FORD MOTOR CO - Annual Report: 2016 (Form 10-K)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

(Mark One) | |

R | Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended December 31, 2016 | |

or | |

o | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from __________ to __________ | |

Commission file number 1-3950 | |

Ford Motor Company

(Exact name of Registrant as specified in its charter)

Delaware | 38-0549190 |

(State of incorporation) | (I.R.S. Employer Identification No.) |

One American Road, Dearborn, Michigan | 48126 |

(Address of principal executive offices) | (Zip Code) |

313-322-3000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered* | |

Common Stock, par value $.01 per share | New York Stock Exchange | |

__________

* In addition, shares of Common Stock of Ford are listed on certain stock exchanges in Europe.

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑

Indicate by check mark if the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☑ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. R

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. Large accelerated filer R Accelerated filer ☐ Non-accelerated filer ☐ Smaller reporting company ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☑

As of June 30, 2016, Ford had outstanding 3,902,375,117 shares of Common Stock and 70,852,076 shares of Class B Stock. Based on the New York Stock Exchange Composite Transaction closing price of the Common Stock on that date ($12.57 per share), the aggregate market value of such Common Stock was $49,052,855,221. Although there is no quoted market for our Class B Stock, shares of Class B Stock may be converted at any time into an equal number of shares of Common Stock for the purpose of effecting the sale or other disposition of such shares of Common Stock. The shares of Common Stock and Class B Stock outstanding at June 30, 2016 included shares owned by persons who may be deemed to be “affiliates” of Ford. We do not believe, however, that any such person should be considered to be an affiliate. For information concerning ownership of outstanding Common Stock and Class B Stock, see the Proxy Statement for Ford’s Annual Meeting of Stockholders currently scheduled to be held on May 11, 2017 (our “Proxy Statement”), which is incorporated by reference under various Items of this Report as indicated below.

As of January 31, 2017, Ford had outstanding 3,903,445,093 shares of Common Stock and 70,852,076 shares of Class B Stock. Based on the New York Stock Exchange Composite Transaction closing price of the Common Stock on that date ($12.36 per share), the aggregate market value of such Common Stock was $48,246,581,349.

DOCUMENTS INCORPORATED BY REFERENCE

Document | Where Incorporated | |

Proxy Statement* | Part III (Items 10, 11, 12, 13, and 14) | |

__________

* | As stated under various Items of this Report, only certain specified portions of such document are incorporated by reference in this Report. |

Exhibit Index begins on page

FORD MOTOR COMPANY

ANNUAL REPORT ON FORM 10-K

For the Year Ended December 31, 2016

Table of Contents | Page | ||

Part I | |||

Item 1 | Business | ||

Overview | |||

Automotive Segment | |||

Financial Services Segment | |||

Governmental Standards | |||

Employment Data | |||

Engineering, Research, and Development | |||

Item 1A | Risk Factors | ||

Item 1B | Unresolved Staff Comments | ||

Item 2 | Properties | ||

Item 3 | Legal Proceedings | ||

Item 4 | Mine Safety Disclosures | ||

Item 4A | Executive Officers of Ford | ||

Part II | |||

Item 5 | Market for Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | ||

Item 6 | Selected Financial Data | ||

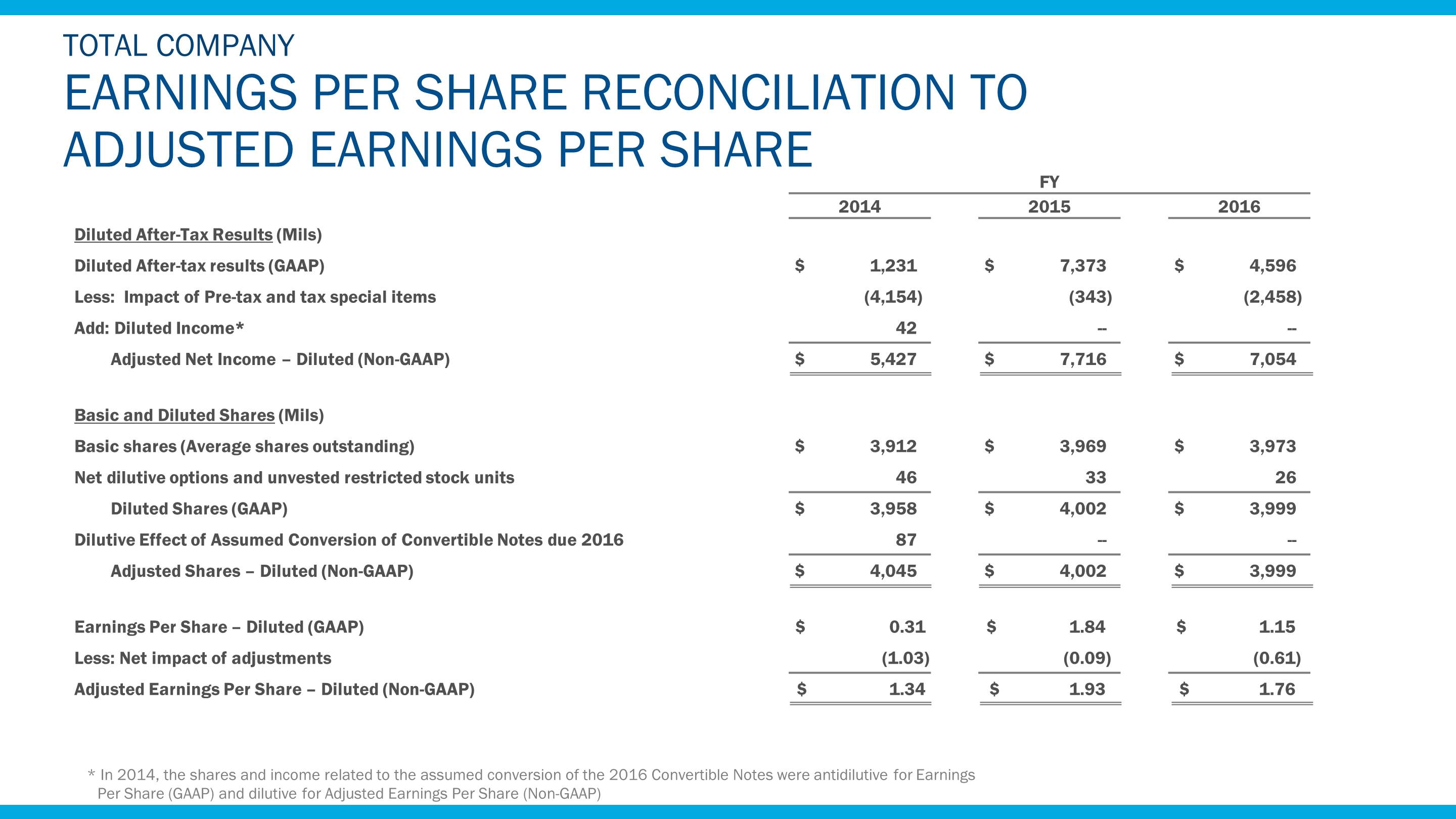

Item 7 | Management’s Discussion and Analysis of Financial Condition and Results of Operations | ||

