UNITED STATES STEEL CORP - Annual Report: 2016 (Form 10-K)

2016

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended December 31, 2016

Commission file number 1-16811

(Exact name of registrant as specified in its charter)

Delaware | 25-1897152 | |

(State of Incorporation) | (I.R.S. Employer Identification No.) | |

600 Grant Street, Pittsburgh, PA 15219-2800

(Address of principal executive offices)

Tel. No. (412) 433-1121

Securities registered pursuant to Section 12 (b) of the Act:

Title of Each Class | Name of Exchange on which Registered | |

United States Steel Corporation Common Stock, par value $1.00 | New York Stock Exchange, Chicago Stock Exchange | |

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes þ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months and (2) has been subject to such filing requirements for at least the past 90 days. Yes þ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer þ | Accelerated filer | |

Non-accelerated filer (Do not check if a smaller reporting company) | Smaller reporting company | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes No þ

Aggregate market value of Common Stock held by non-affiliates as of June 28, 2016 (the last business day of the registrant’s most recently completed second fiscal quarter): $2.5 billion. The amount shown is based on the closing price of the registrant’s Common Stock on the New York Stock Exchange composite tape on that date. Shares of Common Stock held by executive officers and directors of the registrant are not included in the computation. However, the registrant has made no determination that such individuals are “affiliates” within the meaning of Rule 405 under the Securities Act of 1933.

There were 174,290,761 shares of United States Steel Corporation Common Stock outstanding as of February 23, 2017.

Documents Incorporated By Reference:

Portions of the Proxy Statement for the 2017 Annual Meeting of Stockholders are incorporated into Part III.

INDEX

Item 1. | |||

Item 1A | |||

Item 1B | |||

Item 2. | |||

Item 3. | |||

Item 4. | |||

Item 5. | |||

Item 6. | |||

Item 7. | |||

Item 7A | |||

Item 8. | |||

Item 9. | |||

Item 9A | |||

Item 9B | |||

Item 10. | |||

Item 11. | |||

Item 12. | |||

Item 13. | |||

Item 14. | |||

Item 15. | |||

Item 16. | |||

TOTAL NUMBER OF PAGES | 110 | ||

FORWARD-LOOKING STATEMENTS

This report contains information that may constitute “forward-looking statements” within the meaning of Section 27 of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. We intend the forward-looking statements to be covered by the safe harbor provisions for forward-looking statements in those sections. Generally, we have identified such forward-looking statements by using the words “believe,” “expect,” “intend,” “estimate,” “anticipate,” “project,” “target,” “forecast,” “aim,” “will” and similar expressions or by using future dates in connection with any discussion of, among other things, operating performance, trends, events or developments that we expect or anticipate will occur in the future, statements relating to volume growth, share of sales and earnings per share growth, and statements expressing general views about future operating results. However, the absence of these words or similar expressions does not mean that a statement is not forward-looking. Forward-looking statements are not historical facts, but instead represent only the Company’s beliefs regarding future events, many of which, by their nature, are inherently uncertain and outside of the Company’s control. It is possible that the Company’s actual results and financial condition may differ, possibly materially, from the anticipated results and financial condition indicated in these forward-looking statements. Management believes that these forward-looking statements are reasonable as of the time made. However, caution should be taken not to place undue reliance on any such forward-looking statements because such statements speak only as of the date when made. Our Company undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law. In addition, forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from our Company's historical experience and our present expectations or projections. These risks and uncertainties include, but are not limited to the risks and uncertainties described in this report in “Item 1A. Risk Factors” and those described from time to time in our future reports filed with the Securities and Exchange Commission.

References in this Annual Report on Form 10-K to "U. S. Steel," "the Company," "we," "us," and "our" refer to United States Steel Corporation and its consolidated subsidiaries unless otherwise indicated by the context.

Non-Generally Accepted Accounting Policies (non-GAAP)

This report contains certain non-GAAP financial measures such as earnings (loss) before interest, income taxes, depreciation, depletion and amortization (EBITDA), adjusted EBITDA, adjusted net earnings (loss) and adjusted net earnings (loss) per diluted share.

We believe that EBITDA, considered along with the net earnings (loss), is a relevant indicator of trends relating to cash generating activity and provides management and investors with additional information for comparison of our operating results to the operating results of other companies.

Adjusted net earnings (loss) and adjusted net earnings (loss) per diluted share are non-GAAP measures that exclude the effects of restructuring charges, impairment charges, losses associated with U. S. Steel Canada Inc., losses on debt extinguishment, certain postemployment actuarial adjustments and charges for deferred tax asset valuation allowances that are not part of the Company's core operations. Adjusted EBITDA is also a non-GAAP measure that excludes the effects of restructuring charges, impairment charges, certain postemployment actuarial adjustments and losses associated with U. S. Steel Canada, Inc. We present adjusted net earnings (loss), adjusted net earnings (loss) per diluted share and adjusted EBITDA to enhance the understanding of our ongoing operating performance and established trends affecting our core operations, particularly cash generating activity, by excluding the effects of restructuring charges, impairment charges, losses on debt extinguishment, certain postemployment actuarial adjustments, charges for deferred tax asset valuation allowances and losses associated with non-core operations that can obscure underlying trends. U. S. Steel's management considers adjusted net earnings (loss), adjusted net earnings (loss) per diluted share and adjusted EBITDA useful to investors by facilitating a comparison of our operating performance to the operating performance of our competitors, many of which use adjusted net earnings (loss), adjusted net earnings (loss) per diluted share and adjusted EBITDA as alternative measures of operating performance. Additionally, the presentation of adjusted net earnings (loss), adjusted net earnings (loss) per diluted share and adjusted EBITDA provides insight into management's view and assessment of the Company's ongoing operating performance, because management does not consider the adjusting items when evaluating the Company's financial performance. Adjusted net earnings (loss), adjusted net earnings (loss) per diluted share and adjusted EBITDA should not be considered a substitute for net earnings (loss), earnings (loss) per diluted share or other financial measures as computed in accordance with U.S. GAAP and are not necessarily comparable to similarly titled measures used by other companies.

3

10-K SUMMARY

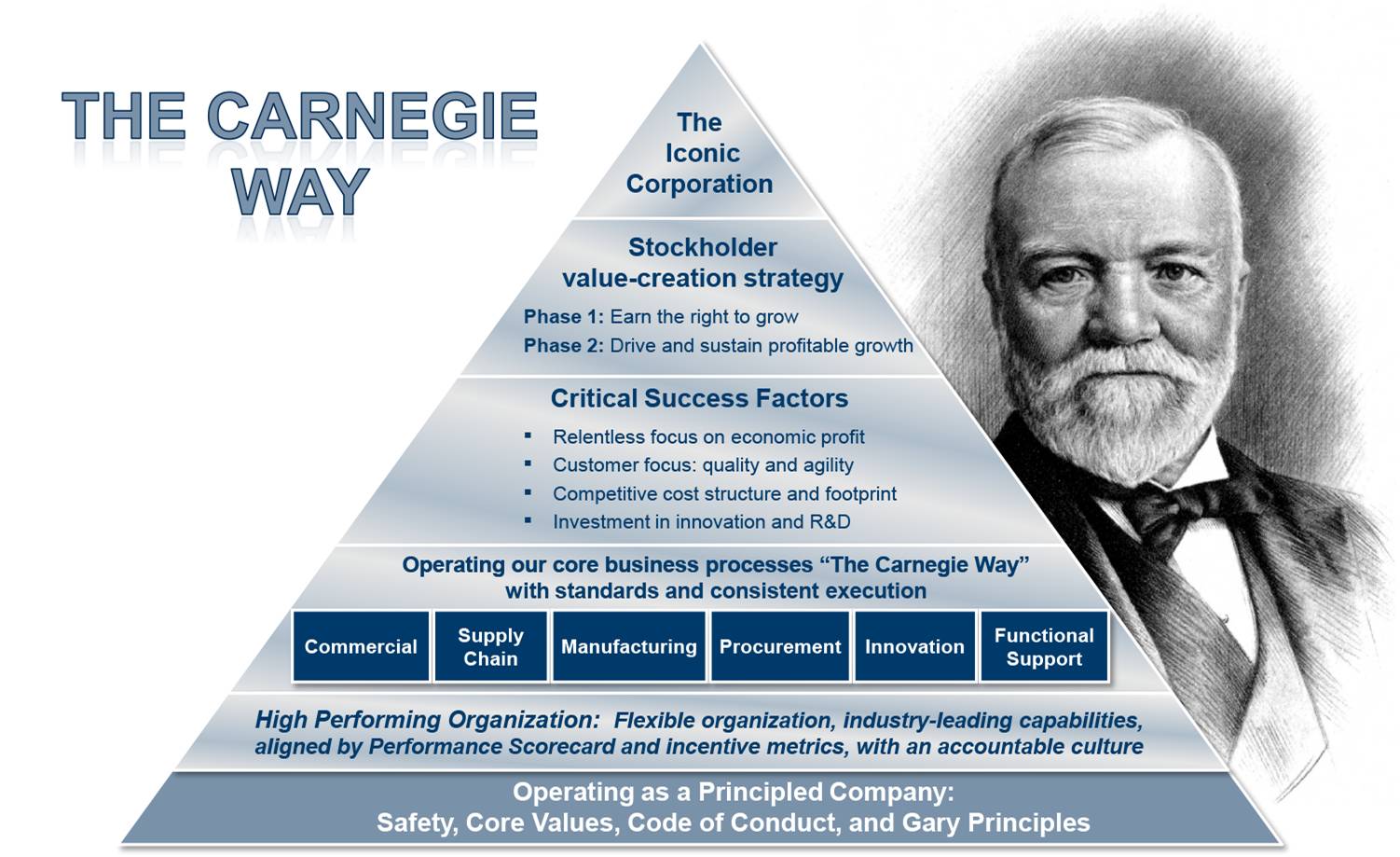

Our Vision is to become the Iconic Corporation, returning to our stature as a leading business in the United States. This vision is about more than U. S. Steel; it is about having a strong manufacturing presence in the United States.

During 2016, we continued to transform U. S. Steel through the two phases of a focused execution on our stockholder value creation strategy: (1) earn the right to grow, and (2) drive and sustain profitable growth. Our long-term success depends on our ability to execute these phases and earn an economic profit across the business cycle. Through a disciplined approach we refer to as “The Carnegie Way,” we continue working towards strengthening our balance sheet, with a strong focus on cash flow, liquidity, and financial flexibility.

