PACCAR INC - Annual Report: 2019 (Form 10-K)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended December 31, 2019

or

☐ Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from ____ to ____.

Commission File Number 001-14817

PACCAR Inc

(Exact name of Registrant as specified in its charter)

|

Delaware |

91-0351110 |

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

|

777 - 106th Ave. N.E., Bellevue, WA |

98004 |

|

(Address of principal executive offices) |

(Zip Code) |

Registrant's telephone number, including area code (425) 468-7400

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class |

Trading Symbol(s) |

Name of Each Exchange on Which Registered |

|

Common Stock, $1 par value |

PCAR |

The NASDAQ Global Select Market LLC |

Securities registered pursuant to Section 12(g) of the Act: NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b‑2 of the Exchange Act.

|

Large accelerated filer |

☒ |

|

|

Accelerated filer |

☐ |

|

|

|

|

|

|

|

|

Non-accelerated filer |

☐ |

|

|

Smaller reporting company |

☐ |

|

|

|

|

|

|

|

|

|

|

|

|

Emerging growth company |

☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the voting stock held by non-affiliates of the registrant as of June 30, 2019:

Common Stock, $1 par value – $24.37 billion

The number of shares outstanding of the registrant's classes of common stock, as of January 31, 2020:

Common Stock, $1 par value – 346,353,327 shares

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the proxy statement for the annual stockholders meeting to be held on April 21, 2020 are incorporated by reference into Part III.

PACCAR Inc – FORM 10-K

INDEX

|

|

|

Page |

|

|

|

|

|

|

3 |

|

|

|

|

|

|

ITEM 1. |

3 |

|

|

ITEM 1A. |

7 |

|

|

ITEM 1B. |

9 |

|

|

ITEM 2. |

9 |

|

|

ITEM 3. |

9 |

|

|

ITEM 4. |

10 |

|

|

|

|

|

|

|

11 |

|

|

|

|

|

|

ITEM 5. |

11 |

|

|

ITEM 6. |

13 |

|

|

ITEM 7. |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

14 |

|

ITEM 7A. |

29 |

|

|

ITEM 8. |

30 |

|

|

ITEM 9. |

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE |

76 |

|

ITEM 9A. |

76 |

|

|

ITEM 9B. |

76 |

|

|

|

|

|

|

|

77 |

|

|

|

|

|

|

ITEM 10. |

77 |

|

|

ITEM 11. |

78 |

|

|

ITEM 12. |

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS |

78 |

|

ITEM 13. |

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE |

78 |

|

ITEM 14. |

79 |

|

|

|

|

|

|

|

80 |

|

|

|

|

|

|

ITEM 15. |

80 |

|

|

|

|

|

|

|

83 |

2

PART I

|

ITEM 1. |

BUSINESS. |

|

(a) |

General Development of Business |

PACCAR Inc (the Company or PACCAR), incorporated under the laws of Delaware in 1971, is the successor to Pacific Car and Foundry Company which was incorporated in Washington in 1924. The Company traces its predecessors to Seattle Car Manufacturing Company formed in 1905.

|

(b) |

Financial Information About Industry Segments and Geographic Areas |

Information about the Company’s industry segments and geographic areas in response to Items 101(b), (c)(1)(i), and (d) of Regulation S-K appears in Item 8, Note S, of this Form 10-K.

|

(c) |

Narrative Description of Business |

PACCAR is a multinational company operating in three principal industry segments:

|

|

(1) |

The Truck segment includes the design, manufacture and distribution of high-quality, light-, medium- and heavy-duty commercial trucks. Heavy-duty trucks have a gross vehicle weight (GVW) of over 33,000 lbs (Class 8) in North America and over 16 metric tonnes in Europe. Medium-duty trucks have a GVW ranging from 19,500 to 33,000 lbs (Class 6 to 7) in North America, and in Europe, light- and medium-duty trucks range between 6 and 16 metric tonnes. Trucks are configured with engine in front of cab (conventional) or cab-over-engine (COE). |

|

|

(2) |

The Parts segment includes the distribution of aftermarket parts for trucks and related commercial vehicles. |

|

|

(3) |

The Financial Services segment includes finance and leasing products and services provided to customers and dealers. PACCAR’s finance and leasing activities are principally related to PACCAR products and associated equipment. |

PACCAR’s Other business includes the manufacturing and marketing of industrial winches.

TRUCKS

PACCAR’s trucks are marketed under the Kenworth, Peterbilt and DAF nameplates. These trucks, which are built in three plants in the United States, three in Europe and one each in Australia, Brasil, Canada and Mexico, are used worldwide for over-the-road and off-highway hauling of commercial and consumer goods. The Company also manufactures engines, primarily for use in the Company’s trucks, at its facilities in Columbus, Mississippi; Eindhoven, the Netherlands; and Ponta Grossa, Brasil. PACCAR competes in the North American Class 8 market, primarily with Kenworth and Peterbilt conventional models. These trucks are assembled at facilities in Chillicothe, Ohio; Denton, Texas; Renton, Washington; Mexicali, Mexico and Ste. Therese, Canada. PACCAR also competes in the North American Class 6 to 7 markets primarily with Kenworth and Peterbilt conventional models. These trucks are assembled at facilities in Ste. Therese, Canada; Denton, Texas, and Mexicali, Mexico. PACCAR competes in the European light/medium market with DAF COE trucks assembled in the United Kingdom (U.K.) by Leyland, one of PACCAR’s wholly owned subsidiaries, and participates in the European heavy market with DAF COE trucks assembled in the Netherlands and the U.K. PACCAR competes in the Brazilian heavy truck market with DAF models assembled at Ponta Grossa in the state of Paraná, Brasil. PACCAR competes in the Australian medium and heavy truck markets with Kenworth conventional and certain DAF COE models assembled at its facility at Bayswater in the state of Victoria, Australia, and DAF COE models primarily assembled in the U.K. Commercial truck manufacturing comprises the largest segment of PACCAR’s business and accounted for 78% of total 2019 net sales and revenues.

Substantially all trucks are sold to independent dealers. The Kenworth and Peterbilt nameplates are marketed and distributed by separate divisions in the U.S. and a foreign subsidiary in Canada. The Kenworth nameplate is also marketed and distributed by foreign subsidiaries in Mexico and Australia. The DAF nameplate is marketed and distributed worldwide by a foreign subsidiary headquartered in the Netherlands and is also marketed and distributed by foreign subsidiaries in Brasil and Australia. The decision to operate as a subsidiary or as a division is incidental to PACCAR’s Truck segment operations and reflects legal, tax and regulatory requirements in the various countries where PACCAR operates.

The Truck segment utilizes centrally managed purchasing, information technology, technical research and testing, treasury and finance functions. Some manufacturing plants in North America produce trucks for more than one nameplate, while other plants produce trucks for only one nameplate, depending on various factors. Best manufacturing practices within the Company are shared on a routine basis reflecting the similarity of the business models employed by each nameplate.