Overview | |||

Results of Operations - 2016 | |||

Automotive Segment | |||

Financial Services Segment | |||

All Other | |||

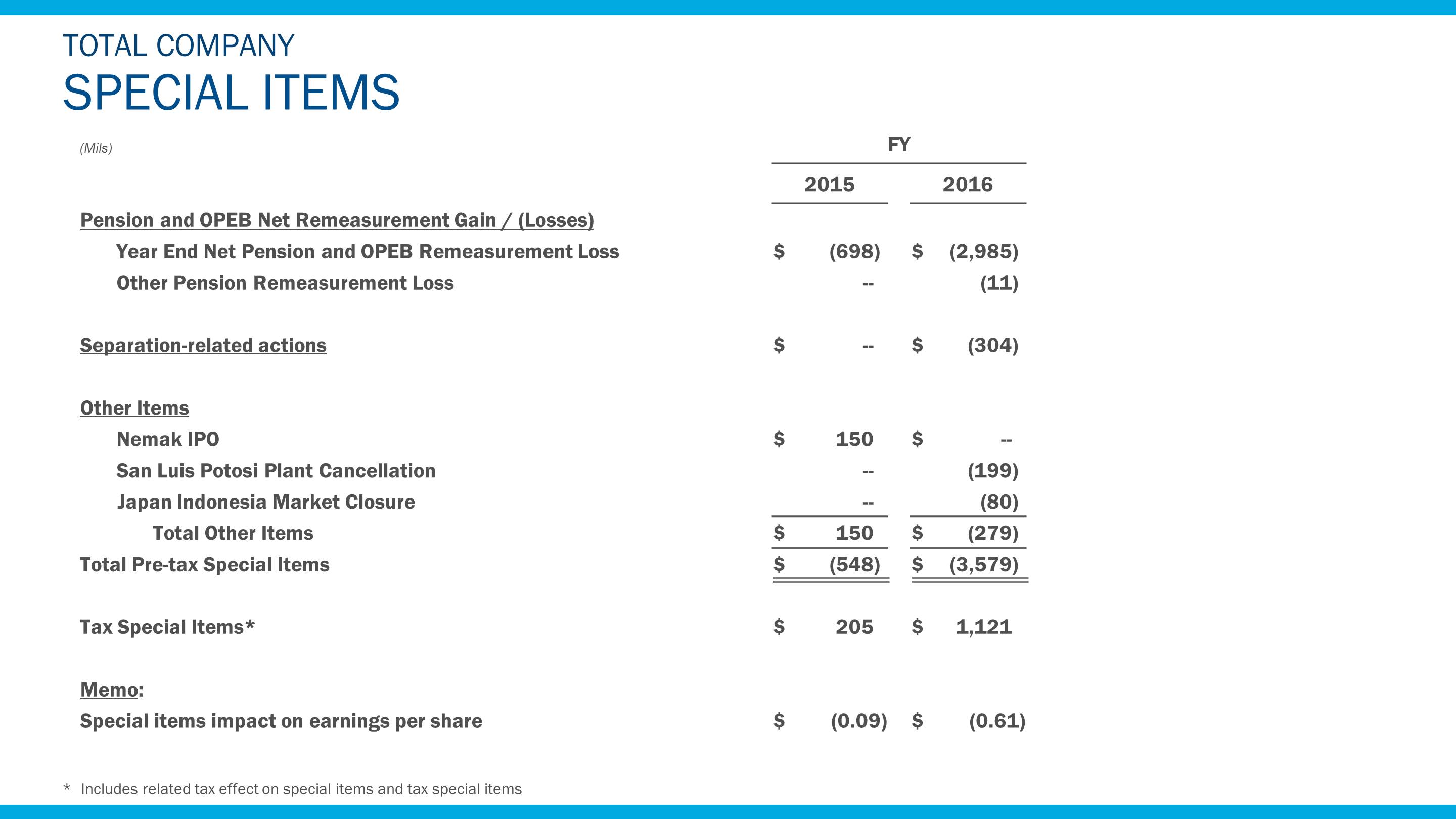

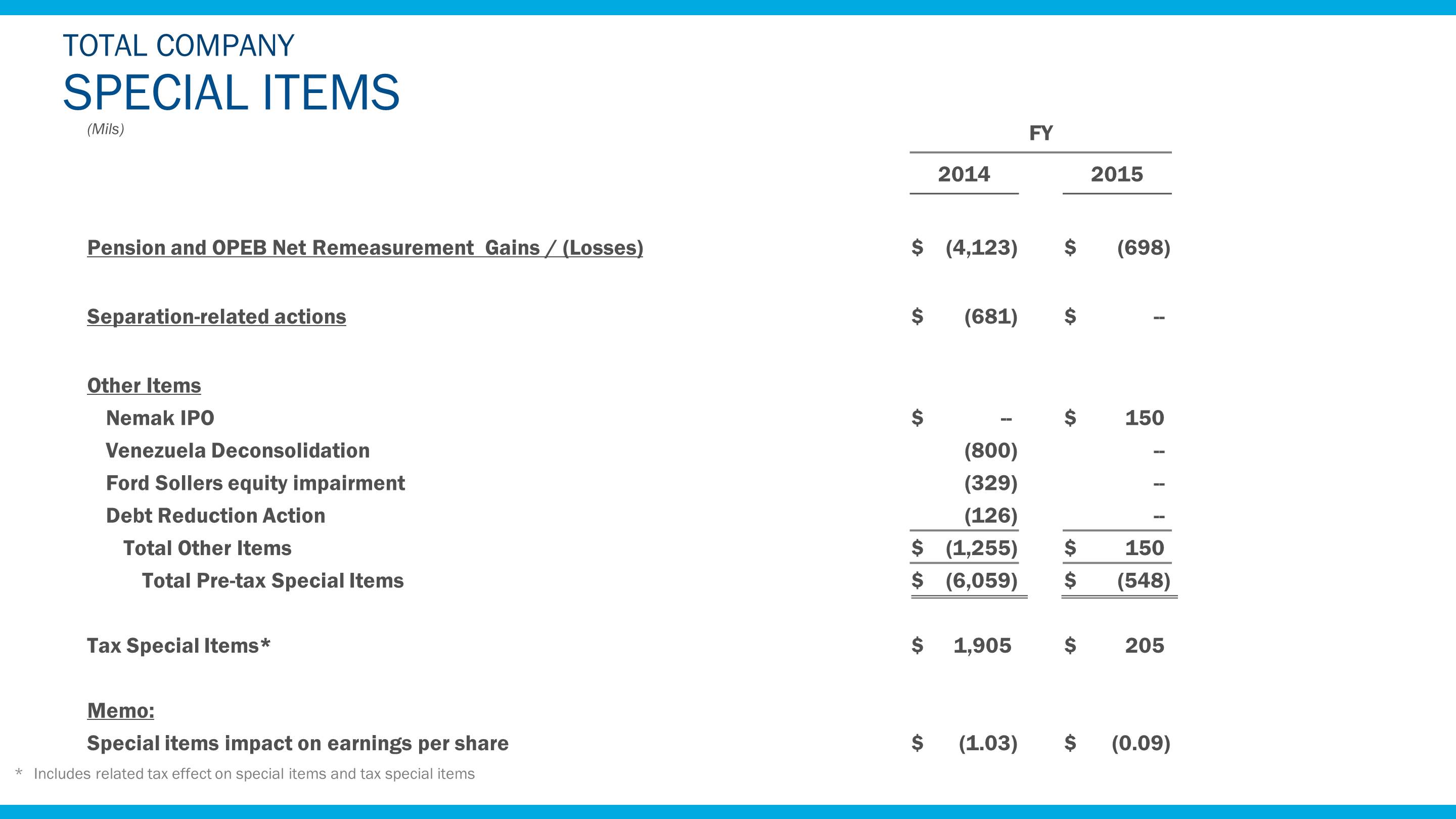

Special Items | |||

Taxes | |||

Results of Operations - 2015 | |||

Automotive Segment | |||

Financial Services Segment | |||

All Other | |||

Special Items | |||

Taxes | |||

Liquidity and Capital Resources | |||

Credit Ratings | |||

2017 Industry and GDP Planning Assumptions | |||

Production Volumes | |||

Outlook | |||

Non-GAAP Financial Measure Reconciliations | |||

2016 Supplemental Financial Information | |||

Critical Accounting Estimates | |||

Accounting Standards Issued But Not Yet Adopted | |||

Aggregate Contractual Obligations | |||

Item 7A | Quantitative and Qualitative Disclosures About Market Risk | ||

Item 8 | Financial Statements and Supplementary Data | ||

Item 9 | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | ||

i

Table of Contents

(continued)

Item 9A | Controls and Procedures | ||

Item 9B | Other Information | ||

Part III | |||

Item 10 | Directors, Executive Officers of Ford, and Corporate Governance | ||

Item 11 | Executive Compensation | ||

Item 12 | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | ||

Item 13 | Certain Relationships and Related Transactions, and Director Independence | ||

Item 14 | Principal Accounting Fees and Services | ||

Part IV | |||

Item 15 | Exhibits and Financial Statement Schedules | ||

Item 16 | Form 10-K Summary | ||

Signatures | |||

Ford Motor Company and Subsidiaries Financial Statements | |||

Report of Independent Registered Public Accounting Firm | |||

Consolidated Income Statement | |||

Consolidated Statement of Comprehensive Income | |||

Consolidated Balance Sheet | |||

Consolidated Statement of Cash Flows | |||

Consolidated Statement of Equity | |||

Notes to the Financial Statements | |||

Schedule II — Valuation and Qualifying Accounts | |||

ii

PART I.

ITEM 1. Business.

Ford Motor Company was incorporated in Delaware in 1919. We acquired the business of a Michigan company, also known as Ford Motor Company, which had been incorporated in 1903 to produce and sell automobiles designed and engineered by Henry Ford. We are a global automotive and mobility company based in Dearborn, Michigan. With about 201,000 employees and 62 plants worldwide, our core business includes designing, manufacturing, marketing, and servicing a full line of Ford cars, trucks, and SUVs, as well as Lincoln luxury vehicles. To expand our business model, we are aggressively pursuing emerging opportunities with investments in electrification, autonomy, and mobility. We provide financial services through Ford Motor Credit Company LLC (“Ford Credit”).

In addition to the information about Ford and our subsidiaries contained in this Annual Report on Form 10-K for the year ended December 31, 2016 (“2016 Form 10-K Report” or “Report”), extensive information about our Company can be found at http://corporate.ford.com, including information about our management team, our brands and products, and our corporate governance principles.

The corporate governance information on our website includes our Corporate Governance Principles, Code of Ethics for Senior Financial Personnel, Code of Ethics for the Board of Directors, Code of Corporate Conduct for all employees, and the Charters for each of the Committees of our Board of Directors. In addition, any amendments to our Code of Ethics or waivers granted to our directors and executive officers will be posted on our corporate website. All of these documents may be accessed by going to our corporate website, or may be obtained free of charge by writing to our Shareholder Relations Department, Ford Motor Company, One American Road, P.O. Box 1899, Dearborn, Michigan 48126-1899.

