NATIONAL BANKSHARES INC - Annual Report: 2008 (Form 10-K)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

x Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

|

For the Fiscal Year Ended December 31, 2008

|

|

o Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from ________ to ________.

Commission File Number: 0-15204

NATIONAL BANKSHARES, INC.

(Exact name of registrant as specified in its charter)

|

Virginia |

54-1375874 |

101 Hubbard Street

P.O. Box 90002

Blacksburg, VA 24062-9002

(540) 951-6300

(Address and telephone number of principal executive offices)

|

Securities registered pursuant to Section 12(b) of the Act: |

Securities registered Pursuant to Section 12(g) of the Act: |

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o |

No x |

|

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o |

No x |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of “accelerated filer, large accelerated filer, and smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o Accelerated filer x Non-accelerated filer o Smaller reporting company o

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o |

No x |

The aggregate market value of the voting common stock of the registrant held by stockholders (not including voting common stock held by Directors, Executive Officers and Corporate Governance) on June 30, 2008 (the last business day of the most recently completed second fiscal quarter) was approximately $131,852,380. As of February 15, 2009, the registrant had 6,929,474 shares of voting common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

|

|

Portions of the following documents are incorporated herein by reference into the Part of the Form 10-K indicated. |

|

Document |

Part of Form 10-K into which incorporated |

|

National Bankshares, Inc. 2008 Annual Report to Stockholders |

Part II |

|

National Bankshares, Inc. Proxy Statement for the 2009 Annual Meeting of Stockholders |

Part III |

NATIONAL BANKSHARES, INC. AND SUBSIDIARIES

Form 10-Q

Index

|

|

Page |

|

|

|

|

|

|

Item 1. |

3 |

|

|

|

|

|

|

Item 1A. |

7 |

|

|

|

|

|

|

Item 1B. |

8 |

|

|

|

|

|

|

Item 2. |

8 |

|

|

|

|

|

|

Item 3. |

8 |

|

|

|

|

|

|

Item 4. |

8 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Item 5. |

8 |

|

|

|

|

|

|

Item 6. |

10 |

|

|

|

|

|

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

11 |

|

|

|

|

|

Item 7A. |

26 |

|

|

|

|

|

|

Item 8. |

27 |

|

|

|

|

|

|

Item 9. |

Changes In and Disagreements With Accountants on Accounting and Financial Disclosure |

57 |

|

|

|

|

|

Item 9A. |

57 |

|

|

|

|

|

|

Item 9B. |

58 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Item 10. |

58 |

|

|

|

|

|

|

Item 11. |

58 |

|

|

|

|

|

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

59 |

|

|

|

|

|

Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

59 |

|

|

|

|

|

Item 14. |

59 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Item 15. |

59 |

|

|

|

|

|

|

|

61 |

|

|

|

|

|

|

|

66 |

$ in thousands, except per share data

History and Business

National Bankshares, Inc. (the Company or NBI) is a financial holding company that was organized in 1986 under the laws of Virginia and is registered under the Bank Holding Company Act of 1956. It conducts most of its operations through its wholly-owned community bank subsidiary, the National Bank of Blacksburg (NBB). It also owns National Bankshares Financial Services, Inc. (NBFS), which does business as National Bankshares Insurance Services and National Bankshares Investment Services.

The National Bank of Blacksburg

The National Bank of Blacksburg, which does business as National Bank, was originally chartered in 1891 as the Bank of Blacksburg. Its state charter was converted to a national charter in 1922 and it became the National Bank of Blacksburg. In 2004, NBB purchased Community National Bank of Pulaski, Virginia. In May, 2006, Bank of Tazewell County, a Virginia bank which since 1996 had also been a wholly-owned subsidiary of NBI, was merged with and into NBB.

NBB is community-oriented, and it offers a full range of retail and commercial banking services to individuals, businesses, non-profits and local governments from its headquarters in Blacksburg, Virginia and its twenty-five branch offices throughout southwest Virginia. NBB has telephone and Internet banking and it operates twenty-five automated teller machines in its service area. Lending is focused at small and mid-sized businesses and at individuals. Loan types include commercial, agricultural, real estate, home equity and consumer. Merchant credit card services and business and consumer credit cards are available. Deposit accounts offered include demand deposit accounts, money market deposit accounts, savings accounts and certificates of deposit. NBB offers other miscellaneous services normally provided by commercial banks, such as letters of credit, night depository, safe deposit boxes, travelers checks, utility payment services and automatic funds transfer. NBB conducts a general trust business that has wealth management and trust and estate services for individual and business customers.

At December 31, 2008, NBB had total assets of $931,420 and total deposits of $817,959. NBB’s net income for 2008 was $13,824, which produced a return on average assets of 1.54% and a return on average equity of 13.17%. Refer to Note 12 of the Notes to Consolidated Financial Statements for NBB’s risk-based capital ratios.

National Bankshares Financial Services, Inc.

In 2001, National Bankshares Financial Services, Inc. was formed in Virginia as a wholly-owned subsidiary of NBI. NBFS offers non-deposit investment products and insurance products for sale to the public. NBFS works cooperatively with Infinex Investments, Inc. to provide investments and with Bankers Insurance, LLC for insurance products. NBFS does not significantly contribute to NBI’s net income.

Operating Revenue

The percentage of total operating revenue attributable to each class of similar service that contributed 15% or more of the Company’s total operating revenue for the years ended December 31, 2008, 2007 and 2006 is set out in the following table.

|

|

|

|

|

Percentage of |

|

|

December 31, 2008 |

|

Interest and Fees on Loans |

|

62.68 |

% |

|

|

|

Interest on Investments |

|

21.21 |

% |

|

December 31, 2007 |

|

Interest and Fees on Loans |

|

62.60 |

% |

|

|

|

Interest on Investments |

|

21.46 |

% |

|

December 31, 2006 |

|

Interest and Fees on Loans |

|

61.51 |

% |

|

|

|

Interest on Investments |

|

21.76 |

% |

Market Area

NBB’s market area in southwest Virginia is made up of the counties of Montgomery, Giles, Pulaski, Tazewell, Wythe, Smyth and Washington. It also includes the independent cities of Radford and Galax, and the portions of Carroll and Grayson Counties that are adjacent to Galax. The bank also serves those portions of Mercer County and McDowell County, West Virginia that are contiguous with Tazewell County, Virginia. Although largely rural, the market area is home to two major universities, Virginia Tech and Radford University, and to three community colleges.

Virginia Tech, located in Blacksburg, Virginia, is the area’s largest employer and is the Commonwealth’s second largest university. A second state supported university, Radford University, is located nearby. Employment at the universities has been stable. In recent years Virginia Tech’s Corporate Research Center has brought several high-tech companies to Montgomery County.

In addition to education, the market area has a diverse economic base, with manufacturing, agriculture, tourism, healthcare, retail and service industries all represented. Large manufacturing facilities in the region include Celanese Acetate, the largest employer in Giles County, and Volvo Heavy Trucks, the largest company in Pulaski County. Both of these firms have experienced layoffs within the past three years. In particular in the past year, Volvo Heavy Trucks has made major cuts in its work force in response to a rapid decline in the demand for trucks because of the recent economic downturn. Pulaski and Galax have been centers for furniture manufacturing. In recent years, this industry has been declining because of growing furniture imports and the loss of demand. Several furniture companies have gone out of business in the recent past. Tazewell County is largely dependent on the coal mining industry and on agriculture for its economic base. Coal production is a cyclical industry that has been improving over the past few years. Both Montgomery County and Bluefield in Tazewell County are regional retail centers and have facilities to provide basic heath care for the region.

