TILE SHOP HOLDINGS, INC. - Annual Report: 2018 (Form 10-K)

|

|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended December 31, 2018

or

☐ Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from to

Commission File Number: 001-35629

TILE SHOP HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

|

|

|

|

Delaware |

45-5538095 |

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

14000 Carlson Parkway, Plymouth, Minnesota 55441

(Address of principal executive offices, including zip code)

(763) 852-2950

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

|

Title of each class |

Name of each exchange on which registered |

|

Common Stock, $0.0001 par value |

The Nasdaq Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

|

|

|

|

Large accelerated filer ☐ |

Accelerated filer ☒ |

|

|

Non-accelerated filer ☐ |

Smaller reporting company ☐ |

|

|

|

Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter was approximately: $300,224,848.

As of February 22, 2019, the registrant had 52,921,546 shares of common stock outstanding.

|

|

TILE SHOP HOLDINGS, INC. FORM 10-K

|

|

|

|

|

|

|

|

|

|

|

PART I |

|

|

|

|

|

1 | ||

|

|

5 | ||

|

|

12 | ||

|

|

13 | ||

|

|

13 | ||

|

|

13 | ||

|

|

|

|

|

|

PART II |

|

|

|

|

|

14 | ||

|

|

16 | ||

|

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

19 | |

|

|

30 | ||

|

|

30 | ||

|

|

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE |

30 | |

|

|

31 | ||

|

|

32 | ||

|

|

|

|

|

|

PART III |

|

|

|

|

|

33 | ||

|

|

39 | ||

|

|

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS |

49 | |

|

|

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE |

51 | |

|

|

52 | ||

|

|

|

|

|

|

PART IV |

|

|

|

|

|

54 | ||

|

|

|

|

|

| 80 | |||

|

|

|

|

|

| 81 | |||

PART I

Overview

The Tile Shop, LLC (“The Tile Shop”) was founded in 1985 and Tile Shop Holdings, Inc. (“Holdings,” and together with its wholly owned subsidiaries, including The Tile Shop, the “Company” or “we”) was incorporated in Delaware in June 2012. We are a specialty retailer of natural stone and man-made tiles, setting and maintenance materials, and related accessories in the United States. Our assortment includes approximately 6,000 products from around the world. Natural stone products include marble, travertine, granite, quartz, sandstone, slate, and onyx tiles. Man-made products include ceramic, porcelain, glass, cement, wood look, and metal tiles. The majority of our tile products are sold under our proprietary Rush River and Fired Earth brand names. We purchase our tile products, accessories and tools directly from our global network of suppliers. We manufacture our own setting and maintenance materials, such as thinset, grout and sealer under our Superior brand name, as well as work with other suppliers to manufacture private label products. As of December 31, 2018, we operated 140 stores in 31 states and the District of Columbia, with an average size of approximately 20,200 square feet.

We believe that our long-term vendor relationships, together with our design, manufacturing and distribution capabilities, enable us to offer a broad assortment of high-quality products to our customers, who are primarily homeowners and professionals, at competitive prices. We have invested significant resources to develop our proprietary brands and product sources and believe that we are a leading retailer of natural stone and man-made tiles, setting and maintenance materials, and related accessories in the United States.

In 2018, we reported net sales and income from operations of $357.3 million and $18.1 million, respectively. Our 2017 and 2016 net sales were $344.6 million and $324.2 million, respectively, and our 2017 and 2016 income from operations was $25.8 million and $32.9 million, respectively. We opened two new stores in 2018 and intend to open five to seven new stores in 2019. As of December 31, 2018 and 2017, we had total assets of $297.6 million and $270.7 million, respectively.

Competitive Strengths

We believe that the following factors differentiate us from our competitors and position us to continue to grow our specialty retailer business.

Broad Product Assortment at Attractive Prices – We offer approximately 6,000 natural stone and made-made products, setting and maintenance materials, accessories, and tools. We are able to maintain competitive prices by purchasing tile and accessories directly from producers and manufacturing our own setting and maintenance materials.

Customer Service and Satisfaction – Our sales personnel are highly-trained and knowledgeable about the technical and design aspects of our products. We offer free design services and the use of our innovative Design Studio software that helps bring our customers ideas to life by enabling them to design and visualize their own customized project. In addition, we provide one-on-one installation training as required to meet customer needs. We accept returns up to six months following the date of the sale, with no restocking fees.

Inspiring Customer Experience – In each store, our products are brought to life by showcasing a broad array of the items we offer in up to 50 different vignettes of bathrooms, kitchens, fireplaces, foyers, and other distinct spaces. Our stores are spacious, well-lit, and organized by product type to simplify our customers’ shopping experience.

Global Sourcing Capabilities – We have long-standing relationships with our tile suppliers throughout the world and work with them to design products exclusively for us. We believe that these direct relationships differentiate us from our competitors.

Proprietary Branding – We sell the majority of our products under our proprietary brand names, which helps us to differentiate our products from those of our competitors. We offer products across a range of price points and quality levels that allow us to target discrete market segments and to appeal to diverse groups of customers.

Centralized Distribution System – We service our store locations from five distribution centers. Our distribution centers, located in Michigan, Oklahoma, New Jersey, Virginia, and Wisconsin, are located to cost effectively service our existing stores.

Strategic Plan

In 2018, we made a number of pivotal changes and strategic investments that included:

|

· |

Adding over 2,000 products to our assortment; |

|

· |

Discontinuing all advertised price promotions; |

1

|

· |

Expanding our regional leadership team to help better support our stores; |

|

· |

Hiring over 20 pro market managers directly responsible for pro outreach within the markets we serve; |

|

· |

Launching our pro loyalty program; |

|

· |

Refining our sales and distribution compensation structures designed to attract and retain top talent; |

|

· |

Completing 10 remodels that included a number of our top stores; |

|

· |

Remerchandising all 140 stores; |

|

· |

Implementing a new customer relationship management capability; and |

|

· |

Positioning ourselves to launch a new enterprise resource planning system. |

Key elements of our 2019 strategy include:

Best Assortment – We offer an extensive assortment of approximately 6,000 natural stone and man-made tile products, setting and maintenance materials, accessories and tools. Our assortment is tailored to provide homeowners and professional customers distinctive products. We feature unique products and partner with industry-leading designers to curate collections that are sold exclusively in our stores. Our buying team sources products from across the world to provide our customers with good, better and best options to appeal to their individual tastes and budgets. We are committed to maintaining a product assortment that meets the needs of an upscale, fashion conscious homeowner, as well as all of the professional customers who serve that homeowner. We believe our ongoing emphasis on maintaining a best-in-class assortment is a critical component of our strategy.

Best Service – We are committed to providing our customers a high degree of in-store service through our motivated, well-trained store team members. We continue to make investments to improve our recruitment, management and development training practices, which reduced our sales associate turnover and increased our average manager tenure. The improvement in turnover and manager tenure has contributed to better product knowledge, store leadership, and overall customer experience. We also engage with our customers through our website (TileShop.com), which provides inspiration, enhanced product information, and research and design tools that support product selection. Our exceptional customer service gives customers the ability to design with confidence.