Our recent periodic reports filed with the Securities and Exchange Commission (“SEC”) pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, are available free of charge at http://shareholder.ford.com. This includes recent Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, and Current Reports on Form 8-K, as well as any amendments to those Reports. Recent Section 16 filings made with the SEC by the Company or any of our executive officers or directors with respect to our Common Stock also are made available free of charge through our website. We post each of these documents on our website as soon as reasonably practicable after it is electronically filed with the SEC. Our reports filed with the SEC also may be found on the SEC’s website at www.sec.gov.

The foregoing information regarding our website and its content is for convenience only and not deemed to be incorporated by reference into this Report nor filed with the SEC.

1

Item 1. Business (Continued)

OVERVIEW

Segments. We have four operating segments that represent the primary businesses reported in our consolidated financial statements: Automotive, Financial Services, Ford Smart Mobility LLC, and Central Treasury Operations.

Automotive Segment. Our Automotive segment primarily includes the sale of Ford and Lincoln brand vehicles, service parts, and accessories worldwide, together with the associated costs to develop, manufacture, distribute, and service the vehicles, parts, and accessories. The segment includes five regional business units: North America, South America, Europe, Middle East & Africa, and Asia Pacific.

Financial Services Segment. The Financial Services segment primarily includes our vehicle-related financing and leasing activities at Ford Motor Credit Company LLC (“Ford Credit”).

All Other. Ford Smart Mobility LLC and Central Treasury Operations are combined in All Other. See Note 4 of the Notes to the Financial Statements for more information regarding All Other.

AUTOMOTIVE SEGMENT

General

Our vehicle brands are Ford and Lincoln. In 2016, we sold approximately 6,651,000 vehicles at wholesale throughout the world. See “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations” (“Item 7”) for discussion of our calculation of wholesale unit volumes.

Substantially all of our vehicles, parts, and accessories are sold through distributors and dealers (collectively, “dealerships”), the substantial majority of which are independently owned. At December 31, 2016, the approximate number of dealerships worldwide distributing our vehicle brands was as follows:

Brand | Number of Dealerships at December 31, 2016 | |

Ford | 10,608 | |

Ford-Lincoln (combined) | 915 | |

Lincoln | 214 | |

Total | 11,737 | |

We do not depend on any single customer or a few customers to the extent that the loss of such customers would have a material adverse effect on our business.

In addition to the products we sell to our dealerships for retail sale, we also sell vehicles to our dealerships for sale to fleet customers, including commercial fleet customers, daily rental car companies, and governments. We also sell parts and accessories, primarily to our dealerships (which in turn sell these products to retail customers) and to authorized parts distributors (which in turn primarily sell these products to retailers). We also offer extended service contracts.

The worldwide automotive industry is affected significantly by general economic conditions over which we have little control. Vehicles are durable goods, and consumers have latitude in determining whether and when to replace an existing vehicle. The decision whether to purchase a vehicle may be affected significantly by slowing economic growth, geopolitical events, and other factors (including the cost of purchasing and operating cars and trucks and the availability and cost of financing and fuel). As we have seen in the United States and Europe, in particular, the number of cars and trucks sold may vary substantially from year to year. Further, the automotive industry is a highly competitive business that has a wide and growing variety of product offerings from a growing number of manufacturers.

Our wholesale unit volumes vary with the level of total industry demand and our share of that industry demand. Our wholesale unit volumes also are influenced by the level of dealer inventory. Our share is influenced by how our products are perceived in comparison to those offered by other manufacturers based on many factors, including price, quality, styling, reliability, safety, fuel efficiency, functionality, and reputation. Our share also is affected by the timing and frequency of new model introductions. Our ability to satisfy changing consumer preferences with respect to type or size of vehicle, as well as design and performance characteristics, affects our sales and earnings significantly.

2

Item 1. Business (Continued)

As with other manufacturers, the profitability of our business is affected by many factors, including:

• | Wholesale unit volumes |

• | Margin of profit on each vehicle sold - which in turn is affected by many factors, such as: |

◦ | Market factors - volume and mix of vehicles and options sold, and net pricing (reflecting, among other factors, incentive programs) |

◦ | Costs of components and raw materials necessary for production of vehicles |

◦ | Costs for customer warranty claims and additional service actions |

◦ | Costs for safety, emissions, and fuel economy technology and equipment |

• | A high proportion of relatively fixed structural costs, so that small changes in wholesale unit volumes can significantly affect overall profitability |

Our industry has a very competitive pricing environment, driven in part by industry excess capacity, which is concentrated in Europe and Asia but affects other markets because much of this capacity can be redirected to other markets. The decline in the value of the yen during the past four years also has contributed significantly to competitive pressures in many of our markets. For the past several decades, manufacturers typically have given price discounts and other marketing incentives to maintain market share and production levels. A discussion of our strategies to compete in this pricing environment is set forth in the “Overview” section in Item 7.

Competitive Position. The worldwide automotive industry consists of many producers, with no single dominant producer. Certain manufacturers, however, account for the major percentage of total sales within particular countries, especially their countries of origin. Key competitors with global presence include Fiat Chrysler Automobiles, General Motors Company, Honda Motor Company, Hyundai-Kia Automotive Group, PSA Peugeot Citroen, Renault-Nissan B.V., Suzuki Motor Corporation, Toyota Motor Corporation, and Volkswagen AG Group.

Seasonality. We generally record the sale of a vehicle (and recognize revenue) when it is produced and shipped or delivered to our customer (i.e., the dealership). See the “Overview” section in Item 7 for additional discussion of revenue recognition practices.

We manage our vehicle production schedule based on a number of factors, including retail sales (i.e., units sold by our dealerships to their customers at retail) and dealer stock levels (i.e., the number of units held in inventory by our dealerships for sale to their customers). Historically, we have experienced some seasonal fluctuation in the business, with production in many markets tending to be higher in the first half of the year to meet demand in the spring and summer (typically the strongest sales months of the year).

Backlog Orders. We generally produce and ship our products on average within approximately 20 days after an order is deemed to become firm. Therefore, no significant amount of backlog orders accumulates during any period.

Raw Materials. We purchase a wide variety of raw materials from numerous suppliers around the world for use in production of our vehicles. These materials include base metals (e.g., steel, iron castings, and aluminum), precious metals (e.g., palladium), energy (e.g., natural gas), and plastics/resins (e.g., polypropylene). We believe we have adequate supplies or sources of availability of raw materials necessary to meet our needs. There always are risks and uncertainties with respect to the supply of raw materials, however, which could impact availability in sufficient quantities to meet our needs. See the “Overview” section of Item 7 for a discussion of commodity and energy price trends, and “Item 7A. Quantitative and Qualitative Disclosures about Market Risk” (“Item 7A”) for a discussion of commodity price risks.

Intellectual Property. We own or hold licenses to use numerous patents, copyrights, and trademarks on a global basis. Our policy is to protect our competitive position by, among other methods, filing U.S. and international patent applications to protect technology and improvements that we consider important to the development of our business. We have generated a large number of patents, and expect this portfolio to continue to grow as we actively pursue additional technological innovation. We have approximately 48,000 active patents and pending patent applications globally, with an average age for patents in our active patent portfolio of just over five years. In addition to this intellectual property, we also rely on our proprietary knowledge and ongoing technological innovation to develop and maintain our competitive position. Although we believe these patents, patent applications, and know-how, in the aggregate, are important to the conduct of our business, and we obtain licenses to use certain intellectual property owned by others, none is individually considered material to our business. We also own numerous trademarks and service marks that contribute to the identity and recognition of our Company and its products and services globally. Certain of these marks are integral to the conduct of our business, a loss of any of which could have a material adverse effect on our business.

3

Item 1. Business (Continued)

Warranty Coverage, Field Service Actions, and Customer Satisfaction Actions. We provide warranties on vehicles we sell. Warranties are offered for specific periods of time and/or mileage, and vary depending upon the type of product and the geographic location of its sale. Pursuant to these warranties, we will repair, replace, or adjust all parts on a vehicle that are defective in factory-supplied materials or workmanship during the specified warranty period. In addition to the costs associated with this warranty coverage provided on our vehicles, we also incur costs as a result of field service actions (i.e., safety recalls, emission recalls, and other product campaigns), and for customer satisfaction actions.

For additional information regarding warranty and related costs, see “Critical Accounting Estimates” in Item 7 and Note 24 of the Notes to the Financial Statements.