Based on the Carnegie Way philosophy, we have launched a series of initiatives that we believe will enable us to add value, re-shape the Company, and improve our performance across our core business processes, including commercial, supply chain, manufacturing, procurement, innovation, and operational and functional support. We are on a mission to become an iconic industry leader, as we create a sustainable competitive advantage with a relentless focus on economic profit, our customers, cost structure, and innovation. In pursuing our financial goals, we will not sacrifice our commitment to safety and environmental stewardship. We recognize that achieving this goal requires exemplary leadership and collaboration of all employees.

4

KEY PERFORMANCE INDICATORS

This section provides an overview of select key performance indicators for U. S. Steel which management and investors use to assess the Company's financial performance. It does not contain all of the information you should consider. Fluctuations for year to year changes are explained in Item 7. "Management's Discussion and Analysis of Financial Condition and Results of Operations." In addition, the results do not include U. S. Steel Canada Inc. (USSC) subsequent to USSC's filing for Companies' Creditors Arrangement Act (CCAA) protection on September 16, 2014. Please read the entire Annual Report on Form 10-K.

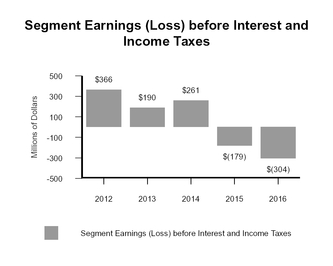

• | The $745 million of Carnegie Way benefits realized in 2016 show that we continue to make significant progress toward our goal of achieving economic profit across the business cycle. Our progress is real and it is substantial, but our 2016 results show that it is not yet enough to fully overcome unfavorable market and business conditions. |

5

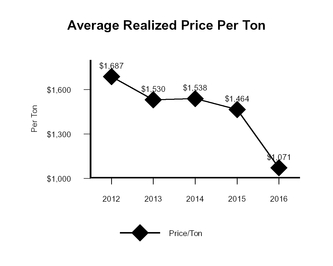

• | The decrease in net sales in 2016 is primarily due to decreased shipment volumes and lower average realized prices as a result of extremely challenging market conditions to start 2016. While imported steel volumes decreased in 2016 because of three favorable trade case rulings in 2016, the cumulative impacts of imported volumes previously shipped into the United States served to reduce our shipment volumes and depress both spot and contract prices in 2016. |

• | Despite the reduced net sales revenue, our net loss decreased in 2016 due to an improved cost structure throughout the Company. |

6

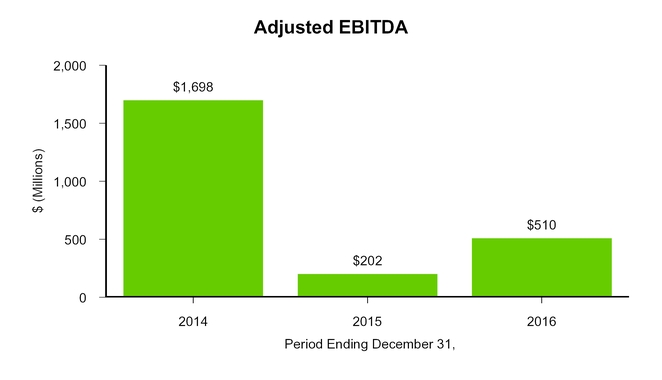

• | These amounts are derived starting from net earnings (loss) as shown on page 5. For a full reconciliation of adjusted EBITDA see page 15. |

• | Under difficult market conditions we reported improved adjusted EBITDA in 2016 as compared to 2015. |

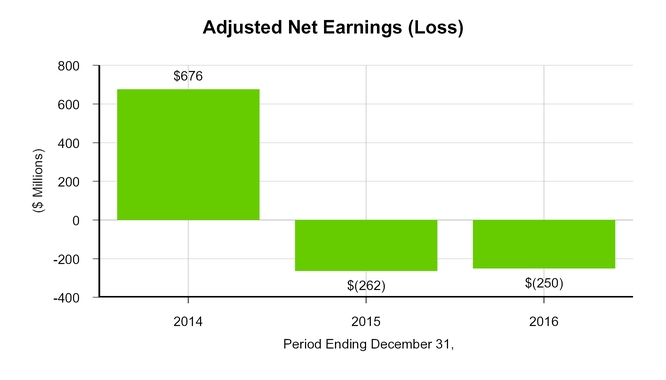

• | These amounts are derived starting from net earnings (loss) as shown on page 5. For a full reconciliation of adjusted net earnings (loss) see page 13. |

• | Our efforts towards achieving economic profit across the business cycle, guided by the Carnegie Way continue, but in 2016 were not enough to overcome difficult market conditions. |

7

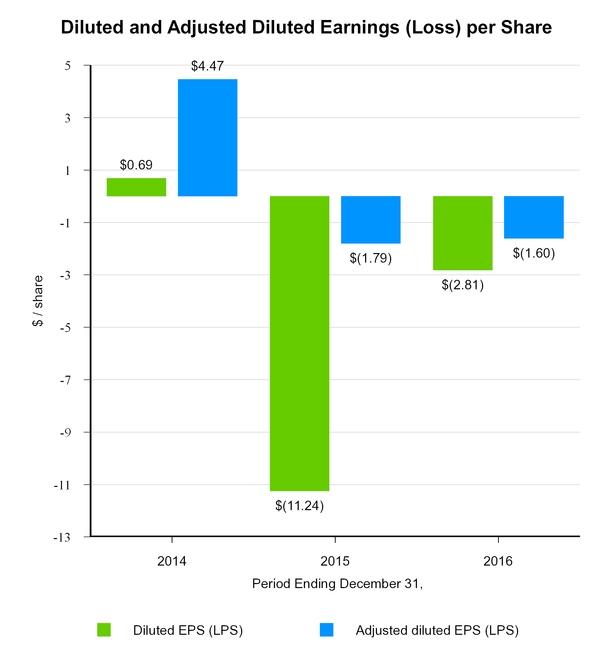

• | See reconciliation from diluted net earnings (loss) per share to adjusted diluted net earnings (loss) per share on page 14. |

8

• | Positive cash from operations due to efficient working capital management in 2016. The working capital reduction was primarily driven by improved inventory management. |

9

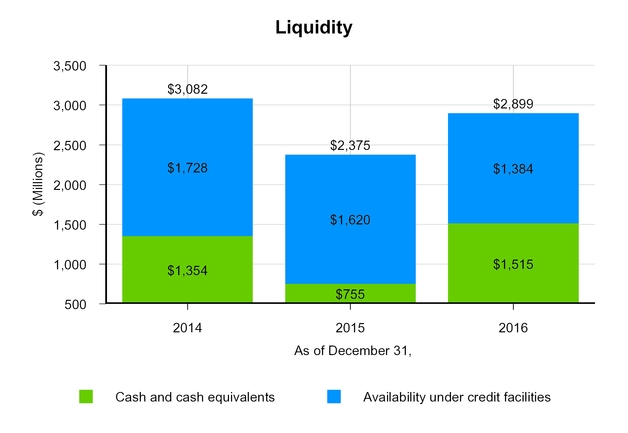

• | Maintaining strong cash and liquidity is a strategic priority. |

• | Successful completion of an equity offering in 2016 resulted in net proceeds of $482 million. |

10

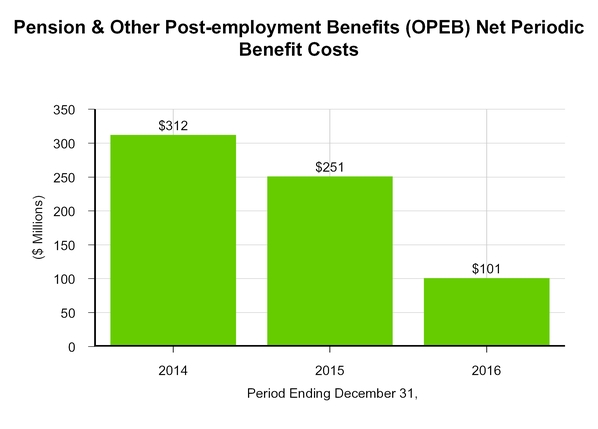

• | The decrease in 2016 pension and OPEB expense is primarily due to the freezing of benefit accruals for non-represented participants effective December 31, 2015. |

• | 2017 pension and OPEB expense is expected to be approximately $180 million. The increase in expected expense is primarily due to a lower return on assets assumption for OPEB benefits as a result of actions taken in 2016 to de-risk the OPEB benefit plan. |

• | For further details, see Note 17 to the Consolidated Financial Statements. |

11

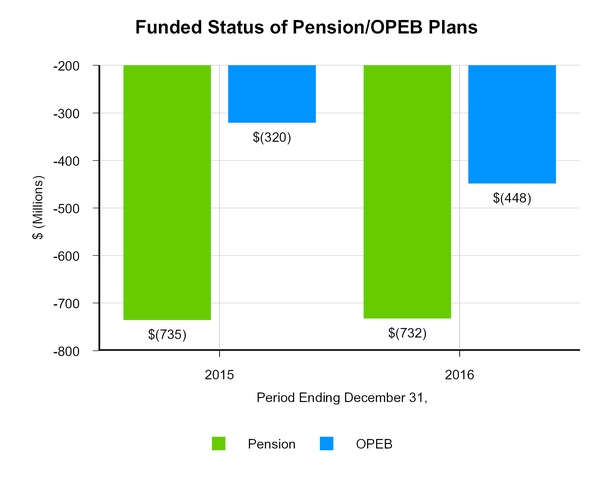

• | Pension funded status remained consistent with 2015, while OPEB funded status decreased due to certain employee and retiree benefit modifications provided in the United Steelworkers (USW) collective bargaining agreement ratified in 2016. |

• | As we maintain focus on strengthening the balance sheet, the unfunded status of our benefit plans is improving. This is partially attributable to the decision to freeze benefit accruals for non-represented participants in the defined benefit pension plan effective December 31, 2015 and the closure of OPEB plans to represented employees hired or rehired under certain conditions on or after January 1, 2016. |

• | In August 2016, U. S. Steel made a voluntary contribution of $100 million in common stock to the Company's main defined benefit pension plan. From the date of the contribution to the end of the year, the investment returned 25%. |

• | At December 31, 2016, the Pension and OPEB obligations were funded 88% and 82% respectively, on a U.S. GAAP basis. |

• | For further details, see Note 17 to the Consolidated Financial Statements. |

12

NON-GAAP FINANCIAL MEASURES

As disclosed on page 3 of this report, we present EBITDA, adjusted EBITDA, adjusted net earnings (loss) and adjusted net earnings (loss) per diluted share, which are non-GAAP measures, as an additional measurement to enhance the understanding of our operating performance and facilitate a comparison with that of our competitors.