Best Presentation – We bring our products to life in our stores by showcasing a broad array of the items we offer in up to 50 different vignettes of bathrooms, kitchens, fireplaces, foyers and other distinct spaces. We also showcase our products on our website. We are committed to maintaining our reputation as a destination store where customers find inspiration.

Reaccelerate Store Growth – We plan to increase our existing store base by five to seven stores in 2019. All stores we intend to open in 2019 will be located in existing markets where we will be able to leverage economies of scale in marketing, distribution and store talent. Longer term, we believe we have exceptional opportunities to continue to add stores in existing markets and expand into new markets. Additionally, we will continue to focus on strategies to further enhance the return on our new store investments by selecting retail spaces that provide us the opportunity to reduce the initial investment to build a new store and, in some cases, the ongoing occupancy costs.

Sales Model

We principally sell our products directly to homeowners and professionals. With regard to individual customers, we believe that due to the average cost and relative infrequency of a tile purchase, many of our individual customers conduct extensive research using multiple channels before making a purchase decision. Our sales strategy emphasizes customer service by providing comprehensive and convenient educational tools on our website and in our stores for our customers to learn about our products and the tile installation process. Our website contains a broad range of information regarding our tile products, setting and maintenance materials, and accessories. Customers can order samples, view catalogs, or purchase products from our stores. Customers can choose to have their purchases delivered or picked up at one of our stores. We believe this strategy also positions us well with professional customers who are influenced by the preferences of individual homeowners.

Our stores are designed to emphasize our products in a visually appealing showroom format. Our average store is approximately 20,200 square feet, with a majority of the square footage devoted to the showroom. Several thousand square feet is used for warehouse space, which is used primarily to hold customer orders waiting to be picked up or delivered. Our stores are typically accessible from major roadways and have significant visibility to passing traffic. We can adapt to a range of existing buildings, whether free-standing or in shopping centers. All of our stores are leased.

Unlike many of our competitors, we devote a substantial portion of our store space to showrooms, including samples of our approximately 6,000 products and up to 50 different vignettes of bathrooms, kitchens, fireplaces, foyers, and other distinct spaces that showcase our products. Our showrooms are designed to provide our customers with a better understanding of how to integrate various types of tile in order to create an attractive presentation in their homes. Many stores are also equipped with a training center designed to teach customers how to properly install tile.

2

A staffing model for a typical store consists of a manager, an assistant manager, sales associates, and a warehouse leader. Our store managers are responsible for store operations and for overseeing our customers’ shopping experience. We offer financing to customers through a branded credit card provided by a third-party consumer finance company.

Marketing

We utilize a variety of marketing strategies and programs to acquire and retain customers, including both consumers and trade professionals. Our advertising primarily consists of digital media, direct marketing, including email and postal mail, in store events, and mobile and traditional media vehicles, including newspaper circular/print ads, radio, video and out-of-home advertising. We continually test and learn from new media and adjust our programs based on performance.

Our website, TileShop.com, supports desktop, tablet, and mobile devices and is designed for consumers, trade professionals and industry stakeholders to learn about our brand, our value propositions, and our product assortment and installation techniques, and to look up our store locations and account information. It hosts our Design Studio, a collaborative platform that enables the creation of customized 3D design renderings to scale, allowing customers to bring their ideas to life. On social media, #TheTileShop provides current and prospective customers a high level of brand engagement and enables customers to share their finished projects in our inspiration gallery.

Products

We offer an extensive and complete assortment of natural stone and man-made tile products, sourced directly from our suppliers. Natural stone products include marble, travertine, granite, quartz, sandstone, slate, and onyx tiles. Man-made products include ceramic, porcelain, glass, cement, wood look, and metal tiles. Our wide assortment of accessories, including trim pieces, mosaics, pencils, listellos, and other unique products encourages our customers to make a fashion statement with their tile project and helps us to deliver a high level of customer satisfaction and drive repeat business. We also offer a broad range of setting and maintenance materials, such as thinset, grout, sealers, and accessories, including installation tools, shower and bath shelves, drains, and similar products. We also offer customers delivery service through third-party freight providers. We sell most of our products under our proprietary brand names, including Superior Adhesives & Chemicals, Superior Tools & Supplies, Rush River, and Fired Earth. In total, we offer approximately 6,000 different tile products, setting and maintenance materials, and accessory products. The percentage of our net sales represented by each product category was as follows for the years ended December 31, 2018 and 2017:

|

|

|||||||

|

|

Years Ended December 31, |

||||||

|

|

2018 |

2017 |

|||||

|

Man-made tiles |

46 |

% |

43 |

% |

|||

|

Natural stone tiles |

28 | 33 | |||||

|

Setting and maintenance materials |

14 | 11 | |||||

|

Accessories |

10 | 11 | |||||

|

Delivery service |

2 | 2 | |||||

|

|

100 |

% |

100 |

% |

|||

Suppliers

We have long-standing relationships with our suppliers throughout the world and work with them to design and manufacture products exclusively for us. We believe that these direct relationships differentiate us from our competitors.

We currently purchase tile products from approximately 250 different suppliers. Our top ten tile suppliers accounted for 49% of our tile purchases in 2018. Our largest supplier accounted for approximately 14% of our total purchases in 2018. We believe that alternative and competitive suppliers are available for many of our products. The percentage of our total purchases from the following continents was as follows for the years ended December 31, 2018 and 2017:

|

|

|||||||

|

|

Years Ended December 31, |

||||||

|

|

2018 |

2017 |

|||||

|

Asia |

43 |

% |

51 |

% |

|||

|

Europe (including Turkey) |

31 | 27 | |||||

|

North America |

21 | 19 | |||||

|

South America |

5 | 2 | |||||

|

Africa |

0 | 1 | |||||

|

|

100 |

% |

100 |

% |

|||

3

Distribution and Order Fulfillment

We take possession of our products in the country of origin and arrange for transportation to our five distribution centers located in Michigan, Oklahoma, New Jersey, Virginia and Wisconsin. We also manufacture many of our setting and maintenance materials in Michigan, Oklahoma, Virginia, and Wisconsin. We maintain a large inventory of products in order to quickly fulfill customer orders.

We fulfill customer orders primarily by shipping our products to our stores where customers can either pick them up or arrange for home delivery. We continue to evaluate logistics alternatives to best serve our store base and our customers. We believe that our existing distribution facilities will continue to play an integral role in our growth strategy, and we expect to establish one or more additional distribution centers to support geographic expansion of our store base and to support our store growth plans.