3

The Company’s trucks have a reputation for high quality products, most of which are ordered by dealers according to customer specifications. Some units are ordered by dealers for stocking to meet the needs of certain customers who require immediate delivery or for customers that require chassis to be fitted with specialized bodies. For a significant portion of the Company’s truck operations, major components, such as engines, transmissions and axles, as well as a substantial percentage of other components, are purchased from component manufacturers pursuant to PACCAR and customer specifications. DAF, which is more vertically integrated, manufactures PACCAR engines and axles and a higher percentage of other components for its heavy truck models. The Company also manufactures engines at its Columbus, Mississippi facility. In 2019, the Company installed PACCAR engines in 43% of the Company’s Kenworth and Peterbilt heavy‑duty trucks in the U.S. and Canada and substantially all of the DAF heavy-duty trucks sold throughout the world. Engines not manufactured by the Company are purchased from Cummins Inc. (Cummins). The Company purchased a significant portion of its transmissions from Eaton Corporation Plc. (Eaton) and ZF Friedrichshafen AG (ZF). The Company also purchased a significant portion of North America stampings used for cabs from Magna International Inc. (Magna). The Company has long-term agreements with Cummins, Eaton, ZF and Magna to provide for continuity of supply. A loss of supply from Cummins, Eaton, ZF or Magna, and the resulting interruption in the production of trucks, would have a material effect on the Company’s results. Purchased materials and parts include raw materials, partially processed materials, such as castings, and finished components manufactured by independent suppliers. Raw materials, partially processed materials and finished components make up approximately 85% of the cost of new trucks. The value of major finished truck components manufactured by independent suppliers ranges from approximately 33% in Europe to approximately 86% in North America. In addition to materials, the Company’s cost of sales includes labor and factory overhead, vehicle delivery and warranty. Accordingly, except for certain factory overhead costs such as depreciation, property taxes and utilities, the Company’s cost of sales are highly correlated to sales.

The Company’s DAF subsidiary purchases fully assembled cabs from a competitor, Renault V.I., for its European light-duty product line pursuant to a joint product development and long-term supply contract. Sales of trucks manufactured with these cabs amounted to approximately 3% of consolidated revenues in 2019. A short-term loss of supply, and the resulting interruption in the production of these trucks, would not have a material effect on the Company’s results of operations. However, a loss of supply for an extended period of time would require the Company to either contract for an alternative source of supply or to manufacture cabs itself.

Other than these components, the Company is not limited to any single source for any significant component, although the sudden inability of a supplier to deliver components could have a temporary adverse effect on production of certain products. Manufacturing inventory levels are based upon production schedules, and orders are placed with suppliers accordingly.

Key factors affecting Truck segment earnings include the number of new trucks sold in the markets served and the margins realized on the sales. The Company’s sales of new trucks are dependent on the size of the truck markets served and the Company’s share of those markets. Truck segment sales and margins tend to be cyclical based on the level of overall economic activity, the availability of capital and the amount of freight being transported. The Company’s costs for trucks consist primarily of material costs, which are influenced by the price of commodities such as steel, copper, aluminum and petroleum. The Company utilizes long-term supply agreements to reduce the variability of the unit cost of purchased materials and finished components. The Company’s spending on research and development varies based on product development cycles and government requirements such as changes to diesel engine emissions and vehicle fuel efficiency standards in the various markets served. The Company maintains rigorous control of selling, general and administrative (SG&A) expenses and seeks to minimize such costs.

There are four principal competitors in the U.S. and Canada commercial truck market. The Company’s share of the U.S. and Canadian Class 8 market was 30.0% of retail sales in 2019, and the Company’s medium-duty market share was 16.9%. In Europe, there are six principal competitors in the commercial truck market, including parent companies to two competitors of the Company in the U.S. In 2019, DAF had a 16.2% share of the European heavy-duty market and a 9.7% share of the light/medium market. These markets are highly competitive in price, quality and service. PACCAR is not dependent on any single customer for its sales. There are no significant seasonal variations in sales.

The Peterbilt, Kenworth and DAF nameplates are recognized internationally and play an important role in the marketing of the Company’s truck products. The Company engages in a continuous program of trademark and trade name protection in all marketing areas of the world.

The Company’s truck products are subject to noise, emission and safety regulations. Competing manufacturers are subject to the same regulations. The Company believes the cost of complying with these regulations will not be detrimental to its business.

The Company had a total production backlog of $6.3 billion at the end of 2019. Within this backlog, orders scheduled for delivery within three months (90 days) are considered to be firm. The 90‑day backlog approximated $3.3 billion at December 31, 2019, $4.5 billion at December 31, 2018 and $4.0 billion at December 31, 2017. Production of the year-end 2019 backlog is expected to be substantially completed during 2020.

4

PARTS

The Parts segment includes the distribution of aftermarket parts for trucks and related commercial vehicles to over 2,200 Kenworth, Peterbilt and DAF dealers in 99 countries around the world. Aftermarket truck parts are sold and delivered to the Company’s independent dealers through the Company’s 18 strategically located parts distribution centers (PDCs) in the U.S., Canada, Europe, Australia, Mexico and Central and South America. Parts are primarily purchased from various suppliers and also manufactured by the Company. Aftermarket parts inventory levels are determined largely by anticipated customer demand and the need for timely delivery. The Parts segment accounted for 16% of total 2019 net sales and revenues.

Key factors affecting Parts segment earnings include the aftermarket parts sold in the markets served and the margins realized on the sales. Aftermarket parts sales are influenced by the total number of the Company’s trucks in service and the average age and mileage of those trucks. To reflect the benefit the Parts segment receives from costs incurred by the Truck segment, certain factory overhead, research and development, engineering and SG&A expenses are allocated from the Truck segment to the Parts segment. The Company’s cost for parts sold consists primarily of material costs, which are influenced by the price of commodities such as steel, copper, aluminum and petroleum. The Company utilizes long-term supply agreements to reduce the variability of the cost of parts sold. The Company maintains rigorous control of SG&A expenses and seeks to minimize such costs.

FINANCIAL SERVICES

PACCAR Financial Services (PFS) operates in 25 countries in North America, Europe, Australia and South America through wholly owned finance companies operating under the PACCAR Financial trade name. PFS also conducts full service leasing operations through operating divisions or wholly owned subsidiaries in North America, Germany and Australia under the PacLease trade name. Selected dealers in North America are franchised to provide full service leasing. PFS provides its franchisees with equipment financing and administrative support. PFS also operates its own full service lease outlets. PFS’s retail loan and lease customers consist of small, medium and large commercial trucking companies, independent owner/operators and other businesses and acquire their PACCAR trucks principally from independent PACCAR dealers. PFS accounted for 6% of total net sales and revenues and 57% of total assets in 2019.

PFS is primarily responsible for managing the sales of the Company’s used trucks. The Company’s Financial Services segment sells used trucks returned from matured operating leases in the ordinary course of business and trucks acquired from repossessions. PFS also obtains used trucks from the Truck segment in trades related to new truck sales and trucks returned from residual value guarantees (RVGs). Certain gains and losses from the sale of used trucks are shared with the Truck segment. The Company’s Financial Services segment records revenue on the sale of used trucks received in trade and RVG returns.

The Company’s finance receivables are classified as dealer wholesale, dealer retail and customer retail segments. The dealer wholesale segment consists of truck inventory financing to independent PACCAR dealers. The dealer retail segment consists of loans and leases to participating dealers and franchises, which use the proceeds to fund their customers’ acquisition of trucks and related equipment. The customer retail segment consists of loans and leases directly to customers for their acquisition of trucks and related equipment. Customer retail receivables are further segregated by fleet and owner/operator classes. The fleet class consists of customers operating more than five trucks. All others are considered owner/operators. Similar methods are employed to assess and monitor credit risk for each class.