Industry Volume, Market Share, and Wholesales

Our industry volume, market share, and wholesale unit volume in each region and in certain key markets within each region during the past three years were as follows:

Industry Volume (a) | Market Share (b) | Wholesales (c) | ||||||||||||||||||||||||

(in millions of units) | (as a percentage) | (in thousands of units) | ||||||||||||||||||||||||

2014 | 2015 | 2016 | 2014 | 2015 | 2016 | 2014 | 2015 | 2016 | ||||||||||||||||||

United States | 16.8 | 17.8 | 17.9 | 14.7 | % | 14.7 | % | 14.6 | % | 2,457 | 2,677 | 2,588 | ||||||||||||||

Canada | 1.9 | 1.9 | 2.0 | 15.5 | 14.4 | 15.4 | 288 | 285 | 313 | |||||||||||||||||

Mexico | 1.2 | 1.4 | 1.6 | 6.9 | 6.4 | 6.2 | 77 | 93 | 103 | |||||||||||||||||

North America | 20.2 | 21.5 | 21.8 | 14.2 | 14.0 | 13.9 | 2,842 | 3,073 | 3,019 | |||||||||||||||||

Brazil | 3.5 | 2.6 | 2.1 | 9.4 | % | 10.4 | % | 9.2 | % | 320 | 250 | 182 | ||||||||||||||

Argentina | 0.7 | 0.6 | 0.7 | 14.1 | 14.9 | 13.6 | 94 | 94 | 101 | |||||||||||||||||

South America | 5.3 | 4.2 | 3.7 | 8.9 | 9.6 | 8.8 | 463 | 381 | 325 | |||||||||||||||||

United Kingdom | 2.8 | 3.1 | 3.1 | 14.4 | % | 14.3 | % | 14.0 | % | 425 | 447 | 428 | ||||||||||||||

Germany | 3.4 | 3.5 | 3.7 | 7.1 | 7.3 | 7.6 | 237 | 261 | 283 | |||||||||||||||||

Russia | 2.5 | 1.6 | 1.5 | 2.6 | 2.4 | 2.9 | 57 | 38 | 45 | |||||||||||||||||

Turkey | 0.8 | 1.0 | 1.0 | 11.7 | 12.6 | 11.4 | 91 | 128 | 116 | |||||||||||||||||

Europe | 18.6 | 19.2 | 20.1 | 7.2 | 7.7 | 7.7 | 1,387 | 1,530 | 1,539 | |||||||||||||||||

Middle East & Africa | 4.3 | 4.3 | 3.6 | 4.6 | % | 4.4 | % | 4.5 | % | 192 | 187 | 161 | ||||||||||||||

China | 24.0 | 23.5 | 26.4 | 4.5 | % | 4.8 | % | 4.8 | % | 1,116 | 1,160 | 1,267 | ||||||||||||||

Australia | 1.1 | 1.2 | 1.2 | 7.2 | 6.1 | 6.9 | 80 | 71 | 82 | |||||||||||||||||

India | 3.2 | 3.5 | 3.7 | 2.4 | 2.1 | 2.4 | 77 | 78 | 86 | |||||||||||||||||

ASEAN (d) | 3.2 | 3.1 | 3.1 | 3.1 | 3.3 | 3.7 | 94 | 94 | 115 | |||||||||||||||||

Asia Pacific (e) | 39.7 | 39.1 | 42.1 | 3.5 | 3.6 | 3.8 | 1,439 | 1,464 | 1,607 | |||||||||||||||||

Global | 88.1 | 88.2 | 91.4 | 7.1 | % | 7.4 | % | 7.3 | % | N/A | N/A | N/A | ||||||||||||||

Total Company | N/A | N/A | N/A | N/A | N/A | N/A | 6,323 | 6,635 | 6,651 | |||||||||||||||||

______________

(a) | Industry volume is an internal estimate based on publicly-available data collected from various government, private, and public sources around the globe and is based, in part, on estimated vehicle registrations; includes medium and heavy trucks. |

(b) | Market share represents reported retail sales of our brands as a percent of total industry volume in the relevant market or region. Market share is based, in part, on estimated vehicle registrations; includes medium and heavy trucks. |

(c) | Wholesale unit volume includes sales of medium and heavy trucks. Wholesale unit volume includes all Ford and Lincoln badged units (whether produced by Ford or by an unconsolidated affiliate) that are sold to dealerships, units manufactured by Ford that are sold to other manufacturers, units distributed for other manufacturers, and local brand units produced by our unconsolidated Chinese joint venture Jiangling Motors Corporation, Ltd. (“JMC”) that are sold to dealerships. Vehicles sold to daily rental car companies that are subject to a guaranteed repurchase option (i.e., rental repurchase), as well as other sales of finished vehicles for which the recognition of revenue is deferred (e.g., consignments), also are included in wholesale unit volume. Revenue from certain vehicles in wholesale unit volume (specifically, Ford badged vehicles produced and distributed by our unconsolidated affiliates, as well as JMC brand vehicles) are not included in our revenue. |

(d) | ASEAN includes Indonesia, Philippines, Thailand, Vietnam, and Malaysia. |

(e) | Asia Pacific market share includes Ford brand and JMC brand vehicles produced and sold by our unconsolidated affiliates. |

4

Item 1. Business (Continued)

FINANCIAL SERVICES SEGMENT

Ford Motor Credit Company LLC

Our wholly-owned subsidiary Ford Credit offers a wide variety of automotive financing products to and through automotive dealers throughout the world. The predominant share of Ford Credit’s business consists of financing our vehicles and supporting our dealers. Ford Credit earns its revenue primarily from payments made under retail installment sale and lease contracts that it originates and purchases; interest rate supplements and other support payments from us and our subsidiaries; and payments made under dealer financing programs.

As a result of these financing activities, Ford Credit has a large portfolio of finance receivables and operating leases which it classifies into two portfolios— “consumer” and “non-consumer.” Finance receivables and operating leases in the consumer portfolio include products offered to individuals and businesses that finance the acquisition of our vehicles from dealers for personal and commercial use. Retail financing includes retail installment sale contracts for new and used vehicles and direct financing leases for new vehicles to retail and commercial customers including leasing companies, government entities, daily rental companies, and fleet customers. Finance receivables in the non-consumer portfolio include products offered to automotive dealers. Ford Credit makes wholesale loans to dealers to finance the purchase of vehicle inventory (i.e., floorplan financing), as well as loans to dealers to finance working capital and improvements to dealership facilities, finance the purchase of dealership real estate, and finance other dealer vehicle programs. Ford Credit also purchases receivables generated by us and our subsidiaries, primarily related to the sale of parts and accessories to dealers, Ford-related loans, and certain used vehicles from daily rental fleet companies.

Ford Credit does business in the United States and Canada through business centers. Outside of the United States, Europe is Ford Credit’s largest operation. Ford Credit’s European operations are managed through its United Kingdom-based subsidiary, FCE Bank plc (“FCE”). Within Europe, FCE’s largest markets are the United Kingdom and Germany, representing 65% of FCE’s finance receivables and operating leases at year-end 2016.

The following table shows Ford Credit’s financing shares of new Ford and Lincoln vehicle retail sales in the United States and new Ford vehicles sold in Europe, as well as its wholesale financing shares of new Ford and Lincoln vehicles acquired by dealers in the United States (excluding fleet) and new Ford vehicles acquired by dealers in Europe:

Years Ended December 31, | ||||||||

2014 | 2015 | 2016 | ||||||

United States - Financing Share | ||||||||

Retail installment and lease share of Ford retail sales | 63 | % | 65 | % | 56 | % | ||

Wholesale | 77 | 76 | 76 | |||||

Europe - Financing Share | ||||||||

Retail installment and lease share of total Ford sales | 36 | % | 37 | % | 37 | % | ||

Wholesale | 98 | 98 | 98 | |||||

See Item 7 and Notes 6, 7, and 8 of the Notes to the Financial Statements for a detailed discussion of Ford Credit’s receivables, credit losses, allowance for credit losses, loss-to-receivables ratios, funding sources, and funding strategies. See Item 7A for discussion of how Ford Credit manages its financial market risks.

We routinely sponsor special retail and lease incentives to dealers’ customers who choose to finance or lease our vehicles from Ford Credit. In order to compensate Ford Credit for the lower interest or lease payments offered to the retail customer, we pay the value of the incentive directly to Ford Credit when it originates the retail finance or lease contract. These programs increase Ford Credit’s financing volume and share. See Note 2 of the Notes to the Financial Statements for information about our accounting for these programs.

We have an Amended and Restated Relationship Agreement with Ford Credit, pursuant to which, if Ford Credit’s managed leverage for a calendar quarter were to be higher than 11.5:1 (as reported in its most recent periodic report), Ford Credit could require us to make or cause to be made a capital contribution to it in an amount sufficient to have caused such managed leverage to have been 11.5:1. No capital contributions have been made pursuant to this agreement. The agreement also allocates to Ford Credit $3 billion of commitments under our corporate credit facility. In a separate agreement with FCE, Ford Credit also has agreed to maintain FCE’s net worth in excess of $500 million; no payments have been made pursuant to that agreement.

5

Item 1. Business (Continued)

GOVERNMENTAL STANDARDS

Many governmental standards and regulations relating to safety, fuel economy, emissions control, noise control, vehicle recycling, substances of concern, vehicle damage, and theft prevention are applicable to new motor vehicles, engines, and equipment manufactured for sale in the United States, Europe, and elsewhere. In addition, manufacturing and other automotive assembly facilities in the United States, Europe, and elsewhere are subject to stringent standards regulating air emissions, water discharges, and the handling and disposal of hazardous substances. The most significant of the standards and regulations affecting us are discussed below:

Vehicle Emissions Control

U.S. Requirements – Federal and California Emission Standards. The federal Clean Air Act imposes stringent limits on the amount of regulated pollutants that lawfully may be emitted by new vehicles and engines produced for sale in the United States. In 2014, the U.S. Environmental Protection Agency (“EPA”) finalized new “Tier 3” regulations that phase in increasingly stringent motor vehicle emission standards beginning with the 2017 model year. Pursuant to the Clean Air Act, California may establish its own vehicle emission standards, which can then be adopted by other states. The California Air Resources Board (“CARB”) has adopted “LEV III” standards, which took effect with the 2015 model year and impose increasingly stringent tailpipe and evaporative emissions requirements for light and medium duty vehicles. Thirteen states, primarily located in the Northeast and Northwest, have adopted the LEV III standards. Compliance with both the Tier 3 and LEV III standards could be challenging.

