Wave Life Sciences Ltd. - Quarter Report: 2018 September (Form 10-Q)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

|

☒ |

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2018

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ______ to ______

Commission File No. 001-37627

WAVE LIFE SCIENCES LTD.

(Exact name of registrant as specified in its charter)

|

Singapore (State or other jurisdiction of incorporation or organization) |

|

Not applicable (I.R.S. Employer Identification No.) |

|

|

|

|

|

7 Straits View #12-00, Marina One East Tower Singapore (Address of principal executive offices) |

|

018936 (Zip Code) |

|

|

+65 6236 3388 (Registrant’s telephone number) |

|

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of ‘‘large accelerated filer,’’ ‘‘accelerated filer,’’ ‘‘smaller reporting company,’’ and ‘‘emerging growth company’’ in Rule 12b–2 of the Exchange Act.

|

Large accelerated filer |

☐ |

|

Accelerated filer |

☒ |

|

Non-accelerated filer |

☐ |

|

Smaller reporting company |

☐ |

|

|

|

|

Emerging growth company |

☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The number of outstanding ordinary shares of the registrant as of November 1, 2018 was 29,463,722.

QUARTERLY REPORT ON FORM 10-Q

TABLE OF CONTENTS

2

PART I - FINANCIAL INFORMATION

UNAUDITED CONSOLIDATED BALANCE SHEETS

(In thousands, except share amounts)

|

|

|

September 30, 2018 |

|

|

December 31, 2017 |

|

||

|

Assets |

|

|

|

|

|

|

|

|

|

Current assets: |

|

|

|

|

|

|

|

|

|

Cash and cash equivalents |

|

$ |

210,489 |

|

|

$ |

142,503 |

|

|

Current portion of accounts receivable |

|

|

10,000 |

|

|

|

1,000 |

|

|

Prepaid expenses and other current assets |

|

|

12,672 |

|

|

|

6,985 |

|

|

Total current assets |

|

|

233,161 |

|

|

|

150,488 |

|

|

Long-term assets: |

|

|

|

|

|

|

|

|

|

Accounts receivable, net of current portion |

|

|

50,000 |

|

|

|

— |

|

|

Property and equipment, net |

|

|

37,722 |

|

|

|

27,334 |

|

|

Restricted cash |

|

|

3,620 |

|

|

|

3,610 |

|

|

Other assets |

|

|

74 |

|

|

|

411 |

|

|

Total long-term assets |

|

|

91,416 |

|

|

|

31,355 |

|

|

Total assets |

|

$ |

324,577 |

|

|

$ |

181,843 |

|

|

Liabilities, Series A preferred shares and shareholders’ equity |

|

|

|

|

|

|

|

|

|

Current liabilities: |

|

|

|

|

|

|

|

|

|

Accounts payable |

|

$ |

11,961 |

|

|

$ |

7,598 |

|

|

Accrued expenses and other current liabilities |

|

|

9,518 |

|

|

|

8,898 |

|

|

Current portion of capital lease obligation |

|

|

— |

|

|

|

16 |

|

|

Current portion of deferred rent |

|

|

90 |

|

|

|

60 |

|

|

Current portion of deferred revenue |

|

|

103,229 |

|

|

|

1,275 |

|

|

Current portion of lease incentive obligation |

|

|

997 |

|

|

|

344 |

|

|

Total current liabilities |

|

|

125,795 |

|

|

|

18,191 |

|

|

Long-term liabilities: |

|

|

|

|

|

|

|

|

|

Deferred rent, net of current portion |

|

|

5,084 |

|

|

|

4,214 |

|

|

Deferred revenue, net of current portion |

|

|

69,494 |

|

|

|

7,241 |

|

|

Lease incentive obligation, net of current portion |

|

|

8,229 |

|

|

|

3,094 |

|

|

Other liabilities |

|

|

1,495 |

|

|

|

1,619 |

|

|

Total long-term liabilities |

|

|

84,302 |

|

|

|

16,168 |

|

|

Total liabilities |

|

$ |

210,097 |

|

|

$ |

34,359 |

|

|

Series A preferred shares, no par value; 3,901,348 shares issued and outstanding at September 30, 2018 and December 31, 2017 |

|

$ |

7,874 |

|

|

$ |

7,874 |

|

|

Shareholders’ equity: |

|

|

|

|

|

|

|

|

|

Ordinary shares, no par value; 29,426,176 and 27,829,079 shares issued and outstanding at September 30, 2018 and December 31, 2017, respectively |

|

$ |

374,502 |

|

|

$ |

310,038 |

|

|

Additional paid-in capital |

|

|

33,757 |

|

|

|

22,172 |

|

|

Accumulated other comprehensive income |

|

|

181 |

|

|

|

116 |

|

|

Accumulated deficit |

|

|

(301,834 |

) |

|

|

(192,716 |

) |

|

Total shareholders’ equity |

|

$ |

106,606 |

|

|

$ |

139,610 |

|

|

Total liabilities, Series A preferred shares and shareholders’ equity |

|

$ |

324,577 |

|

|

$ |

181,843 |

|

The accompanying notes are an integral part of the unaudited consolidated financial statements.

3

UNAUDITED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS

(In thousands, except share and per share amounts)

|

|

|

Three Months Ended September 30, |

|

|

Nine Months Ended September 30, |

|

||||||||||

|

|

|

2018 |

|

|

2017 |

|

|

2018 |

|

|

2017 |

|

||||

|

Revenue |

|

$ |

4,493 |

|

|

$ |

1,315 |

|

|

$ |

10,794 |

|

|

$ |

2,795 |

|

|

Operating expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Research and development |

|

|

32,876 |

|

|

|

20,097 |

|

|

|

94,619 |

|

|

|

53,940 |

|

|

General and administrative |

|

|

9,849 |

|

|

|

7,571 |

|

|

|

26,755 |

|

|

|

20,088 |

|

|

Total operating expenses |

|

|

42,725 |

|

|

|

27,668 |

|

|

|

121,374 |

|

|

|

74,028 |

|

|

Loss from operations |

|

|

(38,232 |

) |

|

|

(26,353 |

) |

|

|

(110,580 |

) |

|

|

(71,233 |

) |

|

Other income (expense), net: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dividend income |

|

|

1,064 |

|

|

|

515 |

|

|

|

2,354 |

|

|

|

1,287 |

|

|

Interest income (expense), net |

|

|

5 |

|

|

|

1 |

|

|

|

16 |

|

|

|

5 |

|

|

Other income (expense), net |

|

|

(468 |

) |

|

|

(75 |

) |

|

|

(384 |

) |

|

|

(211 |

) |

|

Total other income (expense), net |

|

|

601 |

|

|

|

441 |

|

|

|

1,986 |

|

|

|

1,081 |

|

|

Loss before income taxes |

|

|

(37,631 |

) |

|

|

(25,912 |

) |

|

|

(108,594 |

) |

|

|

(70,152 |

) |

|

Income tax benefit (provision) |

|

|

— |

|

|

|

418 |

|

|

|

(172 |

) |

|

|

(1,035 |

) |

|

Net loss |

|

$ |

(37,631 |

) |

|

$ |

(25,494 |

) |

|

$ |

(108,766 |

) |

|

$ |

(71,187 |

) |

|

Net loss per share attributable to ordinary shareholders—basic and diluted |

|

$ |

(1.28 |

) |

|

$ |

(0.92 |

) |

|

$ |

(3.78 |

) |

|

$ |

(2.73 |

) |

|

Weighted-average ordinary shares used in computing net loss per share attributable to ordinary shareholders—basic and diluted |

|

|

29,333,994 |

|

|

|

27,758,792 |

|

|

|

28,804,357 |

|

|

|

26,078,696 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other comprehensive income (loss): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net loss |

|

$ |

(37,631 |

) |

|

$ |

(25,494 |

) |

|

$ |

(108,766 |

) |

|

$ |

(71,187 |

) |

|

Foreign currency translation |

|

|

(20 |

) |

|

|

1 |

|

|

|

65 |

|

|

|

19 |

|

|

Comprehensive loss |

|

$ |

(37,651 |

) |

|

$ |

(25,493 |

) |

|

$ |

(108,701 |

) |

|

$ |

(71,168 |

) |

The accompanying notes are an integral part of the unaudited consolidated financial statements.