Finance receivables are secured by the trucks and related equipment being financed or leased. The terms of loan and lease contracts generally range from three to five years depending on the type and use of equipment. Payment is required on dealer inventory financing when the floored truck is sold to a customer or upon maturity of the flooring loan, whichever comes first. Dealer inventory loans generally mature within one year.

The Company funds its financial services activities primarily from collections on existing finance receivables and borrowings in the capital markets. The primary sources of borrowings in the capital markets are commercial paper and medium-term notes issued in public and private offerings and, to a lesser extent, bank loans. An additional source of funds is loans from other PACCAR companies. PFS matches the maturity and interest rate characteristics of its debt with the maturity and interest rate characteristics of loans and leases.

Key factors affecting the earnings of the Financial Services segment include the volume of new loans and leases, the yield earned on the loans and leases, the costs of funding investments in loans and leases and the ability to collect the amounts owed to PFS. New loan and lease volume is dependent on the volume of new trucks sold by Kenworth, Peterbilt and DAF and the share of those truck sales that are financed by the Financial Services segment. The Company’s Financial Services market share is influenced by the extent of competition in the financing market. PFS’s primary competitors include commercial banks and independent finance and leasing companies.

5

The revenue earned on loans and leases depends on market interest and lease rates and the ability of PFS to differentiate itself from the competition by superior industry knowledge and customer service. Dealer inventory loans have variable rates with rates reset monthly based on an index pertaining to the applicable local market. Retail loan and lease contracts normally have fixed rates over the contract term. PFS obtains funds either through fixed rate borrowings or through variable rate borrowings, a portion of which have been effectively converted to fixed rate through the use of interest-rate contracts. This enables PFS to obtain a stable spread between the cost of borrowing and the yield on fixed rate contracts over the contract term. Included in Financial Services cost of revenues is depreciation on equipment on operating leases. The amount of depreciation on operating leases principally depends on the acquisition cost of leased equipment, the term of the leases, which generally ranges from three to five years, and the residual value of the leases, which generally ranges from 30% to 70%. The margin earned is the difference between the revenues on loan and lease contracts and the direct costs of operation, including interest and depreciation.

PFS incurs credit losses when customers are unable to pay the full amounts due under loan and finance lease contracts. PFS takes a conservative approach to underwriting new retail business in order to minimize credit losses.

The ability of customers to pay their obligations to PFS depends on the state of the general economy, the extent of freight demand, freight rates and the cost of fuel, among other factors. PFS limits its exposure to any one customer, with no one customer or dealer balance representing over 5% of the aggregate portfolio assets. PFS generally requires a down payment and secures its interest in the underlying truck collateral and may require other collateral or guarantees. In the event of default, PFS will repossess the truck and sell it in the open market primarily through its dealer network as well as PFS used truck centers. PFS will also seek to recover any shortfall between the amounts owed and the amounts recovered from sale of the collateral. The amount of credit losses depends on the rate of default on loans and finance leases and, in the event of repossession, the ability to recover the amount owed from sale of the collateral which is affected by used truck prices. PFS’s experience over the last fifty years financing truck sales has been that periods of economic weakness result in higher past dues and increased rates of repossession. Used truck prices also tend to fall during periods of economic weakness. As a result, credit losses tend to increase during periods of economic weakness. PFS provides an allowance for credit losses based on specifically identified customer risks and an analysis of estimated losses inherent in the portfolio, considering the amount of past due accounts, the trends of used truck prices and the economic environment in each of its markets.

Financial Services SG&A expenses consist primarily of personnel costs associated with originating and servicing the loan and lease portfolios. These costs vary somewhat depending on overall levels of business activity, but given the ongoing nature of servicing activities, tend to be relatively stable.

OTHER BUSINESSES

Other businesses include the manufacturing of industrial winches in two U.S. plants and marketing them under the Braden, Carco and Gearmatic nameplates. The markets for these products are highly competitive, and the Company competes with a number of well established firms. Sales of industrial winches were less than 1% of total net sales and revenues in 2019, 2018 and 2017.

The Braden, Carco and Gearmatic trademarks and trade names are recognized internationally and play an important role in the marketing of those products.

PATENTS

The Company owns numerous patents which relate to all product lines. Although these patents are considered important to the overall conduct of the Company’s business, no patent or group of patents is considered essential to a material part of the Company’s business.

REGULATION

As a manufacturer of highway trucks, the Company is subject to the National Traffic and Motor Vehicle Safety Act and Federal Motor Vehicle Safety Standards promulgated by the National Highway Traffic Safety Administration as well as environmental laws and regulations in the United States, and is subject to similar regulations in all countries where it has operations and where its trucks are distributed. In addition, the Company is subject to certain other licensing requirements to do business in the United States and Europe. The Company believes it is in compliance with laws and regulations applicable to safety standards, the environment and other licensing requirements in all countries where it has operations and where its trucks are distributed.

Information regarding the effects that compliance with international, federal, state and local provisions regulating the environment have on the Company’s capital and operating expenditures and the Company’s involvement in environmental cleanup activities is included in Management’s Discussion and Analysis of Financial Condition and Results of Operations and the Company’s Consolidated Financial Statements in Items 7 and 8, respectively.

6

EMPLOYEES

On December 31, 2019, the Company had approximately 27,000 employees.

OTHER DISCLOSURES

The Company’s filings on Forms 10‑K, 10‑Q and 8‑K and any amendments to those reports can be found on the Company’s website www.paccar.com free of charge as soon as practicable after the report is electronically filed with, or furnished to, the Securities and Exchange Commission (SEC). The information on the Company’s website is not incorporated by reference into this report. In addition, the Company’s reports filed with the SEC can be found at www.sec.gov.

|

ITEM 1A. |

RISK FACTORS. |

The following are significant risks which could have a material negative impact on the Company’s financial condition or results of operations.

Business and Industry Risks

Commercial Truck Market Demand is Variable. The Company’s business is highly sensitive to global and national economic conditions as well as economic conditions in the industries and markets it serves. Negative economic conditions and outlook can materially weaken demand for the Company’s equipment and services. The yearly demand for commercial vehicles may increase or decrease more than overall gross domestic product in markets the Company serves, which are principally North America and Europe. Demand for commercial vehicles may also be affected by the introduction of new vehicles and technologies by the Company or its competitors.

Competition and Prices. The Company operates in a highly competitive environment, which could adversely affect the Company’s sales and pricing. Financial results depend largely on the ability to develop, manufacture and market competitive products that profitably meet customer demand.

Production Costs and Supplier Capacity. The Company’s products are exposed to variability in material and commodity costs. Commodity or component price increases and significant shortages of component products may adversely impact the Company’s financial results or use of its production capacity. Many of the Company’s suppliers also supply automotive manufacturers, and factors that adversely affect the automotive industry can also have adverse effects on these suppliers and the Company. Supplier delivery performance can be adversely affected if increased demand for these suppliers’ products exceeds their production capacity. Unexpected events, including natural disasters, may increase the Company’s cost of doing business or disrupt the Company’s or its suppliers’ operations.

The recent outbreak of the Coronavirus “COVID-19” in China has resulted in work stoppages at certain suppliers in China that are part of the Company’s supply chain. As of February 19, 2020, the Company has not experienced shortages in supply as a result of the interruptions, but if the work stoppages were to be prolonged or expanded in scope, there could be resulting supply shortages which could impact the Company’s ability to deliver trucks and parts to customers on schedule and have an adverse effect on the Company’s revenues and profits.