Both federal and California regulations require motor vehicles to be equipped with on-board diagnostic (“OBD”) systems that monitor emission-related systems and components. As OBD requirements become more complex and challenging over time, they could lead to increased vehicle recalls and warranty costs. Compliance with automobile emission standards depends in part on the widespread availability of high-quality and consistent automotive fuels that the vehicles were designed to use. Fuel variables that can affect vehicle emissions include ethanol content, octane ratings, and the use of metallic-based fuel additives, among other things. There are various ongoing regulatory and judicial proceedings related to fuel quality at the national and state level, and the outcome of these proceedings could affect vehicle manufacturers’ warranty costs as well as their ability to comply with vehicle emission standards.

The California vehicle emissions program also includes requirements for manufacturers to produce and deliver for sale zero-emission vehicles (“ZEVs”). The current ZEV regulations mandate substantial annual increases in the production and sale of battery-electric, fuel cell, and plug-in hybrid vehicles, particularly for the 2018–2025 model years. By the 2025 model year, approximately 15% of a manufacturer’s total California sales volume will need to be made up of such vehicles. Compliance with ZEV rules could have a substantial adverse effect on our sales volumes and profits. We are concerned that the market and infrastructure in California may not support the large volume of advanced-technology vehicles that manufacturers will be required to produce, especially if gasoline prices remain relatively low. We also are concerned about enforcement of the ZEV mandate in other states that have adopted California’s ZEV program, where the existence of a market for such vehicles is even less certain. CARB conducts periodic reviews of its upcoming ZEV requirements, taking into account factors such as technology developments and market acceptance. Ford and the industry will be active participants in such reviews, with the goal of ensuring that ZEV requirements are feasible and not excessively burdensome.

European Requirements. European Union (“EU”) directives and related legislation limit the amount of regulated pollutants that may be emitted by new motor vehicles and engines sold in the EU. Stringent new Stage 6 emission standards took effect for vehicle registrations starting in September 2014, with a second phase beginning in September 2017. These standards will drive the need for additional diesel exhaust after-treatment, which will add cost and potentially impact the diesel CO2 advantage. The European Commission has also proposed new Real Driving Emission (“RDE”) rules, which will require manufacturers to conduct on-road emission tests using portable emission analyzers. These on-road emission tests will complement the laboratory-based tests. During the initial phase, which started in January 2016, the RDE tests are used for monitoring purposes. Beginning in September 2017, manufacturers will have to reduce the divergence between the regulatory limit that is tested in laboratory conditions and the values of RDE tests (“conformity factors”). The additional costs associated with conducting the RDE tests and complying with the conformity factors are expected to be significant. Europe is in process of drafting the RDE in-use surveillance rules with proposals to allow third parties to conduct testing and to define a process to challenge the product compliance with Authorities. On a longer term approach, the WVTA (Whole Vehicle Type Approval) Regulations are being adapted to cover market surveillance, which is further expected to increase testing by Authorities across Europe from 2020+.

6

Item 1. Business (Continued)

Other National Requirements. Many countries, in an effort to address air quality concerns, are adopting previous versions of European or United Nations Economic Commission for Europe (“UN-ECE”) mobile source emission regulations. Some countries have adopted more advanced regulations based on the most recent version of European or U.S. regulations; for example, China adopted emission regulations based on European Stage VI emission standards and U.S. evaporative emissions and on-board diagnostic requirements. Korea and Taiwan have adopted very stringent U.S.-based standards for gasoline vehicles and European-based standards for diesel vehicles. Although these countries have adopted regulations based on UN-ECE or U.S. standards, there may be some unique testing provisions that require emission-control systems to be redesigned for these markets. Canadian criteria emissions regulations are aligned with U.S. Tier 2 requirements. In July 2015, the Canadian federal government amended the On-Road Vehicle and Engine Emission Regulations and the Sulphur in Gasoline Regulations to align Canadian emission standards with the U.S. Tier 3 regulations discussed above.

In October 2016, the Canadian Province of Quebec passed legislation enabling regulation of a ZEV mandate. Regulations are still under development but Quebec has signaled that they plan to follow California and Northeast States’ regulations.

Not all countries have adopted appropriate fuel quality standards to accompany the stringent emission standards adopted. This could lead to compliance problems, particularly if on-board diagnostic or in-use surveillance requirements are implemented.

Brazil and Chile have introduced stringent emission and on-board diagnostic standards based on the European Stage 5 standards for light duty vehicles and Stage V standards for heavy duty vehicles. In Brazil, all light duty vehicles are required to meet U.S.-based Proconve L6 standards and more stringent on-board diagnostic standards for diesel light duty vehicles were introduced in 2017. Argentina is phasing in European Stage 5 standards for all new light duty vehicle registrations by 2017 and European Stage V standards for heavy duty vehicles by 2018.

Global Developments. Since September 2015, the EPA and CARB have pursued enforcement actions against a major competitor in connection with its use of “defeat devices” in hundreds of thousands of light-duty diesel vehicles. These actions have resulted in settlements involving billions of dollars for environmental remediation and civil penalties, as well as indictments of several employees on charges of committing federal crimes. The competitor continues to face various class action suits, as well as numerous claims and investigations by various U.S. states and other nations. Defeat devices are elements of design (typically embedded in software) that improperly cause the emission control system to function less effectively during normal on-road driving than during an official laboratory emissions test, without justification. They are prohibited by law in many jurisdictions, including the United States and Europe. We do not use defeat devices in our vehicles.

The investigations by EPA and CARB of our competitor have led to increased scrutiny of automakers’ emission testing by regulators around the world. EPA began carrying out additional non-standard tests as part of its vehicle certification program, following an announcement in September 2015. The EU accelerated efforts to finalize its RDE testing program as described above. In 2016, several European countries, including France and Germany, conducted non-standard emission tests and published the results. In some cases, this supplemental testing has triggered investigations of other manufacturers for possible defeat devices. Testing is expected to continue on an ongoing basis.

Vehicle Fuel Economy and Greenhouse Gas Standards

U.S. Requirements – Light Duty Vehicles. Federal law requires that light duty vehicles meet minimum corporate average fuel economy (“CAFE”) standards set by the National Highway Traffic Safety Administration (“NHTSA”). Manufacturers are subject to substantial civil penalties if they fail to meet the CAFE standard in any model year, after taking into account all available credits for the preceding three model years and expected credits for the five succeeding model years. The law requires NHTSA to promulgate and enforce separate CAFE standards applicable to each manufacturer’s fleet of domestic passenger cars, imported passenger cars, and light duty trucks.

EPA also regulates vehicle greenhouse gas (“GHG”) emissions under the Clean Air Act. Because the vast majority of GHGs emitted by a vehicle are the result of fuel combustion, GHG emission standards effectively are fuel economy standards. Thus, it is necessary for NHTSA and EPA to coordinate with each other on their fuel economy and GHG standards, respectively, to avoid potential inconsistencies.

In 2010, EPA and NHTSA jointly promulgated regulations establishing the “One National Program” of CAFE and GHG regulations for light duty vehicles for the 2012-2016 model years. In 2012, EPA and NHTSA jointly promulgated regulations extending the One National Program framework through the 2025 model year. These rules require

7

Item 1. Business (Continued)

manufacturers to achieve, across the industry, a light duty fleet average fuel economy of approximately 35.5 mpg by the 2016 model year, 45 mpg by the 2021 model year, and 51.4 mpg by the 2025 model year. Each manufacturer’s specific task depends on the mix of vehicles it sells. The rules include the opportunity for manufacturers to earn credits for technologies that achieve real-world CO2 reductions, and fuel economy improvements that are not captured by the EPA fuel economy test procedures. Manufacturers also can earn credits for GHG reductions not specifically tied to fuel economy, such as improvements in air conditioning systems.

The One National Program standards become increasingly stringent over time, and they will be difficult to meet if fuel prices remain relatively low and market conditions do not drive consumers to purchase electric vehicles and other highly fuel-efficient vehicles in large numbers. We are concerned about the commercial feasibility of meeting future model year GHG and CAFE standards, particularly the 2022-2025 standards, because of the many unknowns regarding technology development, market conditions, and other factors so far into the future.

The One National Program rules provided for a midterm evaluation process under which, by April 2018, EPA and NHTSA would re-evaluate their standards for model years 2022-2025 in order to ensure that those standards are feasible and optimal in light of intervening events. Shortly before President Obama left office in January 2017, EPA announced an accelerated decision to maintain the GHG standards originally set for those model years. NHTSA is continuing to conduct its evaluation with respect to the model year 2022-2025 standards. It remains to be seen whether the EPA determination will be reconsidered under President Trump’s administration, and whether the EPA and NHTSA determinations will ultimately be harmonized with each other.