4

UNAUDITED CONSOLIDATED STATEMENTS OF CASH FLOWS

(In thousands)

|

|

|

Nine Months Ended September 30, |

|

|||||

|

|

|

2018 |

|

|

2017 |

|

||

|

Cash flows from operating activities |

|

|

|

|

|

|

|

|

|

Net loss |

|

$ |

(108,766 |

) |

|

$ |

(71,187 |

) |

|

Adjustments to reconcile net loss to net cash provided by (used in) operating activities: |

|

|

|

|

|

|

|

|

|

Amortization of lease incentive obligation |

|

|

(501 |

) |

|

|

(131 |

) |

|

Depreciation of property and equipment |

|

|

3,867 |

|

|

|

1,266 |

|

|

Share-based compensation expense |

|

|

11,585 |

|

|

|

8,966 |

|

|

Net (gain) loss on disposal of property and equipment |

|

|

44 |

|

|

|

— |

|

|

Deferred rent |

|

|

900 |

|

|

|

3,207 |

|

|

Deferred income taxes |

|

|

— |

|

|

|

904 |

|

|

Changes in operating assets and liabilities: |

|

|

|

|

|

|

|

|

|

Accounts receivable |

|

|

(59,000 |

) |

|

|

— |

|

|

Prepaid expenses and other current assets |

|

|

(5,687 |

) |

|

|

(3,887 |

) |

|

Other non-current assets |

|

|

(15 |

) |

|

|

(7 |

) |

|

Accounts payable |

|

|

2,801 |

|

|

|

624 |

|

|

Accrued expenses and other current liabilities |

|

|

647 |

|

|

|

1,898 |

|

|

Deferred revenue |

|

|

164,207 |

|

|

|

(2,795 |

) |

|

Other non-current liabilities |

|

|

(124 |

) |

|

|

225 |

|

|

Net cash provided by (used in) operating activities |

|

|

9,958 |

|

|

|

(60,917 |

) |

|

Cash flows from investing activities |

|

|

|

|

|

|

|

|

|

Purchases of property and equipment |

|

|

(6,475 |

) |

|

|

(14,808 |

) |

|

Net cash used in investing activities |

|

|

(6,475 |

) |

|

|

(14,808 |

) |

|

Cash flows from financing activities |

|

|

|

|

|

|

|

|

|

Proceeds from issuance of ordinary shares, net of offering costs |

|

|

60,000 |

|

|

|

93,509 |

|

|

Payments on capital lease obligation |

|

|

(16 |

) |

|

|

(47 |

) |

|

Proceeds from the exercise of share options |

|

|

4,464 |

|

|

|

323 |

|

|

Net cash provided by financing activities |

|

|

64,448 |

|

|

|

93,785 |

|

|

Effect of foreign exchange rates on cash, cash equivalents and restricted cash |

|

|

65 |

|

|

|

118 |

|

|

Net increase in cash, cash equivalents and restricted cash |

|

|

67,996 |

|

|

|

18,178 |

|

|

Cash, cash equivalents and restricted cash, beginning of period |

|

|

146,113 |

|

|

|

153,894 |

|

|

Cash, cash equivalents and restricted cash, end of period |

|

$ |

214,109 |

|

|

$ |

172,072 |

|

|

Supplemental disclosure of cash flow information: |

|

|

|

|

|

|

|

|

|

Cash paid for taxes, net of refunds |

|

$ |

438 |

|

|

$ |

211 |

|

|

Property and equipment purchases in accounts payable and accrued expenses at period end |

|

$ |

1,853 |

|

|

$ |

1,419 |

|

|

Tenant improvements paid for by the landlord during the period |

|

$ |

2,732 |

|

|

$ |

2,774 |

|

|

Tenant improvements to be reimbursed by the landlord |

|

$ |

4,302 |

|

|

$ |

— |

|

The accompanying notes are an integral part of the unaudited consolidated financial statements.

5

Notes to Unaudited Consolidated Financial Statements

1. THE COMPANY

Organization

Wave Life Sciences Ltd. (together with its subsidiaries, “Wave” or the “Company”) is a biotechnology company with an innovative and proprietary synthetic chemistry drug development platform that the Company is using to rationally design, develop and commercialize a broad pipeline of first-in-class or best-in-class nucleic acid therapeutic candidates for genetically defined diseases. Nucleic acid therapeutics are a growing and innovative class of drugs that have the potential to address diseases that have historically been difficult to treat with small molecule drugs or biologics. Nucleic acid therapeutics, or oligonucleotides, are comprised of a sequence of nucleotides that are linked together by a backbone of chemical bonds. The Company is initially developing oligonucleotides that target genetic defects to either reduce the expression of disease-promoting proteins or transform the production of dysfunctional mutant proteins into the production of functional proteins.

The Company was incorporated in Singapore on July 23, 2012 and has its principal U.S. office in Cambridge, Massachusetts. The Company was incorporated with the purpose of combining two commonly held companies, Wave Life Sciences USA, Inc. (“Wave USA”), a Delaware corporation (formerly Ontorii, Inc.), and Wave Life Sciences Japan, Inc. (“Wave Japan”), a company organized under the laws of Japan (formerly Chiralgen., Ltd.), which occurred on September 13, 2012. On May 31, 2016, Wave Life Sciences Ireland Limited (“Wave Ireland”) was formed as a wholly-owned subsidiary of Wave Life Sciences Ltd. On April 3, 2017, Wave Life Sciences UK Limited (“Wave UK”) was formed as a wholly-owned subsidiary of Wave Life Sciences Ltd.

The Company’s primary activities since inception have been developing an innovative and proprietary synthetic chemistry drug development platform to design, develop and commercialize nucleic acid therapeutic programs, advancing the Company’s neurology franchise, expanding the Company’s research and development activities into additional therapeutic areas including ophthalmology and hepatic, advancing programs into the clinic, furthering clinical development of such clinical-stage programs, building the Company’s intellectual property, recruiting personnel and assuring adequate capital to support these activities.

Risks and Uncertainties

The Company is subject to risks common to companies in the biotechnology industry including, but not limited to, new technological innovations, protection of proprietary technology, establishment of internal manufacturing capabilities, dependence on key personnel, compliance with government regulations and the need to obtain additional financing. The Company’s therapeutic programs will require significant additional research and development efforts, including extensive preclinical and clinical testing and regulatory approval, prior to commercialization of any product candidates. These efforts require significant amounts of additional capital, adequate personnel infrastructure and extensive compliance-reporting capabilities. There can be no assurance that the Company’s research and development will be successfully completed, that adequate protection for the Company’s intellectual property will be obtained, that any products developed will obtain necessary government regulatory approval or that any approved products will be commercially viable. Even if the Company’s product development efforts are successful, it is uncertain when, if ever, the Company will generate significant revenue from product sales. The Company operates in an environment of rapid change in technology and substantial competition from pharmaceutical and biotechnology companies. In addition, the Company is dependent upon the services of its employees and consultants.