Liquidity Risks, Credit Ratings and Costs of Funds. Disruptions or volatility in global financial markets could limit the Company’s sources of liquidity, or the liquidity of customers, dealers and suppliers. A lowering of the Company’s credit ratings could increase the cost of borrowing and adversely affect access to capital markets. The Company’s Financial Services segment obtains funds for its operations from commercial paper, medium-term notes and bank debt. If the markets for commercial paper, medium-term notes and bank debt do not provide the necessary liquidity in the future, the Financial Services segment may experience increased costs or may have to limit its financing of retail and wholesale assets. This could result in a reduction of the number of vehicles the Company is able to produce and sell to customers.

The Financial Services Industry is Highly Competitive. The Company’s Financial Services segment competes with banks, other commercial finance companies and financial services firms which may have lower costs of borrowing, higher leverage or market share goals that result in a willingness to offer lower interest rates, which may lead to decreased margins, lower market share or both. A decline in the Company’s truck unit sales and a decrease in truck residual values and used truck inventory values due to lower used truck pricing are also factors which may affect the Company’s Financial Services segment.

The Financial Services Segment is Subject to Credit Risk. The Financial Services segment is exposed to the risk of loss arising from the failure of a customer, dealer or counterparty to meet the terms of the loans, leases and derivative contracts with the Company.

7

Although the financial assets of the Financial Services segment are secured by underlying equipment collateral, in the event a customer cannot meet its obligations to the Company, there is a risk that the value of the underlying collateral will not be sufficient to recover the amounts owed to the Company, resulting in credit losses.

Interest-Rate Risks. The Financial Services segment is subject to interest-rate risks, because increases in interest rates can reduce demand for its products, increase borrowing costs and potentially reduce interest margins. PFS uses derivative contracts to match the interest rate characteristics of its debt to the interest rate characteristics of its finance receivables in order to mitigate the risk of changing interest rates.

Information Technology. The Company relies on information technology systems and networks to process, transmit and store electronic information, and to manage or support a variety of its business processes and activities. These computer systems and networks may be subject to disruptions during the process of upgrading or replacing software, databases or components; power outages; hardware failures; computer viruses; or outside parties attempting to disrupt the Company’s business or gain unauthorized access to the Company’s electronic data. The Company maintains and continues to invest in protections to guard against such events. Examples of these protections include conducting third-party penetration tests, implementing software detection and prevention tools, event monitoring, and disaster recoverability. Additionally the Company maintains a cybersecurity insurance policy. Despite these safeguards, there remains a risk of system disruptions, unauthorized access and data loss.

If the Company’s computer systems were to be damaged, disrupted or breached, it could impact data availability and integrity, result in a theft of the Company’s intellectual property or lead to unauthorized disclosure of confidential information of the Company’s customers, suppliers and employees. Security breaches could also result in a violation of U.S. and international privacy and other laws and subject the Company to various litigations and governmental proceedings. These events could have an adverse impact on the Company’s results of operations and financial condition, damage its reputation, disrupt operations and negatively impact competitiveness in the marketplace.

Political, Regulatory and Economic Risks

Multinational Operations. The Company’s global operations are exposed to political, economic and other risks and events beyond its control in the countries in which the Company operates. The Company may be adversely affected by political instabilities, fuel shortages or interruptions in utility or transportation systems, natural calamities, wars, terrorism and labor strikes. Changes in government monetary or fiscal policies and international trade policies may impact demand for the Company’s products, financial results and competitive position. PACCAR’s global operations are subject to extensive trade, competition and anti-corruption laws and regulations that could impose significant compliance costs.

U.K. Exit from the European Union (EU). The U.K. formally exited the EU on January 31, 2020. Under the withdrawal agreement between the U.K. and the EU, there is a transition period that will last until December 31, 2020. During the transition period, all EU rules and regulations will continue to apply to the U.K. During 2020, the U.K. and the EU intend to conclude new agreements concerning their future relationship. If no agreement is reached during the transition period, and there is no mutually agreed extension of the transition period, the standard trade protocols of the World Trade Organization (WTO) would become effective.

The Company manufactures medium- and heavy-duty DAF trucks in the U.K. which are sold primarily in the U.K. and to a lesser extent in Europe and other world markets. In 2019, approximately 10% of the Company’s worldwide truck production was manufactured in the U.K. In the event standard trade protocols of the WTO become effective, it is anticipated there would be an increase in tariffs on truck components and parts from the EU which would increase the cost of all trucks and parts in the U.K. The higher cost of trucks and parts may impact truck and parts sales and margins which could have an adverse impact on the Company’s results of operations. The Company’s results could also be impacted by the uncertainty regarding timing and terms of the final agreement, which could cause delays in capital investment decisions.

LIBOR (London Inter-Bank Offered Rate) Transition. Certain financing provided by PFS to dealers and retail customers, as well as financing extended to PFS are based on variable interest rate contracts. These contracts utilize various benchmark rates, including LIBOR, to establish applicable contract interest rates. PACCAR also utilizes hedging instruments and has line of credit arrangements which reference LIBOR (including other similar benchmark rates). In July 2017, the U.K. Financial Conduct Authority, which regulates LIBOR, announced it intends to stop compelling banks to submit rates for calculation of LIBOR after 2021. At this time it is not clear if LIBOR will continue to exist, and if not, what alternative benchmark rate will replace LIBOR. Any new benchmark rate will likely not replicate LIBOR exactly, which could impact currently active contracts which terminate after 2021.

Substantially all of the Company’s contracts which reference LIBOR, including dealer wholesale financing contracts, medium-term notes, hedging instruments and line of credit arrangements, include fall-back language that specifies the methods to establish contract interest rates in the absence of LIBOR, or provide for the use of an alternative benchmark rate should LIBOR be discontinued.

8

The Company has retail loan and lease contracts with a current balance of approximately $220 million, or less than 1.4% of PFS assets, that extend beyond 2021 and do not contain fall-back language or provide for the use of an alternative benchmark rate. The Company will seek to amend these contracts to allow for the use of an alternative benchmark rate.

Changes to benchmark rates will have an uncertain impact on finance receivables and other financial obligations, our current or future cost of funds and/or access to capital markets. The Company will attempt to minimize the impact of differences between the current and replacement benchmark rates through pricing adjustments on the financing provided by PFS, but it is not certain the Company will be able to do so. Based on the current balance of contracts referencing LIBOR (including other similar benchmark rates), it is estimated that for a 10 basis point difference between the current and replacement benchmark rates that the Company is unable to recover through pricing adjustments, income before income taxes would decrease by approximately $2 million. Accordingly, the Company does not expect the anticipated changes to the use of LIBOR as a benchmark rate will have a material impact on the results of operations.

Environmental Regulations. The Company’s operations are subject to environmental laws and regulations that impose significant compliance costs. The Company could experience higher research and development and manufacturing costs due to changes in government requirements for its products, including changes in emissions, fuel, greenhouse gas or other regulations.

Litigation, Product Liability and Regulatory. The Company’s products are subject to recall for environmental, performance and safety-related issues. Product recalls, lawsuits, regulatory actions or increases in the reserves the Company establishes for contingencies may increase the Company’s costs and lower profits. Due to the international nature of the Company’s business, some products are also subject to international trade regulations, including customs and import / export related laws and regulations, government embargoes and sanctions prohibiting sales to specific persons or countries, as well as anti-corruption laws. The Company’s reputation and its brand names are valuable assets, and claims or regulatory actions, even if unsuccessful or without merit, could adversely affect the Company’s reputation and brand images because of adverse publicity.