NBB’s market area offers the advantages of a good quality of life, scenic beauty, moderate climate and historical and cultural attractions. The region has some recent success attracting retirees, particularly from the Northeast and urban northern Virginia.

Because NBB’s market area is economically diverse and includes large public employers, it has historically avoided the most extreme effects of past economic downturns. However, if the current national and state economic problems are severe and prolonged, cutbacks at the state-supported universities and community colleges would have a negative effect on our market. If there were large staff layoffs and smaller student enrollments, both the retail and housing sectors would suffer.

Competition

The banking and financial services industry in NBB’s market area is highly competitive. The competitive business environment is a result of changes in regulation, changes in technology and product delivery systems and competition from non-traditional financial services. NBB competes for loans and deposits with other commercial banks, credit unions, securities and brokerage companies, mortgage companies, insurance companies, retailers, automobile companies and other nonbank financial service providers. Many of these competitors are much larger in total assets and capitalization, have greater access to capital markets and offer a broader array of financial services than NBB. In order to compete, NBB relies upon a service-based business philosophy, personal relationships with customers, specialized services tailored to meet customers’ needs and the convenience of office locations. In addition, the bank is generally competitive with other financial institutions in its market area with respect to interest rates paid on deposit accounts, interest rates charged on loans and other service charges on loans and deposit accounts.

Organization and Employment

NBI, NBB and NBFS are organized in a holding company/subsidiary structure. Functions that serve both subsidiaries, including audit, compliance, loan review and human resources, are at the holding company level for which fees are charged to the respective subsidiary. Until May, 2006, when it was merged with and into NBB, NBI operated a second wholly-owned bank subsidiary, Bank of Tazewell County.

At December 31, 2008, NBI employed 17 full time employees, NBB had 218 full time equivalent employees and NBFS had 3 full time employees.

Regulation, Supervision and Government Policy

NBI and NBB are subject to state and federal banking laws and regulations that provide for general regulatory oversight of all aspects of their operations. As a result of substantial regulatory burdens on banking, financial institutions like NBI and NBB are at a disadvantage to other competitors who are not as highly regulated, and NBI and NBB’s costs of doing business are accordingly higher. A brief summary follows of certain laws, rules and regulations which affect NBI and NBB. Any changes in the laws and regulations governing banking and financial services could have an adverse effect on the business prospects of NBI and NBB. The current economic environment has created uncertainty in this area, as legislators and regulators attempt to address rapidly changing problems with new laws and regulations affecting financial institutions. The federal government has increased involvement in and scrutiny of all financial institutions. There is heightened examination focus, particularly on real estate related assets, and there is the almost certain potential for new laws and regulations.

National Bankshares, Inc.

NBI is a bank holding company qualified as a financial holding company under the Federal Bank Holding Company Act (BHCA), which is administered by the Board of Governors of the Federal Reserve System (the Federal Reserve). NBI is required to file an annual report with the Federal Reserve and may be required to furnish additional information pursuant to the BHCA. The Federal Reserve is

authorized to examine NBI and

its subsidiaries. With some limited exceptions, the BHCA requires a bank holding company to obtain prior approval from the Federal Reserve before acquiring or merging with a bank or before acquiring more than 5% of the voting shares of a bank unless it already controls a majority of shares.

The Bank Holding Company Act. Under the BHCA, a bank holding company is generally prohibited from engaging in nonbanking activities unless the Federal Reserve has found those activities to be incidental to banking. Bank holding companies also may not acquire more than 5% of the voting shares of any company engaged in nonbanking activities. Amendments to the BHCA that were included in the Gramm-Leach-Bliley Act of 1999 (see below) permitted any bank holding company with bank subsidiaries that are well-capitalized, well-managed and which have a satisfactory or better rating under the Community Reinvestment Act (see below) to file an election with the Federal Reserve to become a financial holding company. A financial holding company may engage in any activity that is (i) financial in nature (ii) incidental to a financial activity or (iii) complementary to a financial activity. Financial activities include insurance underwriting, securities dealing and underwriting and providing financial, investment or economic advising services. NBI is a financial holding company.

The Virginia Banking Act. The Virginia Banking Act requires all Virginia bank holding companies to register with the Virginia State Corporation Commission (the Commission). NBI is required to report to the Commission with respect to financial condition, operations and management. The Commission may also make examinations of any bank holding company and its subsidiaries.

The Gramm-Leach-Bliley Act. The Gramm-Leach-Bliley Act (GLBA) permits significant combinations among different sectors of the financial services industry, allows for expansion of financial service activities by bank holding companies and offers financial privacy protections to consumers. GLBA preempts most state laws that prohibit financial holding companies from engaging in insurance activities. GBLA permits affiliations between banks and securities firms in the same holding company structure, and it permits financial holding companies to directly engage in a broad range of securities and merchant banking activities.

The Sarbanes-Oxley Act. The Sarbanes-Oxley Act (SOX) enacted sweeping reforms of the federal securities laws intended to protect investors by improving the accuracy and reliability of corporate disclosures. It impacts all companies with securities registered under the Securities Exchange Act of 1934, including NBI. SOX creates increased responsibility for chief executive officers and chief financial officers with respect to the content of filings with the Securities and Exchange Commission. Section 404 of SOX and related Securities and Exchange Commission rules focused increased scrutiny by internal and external auditors on NBI’s systems of internal controls over financial reporting, which is designed to insure that those internal controls are effective in both design and operation. SOX sets out enhanced requirements for audit committees, including independence and expertise, and it includes stronger requirements for auditor independence and limits the types of non-audit services that auditors can provide. Finally, SOX contains additional and increased civil and criminal penalties for violations of securities laws.

Capital Requirements. The Federal Reserve has adopted risk-based capital guidelines that are applicable to NBI. The guidelines provide that the Company must maintain a minimum ratio of 8% of qualified total capital to risk-weighted assets (including certain off-balance sheet items, such as standby letters of credit). At least half of total capital must be comprised of Tier 1 capital, for a minimum ratio of Tier 1 capital to risk-weighted assets of 4%. In addition, the Federal Reserve has established minimum leverage ratio guidelines of 4% for banks that meet certain specified criteria. The leverage ratio is the ratio of Tier 1 capital to total average assets, less intangibles. NBI is expected to be a source of capital strength for its subsidiary bank, and regulators can undertake a number of enforcement actions against NBI if its subsidiary bank becomes undercapitalized. NBI’s bank subsidiary is well capitalized and fully in compliance with capital guidelines.

Bank regulators could choose to raise capital requirements for banking organizations beyond current levels. NBI is unable to predict if higher capital levels may be mandated in the future.

Emergency Economic Stabilization Act of 2008. On October 14, 2008, the U.S. Treasury announced the Troubled Asset Relief Program (TARP) under the Emergency Economic Stabilization Act of 2008. In the program, the Treasury was authorized to purchase up to $250 million of senior preferred shares in qualifying U.S. banks, saving and loan associations and bank and savings and loan holding companies. The amount of TARP funds was later increased to $350 million. The minimum subscription amount was 1% of risk-weighted assets and the maximum amount was the lesser of $25 billion or 3% of risk-weighted assets. Because of the Company’s high level of capital and the restrictions and uncertainties associated with TARP, the Company’s Board of Directors determined that NBI would not apply to participate.