Competition

The retail tile market is highly-fragmented. We compete directly with regional and local specialty retailers of tile, factory-direct stores, a large number of privately-owned, single-site stores, and online-only competitors. In addition, we complete with large national home improvement centers that offer a wide range of home improvement products, including flooring. We also compete indirectly with companies that sell other types of floor coverings, including wood floors, carpet, and vinyl. The barriers of entry into the retail tile industry are relatively low and new or existing tile retailers could enter our markets and increase the competition that we face. Many of our competitors enjoy competitive advantages over us, such as greater name recognition, longer operating histories, more varied product offerings, and greater financial, technical, and other resources.

We believe that the key competitive factors in the retail tile industry include:

|

· |

product assortment; |

|

· |

product presentation; |

|

· |

customer service; |

|

· |

store location; |

|

· |

availability of inventory; and |

|

· |

price. |

We believe that we compete favorably with respect to each of these factors by providing a highly diverse selection of products to our customers, at an attractive value, in appealing and convenient store locations, with exceptional customer service and on-site instructional opportunities. Further, while some larger factory-direct competitors manufacture their own products, many of our competitors do not maintain their own inventory and instead purchase their tile from domestic manufacturers or distributors when they receive an order from a customer. We also believe that we offer a broader range of products and stronger in-store customer support than these competitors.

Employees

As of December 31, 2018, we had 1,738 employees, 1,626 of whom were full-time and none of whom were represented by a union. Of these employees, 1,340 work in our stores, 87 work in corporate, store support, infrastructure or similar functions, and 311 work in distribution and manufacturing facilities. We believe that we have good relations with our employees.

Property and Trademarks

We have registered and unregistered trademarks for all of our brands, including 24 registered trademarks. We regard our intellectual property as having significant value and our brands are an important factor in the marketing of our products. Accordingly, we have taken, and continue to take, appropriate steps to protect our intellectual property.

Government Regulation

We are subject to extensive and varied federal, state and local government regulation in the jurisdictions in which we operate, including laws and regulations relating to our relationships with our employees, public health and safety, zoning, and fire codes. We operate each of our stores, offices, and distribution and manufacturing facilities in accordance with standards and procedures designed to comply with applicable laws, codes, and regulations.

Our operations and properties are also subject to federal, state and local laws and regulations relating to the use, storage, handling, generation, transportation, treatment, emission, release, discharge and disposal of hazardous materials, substances, and wastes and relating to the investigation and cleanup of contaminated properties, including off-site disposal locations. We do not incur significant costs complying with environmental laws and regulations. However, we could be subject to material costs, liabilities, or claims

4

relating to environmental compliance in the future, especially in the event of changes in existing laws and regulations or in their interpretation.

Products that we import into the United States are subject to laws and regulations imposed in conjunction with such importation, including those issued and enforced by U.S. Customs and Border Protection. We work closely with our suppliers to ensure compliance with the applicable laws and regulations in these areas.

Financial Information about Geographic Areas

A majority of our revenues and profits are generated within the United States and nearly all of our long-lived assets are located within the United States as well. We have also established a sourcing office based in China.

Available Information

We are subject to the reporting requirements of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). The Exchange Act requires us to file periodic reports, proxy statements and other information with the Securities and Exchange Commission (“SEC”). The SEC maintains a website that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. These materials may be obtained electronically by accessing the SEC’s website at http://www.sec.gov.

We maintain a website at www.tileshop.com, the contents of which are not part of or incorporated by reference into this report. We make our annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K and amendments to those reports available on our website, free of charge, as soon as reasonably practicable after such reports have been filed with or furnished to the SEC. Our Code of Business Conduct and Ethics, as well as any waivers from and amendments to the Code of Business Conduct and Ethics, is also posted on our website.

The following are significant factors known to us that could adversely affect our business, financial condition, or operating results, as well as adversely affect the value of an investment in our common stock. These risks could cause our actual results to differ materially from our historical experience and from results predicted by forward-looking statements. All forward-looking statements made by us are qualified by the risks described below. There may be additional risks that are not presently material or known. You should carefully consider each of the following risks and all other information set forth in this report.

Our ability to grow and remain profitable may be limited by direct or indirect competition in the highly-competitive retail tile industry.

The retail tile industry in the United States is highly competitive. Participants in the tile industry compete primarily based on product variety, customer service, store location, and price. There can be no assurance that we will be able to continue to compete favorably with our competitors in these areas. Our store competitors include large national home centers, regional and local specialty retailers of tile, factory-direct stores, privately-owned, single-site stores and online-only competitors. We also compete indirectly with companies that sell other types of floor coverings, including wood floors, carpet, and vinyl sheet. In the past, we have faced periods of heightened competition that materially affected our results of operations. Certain of our competitors have greater name recognition, longer operating histories, more varied product offerings, and substantially greater financial and other resources than us. Accordingly, we may face periods of intense competition in the future that could have a material adverse effect on our planned growth and future results of operations. Moreover, the barriers to entry into the retail tile industry are relatively low. New or existing retailers could enter our markets and increase the competition that we face. In addition, manufacturers and suppliers of tile and related products, including those whose products we currently sell, could enter the United States retail tile market and start directly competing with us. Competition in existing and new markets may also prevent or delay our ability to gain relative market share. Any of the developments described above could have a material adverse effect on our planned growth and future results of operations.

If we fail to successfully manage the challenges that our planned growth poses or encounter unexpected difficulties during our expansion, our revenues and profitability could be materially adversely affected.

One of our long-term objectives is to increase revenue and profitability through market share gains. Our ability to achieve market share growth, however, is contingent upon our ability to open new stores and achieve operating results in new stores at the same level as our similarly situated current stores. We anticipate opening five to seven stores in 2019. There can be no assurance that we will be able to open stores in new markets at the rate required to achieve market leadership in such markets, identify and obtain favorable store sites, arrange favorable leases for stores, obtain governmental and other third-party consents, permits, and licenses needed to open or operate stores in a timely manner, train and hire a sufficient number of qualified managers for new stores, attract a strong customer base and brand familiarity in new markets, or successfully compete with established retail tile stores in the new markets that

5

we enter. Failure to open new stores in an effective and cost-efficient manner could place us at a competitive disadvantage as compared to retailers who are more adept than us at managing these challenges, which, in turn, could negatively affect our overall operating results.

Our same store sales fluctuate due to a variety of economic, operating, industry and environmental factors and may not be a fair indicator of our overall performance.

Our same store sales have experienced fluctuations, which can be expected to continue. Numerous factors affect our same store sales results, including among others, the timing of new and relocated store openings, the relative proportion of new and relocated stores to mature stores, cannibalization resulting from the opening of new stores in existing markets, changes in advertising and other operating costs, the timing and level of markdowns, changes in our product mix, weather conditions, retail trends, the retail sales environment, economic conditions, inflation, the impact of competition, and our ability to execute our business strategy. As a result, same store sales or operating results may fluctuate and may cause the price of our securities to fluctuate significantly. Therefore, we believe that period-to-period comparisons of our same store sales may not be a reliable indicator of our future overall operating performance.