Currency Exchange and Translation. The Company’s consolidated financial results are reported in U.S. dollars, while significant operations are denominated in the currencies of other countries. Currency exchange rate fluctuations can affect the Company’s assets, liabilities and results of operations through both translation and transaction risk, as reported in the Company’s financial statements. The Company uses certain derivative financial instruments and localized production of its products to reduce, but not eliminate, the effects of foreign currency exchange rate fluctuations.

Accounting Estimates. In the preparation of the Company’s financial statements in accordance with U.S. generally accepted accounting principles, management uses estimates and makes judgments and assumptions that affect asset and liability values and the amounts reported as income and expense during the periods presented. Certain of these estimates, judgments and assumptions, such as residual values on operating leases, the allowance for credit losses and product warranty are particularly sensitive. If actual results are different from estimates used by management, they may have a material impact on the financial statements. For additional disclosures regarding accounting estimates, see “Critical Accounting Policies” under Item 7 of this Form 10-K.

Taxes. Changes in statutory income tax rates in the countries in which the Company operates impact the Company’s effective tax rate. Changes to other taxes or the adoption of other new tax legislation could affect the Company’s provision for income taxes and related tax assets and liabilities.

|

ITEM 1B. |

UNRESOLVED STAFF COMMENTS. |

None.

9

|

ITEM 2. |

PROPERTIES. |

The Company and its subsidiaries own and operate manufacturing plants in five U.S. states, three countries in Europe, and in Australia, Brasil, Canada and Mexico. The Company also has 18 parts distribution centers, many sales and service offices, and finance and administrative offices which are operated in owned or leased premises in these and other locations. Facilities for product testing and research and development are located in the state of Washington and the Netherlands. The Company also has an innovation center in Sunnyvale, California. The Company's corporate headquarters is located in owned premises in Bellevue, Washington. The Company considers all of the properties used by its businesses to be suitable for their intended purposes.

The Company invests in facilities, equipment and processes to provide manufacturing and warehouse capacity to meet its customers’ needs and improve operating performance.

The following summarizes the number of the Company’s manufacturing plants and parts distribution centers by geographical location within indicated industry segments:

|

|

|

U.S |

|

|

Canada |

|

|

Australia |

|

|

Mexico |

|

|

Europe |

|

|

Central and So. America |

|

||||||

|

Truck |

|

|

4 |

|

|

|

1 |

|

|

|

1 |

|

|

|

1 |

|

|

|

3 |

|

|

|

1 |

|

|

Parts |

|

|

6 |

|

|

|

2 |

|

|

|

2 |

|

|

|

1 |

|

|

|

5 |

|

|

|

2 |

|

|

Other |

|

|

2 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

ITEM 3. |

LEGAL PROCEEDINGS. |

On July 19, 2016, the European Commission (EC) concluded its investigation of all major European truck manufacturers and reached a settlement with DAF. Following the settlement, claims and lawsuits have been filed against the Company, DAF and certain DAF subsidiaries and other truck manufacturers in various European jurisdictions. These claims and lawsuits include a number of collective proceedings, including proposed class actions in the United Kingdom, alleging EC-related claims and seeking unspecified damages. Others may bring EC-related claims and lawsuits against the Company or its subsidiaries. While the Company believes it has meritorious defenses, such claims and lawsuits will likely take a significant period of time to resolve. The Company cannot reasonably estimate a range of loss, if any, that may result given the early stage of these claims and lawsuits. An adverse outcome of such proceedings could have a material impact on the Company’s results of operations.

The Company and its subsidiaries are parties to various other lawsuits incidental to the ordinary course of business. Management believes that the disposition of such lawsuits will not materially affect the Company's business or financial condition.

|

ITEM 4. |

MINE SAFETY DISCLOSURES. |

Not applicable.

10

PART II

|

ITEM 5. |

MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES. |

|

(a) |

Market Information, Holders, Dividends, Securities Authorized for Issuance Under Equity Compensation Plans and Performance Graph. |

Market Information, Holders and Dividends.

Common stock of the Company is traded on the NASDAQ Global Select Market under the symbol PCAR. The table below reflects the range of trading prices as reported by The NASDAQ Stock Market LLC and cash dividends declared. There were 1,474 record holders of the common stock at December 31, 2019.

|

|

|

2019 |

|

|

2018 |

|

||||||||||||||||||

|

|

|

DIVIDENDS |

|

|

STOCK PRICE |

|

|

DIVIDENDS |

|

|

STOCK PRICE |

|

||||||||||||

|

QUARTER |

|

DECLARED |

|

|

HIGH |

|

|

LOW |

|

|

DECLARED |

|

|

HIGH |

|

|

LOW |

|

||||||

|

First |

|

$ |

.32 |

|

|

$ |

70.35 |

|

|

$ |

55.84 |

|

|

$ |

.25 |

|

|

$ |

79.69 |

|

|

$ |

62.82 |

|

|

Second |

|

|

.32 |

|

|

|

73.00 |

|

|

|

65.78 |

|

|

|

.28 |

|

|

|

71.58 |

|

|

|

60.36 |

|

|

Third |

|

|

.32 |

|

|

|

72.86 |

|

|

|

62.13 |

|

|

|

.28 |

|

|

|

72.89 |

|

|

|

59.82 |

|

|

Fourth |

|

|

.32 |

|

|

|

83.41 |

|

|

|

65.17 |

|

|

|

.28 |

|

|

|

70.76 |

|

|

|

53.43 |

|

|

Year-End Extra |

|

|

2.30 |

|

|

|

|

|

|

|

|

|

|

|

2.00 |

|

|

|

|

|

|

|

|

|

The Company expects to continue paying regular cash dividends, although there is no assurance as to future dividends because they are dependent upon future earnings, capital requirements and financial conditions.

Securities Authorized for Issuance Under Equity Compensation Plans.

The following table provides information as of December 31, 2019 regarding compensation plans under which PACCAR equity securities are authorized for issuance.

|

|

|

Number of Securities Granted and to be Issued Related to Outstanding Options and Restricted Stock Units |

|

|

Weighted-average Exercise Price of Outstanding Options |

|

|

Securities Available for Future Grant |

|

|||

|

Stock compensation plans approved by stockholders |

|

|

4,070,289 |

|

|

$ |

60.18 |

|

|

|

12,473,227 |

|

All stock compensation plans have been approved by the stockholders.

The number of securities to be issued includes those issuable under the PACCAR Inc Long Term Incentive Plan (LTI Plan) and the Restricted Stock and Deferred Compensation Plan for Non-Employee Directors (RSDC Plan). Securities to be issued include 398,757 shares that represent deferred cash awards payable in stock.

Securities available for future grant are authorized under the following two plans: (i) 11,779,721 shares under the LTI Plan, and (ii) 693,506 shares under the RSDC Plan.

11

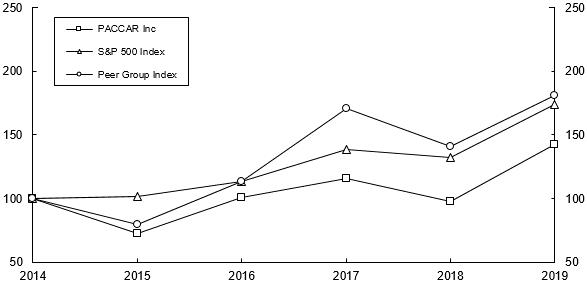

Stockholder Return Performance Graph.