The National Bank of Blacksburg

NBB is a national banking association incorporated under the laws of the United States, and the bank is subject to regulation and examination by the Office of the Comptroller of the Currency (OCC). NBB’s deposits are insured by the Federal Deposit Insurance Corporation (FDIC) up to the limits of applicable law. The OCC, as the primary regulator, and the FDIC regulate and monitor

all areas of NBB’s operation. These areas include adequacy of capitalization and loss reserves, loans, deposits, business practices related to the charging and payment of interest, investments,

borrowings, payment of dividends, security devices and procedures, establishment of branches, corporate reorganizations and maintenance of books and records. NBB is required to maintain certain capital ratios. It must also prepare quarterly reports on its financial condition for the OCC and conduct an annual audit of its financial affairs. OCC requires NBB to adopt internal control structures and procedures designed to safeguard assets and monitor and reduce risk exposure. While

appropriate for the safety and soundness of banks, these requirements add to overhead expense for NBB and other banks.

The Community Reinvestment Act. NBB is subject to the provisions of the Community Reinvestment Act (CRA), which imposes an affirmative obligation on financial institutions to meet the credit needs of the communities they serve, including low- and moderate-income neighborhoods. The OCC monitors NBB’s compliance with the CRA and assigns public ratings based upon the bank’s performance in meeting stated assessment goals. Unsatisfactory CRA ratings can result in restrictions on bank operations or expansion. NBB received a “satisfactory” rating in its last CRA examination by the OCC.

The Gramm-Leach-Bliley Act. In addition to other consumer privacy provisions, the Gramm-Leach-Bliley Act (GLBA) restricts the use by financial institutions of customers’ nonpublic personal information. At the inception of the customer relationship and annually thereafter, NBB is required to provide its customers with information regarding its policies and procedures with respect to handling of customers’ nonpublic personal information. GLBA generally prohibits a financial institution from providing a customer’s nonpublic personal information to unaffiliated third parties without prior notice and approval by the customer.

The USA Patriot Act. The USA Patriot Act (Patriot Act) facilitates the sharing of information among government entities and financial institutions to combat terrorism and money laundering. The Patriot Act imposes an obligation on NBB to establish and maintain anti-money laundering policies and procedures, including a customer identification program. The bank is also required to screen all customers against government lists of known or suspected terrorists. There is additional regulatory oversight to insure compliance with the Patriot Act.

Consumer Laws and Regulations. There are a number of laws and regulations that regulate banks’ consumer loan and deposit transactions. Among these are the Truth in Lending Act, the Truth in Savings Act, the Expedited Funds Availability Act, the Equal Credit Opportunity Act, the Fair Housing Act, the Fair Credit Reporting Act, the Expedited Funds Availability Act and the Fair Debt Collections Practices Act. NBB is required to comply with these laws and regulations in its dealings with customers. There are numerous disclosure and other compliance requirements associated with the consumer laws and regulations.

Deposit Insurance. NBB has deposits that are insured by the Federal Deposit Insurance Corporation (FDIC). FDIC maintains a Bank Insurance Fund (BIF) that is funded by risk-based insurance premium assessments on insured depository institutions. Assessments are determined based upon several factors, including the level of regulatory capital and the results of regulatory examinations. FDIC may adjust assessments if the insured institution’s risk profile changes or if the size of the BIF declines in relation to the total amount of insured deposits. In 2008, NBB had payment credits that offset BIF payments in the first and second quarters. However, NBB paid BIF assessments in the second half of the year. It is anticipated that assessments will increase in the future, to offset demands on the BIF from banks that fail in the troubled economy.

On October 3, 2008, the FDIC announced that deposits at FDIC-insured institutions would be insured up to at least $250,000. Unless Congress acts before January 2010, FDIC deposit insurance is scheduled to return on that date to $100,000 per depositor, except for certain retirement accounts for which coverage will remain at $250,000.

FDIC announced its Transaction Account Guarantee Program on October 14, 2008. The Transaction Account Guarantee Program, which is a part of the Temporary Liquidity Guarantee Program, provides full coverage for non-interest bearing deposit accounts for FDIC-insured institutions that elected to participate. NBB elected to participate in this program, and its BIF assessments will increase to reflect the additional FDIC coverage.

After giving primary regulators an opportunity to first take action, FDIC may initiate an enforcement action against any depository institution it determines is engaging in unsafe or unsound actions or which is in an unsound condition, and the FDIC may terminate that institution’s deposit insurance. NBB has no knowledge of any matter that would threaten its FDIC insurance coverage.

Capital Requirements. The same capital requirements that are discussed above with relation to NBI are applied to NBB by the OCC. The OCC guidelines provide that banks experiencing internal growth or making acquisitions are expected to maintain strong capital positions well above minimum levels, without reliance on intangible assets.

Limits on Dividend Payments. A significant portion of NBI’s income is derived from dividends paid by NBB. As a national bank, NBB may not pay dividends from its capital, and it may not pay dividends if the bank would become undercapitalized, as defined by regulation, after paying the dividend. Without prior OCC approval, NBB’s dividend payments in any calendar year are restricted to the bank’s retained net income for that year, as that term is defined by the laws and regulations, combined with retained net income from the preceding two years, less any required transfer to surplus.

The OCC and FDIC have authority to limit dividends paid by NBB, if the payment were determined to be an unsafe and unsound banking practice. Any payment of dividends that depletes the bank’s capital base could be deemed to be an unsafe and unsound banking practice.

Branching. As a national bank, NBB is required to comply with the state branch banking laws of Virginia, the state in which the bank is located. NBB must also have the prior approval of OCC to establish a branch or acquire an existing banking operation. Under Virginia law, NBB may open branch offices or acquire existing banks or bank branches anywhere in the state. Virginia law also permits banks domiciled in the state to establish a branch or to acquire an existing bank or branch in another state.

Monetary Policy

The monetary and interest rate policies of the Federal Reserve, as well as general economic conditions, affect the business and earnings of NBI. NBB and other banks are particularly sensitive to interest rate fluctuations. The spread between the interest paid on deposits and that which is charged on loans is the most important component of the bank’s profits. In addition, interest earned on investments held by NBI and NBB has a significant effect on earnings. As conditions change in the national and international economy and in the money markets, the Federal Reserve’s actions, particularly with regard to interest rates, can impact loan demand, deposit levels and earnings at NBB. It is not possible to accurately predict the effects on NBI of economic and interest rate changes.

Other Legislative and Regulatory Concerns

Particularly because of current uncertain and volatile economic conditions, federal and state laws and regulations are regularly proposed that could affect the regulation of financial institutions. New regulations could add to the regulatory burden on banks and increase the costs of compliance, or they could change the products that can be offered and the manner in which banks do business. We cannot foresee how regulation of financial institutions may change in the future and how those changes might affect NBI.

Company Website

NBI maintains a website at www.nationalbankshares.com. The Company’s annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and all amendments to those reports are made available on its website as soon as is practical after the material is electronically filed with the Securities and Exchange Commission. The Company’s proxy materials for the 2009 annual meeting of stockholders are also posted on a separate website at www.nationalbanksharesproxy.com.

If the economic downturn is long and severe, our credit risk will increase and there could be greater loan losses.