We intend to open additional stores in both our existing markets and new markets, which poses both the possibility of diminishing sales by existing stores in our existing markets and the risk of a slow ramp-up period for stores in new markets.

Our expansion strategy includes plans to open five to seven additional stores in existing markets during 2019. In future periods, we intend to continue opening stores in new and existing markets. Because our stores typically draw customers from their local areas, additional stores may draw customers away from nearby existing stores and may cause same store sales performance at those existing stores to decline, which may adversely affect our overall operating results. Additionally, stores in new markets typically have a ramp-up period before sales become steady enough for such stores to be profitable. Our ability to open additional stores will be dependent on our ability to promote and/or recruit enough qualified store managers, assistant store managers, and sales associates. The time and effort required to train and supervise a large number of new managers and associates and integrate them into our culture may divert resources from our existing stores. If we are unable to profitably open additional stores in both new and existing markets and limit the adverse impact of those new stores on existing stores, our same store sales and overall operating results may be reduced during the implementation of our expansion strategy.

Our expansion strategy will be dependent upon, and limited by, the availability of adequate capital.

Our expansion strategy will require adequate capital for, among other purposes, opening new stores, distribution centers, and manufacturing facilities, as well as entering new markets. Such expenditures will include researching real estate and consumer markets, leases, inventory, property and equipment costs, integration of new stores and markets into company-wide systems and programs, and other costs associated with new stores and market entry expenses and growth. If cash generated internally is insufficient to fund capital requirements, we will require additional debt or equity financing. Adequate financing may not be available or, if available, may not be available on terms satisfactory to us. In addition, our credit facility may limit the amount of capital expenditures that we may make annually, depending on our leverage ratio. If we fail to obtain sufficient additional capital in the future or we are unable to make capital expenditures under our credit facility, we could be forced to curtail our expansion strategies by reducing or delaying capital expenditures relating to new stores and new market entry. As a result, there can be no assurance that we will be able to fund our current plans for the opening of new stores or entry into new markets.

If we fail to identify and maintain relationships with a sufficient number of suppliers, our ability to obtain products that meet our high quality standards at attractive prices could be adversely affected.

We purchase flooring and other products directly from suppliers located around the world. However, we do not have long-term contractual supply agreements with our suppliers that obligate them to supply us with products exclusively or at specified quantities or prices. As a result, our current suppliers may decide to sell products to our competitors and may not continue selling products to us. In order to retain the competitive advantage that we believe results from these relationships, we need to continue to identify, develop and maintain relationships with qualified suppliers that can satisfy our high standards for quality and our requirements for flooring and other products in a timely and efficient manner at attractive prices. The need to develop new relationships will be particularly important as we seek to expand our operations and enhance our product offerings in the future. The loss of one or more of our existing suppliers or our inability to develop relationships with new suppliers could reduce our competitiveness, slow our plans for further expansion, and cause our net sales and operating results to be adversely affected.

We source the approximately 6,000 products that we stock and sell from approximately 250 domestic and international suppliers. We source a large number of those products from foreign manufacturers, including 49% of our products from a group of ten suppliers located in Asia, Europe and the United States. Our largest supplier accounted for approximately 14% of our total purchases in 2018. We generally take title to these products sourced from foreign suppliers overseas and are responsible for arranging shipment to our distribution centers. Financial instability among key suppliers, political instability, trade restrictions, tariffs, currency exchange rates,

6

and transport capacity and costs are beyond our control and could negatively impact our business if they seriously disrupt the movement of products through our supply chain or increase the costs of our products.

Our ability to offer compelling products, particularly products made of unique stone, depends on the continued availability of sufficient suitable natural products.

Our business strategy depends on offering a wide assortment of compelling products to our customers. We sell, among other things, products made from various natural stones from quarries throughout the world. Our ability to obtain an adequate volume and quality of hard-to-find products depends on our suppliers’ ability to furnish those products, which, in turn, could be affected by many things, including the exhaustion of stone quarries. If our suppliers cannot deliver sufficient products, and we cannot find replacement suppliers, our net sales and operating results may be adversely affected.

If our suppliers do not use ethical business practices or comply with applicable laws and regulations, our reputation could be harmed due to negative publicity and we could be subject to legal risk.

We do not control the operations of our suppliers. Accordingly, we cannot guarantee that our suppliers will comply with applicable environmental and labor laws and regulations or operate in a legal, ethical, and responsible manner. Violation of environmental, labor or other laws by our suppliers or their failure to operate in a legal, ethical, or responsible manner could reduce demand for our products if, as a result of such violation or failure, we attract negative publicity. Further, such conduct could expose us to legal risks as a result of the purchase of products from non-compliant suppliers.

If customers are unable to obtain third-party financing at satisfactory rates, sales of our products could be materially adversely affected.

Our business, financial condition, and results of operations have been, and may continue to be affected, by various economic factors. Deterioration in the current economic environment could lead to reduced consumer and business spending, including by our customers. It may also cause customers to shift their spending to products that we either do not sell or that generate lower profitably for us. Further, reduced access to credit may adversely affect the ability of consumers to purchase our products. This potential reduction in access to credit may adversely impact our ability to offer customers credit card financing through third-party credit providers on terms similar to those offered currently, or at all. In addition, economic conditions, including decreases in access to credit, may result in financial difficulties leading to restructuring, bankruptcies, liquidations and other unfavorable events for our customers, which may adversely impact our industry, business, and results of operations.

Any failure by us to successfully anticipate consumer trends may lead to loss of consumer acceptance of our products, resulting in reduced revenues.

Our success depends on our ability to anticipate and respond to changing trends in the tile industry and consumer demands in a timely manner. If we fail to identify and respond to emerging trends, consumer acceptance of our merchandise and our image with current or potential customers may be harmed, which could reduce our revenue potential. Additionally, if we misjudge market trends, we may significantly overstock unpopular products and be forced to reduce the sales price of such products, which would have a negative impact on our gross profit and cash flow. Conversely, shortages of products that prove popular could cause customers to seek alternative sources of such products, as well as other products they may have purchased from us, which could also reduce our revenues.

We depend on a few key employees, and if we lose the services of these employees, we may not be able to run our business effectively.

Our future success depends in part on our ability to attract and retain key executive, merchandising, marketing, and sales personnel. If any of these key employees ceases to be employed by us, we would have to hire additional qualified personnel. Our ability to successfully hire other experienced and qualified key employees cannot be assured and may be difficult because we face competition for these professionals from our competitors, our suppliers and other companies operating in our industry. As a result, the loss or unavailability of any of our key employees could have a material adverse effect on us.

If we fail to hire, train, and retain qualified store managers, sales associates, and other employees, our enhanced customer service could be compromised and we could lose sales to our competitors.

A key element of our competitive strategy is to provide product expertise to our customers through our extensively trained, commissioned sales associates. If we are unable to attract and retain qualified personnel and managers as needed in the future, including qualified sales personnel, our level of customer service may decline, which may decrease our revenues and profitability.