Basis of Presentation

The Company has prepared the accompanying consolidated financial statements in conformity with generally accepted accounting principles in the United States of America (“U.S. GAAP”) and in U.S. dollars.

6

2. SIGNIFICANT ACCOUNTING POLICIES

The significant accounting policies described in the Company’s audited financial statements as of and for the year ended December 31, 2017, and the notes thereto, which are included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2017, filed with the Securities and Exchange Commission (“SEC”) on March 12, 2018, as amended (the “2017 Annual Report on Form 10-K”), have had no material changes during the three and nine months ended September 30, 2018, other than the Company’s adoption of ASC 606 (as defined below) which is discussed in detail in this note.

Unaudited Interim Financial Data

The accompanying interim consolidated balance sheet as of September 30, 2018, the related interim consolidated statements of operations and comprehensive loss for the three and nine months ended September 30, 2018 and 2017 and cash flows for the nine months ended September 30, 2018 and 2017, and the related interim information contained within the notes to the consolidated financial statements have been prepared in accordance with the rules and regulations of the SEC for interim financial information. Accordingly, they do not include all of the information and the notes required by U.S. GAAP for complete financial statements. The financial data and other information disclosed in these notes related to the three and nine months ended September 30, 2018 and 2017 are unaudited. In the opinion of management, the unaudited interim consolidated financial statements reflect all adjustments, consisting of normal and recurring adjustments, necessary for the fair presentation of the Company’s financial position and results of operations for the three and nine months ended September 30, 2018 and 2017. The results of operations for the interim periods are not necessarily indicative of the results to be expected for the year ending December 31, 2018 or any other interim period or future year or period.

Principles of Consolidation

The Company’s consolidated financial statements include the accounts of the Company and its wholly-owned subsidiaries. All significant intercompany balances and transactions have been eliminated in consolidation.

Revenue Recognition

Effective January 1, 2018, the Company adopted Accounting Standards Codification (“ASC”) Topic 606, Revenue from Contracts with Customers (“ASC 606”), using the full retrospective transition method. Under this method, the Company revised its consolidated financial statements for the years ended December 31, 2017 and 2016, and applicable interim periods within those years, as if ASC 606 had been effective for those periods. This standard applies to all contracts with customers, except for contracts that are within the scope of other standards, such as leases, insurance, and financial instruments. Under ASC 606, an entity recognizes revenue when its customer obtains control of promised goods or services, in an amount that reflects the consideration that the entity expects to receive in exchange for those goods or services. To determine revenue recognition for arrangements that an entity determines are within the scope of ASC 606, the entity performs the following five-step analysis: (i) identify the contract(s) with a customer; (ii) identify the performance obligations in the contract; (iii) determine the transaction price; (iv) allocate the transaction price to the performance obligations in the contract; and (v) recognize revenue when (or as) the entity satisfies a performance obligation. The Company only applies the five-step analysis to contracts when it is probable that the entity will collect the consideration to which it is entitled in exchange for the goods or services it transfers to the customer. At contract inception, once the contract is determined to be within the scope of ASC 606, the Company assesses the goods or services promised within each contract, determines those that are performance obligations, and assesses whether each promised good or service is distinct. The Company then recognizes as revenue the amount of the transaction price that is allocated to the respective performance obligation when (or as) the performance obligation is satisfied.

The Company has entered into collaboration agreements for research, development, and commercial services, under which the Company licenses certain rights to its product candidates to third parties. The terms of these arrangements typically include payment to the Company of one or more of the following: non-refundable, upfront license fees; reimbursement of certain costs; customer option exercise fees; development, regulatory and commercial milestone payments; and royalties on net sales of licensed products. Any variable consideration is constrained, and therefore, the cumulative revenue associated with this consideration is not recognized until it is deemed not to be at significant risk of reversal.

In determining the appropriate amount of revenue to be recognized as the Company fulfills its obligations under each of its agreements for which the collaboration partner is also a customer, the Company performs the following steps: (i) identification of the promised goods or services in the contract; (ii) determination of whether the promised goods or services are performance obligations, including whether they are distinct in the context of the contract; (iii) measurement of the transaction price, including the constraint on variable consideration; (iv) allocation of the transaction price to the performance obligations; and (v) recognition of revenue when (or as) the Company satisfies each performance obligation. As part of the accounting for these arrangements, the Company must use significant judgment to determine: (a) the number of performance obligations based on the determination under step (ii) above; (b) the transaction price under step (iii) above; and (c) the timing of satisfaction of performance obligations as a measure of progress in step (v) above. The Company uses significant judgment to determine whether milestones or other variable consideration, except for royalties, should be included in the transaction price as described further below. The transaction price is allocated to the optional goods and services the Company expects to provide. The Company uses estimates to determine the timing of satisfaction of performance obligations.

7

Amounts received prior to revenue recognition are recorded as deferred revenue. Amounts expected to be recognized as revenue within the 12 months following the balance sheet date are classified as current portion of deferred revenue in the accompanying consolidated balance sheets. Amounts not expected to be recognized as revenue within the 12 months following the balance sheet date are classified as deferred revenue, net of current portion.

Licenses of intellectual property: In assessing whether a promise or performance obligation is distinct from the other promises, the Company considers factors such as the research, development, manufacturing and commercialization capabilities of the customer and the availability of the associated expertise in the general marketplace. In addition, the Company considers whether the customer can benefit from a promise for its intended purpose without the receipt of the remaining promise, whether the value of the promise is dependent on the unsatisfied promise, whether there are other vendors that could provide the remaining promise, and whether it is separately identifiable from the remaining promise. For licenses that are combined with other promises, the Company utilizes judgment to assess the nature of the combined performance obligation to determine whether the combined performance obligation is satisfied over time or at a point in time and, if over time, the appropriate method of measuring progress for purposes of recognizing revenue. The Company evaluates the measure of progress each reporting period and, if necessary, adjusts the measure of performance and related revenue recognition.

Research and development services: If an arrangement is determined to contain a promise or obligation for the company to perform research and development services, the Company must determine whether these services are distinct from other promises in the arrangement. In assessing whether the services are distinct from the other promises, the Company considers the capabilities of the customer to perform these same services. In addition, the Company considers whether the customer can benefit from a promise for its intended purpose without the receipt of the remaining promise, whether the value of the promise is dependent on the unsatisfied promise, whether there are other vendors that could provide the remaining promise, and whether it is separately identifiable from the remaining promise. For research and development services that are combined with other promises, the Company utilizes judgment to assess the nature of the combined performance obligation to determine whether the combined performance obligation is satisfied over time or at a point in time and, if over time, the appropriate method of measuring progress for purposes of recognizing revenue. The Company evaluates the measure of progress each reporting period and, if necessary, adjusts the measure of performance and related revenue recognition.