A long and severe recession could result in a higher rate of business closures and increased job losses in the region in which we do business. This would increase the likelihood that more of our customers would become delinquent or default on their loans. A higher level of loan defaults could result in higher loan losses, which could adversely affect our performance.

A severe recession could increase the risk of losses in our investment portfolio.

We hold both corporate and municipal bonds in our investment portfolio. A prolonged recession could increase the risk of default by both corporate and government issuers.

If the real estate market is depressed for an extended period, our business could be negatively affected.

A depressed real estate market can impact us in several ways. First, the demand for new real estate loans will decline, and existing loans may become delinquent. In addition, if there is a general devaluation in real estate, loan collateral values will decline.

If market interest rates rise, our net interest income can be negatively affected in the short term.

The direction and speed of interest rate changes affect our net interest margin and net interest income. In the short term, rising interest rates may negatively affect our net interest income, because our interest-bearing liabilities (generally deposits) reprice sooner than our interest-earning assets (generally loans).

If more competitors come into our market area, our business could suffer.

The financial services industry in our market area is highly competitive, with a number of commercial banks, credit unions, insurance companies and stockbrokers seeking to do business with our customers. If there is additional competition from new business or if our existing competitors focus more attention on our market, we could lose customers and our business could suffer.

Increased governmental involvement in and scrutiny of financial institutions could lead to a significant increase in our regulatory burden.

Because of problems in the financial services sector, both federal and state governments could enact new regulations. A significant increase in our regulatory burden could have a negative effect on profitability.

Item 1B. Unresolved Staff Comments

|

|

There are none. |

NBB owns and has a branch bank in NBI’s headquarters building located at 101 Hubbard Street, Blacksburg, Virginia. The bank’s main office is at 100 South Main Street, Blacksburg, Virginia. NBB owns an additional twenty branch offices and it leases four. NBI owns a building in Pulaski, Virginia that is rented. We believe that existing facilities are adequate for current needs and to meet anticipated growth.

NBI, NBB, and NBFS are not currently involved in any material pending legal proceedings, other than routine litigation incidental to NBB’s banking business.

Item 4. Submission of Matters to a Vote of Security Holders

|

|

No matters were submitted to a vote of security holders during the fourth quarter ended December 31, 2008. |

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Common Stock Information and Dividends

National Bankshares, Inc.’s common stock is traded on the NASDAQ Capital Market under the symbol “NKSH”. As of December 31, 2008, there were 876 record stockholders of NBI common stock. The following is a summary of the market price per share and cash dividend per share of the common stock of National Bankshares, Inc. for 2008 and 2007.

Common Stock Market Prices

|

|

|

2008 |

|

2007 |

|

Dividends per share |

|

||||||||

|

|

|

High |

|

Low |

|

High |

|

Low |

|

2008 |

|

2007 |

|

||

|

First Quarter |

|

$ |

21.98 |

|

16.86 |

|

$ |

24.49 |

|

23.40 |

$ |

--- |

$ |

--- |

|

|

Second Quarter |

|

|

20.23 |

|

16.16 |

|

|

24.49 |

|

20.20 |

|

0.39 |

|

0.37 |

|

|

Third Quarter |

|

|

19.90 |

|

15.66 |

|

|

20.49 |

|

18.84 |

|

--- |

|

--- |

|

|

Fourth Quarter |

|

|

20.00 |

|

15.00 |

|

|

19.75 |

|

16.48 |

|

0.41 |

|

0.39 |

|

NBI’s primary source of funds for dividend payments is dividends from its bank subsidiary, NBB. Bank dividend payments are restricted by regulators, as more fully disclosed in Note 11 of Notes to Consolidated Financial Statements.

On May 14, 2008, NBI’s Board of Directors approved the repurchase of up to 100,000 shares of equity securities that are registered by the Company pursuant to Section 12 of the Securities Exchange Act of 1934. During the fourth quarter of 2008 there were no shares repurchased, and 100,000 shares may yet be purchased under the program.

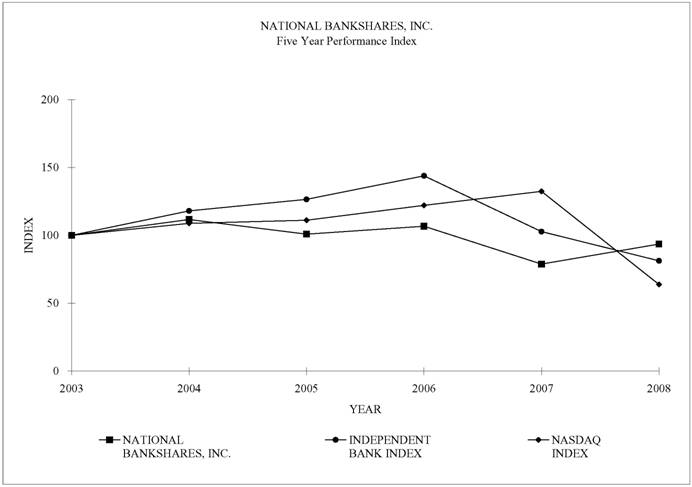

Stock Performance Graph

The following graph compares the yearly percentage change in the cumulative total of stockholder return on NBI common stock with the cumulative return on the NASDAQ Index and a peer group index comprised of southeastern independent community banks and bank holding companies for the five-year period commencing on December 31, 2003. These comparisons assume the investment of $100 in National Bankshares, Inc. common stock and in each of the indices on December 31, 2003, and the reinvestment of dividends.

|

|

|

2003 |

|

2004 |

|

2005 |

|

2006 |

|

2007 |

|

2008 |

|

|

NATIONAL BANKSHARES, INC. |

|

100 |

|

112 |

|

101 |

|

107 |

|

79 |

|

94 |

|

|

INDEPENDENT BANK INDEX |

|

100 |

|

118 |

|

127 |

|

144 |

|

103 |

|

81 |

|

|

NASDAQ INDEX |

|

100 |

|

109 |

|

111 |

|

122 |

|

132 |

|

64 |

|

The peer group Independent Bank Index is the compilation of the total return to stockholders over the past five years of the following group of 25 independent community banks located in the southeastern states of Alabama, Florida, Georgia, North Carolina, South Carolina, Tennessee, Virginia and West Virginia: Auburn National Bancshares, Inc., United Security Bancshares, Inc., TIB Financial Corp., First Community Bank Corp. of America, Seacoast Banking Corp., Fidelity Southern Corp., Southeastern Banking Corporation, Southwest Georgia Financial Corp., Savannah Bancorp, Inc., PAB Bankshares, Inc., Uwharrie Capital Corp., Four Oaks Fincorp, Inc., Bank of Granite Corp., Carolina Trust Bank, BNC Bancorp, CNB Corporation, Geer Bancshares, Peoples Bancorporation, Inc., First Pulaski National Corporation, National Bankshares, Inc., Monarch Financial Holdings, Inc., American National Bankshares, Inc., Central Virginia Bankshares, Inc., C&F Financial Corporation and First Century Bankshares, Inc.