The following line graph compares the yearly percentage change in the cumulative total stockholder return on the Company’s common stock, to the cumulative total return of the Standard & Poor’s Composite 500 Stock Index and the return of the industry peer groups of companies identified in the graph (the “Peer Group Index”) for the last five fiscal years ended December 31, 2019. Standard & Poor’s has calculated a return for each company in the Peer Group Index weighted according to its respective capitalization at the beginning of each period with dividends reinvested on a monthly basis. Management believes that the identified companies and methodology used in the graph for the Peer Group Index provide a better comparison than other indices available. The Peer Group Index consists of AGCO Corporation, Caterpillar Inc., Cummins Inc., Dana Incorporated, Deere & Company, Eaton Corporation, Meritor Inc., Navistar International Corporation, Oshkosh Corporation, AB Volvo and CNH Industrial N.V. The comparison assumes that $100 was invested December 31, 2014, in the Company’s common stock and in the stated indices and assumes reinvestment of dividends.

|

|

|

2014 |

|

|

2015 |

|

|

2016 |

|

|

2017 |

|

|

2018 |

|

|

2019 |

|

||||||

|

PACCAR Inc |

|

|

100 |

|

|

|

72.90 |

|

|

|

100.87 |

|

|

|

115.82 |

|

|

|

98.08 |

|

|

|

142.26 |

|

|

S&P 500 Index |

|

|

100 |

|

|

|

101.38 |

|

|

|

113.51 |

|

|

|

138.29 |

|

|

|

132.23 |

|

|

|

173.86 |

|

|

Peer Group Index |

|

|

100 |

|

|

|

79.55 |

|

|

|

113.15 |

|

|

|

170.75 |

|

|

|

141.11 |

|

|

|

181.31 |

|

|

(b) |

Use of Proceeds from Registered Securities. |

Not applicable.

|

(c) |

Purchases of Equity Securities by the Issuer and Affiliated Purchasers. |

On December 4, 2018, the Company’s Board of Directors approved the repurchase of up to $500.0 million of the Company’s outstanding common stock. As of December 31, 2019, the Company has repurchased $69.5 million of shares under this plan. There were no repurchases made during the fourth quarter of 2019.

12

|

ITEM 6. |

SELECTED FINANCIAL DATA. |

|

|

|

|

2019 |

|

|

|

2018 |

|

|

|

2017 |

|

|

|

2016 |

|

|

|

2015 |

|

|

|

|

(millions except per share data) |

|

|||||||||||||||||

|

Truck, Parts and Other Net Sales and Revenues |

|

$ |

24,119.7 |

|

|

$ |

22,138.6 |

|

|

$ |

18,187.5 |

|

|

$ |

15,846.6 |

|

|

$ |

17,942.8 |

|

|

Financial Services Revenues |

|

|

1,480.0 |

|

|

|

1,357.1 |

|

|

|

1,268.9 |

|

|

|

1,186.7 |

|

|

|

1,172.3 |

|

|

Total Revenues |

|

$ |

25,599.7 |

|

|

$ |

23,495.7 |

|

|

$ |

19,456.4 |

|

|

$ |

17,033.3 |

|

|

$ |

19,115.1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Income |

|

$ |

2,387.9 |

|

|

$ |

2,195.1 |

|

|

$ |

1,675.2 |

|

|

$ |

521.7 |

|

|

$ |

1,604.0 |

|

|

Adjusted Net Income * |

|

|

|

|

|

|

|

|

|

|

1,501.8 |

|

|

|

1,354.7 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Income Per Share: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

|

|

6.88 |

|

|

|

6.25 |

|

|

|

4.76 |

|

|

|

1.49 |

|

|

|

4.52 |

|

|

Diluted |

|

|

6.87 |

|

|

|

6.24 |

|

|

|

4.75 |

|

|

|

1.48 |

|

|

|

4.51 |

|

|

Adjusted Diluted * |

|

|

|

|

|

|

|

|

|

|

4.26 |

|

|

|

3.85 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash Dividends Declared Per Share |

|

|

3.58 |

|

|

|

3.09 |

|

|

|

2.19 |

|

|

|

1.56 |

|

|

|

2.32 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Assets: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Truck, Parts and Other |

|

|

12,289.7 |

|

|

|

11,082.8 |

|

|

|

10,237.9 |

|

|

|

8,444.1 |

|

|

|

8,855.2 |

|

|

Financial Services |

|

|

16,071.4 |

|

|

|

14,399.6 |

|

|

|

13,202.3 |

|

|

|

12,194.8 |

|

|

|

12,254.6 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Financial Services Debt |

|

|

11,222.7 |

|

|

|

9,950.5 |

|

|

|

8,879.4 |

|

|

|

8,475.2 |

|

|

|

8,591.5 |

|

|

Stockholders’ Equity |

|

|

9,706.1 |

|

|

|

8,592.9 |

|

|

|

8,050.5 |

|

|

|

6,777.6 |

|

|

|

6,940.4 |

|

|

* |

See Reconciliation of GAAP to Non-GAAP Financial Measures. |

RECONCILIATION OF GAAP TO NON-GAAP FINANCIAL MEASURES:

Item 6 of this Form 10-K includes “adjusted net income (non-GAAP)” and “adjusted net income per diluted share (non-GAAP)”, which are financial measures that are not in accordance with U.S. generally accepted accounting principles (“GAAP”), since they exclude the one-time tax benefit from the Tax Cuts and Jobs Act (“the Tax Act”) in 2017 and the non-recurring European Commission charge in 2016. These measures differ from the most directly comparable measures calculated in accordance with GAAP and may not be comparable to similarly titled non-GAAP financial measures used by other companies.

Management utilizes these non-GAAP measures to evaluate the Company’s performance and believes these measures allow investors and management to evaluate operating trends by excluding significant non-recurring items that are not representative of underlying operating trends.

Reconciliations from the most directly comparable GAAP measures of adjusted net income (non-GAAP) and adjusted net income per diluted share (non-GAAP) are as follows:

|

($ in millions, except per share amounts) |

|

|

|

|

|

|

|

|

|

Year Ended December 31, |

|

2017 |

|

|

2016 |

|

||

|

Net income |

|

$ |

1,675.2 |

|

|

$ |

521.7 |

|

|

One-time tax benefit from the Tax Act |

|

|

(173.4 |

) |

|

|

|

|

|

Non-recurring European Commission charge |

|

|

|

|

|

|

833.0 |

|

|

Adjusted net income (non-GAAP) |

|

$ |

1,501.8 |

|

|

$ |

1,354.7 |

|

|

|

|

|

|

|

|

|

||

|

Per diluted share: |

|

|

|

|

|

|

|

|

|

Net income |

|

$ |

4.75 |

|

|

$ |

1.48 |

|

|

One-time tax benefit from the Tax Act |

|

|

(.49 |

) |

|

|

|

|

|

Non-recurring European Commission charge |

|

|

|

|

|

|

2.37 |

|

|

Adjusted net income (non-GAAP) |

|

$ |

4.26 |

|

|

$ |

3.85 |

|

13

|

ITEM 7. |

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS. |

OVERVIEW:

PACCAR is a global technology company whose Truck segment includes the design and manufacture of high-quality light-, medium- and heavy-duty commercial trucks. In North America, trucks are sold under the Kenworth and Peterbilt nameplates, in Europe, under the DAF nameplate and in Australia and South America, under the Kenworth and DAF nameplates. The Parts segment includes the distribution of aftermarket parts for trucks and related commercial vehicles. The Company’s Financial Services segment derives its earnings primarily from financing or leasing PACCAR products in North America, Europe and Australia. The Company’s Other business includes the manufacturing and marketing of industrial winches.