RECONCILIATION TO ADJUSTED NET (LOSS) EARNINGS (a) | ||||||||||||

Year Ended December 31, | ||||||||||||

(Dollars in millions) | 2016 | 2015 | 2014 | |||||||||

Reconciliation to adjusted net (loss) earnings attributable to United States Steel Corporation | ||||||||||||

Net (loss) earnings attributable to United States Steel Corporation, as reported | $ | (440 | ) | $ | (1,642 | ) | $ | 102 | ||||

Loss on shutdown of certain tubular pipe mill assets (b) | 126 | — | — | |||||||||

Losses associated with U. S. Steel Canada Inc. | — | 266 | 385 | |||||||||

Loss on shutdown of Fairfield Flat-Rolled Operations (b) (c) | — | 53 | — | |||||||||

Loss on shutdown of coke production facilities (b) | — | 65 | — | |||||||||

Restructuring and other charges (b) (d) | (2 | ) | 64 | — | ||||||||

Granite City Works temporary idling charges | 18 | 99 | — | |||||||||

Postemployment benefit actuarial adjustment | — | 26 | — | |||||||||

Impairment of equity investment | 12 | 18 | — | |||||||||

Loss on retirement of senior convertible notes | — | 36 | — | |||||||||

Deferred tax asset valuation allowance | — | 753 | — | |||||||||

Impairment of carbon alloy facilities (b) | — | — | 161 | |||||||||

Litigation reserves | — | — | 46 | |||||||||

Write-off of pre-engineering costs at Keetac (b) | — | — | 30 | |||||||||

Loss on assets held for sale | — | — | 9 | |||||||||

Gain on sale of real estate assets (e) | — | — | (45 | ) | ||||||||

Curtailment gain | — | — | (12 | ) | ||||||||

Impairment of intangible assets | 14 | — | — | |||||||||

Loss on extinguishment of debt | 22 | — | — | |||||||||

Total Adjustments | 190 | 1,380 | 574 | |||||||||

Adjusted net (loss) earnings attributable to United States Steel Corporation | $ | (250 | ) | $ | (262 | ) | $ | 676 | ||||

(b) Included in restructuring and other charges on the Consolidated Statement of Operations.

(c) Fairfield Flat-Rolled Operations includes the blast furnace and associated steelmaking operations, along with most of the flat-rolled finishing operations at the former Fairfield Works. The #5 coating line continues to operate.

(d) The 2015 amount consists primarily of employee related costs, including costs for severance, supplemental unemployment benefits and continuation of health care benefits.

(e) Gain on sale of surface rights and mineral royalty revenue streams in the state of Alabama.

13

RECONCILIATION TO ADJUSTED NET (LOSS) EARNINGS PER SHARE (a) | ||||||||||||

Year Ended December 31, | ||||||||||||

2016 | 2015 | 2014 | ||||||||||

Reconciliation to adjusted diluted net (loss) earnings per share | ||||||||||||

Diluted net loss per share, as reported | $ | (2.81 | ) | $ | (11.24 | ) | $ | 0.69 | ||||

Loss on shutdown of certain tubular pipe mill assets (b) | 0.80 | — | — | |||||||||

Losses associated with U. S. Steel Canada Inc. | — | 1.82 | 2.52 | |||||||||

Loss on shutdown of Fairfield Flat-Rolled Operations (b) (c) | — | 0.37 | — | |||||||||

Loss on shutdown of coke production facilities (b) | — | 0.44 | — | |||||||||

Restructuring and other charges (b) (d) | (0.01 | ) | 0.44 | — | ||||||||

Granite City Works temporary idling charges | 0.11 | 0.68 | — | |||||||||

Postemployment benefit actuarial adjustment | — | 0.18 | — | |||||||||

Impairment of equity investment | 0.08 | 0.12 | — | |||||||||

Loss on retirement of senior convertible notes | — | 0.25 | — | |||||||||

Deferred tax asset valuation allowance | — | 5.15 | — | |||||||||

Impairment of carbon alloy facilities (b) | — | — | 1.06 | |||||||||

Litigation reserves | — | — | 0.31 | |||||||||

Write-off of pre-engineering costs at Keetac (b) | — | — | 0.21 | |||||||||

Loss on assets held for sale | — | — | 0.06 | |||||||||

Gain on sale of real estate assets (e) | — | — | (0.30 | ) | ||||||||

Curtailment gain | — | — | (0.08 | ) | ||||||||

Impairment of intangible assets | 0.09 | — | — | |||||||||

Loss on extinguishment of debt | 0.14 | — | — | |||||||||

Total adjustments | 1.21 | 9.45 | 3.78 | |||||||||

Adjusted diluted net (loss) earnings per share | $ | (1.60 | ) | $ | (1.79 | ) | $ | 4.47 | ||||

(a) The adjustments included in this table have been tax affected at the quarterly effective tax rate through the third quarter of 2015. Subsequent to the third quarter of 2015, the adjustments have been tax affected at a 0% tax rate due to the recognition of a full valuation allowance which was established in the fourth quarter of 2015.

(b)Included in restructuring and other charges and cost of sales in the Consolidated Statement of Operations.

(c) Fairfield Flat-Rolled Operations includes the blast furnace and associated steelmaking operations, along with most of the flat-rolled finishing operations at the former Fairfield Works. The #5 coating line continues to operate.

(d) The 2015 amount consists primarily of employee related costs, including costs for severance, supplemental unemployment benefits and continuation of health care benefits.

(e) Gain on sale of surface rights and mineral royalty revenue streams in the state of Alabama.

14

RECONCILIATION TO EBITDA AND ADJUSTED EBITDA | ||||||||||||

Year Ended December 31, | ||||||||||||

(Dollars in millions) | 2016 | 2015 | 2014 | |||||||||

Reconciliation to EBITDA and Adjusted EBITDA | ||||||||||||

Net (loss) earnings attributable to U. S. Steel Corporation | $ | (440 | ) | $ | (1,642 | ) | $ | 102 | ||||

Income tax provision | 24 | 183 | 68 | |||||||||

Net interest and other financial costs | 251 | 257 | 243 | |||||||||

Depreciation, depletion and amortization expense | 507 | 547 | 627 | |||||||||

EBITDA | 342 | (655 | ) | 1,040 | ||||||||

Loss on shutdown of certain tubular pipe mill assets (a) | 126 | — | — | |||||||||

Losses associated with U. S. Steel Canada Inc. | — | 392 | 416 | |||||||||

Loss on shutdown of Fairfield Flat-Rolled Operations (a) (b) | — | 91 | — | |||||||||

Loss on shutdown of coke production facilities (a) | — | 153 | — | |||||||||

Restructuring and other charges (a), (c) | (2 | ) | 78 | — | ||||||||

Granite City Works temporary idling charges | 18 | 99 | — | |||||||||

Postemployment benefit actuarial adjustment | — | 26 | — | |||||||||

Impairment of equity investment | 12 | 18 | — | |||||||||

Impairment of carbon alloy facilities (a) | — | — | 195 | |||||||||

Litigation reserves | — | — | 70 | |||||||||

Write-off of pre-engineering costs at Keetac (a) | — | — | 37 | |||||||||

Loss on assets held for sale | — | — | 14 | |||||||||

Gain on sale of real estate assets (d) | — | — | (55 | ) | ||||||||

Curtailment gain | — | — | (19 | ) | ||||||||

Impairment of intangible assets | 14 | — | — | |||||||||

Adjusted EBITDA | $ | 510 | $ | 202 | $ | 1,698 | ||||||

(a) Included in restructuring and other charges in the Consolidated Statement of Operations.

(b) Fairfield Flat-Rolled Operations includes the blast furnace and associated steelmaking operations, along with most of the flat-rolled finishing operations at Fairfield Works. The #5 coating line continues to operate.

(c) The 2015 amount consists primarily of employee related costs, including costs for severance, supplemental unemployment benefits and continuation of health care benefits.

(d) Gain on sale of surface rights and mineral royalty revenue streams in the state of Alabama.

15

PART I

Item 1. BUSINESS

United States Steel Corporation (U. S. Steel) is an integrated steel producer of flat-rolled and tubular products with major production operations in North America and Europe. An integrated steel producer uses iron ore and coke as primary raw materials for steel production. U. S. Steel has annual raw steel production capability of 22.0 million net tons (17.0 million tons in the United States and 5.0 million tons in Europe). U. S. Steel supplies customers throughout the world primarily in the automotive, consumer, industrial and oil country tubular goods (OCTG) markets. According to worldsteel Association’s latest published statistics, U. S. Steel was the twenty-fourth largest steel producer in the world in 2015. Also in 2015, according to publicly available information, U. S. Steel was the third largest steel producer in the United States. U. S. Steel is also engaged in other business activities consisting primarily of railroad services and real estate operations.

The Carnegie Way

In 2013, U. S. Steel launched a transformational process called the “Carnegie Way,” named after the famed American industrialist and U. S. Steel co-founder Andrew Carnegie. The Carnegie Way is a strategic, disciplined approach to transforming the Company to address the new realities of the marketplace. Through the Carnegie Way, we focus on our strengths and where we can create the most value for all U. S. Steel stakeholders, including our stockholders, employees, customers and suppliers. The Carnegie Way is a framework that helps employees address all aspects of our business and achieve sustainable improvements through process efficiencies and strategic investments. We have been working through a series of transformational initiatives that we believe will enable us to more effectively add value, respond to customer needs, get leaner faster, right-size our operations and improve our performance across our core business process capabilities, including commercial, supply chain, manufacturing, procurement, innovation, and operational and functional support. Key accomplishments to date include a more intense focus on cash flow, a stronger balance sheet and a revised approach to how we view shipment volume and production. In pursuing our financial goals, we will not sacrifice our commitment to our core values of safety and environmental stewardship. We also recognize that achieving this goal requires exemplary leadership and collaboration among all employees, and we are committed to attracting, developing and retaining a workforce with the talent, skills and integrity needed for our long-term success. The Carnegie Way has already driven a shift in the Company that has enabled us to withstand the prolonged downturn in steel prices while positioning us for success in a market recovery.