If the agencies seek to impose and enforce fuel economy and GHG standards that are misaligned with market conditions, we likely would be forced to take various actions that could have substantial adverse effects on our sales volume and profits. Such actions likely would include restricting offerings of selected engines and popular options; increasing market support programs for our most fuel-efficient cars and light trucks; and ultimately curtailing the production and sale of certain vehicles such as high-performance cars, utilities, and/or full-size light trucks, in order to maintain compliance.

California has asserted the right to regulate motor vehicle GHG emissions, and other states have asserted the right to adopt the California standards. With the adoption of the federal One National Program standards discussed above, California and the other states have agreed that compliance with the federal program would satisfy compliance with any purported state GHG requirements for the 2012–2025 model years. This avoids a patchwork of potentially conflicting federal and state GHG standards. Should California and other states ever renew their efforts to enforce state-specific motor vehicle GHG rules, this would impose significant costs on automotive manufacturers.

U.S. Requirements – Heavy Duty Vehicles. EPA and NHTSA have jointly promulgated GHG and fuel economy standards on heavy duty vehicles (generally, vehicles over 8,500 pounds gross vehicle weight rating). In our case, the standards primarily affect our heavy duty pickup trucks and vans, plus vocational vehicles such as shuttle buses and delivery trucks. In 2016, EPA and NHTSA finalized GHG and fuel economy standards for these vehicles, covering model years 2019–2027. As the heavy-duty standards increase in stringency, it may become more difficult to comply while continuing to offer a full lineup of heavy duty trucks.

European Requirements. In December 2008, the EU approved regulation of passenger car CO2 emissions beginning in 2012 that limits the industry fleet average to a maximum of 130 grams per kilometer (“g/km”), using a sliding scale based on vehicle weight. This regulation provides different targets for each manufacturer based on the respective average vehicle weight for its fleet of vehicles. Limited credits are available for CO2 off-cycle actions (“eco-innovations”), certain alternative fuels, and vehicles with CO2 emissions below 50 g/km. A penalty system will apply for manufacturers failing to meet targets. Pooling agreements between different manufacturers are possible, although it is not clear that these will be of much practical benefit under the regulations. Starting in 2020, an industry target of 95 g/km has been set, for which 95% of a manufacturer’s fleet has to comply; by 2021, 100% of a manufacturer’s fleet has to comply. Other non-EU European countries are likely to follow with similar regulations. For example, Switzerland has introduced similar rules, which began phasing-in starting in July 2012 with the same targets (which include a 2020 target of 95 g/km, with conditions still to be defined), although the industry average emission target is significantly higher. We face the risk of advance premium payment requirements if, for example, unexpected market fluctuation within a quarter negatively impact our average fleet performance.

In separate legislation, “complementary measures” have been mandated, including requirements related to fuel economy indicators, and more-efficient low-CO2 mobile air conditioning systems. The EU Commission, Council and Parliament have approved a target for commercial light duty vehicles to be at an industry average of 175 g/km (with phase-in from 2014–2017), and 147 g/km in 2020. It is likely that other European countries, will implement similar rules

8

Item 1. Business (Continued)

but under even more difficult conditions. For instance, Switzerland will implement the same 147 g/km target in 2020 but under more difficult conditions. This regulation also provides different targets for each manufacturer based on its respective average vehicle weight in its fleet of vehicles. The final mass and CO2 requirements for “multi-stage vehicles” (e.g., our Transit chassis cabs) are fully allocated to the base manufacturer (e.g., Ford) so that the base manufacturer is fully responsible for the CO2 performance of the final up-fitted vehicles. The EU proposal also includes a penalty system, “super-credits” for vehicles below 50 g/km, and limited credits for CO2 off-cycle eco-innovations, pooling, etc., similar to the passenger car CO2 regulation.

The United Nations developed a new technical regulation for passenger car emissions and CO2. This new world light duty test procedure (“WLTP”) is focused primarily on better aligning laboratory CO2 and fuel consumption figures with customer-reported figures. The introduction of WLTP in Europe is likely to require updates to CO2 labeling as early as 2018 and will increase certain consumer label values, thereby impacting taxes in countries with a CO2 tax scheme. Costs associated with new or incremental testing for WLTP could be significant. The European Commission requires mandatory WLTP testing for regulated emissions and CO2 starting in September 2017. The European Commission has assured comparable stringency to the existing fleet average rules for each automobile manufacturer if the 2021 fleet average targets are required to be measured on WLTP instead of under the current European New European Driving Cycle (“NEDC”) requirements. The legislative framework and process for the target translation is currently under development. The European Commission confirmed in October 2016 that there would be a delay in the introduction of a timetable for a post-2020 CO2 proposal. The proposal is now expected to be released during the second half of 2017.

Some European countries have implemented or are considering other initiatives for reducing CO2 vehicle emissions, including fiscal measures and CO2 labeling. For example, the United Kingdom, France, Germany, Spain, Portugal, and the Netherlands, among others, have introduced taxation based on CO2 emissions. The EU CO2 requirements are likely to trigger further measures. To limit GHG emissions, the EU directive on mobile air conditioning currently requires the replacement of the current refrigerant with a lower “global warming potential” refrigerant for new vehicle types, and for all newly registered vehicles starting in January 2017. A refrigerant change adds considerable costs along the whole manufacturing chain.

Other National Requirements. The Canadian federal government has regulated vehicle GHG emissions under the Canadian Environmental Protection Act, beginning with the 2011 model year. In October 2014, the Canadian federal government published the final changes to the regulation for light duty vehicles, which maintain alignment with U.S. EPA vehicle GHG standards for the 2017–2025 model years. The final regulation for 2014–2018 heavy duty vehicles was published in February 2013. In October 2014, the Canadian federal government published the Notice of Intent to regulate heavy duty vehicles and engines for model year 2019 and beyond, which tracks U.S. EPA standards.

Mexico adopted fuel economy/CO2 standards, based on the U.S. One National Program framework, that took effect in 2014.

Many Asia Pacific countries (such as Australia, China, India, South Korea, Taiwan, and Vietnam) are developing or enforcing fuel efficiency or labeling targets. For example, South Korea has set fuel efficiency targets for 2020, with incentives for early adoption. China published standards for Stage IV fuel efficiency targets for 2016–2020. The fuel efficiency targets will impact the cost of vehicle technology in the future.

In South America, Brazil introduced a voluntary vehicle energy-efficiency labeling program, indicating fuel consumption rates for all light-duty vehicles. Brazil has required inclusion of emission classification on fuel economy labels since January 2016. Brazil also published a new automotive regime establishing a minimum absolute CAFE value as a function of Fleet Corporate Average Mass for 2017 light duty vehicles with a spark ignition engine in order to qualify for industrialized products tax reduction. Additional tax reductions are available if further fuel efficiency improvements are achieved. A severe penalty system will apply to qualified manufacturers failing to meet fuel efficiency requirements for the 2013–2017 sales period. Brazil reduced import tax on electric and hybrid cars. The tax rate, which was 35%, will vary from zero to 7%, depending on a vehicle’s energy efficiency. Discussion on new fuel efficiency requirements has started. Chile introduced a tax based on urban fuel consumption and NOx emission for light and medium vehicles beginning in late 2014. In general, fuel efficiency targets may impact the cost of technology of our models in the future.

In the Middle East, the Kingdom of Saudi Arabia introduced new light duty vehicle fuel economy standards, which are patterned after the U.S. CAFE standard structure, with fuel economy targets following the design of the U.S. 2012–2016 fuel economy standards. The standards became effective on January 1, 2016 and will be fully phased in by the end of 2017.

9

Item 1. Business (Continued)

Vehicle Safety

U.S. Requirements. The National Traffic and Motor Vehicle Safety Act of 1966 (the “Safety Act”) regulates vehicles and vehicle equipment in two primary ways. First, the Safety Act prohibits the sale in the United States of any new vehicle or equipment that does not conform to applicable vehicle safety standards established by NHTSA. Meeting or exceeding many safety standards is costly, in part because the standards tend to conflict with the need to reduce vehicle weight in order to meet emission and fuel economy standards. Second, the Safety Act requires that defects related to motor vehicle safety be remedied through safety recall campaigns. A manufacturer is obligated to recall vehicles if it determines the vehicles do not comply with a safety standard. Should we or NHTSA determine that either a safety defect or noncompliance issue exists with respect to any of our vehicles, the cost of such recall campaigns could be substantial.