2019 Financial Highlights

|

• |

Worldwide net sales and revenues were a record $25.60 billion in 2019 compared to $23.50 billion in 2018 due to record revenues in the Truck, Parts and Financial Services segments. |

|

• |

Truck sales were $19.99 billion in 2019 compared to $18.19 billion in 2018 primarily due to higher truck deliveries in the U.S. and Canada and Latin America. |

|

• |

Parts sales were $4.02 billion in 2019 compared to $3.84 billion in 2018 primarily due to higher demand in the U.S. and Canada. |

|

• |

Financial Services revenues were $1.48 billion in 2019 compared to $1.36 billion in 2018. The increase was primarily due to higher average earning asset balances and higher yields in North America. |

|

• |

In 2019, PACCAR earned net income for the 81st consecutive year. Net income was $2.39 billion ($6.87 per diluted share) in 2019 compared to $2.20 billion ($6.24 per diluted share) in 2018 primarily reflecting higher Truck and Parts revenues and operating results. |

|

• |

Capital investments were $743.9 million in 2019 compared to $437.1 million in 2018 reflecting continued investments in the Company’s manufacturing facilities, new product development and enhanced aftermarket support. |

|

• |

After-tax return on beginning equity (ROE) was 27.8% in 2019 compared to 27.3% in 2018. |

|

• |

Research and development (R&D) expenses were $326.6 million in 2019 compared to $306.1 million in 2018. |

PACCAR opened Global Embedded Software centers in Kirkland, Washington and Eindhoven, the Netherlands, which will accelerate embedded software development and connected vehicle solutions to benefit customers’ operating efficiency.

In January 2020, PACCAR exhibited three vehicles with autonomous and alternative powertrain technologies at the CES 2020 show in Las Vegas, Nevada: a level 4 autonomous Kenworth T680; a battery-electric Peterbilt Model 520EV; and a battery-electric Kenworth K270E. These trucks are designed for a range of customer applications, including over-the-road transportation, refuse collection and urban distribution.

Peterbilt, Kenworth and DAF are field-testing battery-electric, hydrogen fuel cell and hybrid powertrain trucks with customers in North America and Europe. These customer field tests are providing excellent feedback on future truck technologies, which will support PACCAR’s environmental and engineering leadership with the development of innovative alternative powertrain technologies.

PACCAR continues to add global distribution capacity to deliver industry-leading aftermarket parts availability to customers. PACCAR will open a new 250,000 square-foot parts distribution center in Las Vegas, Nevada and a new 160,000 square-foot parts distribution center in Ponta Grossa, Brasil in 2020 to enhance parts availability for customers.

PACCAR has been honored for the second consecutive year as a global leader in environmental practices by environmental reporting firm CDP, earning recognition on the 2019 CDP Climate Change A List. Over 8,000 companies disclosed data about their environmental impacts, risks and opportunities to CDP for independent assessment. PACCAR is one of only 35 companies in the U.S. earning a CDP score of “A” and is placed in the top 2% of reporting companies worldwide.

The PACCAR Financial Services (PFS) group of companies has operations covering four continents and 25 countries. The global breadth of PFS and its rigorous credit application process support a portfolio of loans and leases with record total assets of $16.07 billion. PFS issued $2.49 billion in medium-term notes during 2019 to support portfolio growth and repay maturing debt.

14

Truck Outlook

Heavy-duty truck industry retail sales in the U.S. and Canada in 2020 are expected to decrease to 230,000 to 260,000 units compared to 308,800 in 2019. In Europe, the 2020 truck industry registrations for over 16-tonne vehicles are expected to be 260,000 to 290,000 units compared to 320,200 in 2019. In South America, heavy-duty truck industry sales in 2020 are estimated to be 100,000 to 110,000 units compared to 105,000 units in 2019.

Parts Outlook

In 2020, PACCAR Parts sales are expected to grow 4-6% compared to 2019.

Financial Services Outlook

Based on the truck market outlook, average earning assets in 2020 are expected to remain similar to 2019 levels. Current strong levels of freight tonnage are contributing to customers’ profitability and cash flow. If current freight transportation conditions decline due to weaker economic conditions, then past due accounts, truck repossessions and credit losses would likely increase from the current low levels and new business volume would likely decline.

Capital Spending and R&D Outlook

Capital investments in 2020 are expected to be $625 to $675 million, and R&D is expected to be $310 to $340 million. The Company is investing for long-term growth in aerodynamic truck models, integrated powertrains including diesel, electric, hybrid and hydrogen fuel cell technologies, advanced driver assistance systems, digital services and next-generation manufacturing and distribution capabilities.

See the Forward-Looking Statements section of Management’s Discussion and Analysis for factors that may affect these outlooks.

15

RESULTS OF OPERATIONS:

The Company’s results of operations for the years ended December 31, 2019 and 2018 are presented below. For information on the year ended December 31, 2017, refer to Part II, Item 7 in the 2018 Annual Report on Form 10-K.

|

|

|

|

|

|

|

|

|

|

|

($ in millions, except per share amounts) |

|

|

|

|

|

|

|

|

|

Year Ended December 31, |

|

|

2019 |

|

|

|

2018 |

|

|

Net sales and revenues: |

|

|

|

|

|

|

|

|

|

Truck |

|

$ |

19,989.5 |

|

|

$ |

18,187.0 |

|

|

Parts |

|

|

4,024.9 |

|

|

|

3,838.9 |

|

|

Other |

|

|

105.3 |

|

|

|

112.7 |

|

|

Truck, Parts and Other |

|

|

24,119.7 |

|

|

|

22,138.6 |

|

|

Financial Services |

|

|

1,480.0 |

|

|

|

1,357.1 |

|

|

|

|

$ |

25,599.7 |

|

|

$ |

23,495.7 |

|

|

Income (loss) before income taxes: |

|

|

|

|

|

|

|

|

|

Truck |

|

$ |

1,904.9 |

|

|

$ |

1,672.1 |

|

|

Parts |

|

|

830.8 |

|

|

|

768.6 |

|

|

Other |

|

|

(17.7 |

) |

|

|

2.7 |

|

|

Truck, Parts and Other |

|

|

2,718.0 |

|

|

|

2,443.4 |

|

|

Financial Services |

|

|

298.9 |

|

|

|

305.9 |

|

|

Investment income |

|

|

82.3 |

|

|

|

60.9 |

|

|

Income taxes |

|

|

(711.3 |

) |

|

|

(615.1 |

) |

|

Net Income |

|

$ |

2,387.9 |

|

|

$ |

2,195.1 |

|

|

Diluted earnings per share |

|

$ |

6.87 |

|

|

$ |

6.24 |

|

|

After-tax return on revenues |

|

|

9.3 |

% |

|

|

9.3 |

% |

The following provides an analysis of the results of operations for the Company’s three reportable segments - Truck, Parts and Financial Services. Where possible, the Company has quantified the impact of factors identified in the following discussion and analysis. In cases where it is not possible to quantify the impact of factors, the Company lists them in estimated order of importance. Factors for which the Company is unable to specifically quantify the impact include market demand, fuel prices, freight tonnage and economic conditions affecting the Company’s results of operations.

