| Total finance lease liabilities | $ | 8,579 | $ | 14,126 | |||||||||||||||||||

| Weighted average remaining lease term (years): | |||||||||||||||||||||||

| Operating leases | 8.4 | 9.1 | |||||||||||||||||||||

| Finance lease | 3.4 | 2.8 | |||||||||||||||||||||

| Weighted average discount rate: | |||||||||||||||||||||||

| Operating leases | 5.1 | % | 4.7 | % | |||||||||||||||||||

| Finance leases | 5.9 | % | 5.3 | % | |||||||||||||||||||

Maturities of lease liabilities, as of September 30, 2023, were as follows: | |||||||||||||||||||||||

| Operating Leases | Finance Leases | ||||||||||||||||||||||

| 2023 (three months) | $ | 2,739 | $ | 1,283 | |||||||||||||||||||

| 2024 | 10,294 | 3,052 | |||||||||||||||||||||

| 2025 | 8,165 | 2,435 | |||||||||||||||||||||

| 2026 | 6,414 | 990 | |||||||||||||||||||||

| 2027 | 4,760 | 760 | |||||||||||||||||||||

| 2028 | 3,450 | 513 | |||||||||||||||||||||

| Thereafter | 17,600 | 570 | |||||||||||||||||||||

| Total lease payments | 53,422 | 9,603 | |||||||||||||||||||||

| Less imputed interest | (9,839) | (1,024) | |||||||||||||||||||||

| Present value of lease payments | $ | 43,583 | $ | 8,579 | |||||||||||||||||||

12.COMMITMENTS AND CONTINGENCIES

The Company is party to certain legal actions arising from the ordinary course of business activities. Accruals are recorded when the outcome is probable and can be reasonably estimated. While the ultimate results of claims and litigation cannot be predicted with certainty, management expects that the ultimate resolution of all current pending or threatened claims and

18

litigation will not have a material effect on the Company’s consolidated financial position, results of operations or liquidity. The Company records legal fees as incurred.

In March 2018, we were notified of an investigation by the Canadian Competition Bureau (the “CCB”) into pricing practices by certain asphalt paving contractors in British Columbia, including Winvan Paving, Ltd. (“Winvan”). We believe the investigation is focused on time periods prior to our April 2017 acquisition of Winvan and we are cooperating with the CCB. Although we currently do not believe this matter will have a material adverse effect on our business, financial condition or results of operations, we are currently not able to predict the ultimate outcome or cost of the investigation.

Environmental Remediation and Site Restoration —The Company’s operations are subject to and affected by federal, state, provincial and local laws and regulations relating to the environment, health and safety and other regulatory matters. These operations require environmental operating permits, which are subject to modification, renewal and revocation. The Company regularly monitors and reviews its operations, procedures and policies for compliance with these laws and regulations. Despite these compliance efforts, risk of environmental liability is inherent in the operation of the Company’s business, as it is with other companies engaged in similar businesses and there can be no assurance that environmental liabilities or noncompliance will not have a material adverse effect on the Company’s consolidated financial condition, results of operations or liquidity.