Customer options: If an arrangement is determined to contain customer options that allow the customer to acquire additional goods or services, the goods and services underlying the customer options are not considered to be performance obligations at the outset of the arrangement, as they are contingent upon option exercise. The Company evaluates the customer options for material rights, that is, the option to acquire additional goods or services for free or at a discount. If the customer options are determined to represent a material right, the material right is recognized as a separate performance obligation at the outset of the arrangement. The Company allocates the transaction price to material rights based on the standalone selling price. As a practical alternative to estimating the standalone selling price when the goods or services are both (i) similar to the original goods and services in the contract and (ii) provided in accordance with the terms of the original contract, the Company allocates the total amount of consideration expected to be received from the customer to the total goods or services expected to be provided to the customer. Amounts allocated to any material right are not recognized as revenue until the option is exercised and the performance obligation is satisfied.

Milestone payments: At the inception of each arrangement that includes milestone payments, the Company evaluates whether a significant reversal of cumulative revenue provided in conjunction with achieving the milestones is probable, and estimates the amount to be included in the transaction price using the most likely amount method. If it is probable that a significant reversal of cumulative revenue would not occur, the associated milestone value is included in the transaction price. Milestone payments that are not within the control of the Company or the licensee, such as regulatory approvals, are not considered probable of being achieved until those approvals are received. For other milestones, the Company evaluates factors such as the scientific, clinical, regulatory, commercial, and other risks that must be overcome to achieve the particular milestone in making this assessment. There is considerable judgment involved in determining whether it is probable that a significant reversal of cumulative revenue would not occur. At the end of each subsequent reporting period, the Company reevaluates the probability of achievement of all milestones subject to constraint and, if necessary, adjusts its estimate of the overall transaction price. Any such adjustments are recorded on a cumulative catch-up basis, which would affect revenues and earnings in the period of adjustment.

Royalties: For arrangements that include sales-based royalties, including milestone payments based on a level of sales, and the license is deemed to be the predominant item to which the royalties relate, the Company recognizes revenue at the later of (i) when the related sales occur, or (ii) when the performance obligation to which some or all of the royalty has been allocated has been satisfied (or partially satisfied). To date, the Company has not recognized any royalty revenue resulting from any of its licensing arrangements.

Contract costs: The Company recognizes as an asset the incremental costs of obtaining a contract with a customer if the costs are expected to be recovered. As a practical expedient, the Company recognizes the incremental costs of obtaining a contract as an expense when incurred if the amortization period of the asset that it otherwise would have recognized is one year or less. To date, the Company has not incurred any incremental costs of obtaining a contract with a customer.

For additional discussion of accounting for collaboration revenues, see Note 4, “Collaboration Agreements.”

8

Recently Issued Accounting Pronouncements

The recently issued accounting pronouncements described in the Company’s audited financial statements as of and for the year ended December 31, 2017, and the notes thereto, which are included in the 2017 Annual Report on Form 10-K, have had no material changes during the nine months ended September 30, 2018, except as described below.

In February 2016, the Financial Accounting Standards Board (the “FASB”) issued Accounting Standards Update (“ASU”) No. 2016-02, Leases (“ASU 2016-02”), which was further clarified in July 2018 when the FASB issued Accounting Standards Update No. 2018-10, Codification Improvements to Topic 842, Leases (“ASU 2018-10”) and Accounting Standards Update No. 2018-11, Leases (Topic 842)—Targeted Improvements (“ASU 2018-11”). ASU 2016-02, ASU 2018-10 and ASU 2018-11 require a lessee to recognize assets and liabilities on the balance sheet for operating leases and changes many key definitions, including the definition of a lease. The update includes a short-term lease exception for leases with a term of 12 months or less, in which a lessee can make an accounting policy election not to recognize lease assets and lease liabilities. Lessees will continue to differentiate between finance leases (previously referred to as capital leases) and operating leases, using classification criteria that are substantially similar to the previous guidance. For lessees, the recognition, measurement, and presentation of expenses and cash flows arising from a lease have not significantly changed from previous U.S. GAAP. Lessees and lessors are required to recognize and measure leases at the beginning of the earliest period presented using a modified retrospective approach. The modified retrospective approach includes a number of optional practical expedients that entities may elect to apply, as well as transition guidance specific to nonstandard leasing transactions. ASU 2016-02, ASU 2018-10 and ASU 2018-11 are effective for fiscal years beginning after December 15, 2018, and interim periods within those fiscal years. The Company is currently evaluating the impact of adopting ASU 2016-02, ASU 2018-10 and ASU 2018-11 on its consolidated financial statements.

In February 2018, the FASB issued Accounting Standards Update No. 2018-02, Income Statement—Reporting Comprehensive Income (Topic 220): Reclassification of Certain Tax Effects from Accumulated Other Comprehensive Income (“ASU 2018-02”), which allows companies to make a one-time reclassification of the stranded tax effects (as defined by ASU 2018-02) from accumulated other comprehensive income to retained earnings as a result of the tax legislation enacted in December 2017, commonly known as the “Tax Cuts and Jobs Act” (the “Tax Act”), and requires certain disclosures about the stranded tax effects. The new guidance is effective for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years. The Company is currently evaluating the potential impact that the adoption of ASU 2018-02 may have on its consolidated financial statements.

In March 2018, the FASB issued Accounting Standards Update No. 2018-05, Income Taxes (Topic 740): Amendments to SEC Paragraphs Pursuant to SEC Staff Accounting Bulletin No. 118 (“ASU 2018-05”). The standard amends Accounting Standards Codification 740, Income Taxes (“ASC 740”), to provide guidance on accounting for the tax effects of the Tax Act pursuant to Staff Accounting Bulletin No. 118. The Company is currently evaluating the new guidance included in ASU 2018-05, but does not expect it to have a material impact on its consolidated financial statements.

In November 2018, the FASB issued Accounting Standards Update No. 2018-18, Collaborative Arrangements (Topic 808): Clarifying the Interaction between Topic 808 and Topic 606 (“ASU 2018-18”). The standard amends Accounting Standards Codification 808, Collaborative Agreements and Accounting Standards Codification 606, Revenue from Contracts with Customers, to clarify the interaction between collaborative arrangement participants that should be accounted for as revenue under ASC 606. In transactions when the collaborative arrangement participant is a customer in the context of a unit of account, revenue should be accounted for using the guidance in Topic 606. The amendments in Update No. 2018-18 are effective for fiscal years beginning after December 15, 2019, and interim periods within those fiscal years. The Company is currently evaluating the new guidance included in ASU 2018-18, but does not expect it to have a material impact on its consolidated financial statements.

Recently Adopted Accounting Pronouncements

In May 2014, the FASB issued Accounting Standards Update No. 2014-09, which amends the guidance for accounting for revenue from contracts with customers. This ASU supersedes the revenue recognition requirements in ASC Topic 605, Revenue Recognition, (“ASC 605”), and creates a new topic, ASC 606, Revenue from Contracts with Customers. In 2015 and 2016, the FASB issued additional ASUs related to ASC 606 that delayed the effective date of the guidance and clarified various aspects of the new revenue guidance, including principal versus agent considerations, identifying performance obligations, and licensing, and they include other improvements and practical expedients. The Company adopted this new standard on January 1, 2018 using the full retrospective transition method.