Item 6. Selected Financial Data

National Bankshares, Inc. and Subsidiaries

Selected Consolidated Financial Data

|

$ in thousands, except per share data |

|

Years ended December 31, |

|

|||||||||||||

|

|

|

2008 |

|

2007 |

|

2006 |

|

2005 |

|

2004 |

|

|||||

|

Selected Income Statement Data: |

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Interest income |

|

$ |

50,111 |

|

$ |

50,769 |

|

$ |

47,901 |

|

$ |

45,380 |

|

$ |

41,492 |

|

|

Interest expense |

|

|

18,818 |

|

|

21,745 |

|

|

18,564 |

|

|

14,180 |

|

|

11,125 |

|

|

Net interest income |

|

|

31,293 |

|

|

29,024 |

|

|

29,337 |

|

|

31,200 |

|

|

30,367 |

|

|

Provision for loan losses |

|

|

1,119 |

|

|

423 |

|

|

49 |

|

|

567 |

|

|

1,189 |

|

|

Noninterest income |

|

|

9,087 |

|

|

8,760 |

|

|

8,802 |

|

|

7,613 |

|

|

7,142 |

|

|

Noninterest expense |

|

|

22,023 |

|

|

20,956 |

|

|

21,670 |

|

|

21,898 |

|

|

20,336 |

|

|

Income taxes |

|

|

3,645 |

|

|

3,730 |

|

|

3,788 |

|

|

3,924 |

|

|

3,754 |

|

|

Net income |

|

|

13,593 |

|

|

12,675 |

|

|

12,632 |

|

|

12,424 |

|

|

12,230 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Per Share Data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic net income |

|

|

1.96 |

|

|

1.82 |

|

|

1.80 |

|

|

1.77 |

|

|

1.74 |

|

|

Diluted net income |

|

|

1.96 |

|

|

1.82 |

|

|

1.80 |

|

|

1.76 |

|

|

1.73 |

|

|

Cash dividends declared |

|

|

0.80 |

|

|

0.76 |

|

|

0.73 |

|

|

0.71 |

|

|

0.64 |

|

|

Book value |

|

|

15.89 |

|

|

15.07 |

|

|

13.86 |

|

|

13.10 |

|

|

12.38 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Selected Balance Sheet Data at End of Year: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loans, net |

|

|

569,699 |

|

|

518,435 |

|

|

495,486 |

|

|

487,162 |

|

|

472,199 |

|

|

Total securities |

|

|

264,999 |

|

|

273,343 |

|

|

285,489 |

|

|

272,541 |

|

|

250,708 |

|

|

Total assets |

|

|

935,374 |

|

|

887,647 |

|

|

868,203 |

|

|

841,498 |

|

|

796,154 |

|

|

Total deposits |

|

|

817,848 |

|

|

776,339 |

|

|

764,692 |

|

|

745,649 |

|

|

705,932 |

|

|

Stockholders’ equity |

|

|

110,108 |

|

|

104,800 |

|

|

96,755 |

|

|

91,939 |

|

|

87,088 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Selected Balance Sheet Daily Averages: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loans, net |

|

|

533,190 |

|

|

505,070 |

|

|

488,624 |

|

|

487,130 |

|

|

438,761 |

|

|

Total securities |

|

|

281,367 |

|

|

282,734 |

|

|

271,066 |

|

|

261,743 |

|

|

250,305 |

|

|

Total assets |

|

|

899,462 |

|

|

867,061 |

|

|

840,080 |

|

|

819,341 |

|

|

753,730 |

|

|

Total deposits |

|

|

783,774 |

|

|

758,657 |

|

|

741,071 |

|

|

724,015 |

|

|

665,627 |

|

|

Stockholders’ equity |

|

|

108,585 |

|

|

100,597 |

|

|

94,194 |

|

|

90,470 |

|

|

84,479 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Selected Ratios: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Return on average assets |

|

|

1.51 |

% |

|

1.46 |

% |

|

1.50 |

% |

|

1.52 |

% |

|

1.62 |

% |

|

Return on average equity |

|

|

12.52 |

% |

|

12.60 |

% |

|

13.41 |

% |

|

13.73 |

% |

|

14.48 |

% |

|

Dividend payout ratio |

|

|

40.78 |

% |

|

41.80 |

% |

|

40.44 |

% |

|

40.17 |

% |

|

36.83 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Average equity to average assets |

|

|

12.07 |

% |

|

11.60 |

% |

|

11.21 |

% |

|

11.04 |

% |

|

11.21 |

% |

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

$ in thousands, except per share data

The following discussion and analysis provides information about the results of operations, financial condition, liquidity and capital resources of National Bankshares, Inc. and its subsidiaries. The discussion should be read in conjunction with the material presented in Item 8, “Financial Statements and Supplementary Data”, of this Form 10-K.

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. The Company’s actual results could differ materially from those set forth in the forward-looking statements.

|

|

Per share data has been adjusted to reflect a 2-for-1 stock split effective March 31, 2006. |

Critical Accounting Policies

General

The Company’s financial statements are prepared in accordance with accounting principles generally accepted in the United States (GAAP). The financial information contained within our statements is, to a significant extent, financial information that is based on measures of the financial effects of transactions and events that have already occurred. A variety of factors could affect the ultimate value that is obtained when earning income, recognizing an expense, recovering an asset or relieving a liability. The Company uses historical loss factors as one factor in determining the inherent loss that may be present in the loan portfolio. Actual losses could differ significantly from one previously acceptable method to another method. Although the economics of the Company’s transactions would be the same, the timing of events that would impact the transactions could change.

Allowance for Loan Losses

The allowance for loan losses is an estimate of the losses that may be sustained in our loan portfolio. The allowance is based on two basic principles of accounting: (i) SFAS 5, “Accounting for Contingencies”, which requires that losses be accrued when they are probable of occurring and are estimable and (ii) SFAS 114, “Accounting by Creditors for Impairment of a Loan”, which requires that losses be accrued based on the differences between the value of collateral, present value of future cash flows or values that are observable in the secondary market and the loan balance.

Our allowance for loan losses has three basic components: the formula allowance, the specific allowance and the unallocated allowance. Each of these components is determined based upon estimates that can and do change when the actual events occur. The formula allowance uses a historical loss view as an indicator of future losses and, as a result, could differ from the loss incurred in the future. However, since this history is updated with the most recent loss information, the errors that might otherwise occur are mitigated. The specific allowance uses various techniques to arrive at an estimate of loss. Historical loss information, expected cash flows and fair market value of collateral are used to estimate these losses. The use of these values is inherently subjective, and our actual losses could be greater or less than the estimates. The unallocated allowance captures losses that are attributable to various economic events and to industry or geographic sectors whose impact on the portfolio have occurred but have yet to be recognized either in the formula or in the specific allowance.

Core deposit intangibles

Effective January 1, 2002, the Company adopted Financial Accounting Standards Board Statement No. 142, “Goodwill and Other Intangible Assets”. Accordingly, goodwill is no longer subject to amortization over its estimated useful life, but is subject to at least an annual assessment for impairment by applying a fair value based test. Additionally, Statement 142 requires that acquired intangible assets (such as core deposit intangibles) be separately recognized if the benefit of the asset can be sold, transferred, licensed, rented, or exchanged, and amortized over its estimated useful life. Branch acquisition transactions were outside the scope of the Statement and therefore any intangible asset arising from such transactions remained subject to amortization over their estimated useful life.