Our structured approach, using the Carnegie Way value creation methodology, gives us the confidence that we can continue to make progress and create value for our customers, and when we create value for our customers, we create value for all of our stakeholders - our stockholders, our suppliers, our employees and the communities where we do business.

16

Segments

U. S. Steel has three reportable operating segments: Flat-Rolled Products (Flat-Rolled), U. S. Steel Europe (USSE) and Tubular Products (Tubular). The results of our railroad and real estate businesses that do not constitute reportable segments are combined and disclosed in the Other Businesses category.

Flat-Rolled

The Flat-Rolled segment includes the operating results of U. S. Steel’s integrated steel plants and equity investees in the United States involved in the production of slabs, strip mill plates, sheets and tin mill products, as well as all iron ore and coke production facilities in the United States. These operations primarily serve North American customers in the service center, conversion, transportation (including automotive), construction, container, and appliance and electrical markets.

As part of the Carnegie Way transformation, the Flat-Rolled segment was structured to better service customer needs through the creation of three "commercial entities" to specifically address customers. Our Flat-Rolled segment commercial entities include: (1) automotive, (2) consumer and (3) industrial, service center and mining.

Automotive Solutions collaborates with customers to develop solutions such as the next generation of advanced high strength steel (AHSS) to address challenges facing the automotive industry, including increased fuel economy standards and enhanced safety requirements.

Consumer Solutions partners with customers in the appliance, packaging, container and construction markets. Consumer Solutions has a robust presence with our tin customers, who represent more than one quarter of this market category. Additional product lines within the market category include the Company's COR-TEN AZP®, ACRYLUME®, GALVALUME® and Weathered Metals Series®.

Industrial, Service Center and Mining Solutions focuses on the Company's customers in the service center business, pipe and tube manufacturing markets, and agricultural and industrial equipment markets.

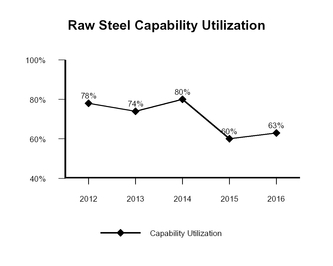

Flat-Rolled has aggregate annual raw steel production capability of 17.0 million tons produced at our Gary Works, Mon Valley Works, Great Lakes Works and Granite City Works facilities. Prior to the permanent shut down of the Fairfield Flat-Rolled operations beginning in August 2015 and the Companies' Creditors Arrangement Act (CCAA) filing and the deconsolidation of U. S. Steel Canada, Inc. (USSC) in September 2014, annual raw steel production capability for Flat-Rolled was 19.4 million tons and 22.0 million tons, respectively. Raw steel production was 10.7 million tons in 2016, 11.3 million tons in 2015 and 17.0 million tons in 2014. Raw steel production averaged 63 percent of capability in 2016, 60 percent of capability in 2015 and 80 percent of capability in 2014. In December 2015 the Granite City Works was temporarily idled and if its production capability is excluded, Flat-Rolled production would have been 75 percent of capability in 2016.

European Operations

The USSE segment includes the operating results of U. S. Steel Košice (USSK), U. S. Steel’s integrated steel plant and coke production facilities in Slovakia. USSE primarily serves customers in the Eastern European construction, service center, conversion, container, transportation (including automotive), appliance and electrical, and oil, gas and petrochemical markets. USSE produces and sells slabs, sheet, strip mill plate, tin mill products and spiral welded pipe, as well as heating radiators and refractory ceramic materials.

USSE has annual raw steel production capability of 5.0 million tons. USSE’s raw steel production was 5.0 million tons in 2016, 4.7 million tons in 2015, and 4.8 million tons in 2014. USSE’s raw steel production averaged 99 percent of capability in 2016, 93 percent of capability in 2015 and 96 percent of capability in 2014.

Tubular

The Tubular segment includes the operating results of U. S. Steel’s tubular production facilities, in the United States, and equity investees in the United States and Brazil. These operations produce and sell seamless and electrical resistance welded (welded) steel casing and tubing (commonly known as OCTG), standard and line pipe and mechanical tubing and primarily serve customers in the oil, gas and petrochemical markets. Tubular’s annual production capability was 2.5 million prior to the permanent shutdown of the Lorain #4 and Lone Star #1 pipe mills and the Bellville

17

Operations, as further described below. After the permanent shutdowns, Tubular's annual production capability is 1.5 million tons.

In December of 2016, U. S. Steel made the strategic decision to permanently close the Lorain #4 and Lone Star #1 pipe mills and the Bellville Operations after considering a number of factors, including challenging market conditions for tubular products, reduced rig counts, and continued high levels of unfairly traded imports.

U. S. Steel Tubular Products, Inc. (USSTP), a wholly owned subsidiary of U. S. Steel, is designing and developing a range of premium and semi-premium connections to address the growing needs for technical solutions to our end users' well site production challenges. Through its wholly owned subsidiary, USS Oilwell Services LLC, USSTP also offers rig site services, which provides the technical expertise for proper installation of our tubular products and proprietary connections at the well site.

For further information, see "Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations" and Note 3 to the Consolidated Financial Statements.

18

Financial and Operational Highlights

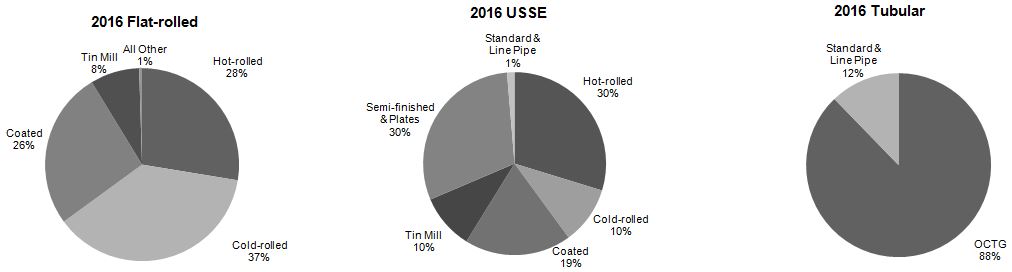

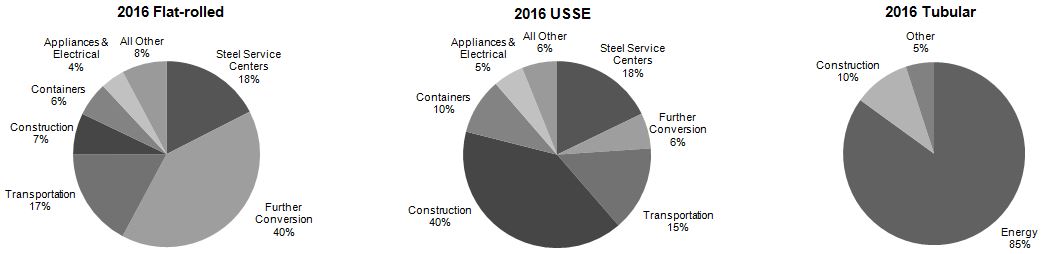

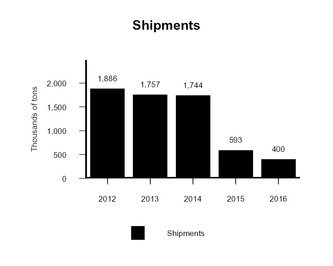

Steel Shipments by Product and Segment

The following table shows steel shipments to end customers, joint ventures and equity investees of U. S. Steel.

(Thousands of Tons) | Flat-Rolled | USSE | Tubular | Total | ||||||||

Product—2016 | ||||||||||||

Hot-rolled Sheets | 2,784 | 1,337 | — | 4,121 | ||||||||

Cold-rolled Sheets | 3,775 | 459 | — | 4,234 | ||||||||

Coated Sheets | 2,655 | 849 | — | 3,504 | ||||||||

Tin Mill Products | 831 | 439 | — | 1,270 | ||||||||

Oil country tubular goods (OCTG) | — | — | 351 | 351 | ||||||||

Standard and line pipe | — | 60 | 49 | 109 | ||||||||

Semi-finished and Plates | 23 | 1,352 | — | 1,375 | ||||||||

Other | 26 | — | — | 26 | ||||||||

TOTAL | 10,094 | 4,496 | 400 | 14,990 | ||||||||

Memo: Intersegment Shipments from Flat-Rolled to Tubular | ||||||||||||

Hot-rolled sheets | 42 | |||||||||||

Product—2015 | ||||||||||||

Hot-rolled Sheets | 3,283 | 1,165 | — | 4,448 | ||||||||

Cold-rolled Sheets | 3,507 | 470 | — | 3,977 | ||||||||

Coated Sheets | 2,511 | 865 | — | 3,376 | ||||||||

Tin Mill Products | 927 | 428 | — | 1,355 | ||||||||

Oil country tubular goods (OCTG) | — | — | 345 | 345 | ||||||||

Standard and line pipe | — | 55 | 248 | 303 | ||||||||

Semi-finished and Plates | 47 | 1,374 | — | 1,421 | ||||||||

Other | 320 | — | — | 320 | ||||||||

TOTAL | 10,595 | 4,357 | 593 | 15,545 | ||||||||

Memo: Intersegment Shipments from Flat-Rolled to Tubular | ||||||||||||

Hot-rolled sheets | 219 | |||||||||||

Rounds | 197 | |||||||||||

Product—2014 | ||||||||||||

Hot-rolled Sheets | 4,909 | 1,374 | — | 6,283 | ||||||||

Cold-rolled Sheets | 4,207 | 518 | — | 4,725 | ||||||||

Coated Sheets | 3,316 | 775 | — | 4,091 | ||||||||

Tin Mill Products | 1,180 | 411 | — | 1,591 | ||||||||

Oil country tubular goods (OCTG) | — | — | 1,308 | 1,308 | ||||||||

Standard and line pipe | — | 62 | 314 | 376 | ||||||||

Semi-finished and Plates | 165 | 1,039 | — | 1,204 | ||||||||

Other | 131 | — | 122 | 253 | ||||||||

TOTAL | 13,908 | 4,179 | 1,744 | 19,831 | ||||||||

Memo: Intersegment Shipments from Flat-Rolled to Tubular | ||||||||||||

Hot-rolled sheets | 863 | |||||||||||

Rounds | 849 | |||||||||||

19

Steel Shipments by Market and Segment

The following table does not include shipments to end customers by joint ventures and other equity investees of U. S. Steel. Shipments of materials to these entities are included in the “Further Conversion – Joint Ventures” market classification. No single customer accounted for more than 10 percent of gross annual revenues.