9

As a result of adopting ASC 606 on January 1, 2018, the Company has revised its comparative financial statements for the prior year as if ASC 606 had been effective for that period. As a result, the following financial statement line items for fiscal year 2017 were affected.

|

Condensed Consolidated Balance Sheets |

|

|||||||||||

|

|

|

As of December 31, 2017 |

|

|||||||||

|

|

|

As revised under ASC 606 |

|

|

As originally reported under ASC 605 |

|

|

Effect of change |

|

|||

|

|

|

(in thousands) |

|

|||||||||

|

Current portion of deferred revenue |

|

$ |

1,275 |

|

|

$ |

2,705 |

|

|

$ |

(1,430 |

) |

|

Deferred revenue, net of current portion |

|

|

7,241 |

|

|

|

5,607 |

|

|

|

1,634 |

|

|

Accumulated deficit |

|

|

(192,716 |

) |

|

|

(192,512 |

) |

|

|

(204 |

) |

|

Condensed Consolidated Statements of Operations and Comprehensive Loss |

|

|||||||||||

|

|

|

Three Months Ended September 30, 2017 |

|

|||||||||

|

|

|

As revised under ASC 606 |

|

|

As originally reported under ASC 605 |

|

|

Effect of change |

|

|||

|

|

|

(in thousands, except per share data) |

|

|||||||||

|

Revenue |

|

$ |

1,315 |

|

|

$ |

676 |

|

|

$ |

639 |

|

|

Loss from operations |

|

|

(26,353 |

) |

|

|

(26,992 |

) |

|

|

639 |

|

|

Income tax benefit (provision) |

|

|

418 |

|

|

|

416 |

|

|

|

2 |

|

|

Net loss |

|

|

(25,494 |

) |

|

|

(26,135 |

) |

|

|

641 |

|

|

Net loss per share attributable to ordinary shareholders—basic and diluted |

|

$ |

(0.92 |

) |

|

$ |

(0.94 |

) |

|

$ |

0.02 |

|

|

|

|

Nine Months Ended September 30, 2017 |

|

|||||||||

|

|

|

As revised under ASC 606 |

|

|

As originally reported under ASC 605 |

|

|

Effect of change |

|

|||

|

|

|

(in thousands, except per share data) |

|

|||||||||

|

Revenue |

|

$ |

2,795 |

|

|

$ |

2,028 |

|

|

$ |

767 |

|

|

Loss from operations |

|

$ |

(71,233 |

) |

|

|

(72,000 |

) |

|

|

767 |

|

|

Income tax benefit (provision) |

|

|

(1,035 |

) |

|

|

(905 |

) |

|

|

(130 |

) |

|

Net loss |

|

|

(71,187 |

) |

|

|

(71,824 |

) |

|

|

637 |

|

|

Net loss per share attributable to ordinary shareholders—basic and diluted |

|

$ |

(2.73 |

) |

|

$ |

(2.75 |

) |

|

$ |

0.02 |

|

|

Condensed Consolidated Statement of Cash Flows |

|

|||||||||||

|

|

|

Nine Months Ended September 30, 2017 |

|

|||||||||

|

|

|

As revised under ASC 606 |

|

|

As originally reported under ASC 605 |

|

|

Effect of change |

|

|||

|

|

|

(in thousands) |

|

|||||||||

|

Net loss |

|

$ |

(71,187 |

) |

|

$ |

(71,824 |

) |

|

$ |

637 |

|

|

Adjustments to reconcile net loss to net cash provided by (used in) operating activities: |

|

|||||||||||

|

Deferred income taxes |

|

|

904 |

|

|

|

774 |

|

|

|

130 |

|

|

Changes in operating assets and liabilities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Deferred revenue |

|

|

(2,795 |

) |

|

|

(2,028 |

) |

|

|

(767 |

) |

|

Net cash provided by (used in) operating activities |

|

|

(60,917 |

) |

|

|

(60,917 |

) |

|

|

— |

|

|

Cash, cash equivalents and restricted cash, beginning of period |

|

|

153,894 |

|

|

|

153,894 |

|

|

|

— |

|

|

Cash, cash equivalents and restricted cash, end of period |

|

|

172,072 |

|

|

|

172,072 |

|

|

|

— |

|

The most significant changes relate to the Company’s revenue recognition pattern for the Pfizer Collaboration Agreement (as defined in Note 4) and the accounting for milestone payments.

Under ASC 605, the Company was recognizing the revenue allocated to each unit of accounting on a straight-line basis over the period the Company is expected to complete its obligations. Under ASC 606, the Company is recognizing the revenue allocated to each performance obligation over time, measuring progress using an input method over the period the Company is expected to complete each performance obligation.

10

Under ASC 605, the Company recognized revenue related to milestone payments as the milestone was achieved, using the milestone method. Under ASC 606, the Company performs an assessment of the probability of milestone achievement at each reporting date and determines whether the cumulative revenue related to the milestone is at risk of significant reversal. See Note 4 for further discussion of the adoption of this standard.

In October 2016, the FASB issued Accounting Standards Update No. 2016-16, Income Taxes (Topic 740): Intra-Entity Transfers of Assets Other Than Inventory (“ASU 2016-16”). Under the new guidance, companies are required to recognize the income tax consequences of an intra-entity transfer of an asset, other than inventory, when the transfer occurs, even though the pre-tax effects of that transaction are eliminated in consolidation. The amendments are effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2017. The Company adopted ASU 2016-16 effective January 1, 2018, which resulted in a $0.4 million cumulative-effect adjustment to retained earnings related to the intercompany sale of intellectual property on October 1, 2017.

In November 2016, the FASB issued Accounting Standards Update No. 2016-18, Statement of Cash Flows (Topic 230): Restricted Cash (“ASU 2016-18”). ASU 2016-18 requires that an entity explain the changes in the total of cash, cash equivalents, restricted cash and restricted cash equivalents on the statement of cash flows. Therefore, amounts generally described as restricted cash and restricted cash equivalents should be included with cash and cash equivalents when reconciling the beginning-of-period and end-of-period total amounts shown on the statement of cash flows. This ASU is effective for annual and interim periods beginning after December 15, 2017. The Company adopted ASU 2016-18 effective January 1, 2018 on a retrospective basis, which resulted in a change in presentation of restricted cash within the Company’s unaudited consolidated statements of cash flows.

3. SHARE-BASED COMPENSATION

The Wave Life Sciences Ltd. 2014 Equity Incentive Plan, as amended (the “2014 Plan”), authorizes the board of directors or a committee of the board of directors to grant incentive share options, non-qualified share options, share appreciation rights, restricted awards, which includes restricted shares and restricted share units (“RSUs”), and performance awards to eligible employees, consultants and directors of the Company. Options generally vest over periods of one to four years, and any options that are forfeited or cancelled are available to be granted again. The contractual life of options is generally five or ten years from the grant date. RSUs generally vest over a period of one or four years, and any RSUs that are forfeited are available to be granted again.

During the nine months ended September 30, 2018, 659,170 options and 309,247 RSUs were granted to employees of the Company.

As of September 30, 2018, 1,695,424 ordinary shares remained available for future grant under the 2014 Plan.

Pfizer Collaboration and Equity Agreements

In May 2016, the Company entered into a Research, License and Option Agreement, as amended (the “Pfizer Collaboration Agreement”), with Pfizer Inc. (“Pfizer”). Pursuant to the terms of the Pfizer Collaboration Agreement, the Company and Pfizer agreed to collaborate on the discovery, development and commercialization of stereopure oligonucleotide therapeutics for up to five programs (the “Pfizer Programs”), each directed at a genetically-defined hepatic target selected by Pfizer (the “Pfizer Collaboration”). The Company received $10.0 million as an upfront license fee under the Pfizer Collaboration Agreement. Subject to option exercises by Pfizer, the Company may earn potential research, development and commercial milestone payments, plus royalties, tiered up to low double-digits, on sales of any products that may result from the Pfizer Collaboration. None of the payments under the Pfizer Collaboration Agreement are refundable.