2019 Compared to 2018:

Truck

The Company’s Truck segment accounted for 78% of revenues in 2019 compared to 77% in 2018.

The Company’s new truck deliveries are summarized below:

|

Year Ended December 31, |

|

|

2019 |

|

|

|

2018 |

|

|

% CHANGE |

|

|

|

U.S. and Canada |

|

|

117,200 |

|

|

|

105,300 |

|

|

|

11 |

|

|

Europe |

|

|

59,900 |

|

|

|

63,800 |

|

|

|

(6 |

) |

|

Mexico, South America, Australia and other |

|

|

21,700 |

|

|

|

20,000 |

|

|

|

9 |

|

|

Total units |

|

|

198,800 |

|

|

|

189,100 |

|

|

|

5 |

|

In 2019, industry retail sales in the heavy-duty market in the U.S. and Canada increased to 308,800 units from 284,800 units in 2018. The Company’s heavy-duty truck retail market share was 30.0% in 2019 compared to 29.4% in 2018. The medium-duty market was 108,100 units in 2019 compared to 98,100 units in 2018. The Company’s medium-duty market share was 16.9% in 2019 compared to 17.7% in 2018.

16

The over 16‑tonne truck market in Europe in 2019 increased to 320,200 units from 318,800 units in 2018, and DAF’s market share was 16.2% in 2019 compared to 16.6% in 2018. The 6 to 16‑tonne market in 2019 increased to 53,600 units from 51,900 units in 2018. DAF’s market share in the 6 to 16-tonne market in 2019 was 9.7% compared to 9.0% in 2018.

The Company’s worldwide truck net sales and revenues are summarized below:

|

($ in millions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Year Ended December 31, |

|

|

2019 |

|

|

|

2018 |

|

|

% CHANGE |

|

|

|

Truck net sales and revenues: |

|

|

|

|

|

|

|

|

|

|

|

|

|

U.S. and Canada |

|

$ |

13,106.5 |

|

|

$ |

11,357.0 |

|

|

|

15 |

|

|

Europe |

|

|

4,797.6 |

|

|

|

4,808.4 |

|

|

|

|

|

|

Mexico, South America, Australia and other |

|

|

2,085.4 |

|

|

|

2,021.6 |

|

|

|

3 |

|

|

|

|

$ |

19,989.5 |

|

|

$ |

18,187.0 |

|

|

|

10 |

|

|

Truck income before income taxes |

|

$ |

1,904.9 |

|

|

$ |

1,672.1 |

|

|

|

14 |

|

|

Pre-tax return on revenues |

|

|

9.5 |

% |

|

|

9.2 |

% |

|

|

|

|

The Company’s worldwide truck net sales and revenues increased to $19.99 billion in 2019 from $18.19 billion in 2018, primarily due to higher truck deliveries in the U.S. and Canada and Latin America, partially offset by unfavorable currency translation effects. Truck segment income before income taxes and pre-tax return on revenues increased in 2019, reflecting higher truck unit deliveries and higher gross margins.

The major factors for the Truck segment changes in net sales and revenues, cost of sales and revenues and gross margin between 2019 and 2018 are as follows:

|

|

|

NET |

|

|

COST OF |

|

|

|

|

|

||

|

|

|

SALES AND |

|

|

SALES AND |

|

|

GROSS |

|

|||

|

($ in millions) |

|

REVENUES |

|

|

REVENUES |

|

|

MARGIN |

|

|||

|

2018 |

|

$ |

18,187.0 |

|

|

$ |

16,039.5 |

|

|

$ |

2,147.5 |

|

|

Increase (decrease) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Truck sales volume |

|

|

1,613.3 |

|

|

|

1,395.8 |

|

|

|

217.5 |

|

|

Average truck sales prices |

|

|

489.8 |

|

|

|

|

|

|

|

489.8 |

|

|

Average per truck material, labor and other direct costs |

|

|

|

|

|

|

297.8 |

|

|

|

(297.8 |

) |

|

Factory overhead and other indirect costs |

|

|

|

|

|

|

65.2 |

|

|

|

(65.2 |

) |

|

Extended warranties, operating leases and other |

|

|

71.9 |

|

|

|

101.9 |

|

|

|

(30.0 |

) |

|

Currency translation |

|

|

(372.5 |

) |

|

|

(337.6 |

) |

|

|

(34.9 |

) |

|

Total increase |

|

|

1,802.5 |

|

|

|

1,523.1 |

|

|

|

279.4 |

|

|

2019 |

|

$ |

19,989.5 |

|

|

$ |

17,562.6 |

|

|

$ |

2,426.9 |

|

|

• |

Truck sales volume primarily reflects higher truck deliveries in the U.S. and Canada ($1,414.4 million sales and $1,180.0 million cost of sales). In Europe, the impact of lower truck unit deliveries was more than offset by a decrease in units accounted for as operating leases, resulting in higher sales ($236.8 million) and cost of sales ($217.9 million). |

|

• |

Average truck sales prices increased sales by $489.8 million, primarily due to higher price realization in North America. |

|

• |

Average cost per truck increased cost of sales by $297.8 million, primarily reflecting higher material and labor costs. |

|

• |

Factory overhead and other indirect costs increased $65.2 million, primarily due to higher salaries and related expenses and higher supplies and maintenance costs to support increased truck production. |

|

• |

Extended warranties, operating leases and other revenues increased by $71.9 million primarily due to a higher volume of repair and maintenance (R&M) and extended warranty contracts, as well as higher revenues from operating leases. Cost of sales and revenues increased by $101.9 million primarily due to higher impairments and losses on used trucks and higher costs of extended warranty and R&M contracts. |

|

• |

The currency translation effect on sales and cost of sales reflects a decline in the value of foreign currencies relative to the U.S. dollar, primarily the euro. |

|

• |

Truck gross margins increased to 12.1% in 2019 from 11.8% in 2018, primarily due to the factors noted above. |

17

Truck selling, general and administrative expenses (SG&A) for 2019 increased to $269.7 million from $248.3 million in 2018. The increase was primarily due to higher professional fees ($24.4 million) and higher salaries and related expenses ($6.8 million), partially offset by favorable currency translation effects ($9.7 million). As a percentage of sales, Truck SG&A decreased to 1.3% in 2019 from 1.4% in 2018 due to higher net sales.

Parts

The Company’s Parts segment accounted for 16% of revenues in 2019 and 2018.

|

($ in millions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Year Ended December 31, |

|

2019 |

|

|

2018 |

|

|

% CHANGE |

|

|||

|

Parts net sales and revenues: |

|

|

|

|

|

|

|

|

|

|

|

|

|

U.S. and Canada |

|

$ |

2,731.7 |

|

|

$ |

2,545.1 |

|

|

|

7 |

|

|

Europe |

|

|

908.5 |

|

|

|

921.4 |

|

|

|

(1 |

) |

|

Mexico, South America, Australia and other |

|

|

384.7 |

|

|

|

372.4 |

|

|

|

3 |

|

|

|

|

$ |

4,024.9 |

|

|

$ |

3,838.9 |

|

|

|

5 |

|

|

Parts income before income taxes |

|

$ |

830.8 |

|

|

$ |

768.6 |

|

|

|

8 |

|

|

Pre-tax return on revenues |

|

|

20.6 |