(Thousands of Tons) | Flat-Rolled | USSE | Tubular | Total | ||||||||

Major Market – 2016 | ||||||||||||

Steel Service Centers | 1,765 | 801 | — | 2,566 | ||||||||

Further Conversion – Trade Customers | 2,650 | 274 | — | 2,924 | ||||||||

– Joint Ventures | 1,423 | — | — | 1,423 | ||||||||

Transportation (Including Automotive) | 1,725 | 660 | — | 2,385 | ||||||||

Construction and Construction Products | 725 | 1,811 | 40 | 2,576 | ||||||||

Containers | 600 | 436 | — | 1,036 | ||||||||

Appliances and Electrical Equipment | 420 | 236 | — | 656 | ||||||||

Oil, Gas and Petrochemicals | — | 4 | 340 | 344 | ||||||||

Exports from the United States | 436 | — | 20 | 456 | ||||||||

All Other | 350 | 274 | — | 624 | ||||||||

TOTAL | 10,094 | 4,496 | 400 | 14,990 | ||||||||

Major Market – 2015 | ||||||||||||

Steel Service Centers | 1,702 | 718 | — | 2,420 | ||||||||

Further Conversion – Trade Customers | 3,039 | 304 | — | 3,343 | ||||||||

– Joint Ventures | 1,254 | — | — | 1,254 | ||||||||

Transportation (Including Automotive) | 2,011 | 705 | — | 2,716 | ||||||||

Construction and Construction Products | 649 | 1,703 | 55 | 2,407 | ||||||||

Containers | 692 | 424 | — | 1,116 | ||||||||

Appliances and Electrical Equipment | 429 | 236 | — | 665 | ||||||||

Oil, Gas and Petrochemicals | — | — | 513 | 513 | ||||||||

Exports from the United States | 234 | — | 25 | 259 | ||||||||

All Other | 585 | 267 | — | 852 | ||||||||

TOTAL | 10,595 | 4,357 | 593 | 15,545 | ||||||||

Major Market – 2014 | ||||||||||||

Steel Service Centers | 2,578 | 682 | — | 3,260 | ||||||||

Further Conversion – Trade Customers | 4,013 | 299 | — | 4,312 | ||||||||

– Joint Ventures | 1,519 | — | — | 1,519 | ||||||||

Transportation (Including Automotive) | 2,445 | 674 | — | 3,119 | ||||||||

Construction and Construction Products | 775 | 1,584 | 122 | 2,481 | ||||||||

Containers | 1,287 | 403 | — | 1,690 | ||||||||

Appliances and Electrical Equipment | 616 | 267 | — | 883 | ||||||||

Oil, Gas and Petrochemicals | — | 3 | 1,545 | 1,548 | ||||||||

Exports from the United States | 263 | — | 77 | 340 | ||||||||

All Other | 412 | 267 | — | 679 | ||||||||

TOTAL | 13,908 | 4,179 | 1,744 | 19,831 | ||||||||

20

Business Strategy

Over the long term, our strategy is to return to our stature as an iconic industry leader, as we create a sustainable competitive advantage with a relentless focus on value creation, customer, quality, cost structure and innovation. In pursuing our strategy, we remain committed to safety and environmental stewardship. We recognize that achieving this goal requires exemplary leadership and collaboration of all employees, and we are committed to attracting, developing and retaining a high-performing workforce with the talent, skills and integrity needed for our long-term success.

We have continued to transform U. S. Steel through the two phases of focused execution of our stockholder value creation strategy: (1) earn the right to grow, and (2) drive and sustain profitable growth. Through a disciplined approach we refer to as “The Carnegie Way,” we continue working toward strengthening our balance sheet, with a strong focus on cash flow, liquidity, and financial flexibility and have launched a series of initiatives that we believe will continue to enable us to add value, re-shape the Company, and improve our performance across our core business processes, including commercial, supply chain, manufacturing, procurement, innovation, and operational and functional support.

We have worked, and continue to work, to position the Company to be best-in-class in innovation, quality and providing customer service and solutions to our customers. The strategic positioning of operations within the commercial entities enhances our ability to better hear the voice of the customer, ensuring that we deliver superior value and drive results in the markets we choose to serve. We believe this enhanced commercial concentration will continue to put U. S. Steel in a stronger position to be best-in-class in product innovation, quality and providing service and solutions to our customers, as well as steel manufacturing.

U. S. Steel continuously evaluates potential strategic and organizational opportunities, which may include the acquisition, divestiture or consolidation of assets. The Company will pursue opportunities based on the financial condition of the Company, its long-term strategy, and what the Board of Directors determines to be in the best interests of the Company's stockholders.

Changes to Operational Footprint

In December 2016, the Company reached agreements to supply iron ore pellets to third party customers over the next several years. The Keetac Iron Ore Operations restarted production in the first quarter of 2017 to take full advantage of these business opportunities. It had previously been idle since May of 2015 due to significantly lower steel production.

In December 2016, U. S. Steel announced it would be restarting production on the hot strip mill at Granite City Works in the first quarter of 2017 to provide better alignment with customer needs and improve service while increasing the pace of our asset revitalization plan. The hot strip mill was temporarily idled in January of 2016.

In December 2016, the Company made the strategic decision to permanently close the Lorain #4 and Lone Star #1 pipe mills and the Bellville Tubular Operations after considering a number of factors, including challenging market conditions for tubular products, reduced rig counts, and unfairly traded imports.

In April 2016, U. S. Steel temporarily idled its Lone Star tubular operations.

During 2015, the Company adjusted operating levels at several of its tubular operations as declining oil prices and rig counts have significantly reduced demand for OCTG products.

In August 2015, U. S. Steel permanently shut down the majority of Fairfield Flat-Rolled operations.

In 2015, the Company permanently closed the coke making operations at Granite City Works and Gary Works. Also, in 2015, U. S. Steel temporarily idled steelmaking operations at Granite City Works.

On September 16, 2014, U. S. Steel Canada, Inc. (USSC), a wholly owned subsidiary of U. S. Steel, applied for relief from its creditors pursuant to Canada’s Companies’ Creditors Arrangement Act (CCAA). As a result of USSC filing for CCAA protection (CCAA filing), U. S. Steel determined that USSC and its subsidiaries would be deconsolidated from U. S. Steel’s financial statements on a prospective basis effective with the date of the CCAA filing.

21

Recent Acquisitions

On May 29, 2015, the Company purchased the 50 percent joint venture interest in Double Eagle Steel Coating Company (DESCO) that it did not previously own for $25 million. The facility coats sheet steel with free zinc or zinc alloy coatings, primarily for use in the automotive industry. DESCO’s annual production capability is approximately 720,000 tons. DESCO's electrolytic galvanizing line (EGL) has become part of the larger operational footprint of U. S. Steel's Great Lakes Works within the Flat-Rolled segment. The EGL is increasing our ability to provide industry-leading AHSS, including Gen 3 grades under development, as well as to provide high quality exposed steel for automotive body and closure applications to our customers.

Safety

U. S. Steel has a long-standing commitment to the safety and health of the men and women who work in our facilities. For our Company, safety is our primary core value. Every employee has the right to return home safely at the end of every day, and we are working to eliminate all injuries and incidents at all of our facilities. Ensuring a safe workplace also improves productivity, quality, reliability and financial performance. By making safety and health a personal responsibility, our employees are making a daily commitment to follow safe work practices, look out for the safety of co-workers and ensure safe working conditions for everyone. A “Safety First” mindset is as essential to our success as the tools and technologies we rely on to do business.