7

The burden of debt under our existing credit facility and additional debt could adversely affect us, make us more vulnerable to adverse economic or industry conditions, and prevent us from fulfilling our debt obligations or from funding our strategies.

We entered into a credit facility with Bank of America, N.A., Fifth Third Bank and Citizens Bank on September 18, 2018. As of December 31, 2018, we had borrowed approximately $53.0 million on our revolving line of credit, leaving $45.9 million available for future borrowings. The terms of our credit facility and the burden of the indebtedness incurred thereunder could have serious consequences for us, such as:

|

· |

limiting our ability to obtain additional financing to fund our working capital, capital expenditures, debt service requirements, expansion strategy, or other needs; |

|

· |

placing us at a competitive disadvantage compared to competitors with less debt; |

|

· |

increasing our vulnerability to, and reducing our flexibility in planning for, adverse changes in economic, industry, and competitive conditions; and |

|

· |

increasing our vulnerability to increases in interest rates if borrowings under the credit facility are subject to variable interest rates. |

Our credit facility also contains negative covenants that limit our ability to engage in specified types of transactions. These covenants limit our ability to, among other things:

|

· |

incur indebtedness; |

|

· |

create liens; |

|

· |

engage in mergers or consolidations; |

|

· |

sell assets (including pursuant to sale and leaseback transactions); |

|

· |

make investments, acquisitions, loans, or advances; |

|

· |

engage in certain transactions with affiliates; |

|

· |

enter into agreements limiting subsidiary distributions; |

|

· |

enter into agreements limiting the ability to create liens; |

|

· |

amend our organizational documents in a way that has a material effect on the lenders or administrative agent under our credit facility; and |

|

· |

change our lines of business. |

A breach of any of these covenants could result in an event of default under our credit facility. Upon the occurrence of an event of default, the lender could elect to declare all amounts outstanding under such facility to be immediately due and payable and terminate all commitments to extend further credit, or seek amendments to our debt agreements that would provide for terms more favorable to such lender and that we may have to accept under the circumstances. If we were unable to repay those amounts, the lender under our credit facility could proceed against the collateral granted to it to secure that indebtedness.

If we are unable to renew or replace current store leases, or if we are unable to enter into leases for additional stores on favorable terms, or if one or more of our current leases is terminated prior to expiration of its stated term and we cannot find suitable alternate store locations, our growth and profitability could be negatively impacted.

We currently lease all of our store locations and certain distribution center locations. Many of our current leases provide us with the unilateral option to renew for several additional rental periods at specific rental rates. Our ability to renegotiate favorable terms on an expiring lease or to negotiate favorable terms for a suitable alternate location, and our ability to negotiate favorable lease terms for additional store locations, could depend on conditions in the real estate market, competition for desirable properties, our relationships with current and prospective landlords, or other factors that are not within our control. Any or all of these factors and conditions could negatively impact our growth and profitability.

Compliance with laws or changes in existing or new laws and regulations or regulatory enforcement priorities could adversely affect our business.

We must comply with various laws and regulations at the local, regional, state, federal, and international levels. These laws and regulations change frequently and such changes can impose significant costs and other burdens of compliance on our business and suppliers. Any changes in regulations, the imposition of additional regulations, or the enactment of any new legislation that affects employment/labor, trade, product safety, transportation/logistics, energy costs, health care, tax, environmental issues, or compliance with the Foreign Corrupt Practices Act could have an adverse impact on our financial condition and results of operations. Changes in

8

enforcement priorities by governmental agencies charged with enforcing existing laws and regulations could increase our cost of doing business.

We may also be subject to audits by various taxing authorities. Changes in tax laws in any of the multiple jurisdictions in which we operate, or adverse outcomes from tax audits that we may be subject to in any of the jurisdictions in which we operate, could result in an unfavorable change in our effective tax rate, which could have an adverse effect on our business and results of operations.

Our results may be adversely affected by fluctuations in material and energy costs.

Our results may be affected by the prices of the materials used in the manufacture of tile, setting and maintenance materials, and related accessories that we sell. These prices may fluctuate based on a number of factors beyond our control, including: oil prices, changes in supply and demand, general economic conditions, labor costs, competition, import duties, tariffs, currency exchange rates, and government regulation. In addition, energy costs have fluctuated dramatically in the past and may fluctuate in the future. These fluctuations may result in an increase in our transportation costs for distribution from the manufacturer to our distribution centers and from our regional distribution centers to our stores, utility costs for our distribution and manufacturing centers and stores, and overall costs to purchase products from our suppliers.

We may not be able to adjust the prices of our products, especially in the short-term, to recover these cost increases in materials and energy. A continual rise in material and energy costs could adversely affect consumer spending and demand for our products and increase our operating costs, both of which could have a material adverse effect on our financial condition and results of operations.

Our success is highly dependent on our ability to provide timely delivery to our customers, and any disruption in our delivery capabilities or our related planning and control processes may adversely affect our operating results.

Our success is due in part to our ability to deliver products quickly to our customers, which requires successful planning and distribution infrastructure, including ordering, transportation and receipt processing, and the ability of suppliers to meet distribution requirements. Our ability to maintain this success depends on the continued identification and implementation of improvements to our planning processes, distribution infrastructure, and supply chain. We also need to ensure that our distribution infrastructure and supply chain keep pace with our anticipated growth and increased number of stores. The cost of these enhanced processes could be significant and any failure to maintain, grow, or improve them could adversely affect our operating results. Our business could also be adversely affected if there are delays in product shipments due to freight difficulties, strikes, or other difficulties at our suppliers’ principal transport providers, or otherwise.

Our success depends on the effectiveness of our marketing strategy.

We believe that our growth was achieved in part through the effectiveness of our marketing strategies. Prior to 2018, we used internet, print, and radio advertisements containing discounts and promotional offers to encourage customers to visit our stores. A significant portion of our advertising was invested to support the opening of new stores and directed at professional customers. Beginning in late 2017, we de-emphasized the use of discount offers to attract customers. Limited use of discount and promotional offers in future periods could fail to attract customers, resulting in a decrease in store traffic. While our marketing strategy continues to support our growth strategy and remains focused on professional customers, we have broadened the reach and frequency of our advertising to increase the recognition of our value proposition and the number of customers served. We may need to further increase our marketing expense to support our business strategies in the future. If our marketing strategies fail to draw customers in the future, or if the cost of advertising or other marketing materials increases significantly, we could experience declines in our net sales and operating results.

Natural disasters, changes in climate and geo-political events could adversely affect our operating results.

The threat or occurrence of one or more natural disasters or other extreme weather events, whether as a result of climate change or otherwise, and the threat or outbreak of terrorism, civil unrest or other hostilities or conflicts could materially adversely affect our financial performance. These events may result in damage to, destruction or closure of, our stores, distribution centers and other properties. Such events can also adversely affect our work force and prevent employees and customers from reaching our stores and other properties, can modify consumer purchasing patterns and decrease disposable income, and can disrupt or disable portions of our supply chain and distribution network.