Other National Requirements. The EU and many countries have established vehicle safety standards and regulations, and are likely to adopt additional or more stringent requirements in the future. The European General Safety Regulation introduced United Nations Economic Commission for Europe (“UN-ECE”) regulations, which will be required for the European Type Approval process. EU regulators also are focusing on active safety features such as lane departure warning systems, electronic stability control, and automatic brake assist. Globally, governments generally have been adopting UN-ECE based regulations with minor variations to address local concerns. Any difference between North American and UN-ECE based regulations can add complexity and costs to the development of global platform vehicles, and we continue to support efforts to harmonize regulations to reduce vehicle design complexity while providing a common level of safety performance; several recently launched bilateral negotiations on free trade can potentially contribute to this goal. New safety and recall requirements in China, India, and Gulf Cooperation Council countries also may add substantial costs and complexity to our global recall practice. In South America, additional safety requirements are being introduced or proposed in Argentina, Brazil, Chile, Colombia, Ecuador, and Uruguay, influenced by The New Car Assessment Program for Latin America and the Caribbean (“Latin NCAP”), which may be a driver for similar actions in other countries. In Canada, regulatory requirements are currently aligned with U.S. regulations. However, recent amendments to the Canadian Motor Vehicle Safety Act have introduced broad powers to the Minister of Transport to order manufacturers to submit a notice of defect or non-compliance when the Minister considers it would be in the interest of safety.

New Car Assessment Programs. Organizations around the globe rate and compare motor vehicles in New Car Assessment Programs (“NCAPs”) to provide consumers with additional information about the safety of new vehicles. NCAPs use crash tests and other evaluations that are different than what is required by applicable regulations, and use stars to rate vehicle safety, with five stars awarded for the highest rating and one for the lowest. Achieving high NCAP ratings can add complexity and cost to vehicles.

EMPLOYMENT DATA

The approximate number of individuals employed by us and entities that we consolidated as of December 31, 2015 and 2016 was as follows (in thousands):

2015 | 2016 | ||||

Automotive | |||||

North America | 96 | 101 | |||

South America | 15 | 15 | |||

Europe | 53 | 52 | |||

Middle East & Africa | 3 | 3 | |||

Asia Pacific | 25 | 23 | |||

Financial Services | |||||

Ford Credit | 7 | 7 | |||

Total | 199 | 201 | |||

Substantially all of the hourly employees in our Automotive operations are represented by unions and covered by collective bargaining agreements. In the United States, approximately 99% of these unionized hourly employees in our Automotive segment are represented by the International Union, United Automobile, Aerospace and Agricultural Implement Workers of America (“UAW” or “United Auto Workers”). At December 31, 2016, approximately 57,000 hourly employees in the United States were represented by the UAW, an increase of about 3,000 employees since December 31, 2015. Approximately 1.5% of our U.S. salaried employees are represented by unions. Many non-management salaried employees at our operations outside of the United States also are represented by unions.

10

Item 1. Business (Continued)

In 2016, we entered into collective bargaining agreements (covering wages, benefits and/or other employment provisions) with unions in Argentina, Brazil, Canada, France, Germany, Italy, Mexico, Romania, Russia, South Africa, Taiwan and Thailand.

In 2017, we will negotiate collective bargaining agreements (covering wages, benefits and/or other employment provisions) with unions in Argentina, Australia, Brazil, Britain, France, India, Mexico, Romania, Russia, and Thailand.

ENGINEERING, RESEARCH, AND DEVELOPMENT

We engage in engineering, research, and development primarily to improve the performance (including fuel efficiency), safety, and customer satisfaction of our products, and to develop new products and services (including for emerging opportunities). Engineering, research, and development expenses for 2014, 2015, and 2016 were $6.7 billion, $6.7 billion, and $7.3 billion, respectively.

ITEM 1A. Risk Factors.

We have listed below (not necessarily in order of importance or probability of occurrence) the most significant risk factors applicable to us:

Decline in industry sales volume, particularly in the United States, Europe, or China, due to financial crisis, recession, geopolitical events, or other factors. Because we, like other manufacturers, have a high proportion of relatively fixed structural costs, relatively small changes in industry sales volume can have a substantial effect on our cash flow and profitability. If industry vehicle sales were to decline to levels significantly below our planning assumption, particularly in the United States, Europe, or China, due to financial crisis, recession, geopolitical events, or other factors, the decline could have a substantial adverse effect on our financial condition, results of operations, and cash flow. For discussion of economic trends, see the “Overview” section of Item 7.

Lower-than-anticipated market acceptance of Ford’s new or existing products or services, or failure to achieve expected growth. Although we conduct extensive market research before launching new or refreshed vehicles and introducing new services, many factors both within and outside our control affect the success of new or existing products and services in the marketplace. Offering vehicles and services that customers want and value can mitigate the risks of increasing price competition and declining demand, but products and services that are perceived to be less desirable (whether in terms of price, quality, styling, safety, overall value, fuel efficiency, or other attributes) can exacerbate these risks. With increased consumer interconnectedness through the internet, social media, and other media, mere allegations relating to quality, safety, fuel efficiency, corporate social responsibility, or other key attributes can negatively impact our reputation or market acceptance of our products or services, even where such allegations prove to be inaccurate or unfounded. Further, our ability to successfully grow through investments in the area of emerging opportunities depends on many factors, including advancements in technology, regulatory changes, and other factors that are difficult to predict, that may significantly affect the future of electrification, autonomy, and mobility.

Market shift away from sales of larger, more profitable vehicles beyond Ford’s current planning assumption, particularly in the United States. A shift in consumer preferences away from larger, more profitable vehicles at levels beyond our current planning assumption—whether because of spiking fuel prices, a decline in the construction industry, government actions or incentives, or other reasons—could result in an immediate and substantial adverse effect on our financial condition and results of operations.

Continued or increased price competition resulting from industry excess capacity, currency fluctuations, or other factors. The global automotive industry is intensely competitive, with manufacturing capacity far exceeding current demand. According to the December 2016 report issued by IHS Automotive, the global automotive industry is estimated to have had excess capacity of about 32 million units in 2016. Industry overcapacity has resulted in many manufacturers offering marketing incentives on vehicles in an attempt to maintain and grow market share; these incentives historically have included a combination of subsidized financing or leasing programs, price rebates, and other incentives. As a result, we are not necessarily able to set our prices to offset higher costs of marketing incentives, commodity or other cost increases, or the impact of adverse currency fluctuations, including pricing advantages foreign competitors may have because of their weaker home market currencies. Continuation of or increased excess capacity could have a substantial adverse effect on our financial condition and results of operations.

11

Item 1A. Risk Factors (Continued)

Fluctuations in foreign currency exchange rates, commodity prices, and interest rates. As a resource-intensive manufacturing operation, we are exposed to a variety of market and asset risks, including the effects of changes in foreign currency exchange rates, commodity prices, and interest rates. We monitor and manage these exposures as an integral part of our overall risk management program, which recognizes the unpredictability of markets and seeks to reduce potentially adverse effects on our business. Nevertheless, changes in currency exchange rates, commodity prices, and interest rates cannot always be predicted or hedged. In addition, because of intense price competition and our high level of fixed costs, we may not be able to address such changes even if foreseeable. As a result, substantial unfavorable changes in foreign currency exchange rates, commodity prices, or interest rates could have a substantial adverse effect on our financial condition and results of operations. See “Overview” to Item 7 and Item 7A for additional discussion of currency, commodity price, and interest rate risks.

Adverse effects resulting from economic, geopolitical, protectionist trade policies, or other events. With the increasing interconnectedness of global economic and financial systems, a financial crisis, natural disaster, geopolitical crisis, or other significant event in one area of the world can have an immediate and material adverse impact on markets around the world. Concerns persist regarding the overall stability of the European Union, given the diverse economic and political circumstances of individual European currency area (“euro area”) countries. These concerns have been exacerbated by Brexit, which, among other things, has resulted in a weaker sterling versus U.S. dollar and euro. We have a sterling revenue exposure and a euro cost exposure; a sustained weakening of sterling against euro may have an adverse effect on our profitability. Further, the United Kingdom may be at risk of losing access to free trade agreements for goods and services with the European Union and other countries, which may result in increased tariffs on U.K. imports and exports that could have an adverse effect on our profitability.

FCE Bank plc (“FCE”), our subsidiary, is a bank authorized by the U.K. government to carry on a range of regulated activities within the United Kingdom and through a branch network in 11 other European countries through a passporting system, which allows it to establish or provide its services in the EU27 without further authorization requirements. If passporting arrangements cease to be effective as a result of Brexit, FCE could be required to reconsider its structure or seek additional authorizations to continue to do business in the EU27, which may be time-consuming and costly.

The economic and policy uncertainty on-going in the euro area highlights potential longer-term risks regarding its sustainability. This uncertainty could cause financial and capital markets within and outside Europe to constrict, thereby negatively impacting our ability to finance our business or, if a country within the euro area were to default on its debt or withdraw from the euro currency, or-—in a more extreme circumstance—the euro currency were to be dissolved entirely, the impact on markets around the world, and on Ford’s global business, could be immediate and significant.

In addition, we have operations in various markets with volatile economic or political environments and are pursuing growth opportunities in a number of newly developed and emerging markets. These investments may expose us to heightened risks of economic, geopolitical, or other events, including governmental takeover (i.e., nationalization) of our manufacturing facilities or intellectual property, restrictive exchange or import controls, disruption of operations as a result of systemic political or economic instability, outbreak of war or expansion of hostilities, and acts of terrorism, each of which could have a substantial adverse effect on our financial condition and results of operations. Further, the U.S. government, other governments, and international organizations could impose additional sanctions that could restrict us from doing business directly or indirectly in or with certain countries or parties, which could include affiliates.