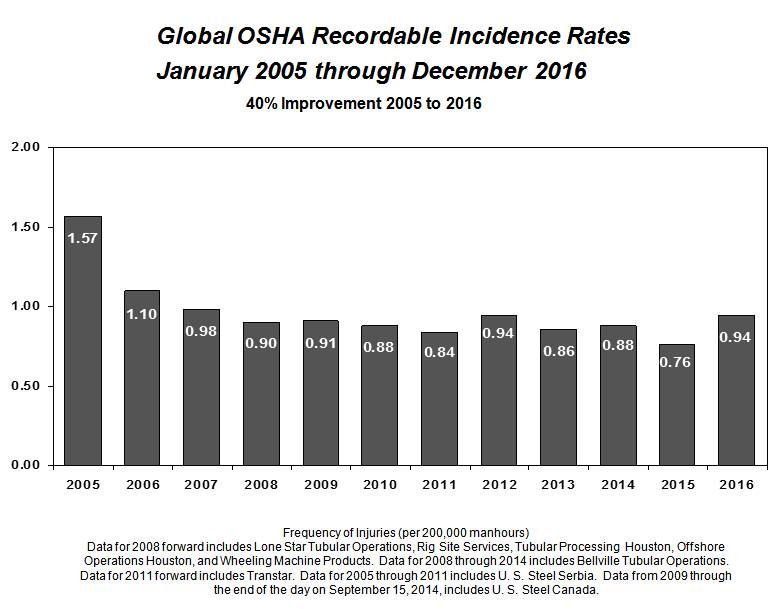

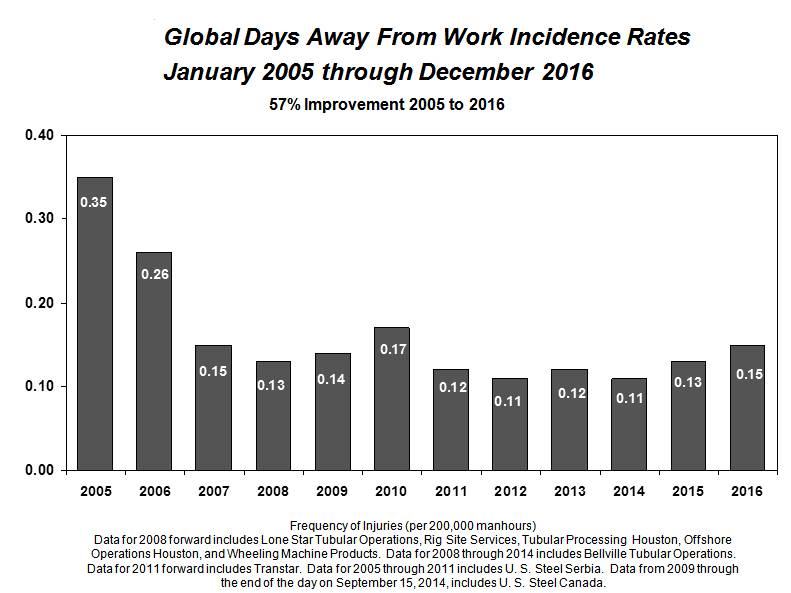

U. S. Steel finished 2016 with a Global Total OSHA Recordable Rate of 0.94, which is 73% better than the Bureau of Labor Statistics for Iron & Steel rate of 3.50 and 44% better than American Iron and Steel Institute rate of 1.67. U. S. Steel finished 2016 with a Days Away From Work Rate of 0.15, which is 85% better than the Bureau of Labor Statistics for Iron & Steel rate of 1.0 and 63% better than American Iron and Steel Institute rate of 0.40. Additionally, when comparing our most severe injuries - cases involving 31 or more days away from work - U. S. Steel performs at a level almost 6 times better than the Bureau of Labor Statistics for Iron and Steel.

In 2016 we experienced two domestic U. S. Steel fatalities and 1 contractor fatality in Europe. These tragic events serve as a reminder that we must remain vigilant in our safety efforts to ensure every employee returns home safely every day.

Through 2016, the 12 year performance for our key safety measures: Total Recordable and Days Away From Work rates show improvement of 40% and 57% respectively, as shown on the following graphs.

22

23

Environmental Stewardship

Throughout its history, U. S. Steel has either led the industry or used methods consistent with prevailing industry practices in its commitment to environmental stewardship. We have implemented and continue to develop business practices that are environmentally effective. We believe part of being a good corporate citizen requires a dedicated focus on how our industry affects the environment, and we have taken the actions described below in furtherance of that goal.

U. S. Steel, largely through the American Iron and Steel Institute (AISI), the worldsteel Association and the European Confederation of Iron and Steel Industries (Eurofer), is involved in the promotion of cost effective environmental strategies through the development of appropriate air, water, waste and climate change laws and regulations at the local, state, national and international levels.

We are committed to reducing emissions as well as our carbon footprint. We have investigated, created and implemented innovative, best practice solutions throughout U. S. Steel to manage and reduce energy consumption. We are also committed to investing in technologies to further improve the environmental performance of our steelmaking process. In addition, we continue to focus on implementing energy reduction strategies, use of efficient energy sources, waste reduction management and the utilization of by-product fuels.

According to the AISI, relative to competing materials, steel has approximately one-fifth the carbon footprint of aluminum, one-twelfth the footprint of magnesium, and about one-ninth the footprint of carbon fiber composites. Our AHSS used in today’s vehicles afford significant light-weighting opportunities. When comparing steel to aluminum, in terms of sustainability, steel has a smaller carbon footprint and costs less.

U. S. Steel has historically recycled between 4 and 5 million tons of purchased and produced steel scrap every year. Because of steel’s physical properties, our products can be recycled at the end of their useful life without loss of quality, contributing to steel’s high recycling rate and affordability. Comparatively, due to limitations in aluminum processing, very little recycled aluminum is included in aluminum sheet goods used for automotive or aircraft applications. This means that any increased use of aluminum sheet for high-end applications must come from Greenhouse Gas (GHG) intensive primary aluminum, which generates significantly more GHG emissions than steel.

All of our major production facilities have Environmental Management Systems that are certified to the ISO 14001 Standard. This standard, published by the International Organization for Standardization, provides the framework for the measurement and improvement of environmental impacts of the certified facility.

Commercial Strategy

Our commercial strategy is focused on providing customer focused solutions with value-added steel products, including AHSS and coated sheets for the automotive and appliance industries, electrical steel sheets for the manufacture of motors and electrical equipment, galvanized and Galvalume® sheets for construction, tin mill products for the packaging industry and a vast array of steel products, including OCTG and premium connections, for use in the drilling, storage, and transmission of North American shale oil and gas.

We are committed to anticipating our customers' changing needs by developing new steel products and uses for steel that meet the evolving market and regulatory demands imposed on them. In connection with this commitment, we have research centers in Pittsburgh, Pennsylvania, and Košice, Slovakia, an automotive center in Troy, Michigan and an Innovation and Technology Center for Tubular products in Houston, Texas. The focus of these centers is to develop new products and work with our customers to better serve their needs. Examples of our customer focused product innovation include the development of the first commercially available coated AHSS and GEN3 steels and embedding application engineers at original equipment manufacturers to demonstrate how to best utilize the material in body design to meet automobile passenger safety requirements while significantly reducing weight to meet future vehicle fuel efficiency standards; and a line of premium and semi-premium tubular connections to meet our customers’ increasingly complex needs for offshore and horizontal drilling. Designed and developed at the Innovation and Technology Center in Houston, USS- Liberty TC™ is the first domestically made, threaded and coupled premium connection with a metal-to-metal seal that has been tested to the 2014 version of API 5C5 CAL IV. USS- Liberty TC™ was successfully installed by a subsidiary of Range Resources Corporation and is available to other energy producers. This work in premium connection development is supported by our investment in a new full scale tubular connection test frame located at Offshore Operations in Houston, Texas. Please refer to Item I. Business Strategy for further details of our commercial entities and related strategies.

24

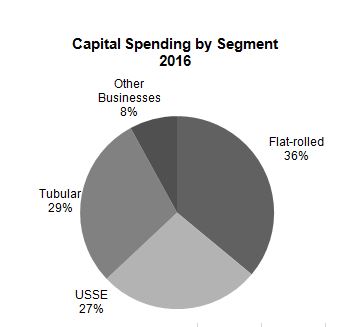

Capital Projects and Other Investments

We are currently developing projects within our Flat-Rolled, USSE and Tubular segments to revitalize our assets, enhance quality and reliability, expand production of AHSS, deliver additional premium connections, and improve our capabilities in packaging. This will further enhance our ability to support our customers’ evolving needs and increase our value-added product capabilities. We have substantially completed the implementation of an Enterprise Resource Planning (ERP) system to replace our existing information technology systems, which will enable us to operate more efficiently. The completion of the ERP system is expected to provide further opportunities to streamline, standardize and centralize business processes in order to maximize cost effectiveness, efficiency and control across our global operations.

Workforce

At U. S. Steel, we are committed to attracting, developing, and retaining a workforce of talented, high integrity, diverse people — all working together to deliver superior results for our Company, stockholders, customers and communities. We regularly review our human capital needs and focus on the selection, development and retention of employees in order to sustain and enhance our competitive position in the markets we serve.

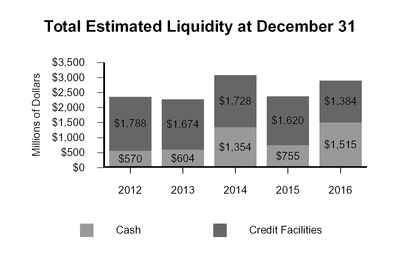

Capital Structure and Liquidity

Our primary financial goal is to enhance stockholder value by focusing on our capital structure, liquidity, and financial flexibility by deploying cash strategically as we earn the right to grow. Our cash deployment strategy includes maintaining a healthy pension plan; delivering operational excellence with a focus on safety, quality and reliability; and the revitalization of our capital, both human and equipment, to enable sustainable growth.

In 2016, we undertook several steps to support these goals. The Company issued $980 million of 8.375% Senior Secured Notes due July 1, 2021 and received net proceeds of approximately $958 million, which was used to repay certain of the Company's outstanding debt obligations. Additionally, the Company completed an optional redemption of its outstanding 6.05% Senior Notes due 2017 for an aggregate principal amount of approximately $444 million plus a total make whole premium of approximately $22 million. Further, the Company repurchased approximately $6 million of its 6.05% Senior Notes due 2017, approximately $339 million of its 7.00% Senior Notes dues 2018, approximately $168 million of its 7.375% Senior Notes due 2020 and approximately $75 million of its 6.875% Senior Notes due 2021 through various tender offers and open market purchases.

During August 2016, we made a voluntary contribution of 3,763,643 shares of the Company’s common stock to U. S. Steel's main defined benefit pension plan as part of our long term pension liability management strategy. The shares were valued at a price of $26.57 per share, or approximately $100 million in the aggregate, which was the closing price of the Company's common stock on the date of the contribution. Also during August 2016, U. S. Steel issued 21,735,000 of common shares in an underwritten public offering, resulting in net proceeds of approximately $482 million, which will be used for financial flexibility, revitalization of assets and general corporate purposes.

During 2016, U. S. Steel repaid $1.0 billion of debt. We ended 2016 with $1.5 billion of cash and cash equivalents on hand and total liquidity of approximately $2.9 billion.

Steel Industry Background and Competition

The global steel industry is cyclical, highly competitive and has historically been characterized by overcapacity.

U. S. Steel's competitive position may be affected by, among other things, differences among U. S. Steel's and its competitors' cost structure, labor costs, environmental remediation and compliance costs, global capacity and the existence and magnitude of government subsidies.

U. S. Steel competes with many North American and international steel producers. Competitors include integrated producers, which, like U. S. Steel, use iron ore and coke as the primary raw materials for steel production, as well as electric arc furnace (EAF) producers, which primarily use steel scrap and other iron-bearing feedstocks as raw materials. Global steel capacity has continued to increase, with some published sources estimating that steel capacity in China alone is over one billion metric tons per year. In addition, other products, such as aluminum, plastics and composites, compete with steel in several applications.