In October 2002, the Financial Accounting Standards Board issued Statement No. 147, “Acquisitions of Certain Financial Institutions”. The Statement amends previous interpretive guidance on the application of the purchase method of accounting to acquisitions of financial institutions, and requires the application of Statement No. 141, “Business Combinations”, and Statement No. 142 to branch acquisitions if such transactions meet the definition of a business combination. The provisions of the Statement do not apply to transactions between two or more mutual enterprises. In addition, the Statement amends Statement No. 144, “Accounting for the Impairment of Long-Lived Assets”, to include in its scope core deposit intangibles of financial institutions. Accordingly, such intangibles are subject to a recoverability test based on undiscounted cash flows, and to the impairment recognition and measurement provisions required for other long-lived assets held and used. The Company has determined that the acquisitions that generated the intangible assets and goodwill on the consolidated balance sheets in the amount of $9,958 and $10,912 at December 31, 2003 and 2002, respectively, did not constitute the acquisition of a business, and therefore will continue to be amortized.

Overview

National Bankshares, Inc. is a financial holding company incorporated under the laws of Virginia. Located in southwest Virginia, NBI has two wholly-owned subsidiaries, the National Bank of Blacksburg and National Bankshares Financial Services, Inc. The National Bank of Blacksburg, which does business as National Bank from twenty-six office locations, is a community bank. NBB is the source of nearly all of the Company’s revenue. National Bankshares Financial Services, Inc. does business as National Bankshares Investment Services and National Bankshares Insurance Services. Income from NBFS is not significant at this time, nor is it expected to be so in the near future. Until May 26, 2006, NBI operated a second wholly-owned bank subsidiary, Bank of Tazewell County. On that date it was merged with and into the National Bank of Blacksburg.

Performance Summary

|

|

The following table presents NBI’s key performance ratios for the years ending December 31, 2008 and December 31, 2007: |

|

|

|

12/31/08 |

|

12/31/07 |

|

||

|

Return on average assets |

|

|

1.51 |

% |

|

1.46 |

% |

|

Return on average equity |

|

|

12.52 |

% |

|

12.60 |

% |

|

Basic net earnings per share |

|

$ |

1.96 |

|

$ |

1.82 |

|

|

Fully diluted net earnings per share |

|

$ |

1.96 |

|

$ |

1.82 |

|

|

Net interest margin (1) |

|

|

4.12 |

% |

|

3.98 |

% |

|

Noninterest margin (2) |

|

|

1.46 |

% |

|

1.41 |

% |

|

|

(1) |

Net Interest Margin – Year-to-date tax equivalent net interest income divided by year-to-date average earning assets. |

|

|

(2) |

Noninterest Margin – Noninterest income (excluding securities gains and losses) less noninterest expense (excluding the provision for bad debts and income taxes) divided by average year-to-date assets. |

Because net earnings were higher in 2008 than in 2007, basic earnings per share grew by $0.14. Return on average assets increased 5 basis points, from 1.46% in 2007 to 1.51% in 2008. Return on average assets increased because net earnings in 2008 grew at a faster rate than internally generated asset growth. Return on average equity declined by 8 basis points, from 12.60% for 2007 to 12.52% in 2008. Return on average equity was lower in 2008 because the Company’s equity, mostly from retained earnings, increased more rapidly than did the current year’s net earnings. Reflecting both the effects of the 2008 drop in Federal Reserve interest rates on NBI’s funding costs as deposit rates declined and the Company’s own asset/liability management practices, the net interest margin increased from 3.98% for 2007 to 4.12% for 2008. The noninterest margin increased from 1.41% to 1.46% over the same period.

Management’s longtime focus on profitability over growth for the sake of growth and NBB’s conservative credit culture served the Company well in 2008’s uncertain economic environment.

Growth

|

|

NBI’s key growth indicators are shown in the following table: |

|

|

|

12/31/08 |

|

12/31/07 |

|

||

|

Securities |

|

$ |

264,999 |

|

$ |

273,343 |

|

|

Loans, net |

|

|

569,699 |

|

|

518,435 |

|

|

Deposits |

|

|

817,848 |

|

|

776,339 |

|

|

Total assets |

|

|

935,374 |

|

|

887,647 |

|

Total assets at December 31, 2008 were $935,374, an increase of $47,727 or 5.4%. Net loans increased $51,264 or 9.9%. Total deposits at period-end were $817,848, an increase of $41,509 or 5.4%. Growth in 2008 and 2007 was internally generated.

Asset Quality

|

|

Key indicators of NBI’s asset quality are presented in the following table: |

|

|

|

12/31/08 |

|

12/31/07 |

|

||

|

Nonperforming loans |

|

$ |

1,333 |

|

$ |

1,150 |

|

|

Loans past due over 90 days and accruing |

|

|

1,127 |

|

|

1,181 |

|

|

Other real estate owned |

|

|

1,984 |

|

|

263 |

|

|

Allowance for loan losses to loans |

|

|

1.02 |

% |

|

1.00 |

% |

|

Net charge-off ratio |

|

|

0.09 |

% |

|

0.07 |

% |

There were two nonperforming loans at December 31, 2008, both of which were nonaccrual loans. The total of nonperforming loans at year-end was $1,333, or 0.23% of loans net of unearned income. One loan of $1,028 accounted for the majority of the nonperforming loans total. At December 31, 2007, there was $1,150, or 0.22% of loans net of unearned income, in nonperforming loans. At year-end 2008, loans past due 90 days or more were $1,127, a decrease of $95 from December 31, 2007. Other real estate owned (OREO) grew from $263 at December 31, 2007 to $1,984 at December 31, 2008. Two retail properties constitute a large percentage of the OREO balance at year-end. Additional information about nonaccrual and past due loans is provided in “Balance Sheet – Loans – Risk Elements”

The ratio of the allowance for loan losses to loans net of unearned income was 1.02% and 1.00% at December 31, 2008 and 2007, respectively. The increase in the allowance takes into account both the historical loss projections that accompany growth in the loan portfolio and the higher level of nonperforming loans at year-end 2008.

During the last quarter of 2008, there were serious disruptions in the nation’s financial markets which were caused largely by the country’s housing crisis. NBI’s market did not participate in the rapid inflation of real estate prices that pre-dated recent problems. To date, there have not been the large number of home foreclosures in the Company’s markets, particularly in its core area, as have occurred in other regions. If the economic downturn is prolonged, management anticipates that the level of future loan delinquencies will increase. The Company will continue to monitor asset quality and will regularly review the adequacy of the allowance for loan losses. For more information, see “Provision and Allowance for Loan Losses”.

Net Interest Income

Net interest income for the period ended December 31, 2008 was $31,293, an increase of $2,269, or 7.8%, when compared to the prior year. Net interest income for the period ended December 31, 2007 was $29,024, a decrease of $313, or 1.1%, from 2006. The net interest margin for 2008 was 4.12%, compared to 3.98% for 2007. Total interest income for the period ended December 31, 2008 was $50,111, a decrease of $658 from the period ended December 31, 2007. Interest expense was down by $2,927 during the same time frame. The decline in interest expense came about because of rapidly falling interest rates in the money markets combined with the Company’s liability sensitive balance sheet. In summary, the rates paid on the Company’s deposit liabilities declined at a more rapid pace than the interest rates on its interest earning assets.

The amount of net interest income earned is affected by various factors, including changes in market interest rates due to the Federal Reserve Board’s monetary policy; the level and composition of the earning assets; and the level and composition of interest-bearing liabilities. The Company has the ability to respond to interest rate movements and reduce volatility in the net interest margin. However, the frequency and/or magnitude of changes in market interest rates are difficult to predict and may have a greater impact on net interest income than adjustments by management.