Our ability to control labor costs is limited, which may negatively affect our business.

Our ability to control labor costs is subject to numerous external factors, including prevailing wage rates, the impact of legislation or regulations governing healthcare benefits or labor relations, such as the Affordable Care Act, and health and other insurance costs. If our labor and/or benefit costs increase, we may not be able to hire or maintain qualified personnel to the extent necessary to execute our competitive strategy, which could adversely affect our results of operations.

9

Our business operations could be disrupted if we are unable to protect the integrity and security of our customer information.

In connection with payment card sales and other transactions, including bank cards, debit cards, credit cards and other merchant cards, we process and transmit confidential banking and payment card information. Additionally, as part of our normal business activities, we collect and store sensitive personal information related to our employees, customers, suppliers and other parties. Despite our security measures, our information technology and infrastructure may be vulnerable to criminal cyber-attacks or security incidents due to employee error, malfeasance or other vulnerabilities. Any such incidents could compromise our networks and the information stored there could be accessed, publicly disclosed, lost or stolen. Third parties may have the technology and know-how to breach the security of this information, and our security measures and those of our banks, merchant card processing and other technology suppliers may not effectively prohibit others from obtaining improper access to this information. The techniques used by criminals to obtain unauthorized access to sensitive data change frequently and often are not recognized until launched against a target; accordingly, we may be unable to anticipate these techniques or implement adequate preventative measures.

Many states have enacted laws requiring companies to notify individuals of data security breaches involving their personal data. These mandatory disclosures regarding a security breach often lead to widespread negative publicity, which may cause our customers to lose confidence in the effectiveness of our data security measures. Any security breach, whether successful or not, would harm our reputation and could cause the loss of customers.

If our management information systems experience disruptions, it could disrupt our business and reduce our net sales.

We depend on our management information systems to integrate the activities of our stores, to process orders, to manage inventory, to purchase merchandise and to sell and ship goods on a timely basis. We may experience operational problems with our information systems as a result of system failures, viruses, computer “hackers” or other causes. We may incur significant expenses in order to repair any such operational problems. Any significant disruption or slowdown of our systems could cause information, including data related to customer orders, to be lost or delayed, which could result in delays in the delivery of products to our stores and customers or lost sales. Accordingly, if our network is disrupted, we may experience delayed communications within our operations and between our customers and ourselves.

The selection and implementation of information technology initiatives may impact our operational efficiency and productivity.

In order to better manage our business, we expect to invest in our information systems. In doing so, we must select the correct investments and implement them in an efficient manner. The costs, potential problems and interruptions associated with implementing technology initiatives could disrupt or reduce the efficiency of our operations. Furthermore, these initiatives might not provide the anticipated benefits or provide them in a delayed or more costly manner. Accordingly, issues relating to our selection and implementation of information technology initiatives may negatively impact our business and operating results.

Our insurance coverage and self-insurance reserves may not cover future claims.

We maintain various insurance policies for employee health and workers’ compensation. We are self-insured on certain health insurance plans and are responsible for losses up to a certain limit for these respective plans. We are also self-insured with regard to workers’ compensation coverage, in which case we are responsible for losses up to certain retention limits on both a per-claim and aggregate basis.

For policies under which we are responsible for losses, we record a liability that represents our estimated cost of claims incurred and unpaid as of the balance sheet date. Our estimated liability is not discounted and is based on a number of assumptions and factors, including historical trends and economic conditions, and is closely monitored and adjusted when warranted by changing circumstances. Fluctuating healthcare costs, our significant growth rate and changes from our past experience with workers’ compensation claims could affect the accuracy of estimates based on historical experience. Should a greater amount of claims occur compared to what was estimated or employee health insurance costs increase beyond what was expected, our accrued liabilities might not be sufficient, and we may be required to record additional expense. Unanticipated changes may produce materially different amounts of expense than that reported under these programs, which could adversely impact our operating results.

We are involved in legal proceedings and, while we cannot predict the outcomes of such proceedings and other contingencies with certainty, some of these outcomes could adversely affect our business, financial condition and results of operations.

We are, and may become, involved in shareholder, consumer, employment, tort or other litigation. We cannot predict with certainty the outcomes of these legal proceedings. The outcome of some of these legal proceedings could require us to take, or refrain from taking, actions which could negatively affect our operations or could require us to pay substantial amounts of money adversely affecting our financial condition and results of operations. Additionally, defending against lawsuits and proceedings may involve significant expense and diversion of management's attention and resources.

10

The market price of our securities may decline and/or be volatile.

The market price of our common stock has fluctuated significantly in the past and may continue to fluctuate in the future. Future fluctuations could be based on various factors in addition to those otherwise described in this report, including:

|

· |

our operating performance and the performance of our competitors; |

|

· |

the public’s reaction to our filings with the SEC, our press releases and other public announcements; |

|

· |

changes in recommendations or earnings estimates by research analysts who follow us or other companies in our industry; |

|

· |

variations in general economic conditions; |

|

· |

actions of our current stockholders, including sales of common stock by our directors and executive officers; |

|

· |

the arrival or departure of key personnel; and |

|

· |

other developments affecting us, our industry or our competitors. |

In addition, the stock market may experience significant price and volume fluctuations. These fluctuations may be unrelated to the operating performance of particular companies but may cause declines in the market price of our common stock. The price of our common stock could fluctuate based upon factors that have little or nothing to do with our company or its performance.

If we discontinue or alter our quarterly dividend program, or if we are unable to pay quarterly dividends at intended levels, our reputation and stock price may be harmed.

The payment of, or continuation of, our quarterly dividend is at the discretion of our Board of Directors and is dependent upon our financial condition, results of operations, capital requirements, general business conditions, tax treatment of dividends in the United States, potential future contractual restrictions contained in credit agreements and other agreements and other factors deemed relevant by our Board of Directors. Additionally, because our quarterly dividend program requires the use of a moderate portion of our cash flow, our ability to pay dividends will depend on our ability to generate sufficient cash flows from operations in the future. This ability may be subject to certain economic, financial, competitive and other factors that are beyond our control. Any failure to pay quarterly dividends after we have announced our intention to do so, or any changes to our quarterly dividend program, may negatively impact our reputation, our stock price, and investor confidence in us.

We are a holding company with no business operations of our own and depend on cash flow from The Tile Shop to meet our obligations.

We are a holding company with no business operations of our own or material assets other than the equity of our subsidiaries. All of our operations are conducted by our subsidiary, The Tile Shop. As a holding company, we will require dividends and other payments from our subsidiaries to meet cash requirements. The terms of any future credit facility may restrict our subsidiaries from paying dividends and otherwise transferring cash or other assets to us, although our current facility does not restrict this action. If there is an insolvency, liquidation, or other reorganization of any of our subsidiaries, our stockholders likely will have no right to proceed against their assets. Creditors of those subsidiaries will be entitled to payment in full from the sale or other disposal of the assets of those subsidiaries before us, as an equity holder, would be entitled to receive any distribution from that sale or disposal. If The Tile Shop is unable to pay dividends or make other payments to us when needed, we will be unable to satisfy our obligations.