25

EAF producers typically require lower capital expenditures for construction of facilities and may have lower total employment costs; however, these competitive advantages may be minimized or eliminated by the cost of scrap when scrap prices are high, which was not the case in 2015 and 2016. Some mini-mills utilize thin slab casting technology to produce flat-rolled products and are increasingly able to compete directly with integrated producers in many flat-rolled product applications previously produced only by integrated steelmakers.

U. S. Steel provides defined benefit pension and/or other postretirement benefits to approximately 100,000 current employees, retirees and their beneficiaries. Many of our competitors do not have comparable retiree obligations. Participation in U. S. Steel's main defined benefit pension plan was closed to new entrants on July 1, 2003 and benefit accruals for all non-represented participants were frozen effective December 31, 2015. The 2015 Labor Agreements provided for the closure of other post-retirement benefits (OPEB) plans to represented employees hired or rehired under certain conditions on or after January 1, 2016.

U. S. Steel believes that our major North American and many European integrated steel competitors are confronted with substantially similar environmental regulatory conditions and thus does not believe that its relative position with regard to such competitors will be materially affected by the impact of environmental laws and regulations. However, if future regulations do not recognize the fact that the integrated steel process involves a series of chemical reactions involving carbon that create CO2 emissions without linking these emissions to steel scrap as well, our competitive position relative to mini-mills will be adversely impacted. Our competitive position compared to producers in developing nations such as China, Russia, Ukraine and India, will be harmed unless such nations require commensurate reductions in CO2 emissions. Competing materials such as plastics may not be similarly impacted. The specific impact on each competitor will vary depending on a number of factors, including the age and location of its operating facilities and its production methods. U. S. Steel is also responsible for remediation costs related to former and present operating locations and disposal of environmentally sensitive materials. Many of our competitors, including North American producers, or their successors, that have been the subject of bankruptcy relief have no or substantially lower liabilities for such environmental remediation matters.

International Trade

U. S. Steel faces competition from non-U.S. steel producers, many of which are heavily subsidized by their governments and dump steel into the U.S. market. Trade-distorting policies and practices, coupled with global steel overcapacity, impact pricing in the U.S. market and influence the Company's ability to compete on a level playing field. Several

flat-rolled products were granted trade relief through a series of three trade cases which concluded during 2016.

U. S. Steel continues to lead the industry in efforts to address illegal dumping and subsidized imports that injure the economic health of our country, our Company and our workers.

On June 3, 2015, U. S. Steel filed antidumping (AD) and countervailing duty (CVD) cases against China, India, Italy, South Korea, and Taiwan for the import of unfairly traded corrosion-resistant steel (CORE). On June 2, 2016, the U.S. Department of Commerce (DOC) issued its affirmative CVD determinations against China, India, Italy, and South Korea, and affirmative AD determinations against China, India, Italy, South Korea, and Taiwan. On June 24, 2016, the U.S. International Trade Commission (USITC) determined that the U.S. industry is materially injured by reason of imports of CORE from all five countries. Following the USITC's affirmative determinations, the DOC published its AD and CVD orders on July 25, 2016. U.S. Customs and Border Protection (CBP) is now enforcing these decisions and collecting AD and CVD duties.

Shortly before the DOC published the final AD/CVD orders on CORE from China, imports of CORE from Vietnam surged dramatically. Suspecting that Chinese producers were diverting cold-rolled steel to Vietnam to undergo minor processing before exporting to the United States in an attempt to avoid paying the new duties, U. S. Steel and the other domestic producers filed a request on June 3, 2016, asking the DOC to conduct an anti-circumvention investigation. DOC initiated its investigation on November 14, 2016, and in December 2016 identified and sent questionnaires to Vietnamese producers, requesting confidential quantity and value information. The DOC received responses from Vietnamese producers on December 28, 2016. If the DOC determines that imports of CORE from China are being channeled through Vietnam, it will impose duties on Vietnamese imports of CORE. The entire proceeding should be completed within 300 days of the initiation date, unless the deadline is extended by the DOC.

On July 28, 2015, U. S. Steel filed AD and CVD petitions charging that unfairly-traded imports of cold-rolled steel products from Brazil, China, India, Japan, South Korea, the Netherlands, Russia, and the United Kingdom are causing material injury to the domestic industry and that the foreign producers in Brazil, China, India, South Korea, and Russia

26

benefit from numerous countervailable subsidies. On May 24, 2016, the DOC published its final determinations in the AD investigations against China and Japan and the CVD investigation against China. On June 22, 2016, the USITC announced its affirmative determinations against China and Japan on the basis of cumulated subject imports from all seven countries. The DOC published its AD and CVD order against China and Japan on July 14, 2016. For the remaining countries - Brazil, India, South Korea, Russia, and the United Kingdom - the DOC issued its final AD and CVD determinations on July 29, 2016, which was followed by a final affirmative injury determination by the USITC against Brazil, India, South Korea, and the United Kingdom. The DOC published its final AD and CVD orders on September 20, 2016. CBP is now enforcing these decisions and collecting AD duties on cold-rolled steel imports from Brazil, China, India, Japan, South Korea, and the United Kingdom, and CVD duties on imports from Brazil, China, India, and South Korea.

Following the publication of the AD/CVD orders, imports of cold-rolled steel from Vietnam significantly increased. Suspecting that Chinese producers were diverting cold-rolled steel to Vietnam to undergo minor processing before exporting to the United States in an attempt to avoid paying the new duties, U. S. Steel and several other domestic producers filed a request on September 27, 2016, for DOC to conduct an anti-circumvention investigation. The DOC initiated its investigation on November 14, 2016, and in December 2016 identified and sent questionnaires to Vietnamese producers, requesting confidential quantity and value information. The DOC received responses from Vietnamese producers on December 28, 2016. If the DOC determines that imports of cold-rolled steel from China are being redirected through Vietnam en route to the United States, it will impose duties on imports of cold-rolled steel from Vietnam. The entire proceeding should be completed within 300 days of the initiation date, unless the deadline is extended by the DOC.

On August 11, 2015, U. S. Steel filed AD and CVD petitions for the imposition of duties on hot-rolled coil from Australia, Brazil, Japan, South Korea, the Netherlands, Turkey, and the United Kingdom. On August 12, 2016, the DOC published affirmative final determinations in the CVD investigations against Brazil, South Korea, and Turkey and the AD investigations against Australia, Brazil, Japan, South Korea, the Netherlands, Turkey, and the United Kingdom. On September 12, 2016, the USITC announced its determination that the industry in the United States is materially injured by reason of imports of hot-rolled steel products from Australia, Brazil, Japan, South Korea, the Netherlands, and the United Kingdom, as well as subject imports from Turkey, that were sold in the United States at less than fair value. The DOC published AD and CVD orders on October 3, 2016.

At present, U. S. Steel is also involved in several appeals filed with the Court of International Trade from the OCTG cases. In addition to defending on-going appeals, U. S. Steel continues to be actively engaged in relevant administrative reviews and five-year ("sunset") reviews before the USITC and the DOC.

In April 2016, U. S. Steel launched a case under Section 337 of the Tariff Act of 1930 against ten of the eleven largest Chinese producers and their distributors. The complaint alleges three causes of action: 1) illegal conspiracy to fix prices and control output and export volumes; 2) the theft of trade secrets through industrial espionage; 3) circumvention of duties by false labeling and transshipment. On May 26, 2016, the USITC instituted an investigation on all three causes. The remedy sought in the petition is the barring of Chinese steel and alloy products from the U.S. market. Of the original forty named respondents, twenty Chinese producers and distributors failed to appear and defaults have been entered against them, including the ninth largest steel company in China (which is also the eighteenth largest in the world).

On November 14, 2016, the Administrative Law Judge (ALJ) initially granted Chinese respondent’s motion to dismiss U. S. Steel’s antitrust claim. On November 23, 2016, U. S. Steel petitioned for review of the ALJ’s determination granting the Respondent’s motion to terminate the antitrust claim. On December 19, 2016, the USITC announced it will review the ALJ’s determination and invited interested parties to file written submissions. The USITC is expected to issue a determination in the first quarter of 2017. Upon review of all written submissions, the USITC will also determine whether to conduct oral arguments, which, if granted, will be held on March 14, 2017.

On January 12, 2017, the ALJ granted the Respondent’s motion to dismiss U. S. Steel’s trans-shipment claim. On January 23, 2017, U. S. Steel filed a petition for review of that determination. The USITC is expected to decide whether to review the dismissal of this claim in the first quarter of 2017.

On February 15, 2017, U. S. Steel filed a motion to withdraw its trade secrets claim without prejudice and to stay all matters on this claim until the ALJ can rule on the motion. The motion is unopposed. The trade secrets claim was the only one of three claims that avoided dismissal by the ALJ. While Section 337 offers U.S. companies the ability to seek relief against unfair methods of competition and the items being unfairly imported as a result of those actions, the

27

decade's old law never contemplated the technological advancements over the past 50 years that have led to the proliferation of cyber theft and other cyber crimes committed against American companies. As such, the burdens imposed by the law are impracticable for corporate victims of cybercrime. U. S. Steel continues to advocate for legal reforms to address these issues and will revisit its trade secrets claim when the legal environment for such claims improves.

In the European Union (EU), USSK is participating in and cooperating with the European Commission's (EC) dumping action concerning hot-rolled steel flat products from China, which was initiated in February 2016. On October 6, 2016, the EC imposed provisional duties on hot-rolled steel flat products imported from China of between 13.2 and 22.6 percent. These duties are intended to offset the harm caused to the domestic steel industry by below-cost Chinese imports. The EC is expected to impose definitive duties in April 2017.

The EC initiated a concurrent subsidies investigation regarding hot-rolled steel flat products from China on May 13, 2016. The EC is expected to impose provisional duties to countervail unfair subsidies in February 2017.

On July 7, 2016, the EC opened an investigation against Russia, Ukraine, Serbia, Iran and Brazil to determine whether exporters of hot-rolled flat products from the subject countries sold in the EU below cost, and to assess whether the subject imports caused injury to the industry. If the case is successful, duties could be levied against hot-rolled steel products from the subject countries. The EC is expected to impose provisional duties in April 2017.

On February 13, 2016, the EC initiated an investigation to determine whether imports of heavy steel plate from China are being sold in the EU below cost, and to assess whether such imports are harming the domestic industry. On October 6, 2016, the EC imposed provisional dumping duties of between 65.1 and 73.7 percent on imports of heavy steel plate from China. The EC is expected to impose definitive duties in April 2017.