Simultaneously with the entry into the Pfizer Collaboration Agreement, the Company entered into a Share Purchase Agreement (the “Pfizer Equity Agreement,” and together with the Pfizer Collaboration Agreement, the “Pfizer Agreements”) with C.P. Pharmaceuticals International C.V., an affiliate of Pfizer (the “Pfizer Affiliate”). Pursuant to the terms of the Pfizer Equity Agreement, the Pfizer Affiliate purchased 1,875,000 of the Company’s ordinary shares (the “Shares”) at a purchase price of $16.00 per share, for an aggregate purchase price of $30.0 million. The Company did not incur any material costs in connection with the issuance of the Shares.

Under the Pfizer Collaboration Agreement, the parties agreed to collaborate during a four-year research term. During the research term, the Company is responsible to use its commercially reasonable efforts to advance up to five programs through to the selection of clinical candidates. At that stage, Pfizer may elect to license any of these Pfizer Programs exclusively and obtain exclusive rights to undertake the clinical development of the resulting clinical candidates into products and the potential commercialization of any such products thereafter. In addition, the Company received a non-exclusive, royalty-bearing sublicensable license to use Pfizer’s hepatic targeting technology in any of the Company’s own hepatic programs that are outside the scope of the Pfizer Collaboration (the “Wave Programs”). If the Company uses this technology on the Wave Programs, Pfizer is eligible to receive potential development and commercial milestone payments from the Company. Pfizer is also eligible to receive tiered royalties on sales of any products that include Pfizer’s hepatic targeting technology.

11

The stated term of the Pfizer Collaboration Agreement commenced on May 5, 2016 and terminates on the date of the last to expire payment obligation with respect to each Pfizer Program and, with respect to each Wave Program, expires on a program-by-program basis accordingly. Pfizer may terminate its rights related to a Pfizer Program under the Pfizer Collaboration Agreement at its own convenience upon 90 days’ notice to the Company. The Company may also terminate its rights related to a Wave Program at its own convenience upon 90 days’ notice to Pfizer. The Pfizer Collaboration Agreement may also be terminated by either party in the event of an uncured material breach of the Pfizer Collaboration Agreement by the other party.

Pfizer nominated two hepatic targets upon entry into the Pfizer Collaboration in May 2016. The Pfizer Collaboration Agreement provides Pfizer with options to nominate up to three additional programs by making nomination milestone payments. Pfizer nominated the third, fourth and fifth hepatic targets in August 2016, March 2018 and April 2018, respectively.

The Pfizer Collaboration is managed by a joint steering committee in which both parties are represented equally, which will oversee the scientific progression of each Pfizer Program up to the clinical candidate stage. During the four-year research term and for a period of two years thereafter, the Company has agreed to work exclusively with Pfizer with respect to using any of the Company’s stereopure oligonucleotide technology that is specific for the applicable hepatic target which is the basis of any Pfizer Program. Within 120 days of receiving a data package for a candidate under each nominated program, Pfizer may exercise an option to obtain a license to develop, manufacture and commercialize the program candidate by paying an exercise price per program.

The Company assessed this arrangement in accordance with ASC 606 and concluded that the contract counterparty, Pfizer, is a customer. The Company identified the following promises under the arrangement: (1) the non-exclusive, royalty-free research and development license; (2) the research and development services for Programs 1 and 2; (3) the program nomination options for Programs 3, 4 and 5; (4) the research and development services associated with Programs 3, 4 and 5; (5) the options to obtain a license to develop, manufacture and commercialize Programs 1 and 2; and (6) the options to obtain a license to develop, manufacture and commercialize Programs 3, 4 and 5. The research and development services for each of Programs 1 and 2 were determined to not be distinct from the research and development license and should be combined into a single performance obligation for each program. The promises under the Pfizer Collaboration Agreement relate primarily to the research and development required by the Company for each of the programs nominated by Pfizer.

Additionally, the Company determined that the program nomination options for Programs 3, 4 and 5 were priced at a discount and, as such, provide material rights to Pfizer, representing three separate performance obligations. The research and development services associated with Programs 3, 4 and 5 and the options to obtain a license to develop, manufacture and commercialize Programs 3, 4 and 5 are subject to Pfizer’s exercise of the program nomination options for such programs and therefore do not represent performance obligations at the outset of the arrangement. The options to obtain a license to develop, manufacture and commercialize Programs 1 and 2 do not represent material rights; as such, they are not representative of performance obligations at the outset of the arrangement. Based on these assessments, the Company identified five performance obligations in the Pfizer Collaboration Agreement: (1) research and development services and license for Program 1; (2) research and development services and license for Program 2; (3) material right provided for the option to nominate Program 3; (4) material right provided for the option to nominate Program 4; and (5) material right provided for the option to nominate Program 5.

At the outset of the arrangement, the transaction price included only the $10.0 million up-front consideration received. The Company determined that the Pfizer Collaboration Agreement did not contain a significant financing component. The program nomination option exercise fees for research and development services associated with Programs 3, 4 and 5 that may be received are excluded from the transaction price until each customer option is exercised. The potential milestone payments were excluded from the transaction price, as all milestone amounts were fully constrained at the inception of the Pfizer Collaboration Agreement. The exercise fees for the options to obtain a license to develop, manufacture and commercialize Programs 3, 4 and 5 that may be received are excluded from the transaction price until each customer option is exercised. The Company will reevaluate the transaction price at the end of each reporting period and as uncertain events are resolved or other changes in circumstances occur, and, if necessary, will adjust its estimate of the transaction price.

During the three months ended September 30, 2017, it became probable that a significant reversal of cumulative revenue would not occur for a developmental milestone under the Pfizer Collaboration Agreement. At such time, the associated consideration was added to the estimated transaction price and allocated to the existing performance obligations, and the Company recognized a cumulative catch-up to revenue for this developmental milestone, representing the amount that would have been recognized had the milestone payment been included in the transaction price from the outset of the arrangement. The remainder will be recognized in the same manner as the remaining, unrecognized transaction price over the remaining period until each performance obligation is satisfied. The milestone was achieved in November 2017.

Revenue associated with the performance obligations relating to Programs 1 and 2 is being recognized as revenue as the research and development services are provided using an input method, according to the full-time employee (“FTE”) hours incurred on each program and the FTE hours expected to be incurred in the future to satisfy the performance obligation. The transfer of control occurs

12

over time and, in management’s judgment, this input method is the best measure of progress towards satisfying the performance obligation. The amount allocated to the three material rights will be recognized as the underlying research and development services are provided commencing from the date that Pfizer exercises each respective option, or immediately as each option expires unexercised. The amounts received that have not yet been recognized as revenue are recorded in deferred revenue on the Company’s consolidated balance sheet.

Pfizer nominated the third, fourth and fifth hepatic targets in August 2016, March 2018 and April 2018, respectively. Upon each exercise, the Company allocated the transaction price amount allocated to the material right at inception of the arrangement plus the program nomination option exercise fee paid by Pfizer at the time of exercising the option to a new performance obligation, which will be recognized as revenue as the research and development services are provided using the same method as the performance obligations relating to Programs 1 and 2.