Concentration of ownership may have the effect of delaying or preventing a change in control.

Our directors and executive officers, together with their affiliates, beneficially hold approximately 27% of our outstanding shares of common stock. As a result, these stockholders, if acting together, have the ability to influence the outcome of corporate actions requiring stockholder approval. This concentration of ownership may have the effect of delaying or preventing a change in control and might adversely affect the market price of our securities.

11

Anti-takeover provisions contained in our certificate of incorporation and bylaws, as well as provisions of Delaware law, could impair a takeover attempt.

Our certificate of incorporation and bylaws contain provisions that, alone or together, could have the effect of delaying or preventing hostile takeovers or changes in control or changes in our management without the consent of our Board of Directors. These provisions include:

|

· |

a classified Board of Directors with three-year staggered terms, which may delay the ability of stockholders to change the membership of a majority of our Board of Directors; |

|

· |

no cumulative voting in the election of directors, which limits the ability of minority stockholders to elect director candidates; |

|

· |

the exclusive right of our Board of Directors to elect a director to fill a vacancy created by the expansion of the Board of Directors or the resignation, death, or removal of a director, which prevents stockholders from being able to fill vacancies on our Board of Directors; |

|

· |

the ability of our Board of Directors to determine whether to issue shares of preferred stock and to determine the price and other terms of those shares, including preferences and voting rights, without stockholder approval, which could be used to significantly dilute the ownership of a hostile acquirer; |

|

· |

a prohibition on stockholder action by written consent, which forces stockholder action to be taken at an annual or special meeting of our stockholders; |

|

· |

the requirement that a special meeting of stockholders may be called only by the chairman of the Board of Directors, the chief executive officer, or the Board of Directors, which may delay the ability of our stockholders to force consideration of a proposal or to take action, including the removal of directors; |

|

· |

limiting the liability of, and providing indemnification to, our directors and officers; |

|

· |

controlling the procedures for the conduct and scheduling of stockholder meetings; |

|

· |

providing the Board of Directors with the express power to postpone previously scheduled annual meetings of stockholders and to cancel previously scheduled special meetings of stockholders; |

|

· |

providing that directors may be removed prior to the expiration of their terms by stockholders only for cause; and |

|

· |

advance notice procedures that stockholders must comply with in order to nominate candidates to our Board of Directors or to propose matters to be acted upon at a stockholders’ meeting, which may discourage or deter a potential acquirer from conducting a solicitation of proxies to elect the acquirer’s own slate of directors or otherwise attempting to obtain control of us. |

As a Delaware corporation, we are also subject to provisions of Delaware law, including Section 203 of the Delaware General Corporation Law, which prevents some stockholders holding more than 15% of our outstanding common stock from engaging in certain business combinations without approval of the holders of substantially all of our outstanding common stock. Any provision of our certificate of incorporation or bylaws or Delaware law that has the effect of delaying or deterring a change in control could limit the opportunity for our stockholders to receive a premium for their shares of our common stock, and could also affect the price that some investors are willing to pay for our common stock.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

12

As of December 31, 2018, we operated 140 stores located in 31 states and the District of Columbia with an average square footage of approximately 20,200 square feet. The table below sets forth the store locations (alphabetically by state) of our 140 stores in operation as of December 31, 2018.

|

|

||||||||||

|

State |

Stores |

State |

Stores |

State |

Stores |

State |

Stores |

|||

|

Arkansas |

1 |

Iowa |

1 |

Minnesota |

7 |

Oklahoma |

2 | |||

|

Arizona |

4 |

Illinois |

11 |

Missouri |

5 |

Pennsylvania |

5 | |||

|

Colorado |

4 |

Indiana |

4 |

North Carolina |

4 |

Rhode Island |

1 | |||

|

Connecticut |

3 |

Kansas |

2 |

Nebraska |

1 |

South Carolina |

2 | |||

|

Delaware |

1 |

Kentucky |

3 |

New Jersey |

7 |

Tennessee |

4 | |||

|

District of Columbia |

1 |

Massachusetts |

3 |

New Mexico |

1 |

Texas |

17 | |||

|

Florida |

5 |

Maryland |

5 |

New York |

8 |

Virginia |

6 | |||

|

Georgia |

4 |

Michigan |

7 |

Ohio |

8 |

Wisconsin |

3 | |||

|

|

Total |

140 |

We lease all of our stores. Our approximately 15,000 square foot headquarters in Plymouth, Minnesota is attached to our store. We own four regional facilities used for distribution of purchased product and manufacturing of setting and maintenance materials, located in Spring Valley, Wisconsin; Ottawa Lake, Michigan; Ridgeway, Virginia; and Durant, Oklahoma, which consist of 69,000, 271,000, 134,000, and 260,000 square feet, respectively. We also lease a distribution facility in Dayton, New Jersey that is 103,000 square feet.

We believe that our material property holdings are suitable for our current operations and purposes. We intend to open five to seven new stores in 2019.

The Company is, from time to time, subject to claims and disputes arising in the normal course of business. In the opinion of management, while the outcome of such claims and disputes cannot be predicted with certainty, the Company’s ultimate liability in connection with these matters is not expected to have a material adverse effect on the results of operations, financial position, or cash flows.

ITEM 4. MINE SAFETY DISCLOSURES

None.

13

Part II

ITEM 5. MARKET FOR THE REGISTRANT'S COMMON EQUITY, RELATED SHAREHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our common stock is traded on The Nasdaq Stock Market under the symbol “TTS”.

As of February 22, 2019, we had approximately 129 holders of record of our common stock. This figure does not include the number of persons whose securities are held in nominee or “street” name accounts through brokers.

As of February 22, 2019, we had 52,921,546 shares of common stock outstanding. The last reported sales price for our common stock on February 22, 2019 was $6.14.

Dividends Paid Per Share

|

|

|

|

|

|

|

|

|

|

|

Date Paid |

|

|

Amount |

|

March 24, 2017 |

|

$ |

0.05 |

|

May 16, 2017 |

|

$ |

0.05 |

|

August 15, 2017 |

|

$ |

0.05 |

|

November 14, 2017 |

|

$ |

0.05 |

|

March 16, 2018 |

|

$ |

0.05 |

|

May 11, 2018 |

|

$ |

0.05 |

|

August 10, 2018 |

|

$ |

0.05 |

|

November 9, 2018 |

|

$ |

0.05 |

Prior to 2017, we did not pay dividends to our stockholders. Our first dividend was paid on March 24, 2017. On February 19, 2019 we declared a $0.05 dividend to stockholders of record as of the close of business on March 4, 2019. This is our 9th consecutive quarterly dividend. The dividend will be paid on March 15, 2019. We intend to continue to pay quarterly dividends in the future; however, we may suspend or change this program at any time and there can be no guarantee that we will continue to pay dividends in any specific amount or at any specific time.