Interest rates are at historic lows, and low and stable interest rates benefit the Company. Offsetting the effect of low interest rates is the fact that some higher yielding securities in the Company’s investment portfolio may be called when rates are low and are replaced with securities yielding at the lower market rate.

The primary source of funds used to support the Company’s interest-earning assets is deposits. Deposits are obtained in the Company’s trade area through traditional marketing techniques. Other funding sources, such as the Federal Home Loan Bank, while available, are only occasionally used. The cost of funds is dependent on interest rate levels and competitive factors. This limits the ability of the Company to react to interest rate movements.

If interest rates remain low and stable, management anticipates that there will be less pressure on the net interest margin as management is able to price loans and deposits rationally. If interest rates were to rise quickly, the net interest margin would narrow, because deposit rates would increase at a faster rate than loan rates. If interest rates rise more slowly, the negative effect on the net interest margin would be less pronounced.

Analysis of Net Interest Earnings

The following table shows the major categories of interest-earning assets and interest-bearing liabilities, the interest earned or paid, the average yield or rate on the daily average balance outstanding, net interest income and net yield on average interest-earning assets for the years indicated.

|

|

|

December 31, 2008 |

|

December 31, 2007 |

|

December 31, 2006 |

|

||||||||||||||||||

|

|

|

|

|

|

Average |

|

|

|

|

|

Average |

|

|

|

|

|

Average |

|

|||||||

|

Interest-earning assets: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loans, net (1)(2)(3) |

|

$ |

538,868 |

|

$ |

37,356 |

|

6.93 |

% |

$ |

510,772 |

|

$ |

37,549 |

|

7.35 |

% |

$ |

494,495 |

|

$ |

35,134 |

|

7.11 |

% |

|

Taxable securities |

|

|

137,497 |

|

|

6,817 |

|

4.96 |

% |

|

152,422 |

|

|

7,476 |

|

4.90 |

% |

|

152,715 |

|

|

7,462 |

|

4.89 |

% |

|

Nontaxable securities (1)(4) |

|

|

144,137 |

|

|

8,911 |

|

6.18 |

% |

|

131,864 |

|

|

8,233 |

|

6.24 |

% |

|

119,931 |

|

|

7,502 |

|

6.25 |

% |

|

Interest bearing deposits |

|

|

21,440 |

|

|

449 |

|

2.09 |

% |

|

14,180 |

|

|

726 |

|

5.12 |

% |

|

13,457 |

|

|

684 |

|

5.08 |

% |

|

Total interest-earning assets |

|

$ |

841,942 |

|

$ |

53,533 |

|

6.36 |

% |

$ |

809,238 |

|

$ |

53,984 |

|

6.67 |

% |

$ |

780,598 |

|

$ |

50,782 |

|

6.51 |

% |

|

Interest-bearing liabilities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest-bearing demand deposits |

|

$ |

243,409 |

|

$ |

3,486 |

|

1.43 |

% |

$ |

223,771 |

|

$ |

4,371 |

|

1.95 |

% |

$ |

221,927 |

|

$ |

4,152 |

|

1.87 |

% |

|

Savings deposits |

|

|

45,796 |

|

|

132 |

|

0.29 |

% |

|

46,943 |

|

|

237 |

|

0.50 |

% |

|

51,745 |

|

|

259 |

|

0.50 |

% |

|

Time deposits |

|

|

381,961 |

|

|

15,188 |

|

3.98 |

% |

|

379,089 |

|

|

17,102 |

|

4.51 |

% |

|

358,422 |

|

|

14,127 |

|

3.94 |

% |

|

Short-term borrowings |

|

|

297 |

|

|

12 |

|

4.04 |

% |

|

626 |

|

|

35 |

|

5.59 |

% |

|

420 |

|

|

26 |

|

6.19 |

% |

|

Total interest-bearing liabilities |

|

$ |

671,463 |

|

$ |

18,818 |

|

2.80 |

% |

$ |

650,429 |

|

$ |

21,745 |

|

3.34 |

% |

$ |

632,514 |

|

$ |

18,564 |

|

2.94 |

% |

|

Net interest income and interest rate spread |

|

|

|

|

$ |

34,715 |

|

3.56 |

% |

|

|

|

$ |

32,239 |

|

3.33 |

% |

|

|

|

$ |

32,218 |

|

3.57 |

% |

|

Net yield on average interest-earning assets |

|

|

|

|

|

|

|

4.12 |

% |

|

|

|

|

|

|

3.98 |

% |

|

|

|

|

|

|

4.13 |

% |

|

(1) |

Interest on nontaxable loans and securities is computed on a fully taxable equivalent basis using a Federal income tax rate of 35% in the three years presented. |

|

(2) |

Loan fees of $859 in 2008, $851 in 2007 and $798 in 2006 are included in total interest income. |

|

(3) |

Nonaccrual loans are included in average balances for yield computations. |

|

(4) |

Daily averages are shown at amortized cost. |

Analysis of Changes in Interest Income and Interest Expense

The Company’s primary source of revenue is net interest income, which is the difference between the interest and fees earned on loans and investments and the interest paid on deposits and other funds. The Company’s net interest income is affected by changes in the amount and mix of interest-earning assets and interest-bearing liabilities and by changes in yields earned on interest-earning assets and rates paid on interest-bearing liabilities. The following table sets forth, for the years indicated, a summary of the changes in interest income and interest expense resulting from changes in average asset and liability balances (volume) and changes in average interest rates (rate).

|

|

|

2008 Over 2007 |

|

2007 Over 2006 |

|

||||||||||||||

|

|

|

Changes Due To |

|

|

Changes Due To |

|

|

||||||||||||

|

|

|

|

|

|

Net Dollar |

|

|

|

|

|

Net Dollar Change |

|

|||||||

|

Interest income:(1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loans |

|

$ |

(2,200 |

) |

$ |

2,008 |

|

$ |

(192 |

) |

$ |

1,239 |

|

$ |

1,176 |

|

$ |

2,415 |

|

|

Taxable securities |

|

|

80 |

|

|

(739 |

) |

|

(659 |

) |

|

28 |

|

|

(14 |

) |

|

14 |

|

|

Nontaxable securities |

|

|

(82 |

) |

|

759 |

|

|

677 |

|

|

(14 |

) |

|

745 |

|

|

731 |

|

|

Interest-bearing deposits |

|

|

(547 |

) |

|

270 |

|

|

(277 |

) |

|

5 |

|

|

37 |

|

|

42 |

|

|

Increase (decrease) in income on interest-earning assets |

|

$ |

(2,749 |

) |

$ |

2,298 |

|

$ |

(451 |

) |

$ |

1,258 |

|

$ |

1,944 |

|

$ |

3,202 |

|

|

Interest expense: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest-bearing demand deposits |

|

$ |

(1,243 |

) |

$ |

358 |

|

$ |

(885 |

) |

$ |

184 |

|

$ |

35 |

|

$ |

219 |

|

|

Savings deposits |

|

|

(99 |

) |

|

(6 |

) |

|

(105 |

) |

|

2 |

|

|

(24 |

) |

|

(22 |

) |

|

Time deposits |

|

|

(2,043 |

) |

|

129 |

|

|

(1,914 |

) |

|

2,127 |

|

|

848 |

|

|

2,975 |

|

|

Short-term borrowings |

|

|

(8 |

) |

|

(15 |

) |

|

(23 |

) |

|

(3 |

) |

|

12 |

|

|

9 |

|

|

Increase (decrease) in expense of interest- bearing liabilities |

|

$ |

(3,393 |

) |

$ |

466 |

|

$ |

(2,927 |

) |

$ |

2,310 |

|

$ |

871 |

|

$ |

3,181 |

|

|

Increase (decrease) in net interest income |

|

$ |

644 |

|

$ |

1,832 |

|

$ |

2,476 |

|

$ |

(1,052 |

) |

$ |

1,073 |

|

$ |

21 |

|

|

(1) |

Taxable equivalent basis using a Federal income tax rate of 35% in 2008, 2007 and 2006. |

|

(2) |

Variances caused by the change in rate times the change in volume have been allocated to rate and volume changes proportional to the relationship of the absolute dollar amounts of the change in each. |