Through September 30, 2018, the Company had recognized revenue of $8.8 million as collaboration revenue in the Company’s consolidated statements of operations and comprehensive loss under the Pfizer Collaboration Agreement. During the three and nine months ended September 30, 2018, the Company recognized revenue of $1.0 million and $3.9 million, respectively, under the Pfizer Collaboration Agreement. The aggregate amount of the transaction price allocated to the Company’s partially unsatisfied performance obligations and recorded in deferred revenue at September 30, 2018 is $9.7 million, of which $6.7 million is included in current liabilities. The Company expects to recognize this amount according to FTE hours incurred, over the remaining research term, which is 19 months as of September 2018.

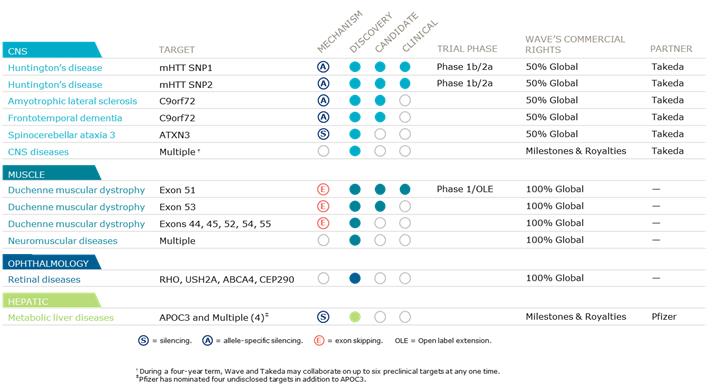

Takeda Collaboration and Equity Agreements

In February 2018, Wave USA and Wave UK entered into a global strategic collaboration (the “Takeda Collaboration”) with Takeda Pharmaceutical Company Limited (“Takeda”), pursuant to which Wave USA, Wave UK and Takeda agreed to collaborate on the research, development and commercialization of oligonucleotide therapeutics for disorders of the Central Nervous System (“CNS”). The Takeda Collaboration provides Wave with at least $230.0 million in committed cash and Takeda with the option to co-develop and co-commercialize Wave’s CNS development programs in (1) Huntington’s disease (“HD”); (2) amyotrophic lateral sclerosis (“ALS”) and frontotemporal dementia (“FTD”); and (3) Wave’s discovery-stage program targeting ATXN3 for the treatment of spinocerebellar ataxia 3 (“SCA3”) (collectively, “Category 1 Programs”). In addition, Takeda will have the right to exclusively license multiple preclinical programs for CNS disorders, including Alzheimer’s disease and Parkinson’s disease (collectively, “Category 2 Programs”). In April 2018, the Takeda Collaboration became effective and Takeda paid Wave $110.0 million as an upfront payment. Takeda also agreed to fund Wave’s research and preclinical activities in the amount of $60.0 million during the four-year research term and to reimburse Wave for any collaboration-budgeted research and preclinical expenses incurred by Wave that exceed that amount.

Simultaneously with Wave USA and Wave UK’s entry into the collaboration and license agreement with Takeda (the “Takeda Collaboration Agreement”), the Company entered into a share purchase agreement with Takeda (the “Takeda Equity Agreement,” and together with the Takeda Collaboration Agreement, the “Takeda Agreements”) pursuant to which it agreed to sell to Takeda 1,096,892 of its ordinary shares at a purchase price of $54.70 per share. In April 2018, the Company closed the Takeda Equity Agreement and received aggregate cash proceeds of $60.0 million. The Company did not incur any material costs in connection with the issuance of shares.

With respect to Category 1 Programs, Wave will be responsible for researching and developing products and companion diagnostics for Category 1 Programs through completion of the first proof of mechanism study for such products. Takeda will have an exclusive option for each target and all associated products and companion diagnostics for such target, which it may exercise at any time through completion of the proof of mechanism study. If Takeda exercises this option, Wave will receive an opt-in payment and will lead manufacturing and joint clinical co-development activities and Takeda will lead joint co-commercial activities in the United States and all commercial activities outside of the United States. Global costs and potential profits will be shared 50:50 and Wave will be eligible to receive development and commercial milestone payments. In addition to its 50% profit share, Wave is eligible to receive option exercise fees and development and commercial milestone payments for each of the Category 1 Programs.

13

With respect to Category 2 Programs, Wave has granted Takeda the right to exclusively license multiple preclinical programs during a four-year research term (subject to limited extension for programs that were initiated prior to the expiration of the research term, in accordance with the Takeda Collaboration Agreement) (“Category 2 Research Term”). During that term, the parties may collaborate on preclinical programs for up to six targets at any one time. Wave will be responsible for researching and preclinically developing products and companion diagnostics directed to the agreed upon targets through completion of IND-enabling studies in the first major market country. Thereafter, Takeda will have an exclusive worldwide license to develop and commercialize products and companion diagnostics directed to such targets, subject to Wave’s retained rights to lead manufacturing activities for products directed to such targets. Takeda will fund Wave’s research and preclinical activities in the amount of $60.0 million during the research term and will reimburse Wave for any collaboration-budgeted research and preclinical expenses incurred by Wave that exceed that amount. Wave is also eligible to receive tiered high single-digit to mid-teen royalties on Takeda’s global commercial sales of products from each Category 2 Program.

Under the Takeda Collaboration Agreement, each party grants to the other party specific intellectual property licenses to enable the other party to perform its obligations and exercise its rights under the Takeda Collaboration Agreement, including license grants to enable each party to conduct research, development and commercialization activities pursuant to the terms of the Takeda Collaboration Agreement.

The term of the Takeda Collaboration Agreement commenced on April 2, 2018 and, unless terminated earlier, will continue until the date on which: (i) with respect to each Category 1 Program target for which Takeda does not exercise its option, the expiration or termination of the development program with respect to such target; (ii) with respect to each Category 1 Program target for which Takeda exercises its option, the date on which neither party is researching, developing or manufacturing any products or companion diagnostics directed to such target; or (iii) with respect to each Category 2 Program target, the date on which royalties are no longer payable with respect to products directed to such target.

Takeda may terminate the Takeda Collaboration Agreement for convenience on 180 days’ notice, in its entirety or on a target-by-target basis. Subject to certain exceptions, each party has the right to terminate the Takeda Collaboration Agreement on a target-by-target basis if the other party, or a third party related to such party, challenges the patentability, enforceability or validity of any patents within the licensed technology that cover any product or companion diagnostic that is subject to the Takeda Collaboration Agreement. In the event of any material breach of the Takeda Collaboration Agreement by a party, subject to cure rights, the other party may terminate the Takeda Collaboration Agreement in its entirety if the breach relates to all targets or on a target-by-target basis if the breach relates to a specific target. In the event that Takeda and its affiliates cease development, manufacturing and commercialization activities with respect to compounds or products subject to the Takeda Collaboration Agreement and directed to a particular target, Wave may terminate the Takeda Collaboration Agreement with respect to such target. Either party may terminate the Takeda Collaboration Agreement for the other party’s insolvency. In certain termination circumstances, Wave would receive a license from Takeda to continue researching, developing and manufacturing certain products, and companion diagnostics.