Also on February 13, 2016, the EC initiated a dumping investigation regarding seamless pipe and tube of non-stainless steel imported from China. On November 12, 2016, the EC imposed provisional dumping duties between 43.5 and 81.1 percent. The EC is expected to impose definitive duties in May 2017.

On December 9, 2016, the EC initiated an investigation to determine whether imported CORE from China is being sold in the EU below cost and to assess whether such imports are harming the domestic industry. The EC is expected to impose provisional duties in September 2017.

USSK actively participated in an investigation concerning cold-rolled steel flat products from China and Russia. On July 29, 2016, the EC imposed definitive dumping duties of between 19.7 and 22.1 percent against Chinese imports and between 18.7 and 36.1 percent against Russian imports of cold-rolled steel flat products.

On December 12, 2016, China filed a complaint at the World Trade Organization (WTO) against the United States and the European Union. The complaint alleges that the U.S. and EU are violating their treaty obligations by continuing to use the non-market economy (NME) methodology for price comparisons in antidumping duty investigations. China’s Accession Protocol, the agreement that China entered into in order to become a WTO Member, contemplated that China would have made the transition from NME to market economy by December 11, 2016. However, the U.S. and EU continue to find that China exercises too much control over its economy and have committed to continuing to use the NME methodology in AD investigations. U. S. Steel is actively monitoring this dispute as the outcome will impact all U.S. and EU dumping orders on Chinese goods, including many steel products.

U. S. Steel continually assesses the impact of imports from foreign countries on our business, and continues to execute a broad, global strategy to enhance the means and manner in which it competes in the U.S. market and internationally. In an effort to mitigate the negative impact of unfairly traded foreign imports on our business, U. S. Steel has commenced substantive work with regional trade partners and organizations, and outlined a robust engagement with the Administration to tackle global overcapacity. Across diverse platforms, U. S. Steel is leveraging its unique experience, knowledge, and reputation to forge alliances and partnerships to advance innovative structural changes to commercial and legal regimes to better position and support the U.S. steel industry in the 21st century and beyond.

28

Facilities and Locations

29

Flat-Rolled

During 2016, U. S. Steel continued to review and adjust its operating levels at several of its Flat-Rolled operations as a result of actions that were taken during 2015 in response to unfavorable market conditions, primarily driven by lower oil prices, lower steel prices, the impact of the stronger U.S. dollar, global overcapacity and imports on our operations. Customer order rates will determine the size and duration of any adjustments that we make at our Flat-Rolled operations during 2017.

The operating results of all facilities within U. S. Steel’s integrated steel plants in the U.S. are included in Flat-Rolled. These facilities include Gary Works, Great Lakes Works, Mon Valley Works and Granite City Works. During 2015, the steelmaking operations at the Fairfield Works facility were shut down. The operating results of U. S. Steel’s coke and iron ore pellet operations and many equity investees in the United States are also included in Flat-Rolled.

Gary Works, located in Gary, Indiana, has annual raw steel production capability of 7.5 million tons. Gary Works has four blast furnaces, six steelmaking vessels, a vacuum degassing unit and four slab casters. Finishing facilities include a hot strip mill, two pickling lines, two cold reduction mills, three temper mills, a double cold reduction line, four annealing facilities and two tin coating lines. Principal products include hot-rolled, cold-rolled and coated sheets and tin mill products. Gary Works also produces strip mill plate in coil. In May 2015, the one remaining coke battery at Gary Works was shut down.

The Midwest Plant, located in Portage, Indiana, processes hot-rolled and cold rolled bands and produces tin mill products, hot dip galvanized, cold-rolled and electrical lamination sheets. Midwest facilities include a currently idle pickling line, two cold reduction mills, two temper mills, a double cold reduction mill, two annealing facilities, two hot dip galvanizing lines, a tin coating line and a tin-free steel line.

East Chicago Tin is located in East Chicago, Indiana and produces tin mill products. Facilities include a pickling line, a cold reduction mill, two annealing facilities, a temper mill, a tin coating line and a tin-free steel line.

Great Lakes Works, located in Ecorse and River Rouge, Michigan, has annual raw steel production capability of 3.8 million tons. Great Lakes facilities include three blast furnaces, two steelmaking vessels, a vacuum degassing unit, two slab casters, a hot strip mill, a pickling line, a tandem cold reduction mill, three annealing facilities, a temper mill, a recoil and inspection line, two electrolytic galvanizing lines (one being the former Double Eagle Steel Coating Company's (DESCO) line) and a hot dip galvanizing line. Principal products include hot-rolled, cold-rolled and coated sheets.

Mon Valley Works consists of the Edgar Thomson Plant, located in Braddock, Pennsylvania; the Irvin Plant, located in West Mifflin, Pennsylvania; the Fairless Plant, located in Fairless Hills, Pennsylvania; and the Clairton Plant, located in Clairton, Pennsylvania. Mon Valley Works has annual raw steel production capability of 2.9 million tons. Facilities at the Edgar Thomson Plant include two blast furnaces, two steelmaking vessels, a vacuum degassing unit and a slab caster. Irvin Plant facilities include a hot strip mill, two pickling lines, a cold reduction mill, three annealing facilities, a temper mill and two hot dip galvanizing lines. The Fairless Plant operates a hot dip galvanizing line. Principal products from Mon Valley Works include hot-rolled, cold-rolled and coated sheets, as well as coke and coke by-products produced at the Clairton Plant.

The Clairton Plant is comprised of ten coke batteries with an annual coke production capacity of 4.3 million tons. Almost all of the coke we produce is consumed by U. S. Steel facilities, or swapped with other domestic steel producers. Coke by-products are sold to the chemicals and raw materials industries.

Granite City Works, located in Granite City, Illinois, has annual raw steel production capability of 2.8 million tons. Granite City’s facilities includes two blast furnaces, two steelmaking vessels, two slab casters, a hot strip mill, a pickling line, a tandem cold reduction mill, a hot dip galvanizing line and a hot dip galvanizing/Galvalume® line. Principal products include hot-rolled and coated sheets. Gateway Energy and Coke Company LLC (Gateway) constructed a coke plant, which began operating in October 2009 to supply Granite City Works under a 15 year agreement with Suncoke.

U. S. Steel owns and operates a cogeneration facility that utilizes by-products from the Gateway coke plant to generate heat and power. During December 2015, the Granite City Works steelmaking operations and hot strip mill were temporarily idled. In December 2016, U. S. Steel announced it would be restarting the hot strip mill in the first quarter of 2017.

Subsequent to the permanent shutdown of the steelmaking operations in August 2015, Fairfield Works, located in Fairfield, Alabama, consists of the #5 coating line.

30

U. S. Steel owns a Research and Technology Center located in Munhall, Pennsylvania (near Pittsburgh) where we carry out a wide range of applied research, development and technical support functions.

U. S. Steel also owns an automotive technical center in Troy, Michigan. This facility brings automotive sales, service, distribution and logistics services, product technology and applications research into one location. Much of U. S. Steel’s work in developing new grades of steel to meet the demands of automakers for high-strength, light-weight and formable materials is carried out at this location.

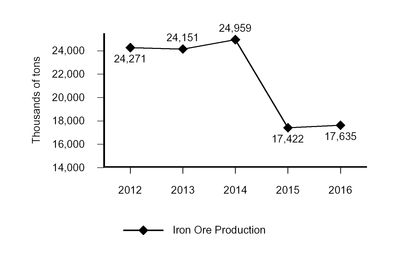

U. S. Steel has iron ore pellet operations located at Mt. Iron (Minntac) and Keewatin (Keetac), Minnesota with annual iron ore pellet production capability of 22.4 million tons. During 2016, 2015 and 2014, these operations produced 15.0 million, 15.5 million and 22.2 million tons of iron ore pellets, respectively. The Keetac Iron Ore Operations restarted production in the first quarter of 2017. It had previously been idle since May of 2015 due to significantly lower steel production.

Joint Ventures Within Flat-Rolled

U. S. Steel participates in a number of joint ventures that are included in Flat-Rolled, most of which are conducted through subsidiaries or other separate legal entities. All of these joint ventures are accounted for under the equity method. The significant joint ventures and other investments are described below. For information regarding joint ventures and other investments, see Note 11 to the Consolidated Financial Statements.

U. S. Steel has a 14.7 percent ownership interest in Hibbing Taconite Company (Hibbing), which is based in Hibbing, Minnesota. Hibbing’s rated annual production capability is 9.1 million tons of iron ore pellets, of which our share is about 1.3 million tons.

U. S. Steel has a 15 percent ownership interest in Tilden Mining Company (Tilden), which is based in Ishpeming, Michigan. Tilden’s rated annual production capability is 8.7 million tons of iron ore pellets, of which our share is about 1.3 million tons.

U. S. Steel and POSCO of South Korea participate in a 50-50 joint venture, USS-POSCO Industries (UPI), located in Pittsburg, California. The joint venture markets sheet and tin mill products, principally in the western United States. UPI produces cold-rolled sheets, galvanized sheets, tin plate and tin-free steel from hot bands principally provided by POSCO and U. S. Steel. UPI’s annual production capability is approximately 1.5 million tons.

U. S. Steel and Kobe Steel, Ltd. of Japan participate in a 50-50 joint venture, PRO-TEC Coating Company

(PRO-TEC). PRO-TEC owns and operates two hot dip galvanizing lines and a continuous annealing line (CAL) in Leipsic, Ohio, which primarily serve the automotive industry. PRO-TEC’s annual production capability is approximately 1.5 million tons. U. S. Steel's domestic production facilities supply PRO-TEC with cold-rolled sheets and U. S. Steel markets all of PRO-TEC's products. The CAL produces high strength, lightweight steels that are an integral component in automotive manufacturing as vehicle emission and safety requirements become increasingly stringent.

U. S. Steel and ArcelorMittal participate in the Double G Coatings Company, L.P. a 50-50 joint venture (Double G), which operates a hot dip galvanizing and Galvalume® facility located near Jackson, Mississippi and primarily serves the construction industry. Double G processes steel supplied by each partner and each partner markets the steel it has processed by Double G. Double G’s annual production capability is approximately 315,000 tons.