Work stoppages at Ford or supplier facilities or other limitations on production (whether as a result of labor disputes, natural or man-made disasters, tight credit markets or other financial distress, production constraints or difficulties, or other factors). A work stoppage or other limitation on production could occur at Ford or supplier facilities for any number of reasons, including as a result of disputes under existing collective bargaining agreements with labor unions or in connection with negotiation of new collective bargaining agreements, or as a result of supplier financial distress or other production constraints or difficulties, or for other reasons. A work stoppage or other limitations on production at Ford or supplier facilities for any reason (including but not limited to labor disputes, natural or man-made disasters, tight credit markets or other financial distress, or production constraints or difficulties) could have a substantial adverse effect on our financial condition and results of operations.

12

Item 1A. Risk Factors (Continued)

Single-source supply of components or materials. Many components used in our vehicles are available only from a single supplier and cannot be re-sourced quickly or inexpensively to another supplier (due to long lead times, new contractual commitments that may be required by another supplier before ramping up to provide the components or materials, etc.). In addition to the general risks described above regarding interruption of supplies, which are exacerbated in the case of single-source suppliers, the exclusive supplier of a key component potentially could exert significant bargaining power over price, quality, warranty claims, or other terms relating to a component.

Labor or other constraints on Ford’s ability to maintain competitive cost structure. Substantially all of the hourly employees in our Automotive operations in the United States and Canada are represented by unions and covered by collective bargaining agreements. These agreements provide guaranteed wage and benefit levels throughout the contract term and some degree of income security, subject to certain conditions. As a practical matter, these agreements may restrict our ability to close plants and divest businesses. A substantial number of our employees in other regions are represented by unions or government councils, and legislation or custom promoting retention of manufacturing or other employment in the state, country, or region may constrain as a practical matter our ability to sell or close manufacturing or other facilities.

Substantial pension and other postretirement liabilities impairing liquidity or financial condition. We have defined benefit retirement plans in the United States that cover many of our hourly and salaried employees. We also provide pension benefits to non-U.S. employees and retirees, primarily in Europe. In addition, we and certain of our subsidiaries sponsor plans to provide other postretirement benefits (“OPEB”) for retired employees (primarily health care and life insurance benefits). See Note 13 of the Notes to the Financial Statements for more information about these plans. These benefit plans impose significant liabilities on us and could require us to make additional cash contributions, which could impair our liquidity. If our cash flows and capital resources were insufficient to meet any pension or OPEB obligations, we could be forced to reduce or delay investments and capital expenditures, suspend dividend payments, seek additional capital, or restructure or refinance our indebtedness.

Worse-than-assumed economic and demographic experience for pension and other postretirement benefit plans (e.g., discount rates or investment returns). The measurement of our obligations, costs, and liabilities associated with benefits pursuant to our pension and other postretirement benefit plans requires that we estimate the present value of projected future payments to all participants. We use many assumptions in calculating these estimates, including assumptions related to discount rates, investment returns on designated plan assets, and demographic experience (e.g., mortality and retirement rates). We generally remeasure these estimates at each year end, and recognize any gains or losses associated with changes to our plan assets and liabilities in the year incurred. To the extent actual results are less favorable than our assumptions, we may recognize a substantial remeasurement loss in our results. For discussion of our assumptions, see “Critical Accounting Estimates” in Item 7 and Note 13 of the Notes to the Financial Statements.

Restriction on use of tax attributes from tax law “ownership change.” Section 382 of the U.S. Internal Revenue Code restricts the ability of a corporation that undergoes an ownership change to use its tax attributes, including net operating losses and tax credits (“Tax Attributes”). For these purposes, an ownership change occurs if 5 percent shareholders of an issuer’s outstanding common stock, collectively, increase their ownership percentage by more than 50 percentage points over a rolling three-year period. At December 31, 2016, we had Tax Attributes that would offset more than $15 billion of taxable income. In 2015, we renewed for an additional three-year period our tax benefit preservation plan (the “Plan”) to reduce the risk of an ownership change under Section 382. Under the Plan, shares held by any person who acquires, without the approval of our Board of Directors, beneficial ownership of 4.99% or more of our outstanding Common Stock could be subject to significant dilution. Our shareholders approved the renewal at our annual meeting in May 2016.

13

Item 1A. Risk Factors (Continued)

The discovery of defects in vehicles resulting in delays in new model launches, recall campaigns, or increased warranty costs. Government safety standards require manufacturers to remedy defects related to vehicle safety through safety recall campaigns, and a manufacturer is obligated to recall vehicles if it determines that the vehicles do not comply with a safety standard. NHTSA’s enforcement strategy has shifted to a significant increase in civil penalties levied and the use of consent orders requiring direct oversight by NHTSA of certain manufacturers’ safety processes, a trend that could continue. Should we or government safety regulators determine that a safety or other defect or a noncompliance exists with respect to certain of our vehicles prior to the start of production, the launch of such vehicle could be delayed until such defect is remedied. The costs associated with any protracted delay in new model launches necessary to remedy such defects, or the cost of recall campaigns or warranty costs to remedy such defects in vehicles that have been sold, could be substantial. Such recall and customer satisfaction actions may relate to defective components we receive from suppliers. The cost to complete a recall or customer satisfaction action could be exacerbated to the extent such action relates to a global platform. Furthermore, launch delays or recall actions could adversely affect our reputation or market acceptance of our products as discussed above under “Lower-than-anticipated market acceptance of Ford’s new or existing products or services, or failure to achieve expected growth.”

Increased safety, emissions, fuel economy, or other regulations resulting in higher costs, cash expenditures, and/or sales restrictions. The worldwide automotive industry is governed by a substantial amount of government regulation, which often differs by state, region, and country. Government regulation has arisen, and proposals for additional regulation are advanced, primarily out of concern for the environment (including concerns about the possibility of global climate change and its impact), vehicle safety, and energy independence. For example, as discussed above under “Item 1. Business - Governmental Standards,” in the United States the CAFE standards for light duty vehicles increase sharply to 51.4 mpg by the 2025 model year; EPA’s parallel CO2 emission regulations impose similar standards. California’s ZEV rules also mandate steep increases in the sale of electric vehicles and other advanced technology vehicles beginning in the 2018 model year. In addition, many governments regulate local product content and/or impose import requirements as a means of creating jobs, protecting domestic producers, and influencing the balance of payments.

In recent years, we have made significant changes to our product cycle plan to improve the overall fuel economy of vehicles we produce, thereby reducing their GHG emissions. There are limits on our ability to achieve fuel economy improvements over a given time frame, however, primarily relating to the cost and effectiveness of available technologies, consumer acceptance of new technologies and changes in vehicle mix, willingness of consumers to absorb the additional costs of new technologies, the appropriateness (or lack thereof) of certain technologies for use in particular vehicles, the widespread availability (or lack thereof) of supporting infrastructure for new technologies, and the human, engineering, and financial resources necessary to deploy new technologies across a wide range of products and powertrains in a short time. The current fuel economy, CO2, and ZEV standards will be difficult to meet if fuel prices remain relatively low and market conditions do not drive consumers to purchase electric vehicles and other highly fuel-efficient vehicles in large numbers.

The U.S. government has pursued an enforcement action against a major competitor in connection with its alleged use of “defeat devices” in hundreds of thousands of light duty diesel vehicles, collecting billions of dollars for environmental remediation projects and civil penalties. Several of the competitor’s employees have been indicted on charges of committing federal crimes. The competitor also faces various class action suits, as well as numerous claims and investigations by various U.S. states and other nations. The emergence of this issue has led to increased scrutiny of automaker emission testing by regulators around the world, which in turn has triggered investigations of other manufacturers. These events may lead to new regulations, more stringent enforcement programs, requests for field actions, and/or delays in regulatory approvals. The cost to comply with existing government regulations is substantial and additional regulations or changes in consumer preferences that affect vehicle mix could have a substantial adverse impact on our financial condition and results of operations. For more discussion of the impact of such standards on our global business, see the “Governmental Standards” discussion in “Item 1. Business” above. In addition, a number of governments, as well as non-governmental organizations, publicly assess vehicles to their own protocols. The protocols could change aggressively, and any negative perception regarding the performance of our vehicles subjected to such tests could reduce future sales.

14

Item 1A. Risk Factors (Continued)

Unusual or significant litigation, governmental investigations, or adverse publicity arising out of alleged defects in products, perceived environmental impacts, or otherwise. We spend substantial resources ensuring that we comply with governmental safety regulations, mobile and stationary source emissions regulations, and other standards. Compliance with governmental standards, however, does not necessarily prevent individual or class actions, which can entail significant cost and risk. In certain circumstances, courts may permit tort claims even where our vehicles comply with federal and/or other applicable law. Furthermore, simply responding to actual or threatened litigation or government investigations of our compliance with regulatory standards, whether related to our products or business or commercial relationships, may require significant expenditures of time and other resources. Litigation also is inherently uncertain, and we could experience significant adverse results. In addition, adverse publicity surrounding an allegation may cause significant reputational harm that could have a significant adverse effect on our sales.