The Company assessed this arrangement in accordance with ASC 606 and concluded that the contract counterparty, Takeda, is a customer for Category 1 Programs prior to Takeda exercising its option, and for Category 2 Programs during the Category 2 Research Term. The Company identified the following material promises under the arrangement: (1) the non-exclusive, royalty-free research and development license for each Category 1 Program; (2) the research and development services for each Category 1 Program through completion of the first proof of mechanism study; (3) the exclusive option to license, co-develop and co-commercialize each Category 1 Program; (4) the right to exclusively license the Category 2 Programs; and (5) the research and preclinical development services of the Category 2 Programs through completion of IND-enabling studies. The research and development services for each Category 1 Program were determined to not be distinct from the research and development license and should therefore be combined into a single performance obligation for each Category 1 Program. The research and preclinical development services for the Category 2 Programs were determined to not be distinct from the exclusive licenses for the Category 2 Programs and should therefore be combined into a single performance obligation.

Additionally, the Company determined that the exclusive option for each Category 1 Program was priced at a discount, and, as such, provide material rights to Takeda, representing three separate performance obligations. Based on these assessments, the Company identified seven performance obligations in the Takeda Collaboration Agreement: (1) research and development services through completion of the first proof of mechanism and non-exclusive research and development license for HD; (2) research and development services through completion of the first proof of mechanism and non-exclusive research and development license for ALS and FTD; (3) research and development services through completion of the first proof of mechanism and non-exclusive research and development license for SCA3; (4) the material right provided for the exclusive option to license, co-develop and co-commercialize HD; (5) the material right provided for the exclusive option to license, co-develop and co-commercialize ALS and FTD; (6) the material right provided for the exclusive option to license, co-develop and co-commercialize SCA3; and (7) the research and preclinical development services and right to exclusively license the Category 2 Programs.

14

At the outset of the arrangement, the transaction price included the $110.0 million upfront consideration received and the $60.0 million of committed research and preclinical funding for the Category 2 Programs. The Company determined that the Takeda Collaboration Agreement did not contain a significant financing component. The option exercise fees to license, co-develop and co-commercialize each Category 1 Program that may be received are excluded from the transaction price until each customer option is exercised. The potential milestone payments were excluded from the transaction price, as all milestone amounts were fully constrained at the inception of the Takeda Collaboration Agreement. The Company will reevaluate the transaction price at the end of each reporting period and as uncertain events are resolved or other changes in circumstances occur, if necessary, will adjust its estimate of the transaction price.

Revenue associated with the research and development services for each Category 1 Program performance obligation is being recognized as the research and development services are provided using an input method, according to the costs incurred on each Category 1 Program and the total costs expected to be incurred to satisfy each Category 1 Program performance obligation. Revenue associated with the research and preclinical development services for the Category 2 Programs performance obligation is being recognized as the research and preclinical development services are provided using an input method, according to the costs incurred on Category 2 Programs and the total costs expected to be incurred to satisfy the performance obligation. The transfer of control for these performance obligations occurs over time and, in management’s judgment, this input method is the best measure of progress towards satisfying the performance obligations. The amount allocated to the material right for each Category 1 Program option will be recognized on the date that Takeda exercises each respective option, or immediately as each option expires unexercised. The amounts received that have not yet been recognized as revenue are recorded in deferred revenue on the Company’s consolidated balance sheet.

During the three and nine months ended September 30, 2018, the Company recognized revenue of $3.5 million and $6.9 million, respectively, as collaboration revenue in the Company’s consolidated statements of operations and comprehensive loss under the Takeda Collaboration Agreement. The aggregate amount of the transaction price allocated to the Company’s unsatisfied and partially unsatisfied performance obligations and recorded in deferred revenue at September 30, 2018 is $163.1 million, of which $96.6 million is included in current liabilities. The Company expects to recognize revenue for the portion of the deferred revenue that relates to the research and development services for each Category 1 Program and the Category 2 Programs as costs are incurred, over the remaining research term. The Company expects to recognize revenue for the portion of the deferred revenue that relates to the material right for each Category 1 Program option upon Takeda’s exercise of such option, or immediately as each option expires unexercised. The aggregate amount of the transaction price included in accounts receivable at September 30, 2018 is $60.0 million, of which $10.0 million is included in current assets.

5. NET LOSS PER ORDINARY SHARE

The Company applies the two-class method to calculate its basic and diluted net loss per share attributable to ordinary shareholders, as its Series A preferred shares are participating securities. The two-class method is an earnings allocation formula that treats a participating security as having rights to earnings that otherwise would have been available to ordinary shareholders. However, for the periods presented, the two-class method does not impact the net loss per ordinary share as the Company was in a net loss position for each of the periods presented and holders of Series A preferred shares do not participate in losses.

Basic loss per share is computed by dividing net loss attributable to ordinary shareholders by the weighted-average number of ordinary shares used in computing net loss per share attributable to ordinary shareholders.

The Company’s potentially dilutive shares, which include outstanding share options to purchase ordinary shares, RSUs and Series A preferred shares, are considered to be ordinary share equivalents and are only included in the calculation of diluted net loss per share when their effect is dilutive.

The following ordinary share equivalents, presented based on amounts outstanding at each period end, were excluded from the calculation of diluted net loss per share attributable to ordinary shareholders for the periods indicated because including them would have had an anti-dilutive effect:

|

|

|

As of September 30, |

|

|||||

|

|

|

2018 |

|

|

2017 |

|

||

|

Options to purchase ordinary shares |

|

|

3,912,336 |

|

|

|

3,805,795 |

|

|

RSUs |

|

|

408,534 |

|

|

|

162,280 |

|

|

Series A preferred shares |

|

|

3,901,348 |

|

|

|

3,901,348 |

|

15

The Company is a Singapore multi-national company subject to taxation in the United States and various other jurisdictions.

During the three months ended September 30, 2018 and 2017, the Company recorded no income tax benefit or provision and an income tax benefit of $0.4 million, respectively. No income tax benefit or provision was recorded during the three months ended September 30, 2018 as a result of having a full valuation in all jurisdictions. The income tax benefit recorded during the three months ended September 30, 2017 was the result of the implementation of a revised international corporate structure aligned with the Company’s international operations.

During the nine months ended September 30, 2018 and 2017, the Company recorded an income tax provision of $0.2 million and $1.0 million, respectively. The income tax provision recorded during the nine months ended September 30, 2018 was mainly the result of return to provision adjustments related to the filing of Wave Japan’s 2017 tax return. The income tax provision recorded during the nine months ended September 30, 2017 was primarily the result of the establishment of a valuation allowance against our U.S. deferred tax assets.

The Company recorded no income tax benefits for the net operating losses incurred during the three and nine months ended September 30, 2018 in Singapore, the United States, the United Kingdom or Ireland, due to its uncertainty of realizing a benefit from those items. The Company recorded no income tax benefits for the net operating losses incurred during the three and nine months ended September 30, 2017 in Singapore, Japan, the United Kingdom or Ireland, due to its uncertainty of realizing a benefit from those items.

The Company’s reserves related to taxes and its accounting for uncertain tax positions are based on a determination of whether and how much of a tax benefit taken by the Company in its tax filings or positions is more-likely-than-not to be realized following resolution of any potential contingencies present related to the tax benefit.

7. RELATED PARTIES

The Company had the following related party transactions for the periods presented in the accompanying consolidated financial statements, which have not otherwise been discussed in these notes to the consolidated financial statements:

|

|

• |

Pursuant to the terms of various service agreements with Shin Nippon Biomedical Laboratories Ltd., one of the Company’s shareholders, and its affiliates (together “SNBL”), the Company paid SNBL less than $0.1 million and $0.1 million during the three months ended September 30, 2018 and 2017, respectively, and $1.3 million and $0.2 million during the nine months ended September 30, 2018 and 2017, respectively, for contract research services provided to the Company and its affiliates. |

|

|