Securities Authorized for Issuance Under Equity Compensation Plans

For information on our equity compensation plans, refer to Item 12, “Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters.”

Recent Sales of Unregistered Securities

None.

Issuer Purchases of Equity Securities

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Number of Shares Purchased |

|

Average Price Paid per Share |

|

Total Number of Shares Purchased as Part of Publicly Announced Plans or Program |

|

Maximum Number of Shares that May Yet be Purchased Under Plans or Programs |

|

|

October 1, 2018 - October 31, 2018 |

|

30,622 |

(1) |

$ |

1.43 |

(1) |

- |

|

- |

|

November 1, 2018 - November 30, 2018 |

|

14,454 |

(2) |

|

1.65 |

(2) |

- |

|

- |

|

December 1, 2018 - December 31, 2018 |

|

13,150 |

(3) |

|

0.00 |

(3) |

- |

|

- |

|

|

|

58,226 |

|

$ |

1.16 |

|

- |

|

- |

|

(1) |

We withheld total of 6,547 shares to satisfy tax withholding obligations due upon the vesting of restricted stock grants, as allowed by the 2012 Omnibus Incentive Plan (the “2012 Plan”). We did not pay cash to repurchase these shares, nor were these repurchases part of a publicly announced plan or program. We repurchased the remaining 24,075 shares pursuant to the terms of the underlying restricted stock agreements, as allowed by the 2012 Plan. We paid $0.0001 per share, the par value, to repurchase these shares. These repurchases were not part of a publicly announced plan or program. |

|

(2) |

We withheld total of 3,633 shares to satisfy tax withholding obligations due upon the vesting of restricted stock grants, as allowed by the 2012 Plan. We did not pay cash to repurchase these shares, nor were these repurchases part of a publicly announced plan or program. We repurchased remaining 10,821 shares pursuant to the terms of the underlying restricted stock agreements, as allowed

14 |

by the 2012 Plan. We paid $0.0001 per share, the par value, to repurchase these shares. These repurchases were not part of a publicly announced plan or program. |

|

(3) |

We repurchased these shares pursuant to the terms of the underlying restricted stock agreements, as allowed by the 2012 Plan. We paid $0.0001 per share, the par value, to repurchase these shares. These repurchases were not part of a publicly announced plan or program. |

Stock Performance Graph

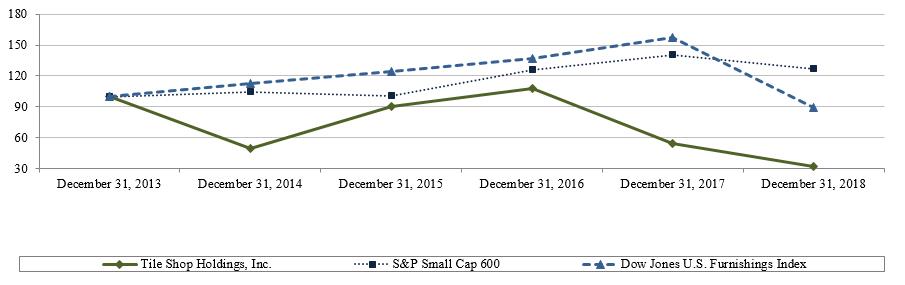

The graph and table below present our cumulative total stockholder returns relative to the performance of the S&P SmallCap 600 and the Dow Jones U.S. Furnishings Index for the period commencing December 31, 2014 and ending December 31, 2018, the last trading day of fiscal year 2018. The comparison assumes $100 invested at the close of trading on December 31, 2013 in (i) our common stock, (ii) the stocks comprising the S&P SmallCap 600, and (iii) the stocks comprising the Dow Jones U.S. Furnishings Index. All values assume that all dividends were reinvested on the date paid. The points on the graph represent fiscal quarter-end amounts based on the last trading day in each fiscal quarter. The stock price performance included in the line graph below is not necessarily indicative of future stock price performance.

|

|

|||||||||

|

|

Tile Shop Holdings, Inc. |

S&P Small Cap 600 |

Dow Jones |

||||||

|

December 31, 2013 |

$ |

100.00 |

$ |

100.00 |

$ |

100.00 | |||

|

December 31, 2014 |

$ |

49.14 |

$ |

104.44 |

$ |

112.97 | |||

|

December 31, 2015 |

$ |

90.76 |

$ |

100.93 |

$ |

124.17 | |||

|

December 31, 2016 |

$ |

108.19 |

$ |

125.91 |

$ |

137.39 | |||

|

December 31, 2017 |

$ |

53.90 |

$ |

140.68 |

$ |

157.31 | |||

|

December 31, 2018 |

$ |

31.70 |

$ |

126.96 |

$ |

88.98 | |||

15

ITEM 6. SELECTED FINANCIAL DATA

The following table sets forth selected historical financial information derived from (i) our audited financial statements included elsewhere in this report as of December 31, 2018 and 2017 and for the years ended December 31, 2018, 2017, and 2016 and (ii) our audited financial statements not included elsewhere in this report as of December 31, 2016, 2015, and 2014 and for the years ended December 31, 2015 and 2014. The following selected financial data should be read in conjunction with the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the financial statements and the related notes appearing elsewhere in this report.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

As of December 31, or for the year ended December 31, |

|

|||||||||||||||||

|

|

|

2018 |

|

|

2017 |

|

|

2016 |

|

|

2015 |

|

|

2014 |

|

|||||

|

|

|

(in thousands, except per share) |

|

|||||||||||||||||

|

Statement of Income Data |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net sales |

|

$ |

357,254 |

|

|

$ |

344,600 |

|

|

$ |

324,157 |

|

|

$ |

292,987 |

|

|

$ |

257,192 |

|

|

Cost of sales |

|

|

105,915 |

|

|

|

108,378 |

|

|

|

97,261 |

|

|

|

89,377 |

|

|

|

78,300 |

|

|

Gross profit |

|

|

251,339 |

|

|

|

236,222 |

|

|

|

226,896 |

|

|

|

203,610 |

|

|

|

178,892 |

|

|

Selling, general and administrative |

|

|

233,201 |

|

|

|

210,376 |

|

|

|

193,983 |

|

|

|

174,384 |

|

|

|

157,316 |

|

|

Income from operations |

|

|

18,138 |

|

|

|

25,846 |

|

|

|

32,913 |

|

|

|

29,226 |

|

|

|

21,576 |

|

|

Interest expense |

|

|

(2,690) |

|

|

|

(1,857) |

|

|

|

(1,715) |

|

|

|

(2,584) |

|

|

|

(3,141) |

|

|

Other income (expense) |

|

|

152 |

|

|

|

170 |

|

|

|

141 |

|

|

|

130 |

|

|

|

(506) |

|

|

Income before income taxes |

|

|

15,600 |

|

|

|

24,159 |

|

|

|

31,339 |

|