As shown in the chart above, interest expense declined at a faster rate than interest income in 2008. In particular, there was a significant decline in interest expense associated with time deposits. When 2008 and 2007 are compared, time deposit interest expense was $1,914 lower. Of the total decline, $2,043 was due to rates, offset by $129 from higher deposit volume. For the same period, interest-bearing demand deposits had a net decline of $885, of which $1,243 is attributable to rates, offset by $358 from volume.

Lower interest expense in 2008 was the result of the declining interest rate environment caused in part by the Federal Reserve lowering the federal funds rate seven times during the year. Management focused on deposit pricing throughout 2008 and took advantage of falling rates to lower interest expense.

From 2007 to 2008, interest on loans was down by $192. This total came about because rates were $2,200 lower, while volume increased by $2,008. An average volume increase of $28,096 offset to a large degree the decline in loan interest income caused by the effect of falling interest rates.

In 2009, management anticipates that the net interest margin will improve if interest rates remain low and stable. This is because, as the year progresses, the near term pressure on loan rates from 2008 Federal Reserve interest rate cuts may be offset by an improving ability to price loans favorably and to price deposits rationally.

Interest Rate Sensitivity

The Company considers interest rate risk to be a significant market risk and has systems in place to measure the exposure of net interest income and fair market values to movement in interest rates. Among the tools available to management is interest rate sensitivity analysis, which provides information related to repricing opportunities. Interest rate shock simulations indicate potential economic loss due to future interest rate changes. Shock analysis is a test that measures the effect of a hypothetical, immediate and parallel shift in interest rates. The following table shows the results of a rate shock and the effects on net income and return on average assets and return on average equity projected at December 31, 2008 and 2007. For purposes of this analysis, noninterest income and expenses are assumed to be flat.

|

$ in thousands, except percent data |

|

||||||||

|

Rate Shift (bp) |

|

Return on Average Assets |

|

Return on Average Equity |

|

||||

|

|

|

2008 |

|

2007 |

|

2008 |

|

2007 |

|

|

300 |

|

0.83 |

% |

1.21 |

% |

6.87 |

% |

10.24 |

% |

|

200 |

|

1.08 |

% |

1.30 |

% |

8.81 |

% |

11.01 |

% |

|

100 |

|

1.32 |

% |

1.39 |

% |

10.71 |

% |

11.77 |

% |

|

(-)100 |

|

1.81 |

% |

1.56 |

% |

14.46 |

% |

13.20 |

% |

|

(-)200 |

|

1.85 |

% |

1.60 |

% |

14.79 |

% |

13.54 |

% |

|

(-)300 |

|

1.74 |

% |

1.60 |

% |

13.93 |

% |

13.52 |

% |

|

|

|

|

|

|

|

|

|

|

|

Simulation analysis is another tool available to the Company to test asset and liability management strategies under rising and falling rate conditions. As a part of the simulation process, certain estimates and assumptions must be made. These include, but are not limited to, asset growth, the mix of assets and liabilities, rate environment and local and national economic conditions. Asset growth and the mix of assets can, to a degree, be influenced by management. Other areas, such as the rate environment and economic factors, cannot be controlled. In addition, competitive pressures can make it difficult to price deposits and loans in a manner that optimally minimizes interest rate risk. Therefore, actual results may vary materially from any particular forecast or shock analysis. This shortcoming is offset somewhat by the periodic reforecasting of the balance sheet to reflect current trends and economic conditions. Shock analysis must also be updated periodically as a part of the asset and liability management process.

Noninterest Income

|

|

|

Year Ended |

|

|||||||

|

|

|

December 31, 2008 |

|

December 31, 2007 |

|

December 31, 2006 |

|

|||

|

Service charges on deposits |

|

$ |

3,425 |

|

$ |

3,291 |

|

$ |

3,361 |

|

|

Other service charges and fees |

|

|

326 |

|

|

330 |

|

|

370 |

|

|

Credit card fees |

|

|

2,808 |

|

|

2,740 |

|

|

2,396 |

|

|

Trust fees |

|

|

1,231 |

|

|

1,333 |

|

|

1,528 |

|

|

Other income |

|

|

1,122 |

|

|

1,015 |

|

|

1,117 |

|

|

Realized securities gains/losses |

|

|

175 |

|

|

51 |

|

|

30 |

|

|

Total noninterest income |

|

$ |

9,087 |

|

$ |

8,760 |

|

$ |

8,802 |

|

Service charges on deposit accounts increased by $134, or 4.1%, from 2007 to 2008. For 2007, service charges on deposits were $3,291, which was a decline of $70, or 2.1%, over year-end 2006. This category of fees is impacted by the level of service charges, the number of deposit accounts and the volume of checking account overdrafts. Service charges were increased in mid-2008, and the change accounted for the growth in this income category. Of the $134 increase, approximately $120 is attributable to fees for overdrafts and return checks. The decline in 2007 resulted from a decrease in fees paid for checking account overdrafts and for checks returned because of insufficient funds.

A variety of fees are included in the other service charges and fees category. Among them are fees for official checks, income from the sale of checks to customers, safe deposit box rent, fees for letters of credit and commission earned on the sale of credit life, accident and health insurance. At December 31, 2008, the total for other service charges and fees was $326, a decrease of $4 from the year ended December 31, 2007. In 2007, other service charges and fees were $330, a decrease of $40, from 2006. The 2008 and 2007 declines were the result of small decreases in several types of fees, none of which is significant by itself.

Credit card fees for 2008 grew by $68, or 2.5%. In 2007, that category was up by $344, or 14.4%. Internal growth, resulting in a higher volume of accounts, transactions and merchant transactions, caused the increases in 2008 and 2007 credit card fee income.

For the year ended December 31, 2008, trust fees were $1,231, as compared with $1,333 in 2007 and $1,528 in 2006. This represents a decline of $102, or 7.7%, from 2007 and 2008 and a drop of $195, or 12.8% between 2006 and 2007. Trust fees are generated from a number of different types of accounts, including estates, personal trusts, employee benefit trusts, investment management accounts, attorney-in-fact accounts and guardianships. Trust income varies depending upon the types of accounts under management and with market conditions. Trust account values are affected by financial market conditions, and this leads to fluctuations in trust income. The decline in 2007 from 2006 was primarily accounted for by a $127 decline in estate management fees. The decrease in trust fees for 2008 from 2007 is attributable to both factors, the mix of account types and negative financial market performance.